Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

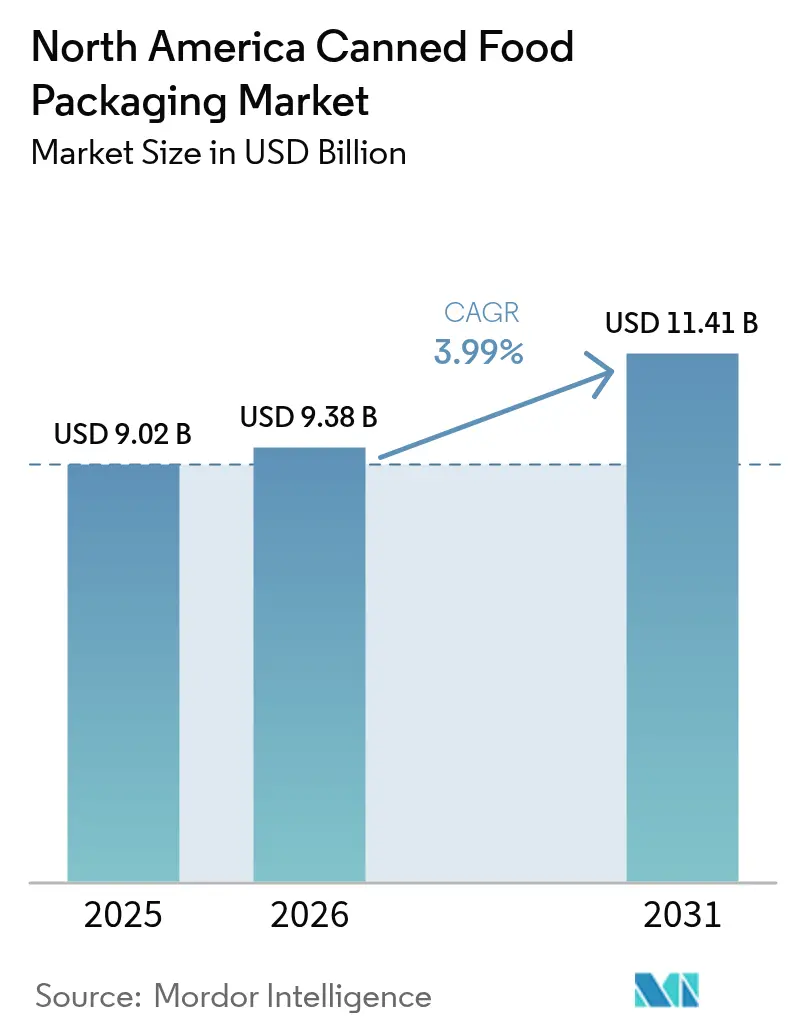

| Base Year Market Size (2025) | USD 9.02 Billion |

| Market Size (2026) | USD 9.38 Billion |

| Market Size (2031) | USD 11.41 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

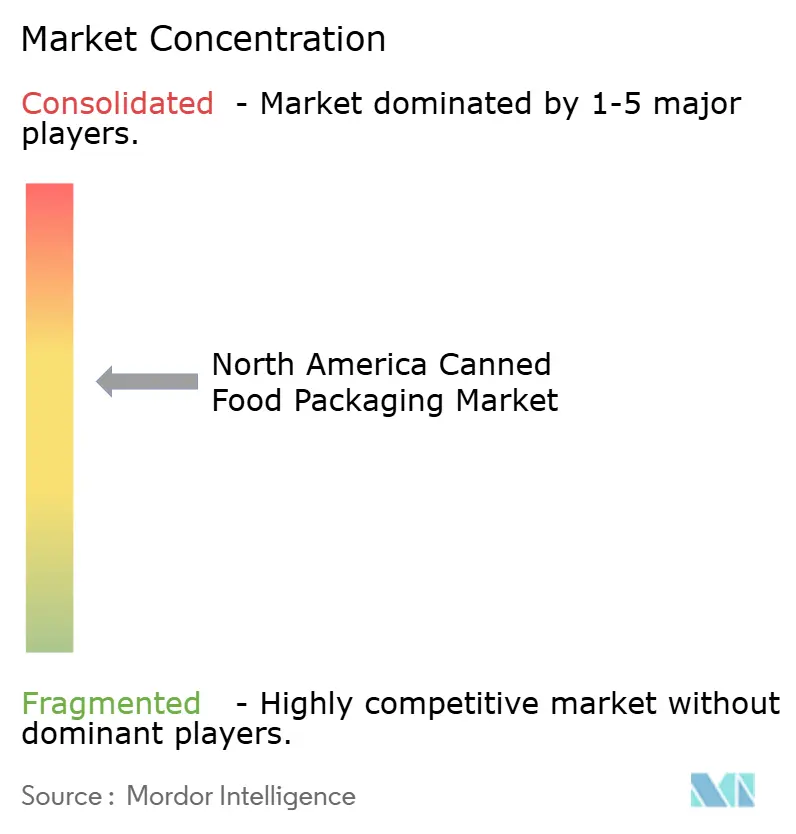

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Canned Food Packaging Market Analysis by Mordor Intelligence

The North America canned food packaging market size in 2026 is estimated at USD 9.38 billion, growing from 2025 value of USD 9.02 billion with 2031 projections showing USD 11.41 billion, growing at 3.99% CAGR over 2026-2031. Aluminum retained leadership with 54.57% share in 2024, supported by closed-loop recycling systems that match government recycling targets and reinforce premium brand positioning.[1]“Crown Holdings, Inc. Reports First Quarter 2025 Results,” Crown Holdings, crowncork.com Ready-made meals dominated consumption at 28.95% of value thanks to remote-work lifestyles and rising single-serve preferences, while soups and broths posted the fastest growth at a 5.68% CAGR as shoppers leaned toward comfort fare during economic uncertainty. Structural innovation is another growth catalyst: two-piece draw-and-redraw (DRD) formats are scaling at 6.01% CAGR because they trim metal use and integrate easy-open ends that simplify meal prep. Regionally, the United States controlled a 72.95% share in 2024 on the back of robust grocery retail networks, whereas Mexico is accelerating at a 6.534% CAGR through 2030 amid industrialization and middle-class expansion.

Key Report Takeaways

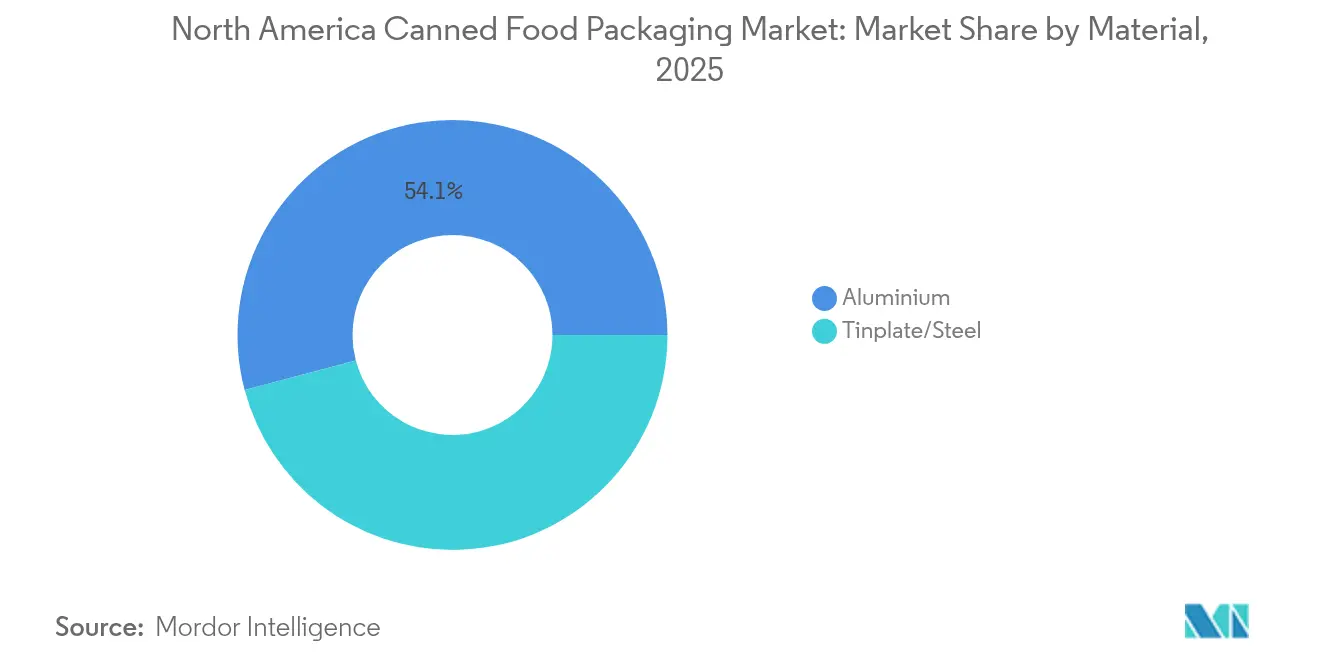

- By material, aluminum led with 54.12% share of the North America canned food packaging market in 2025; aluminum is projected to grow at a 5.18% CAGR through 2031.

- By application, ready-made meals held 28.61% revenue share in 2025; soups and broths are forecast to advance at a 5.51% CAGR to 2031.

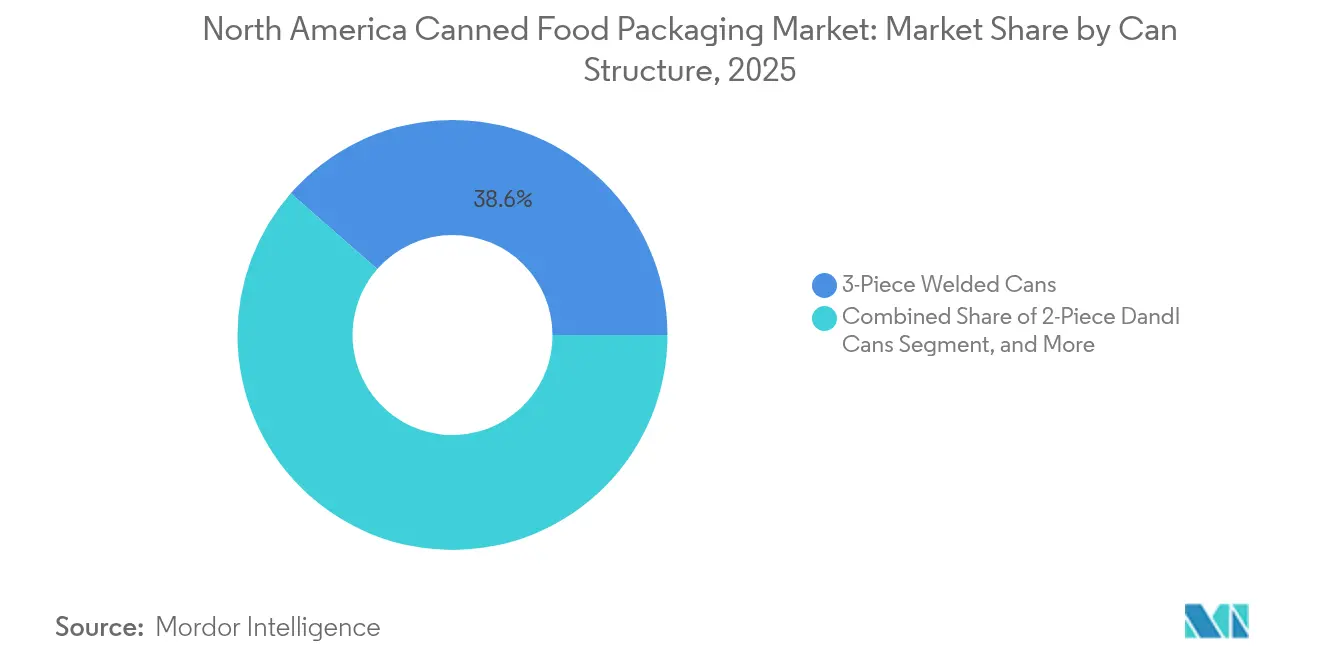

- By can structure, three-piece welded formats accounted for 38.55% share in 2025, while two-piece DRD cans are expanding at a 5.82% CAGR.

- By can capacity, the 201–500 g segment captured 29.42% share of the North America canned food packaging market size in 2025 and is pacing at a 5.66% CAGR.

- By geography, the United States commanded a 72.40% share of the North America canned food packaging market size in 2025; Mexico records the highest projected CAGR at 6.34% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Canned Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of convenience and ready-made meals | +1.2% | United States and Canada, with spillover to Mexico urban centers | Medium term (2-4 years) |

| Sustainability push for infinitely-recyclable metal cans | +0.8% | North America-wide, strongest in California, Ontario, British Columbia | Long term (≥ 4 years) |

| Surge in pet-food canning capacity across U.S. and Canada | +0.9% | United States and Canada, concentrated in Midwest and Ontario | Short term (≤ 2 years) |

| Retailer private-label expansion in canned categories | +0.7% | United States and Canada, led by major retail chains | Medium term (2-4 years) |

| On-shoring of metal-can production to avoid Section-232 tariffs | +0.5% | United States, with indirect benefits to Canadian suppliers | Short term (≤ 2 years) |

| OEM demand for QR-coded smart cans enabling traceability | +0.3% | North America-wide, early adoption in premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Convenience and Ready-Made Meals

Ready-made meals already represent 28.95% of the North America canned food packaging market and continue to climb as workers balance hybrid schedules with limited cooking time. Mars is spending USD 2 billion on U.S. production through 2026, a figure that illustrates brand confidence in shelf-stable formats that allow streamlined distribution and year-long inventory cycles. Two-piece DRD lines added by Crown in Iowa and Minnesota shorten seaming steps, yielding sleeker cans that fit cup-holder-style niches popular in single-serve soups. FDA traceability rules are further motivating adoption of lot-coded ends that simplify recalls and reinforce consumer trust. Taken together, these dynamics keep the North America canned food packaging market firmly aligned with the convenience trend.

Sustainability Push for Infinitely-Recyclable Metal Cans

Aluminum’s infinite recyclability resonates with state mandates in California, Ontario, and British Columbia that require high post-consumer content by 2028. Crown reports that roughly 80% of new beverage product launches now rely on aluminum, a signal that food portfolios will follow the same path as brand owners sync packaging choices with ESG metrics. Electrolit’s USD 400 million Waco plant is designed for non-virgin substrates, illustrating how incoming capacity is future-proofed for circular-economy targets. Because metal can be remelted endlessly with no barrier loss, retailers use its credentials as an on-pack storytelling theme to justify premium shelf pricing. As regulations tighten, the sustainability moat strengthens, locking in long-run growth for the North America canned food packaging market.

Surge in Pet-Food Canning Capacity Across U.S. and Canada

Pet humanization means owners demand microbiological safety equal to infant food, favoring retortable metal that delivers a 24-month shelf life without preservatives. Nestlé Purina is investing USD 220 million in Mexico while ADM opens a USD 39 million wet-food plant in the U.S., collectively adding millions of 3-oz to 13-oz cans per week. Crown’s Dubuque and Owatonna lines specialize in tapered shapes that ease bowl emptying for small-breed diets, proving that format customization captures niche demand. Mid-size 201–500 g containers, already the fastest-growing capacity band, benefit most from these launches. The category’s recession resilience offsets raw-material swings, thereby anchoring near-term volumes in the North America canned food packaging market.

Retailer Private-Label Expansion in Canned Categories

Private labels give grocers a margin hedge as branded inflation persists. Amazon’s Saver entry leverages QR-enabled lids to push recipe videos, elevating engagement while keeping retail prices 10–15% under national offers. Crown notes that 46% of U.S. shoppers now buy private-label products exclusively, pushing converters to flex plant schedules for shorter runs and varied label art. Silgan secures multi-year supply deals that currently cover roughly 90% of the 2024 forecast can volumes, locking in asset utilization above 88% and stabilizing EBITDA despite metal volatility. As more retailers treat canned aisles as loyalty battlegrounds, procurement teams increasingly favor the North America canned food packaging market for its scale, supply security, and track-and-trace capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic retort pouches displacing mid-size food cans | -0.7% | United States and Canada, strongest in ready-meal segments | Medium term (2-4 years) |

| Tinplate and aluminium price volatility squeezing converters | -0.9% | North America-wide, acute impact on specialty manufacturers | Short term (≤ 2 years) |

| Regulatory uncertainty around BPA-replacement chemistries | -0.4% | United States and Canada, varying by state/province | Long term (≥ 4 years) |

| Labour shortages at North-American can-making plants | -0.6% | United States and Canada, concentrated in manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic Retort Pouches Displacing Mid-Size Food Cans

Lightweight flexible retort packs cut logistics costs by up to 30% compared with three-piece cans, attracting ready-meal brands that target urban millennials prioritizing portability. Retailers favor stand-up pouches, too, because each linear foot of shelf holds roughly 15% more SKUs than equivalent can facings, boosting category revenue density. Yet cans still prevail in 121 °C retort cycles where pouch delamination risk rises, and in value-pack formats where dent resistance matters during e-commerce fulfillment. Converters defend share by offering peel-off foil membranes and microwavable coatings that replicate pouch convenience. The contest limits, but does not reverse, volume growth for the North America canned food packaging market.

Tinplate and Aluminum Price Volatility Squeezing Converters

Tinplate now trades near USD 1,400 per metric ton after Section 232 tariffs removed tariff-rate quotas, driving two price hikes of 8–16% at Independent Can in 2025 alone. Crown had to pass along USD 94 million of metal inflation in Q1 2025, yet contractual lags compressed quarterly margins by 240 basis points. Domestic tinplate capacity covers barely 1% of U.S. steel output, so specialty grades often rely on imports from Germany or Taiwan, creating supply gaps when vessel slots tighten. As metals swing, some niche converters trim SKUs or exit low-volume lines, consolidating demand among the top five suppliers. Volatility, therefore, clouds near-term EBITDA trajectories across the North America canned food packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Aluminum’s Sustainability Premium Underpins Leadership

Aluminum garnered 54.12% of North America canned food packaging market share in 2025 and is expanding at a 5.18% CAGR as brands highlight closed-loop recovery rates exceeding 70%. The substrate’s light weight slashes freight emissions and its bright surface supports high-definition printing that elevates shelf appeal. Steel remains indispensable for bulk tomato paste and institutional soup packs, especially Sizes #10 and #300, yet Section 232 tariffs have tilted cost curves, nudging mainstream processors toward aluminum ends even on steel bodies.

Innovation furthers aluminum uptake: alloy refinements let mills roll gauges down to 0.205 mm without pinhole risk, yielding an immediate 6% metal saving per can. Nestlé’s La Choy line adopted this thin wall in 2025, cutting annual metal needs by 1,200 tons. As state deposit programs add multipliers for containers with >70% recycled content, can makers that leverage used-beverage-can (UBC) feedstock can gain cost insurance. These fundamentals secure aluminum’s top slot in the North America canned food packaging market.

By Application: Ready-Made Meals Still Rule, Soups Surge Ahead

Ready-made meals commanded a 28.61% share of the North America canned food packaging market in 2025 as time-starved households embraced heat-and-eat kits that eliminate perishability concerns. Brand owners cooperated with converters to roll out integrated easy-open ends and microwave-safe lacquers that shorten prep to under two minutes.

Soups and broths, while smaller, are growing quickest at 5.51% CAGR on the strength of premium bone broths that retail above USD 4.25 per 14 oz can. Large pull tabs and matte varnishes reinforce artisan cues even in mass grocery, widening price bandwidth. The North America canned food packaging market size for soup alone is projected to reach USD 1.82 billion by 2031, reflecting steady cold-weather consumption patterns and category reinvention around global flavors.

By Can Structure: Three-Piece Predominates but Two-Piece DRD Gains Pace

Three-piece welded formats held 38.55% share in 2025, thanks to entrenched line assets capable of 1,800 cans per minute changeovers. These lines deliver the lowest cost per thousand for traditional stack-height cans used in diced tomato and vegetable staples.

Two-piece DRD cans, however, are surging at a 5.82% CAGR because fewer seams translate to 9–11% metal savings and lower micro-leak risk. Crown’s 2024-25 Iowa plant switches between 211×400 and 300×407 bodies with less than 40 minutes of idle time, enabling mixed-SKU output for private-label customers. As canners chase e-commerce durability, DRD’s monolithic body offers dent resistance that reduces returns. Thus, structure choice is becoming a strategic lever within the North America canned food packaging market.

By Can Capacity: Mid-Size 201–500 g Aligns with Portion Control

Mid-range cans captured 29.42% share of the North America canned food packaging market size in 2025 and are advancing at 5.66% CAGR as health-focused shoppers portion calories more tightly. These cans cover single or dual servings, curbing food waste for smaller households.

Pet food magnifies the trend: 5.5 oz and 12.5 oz units make up nearly 70% of wet formulas, providing easy-lift formats for senior owners. Above-1,000 g cans persevere in foodservice beans and institutional soup, but limited freezer space in urban restaurants places a cap on volume. Up to Up-to-200 g slim cans appeal to gourmet pâtés and keto meals, yet their higher lid-to-body metal ratio keeps costs above the mass-market norm.

Geography Analysis

The United States accounted for 72.40% of the North America canned food packaging market in 2025 on the back of deep grocery penetration and a resilient manufacturing base clustered in the Midwest. Section 232 import duties are accelerating domestic sourcing, prompting players like Kimberly-Clark to budget over USD 2 billion for in-region automation and distribution hubs through 2030, further solidifying U.S. dominance.

Canada delivers steady incremental gains underpinned by producer responsibility laws in Ontario and Québec that incentivize high recycling rates for metal. Lassonde’s USD 200 million New Jersey facility, although located in the U.S., is set to serve Canadian private-label volumes too, showcasing supply-chain integration. Concurrently, ingredient makers such as Jungbunzlauer invest CAD 200 million in Ontario fermentation plants, anchoring upstream inputs required by Canadian packers.

Mexico is the growth hot spot, climbing at 6.34% CAGR to 2031 as urbanization lifts demand for shelf-stable proteins and beans, core uses for two-piece D&I cans. Nestlé’s USD 1 billion 2025-27 capex plan selects Mexico for new culinary lines, banking on a swelling middle class that values longer pantry life in warmer climates. Local steelmaker Ternium boosts lacquered-coil output, trimming inbound freight and enhancing regional competitiveness within the North America canned food packaging market.

Competitive Landscape

Market concentration is moderate: Silgan controls just above 50% U.S. unit volume, while Crown, Ball Metalpack (now Sonoco Metal Packaging), and Ardagh hold most of the rest.[3]“Quarterly Reports: Q4 2024,” Silgan Holdings, sec.gov Capital intensity-new two-piece presses that exceed USD 22 million per line-limits new entrants.

Aluminum supply alliances are strategic. Novelis guarantees Crown 300,000 tons of UBC-based coil annually, insulating it from London Metal Exchange shocks. Silgan’s 2024 Weener acquisition added 4,000 staff and advanced dispensing closures that cross-sell with food cans, giving the firm a wider customer toolkit.

Digital traceability is emerging as a differentiator. Trials pairing near-infrared inks with blockchain registries record retort date, seal pressure, and pallet ID, allowing pet-food brand owners to pinpoint quality deviations in under eight minutes, versus days previously. Players able to embed these smart features at line speed are poised to widen their share inside the North America canned food packaging market.

North America Canned Food Packaging Industry Leaders

Amcor plc

Crown Holdings, Inc.

Ball Corporation

CANPACK S.A.

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mars announced a USD 2 billion commitment to U.S. manufacturing through 2026, including a USD 240 million Nature’s Bakery site in Utah and a USD 450 million Royal Canin plant in Ohio.

- May 2025: Kimberly-Clark unveiled plans to invest more than USD 2 billion in a new Warren, Ohio, facility and in expanding Beech Island, South Carolina, operations.

- April 2025: Crown Holdings reported Q1 2025 net sales of USD 2.89 billion and increased full-year EPS guidance to USD 6.70–7.10.

- March 2025: U.S. reinstated 25% Section 232 tariffs on all steel and aluminum imports, ending exemptions for Canada and Mexico.

North America Canned Food Packaging Market Report Scope

The market is defined by the revenue accrued from sales of canned food packaging products offered by vendors in the North American region.

The North America canned food packaging market is segmented by material (tin/steel, aluminum), product type (ready meals, meat, seafood, others), and country (United States, Canada). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material

| Tinplate/Steel |

| Aluminium |

By Application

| Ready-made Meals |

| Meat |

| Sea Food |

| Pet Food |

| Fruits and Vegetables |

| Soups and Broths |

| Dairy and Infant Nutrition |

| Other Applications |

By Can Structure

| 2-Piece D&I Cans |

| 2-Piece DRD Cans |

| 3-Piece Welded Cans |

By Can Capacity

| Up to 200 g |

| 201 – 500 g |

| 501 – 1000 g |

| Above 1 000 g |

By Country

| United States |

| Canada |

| Mexico |

| By Material | Tinplate/Steel |

| Aluminium | |

| By Application | Ready-made Meals |

| Meat | |

| Sea Food | |

| Pet Food | |

| Fruits and Vegetables | |

| Soups and Broths | |

| Dairy and Infant Nutrition | |

| Other Applications | |

| By Can Structure | 2-Piece D&I Cans |

| 2-Piece DRD Cans | |

| 3-Piece Welded Cans | |

| By Can Capacity | Up to 200 g |

| 201 – 500 g | |

| 501 – 1000 g | |

| Above 1 000 g | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America canned food packaging market in 2026?

The market stands at USD 9.38 billion in 2026 and is on track to reach USD 11.41 billion by 2031 at a 3.99% CAGR.

Which material leads in North American food cans?

Aluminum leads with 54.12% share thanks to its infinite recyclability and barrier performance.

What is the fastest-growing application for food cans?

Soups and broths register the highest growth, advancing at a 5.51% CAGR through 2031.

Why are two-piece DRD cans gaining traction?

They cut metal use up to 11%, integrate easy-open ends, and deliver stronger dent resistance, lifting adoption at a 5.82% CAGR.

Which country shows the quickest growth in canned food packaging?

Mexico is expanding the fastest, recording a 6.34% CAGR driven by industrialization and rising middle-class demand.

How are tariffs affecting can makers?

The reinstated 25% Section 232 tariffs raise tinplate and aluminum costs, compressing margins and accelerating domestic sourcing.

Page last updated on: