Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

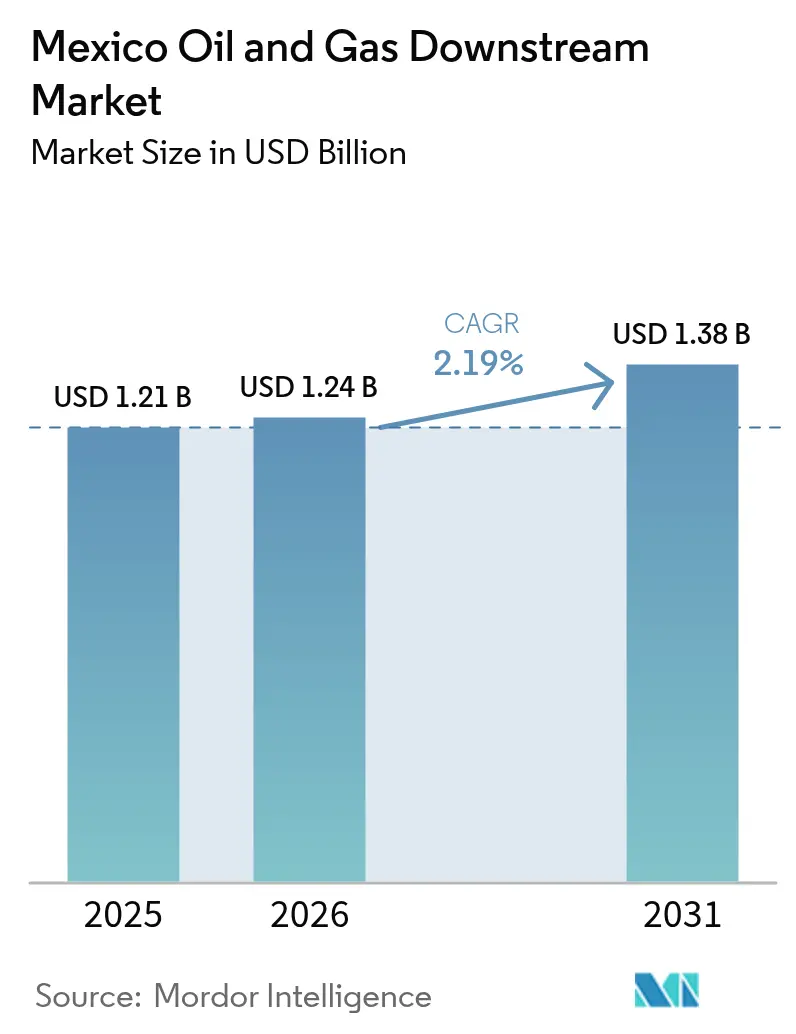

| Base Year Market Size (2025) | USD 1.21 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 2.19% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Oil And Gas Downstream Market Analysis by Mordor Intelligence

Mexico Oil And Gas Downstream Market size in 2026 is estimated at USD 1.24 billion, growing from 2025 value of USD 1.21 billion with 2031 projections showing USD 1.38 billion, growing at 2.19% CAGR over 2026-2031.

State‐backed refinery upgrades, the integration of Deer Park, and the phased start-up of Dos Bocas underpin the gradual expansion of the Mexico oil and gas downstream market, while chronic maintenance shortfalls curb utilization gains. Demand tailwinds stem from a larger vehicle fleet, near-shoring-driven petrochemical requirements, and growth in marine bunkering at Gulf and Pacific ports. Competitive intensity remains moderate because PEMEX retains operational control of pipelines, terminals, and retail pricing. Nonetheless, specialized storage and import terminals being built by private firms reveal niches where the Mexico oil and gas downstream market can still liberalize. The shift from autonomous regulators to a single National Energy Commission simplifies permitting but heightens policy risk for foreign investors.(1)Wilson Center Analysts, “President Sheinbaum Signs Secondary Laws,” Wilson Center, wilsoncenter.org

Key Report Takeaways

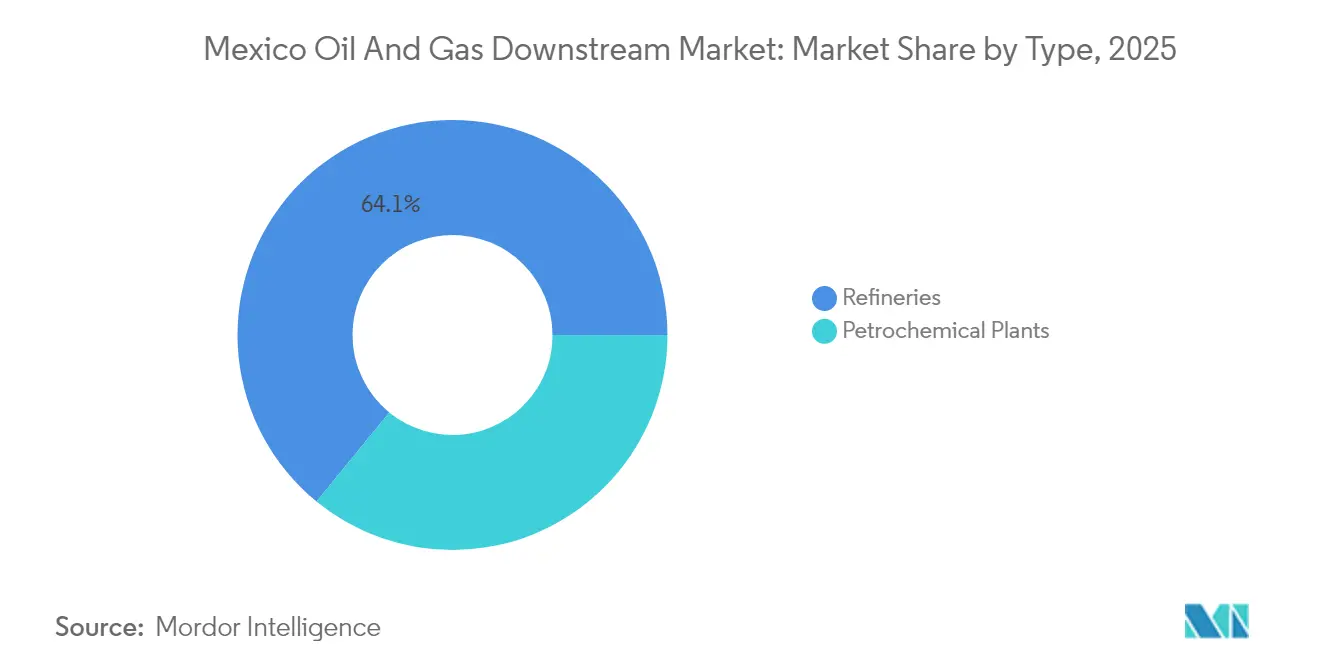

- By type, refineries led with 64.10% of the Mexico oil and gas downstream market share in 2025; petrochemical plants are projected to grow at a 4.03% CAGR to 2031.

- By product type, refined petroleum products accounted for 49.30% of the Mexican oil and gas downstream market size in 2025; petrochemicals are expected to advance at a 3.74% CAGR through 2031.

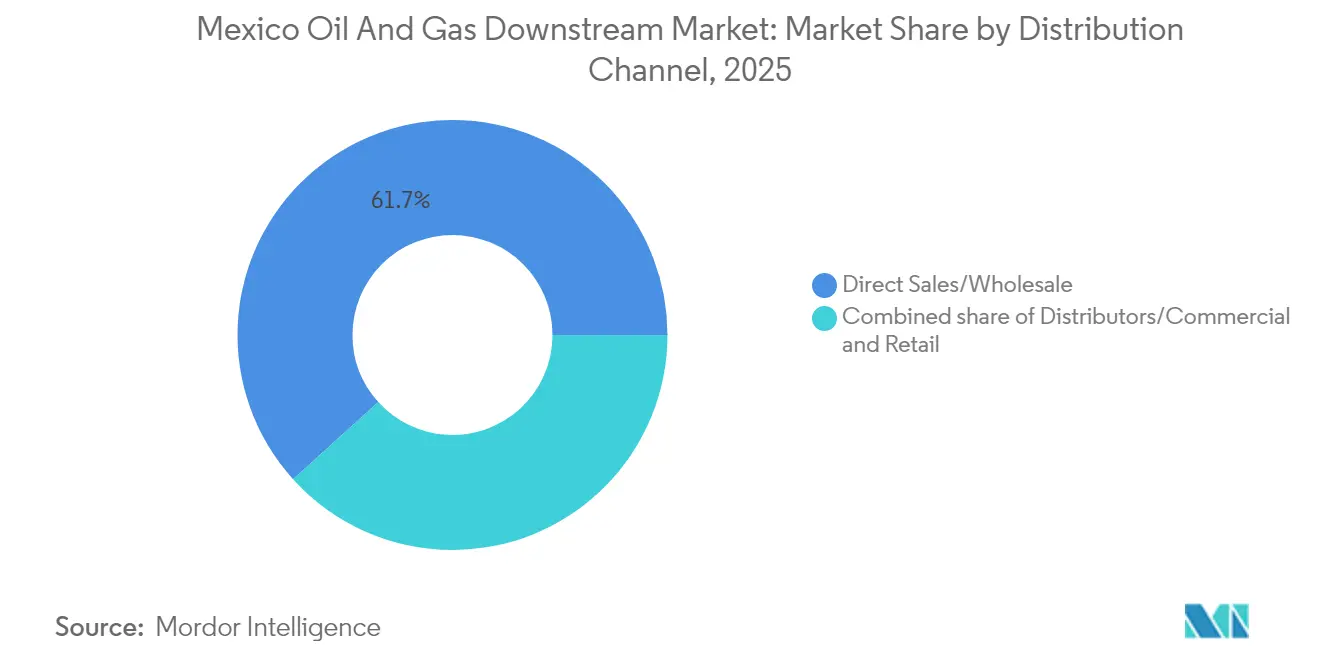

- By distribution channel, direct sales and wholesale held 61.70% of the Mexican oil and gas downstream market share in 2025, whereas distributors and commercial channels are expected to post the highest 4.41% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government refinery-upgrade program | +0.8% | Gulf Coast refineries | Medium term (2-4 years) |

| Rising gasoline & diesel consumption | +0.6% | Nationwide, stronger in northern border states | Long term (≥ 4 years) |

| Commissioning of Dos Bocas capacity | +0.4% | Gulf Coast | Short term (≤ 2 years) |

| Liberalized fuel-retail rules | +0.3% | Major urban centers | Medium term (2-4 years) |

| Near-shoring petrochemical demand | +0.7% | Northern clusters | Long term (≥ 4 years) |

| Marine bunkering surge | +0.2% | Gulf & Pacific ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government refinery-upgrade program bolstering utilization rates

Processing volumes across PEMEX’s six refineries climbed from 511 kb/d in 2018 to 1.23 MMb/d by early 2024 after successive rehabilitation outlays and Deer Park’s integration. The National Refining System is budgeted MX$136 billion through 2030 to replace critical units, debottleneck coking trains, and raise power reliability. While these efforts underpin the Mexican oil and gas downstream market, actual utilization still lingers below 60% because recurring maintenance backlogs outpace annual capital expenditure (capex) allocations. Dos Bocas reached only 115 kb/d throughput—34% of its design capacity—by May 2025, reflecting the absence of cogeneration and gas interconnects. The 2025-2035 roadmap now prioritizes debt reduction to unlock cash flow for turnarounds, a move expected to lift the Mexico oil and gas downstream market in the medium term.(2)Mexico Business News Staff, “The Year in Oil and Gas: A New Administration,” Mexico Business News, mexicobusiness.news

Commissioning of Dos Bocas refinery adding 340 kbd new capacity

Dos Bocas is the country’s largest downstream investment in decades, designed for 340,000 barrels per day of heavy-crude runs that could trim Mexico’s gasoline and diesel import dependence by 30%. Operational reality diverged from design: the plant reached only 115 kbd—34% of its nameplate capacity—by May 2025 because the cogeneration island and natural-gas interconnects were not yet finished. Its location in Tabasco provides direct access to Maya crude from Cantarell and Ku-Maloob-Zaap, reducing haulage costs compared to imported light blends. Even at reduced throughput, Dos Bocas has proven it can yield gasoline, diesel, and fuel oil that previously required costly imports. Once the cogeneration unit, sulfur-recovery trains, and tank-farm tie-ins are completed, the refinery is expected to increase national processing capacity beyond 1.5 MMb/d, thereby reinforcing the Mexican oil and gas downstream market. Continuous monitoring through SEMARNAT’s environmental framework ensures emissions control and wastewater handling, aligning with federal energy sovereignty goals.

Rising gasoline & diesel consumption from an expanding vehicle fleet

Mexico added nearly 900,000 light and heavy vehicles in 2024, maintaining nationwide sales resilience despite inflationary pressures. Northern border states post the fastest demand growth because cross-border logistics rely heavily on diesel, thereby elevating regional demand for the Mexican oil and gas downstream market. The federal government capped average retail prices at MX$23 per liter in 2025 and synchronized the IEPS tax adjustment at 4.5%, shielding demand from volatility. These measures stabilize margins for wholesale distributors while sustaining throughput requirements at refineries. Pipeline congestion and limited storage capacity, however, still hamper timely product flow to inland terminals.

Near-shoring-led petrochemical demand boom in northern clusters

Relocation of electronics, automotive, and packaging supply chains has attracted more than USD 20 billion of greenfield commitments into Tamaulipas, Nuevo León, and Coahuila. This surge prompts the addition of ethane and propane streams, encouraging joint ventures and the construction of import terminals that expand the Mexican oil and gas downstream market. Braskem Idesa’s ethane terminal and the Pacifico Mexinol complex—set to deliver 2.1 million t/y methanol using carbon-capture technology—represent flagship investments supported by IFC and multilaterals.(3)ChemAnalyst Editorial Team, “NextChem Secures Licensing Contract for Ultra-Low Carbon Methanol Plant in Mexico,” ChemAnalyst, chemanalyst.com Although feedstock tightness persists, PEMEX has signaled its willingness to formalize supply contracts, anchoring private confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Maintenance backlogs keeping utilization <60% | -0.5% | All six refineries | Short term (≤ 2 years) |

| Policy volatility deterring FDI | -0.4% | Nationwide | Medium term (2-4 years) |

| Decarbonization limits on fossil funding | -0.3% | ESG-sensitive regions | Long term (≥ 4 years) |

| High-sulfur fuel-oil surplus | -0.2% | Gulf Coast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic maintenance backlogs keeping utilization below 60%

Supplier arrears topping MX$430 billion have led key contractors to idle rigs and curtail works, a scenario that translates into fewer spare parts and delayed turnarounds across the Mexico oil and gas downstream market. The Cadereyta refinery is scheduled to face 2025 environmental hearings that could restrict throughput until emission controls are improved. Pemex secured a USD 10 billion liability management package but still requires additional funding to cover pipeline inspections, storage roof repairs, and delayed coker upgrades. The new “Oil Rights for Well-Being” fiscal scheme promises lighter royalty loads; however, the timing of its execution remains uncertain. Until full funding is secured, operational rates remain subdued.

Policy volatility and frequent contract reviews deterring FDI

The January 2025 secondary energy laws merged CRE and CNH into a National Energy Commission, centralizing approvals under SENER and boosting state oversight. Shell’s sale of more than 200 stations to Iconn underscores how abrupt rule changes are pushing established multinationals to scale back. Although mixed contracts remain possible, uncertainty surrounding import permits, storage concessions, and clean-fuel targets makes long-term capital expenditures unattractive. This restraint tempers external capital inflows that could otherwise expand the Mexico oil and gas downstream market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Refineries drive capacity while petrochemicals accelerate

Refineries accounted for 64.10% of Mexico's oil and gas downstream market in 2025, a dominance amplified by the Deer Park acquisition and the start-up of Dos Bocas. Despite the increase, refinery utilization lags behind design capacity because maintenance scheduling cannot keep pace with component failures. The Mexico oil and gas downstream market size attributed to refineries is expected to increase, as MXD 136 billion in federal funds is allocated to desulfurization, power generation, and dock expansion.

Petrochemical plants, in contrast, are expected to log a 4.03% CAGR to 2031, the fastest within the Mexican oil and gas downstream market. The Pacifico Mexinol project and Braskem Idesa's ethane terminal open additional capacity that meets near-shoring-driven demand, positioning northern clusters as major consumers. Sustained feedstock contracts and private-sector operational discipline underpin the petrochemical trajectory.

By Product Type: Refined products maintain leadership despite petrochemical momentum

Refined petroleum products accounted for 49.30% of Mexico's oil and gas downstream market in 2025, supported by price caps and import substitution drives that raised domestic throughput. The Mexico oil and gas downstream market size for refined products is projected to expand steadily as improved utilization lifts diesel and gasoline output.

Petrochemicals, although smaller today, are experiencing a 3.74% CAGR driven by near-shoring and low-carbon mandates that favor methanol, polyethylene, and specialty resins. Lubricants remain a niche but stable segment, feeding heavy-industry hubs in Monterrey and Saltillo.

By Distribution Channel: Wholesale dominance faces commercial-channel growth

Direct sales and wholesale operations accounted for 61.70% of the Mexican oil and gas downstream market in 2025, as PEMEX Logística utilized its pipeline and terminal network to supply government agencies and large distributors. The Mexico oil and gas downstream market share of wholesale channels may contract modestly as specialized distributors capture customers seeking flexible terms and conditions.

Distributors and commercial outlets will post a 4.41% CAGR through 2031, leveraging import terminals and private storage to offer blended grades, low-sulfur bunkers, and petrochemical feedstocks. Retail remains constrained by brand exits, yet domestic players, such as Oxxo Gas and Iconn, continue to expand their networks under local franchise models.

Geography Analysis

The Gulf Coast remains the operational backbone of the Mexico oil and gas downstream market, hosting five of six PEMEX refineries and the new Dos Bocas site. Crude proximity and dock infrastructure provide the region with scale advantages, although lingering maintenance gaps limit utilization. Northern border states form the fastest-growing demand corridor, fueled by USMCA trade flows and USD-pegged retail pricing that encourages diesel uptake for logistics fleets.

Central Mexico, anchored by Mexico City, Guadalajara, and Querétaro, consumes more than one-third of the nation's gasoline yet relies on long-haul pipelines and rail. IEnova's 650,000-barrel terminal, located outside the capital, reduces stock-out risk and increases flexibility for the Mexican oil and gas downstream market.

Pacific ports—Manzanillo, Topolobampo, and Lázaro Cárdenas—are emerging as bunkering and petrochemical export hubs. The Pacifico Mexinol complex utilizes Topolobampo's deepwater access to ship green and blue methanol to Asian customers, reflecting geographic diversification within the Mexican oil and gas downstream market.

Competitive Landscape

The Mexico oil and gas downstream market is moderately concentrated. PEMEX maintains ownership of refining, trunk pipelines, and key storage terminals, thereby gaining structural control over approximately 80% of the national throughput. Foreign firms continue to participate, but now favor joint ventures or service contracts over equity stakes, as illustrated by Transition Industries' partnership with NextChem and Veolia on the Pacifico Mexinol facility.

Private players are directing capital toward complementary assets—such as import terminals, ethane logistics, and digital fuel management systems—that do not directly challenge PEMEX's core refineries. IEnova and Monterra Energy focus on multi-product terminals that fill regional supply gaps. EPC specialists, such as Bonatti, secure infrastructure packages tied to government priorities, thereby avoiding the regulatory headwinds that confront retail and midstream newcomers.

Retail consolidation persists: Shell transferred its network to Iconn while BP and Repsol slowed site roll-outs, preferring branded fuel supply contracts over owned stations. Domestic operators Oxxo Gas and G500 pursue scale through franchising, but their broader impact on the Mexico oil and gas downstream market will depend on securing consistent supply from PEMEX or alternative importers.

Mexico Oil And Gas Downstream Industry Leaders

-

Petróleos Mexicanos

-

Braskem Idesa

-

IEnova (Sempra Infraestructura)

-

Valero Energy México

-

Shell México

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Transition Industries appointed Bonatti for port upgrades and methanol pipelines linked to Mexinol.

- August 2025: The federal budget allocated MXD136 billion to PEMEX’s 2025-2035 roadmap, focusing on debt reduction and the relaunch of petrochemicals.

- July 2025: Grupo México suspended four offshore rigs after PEMEX delayed payments exceeding MXD 430 billion.

- May 2025: Dos Bocas reached a throughput of 115 kb/d—34% of its nameplate capacity—owing to incomplete power and gas utilities.

- April 2025: CNH green-lit an extra USD 400 million for the Lakach deepwater gas project, raising total spend to USD 2.218 billion.

- March 2025: PEMEX reported 70 million liters of seized stolen fuel in eight months, surpassing the total of the prior administration’s six years.

Mexico Oil And Gas Downstream Market Report Scope

The downstream market refers to the activities undertaken post-production of crude oil and natural gas. It is the last step in the entire value chain of the oil and gas sector, which includes refining crude oil into consumable products and its marketing and distribution for end-users. The Mexico oil and gas downstream market is segmented by Type. By type, the market is segmented into Refineries and Petrochemicals Plants. The report also covers the market size and forecasts for the region. For each segment, the market sizing and forecasts have been done based on refining capacity (million barrels per day).

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

What is the projected value of the Mexico oil and gas downstream sector by 2031?

The market is expected to reach USD 1.38 billion by 2031, reflecting a 2.19% CAGR.

How much capacity did Dos Bocas achieve by mid-2025?

The refinery operated at 115 kb/d, equivalent to 34% of its 340 kb/d design.

Which segment grows fastest within the downstream chain?

Petrochemical plants post the quickest growth at a 4.03% CAGR through 2031.

Why are private distributors investing in storage terminals?

They aim to secure flexible supply and capture a 4.41% CAGR opportunity as commercial channels expand.

How does the new National Energy Commission affect investors?

Centralized rule-making speeds up permits but raises policy risk, moderating foreign capital inflows.

Page last updated on: