Maritime Security Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 28.02 Billion |

| Market Size (2031) | USD 44.29 Billion |

| Growth Rate (2026 - 2031) | 9.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maritime Security Market Analysis by Mordor Intelligence

The maritime security market size is expected to grow from USD 24.67 billion in 2025 to USD 28.02 billion in 2026 and is forecasted to reach USD 44.29 billion by 2031 at a 9.59% CAGR over 2026-2031. Demand consolidates around two related forces that shape near-term adoption patterns: regulators and insurers moving toward cyber resilience certifications for vessel and facility access, and persistent piracy in chokepoints pushing commercial operators to modernize deferred surveillance and screening stacks. The regulatory path is firming as GMDSS modernization and classification society cyber rules make always-on connectivity and equipment cyber-hardening a baseline expectation rather than a choice. Rerouting pressure from heightened conflict risk has lifted shipping activity measures and accelerated deployment of autonomous patrol assets and satellite-linked command suites in sensitive sea lanes.

Key Report Takeaways

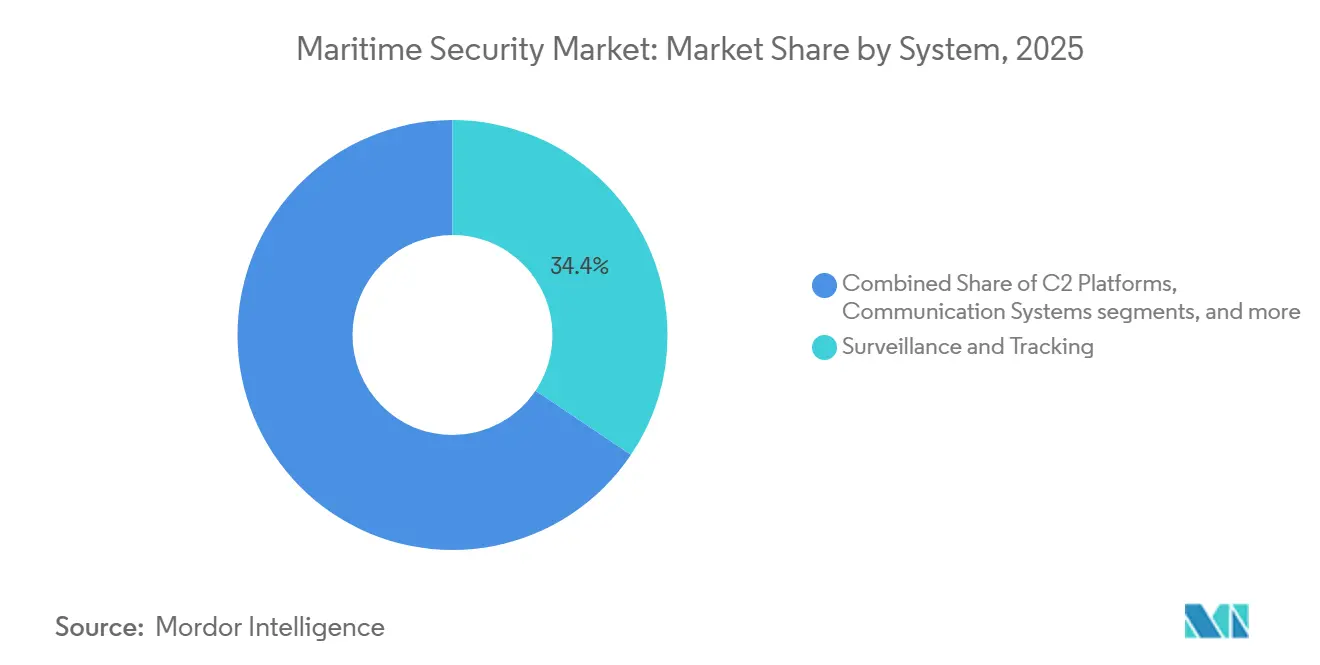

- By system, surveillance and tracking held 34.41% revenue share in 2025, while command and control (C2) systems are projected to grow at the fastest 11.28% CAGR through 2031.

- By type, port and critical infrastructure security accounted for 48.78% in 2025, while coastal and border security is forecast to expand at a 10.62% CAGR through 2031.

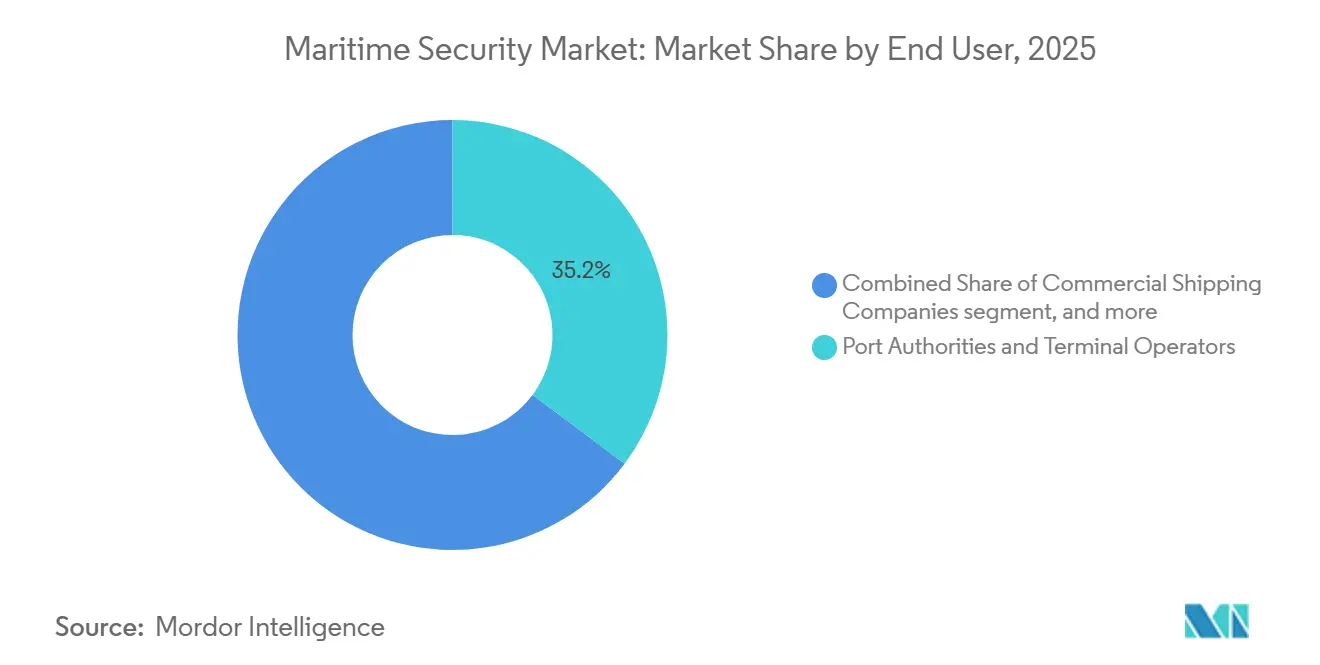

- By end user, port authorities and terminal operators led with a 35.22% share in 2025, while the naval and coast guard is expected to grow at the highest 10.21% CAGR through 2031.

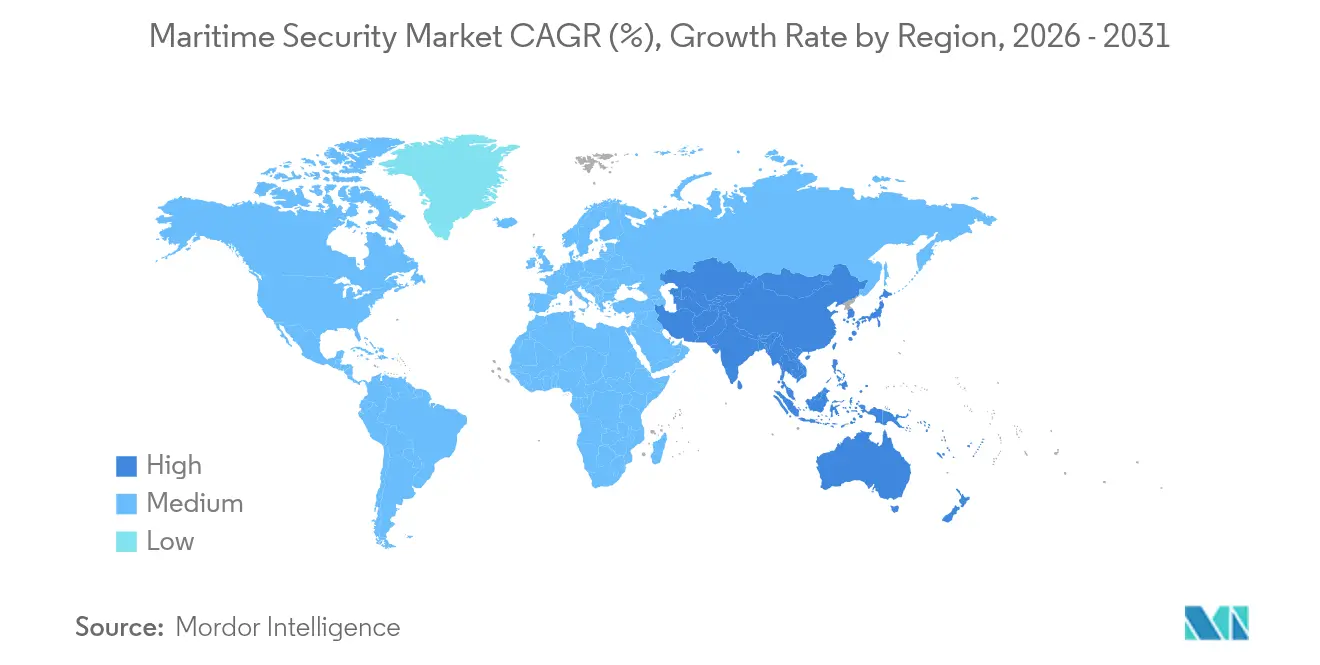

- By geography, North America held 37.41% of the maritime security market share in 2025, while the Asia-Pacific is projected to record the fastest 11.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Maritime Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising piracy and maritime threats | +2.1% | Global, concentrated in Singapore Straits, Gulf of Guinea, Indonesian archipelago | Short term (≤ 2 years) |

| Stricter international security regulations | +1.8% | Global, with accelerated adoption in US, EU, Belgium | Medium term (2-4 years) |

| Growth of global seaborne trade | +1.4% | Global, spill-over to transshipment hubs such as Singapore, Rotterdam, Dubai | Medium term (2-4 years) |

| Adoption of integrated surveillance and screening | +1.5% | Asia-Pacific core such as Singapore Tuas and Chinese Tier-1 ports, spill-over to Middle East and Africa greenfield terminals | Short term (≤ 2 years) |

| Security-linked insurance premium incentives | +0.9% | Global, early gains in London, Scandinavia, Singapore marine-insurance markets | Long term (≥ 4 years) |

| ESG-linked financing drives cyber-resilience | +0.7% | Europe, North America, select Asia-Pacific jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Piracy and Maritime Threats

The International Maritime Bureau reported 137 incidents in 2025, up from 116 in 2024, with the Singapore Straits accounting for 80 incidents, or 58% of the global total. This concentration has shifted security investments toward chokepoints, where fusing AIS, radar, and electro-optical sensors into unified dashboards enables faster interdiction and incident documentation. ReCAAP alerts reinforce the pattern across Southeast Asia and provide operational details that port authorities and ship operators translate into patrol routing and crew procedures. The Red Sea disruption across late 2023 and 2024 led to rerouting around the Cape of Good Hope. It extended voyages, tightening vessel schedules, and increasing the risk of crew fatigue on longer routes.[1]United Nations Conference on Trade and Development, “Review of Maritime Transport 2025,” UNCTAD, unctad.org The maritime security market is expected to grow as operators integrate vessel tracking, shoreside surveillance, and incident reporting to align with insurance and regulatory compliance requirements.

Stricter International Security Regulations

The US Coast Guard’s cybersecurity rule, effective July 2025, mandates incident reporting, cybersecurity training, and comprehensive governance controls, including risk assessments and independent validations, ensuring robust cybersecurity compliance across operations. The EU’s NIS2 has tightened disclosure requirements with 24-hour reporting timelines and widened the scope to cover ports and connected services within the maritime transport ecosystem. GMDSS modernization in January 2024 enhanced distress alerting and vessel-to-shore connectivity, raising baseline expectations for resilient communications in security-critical operations.

Growth of Global Seaborne Trade

Maritime trade volumes reached 12,720 million tons in 2024, posting a modest 2.2% gain. Yet, ton-miles surged 5.9%, the fastest expansion since 2011, as Red Sea attacks forced carriers to reroute via the Cape of Good Hope, adding 10-14 days to Asia-Europe voyages and extending the operational window during which vessels require persistent satellite tracking and threat monitoring. Transshipment hubs like Singapore, Rotterdam, and Dubai face concentrated security checks as rerouted flows converge at fewer chokepoints. Singapore's Tuas Mega Port employs autonomous vehicles and AI-powered surveillance to manage congestion efficiently. At the same time, DP World's Jebel Ali terminal leverages AI-driven gate controls to optimize truck processing and ensure biometric-based operator authentication.

Adoption of Integrated Surveillance and Screening

The January 2024 GMDSS modernization mandates satellite-based distress systems, establishing an installed base for broader maritime digitalization; terminals and navies now extend those satellite links to surveillance feeds, cargo tracking, and cyber-incident reporting rather than deploying parallel infrastructure. In February 2025, Singapore introduced uncrewed harbor patrol boats capable of extended missions without crew rotation, reducing operational fatigue and achieving significant cost efficiency compared to traditional manned vessels. Greenfield terminals in Asia-Pacific and the Middle East embed integrated surveillance from inception; Singapore's Tuas Mega Port and China's Ningbo-Zhoushan deploy AI-powered container inspection that cross-references manifest data with X-ray density maps in under 90 seconds, flagging anomalies for manual review.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and budget constraints | -1.2% | Global, acute in emerging-market ports with constrained capex budgets | Short term (≤ 2 years) |

| Legacy infrastructure integration complexity | -0.9% | Europe, North America, select Asia-Pacific facilities | Medium term (2-4 years) |

| Data-privacy and sovereignty concerns | -0.4% | EU and select Middle East jurisdictions | Long term (≥ 4 years) |

| Maritime-cyber talent shortage | -0.6% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Budget Constraints

Major port-security upgrades require capital that many terminal operators cannot mobilize on short timelines, slowing the rollout of screening lanes, integrated C2, and biometrics. Public budget commitments in the US, along with targeted allocations by authorities such as the Port Authority of New York and New Jersey, highlight what a fully funded cybersecurity program looks like. Still, regional and municipal ports often face multi-year prioritization cycles that delay similar initiatives. Procurement for complex inspection equipment spans long bid and commissioning cycles, leaving specifications behind as threat evolution advances if refresh planning is not embedded in yearly budgets. Insurance incentives encourage earlier adoption, but cash-strapped operators often postpone cyber-hardening until mandated by audits or obligations. Emerging financing mechanisms link cybersecurity to ESG outcomes via retrofit funds, yet their scale remains limited compared to the extensive modernization needs of legacy systems globally.

Legacy Infrastructure Integration Complexity

Brownfield integration remains difficult where port equipment control, gate management, and enterprise IT have developed separately over decades without consistent network segmentation. The lack of standardized interfaces among cranes, yard vehicles, and berth systems hinders seamless integration with real-time C2 systems, requiring the assimilation of AIS, radar, video analytics, and access-control logs into a unified operational framework. IACS cyber requirements for newbuilds raise the baseline for future compatibility, yet many terminals operate mixed fleets of equipment and software that are not straightforward to converge. Incident disclosure obligations complicate processes for operators, requiring coordinated reporting across entities and ensuring vendor compliance with controls. These measures streamline operations and enhance compliance management across terminal footprints, effectively addressing operational complexities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Surveillance Dominance Drives AI Integration

Surveillance and tracking systems accounted for 34.41% of the maritime security market size in 2025, supported by mandatory AIS carriage and the January 2024 GMDSS modernization, which improved distress alerting and reinforced the need for reliable ship-to-shore communications.[2]Source: International Maritime Organization, “Global Maritime Distress and Safety System Modernization,” International Maritime Organization, imo.org C2 systems are projected to grow at 11.28% through 2031 as the USCG cybersecurity rule requires designated cybersecurity officers on vessels and MTSA facilities, incident reporting, and formal governance, which together drive unification of radar, AIS, video, and access-control data. Screening and scanning systems are moving toward AI-enhanced detection and adaptive workflows, supported by product launches that aim to increase container throughput and improve anomaly flagging at busy terminals.

System integrators are consolidating feeds into role-based dashboards that align with incident reporting workflows under US and EU rules, thereby improving audit readiness and reducing response times. Shifts in the maritime security market drive increased C2 adoption, as operators focus on leveraging real-time intelligence for operational value rather than limiting cybersecurity to compliance obligations.

By Type: Port and Critical Infrastructure Security Leads Coastal Growth

Port and critical infrastructure security accounted for 48.78% of 2025 revenue, reflecting the concentration of inspection, access control, and video analytics at major chokepoints, supported by high-visibility program budgets that include cyber investments in large US authorities. Coastal and border systems are forecasted to grow 10.62% annually through 2031 as states harden exclusive economic zones. Systems integration across shore-based radar, satellite AIS, and electro-optical sensors enhances coverage and closure speed on alerts that require boarding or interception.

The maritime security industry is expanding the role of tele-operated and autonomous assets that can sustain patrols over long durations and feed continuous intelligence to C2 nodes. Port and infrastructure operators are aligning screening and access solutions with zero-trust practices and stricter incident reporting, which is guiding specifications toward biometric authentication, continuous anomaly detection, and integrated audit trails. Capital investments focused on environmental and cyber-resilience are driving advancements that incorporate energy efficiency with secure operational systems. These developments enhance growth opportunities in coastal and border security while sustaining the revenue potential of port and critical infrastructure security within the maritime security market.

By End User: Defense Budgets Fund Naval Modernization

Port authorities and terminal operators commanded 35.22% of 2025 revenue, driven by compliance mandates, disclosure timelines, and public funding that prioritize cybersecurity across critical nodes. Naval and Coast Guard end users are forecasted to expand at 10.21% through 2031 as governments respond to sovereignty risks and shifting shipping routes by investing in satellite-linked C2 architectures. Commercial shipping companies are primarily investing to meet cyber-insurance requirements and maintain port access. Offshore oil and gas operators are enhancing surveillance systems to strengthen maritime security measures. Cruise and ferry operators emphasize maintaining screening throughput while preserving turnaround times, supported by AI-assisted baggage and passenger screening.

Defense procurement activity underscores growth in airborne and coastal defense capabilities that integrate with naval C2. US policy timelines continue to shape incident reporting and training, which will drive consistent controls across facilities and flag-state vessels in the coming years. US policy timelines shape incident reporting and training, driving standardized controls across facilities and flag-state vessels. These developments position public-sector end users as primary drivers of spending growth in the maritime security market, while influencing commercial adoption as ports and carriers align with consistent baseline standards.

Geography Analysis

North America maintains a leading revenue position with a 37.41% share in 2025, sustained by strong public funding, rigorous compliance timelines, and active modernization programs at high-traffic hubs. Demand centers on integrated C2, cyber-hardened communications, and AI-enhanced screening that can deliver measurable risk reduction and meet audit requirements. These investments reinforce the capability baseline for critical ports and are likely to cascade into mid-tier facilities as funding and vendor capacity scale.

Asia-Pacific shows the fastest growth trajectory at 11.05% through 2031 as greenfield developments and major terminals adopt AI-based inspection systems and autonomous harbor patrols. Regional maritime services continue to modernize surveillance networks and integrate satellite AIS with coastal radar and electro-optical sensors to track risk signals and speed interdictions. These deployments are supported by active exercises and demonstrations that validate the effectiveness of autonomous and semi-autonomous systems in diverse coastal environments.

Europe is aligning with NIS2 reporting obligations, raising the operational bar for ports and associated services and compelling greater transparency and accountability across terminal operators, service providers, and logistics partners.[3]SEA News, “NIS2 Raises the Cybersecurity Bar for Maritime (Awareness Alone Won’t Cut It),” seanews.co.uk National modernization programs, coastal surveillance upgrades, and defense procurements add momentum, especially where airborne maritime patrol and coastal defense systems plug into national and regional C2 networks. These elements position Europe for steady growth as compliance timelines converge with budget cycles and project delivery capacity.

Competitive Landscape

The maritime security market is moderately fragmented, creating opportunities for both primes and specialists to compete for integrated projects and software-led contracts. Defense-aligned leaders, including Thales Group, Saab AB, BAE Systems plc, and OSI Maritime Systems Ltd., leverage established naval relationships to expand into port C2 and coastal surveillance programs. Specialists such as Smiths Detection Group Limited and Nuctech Technology Co., Ltd. run cargo-inspection portfolios with embedded service agreements and analytics updates.

Vendors are aligning their portfolios with regulatory requirements and insurance incentives that drive the adoption of integrated, auditable systems. Zero-trust principles and continuous monitoring are driving demand for access management, encrypted communications, and data integrity checks in AIS and navigation systems.

Price pressures and integration risks are driving consolidation, as buyers increasingly favor single-vendor suites over standalone tools. Consequently, the maritime security market is expected to favor companies that integrate hardware sensors, AI analytics, and compliance management solutions.

Maritime Security Industry Leaders

Thales Group

BAE Systems plc

Saab AB

Smiths Detection Group Limited (Smiths Group plc)

OSI Maritime Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Indian Coast Guard and the UAE National Guard Command signed an MoU to enhance maritime security, improve joint operational capabilities, and strengthen regional stability through strategic cooperation in safety and security measures.

- February 2024: The UK Ministry of Defense awarded Thales a contract to strengthen the country's national security. Valued at USD 2.3 billion, this 15-year agreement will enable the Thales Maritime Sensor Enhancement Team (MSET) project to introduce a new era for the Royal Navy. This project aims to optimize ship availability and resilience by harnessing advanced AI and data management tools.

Global Maritime Security Market Report Scope

Maritime security concerns the protection of vessels, ports, and other infrastructure related to the shipping business from intentional damage caused by terrorism, sabotage, or subversion.

The maritime security market is segmented by system, type, end user, and geography. By system, the market is segmented into screening and scanning, communications systems, surveillance and tracking, access control and biometrics, command and control (C2) systems, and navigation management and AIS. By type, the market is classified into port and critical infrastructure security, vessel security, and coastal and border security. By end user, the market is segmented into commercial shipping companies, port authorities and terminal operators, naval and coast guard, oil and gas offshore operators, and cruise and ferry lines. The report also covers the sizes and forecasts for the maritime security market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Screening and Scanning |

| Communication Systems |

| Surveillance and Tracking |

| Access Control and Biometrics |

| Command and Control (C2) Systems |

| Navigation Management and AIS |

| Port and Critical Infrastructure Security |

| Vessel Security |

| Coastal and Border Security |

| Commercial Shipping Companies |

| Port Authorities and Terminal Operators |

| Naval and Coast Guard |

| Oil and Gas Offshore Operators |

| Cruise and Ferry Lines |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System | Screening and Scanning | ||

| Communication Systems | |||

| Surveillance and Tracking | |||

| Access Control and Biometrics | |||

| Command and Control (C2) Systems | |||

| Navigation Management and AIS | |||

| By Type | Port and Critical Infrastructure Security | ||

| Vessel Security | |||

| Coastal and Border Security | |||

| By End User | Commercial Shipping Companies | ||

| Port Authorities and Terminal Operators | |||

| Naval and Coast Guard | |||

| Oil and Gas Offshore Operators | |||

| Cruise and Ferry Lines | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook of the Maritime Security market?

The maritime security market size was USD 24.67 billion in 2025 and is projected to reach USD 44.29 billion by 2031 at a 9.59% CAGR.

Which segments lead in revenue and growth within Maritime Security?

Surveillance and tracking led with 34.41% revenue share in 2025, while Command and Control (C2) platforms are set to grow at 11.28% through 2031.

Which end user and region are most influential for near-term demand?

Port authorities and terminal operators held 35.22% in 2025, and North America led with 37.41% share, while Asia-Pacific is the fastest growing at 11.05% through 2031.

What regulations are shaping procurement in Maritime Security in 2026?

The USCG cybersecurity rule is phasing in reporting, training, and governance by July 2027, NIS2 enforces 24-hour incident disclosure, and IACS UR E26/E27 are mandatory for newbuilds.

How are insurers influencing cybersecurity adoption at sea and ashore?

Insurers are connecting coverage terms to cyber maturity, and classification frameworks such as Lloyd’s Register’s cyber resilience programs are guiding upgrades and audits.

Which technologies are priorities for operators upgrading security programs?

Integrated C2, AI-enhanced screening, encrypted communications aligned with IACS requirements, and autonomous patrol assets are priority investments across ports and fleets.

Page last updated on: