Market Overview

| Study Period | 2020 - 2031 |

|---|---|

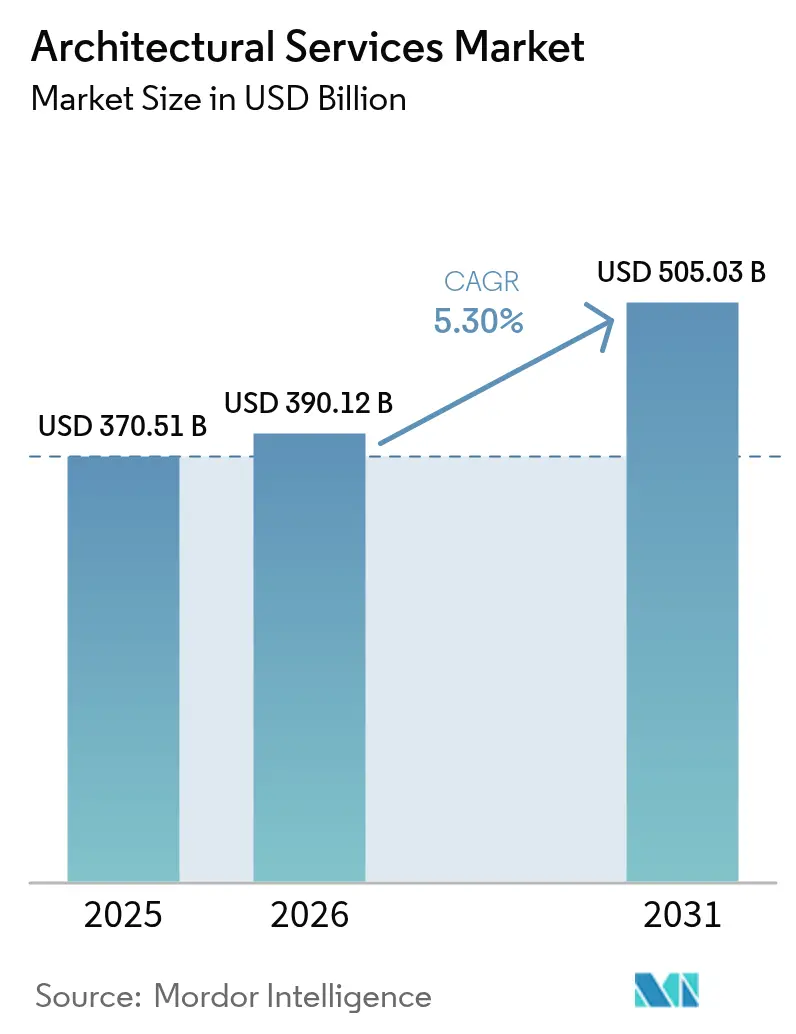

| Market Size (2026) | USD 390.12 Billion |

| Market Size (2031) | USD 505.03 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

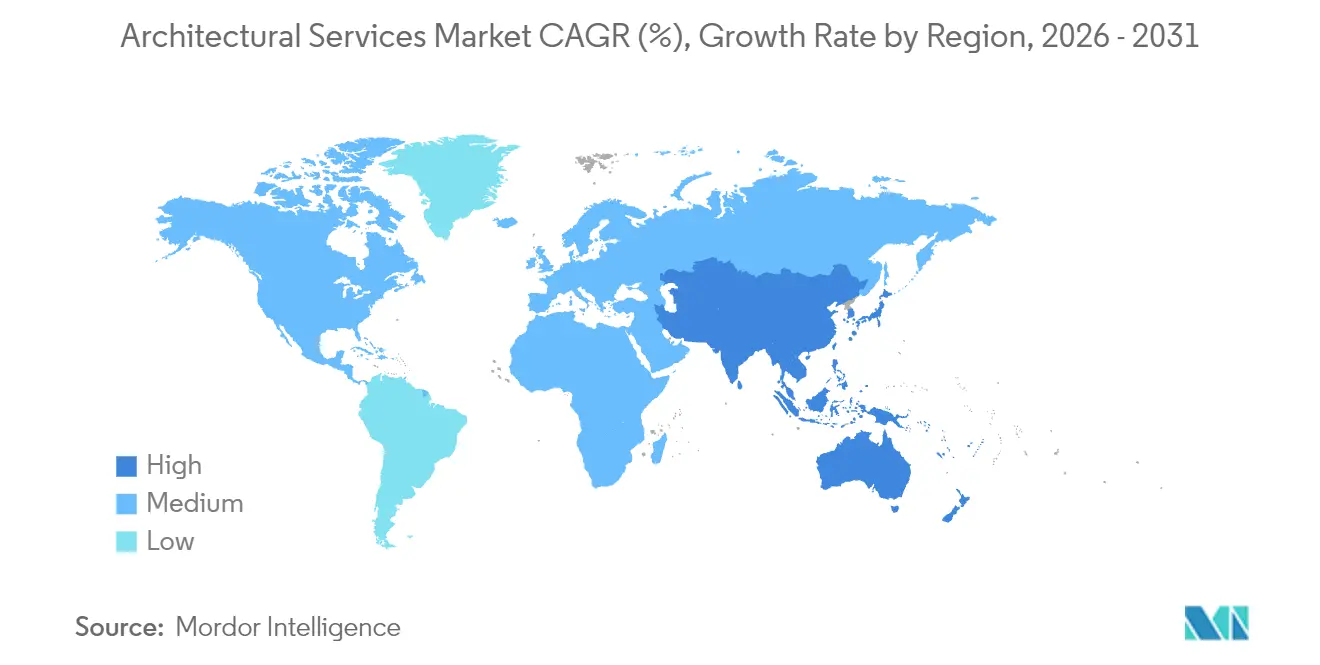

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

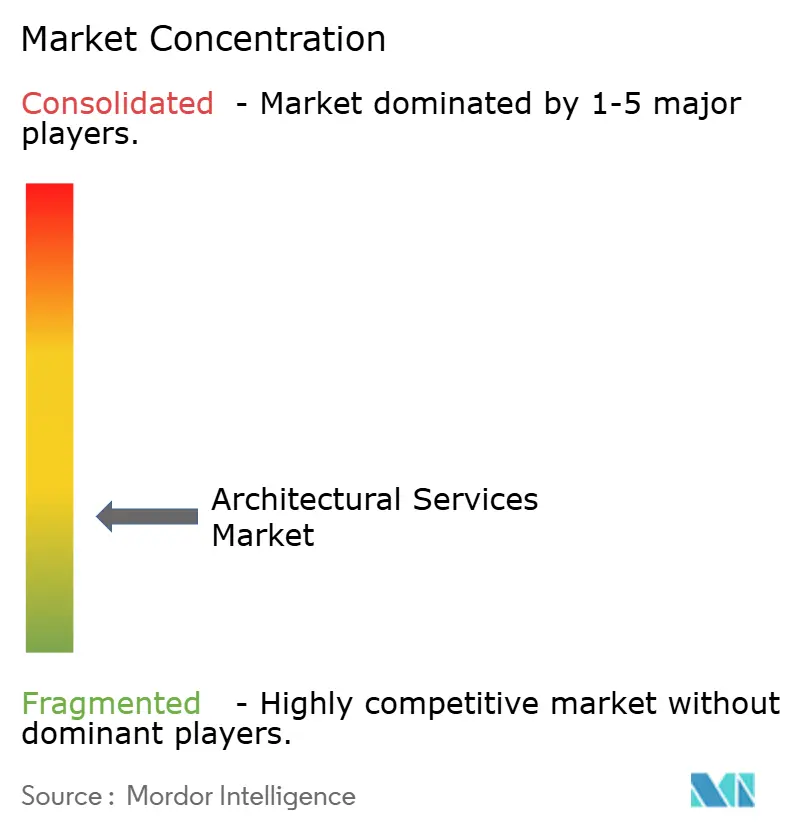

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Architectural Services Market Analysis by Mordor Intelligence

The architectural services market size was valued at USD 370.51 billion in 2025 and estimated to grow from USD 390.12 billion in 2026 to reach USD 505.03 billion by 2031, at a CAGR of 5.30% during the forecast period (2026-2031). Post-pandemic infrastructure outlays, a surge in smart-city programs, and growing sustainability mandates anchor this expansion, while artificial intelligence (AI) and digital-twin platforms improve project speed and accuracy. North America keeps its revenue lead through federally funded transport, power, and water upgrades, yet Asia Pacific produces the steepest growth curve as governments commit large-scale capital to meet urban housing and mobility gaps. Across all regions, heightened client focus on carbon neutrality and operational resilience pushes firms toward low-embodied-carbon materials, net-zero design targets, and climate-risk scoring. Competitive intensity rises as global firms acquire niche specialists to secure multidisciplinary talent and to widen local regulatory expertise. Meanwhile, rising wages and volatile input costs pressure margins, prompting broader use of automation for repetitive documentation and early-stage massing studies.

Key Report Takeaways

- By service type, Design and Documentation commanded 40.92% of the architectural services market share in 2025, while Urban Planning and Master-planning is projected to expand at a 6.28% CAGR through 2031.

- By end user, residential projects accounted for 34.21% of the architectural services market size in 2025; industrial and manufacturing is poised for the fastest growth at 6.12% CAGR to 2031.

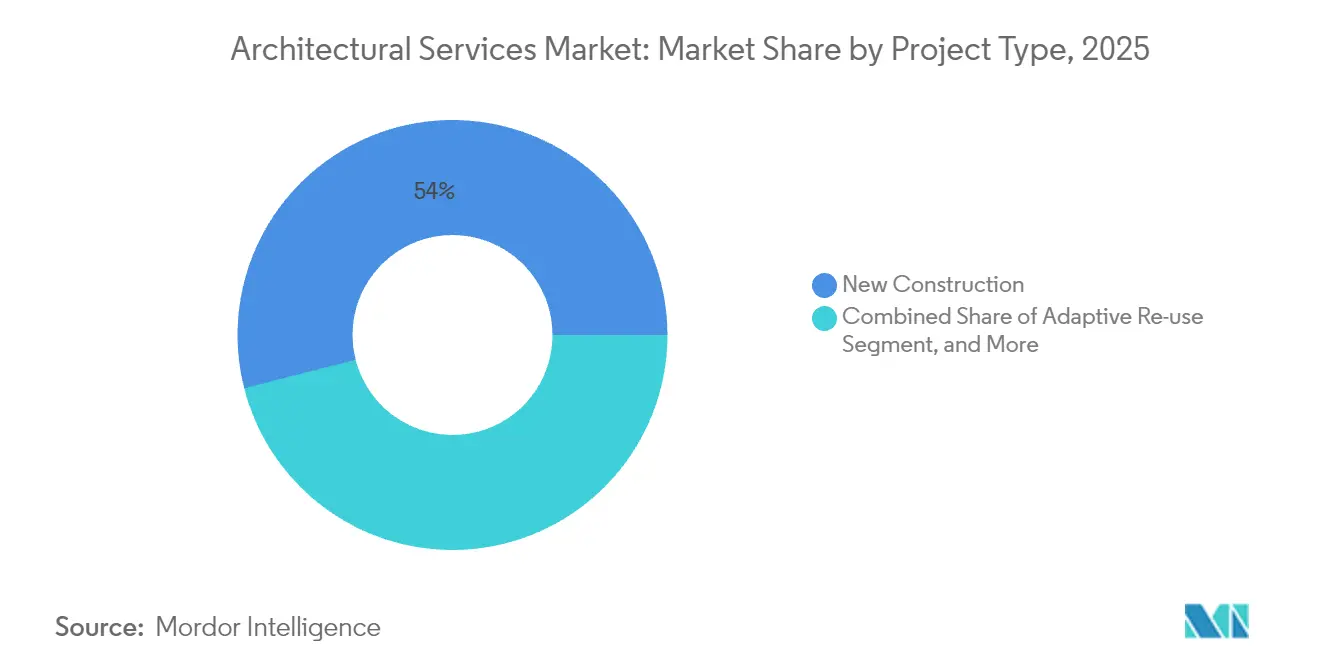

- By project type, new construction held 53.98% of the architectural services market share in 2025, whereas adaptive reuse is set to advance at a 5.98% CAGR during 2026-2031.

- By BIM adoption level, Level 1 workflows represented 54.72% of the architectural services market size in 2025, with Level 3+ integrated environments forecast to grow at 6.29% CAGR through 2031.

- By region, North America led with 39.14% revenue share in 2025 and Asia Pacific is projected to realize the strongest regional CAGR of 6.07% to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Architectural Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for green buildings | +1.2% | Global, with early gains in California, EU, Singapore | Medium term (2-4 years) |

| Growing adoption of Building Information Modelling (BIM) | +0.9% | North America and EU core, spill-over to APAC | Long term (≥ 4 years) |

| Expansion of modular and prefabricated construction | +0.8% | APAC core, Middle East expansion | Short term (≤ 2 years) |

| Urban infrastructure spending rebound post-COVID-19 | +1.1% | Global, concentrated in APAC and North America | Medium term (2-4 years) |

| Generative-AI-driven concept design workflows | +0.7% | North America and EU early adoption | Long term (≥ 4 years) |

| Design-build-operate digital-twin subscription models | +0.6% | Global, with enterprise focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for green buildings drives market transformation

Mandatory sustainability codes such as California’s CALGreen and the International Green Construction Code enforce energy-, water-, and carbon-performance thresholds that now shape baseline client expectations.[1]California Building Standards Commission, “CALGreen,” dgs.ca.gov Global corporations link facility strategies to environmental, social, and governance (ESG) targets, rewarding firms that present costed net-zero pathways and cradle-to-cradle material schedules. As LEED v4 remains the dominant global certification, architects build internal capability in daylight simulation, whole-building life-cycle analysis, and renewable-energy integration.[2]U.S. Green Building Council, “LEED v4 for Building Design and Construction,” usgbc.org Fee premiums for verified green design offset rising labor and software costs, and project pipelines advance in healthcare, education, and logistics where net-zero metrics unlock cheaper finance.

Growing adoption of Building Information Modelling transforms project delivery

Singapore’s 90% BIM utilization demonstrates how coordinated 3D environments and design-for-manufacture principles shorten construction cycles and limit rework. Global market value for BIM software is projected to reach USD 22.1 billion by 2030 under a 16.3% CAGR, with advanced Level 3+ environments attracting the highest momentum. Natural-language Text2BIM agents streamline object creation and parameter tagging, curbing authoring time and lowering entry barriers for small studios. Set against this potential, firms cite acute shortages of mid-career BIM managers, intensifying recruitment costs and delaying complex multidisciplinary projects. Governments answer with mandatory BIM documentation on public buildings, accelerating demand despite transitional skill gaps.

Expansion of modular and prefabricated construction reshapes design practices

Permanent modular construction revenue in the Gulf Cooperation Council hit USD 3.4 billion in 2023 and is scaling further on the back of Saudi Vision 2030 megaprojects. Prefabricated and volumetric systems promise 30%-50% faster schedules and significant waste reductions under factory-controlled tolerances. Architect workflows now integrate manufacturing constraints-such as module size limits and robotic welding clearances-conceptually to secure regulatory approvals and site logistics. The Asia Pacific region leads in high-rise modular towers, with proof-of-concept projects exceeding 20 stories and demonstrating viable seismic and fire safety performance. Sustainability dividends arise from material optimization and reduced on-site crew travel, dovetailing with green-building incentives.

Generative-AI-driven concept design workflows enhance speed and creativity

More than half of surveyed construction professionals already apply AI to feasibility testing, zoning analysis, and quantity take-offs. Generative algorithms iterate thousands of massing and façade options against performance metrics, helping clients weigh daylight, structural efficiency, and cost within hours. Firms confirm productivity gains of up to 31% on schematic-design phases, freeing senior architects to focus on client interaction and code negotiation. Intellectual-property concerns and cyber-security risks remain, but early adopters gain a pricing edge, especially in build-to-rent residential and data-center briefs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of BIM-proficient architects | -0.8% | Global, acute in North America and EU | Medium term (2-4 years) |

| Volatile construction-material prices | -0.6% | Global, with regional variations | Short term (≤ 2 years) |

| Regulatory fragmentation across municipalities | -0.4% | North America and EU primarily | Long term (≥ 4 years) |

| Cyber-security risk in connected-building design files | -0.3% | Global, enterprise-focused markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of BIM-proficient architects constrains market growth

Industry surveys show that 96% of design firms experience skills shortages, especially at intermediate BIM levels, forcing 51% of companies to decline new work. U.S. architecture services lost 1,300 jobs in November 2024, even as the wider construction sector must add 439,000 workers by 2025 to meet demand. Salaries for BIM coordinators have climbed faster than inflation, eroding profit margins. Companies fund internal academies and partner with universities, yet training cycles lag behind project timetables. AI-assisted modeling automates repetitive layout tasks but cannot replace human code interpretation, client liaison, or context-specific detailing, keeping skilled labor pivotal.

Regulatory fragmentation across municipalities creates compliance challenges

The 2024 International Building Code introduced sweeping revisions on energy storage and wind-borne debris, while local overlays differ in carbon-emission caps and accessibility provisions. Developers working across states face varying plan-check timelines, fee structures, and sustainability thresholds, complicating cost certainty. National Multifamily Housing Council research indicates that code variance can add double-digit percentage premiums to baseline construction budgets. Continuous updates require architects to track multiple amendment cycles, raising internal legal and documentation overheads. Digital-plan-review portals improve transparency, yet uneven adoption across jurisdictions sustains project-start risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Design services retain scale while planning accelerates

Design and Documentation held 40.92% revenue in 2025, underlining their place as the indispensable core of every capital project. This dominance safeguards predictable fee flows because regulatory submittals mandate sealed drawings and specifications. The architectural services market size for Urban Planning and Master-planning is predicted to grow at a 6.28% CAGR, driven by new-town developments in India and rail-corridor rejuvenations in the United States. Municipalities demand advanced scenario modeling that blends land-use analytics, mobility forecasts, and green-infrastructure overlays, encouraging firms to expand GIS and socio-economic research teams. Interior and Space Planning keeps steady volume as hybrid workplaces and data-center suites require reconfigurable layouts that support well-being standards. Restoration and Conservation, although niche, rises on incentives for embodied-carbon retention and cultural-tourism value. Across every service, AI-assisted parametric templates speed code-compliant detailing, with pilot studies showing 31% document-production savings by 2030.

Project-management add-ons grow as owners favor single-contract design-build packaging to reduce risk. Stantec’s 2025 acquisition of Page exemplifies how multidisciplinary scope wins market share in advanced manufacturing and healthcare, sectors that prize integrated design-construction oversight. Firms also integrate digital-twin maintenance dashboards, transforming one-off contracts into recurring facilities-support subscriptions.

By End User: Housing scale meets industrial momentum

Residential schemes yielded 34.21% of 2025 billings as national housing deficits persist, ranging between 1.5 million and 7.3 million units in the United States alone. Yet tighter lending terms, higher mortgage rates, and land scarcity in core metros push architects toward middle-income multifamily, senior living, and build-to-rent platforms that promise predictable occupancy. Conversely, industrial and manufacturing inquiries surge at 6.12% CAGR through 2031 on reshoring of semiconductor fabs, battery plants, and cloud-computing data centers. These programs demand clean-room design, thermal-load balancing, and resilience audits against power interruptions, placing premium fees on specialist consultants.

Office pipelines remain subdued following hybrid-work adoption; however, adaptive reuse of under-occupied towers into life-science labs or residential lofts unlocks new revenue. Healthcare and education remain counter-cyclical mainstays; demographic aging sustains clinic and long-term-care expansion, while universities modernize research wings to compete for grants. Public-sector infrastructure, funded by multiyear appropriations, offers stable volume in transit, courthouse, and water-treatment segments, especially for firms versed in Davis-Bacon wage and Buy-America sourcing rules.

By Project Type: New builds dominate but reuse gains speed

New construction still accounts for 53.98% of architectural services market share due to relentless urbanization and large-scale manufacturing investments. In Asia Pacific, metro-rail stations, mixed-use superblocks, and logistics parks demand ground-up solutions. However, adaptive reuse projects register the highest growth at 5.98% CAGR as city councils favor carbon-saving refurbishments over demolition. Tax credits and expedited entitlements for repositioning heritage warehouses or mid-century offices lower carrying costs for developers. Renovation and retrofit pipelines likewise strengthen because commercial landlords seek energy-performance upgrades that satisfy incoming leasing-disclosure rules in New York City and London.

Heritage restoration garners cultural and tourism funding, such as the regeneration of industrial waterfronts into arts precincts. Architects balance original fabric conservation against modern accessibility and mechanical-electrical-plumbing integration, often using laser scan-to-BIM workflows for precision. Lifecycle carbon accounting now regularly ranks beside cost and aesthetics in briefing documents, steering materials selection toward recycled steel and mass timber where codes allow.

By BIM Adoption Level: Basic modeling cedes ground to integrated environments

Level 1 BIM environments, characterized by 3D modeling with minimal data linking, represented 54.72% of the architectural services market size in 2025. Adoption remains high because software entry costs are modest and model exchanges occur via traditional PDF outputs. Nonetheless, Level 3+ integrated data environments grow at 6.29% CAGR as owners pursue digital twins for facility management. Cloud platforms consolidate structural, environmental, and asset-tag information, enabling predictive maintenance and energy optimization without manual draw-downs.

Level 2 collaboration gains moderate ground where public procurers insist on federated models shared among architects, engineers, and contractors. Implementation barriers persist, chiefly training budgets, process re-engineering, and contractual risk allocation. Non-BIM or 2D-CAD usage continues its slide as insurers, lenders, and regulators deem manually coordinated sets prone to conflict. Overall, the architectural services market benefits from layered software revenue and consulting add-ons linked to BIM maturity journeys.

Geography Analysis

North America sustained 39.14% of global billings in 2025, buoyed by USD 1.2 trillion in federal infrastructure allocations that translate into sustained design spending across highways, rail, and flood-control systems. Mandatory BIM on federal buildings, stringent energy codes, and voluntary WELL and LEED commitments encourage high-fee technical consulting. Nevertheless, the Architecture Billings Index fell to 45.6 in January 2025, showing softness in private commercial work as higher interest rates defer speculative office and retail starts. Mergers such as Stantec-Page shore up geographic coverage and deepen advanced manufacturing competencies to capture reshoring demand.

Asia Pacific delivers the fastest regional CAGR at 6.07% through 2031 on back of USD 1.7 trillion average annual infrastructure needs.Southeast Asian economies attract industrial plant designs due to competitive labor and export-zone incentives, while India’s smart-city program accelerates metro-station and affordable-housing tenders. Singapore’s 90% BIM penetration sets a regional benchmark, with governments in Malaysia and Indonesia launching similar mandates. In the Gulf, sovereign wealth-funded giga-projects spur modular high-rise adoption and data-center clusters, opening opportunities for mission-critical designers.

Europe posts steady gains under rigorous decarbonization policies. The European Union’s Renovation Wave strategy seeds pipeline certainty for deep-energy retrofits, while cultural preservation funding supports restoration specialists. Diverse code bases complicate cross-border delivery, yet pan-EU digital-twin research consortia promote standardization. South America and Africa remain smaller contributors but grow off low bases as urbanization and private-equity investment in logistics and renewable energy schemes widen design scope.

Competitive Landscape

Market concentration is moderate. The top 5 global firms account for roughly 22% of revenue, leaving room for regional champions and boutique specialists. Stantec’s USD 546.2 million acquisition of Page propels combined revenue above USD 1.3 billion and doubles its Texas footprint. Gensler leads with USD 1.83 billion, leveraging workplace strategy and data-center depth to defend share. Perkins&Will and HKS pursue healthcare innovation hubs and university laboratories, respectively, while bolstering AI-powered design teams.

Technology differentiation intensifies. Over 52% of construction professionals already deploy AI in project management, and leading firms embed custom language models into Revit and Rhino environments for automatic code checks. Digital-twin subscriptions secure multiyear engagements; clients pay monthly for asset performance dashboards, sensor calibration, and regulatory reporting. Private-equity capital continues to roll up mid-sized practices, exemplified by MG2’s merger with Colliers Engineering, driving economies of scale in back-office systems and software licensing.

Firms visualize whitespace in adaptive reuse, net-zero retrofits, and mass-timber commercial buildings. Client selection criteria now weigh cyber-security posture, favoring practices that certify to ISO 27001 and deploy secure common-data environments. Geographic diversification protects against local downturns; for example, North America-based firms open delivery hubs in Vietnam and the Philippines to cover time-zone gaps and lower production costs.

Architectural Services Industry Leaders

IBI Group Inc.

Aedas Ltd.

AECOM

HDR Architecture Inc.

Gensler Design and Planning Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stantec acquired Page for USD 546.2 million, advancing its rank to the second-largest U.S. architecture firm and expanding into advanced manufacturing and healthcare sectors.

- February 2025: Stantec posted record 2024 net revenue of USD 5.9 billion, lifted its dividend 7%, and guided 2025 revenue growth of 7%–10%.

- February 2025: MG2 Architecture merged with Colliers Engineering and Design, creating a 3,000-employee national platform spanning retail and hospitality design.

- January 2025: Gannett Fleming and TranSystems combined into a USD 1.3 billion transportation-focused design powerhouse.

Global Architectural Services Market Report Scope

The architectural services market study defines the revenues generated from services such as architectural advisory services, construction and project management services, engineering services, interior designing services, urban planning services, and other services deployed for various end users such as residential, education, healthcare, corporate, and other end users across the globe. The study includes qualitative coverage of the most adopted strategies and an analysis of the key base indicators in emerging markets.

The architectural services market is segmented by end user (residential, education, healthcare, corporate, and other end users) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the segments.

By Service Type

| Design and Documentation |

| Construction and Project Management |

| Interior and Space Planning |

| Urban Planning and Master-planning |

| Restoration and Conservation |

By End User

| Residential |

| Corporate / Commercial Offices |

| Retail and Hospitality |

| Healthcare |

| Educational and Cultural |

| Industrial and Manufacturing |

| Public Infrastructure and Government |

| Other End Users |

By Project Type

| New Construction |

| Renovation and Retrofit |

| Adaptive Re-use |

| Heritage Restoration |

By BIM Adoption Level

| Non-BIM / 2D-CAD |

| BIM Level 1 (3D Modelling) |

| BIM Level 2 (Collaboration) |

| BIM Level 3+ (Integrated Data Environment) |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Design and Documentation | ||

| Construction and Project Management | |||

| Interior and Space Planning | |||

| Urban Planning and Master-planning | |||

| Restoration and Conservation | |||

| By End User | Residential | ||

| Corporate / Commercial Offices | |||

| Retail and Hospitality | |||

| Healthcare | |||

| Educational and Cultural | |||

| Industrial and Manufacturing | |||

| Public Infrastructure and Government | |||

| Other End Users | |||

| By Project Type | New Construction | ||

| Renovation and Retrofit | |||

| Adaptive Re-use | |||

| Heritage Restoration | |||

| By BIM Adoption Level | Non-BIM / 2D-CAD | ||

| BIM Level 1 (3D Modelling) | |||

| BIM Level 2 (Collaboration) | |||

| BIM Level 3+ (Integrated Data Environment) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the valuation of the architectural services market in 2026?

The architectural services market size stands at USD 390.12 billion in 2026.

How fast is the architectural services market expected to grow?

Industry revenue is projected to rise at a 5.30% CAGR, reaching USD 505.03 billion by 2031.

Which region leads in architectural services revenue?

North America holds the highest 2025 share at 39.14%, supported by large federal infrastructure programs.

Which region is expanding the quickest?

Asia Pacific shows the fastest CAGR of 6.07% through 2031 due to massive infrastructure investments.

What service segment is growing most rapidly?

Urban Planning and Master-planning leads with a forecast 6.28% CAGR as cities launch smart-growth initiatives.

How are digital twins influencing future fees?

Subscription-based digital-twin services turn one-time design contracts into recurring revenue streams by providing ongoing building-performance analytics.

Page last updated on: