Marine Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

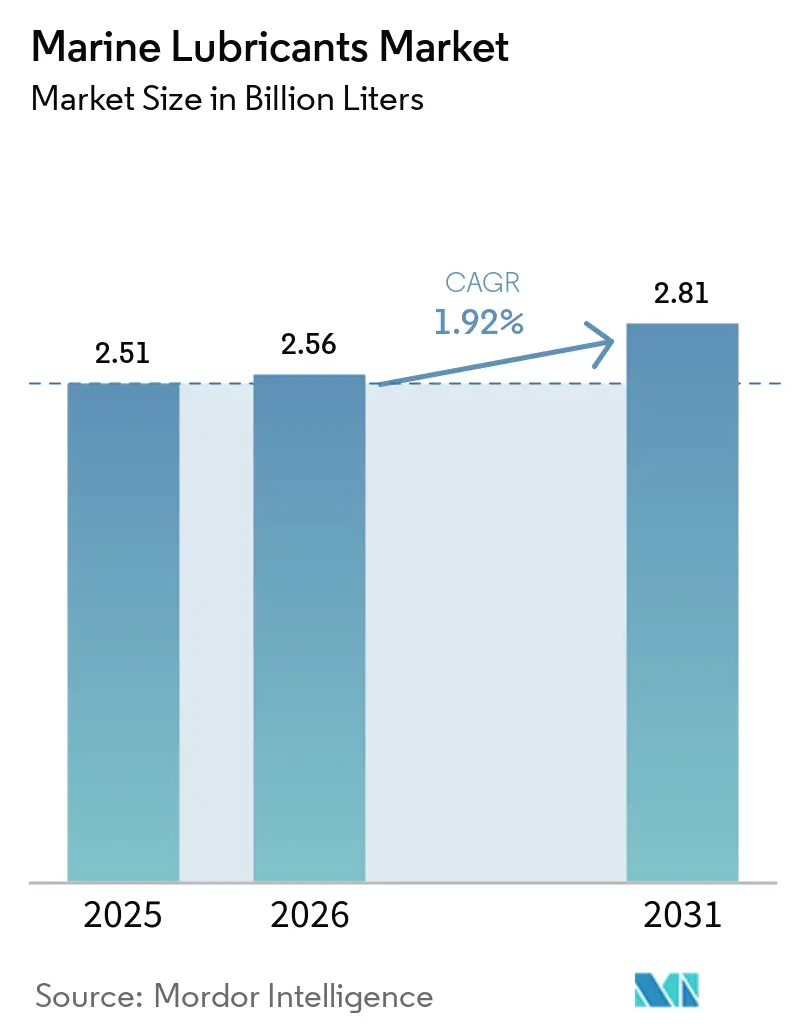

| Market Volume (2026) | 2.56 Billion liters |

| Market Volume (2031) | 2.81 Billion liters |

| Growth Rate (2026 - 2031) | 1.92% CAGR |

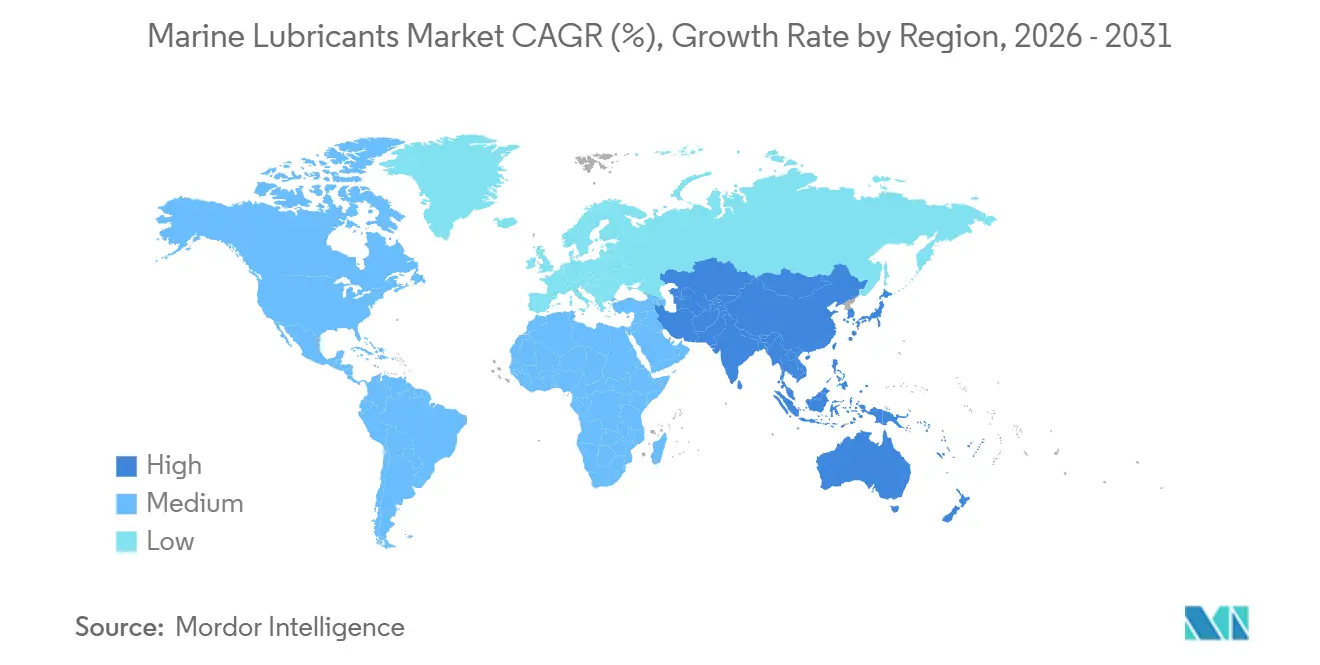

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Lubricants Market Analysis by Mordor Intelligence

The Marine Lubricants Market size was valued at 2.51 billion liters in 2025 and is estimated to grow from 2.56 billion liters in 2026 to reach 2.81 billion liters by 2031, at a CAGR of 1.92% during the forecast period (2026-2031). As the IMO-2020 sulfur cap continues to be enforced, demand is increasingly shifting towards premium 40-BN cylinder oils. Meanwhile, the Asia-Pacific region's leadership in shipbuilding is bolstering consistent consumption of trunk-piston oil. Engines running on dual-fuel LNG and methanol are turning to specialized formulations. These not only extend drain intervals but also reduce consumption per voyage. This trend, while resulting in modest volumes, is concealing a significant underlying value growth. The construction of offshore wind vessels, dynamic-positioned support vessels, and the slowly emerging Arctic routes are all leaning towards synthetic and bio-based grades, moving away from traditional mineral oils. Furthermore, digitized procurement platforms, exemplified by Chevron’s OnePort-Closelink, are streamlining lead times, boosting transparency, and prompting smaller fleets to sidestep conventional distributors.

Key Report Takeaways

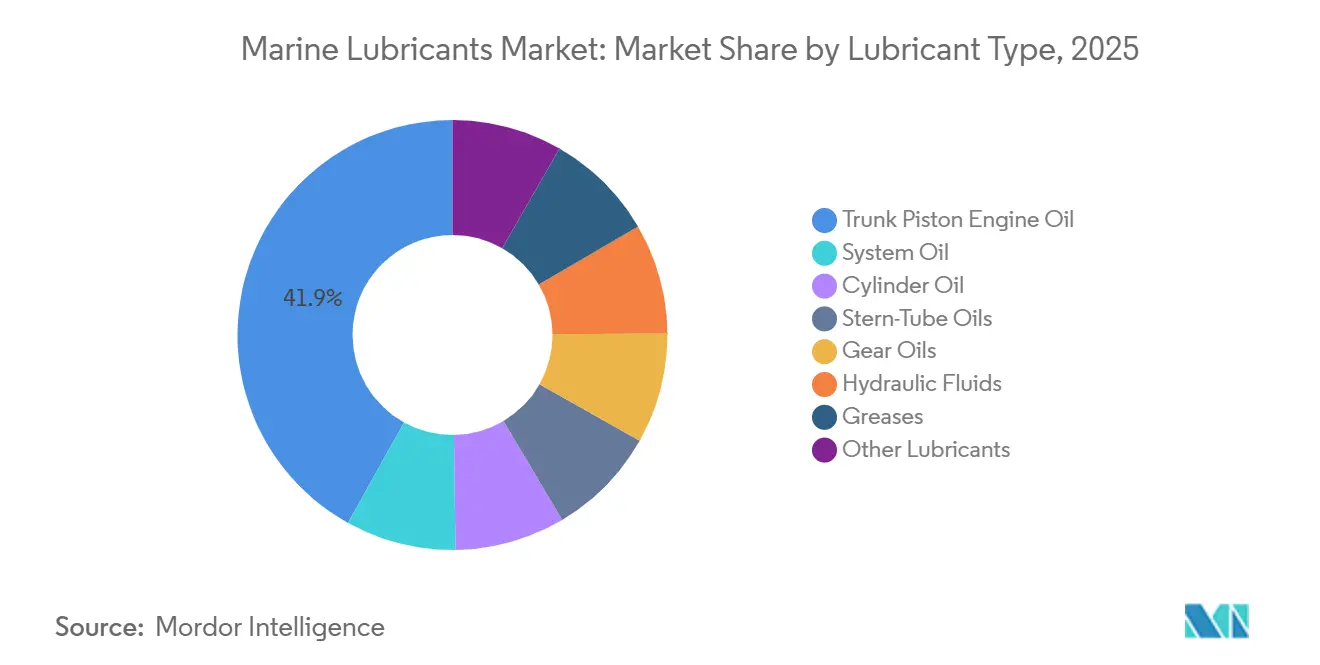

- By lubricant type, trunk-piston engine oil led with 41.92% of 2025 volume, while stern-tube oils advance at a 2.11% CAGR through 2031.

- By base stock, mineral oil commanded 71.96% of 2025 volume; bio-based lubricants are the fastest-growing subsegment at a 2.18% CAGR.

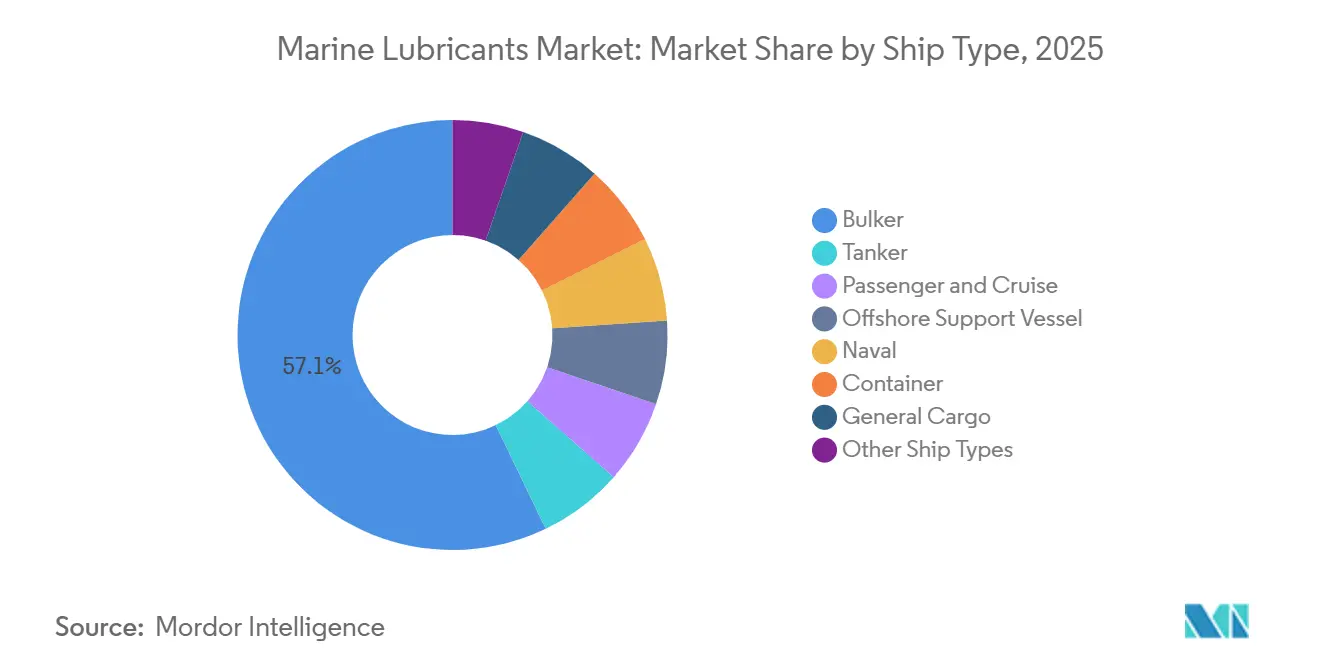

- By ship type, bulkers held 57.14% of the 2025 demand; offshore support vessels record the highest projected CAGR at 2.13% through 2031.

- By application, main propulsion captured 52.21% of the 2025 volume; auxiliary engines and generators expand at a 2.17% CAGR to 2031.

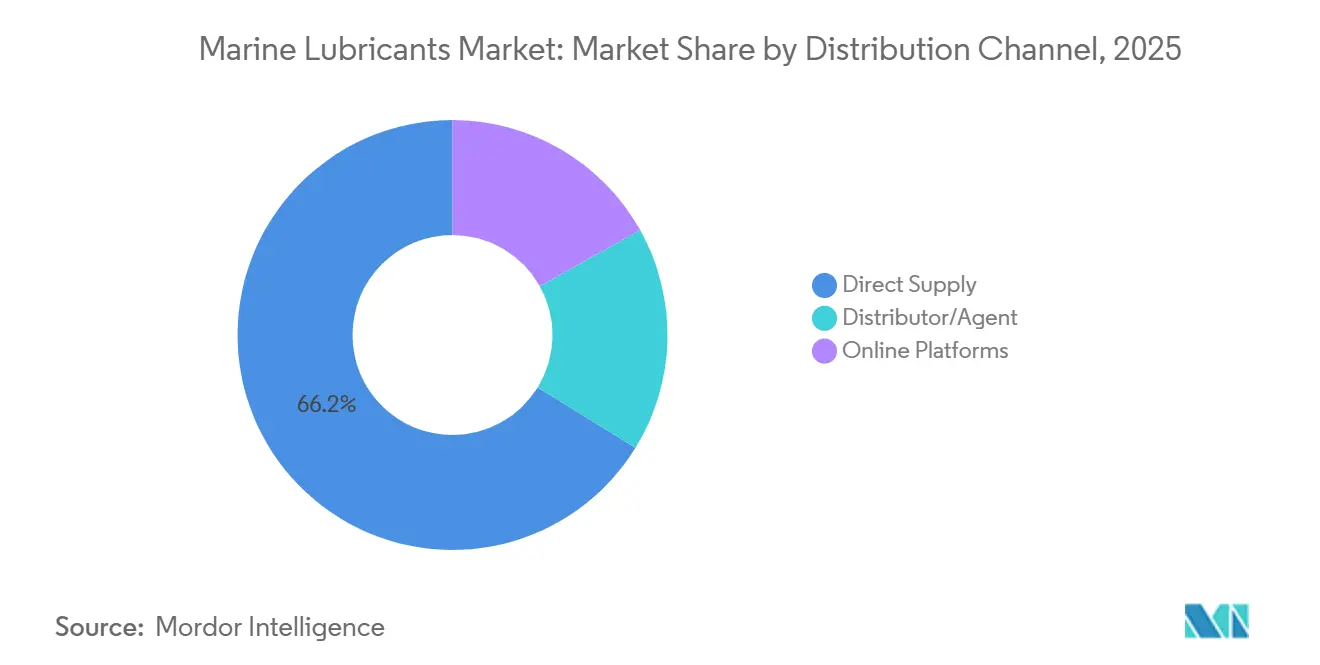

- By distribution channel, direct supply secured 66.22% of the 2025 volume; online platforms posted the fastest growth at a 2.35% CAGR through 2031.

- By geography, Asia-Pacific led with 46.45% of 2025 volume and is advancing at a CAGR of 2.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marine Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| IMO-2020 sulfur cap boosting premium lubricant demand | +0.40% | Global, with highest compliance enforcement in EU and North America | Medium term (2-4 years) | |

| Fleet modernization and expansion in Asia | +0.50% | Asia-Pacific core, spill-over to Middle-East and Africa | Long term (≥ 4 years) | |

| Offshore-wind installation vessel boom | +0.20% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) | |

| Dual-fuel LNG engines needing specialized cylinder oils | +0.30% | Global, led by Asia-Pacific and Europe | Short term (≤ 2 years) | |

| Opening of Arctic shipping routes | +0.10% | Arctic Council member states (Russia, Norway, Canada) | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

IMO-2020 Sulfur Cap Boosting Premium Lubricant Demand

As global enforcement tightens on the sulfur limit, the uptake of 40-BN cylinder oils is on the rise. These oils play a crucial role in mitigating corrosive wear in two-stroke engines that utilize very-low-sulfur fuel oil. ExxonMobil’s Mobilgard 540, Shell’s Alexia 40, and Chevron’s Taro Ultra Advanced 40 have anchored a premium segment, now accounting for a significant portion of cylinder oil volume, a notable increase from earlier years. Port-state-control audits in key locations like Singapore, Rotterdam, and Los Angeles ensure high compliance among liner fleets. This compliance has led operators with scrubber-fitted bulkers to strategically hedge between 70-BN and 40-BN formulations. While premium liter prices have seen an uptick, the combination of longer drain intervals and reduced feed rates has effectively curbed the total voyage cost, driving value-led growth in the marine lubricants market.

Fleet Modernization and Expansion in Asia

In recent years, Asia-Pacific shipyards have delivered substantial gross tons, accounting for a significant share of global newbuilds. This surge directly boosts the demand for initial-fill and first-service lubricants. With a robust vessel backlog at China State Shipbuilding Corporation and a notable surge in orders in India, thanks to the Sagarmala corridor, the orderbook remains strong through the coming years. New designs for dual-fuel containers, bulkers, and PCTCs are now seeking specialized cylinder oils, compatible with methanol, LNG, or even ammonia test runs. This demand is creating a widening formulation gap between regional blenders in Asia and global majors. As charterers enforce IMO Tier III clauses, Southeast Asia’s aging fleet faces an intensified replacement cycle, leading to an uplift in the CAGR outlook for the marine lubricants market.

Offshore-Wind Installation Vessel Boom

By the end of the decade, global offshore wind capacity is set to expand significantly. This growth will give rise to jack-up, service-operation, and cable-laying vessels, which consume hydraulic fluid and stern-tube oil at rates much higher than similarly sized cargo ships. Under EPA VGP rules, overboard interfaces are mandated to use biodegradable lubricants. This regulation is accelerating the adoption of synthetic esters and bio-based polyalphaolefins, despite their higher cost compared to mineral grades. Onboard DEME’s Norse Wind, dynamic-positioning thrusters and a 3,000-ton crane amplify the frequency of hydraulic-oil change-outs. This mechanical complexity, combined with regulatory demands, carves out a lucrative niche in the marine lubricants market.

Dual-Fuel LNG Engines Needing Specialized Cylinder Oils

Maersk’s upcoming methanol-ready container ships, highlight the lubricant challenges associated with low-viscosity, high-water fuels. Platforms like MAN’s ME-GI and WinGD’s X-DF are pushing the envelope on requirements for detergency, alkalinity, and film strength. This demand has led to the creation of bespoke 40-BN products, including Shell Alexia S5. However, the landscape is complicated by fragmented OEM protocols, necessitating blenders to validate their formulations for each engine brand, be it MAN, WinGD, or Wärtsilä. While this elongates certification cycles, it simultaneously fosters brand loyalty. The uptick in engine orders has spurred incremental growth in demand for specialized grades, enhancing revenue prospects in the marine lubricants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| On-board oil-purification/reuse systems | -0.30% | Global, highest adoption in Europe and North America | Medium term (2-4 years) | |

| Emerging water-lubricated bearing technology | -0.20% | Europe and Asia-Pacific, driven by environmental regulations | Long term (≥ 4 years) | |

| Rapid uptake of condition-based monitoring reducing top-ups | -0.20% | Global, led by digitally advanced fleets in Europe and Asia | Short term (≤ 2 years) | |

| Source: Mordor Intelligence | ||||

On-Board Oil-Purification/Reuse Systems

Alfa Laval's PureDry centrifuge efficiently removes water and particulates, significantly extending drain intervals and reducing annual lubricant purchases for each vessel[1]Alfa Laval, “PureDry Centrifuge System 2024,” ALFALAVAL.COM . At the same time, fleets using PANOLIN's closed-loop system are achieving savings on waste oil. This financial advantage highlights the return on investment, particularly in light of stricter EU Ship Recycling norms. With quick paybacks, cost-conscious bulker owners are drawn to these solutions, even as this trend moderates net volume growth in the marine lubricants market, despite an expanding fleet.

Emerging Water-Lubricated Bearing Technology

Thordon's SXL bearing, now widely adopted across vessels, has eliminated oil use from stern-tubes, significantly reducing spill risks and maintenance demands[2]Thordon Bearings, “SXL System Press Release,” THORDONBEARINGS.COM . Wärtsilä's EnergoProW, installed on cruise ships, reduces underwater radiated noise and aligns with emerging IMO noise guidelines. However, the technology faces challenges, as abrasive wear in sediment-heavy deltas has slowed its adoption among Southeast Asian coasters. Nevertheless, each conversion to water-lubrication results in an annual reduction in environmentally friendly stern-tube oil consumption, slightly dampening the growth trajectory of the marine lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lubricant Type: Trunk-Piston Dominates, Stern-Tube Oils Surge

In 2025, trunk-piston engine oil dominated the marine lubricants market, accounting for 41.92% of the total volume. Meanwhile, stern-tube oils, driven by the rising adoption of biodegradable grades due to mandates from offshore wind vessels and the EPA's VGP directives, are on track for the fastest growth at a 2.11% CAGR during the forecast period of 2026-2031.

Next-generation installation vessels, equipped with dynamic-positioning thrusters and jacking systems, significantly boosted the consumption of stern-tube and hydraulic fluids. Cylinder oil demand, now transitioning to the 40-BN grade, held steady at a notable volume. While system-oil demand declined due to fewer gearboxes from integrated electric drives, consumption of grease and hydraulic fluids increased, fueled by the growing complexity of deck machinery. In summary, while premium niches experienced robust growth, the decline in system oils was offset, ensuring continued revenue prospects for stakeholders in the marine lubricants market.

By Base Stock Type: Mineral Holds, Bio-Based Gains

In 2025, mineral basestocks made up 71.96% of the total liters delivered. However, bio-based volumes, supported by EPA and EU ecolabel regulations, are on a growth trajectory, stimulating a 2.18% CAGR during the forecast period of 2026-2031. This trend is set to elevate their market share in marine lubricants from the current single digits to the low teens by 2031. Despite challenges such as limited oxidative stability in equatorial heat and constrained Group III+ supply chains in the Asia-Pacific, bio-based volumes gained traction. Synthetics carved out a niche in Arctic operations and LNG compressors.

Additionally, Petronas-Eni's biorefinery in Pengerang, scheduled to commence in 2028, promises to ease availability bottlenecks and advocate for regional price parity. While mineral oils are expected to retain their dominance until 2031, increasing regulatory scrutiny and stringent port inspections are gradually steering the market towards more lucrative biodegradable alternatives.

By Ship Type: Bulkers Lead, OSVs Accelerate

In 2025, bulkers accounted for 57.14% of the total liters consumed, driven by their substantial deadweight and extended voyage durations. While the marine lubricants market for bulkers is projected to grow modestly, offshore support vessels are expected to grow faster at a rate of 2.13% during the forecast period of 2026-2031. This acceleration is largely due to their pivotal role in servicing the ambitious global offshore wind capacity. As container lines roll out alternative-fuel-ready tonnage, specialized cylinder-oil demand is seeing a corresponding increase. This demand remains robust even as the trend of slow-steaming moderates overall engine hours.

Tankers continue to grapple with fuel-saving measures, while cruise ships expand their auxiliary-engine capacity to handle increased hotel loads. Although naval and niche vessels constitute a smaller segment, their premium synthetic consumption highlights their value, bolstering overall margins in the marine lubricants market.

By Application: Main Propulsion Leads, Auxiliaries Gain

Main propulsion engines consumed 52.21% of the total liters in 2025. While feed-rate optimization and condition monitoring moderated growth, the introduction of new horsepower in vessels upheld overall volume. Auxiliary engines, benefiting from hybrid-power retrofits and increased hotel loads in cruise and RoPax segments, are expected to log a 2.17% CAGR during the forecast period of 2026-2031. Although stern-tube and bearing applications face potential substitution from water-lubricated systems, the EPA's VGP regulations are bolstering bio-based demand. The expanding offshore wind sector is diversifying revenue streams, with gearbox, hydraulic, and deck machinery needs reflecting this growth.

By Distribution Channel: Direct Contracts Rule, Online Platforms Rise

In 2025, direct supply constituted 66.22% of the total liters, as major oil companies cemented their presence by offering multi-port coverage guarantees to liner clients. Distributor networks played a pivotal role in supporting smaller tramp fleets. However, digital marketplaces, led by Chevron's integrated API, transformed the landscape, enhancing transparency and streamlining procurement cycles. While online channels captured only a single-digit share in 2025, their projected 2.35% CAGR growth during the forecast period of 2026-2031 positions them as a potential game-changer in the marine lubricants market, especially in Europe and North America, where e-payments and data-driven inventory systems have become standard.

Geography Analysis

Asia-Pacific, accounting for 46.45% of 2025's liters, is set to post a 2.11% CAGR through the forecast period of 2026-2031. China's robust order book, combined with India's Sagarmala-driven yard revival, fuels initial-fill demand. South Korea's orders for LNG-ready super-carriers are increasingly favoring high-spec cylinder oils. In Indonesia and Vietnam, fragmented distribution offers opportunities for agile regional blenders.

North America, seizing a significant slice of the 2025 volume, is witnessing a shift in lubricant mixes. This evolution, leaning towards EPA-mandated biodegradable stern-tube oils, is spurred by the renewal of Jones Act tonnage and the Atlantic's offshore wind project constructions. Canada's Arctic passages are demanding low-temperature synthetics, while Mexico's resurgent upstream activities are amplifying Offshore Support Vessel (OSV) consumption.

Europe, anchoring a considerable chunk of the 2025 volume, is buoyed by offshore wind activities in the North Sea and Baltic. EU regulations on ship recycling and waste oil are advocating for onboard purification. While this push has constrained volume, it has simultaneously elevated unit value. Following Russia's market exit due to sanctions, Gazprom Neft and LUKOIL have stepped in to bridge the supply voids. Yet, their broader market penetration remains hampered by a lack of Original Equipment Manufacturer (OEM) approvals.

South America, with Brazil's pre-salt OSVs ensuring a steady consumption baseline, contributed a notable share of the 2025 volume. However, currency fluctuations in Argentina and Colombia are curtailing their import capabilities.

The Middle East and Africa, together, represent a significant chunk of global lubricant consumption. In Qatar, booming LNG megaprojects, coupled with growth at Jebel Ali and Suez diversions via Cape routes, are extending voyage distances and amplifying lubricant consumption per trip. Meanwhile, in the Gulf and East Africa, ADNOC Distribution's digital expansion is reshaping the competitive landscape for marine lubricants.

Mordor Intelligence provides coverage of the marine lubricants market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The marine lubricants market is moderately consolidated. Major players, including Shell, ExxonMobil, Chevron, TotalEnergies, and BP, dominate the global lubricant scene. They control a substantial share of consumption through direct supply networks that span over 800 ports. A partial sale of Castrol to Stonepeak underscores the private equity sector's keen interest in the lubricant market's steady cash flows. Chevron's strategic integration with API aims to solidify its digital presence. Regional players like Petronas, ENEOS, and Sinopec are capitalizing on their proximity to Asia-Pacific yards and burgeoning biolubricant capabilities to expand their market share.

The race for technological differentiation is heating up: Shell and Chevron have secured OEM approvals for ammonia-ready lubricants, positioning themselves ahead of potential latecomers. FUCHS's strategic maneuvers, including acquisitions like Lubcon and a full takeover of its Turkish joint venture, spotlight a trend of mid-tier consolidation targeting high-performance niches. While niche bio-players such as PANOLIN have carved out a commendable share of the EPA-compliant stern-tube sales, their global footprint remains modest, underscoring both the market's potential and its fragmentation.

Marine Lubricants Industry Leaders

Chevron Corporation

Shell plc

TotalEnergies SE

Exxon Mobil Corporation

BP plc (Castrol)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Turkish shipowner Susesea enhanced the cylinder lubrication strategy for its fleet of six bulk carriers by implementing Chevron’s Taro Ultra Advanced 40 (TUA 40). In collaboration with Chevron Marine Lubricants and its regional distributor, Petrol Ofisi, Susesea optimized vessel operations and achieved a reduction in cylinder oil feed rates by approximately 33%, resulting in both technical and commercial advantages.

- February 2025: Lubrication Engineers has entered into a definitive agreement to acquire the industrial brands of Royal Purple, including marine lubricants and related products. Upon completion of the transaction, Lubrication Engineers will hold exclusive rights to manufacture and sell Royal Purple-branded industrial products.

Global Marine Lubricants Market Report Scope

Marine lubricants are engineered to withstand the rigors of the marine environment, including high temperatures and humidity, as well as the corrosive effects of saltwater. These lubricants play a crucial role across various components and operations of cargo fleets, oil tankers, and other maritime vessels.

The marine lubricants market is segmented by lubricant type, base stock type, ship type, application, distribution channel, and geography. By lubricant type, the market is segmented into system oil, cylinder oil, trunk piston engine oil, stern-tube oils, gear oils, hydraulic fluids, greases, and other lubricants. By base stock type, the market is segmented into mineral oil, synthetic lubricants, and bio-based lubricants. By ship type, the market is segmented into bulker, tanker, container, general cargo, passenger and cruise, offshore support vessel, naval, and other ship types. By application, the market is segmented into main propulsion engine, auxiliary engine and generators, gearbox and transmission, stern-tube and bearings, air-compressor and hydraulic systems, and other applications. By distribution channel, the market is segmented into, direct supply, distributor/agent, online platforms. The report also covers the market size and forecasts for marine lubricants in 24 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

| System Oil |

| Cylinder Oil |

| Trunk Piston Engine Oil |

| Stern-Tube Oils |

| Gear Oils |

| Hydraulic Fluids |

| Greases |

| Other Lubricants |

| Mineral Oil |

| Synthetic Lubricants |

| Bio-Based Lubricants |

| Bulker |

| Tanker |

| Container |

| General Cargo |

| Passenger and Cruise |

| Offshore Support Vessel |

| Naval |

| Other Ship Types |

| Main Propulsion Engine |

| Auxiliary Engine and Generators |

| Gearbox and Transmission |

| Stern-Tube and Bearings |

| Air-Compressor and Hydraulic Systems |

| Other Applications |

| Direct Supply |

| Distributor/Agent |

| Online Platforms |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Lubricant Type | System Oil | |

| Cylinder Oil | ||

| Trunk Piston Engine Oil | ||

| Stern-Tube Oils | ||

| Gear Oils | ||

| Hydraulic Fluids | ||

| Greases | ||

| Other Lubricants | ||

| By Base Stock Type | Mineral Oil | |

| Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By Ship Type | Bulker | |

| Tanker | ||

| Container | ||

| General Cargo | ||

| Passenger and Cruise | ||

| Offshore Support Vessel | ||

| Naval | ||

| Other Ship Types | ||

| By Application | Main Propulsion Engine | |

| Auxiliary Engine and Generators | ||

| Gearbox and Transmission | ||

| Stern-Tube and Bearings | ||

| Air-Compressor and Hydraulic Systems | ||

| Other Applications | ||

| By Distribution Channel | Direct Supply | |

| Distributor/Agent | ||

| Online Platforms | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the marine lubricants market in 2026?

The marine lubricants market size stands at 2.56 billion liters in 2026, and it is projected to reach 2.81 billion liters by 2031 at a 1.92% CAGR.

Which lubricant type accounts for the biggest marine lubricants market share?

Trunk-piston engine oil led with 41.92% of 2025 volume driven by its ubiquity across medium-speed auxiliaries.

What CAGR is expected for bio-based marine lubricants?

Bio-based grades advance at about 2.18% CAGR through 2031, outperforming the overall market.

Which region dominates demand?

Asia-Pacific captured 46.45% of 2025 volume and continues to outpace global growth at 2.11% CAGR.

Page last updated on: