Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.87 Billion |

| Market Size (2031) | USD 18.09 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

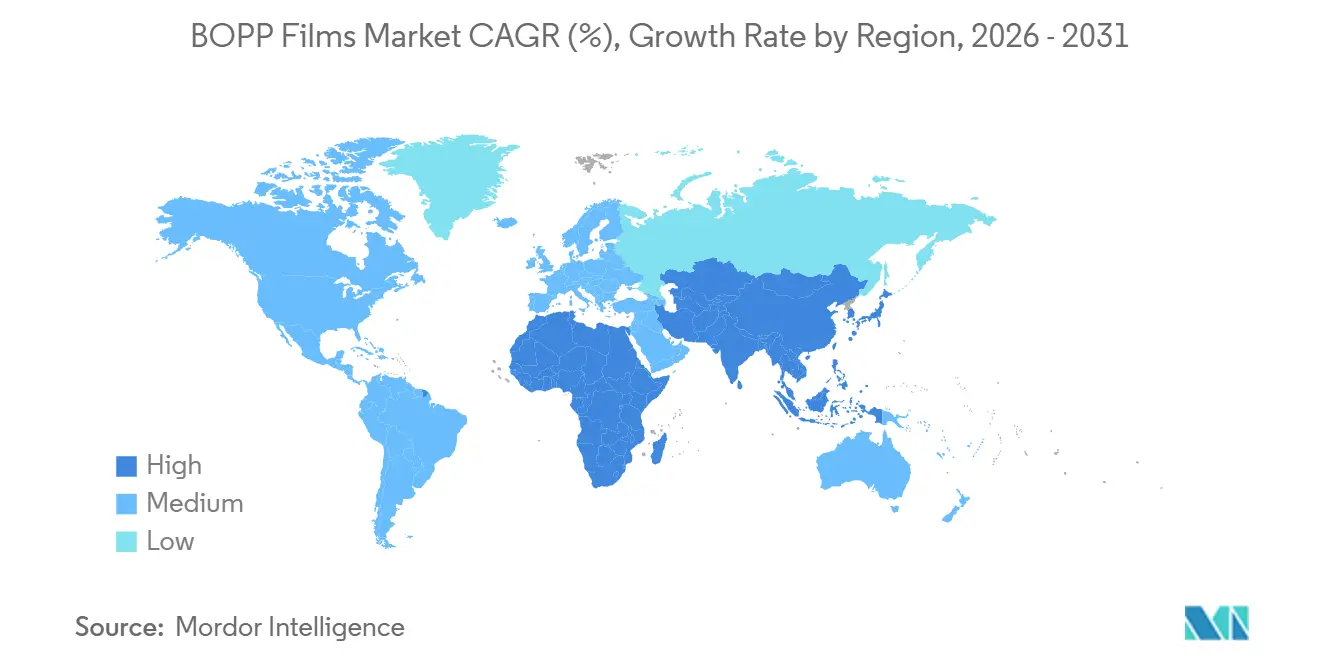

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

BOPP Films Market Analysis by Mordor Intelligence

The BOPP Films Market size is expected to increase from USD 14.25 billion in 2025 to USD 14.87 billion in 2026 and reach USD 18.09 billion by 2031, growing at a CAGR of 4.01% over 2026-2031. Continued migration from polyvinyl chloride wraps to mono-material polypropylene formats, stricter recyclability mandates across the European Union, and multi-year supply agreements with e-commerce logistics operators collectively underpin steady demand momentum. Brand owners prioritize heat-sealable, curbside-recyclable mailer films that meet both cost and carbon-footprint targets, while integrated polyolefin producers leverage captive propylene streams to cushion feedstock volatility. Metallized grades gain traction in high-barrier snack, pharmaceutical, and premium coffee pouches, and ultra-thin gauges below 15 micrometers satisfy corporate lightweighting goals without compromising tensile strength. Even so, legacy overcapacity in China keeps spot prices 12-18% below Western benchmarks, tempering near-term margin expansion for non-integrated converters.

Key Report Takeaways

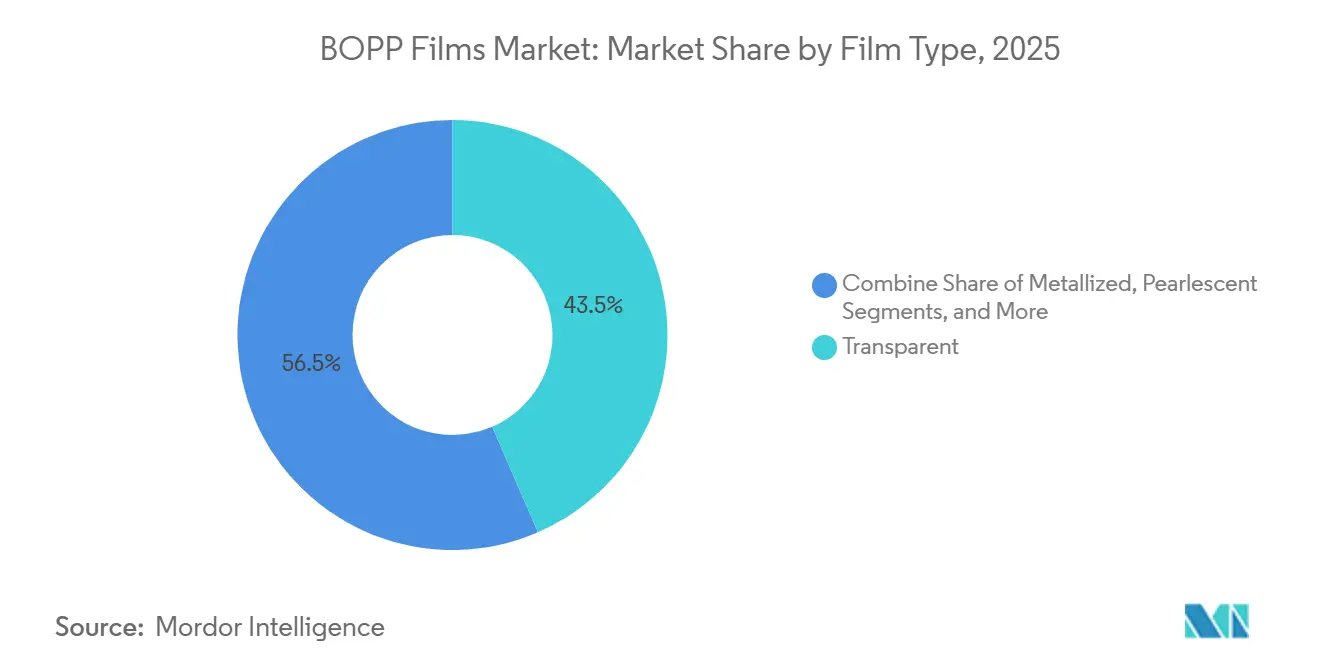

- By film type, transparent grades led with 43.50% revenue share in 2025, while metallized grades are forecast to expand at 7.90% CAGR through 2031.

- By thickness, 15-30 micrometer films held 51.03% of BOPP films market share in 2025, and sub-15 micrometer grades are projected to post an 8.40% CAGR over 2026-2031.

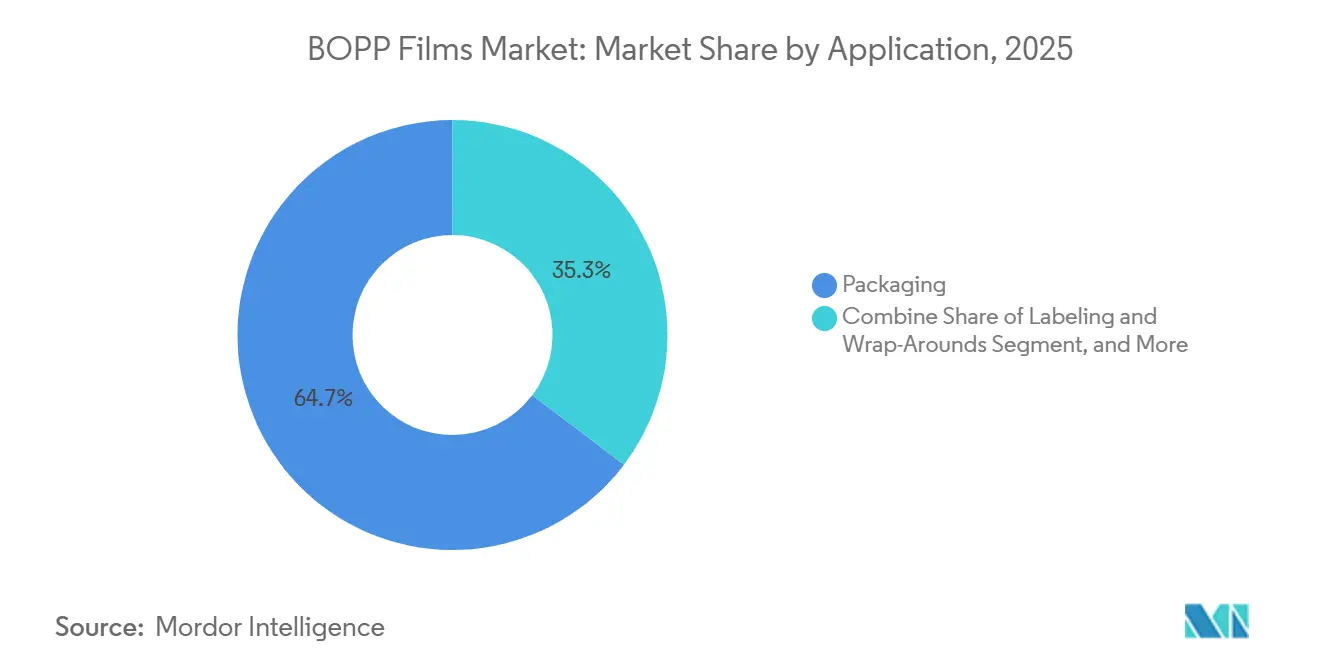

- By application, packaging accounted for 64.70% of the BOPP films market size in 2025, whereas e-commerce mailers are poised to grow at 9.60% CAGR to 2031.

- By end-user vertical, food captured 58.34% revenue in 2025, and pharmaceutical and medical packaging is expected to advance at 7.20% CAGR through 2031.

- By geography, Asia-Pacific represented 59.40% of global volume in 2025, while Africa is projected to register a 7.50% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global BOPP Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for High-Clarity Snack Packaging in Developing Economies | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Brand-Owner Switch from PVC Wrap to BOPP for Sustainability Goals | +0.9% | Global, early adoption in Europe and North America | Short term (≤ 2 years) |

| E-Commerce Boom Driving Heat-Sealable Mailer Films | +1.5% | Global, led by North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Rapid Capacity Additions by Integrated Polyolefin Producers | +0.8% | Asia-Pacific and Middle East | Medium term (2-4 years) |

| Commercialization of Recycle-Ready Mono-Material Laminates | +0.7% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| AI-Enabled Process Control Lowering Scrap Rates and Energy Use | +0.5% | Global, early implementations in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for High-Clarity Snack Packaging in Developing Economies

Rising disposable incomes across Southeast Asia, India, and Sub-Saharan Africa are shifting consumption from bulk staples toward branded single-serve snacks that require transparent films with gloss above 85% and haze below 3% to display product freshness at retail. Transparent BOPP grades provide better optical clarity than cast polypropylene or low-density polyethylene, enabling converters to drop secondary cartons and trim package mass by up to 30%. Cosmo First commissioned an 81,200-metric-tonne line in June 2025 to serve Indian confectionery and namkeen brands seeking moisture-vapor transmission rates below 5 g/m²/day[1]Cosmo First, “Investor Presentation June 2025,” cosmofilms.com. African converters now replace imported polyethylene wraps with locally extruded BOPP, capturing foreign-exchange savings and meeting emerging extended-producer-responsibility rules in Nigeria, South Africa, and Kenya. Anti-dumping duties imposed on Chinese exports accelerate this regional diversification and open space for tolling partnerships with global resin suppliers.

Brand-Owner Switch from PVC Wrap to BOPP for Sustainability Goals

Retailers and consumer-goods companies commit to phasing out chlorinated plastics because hydrochloric acid forms during incineration and PVC complicates mechanical recycling. The European Union’s Packaging and Packaging Waste Regulation sets recyclability and recycled-content thresholds that PVC cannot meet, prompting supermarket chains to demand PVC-free private-label packaging by 2027. BOPP aligns with polypropylene recycling streams that already capture roughly one-fifth of post-consumer plastic waste in Europe. Innovia Films and Taghleef Industries commercialized mono-material BOPP laminates in 2024 that integrate sealant, barrier, and print surfaces in one polymer family and remove polyethylene terephthalate or aluminum foil layers. Early adopters absorbed a 15-25% cost premium, yet this differential narrows as extrusion tooling is amortized and resin suppliers incentivize volume uptake.

E-Commerce Boom Driving Heat-Sealable Mailer Films

Flexible packaging now constitutes more than 40% of direct-to-consumer parcel volumes as online retailers replace corrugated boxes with lightweight BOPP pouches to avoid dimensional-weight surcharges. A 60 micrometer mailer weighs 85% less than a comparable cardboard box, delivers tamper evidence, and maintains seal integrity between −20 °C and 50 °C. Amazon, Zalando, and Flipkart standardize on BOPP mailers, propelling a 9.60% CAGR through 2031. Converters install inline digital print and laser-perforation units to embed QR codes and easy-open features that reduce return rates. UFlex brought a dedicated mailer-film line online in Egypt in late 2025, leveraging Euro-Mediterranean duty-free access and positioning near European logistics hubs.

Rapid Capacity Additions by Integrated Polyolefin Producers

Petrochemical majors co-locate BOPP lines beside propylene crackers, locking in resin cost at transfer prices 8-12% below merchant levels and capturing full-value-chain margin. SABIC, Reliance Industries, and China National Petroleum Corporation exploit this model, shielding film businesses from propylene volatility that ranged from USD 905 per t in Saudi Arabia to USD 1,371 per t in the United States during early 2025. Taghleef Industries expanded its Al Ghail site with a 60,000-t line in 2024, while Jindal Poly Films invested INR 700 crore (USD 84 million) in 2025 to add multi-polymer capacity adjacent to a 200,000-t polypropylene plant sourcing propylene through pipeline linkage to Reliance’s Jamnagar refinery. Brownfield integration trims capital intensity by up to 30% compared with standalone projects and cuts commissioning time to 12-18 months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Polypropylene Resin Prices | -1.1% | Global, acute impact in import-dependent regions | Short term (≤ 2 years) |

| Under-Utilized Legacy Lines in China Depressing Global Margins | -0.8% | Originating in China, spill-over to export markets | Medium term (2-4 years) |

| Competition from Bio-Based Barrier Films in Premium Niches | -0.4% | North America and Europe, limited Asia-Pacific | Long term (≥ 4 years) |

| Rising Carbon-Border Tariffs on Conventional Plastics | -0.6% | Europe and emerging carbon-pricing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polypropylene Resin Prices

Polypropylene accounts for roughly two-thirds of BOPP cash-costs, so film margins swing sharply when crude prices spike or when propylene crackers go offline for unplanned maintenance. Spot resin touched USD 1,371 per t in the United States and USD 1,010 per t in Southeast Asia in early 2025, forcing converters on annual fixed-price contracts to absorb losses or renegotiate under hardship clauses[2]ICIS, “Polypropylene Pricing Report May 2025,” icis.com. Futures hedging instruments remain illiquid outside North America and Europe, and basis risk between crude and propylene undermines perfect cost coverage. Integrated producers withstand the turbulence, whereas stand-alone converters face precarious cash flows and delayed capital upgrades that could otherwise improve productivity.

Under-Utilized Legacy Lines in China Depressing Global Margins

Chinese capacity grew faster than domestic demand in the early 2020s, leaving many lines running at 65-70% utilization versus the 85% threshold needed for healthy returns. Surplus film is exported at discounts of 12-18% below Western benchmarks, dragging global spot prices lower. European producers have petitioned for anti-dumping duties, yet enforcement gaps and rules-of-origin workarounds blunt the remedy. Until plant closures or consolidation removes redundant tonnage, global pricing discipline will stay weak and return-on-invested capital will lag the 12-15% hurdle rate that justifies new capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Metallized Grades Gain Share in Barrier Applications

Transparent films dominated the BOPP films market in 2025 with 43.50% value, reflecting their role in snack wrappers, adhesive-tape backings, and floral sleeves. Metallized films, however, are tracking a 7.90% CAGR through 2031 as pharmaceutical blister lidding and premium snack sachets demand oxygen transmission rates below 5 cc/m²/day. Metallization thickness of 30-50 nm lowers material cost by up to 30% compared with aluminum-foil laminates while keeping packages in polypropylene recycling streams. Opaque and pearlescent variants fill label and gifting niches where opacity, surface gloss, or visual effects command premiums of 40-60% over commodity transparent grades.

Growth in metallized BOPP supports the broader pivot toward mono-material packaging that satisfies European recyclability criteria without sacrificing barrier performance. Drug makers embrace the shift because the film complies with USP <661.1> extractables limits and European Medicines Agency moisture targets. Suppliers respond with capacity investments: SRF Limited disclosed a 15,000-t expansion at Indore in early 2025 aimed at export markets that pay 30-40% margins above food-wrap applications. Combined, these moves ensure metallized output keeps pace with rising demand for barrier packages in snacks, coffee, and over-the-counter medicines.

By Thickness: Ultra-Thin Films Capture Lightweighting Demand

The 15-30 micrometer range represented 51.03% of BOPP films market volume in 2025, balancing mechanical strength and cost efficiency for general-purpose packaging. Yet sub-15 micrometer films are projected to log an 8.40% CAGR to 2031, mirroring brand owner commitments to curb virgin plastic per package by one-fifth. Achieving gauges below 15 micrometers requires precise biaxial orientation ratios and advanced line controls that hold gauge variation within ±0.3 micrometers across webs up to 10 m wide. Simultaneous-stretch technology, licensed by Brückner Maschinenbau, underpins recent installations at Jindal Poly Films and Cosmo Films.

Demand for 30-45 micrometer films persists in pressure-sensitive tape backings and capacitor dielectrics that value stiffness and dimensional stability. Above 45 micrometers, BOPP serves synthetic-paper and harsh-environment labels, although this niche grows only 3-4% annually. Regulatory frameworks focus mainly on recyclability rather than gauge, yet any European directive imposing minimum film thickness would temper the lightweighting trajectory and spur a shift toward functional barrier coatings at higher gauges.

By Application: E-Commerce Mailers Outpace Traditional Packaging

Packaging activities accounted for 64.70% of the BOPP films market in 2025, spanning food wrappers, tobacco overwraps, and tape substrates. Inside that umbrella, e-commerce mailers stand out with a 9.60% CAGR, driven by parcel shippers looking to trim dimensional-weight charges and achieve curbside recyclability. A 60 micrometer BOPP mailer weighs roughly 8 g and can cut freight cost by USD 0.15 per parcel on transcontinental routes. Converters invest in inline customization, laser scoring, and antimicrobial coatings to differentiate mailers in an increasingly crowded fulfillment environment.

Labeling and wrap-around sleeves, pressure-sensitive tapes, and laminating substrates hold 20-25% share and grow 3-5% per year. Pressure-sensitive applications leverage BOPP’s high modulus to deliver equivalent holding force with 30% less material than polyethylene terephthalate. Laminating demand faces headwinds as brand owners seek mono-material formats, although stand-up pouches for pet food and coffee retain multi-layer constructions where ultra-low oxygen-transmission rates remain critical. European recycling rules allow exemptions for high-barrier multilayers until substitutes achieve parity in shelf-life performance, preserving an outlet for BOPP-polyethylene laminates.

By End-User Vertical: Pharmaceutical Compliance Drives Premium Demand

Food applications consumed 58.34% of BOPP tonnage in 2025 and mirror broader packaged-food trends, rising 3-4% annually as urbanization lifts demand for branded ready-to-eat snacks. Beverage shrink-labels and multipack wraps expand at similar rates but face substitution pressure from reusable glass and aluminum cans in deposit-return jurisdictions. Pharmaceutical and medical packaging, however, advances at 7.20% CAGR through 2031, propelled by tightened extractables thresholds under USP 661.2 and ICH Q3E. Polypropylene’s lower migration profile versus polyethylene terephthalate positions BOPP as the preferred blister-lidding and unit-dose substrate for moisture-sensitive active ingredients.

Personal care and cosmetics rise 5-6% annually as single-use sachets and wet-wipe packs gain favor among hygiene-conscious consumers. Industrial uses such as capacitor film and release liners grow modestly at 2-3% because competing materials better tolerate elevated temperatures or aggressive chemistries. Across segments, certification against FDA 21 CFR 175.105 for food contact and internal pharmaceutical quality systems adds compliance costs that small converters struggle to absorb, reinforcing the pricing power of incumbents that have accredited test laboratories and robust documentation.

Geography Analysis

Asia-Pacific accounted for 59.40% of global volume in 2025, anchored by China’s output above 3 million t and India’s expanding converter base. Despite excess capacity, regional demand remains resilient, supported by snack-food growth, e-commerce packaging, and regulatory pushes for mono-material recyclability. Integrated complexes in China, India, and the Middle East supply resin at transfer discounts that ensure the BOPP films market in the region remains cost-competitive, while export of surplus tonnage tempers global price escalation.

Africa is the fastest-growing region at 7.50% CAGR to 2031 as food and beverage distributors migrate from rigid containers to flexible pouches that exploit BOPP’s moisture barrier and printability advantages. Nigeria, South Africa, and Egypt spearhead investment, with UFlex commissioning a new Egyptian line in late 2025 that positions the country as a regional export hub. Localized production insulates brand owners from currency swings and import tariffs, while emerging extended-producer-responsibility frameworks encourage converters to adopt mono-material polypropylene solutions.

North America and Europe advance at a steady 2-3% CAGR, reflecting mature consumption patterns in packaged food but buoyed by premium demand in pharmaceutical and e-commerce applications. The Carbon Border Adjustment Mechanism slated for full implementation in 2026 embeds a carbon cost into every imported tonne of polypropylene, nudging European buyers toward regionally produced or certified low-carbon films. South America grows at 3-4%, constrained by macroeconomic volatility in Brazil and Argentina that raises financing costs for capital-intensive extrusion lines.

Competitive Landscape

The BOPP films market exhibits moderate concentration. The ten largest players control roughly 60-70% of global capacity, yet price competition remains intense because Chinese exporters offload surplus film at discounts that erode Western margins. Integrated petrochemical firms such as Reliance Industries and SABIC leverage captive propylene supply, buffering them against resin volatility and enabling aggressive contract pricing that smaller converters struggle to match. Independents including Cosmo Films, Treofan Group, and Vacmet India defend profitability by focusing on specialty metallized, cavitated, and ultra-thin grades that fetch 30-40% premiums over commodity transparent stock.

Recycle-ready mono-material laminates are the current battleground. Jindal Films, Borealis, and Coveris scale production of all-polypropylene structures that meet Association of Plastic Recyclers guidelines while delivering oxygen-transmission rates below 10 cc/m²/day. Early adopters secure extended-producer-responsibility fee discounts in Germany, France, and the Netherlands, offsetting the 10-15% cost premium versus legacy multilayers. Equipment suppliers Brückner Maschinenbau and DMT embed AI-driven process controls into new lines, cutting scrap below 1.5% and energy use by 8-12%[3]Plastics Technology, “BOPP Film Technology Trends,” ptonline.com. Converters lacking capital for retrofits face widening cost gaps and increased consolidation pressure.

Barriers to entry include compliance with USP <661> and FDA food-contact standards, access to high-clarity resins, and investment in in-house metallizing or plasma-coating systems. Patent filings concentrate on barrier coatings that match metallized film performance while retaining transparency, with Innovia Films and Taghleef Industries disclosing plasma-enhanced chemical vapor deposition techniques in 2025. Emergent bio-based film challengers such as Fraunhofer’s Plactid target premium organic-snack and specialty-coffee niches, yet overall share remains below 2% and does not materially threaten polypropylene incumbency within the forecast window.

BOPP Films Industry Leaders

Taghleef Industries LLC

SRF Limited

Toray Industries Inc.

Oben Holding Group

Uflex Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cosmo First commissioned an INR 400 crore BOPP line (81,200 tpa) using latest-generation stretching technology, lifting its total BOPP capacity by roughly 40% to 277,000 tpa.

- April 2025: South Mill Champs and Sprouts Farmers Market introduced bamboo tills flow-wrapped with perforated BOPP film for fresh mushrooms, improving shelf life while supporting recyclable, fiber-based packaging goals.

- February 2025: Oben Holding Group ordered a Brückner 10.4 m BOPP film line for a new Monterrey, Mexico plant, a project that will add 60,000 tpa of capacity once start-up is completed in 2026.

- May 2024: Plastchim-T acquired Manucor, boosting combined BOPP capacity to 200,000 tpa

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the BOPP films market as the value generated from biaxially oriented polypropylene films that are stretched in both machine and transverse directions and then sold for packaging, labeling, lamination, tapes, and similar converted products. These films are valued at transactional prices that reflect normal trade terms across all end-user verticals and regions covered in the report.

Scope Exclusions: Cast polypropylene, blown PP sheet, post-consumer re-granulate, and dielectric capacitor films are excluded.

Segmentation Overview

- By Film Type

- Transparent

- Metallized

- Opaque / White

- Pearlescent

- Other Film Type

- By Thickness

- Less than 15 μm

- 15 - 30 μm

- 30 - 45 μm

- More than 45μm

- By Application

- Packaging

- Labeling and Wrap-Arounds

- Laminating

- Pressure-Sensitive Tapes

- Other Application

- By End-User Vertical

- Food

- Beverage

- Pharmaceutical and Medical

- Personal Care and Cosmetics

- Industrial

- Other End-User Vertical

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed converters, resin suppliers, and procurement leads in Asia-Pacific, North America, and Europe, using structured questionnaires to validate gauge-wise yield losses, realistic price spreads, and emerging recyclable mono-material specifications. Follow-up calls with packaging engineers and brand owners confirmed adoption rates and provided early signals that could not be found in public data.

Desk Research

We began with trusted public datasets such as UN Comtrade shipment codes for polypropylene film, FAO food output indices that flag packaging demand shifts, and Eurostat plastics converters' production data. Trade association portals, including the Flexible Packaging Association and PlasticsEurope, provided capacity additions and resin balance sheets, while patent analytics from Questel helped us track novel high-barrier BOPP formulations. Company 10-K filings, investor decks, and press releases filled gaps on plant start-ups and average selling prices. D&B Hoovers and Dow Jones Factiva rounded out supplier revenues and mergers. This list is illustrative; many additional open sources were tapped for cross-checks and context.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of apparent consumption. Global polypropylene resin output is aligned with orientation line utilization, and then net exports are adjusted to derive film availability. Supplier roll-ups of five representative producers plus channel checks on converter sales give a bottom-up reasonableness test, which is used to tune regional leakages. Key variables include resin price curves, average film gauge mix, packaged snack volumes, e-commerce parcel counts, and label-stock penetration in beverages; each drives either value or volume in the equation. Our team applies multivariate regression blended with ARIMA to project demand, and expert feedback shapes scenario weights when regulatory bans on PVC or single-use plastics accelerate substitution.

Data Validation & Update Cycle

Outputs are passed through variance thresholds against historical trade, corporate guidance, and macroeconomic baselines. Any anomaly triggers analyst rework before senior review. Models refresh annually, and material events such as large capacity debottlenecks prompt interim updates so clients always receive the latest view.

Why Mordor's BOPP Films Baseline Deserves Your Trust

Published estimates often diverge because firms pick wider plastic scopes, convert resin weight directly to film value, or freeze currency at outdated rates.

Key gap drivers include inclusion of cast and capacitor films, omission of converter yield losses, and reliance on desk research without field validation, which can inflate current-year numbers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.22 B (2025) | Mordor Intelligence | - |

| USD 26.07 B (2025) | Global Consultancy A | Counts cast PP and dielectric film; limited primary checks |

| USD 31.40 B (2025) | Industry Association B | Uses resin shipment value; constant 2020 exchange rates |

These comparisons show that Mordor's disciplined scope choices, dual-path validation, and live refresh cycle deliver a balanced, transparent baseline that decision-makers can confidently rely on.

Key Questions Answered in the Report

How large is the BOPP films market in 2026?

The BOPP films market size reached USD 14.87 billion in 2026 and is projected to climb to USD 18.09 billion by 2031.

Which region leads global demand?

Asia-Pacific holds nearly 60% of global volume, driven by China’s large production base and India’s rapid capacity additions.

What is driving rapid growth in e-commerce mailer films?

Online retailers prefer lightweight, heat-sealable BOPP pouches that cut dimensional-weight charges and meet curbside recyclability mandates, supporting a 9.60% CAGR through 2031.

Why are metallized BOPP films gaining share?

Metallized grades deliver oxygen barrier performance under 5 cc/m²/day without leaving polyolefin recycling streams, making them attractive for premium snacks and pharmaceuticals.

Page last updated on: