Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.82 Billion |

| Market Size (2026) | USD 3.99 Billion |

| Market Size (2031) | USD 4.95 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Carbon Black Market Analysis by Mordor Intelligence

The North America Carbon Black Market size is projected to expand from USD 3.82 billion in 2025 and USD 3.99 billion in 2026 to USD 4.95 billion by 2031, registering a CAGR of 4.42% between 2026 to 2031. This steady climb reflects a balanced mix of supportive forces—rising electric-vehicle (EV) production, growth in high-surface-area furnace blacks, and corporate sustainability mandates favoring recovered carbon black—and counterweights such as feedstock volatility linked to Gulf Coast refinery cycles and silica–silane substitution in passenger tire treads. Furnace black continues to dominate value creation because it satisfies the reinforcement, conductivity, and tinting needs of multiple downstream sectors. Specialty grades capture incremental value as electronics, battery systems, and near-infrared-sortable packaging demand tighter particle-size control and very low polycyclic-aromatic-hydrocarbon content. Competitive dynamics remain intense: incumbents are racing to install emission-control projects while early movers in methane-pyrolysis and tire-pyrolysis technologies pitch fossil-free or circular supply options that hedge against decant-oil price spikes. On the customer side, tire makers are committing to higher recovered-content levels, plastics processors are pivoting to NIR-detectable masterbatch systems, and battery-component suppliers are locking in conductive blacks to meet surging cell output.

Key Report Takeaways

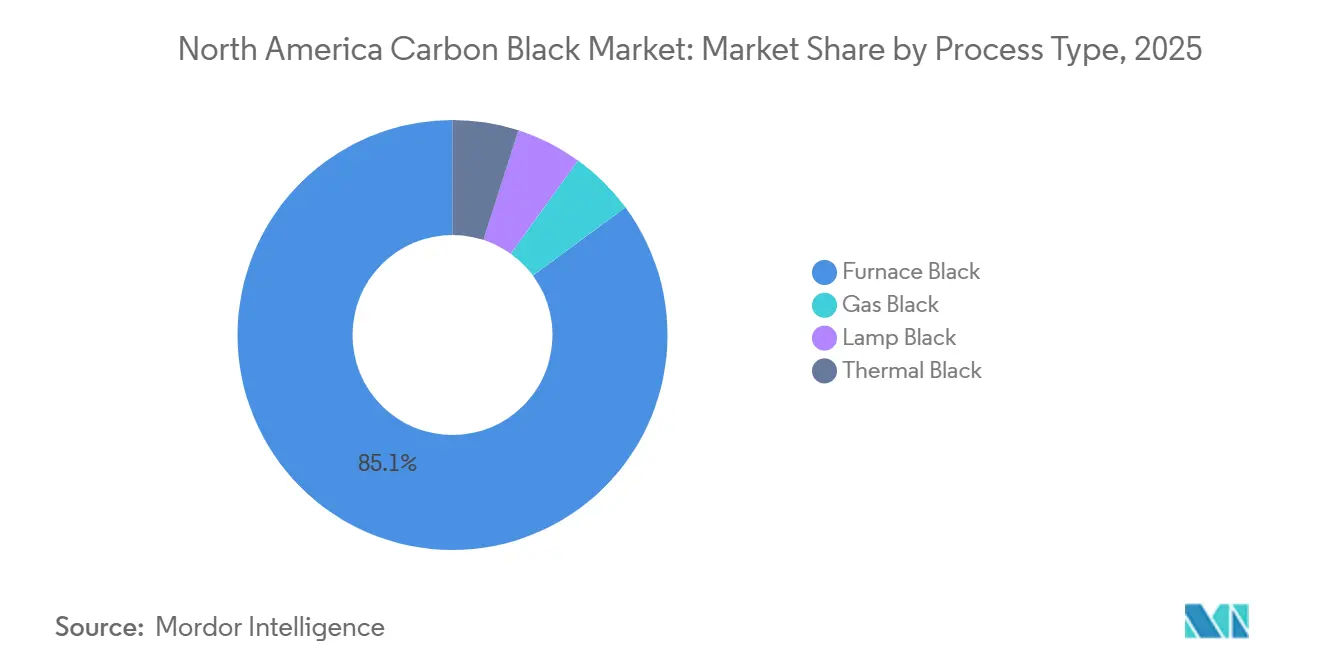

- By process type, furnace black held 85.12% of the North America carbon black market share in 2025, and the segment is forecast to grow at a 4.73% CAGR through 2031.

- By grade, standard products accounted for 77.78% of the North America carbon black market size in 2025, while specialty formulations are poised to expand at a 5.26% CAGR to 2031.

- By application, tires and industrial rubber captured 68.12% of the North America carbon black market in 2025, and the segment is anticipated to grow with the fastest CAGR of 4.61% through 2031.

- By end-user industry, automotive and transportation commanded 68.22% of the North America carbon black market size in 2025, whereas packaging is the fastest-growing end-user industry with a 5.31% CAGR through 2031.

- By geography, the United States led with 60.41% of regional volume in 2025, and Mexico is projected to deliver the highest growth at a 4.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Carbon Black Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for wide-base EV tires needing high-SA furnace blacks | +1.2% | United States, Canada, spillover to Mexico EV hubs | Medium term (2-4 years) |

| Low-cost decant oil availability elevating producer margins | +0.9% | Texas and Louisiana corridor | Short term (≤ 2 years) |

| Canadian tire-label regulations boosting specialty grades | +0.6% | Nationwide Canada | Medium term (2-4 years) |

| Recovered carbon black uptake under OEM ESG mandates | +0.8% | Region-wide, OEM supply chains | Long term (≥ 4 years) |

| On-site modular carbon black units for tire makers | +0.5% | Major U.S. and Mexican tire-manufacturing clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Wide-Base EV Tires Needing High-SA Furnace Blacks

Electric-vehicle tires must accommodate heavier curb weight, instant torque, and low rolling-resistance requirements. As a result, compounders specify N100 and N200 series furnace blacks with surface areas above 100 m²/g, which improve tear strength and lower hysteresis[1]Product-Marketing Group, “PROPEL E8 Launch Press Release,” Cabot Corporation, cabotcorp.com. U.S. EV output from Tesla, Rivian, the Detroit Three, and new entrants is set to exceed 3 million units annually by 2027, ratcheting up demand for these high-performance grades. Cabot’s PROPEL E8 launch in 2025 validated the commercial pull for such products, and ZC Rubber’s Saltillo plant in Mexico will channel large volumes of wide-base and OE EV tires into the region after ramp-up in late 2025. Canada’s Clean Fuel Regulations also add momentum because lower carbon-intensity transportation scenarios accelerate electrification[2]Regulatory Affairs Division, “Clean Fuel Regulations,” Government of Canada, canada.ca. In aggregate, these dynamics raise the baseline growth path for the North America carbon black market while lifting average selling prices.

Low-Cost Decant Oil Availability Elevating Producer Margins

Decant oil from Gulf Coast fluid-catalytic-cracking units delivers the aromatic content, low ash, and high BMCI index required for furnace-black reactors. Utilization across major Texas and Louisiana refineries remained high through 2024–2025, keeping feedstock prices well below the 10-year average despite hurricane-related outages. Tokai Carbon’s cluster of Big Spring, Borger, and Addis plants directly benefits from this cost angle, supporting above-regional average margins even as tire OEMs negotiate tougher transfer-price formulas. The cost edge is less pronounced in Canada and Mexico, where producers either import decant oil or rely on smaller, less optimized domestic refineries. Over the short term, the favorable feedstock environment buttresses capacity utilization decisions and underpins the near-term health of the North America carbon black market.

Canadian Tire-Label Regulations Boosting Specialty Grades

Ontario’s Carbon Black Industry Technical Standard demands a 95% cut in sulfur dioxide emissions at Cabot’s Sarnia and Birla Carbon’s Hamilton sites by July 1, 2028. Compliance investment induces producers to prioritize higher-margin specialty blacks that carry price premiums sufficient to amortize scrubbers and oxidation catalysts. Parallel Clean Fuel Regulations penalize high carbon-intensity inputs, indirectly steering tire and packaging firms toward low-rolling-resistance and ultra-pure blacks. Cabot’s BLACK PEARLS 4350 and 4750 grades, already cleared under U.S. FDA Food Contact Notification 1789, meet these twin objectives and are gaining traction among converters shipping films across the U.S.–Canada border. Consequently, specialty output is increasing faster than commodity grades in Canada, nudging regional mix toward higher value-added products.

Recovered Carbon Black Uptake Under OEM ESG Mandates

Automakers and tier-one suppliers have codified recycled-content targets that include recovered carbon black (rCB). Michelin’s 2024 joint venture with Enviro and Antin aims to scale multi-thousand-ton pyrolysis capacity across North America by 2027. Bridgestone opened a 2025 pilot plant to validate rCB in passenger-tire sidewalls, while ASTM’s D8510 standard now offers an accepted quality-control framework. Offtake agreements between Pyrolyx and Continental underscore growing OEM confidence in rCB consistency, and North America’s 300 million annual scrap-tire pool ensures sufficient feedstock. Over the long term, rising rCB adoption erodes conventional volume growth but raises average unit value, supporting the revenue outlook for the North America carbon black industry.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility on Gulf-Coast shutdowns | -0.7% | Texas and Louisiana corridor | Short term (≤ 2 years) |

| Silica–silane substitution in passenger treads | -1.1% | United States and Canada | Medium term (2-4 years) |

| Competition from Tire-Pyrolysis Derived Fillers | -0.5% | Region-wide, OEM and replacement tire supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility on Gulf-Coast Shutdowns

Hurricanes, planned turnarounds, and crude-slate shifts periodically curtail FCCU output, pushing decant-oil spot prices 30–50% higher within weeks. Tokai Carbon’s 2025 outlook cited feedstock inflation among the chief reasons operating profit could fall 6.1% year-over-year. Orion Engineered Carbons has no long-term fixed-price contracts, so lagged pass-through mechanisms dent margins when oil spikes. Although new refinery projects and crude-to-chemicals configurations might temper volatility beyond 2027, near-term risk remains material for the North America carbon black market.

Silica–Silane Substitution in Passenger Treads

Since the early 1990s, silica reinforced with bifunctional silane has displaced carbon black in passenger tire treads owing to lower rolling resistance and superior wet braking. Evonik, the dominant silane supplier, continues to expand ULTRASIL and COUPSIL capacity, and premium tire models now exceed 50 parts silica per hundred rubber in treads. U.S. and Canadian replacement markets skew toward fuel-efficient designs, magnifying substitution pressure. While commercial, off-the-road, and sidewall applications remain carbon-black heavy, the tread shift subtracts incremental growth points from the North America carbon black market through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Furnace Black Anchors Regional Volume

The North America carbon black market size for the furnace-black segment accounted for 85.12% of the total volume in 2025. Growth to 2031 is set at a 4.73% CAGR, buoyed by the process’s flexibility in generating N100–N900 grades for tires, hoses, belts, inks, and plastics. Orion Engineered Carbons is capitalizing on a USD 215.9 million high-surface-area line at La Porte, Texas, that targets EV tire compounds. The niche roles of gas, lamp, and thermal blacks in conductive coatings, artist pigments, and ultraclean semiconductor packaging keep them relevant.

Monolith Materials offers a disruptive complement: its methane-pyrolysis route yields 14,000 t per annum of fossil-free carbon black and coproduces hydrogen, eliminating Scope 1 emissions. Goodyear commercialized tires using this material in 2025. The North America carbon black market now features a dual pathway—traditional furnace reactors optimized for cost and scale, and low-carbon pyrolysis units optimized for ESG performance. Over time, the successful scale-up of Monolith’s Olive Creek 2 expansion to 56,000 t by 2027 could recalibrate competitive benchmarks on carbon intensity and influence investment priorities among incumbents.

By Grade: Specialty Blacks Outpacing Commodity Supply

Standard grades represented 77.78% of North America's carbon black market volume in 2025, but specialty, conductive, and ESD grades will capture a larger growth delta by logging a 5.26% CAGR to 2031. Cabot’s VULCAN XC and Orion’s PRINTEX brands dominate conductive use cases, reaching bulk resistivity below 1 ohm-cm for lithium-ion cathodes and semiconductor trays. Demand tailwinds include rapid EV battery cell expansion and hyperscale data-center build-outs requiring ESD-safe infrastructure.

Standard products remain the tire workhorses, yet new vehicle platforms and autonomous-driving sensor arrays are pushing OEMs to specify higher-dispersion and lower-PAH blacks even in mainstream compounds. Specialty food-contact variants such as BLACK PEARLS 4350 satisfy benzo[a]pyrene limits of 5 ppb set by the U.S. FDA. As cross-border e-commerce pushes converters to harmonize with the stricter standard, specialty penetration inches upward, lifting the revenue mix of the North America carbon black market.

By Application: Tires Dominate While Packaging Accelerates

Tires and industrial rubber absorbed 68.12% of regional volume in 2025 and will grow at the fastest CAGR of 4.61% through 2031, a trajectory anchored in commercial fleet expansion and the proliferation of EV tire lines. High-structure blacks, needed for wide-base heavy-duty tires that replace dual assemblies, support compound integrity under 4,000-lb axle loads.

The packaging segment is also witnessing significant demand as converters adopt near-infrared detectable masterbatches to unlock higher recycling rates. Ampacet’s REC-NIR-BLACK series illustrates how pigmentation can shift toward lighter-spectra formulations without sacrificing opacity. At the same time, heightened scrutiny of PAH levels forces the switch to ultra-pure blacks, introducing a premium-priced subsegment inside the North America carbon black market. Plastics, toners, inks, coatings, and textile fibers collectively capture the remainder, each harnessing carbon black’s UV-blocking, tinting, or conductivity properties to solve niche performance challenges.

By End-User Industry: Automotive Leads, Electronics Gains Momentum

Automotive and transportation secured 68.22% of tonnage in 2025, mirroring the dominance of tires, belts, hoses, and weather seals. The segment’s growth trajectory aligns with replacement-tire cycles and new-vehicle production forecasts. Yet electronics is punching above its weight: semiconductor fabs in Arizona, Ohio, and Texas alongside multiple U.S. and Canadian battery gigafactories are driving double-digit demand for conductive blacks used in electrodes, EMI-shielded housings, and ESD flooring.

The carbon black demand from the packaging industry is growing at the fastest CAGR of 5.31% through 2031, propelled by e-commerce logistics that require film structures with anti-static and UV-protection attributes. Construction applications such as roofing membranes and sealants remain tied to residential starts and public-works spending, logging steady low-single-digit growth. Textile and apparel uses, currently niche, may scale once smart-fabric rollouts in defense and healthcare migrate from pilots to production. The diversified pull pattern across industries underpins stability in the North America carbon black market, even as individual verticals cycle.

Geography Analysis

The United States contributed 60.41% of carbon black volume in 2025, underpinned by Tokai Carbon’s three-plant network that completed USD 200 million in scrubber and related upgrades during 2024. Abundant decant-oil availability and established tire clusters in Georgia, Tennessee, and Ohio keep unit costs competitive. However, rising Asian tire imports add margin pressure, and continued silica-silane substitution weighs on passenger-tread share. The market also acts as a testing ground for lower-carbon pathways: Monolith’s Nebraska plant is now the world’s first large-scale methane-pyrolysis carbon-black source, giving the United States a strategic lead in fossil-free supply.

Mexico is the fastest grower with a 4.90% CAGR to 2031. ZC Rubber’s USD 550 million Saltillo tire complex will supply 13.5 million passenger-car and 50,000 t off-the-road tires annually after ramp-up, increasing localized black demand. Cabot’s USD 70 million takeover of Mexico Carbon Manufacturing adds 50,000 tons of furnace-black capacity and secures access to a rapidly expanding OE production base. Tariffs of up to 32.24% on Chinese tire imports plus a temporary 35% safeguard duty imposed in April 2024 preserve domestic share for Mexican manufacturers, indirectly lifting the outlook for the North America carbon black market.

Canada presents a nuanced picture. Environmental rules such as Ontario’s Carbon Black Industry Technical Standard impose a 95% SO₂ reduction requirement by mid-2028. Capital spending at Cabot’s Sarnia and Birla Carbon’s Hamilton facilities will raise cost curves but allow premium price capture through specialty offerings. Federal Clean Fuel Regulations further encourage low-rolling-resistance tire compounds, nudging local converters toward high-surface-area or low-PAH blacks. Consequently, Canada’s growth remains positive though constrained to mid-single-digit rates.

Regulatory Landscape

In the United States, carbon black manufacturing is regulated primarily under the EPA National Emission Standards for Hazardous Air Pollutants (NESHAP) framework for Carbon Black Production (40 CFR Part 63). The 2021 residual risk and technology review actions reinforced controls for process vents and compliance obligations such as electronic reporting. These requirements keep air-permit compliance and continuous environmental upgrades central to plant operating strategies, particularly for furnace-black assets concentrated along the Gulf Coast feedstock corridor.

In Canada, Environment and Climate Change Canada (ECCC) provides national environmental oversight, while Ontario has advanced a Carbon Black Industry Technical Standard that requires a 95% sulfur dioxide (SO2) reduction by July 1, 2028 for key facilities in the province, including Cabot in Sarnia and Birla Carbon in Hamilton as referenced in the report context. Across North America, trade and customs policy also influences cost and sourcing decisions for carbon black and related inputs, with U.S. CBP tariff guidance and USTR trade-policy actions creating periodic uncertainty around imported industrial materials even when carbon black is not singled out as a standalone tariff headline.

Value Chain Analysis

The North America carbon black value chain begins with hydrocarbon feedstocks, led by heavy aromatic refinery streams (notably clarified slurry oil/decant oil) that are converted into furnace blacks. Smaller pathways include thermal black made through natural-gas decomposition, along with emerging low-carbon routes such as methane pyrolysis (for example, Monolith Materials). Feedstock availability and pricing are tied to refinery utilization and outage cycles in the U.S. Gulf Coast, shaping producer margins and operating rates for major regional manufacturers.

Manufacturing is dominated by large integrated producers (Cabot, Orion Engineered Carbons, Tokai Carbon, Birla Carbon, Continental Carbon, and Cancarb), supported by circular inputs and substitutes, including recovered carbon black (rCB) from tire pyrolysis and tire-pyrolysis-oil (TPO) use in circular reinforcing carbons. Distribution is largely bulk via rail and truck in pelletized or powder forms to downstream compounders and converters in tires and industrial rubber, plastics and packaging masterbatch, inks and coatings, and electronics-related ESD and conductive applications. Quality control and specification alignment (for low-PAH, conductive, and specialty grades) shape supplier qualification and long-term offtake agreements.

Competitive Landscape

The North America carbon black market is moderately consolidated, with the top five players accounting for a significant market share. Cabot is reinforcing its footprint by acquiring Mexico Carbon Manufacturing, bolstering access to the fastest-growing geography. Orion, for its part, is allocating USD 215.9 million to a La Porte, Texas, expansion tailored to EV and conductive-plastic markets. Investment priorities center on environmental controls and differentiated product portfolios. Tokai completed USD 200 million in emission retrofits across all U.S. plants during 2024, while Orion finished scrubber installations at four sites the same year. Birla Carbon has elected to expand overseas rather than chase a marginal U.S. share, leveraging global scale to feed North America via imports when economics align. Meanwhile, disruptors attack from two flanks: Monolith’s methane-pyrolysis route promises fossil-free carbon black with captive hydrogen sales, and Pyrolyx leads the rCB subset after earning ASTM D8510 compliance, winning offtakes from Continental. Although these challengers represent well under 2% of current tonnage, their ESG credentials win disproportionate mindshare among tire and plastics customers. Price discovery is increasingly indexed to feedstock moves plus formal sustainability attributes. Major buyers are willing to sign multi-year agreements that embed surcharges for certified rCB or low-carbon grades, signaling a gradual shift away from pure cost-plus frameworks. This evolution challenges traditional producers to quantify and market their emission reductions or risk ceding premium niches. At the same time, capacity creep in Asia, particularly in China, keeps import parity low, forcing North American players to differentiate on service level, supply reliability, and environmental footprint rather than on base-grade commodity pricing alone.

North America Carbon Black Industry Leaders

Cabot Corporation

Birla Carbon

Orion Engineered Carbons S.A.

Continental Carbon Company

Tokai Carbon Co., Ltd. (incl. Cancarb)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity area sits where compliance-driven plant upgrades intersect with customer demand for lower-carbon materials. Producers that pair emission-control investments with differentiated product offerings can capture higher-margin specialty and circular grades while meeting tightening air-quality requirements. In Canada, Ontario's Carbon Black Industry Technical Standard targeting a 95% SO2 reduction by July 1, 2028 acts as a concrete catalyst pushing facilities toward capex-heavy controls and product-mix strategies that prioritize premium grades to help amortize compliance costs.

Circular reinforcing carbons and recovered carbon black also form a visible whitespace where tire and plastics customers can secure sustainability attributes without changing end-use performance specifications. Cabot's October 2025 upgrade at Ville Platte, Louisiana, to strengthen circular reinforcing carbon manufacturing using tire pyrolysis oil under an ISCC PLUS mass balance approach points to commercialization beyond pilot-only activity, and the region's large scrap-tire pool supports rCB scaling efforts referenced in the report context. The need for high-surface-area furnace blacks and conductive grades for EV tires and battery supply chains is another near-term value lever, since tighter particle-size control and low-PAH performance requirements can lift value per ton relative to standard reinforcing blacks.

Recent Industry Developments

- February 2026: Cabot Corporation completed its acquisition of Mexico Carbon Manufacturing S.A. de C.V. from Bridgestone, expanding its North American manufacturing footprint with added furnace-black capacity in Mexico. The deal strengthens Cabot's ability to supply tire and rubber customers in the region's fastest-growing geography while improving proximity to expanding OEM tire production corridors.

- October 2025: Cabot Corporation strengthened manufacturing capabilities in North America for circular reinforcing carbons at its Ville Platte, Louisiana, facility under its EVOLVE Sustainable Solutions technology platform. The upgrade supports production using tire pyrolysis oil with an ISCC PLUS mass balance approach, widening the availability of circular-grade supply options for tire makers and other rubber applications.

- December 2024: Orion Engineered Carbons completed emission-control upgrades at four U.S. plants and continued building its La Porte, Texas, high-surface-area line under a USD 215.9 million program. The work improves regulatory compliance headroom while positioning additional output toward EV-tire and conductive-plastics demand that requires tighter performance specifications than standard reinforcing grades.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the annual value of carbon black sold for use across North America, covering material supplied to end users in rubber and non-rubber applications where carbon black is used for reinforcement, pigmentation, and conductivity.

Scope exclusions: We exclude carbon black production equipment, upstream feedstock trading, and carbon black used only for laboratory or pilot research.

Segmentation Overview

- By Process Type

- Furnace Black

- Gas Black

- Lamp Black

- Thermal Black

- By Grade

- Standard Grade Carbon Black

- Specialty Carbon Black

- Conductive and ESD Carbon Black

- By Application

- Tires and Industrial Rubber Products

- Plastics

- Toners and Printing Inks

- Coatings

- Textile Fibers

- Other Applications

- By End-User Industry

- Automotive and Transportation

- Packaging

- Building and Construction

- Electrical and Electronics

- Textile and Apparel

- Others

- By Geography

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk work sets the frame for the model by clarifying how much carbon black is produced, traded, and consumed in the United States, Canada, and Mexico. We used public sources such as USITC trade statistics, US Census Bureau manufacturing data, Statistics Canada industrial datasets, Mexico trade and industry releases, and environmental agency publications that describe emissions-related operating conditions for carbon black plants.

On top of that, company annual reports, investor presentations, and association webpages were reviewed to map capacity additions, shutdowns, and application mix shifts that can move demand year to year. Where needed, paid subscriptions available internally were used to pull company financials and intelligence, run patent checks, and read shipment-level import and export data to stress-test the public totals. These examples are not exhaustive, and additional sources were also reviewed for data collection, validation, and clarification during the analysis.

Primary Interviews and Surveys

Primary work was used to confirm how demand is split across tires, industrial rubber goods, plastics, coatings, and ink related uses, and then to validate typical pricing behavior by grade and contract structure. We spoke with producers, distributors, compounders, and large end users across the United States, Canada, and Mexico, so secondary signals could be challenged and corrected where they did not match on-the-ground purchasing patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 31% | |

| Smaller Players: 16% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production and trade data are used to reconstruct the available supply in North America, which is then aligned to end-use consumption across key application pools. Once that high-level total is set, we corroborate it with selective bottom-up approximations, such as sampling supplier sales by application, checking distributor throughput, and using typical price per ton ranges multiplied by estimated tonnage to keep the value result realistic.

Inputs that were treated as core market fingerprints include tire output and replacement demand trends, non-tire rubber goods activity, plastics and coatings production indicators, regional operating rates and capacity changes at carbon black plants, and the spread between specialty grades and conventional grades that drives average selling prices. When a data gap appeared (for example, limited visibility on smaller importers or short-term production outages), it was handled through conservative interpolation anchored to trade flows, utilization discussions from interviews, and neighboring-year patterns.

For forecasting, scenario analysis was used so the base case stays grounded in what buyers and suppliers expect for automotive production, tire demand, and industrial output, followed by adjustments for feedstock and energy cost pass-through timing. Final year values were checked for consistency with expected capacity availability and a reasonable price progression, before the forecast line was locked.

Data Validation & Update Cycle

Validation is done in layers so the model does not rely on one data stream. We compare the calculated market value against independent signals like import intensity, visible capacity changes, and application demand markers, and then we review any large variances before sign-off. Where an outlier is found, the assumption is revisited and, if needed, experts are re-contacted to confirm whether the change was structural or temporary.

Each report is refreshed annually, and interim checks are made when a material event occurs, such as a plant shutdown, major capacity addition, or a sharp feedstock price movement that can shift selling prices quickly. Before delivery, a final pass is completed so clients receive the most current view that still ties back to a repeatable set of steps and inputs.

Mordor Intelligence's North America Carbon Black Market Size Compared With Other Published Estimates

Published market values for North America carbon black can look different because firms use different coverage rules, different price build-ups, and different timing for currency and base-year updates. In practice, the split between conventional grades and specialty grades, and whether recovered material is counted, can change the value number even when tonnage trends look similar.

Recovered carbon black sits inside Mordor Intelligence's scope, and that inclusion can raise the total versus studies that only count virgin material sold from primary production. Differences also come from whether Mexico and cross-border imports are fully captured, how tire versus non-tire demand is allocated, and whether prices are modeled as a simple average or are adjusted by grade mix and contract lag, followed by how often those assumptions are refreshed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.82 B (2025) | |

| Global Consultancy A | USD 3.94 B (2025) | Uses a revenue view that appears to lean more heavily on tire-led demand weighting, and it provides limited transparency on whether recovered carbon black and smaller import flows are included in the same way. |

| Trade Journal B | USD 2.09 B (2022) | Anchored to an earlier base year, which can understate later pricing and mix shifts, and it may reflect a narrower counted basket by type or channel rather than a full application-weighted grade mix. |

The spread in values is mostly explained by what is included in the counted material set, how grade mix influences average prices, and whether trade and regional coverage are fully captured. By tying assumptions to observable production and trade signals, and then re-checking them through interviews, the final estimate stays easier to trace and repeat when conditions change.

Key Questions Answered in the Report

What is the projected value of the North America carbon black market in 2031?

The market is expected to reach USD 4.95 billion by 2031.

Which process type dominates regional production?

Furnace black accounts for 85.12% of volume in 2025 and is on track for a 4.73% CAGR through 2031.

Why is specialty carbon black growing faster than standard grades?

Specialty and conductive blacks benefit from EV batteries, electronics, and stricter food-contact rules, delivering a 5.26% CAGR versus the overall 4.42%.

Which country shows the fastest growth outlook?

Mexico leads with a 4.90% CAGR, supported by new tire plants and added furnace-black capacity.

How are producers addressing sustainability pressures?

Companies are investing in emission-control upgrades, scaling recovered carbon black, and piloting methane-pyrolysis routes that cut Scope 1 emissions to zero.

What is the impact of silica–silane substitution on carbon black demand?

Substitution in passenger-car treads trims growth by about 1.1% on the CAGR forecast, especially in the U.S. and Canada.

Page last updated on: