Automotive 3D Printing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

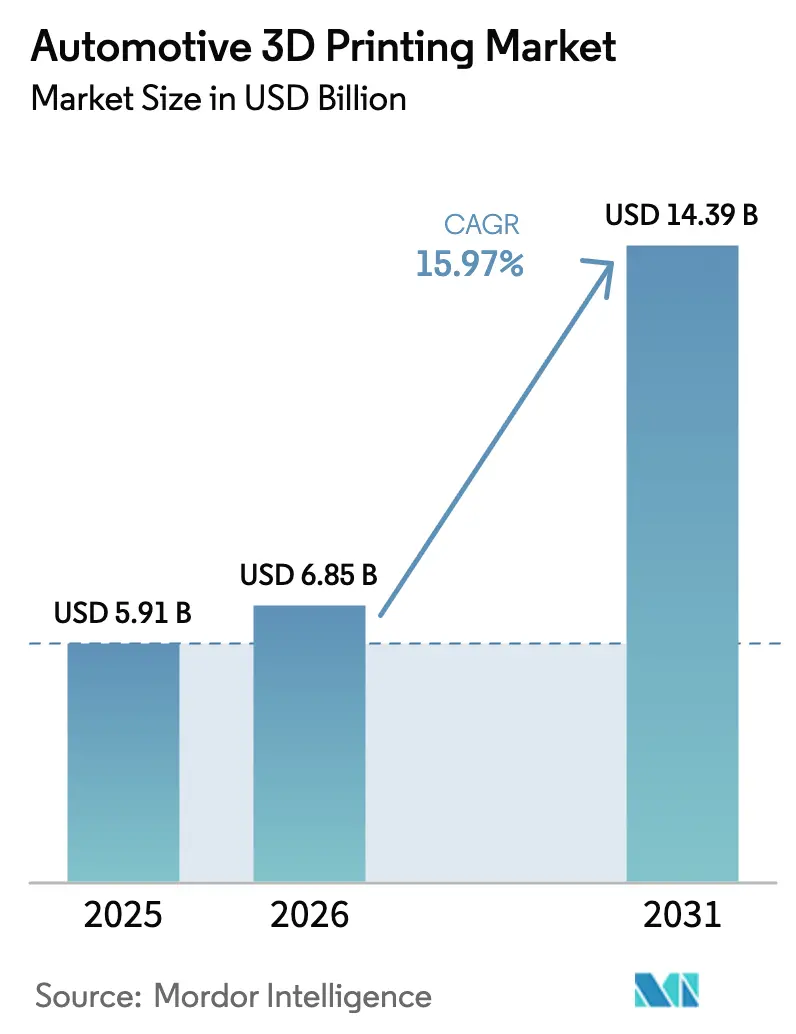

| Market Size (2026) | USD 6.85 Billion |

| Market Size (2031) | USD 14.39 Billion |

| Growth Rate (2026 - 2031) | 15.97% CAGR |

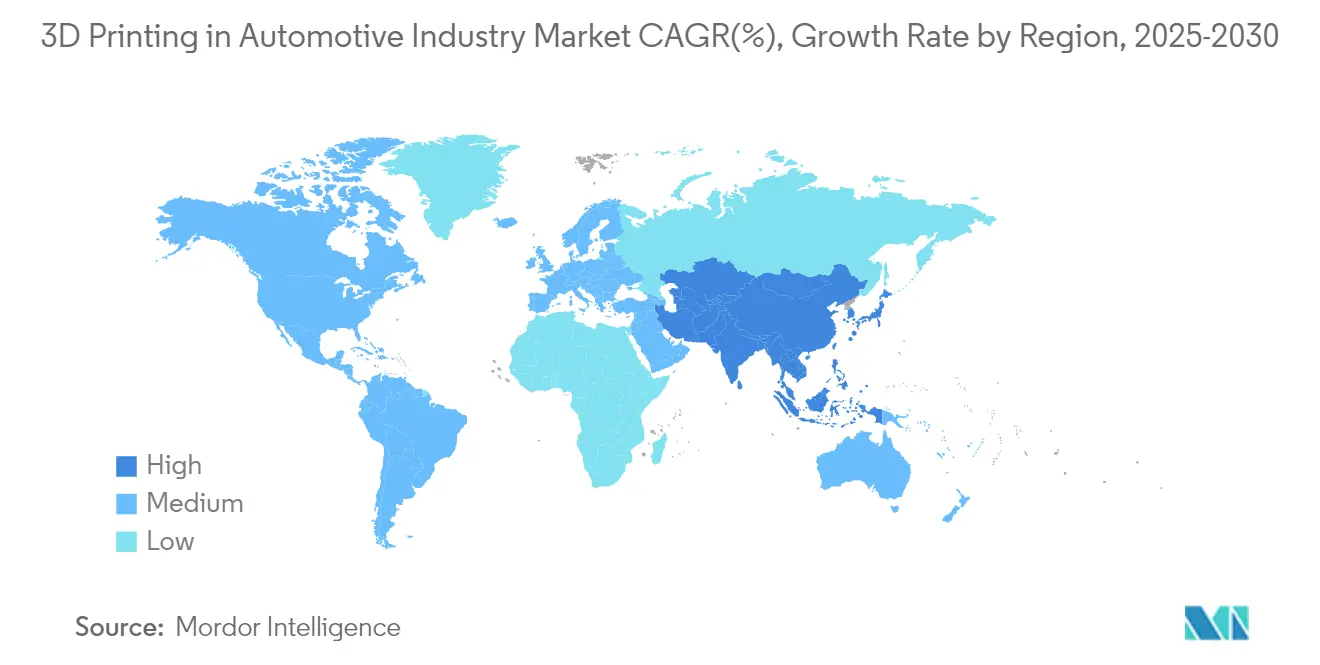

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

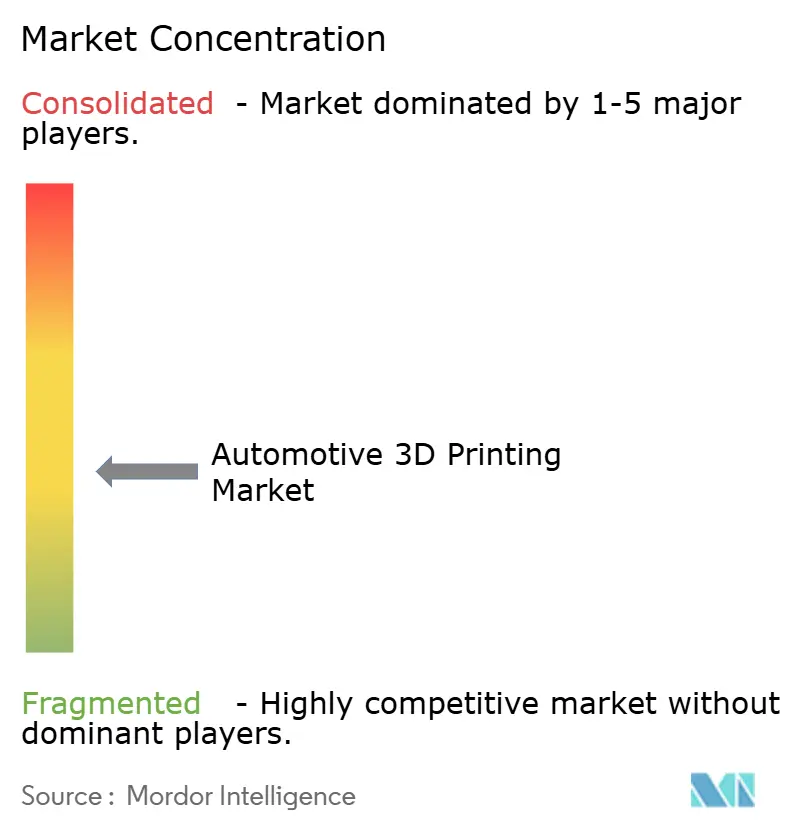

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive 3D Printing Market Analysis by Mordor Intelligence

The Automotive 3D printing market size was valued at USD 5.91 billion in 2025 and estimated to grow from USD 6.85 billion in 2026 to reach USD 14.39 billion by 2031, at a CAGR of 15.97% during the forecast period (2026-2031). The shift from prototyping toward full-scale production is accelerating as breakthroughs in multi-material processing, digital supply-chain orchestration, and artificial-intelligence-driven quality control redefine manufacturing economics. Demand for lightweight components that meet stringent emissions rules, illustrated by BMW’s 27% emissions reduction using wire-arc additive manufacturing, underpins growth[1]“Wire-Arc Additive Manufacturing Cuts Emissions,”, BMW Group Press Office, bmwgroup.com. Hardware advances in fused deposition modeling (FDM) and selective laser sintering (SLS) improve throughput, while cost-effective iron–silicon powders open metal applications for electric-vehicle (EV) motor parts. Regulatory pressure, on-shoring strategies, and the availability of sustainable feedstocks align to expand the Automotive 3D printing market across established and emerging economies.

Key Report Takeaways

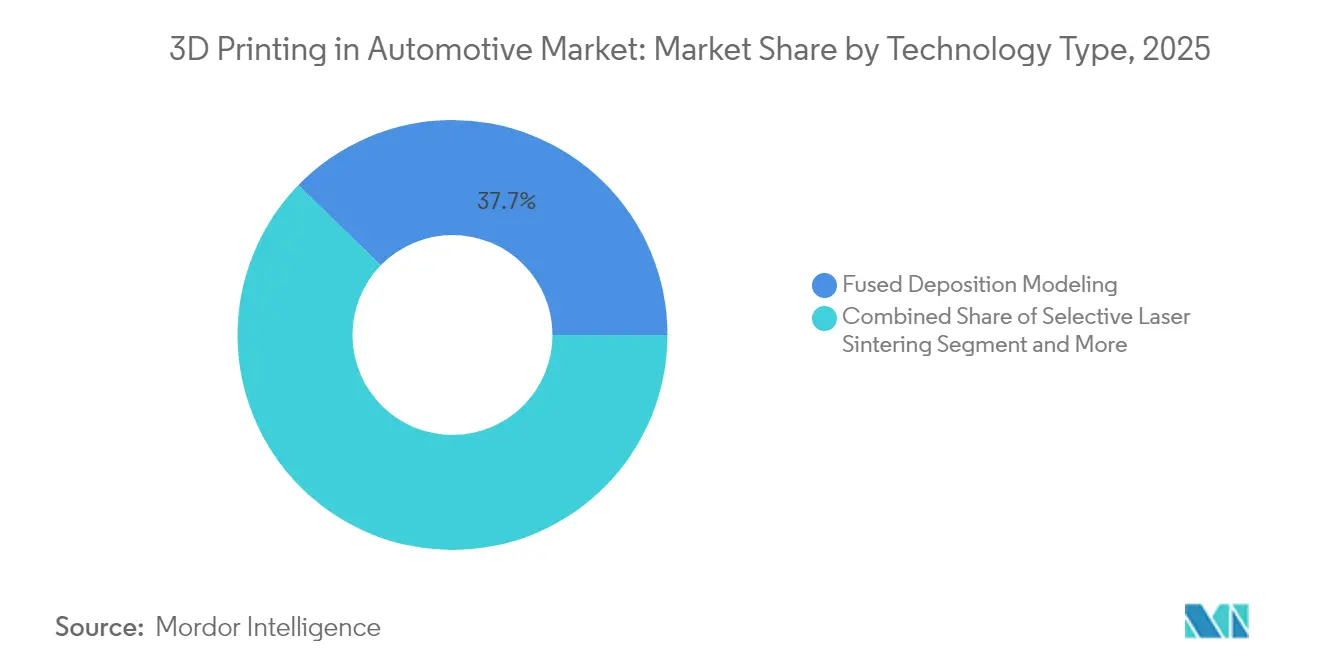

- By technology, FDM commanded 37.74% of the Automotive 3D printing market share in 2025, SLS is poised to grow fastest at an 18.02% CAGR to 2031.

- By component, hardware led with 56.61% revenue share in 2025, while software is forecast to expand at 18.21% CAGR through 2031.

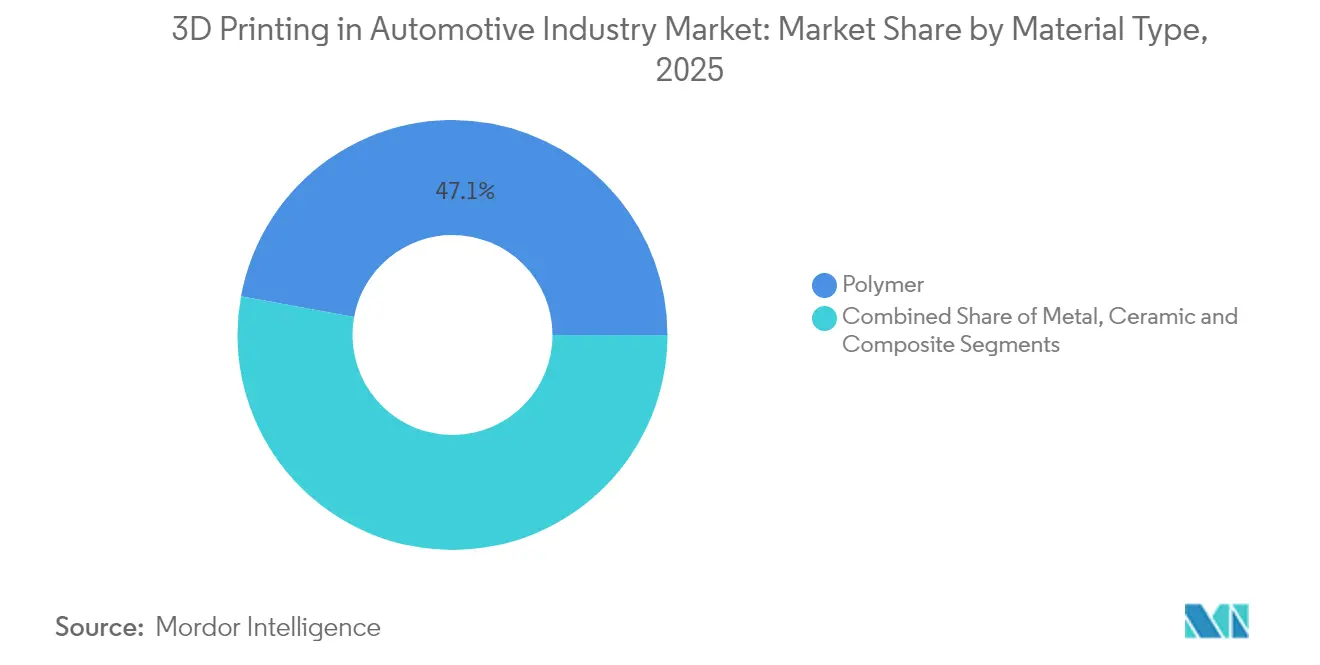

- By material, polymers held a 47.12% share of the Automotive 3D printing market in 2025, metal printing is projected to grow at a 19.05% CAGR between 2026 and 2031.

- By application, production parts are advancing at 25.11% CAGR through 2031, outpacing prototyping’s 43.12% revenue share in 2025.

- By geography, North America accounted for 38.02% of the Automotive 3D printing market share in 2025, whereas Asia-Pacific is the fastest-growing region at a 18.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive 3D Printing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Lightweight Parts Demand | +3.2% | Global, focused in North America & Europe | Medium term (2-4 years) |

| Rapid Prototyping Cost-Cuts | +2.8% | Global, strongest in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Custom Production Tooling | +2.5% | North America & EU industrial corridors | Medium term (2-4 years) |

| Digital Spare-Parts Inventory | +2.1% | Global, early in aerospace & automotive | Long term (≥ 4 years) |

| Multi-Material AM Integration | +1.9% | Advanced manufacturing regions worldwide | Long term (≥ 4 years) |

| Supply-Chain on-Shoring Push | +1.7% | North America & EU, ripple into Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV Lightweight-Parts Demand

Electric vehicle makers pursue weight optimization to extend their range and comply with emissions standards. General Motors integrates more than 130 printed parts in the Cadillac Celestiq, including the largest additively manufactured aluminum component in automotive production[2]Scott Wolff, “Iron–Silicon Powders for EV Motors,” Assembly Magazine, assemblymag.com. Europe’s Euro 7 norms accelerate adoption for brake-disc coatings and structural elements. Sand-based 3D printing shortens mold-development cycles, enabling casting designs that reduce mass while preserving tolerance targets. The need to offset battery weight intensifies competitive incentives to remove every gram across vehicle platforms.

Rapid Prototyping Cost-Cuts

Enterprises report up to 90% reductions in prototype lead times and sharp declines in single-part costs as additive manufacturing replaces machining for early-stage design iterations. Stereolithography’s high dimensional accuracy supports low-cost investment casting alternatives, while AI-based build-parameter optimization elevates first-time-right success rates. Desktop SLS printers priced below USD 3,000 broaden access for small and midsize suppliers, compressing innovation cycles across Asia-Pacific manufacturing clusters.

Custom Production Tooling

BMW leverages wire-arc additive manufacturing for bespoke tooling that cuts material waste by 70% and accommodates conformal-cooling channels otherwise impossible with subtractive techniques. Rocket-engine nozzle programs illustrate multi-material builds where thermal and structural properties are co-optimized within one part. The ability to produce jigs, fixtures, and dies on demand slashes inventory costs and supports sustainability objectives through metal-powder recyclability. These capabilities lift the Automotive 3D printing market CAGR by another 2.5 percentage points.

Digital Spare-Parts Inventory

Manufacturers deploying cloud-linked digital inventories have cut engineering-monitoring time by 98% and scrap by 18% through automated workflows that trigger printing only when sensors flag component wear[3]“Oqton Deployment at Baker Hughes,” 3D Systems Application Note, 3dsystems.com. During the COVID-19 crisis, on-demand production mitigated supply-chain breakdowns, underscoring additive’s resilience benefits. As companies migrate from reactive to predictive maintenance, additive printing lowers the total cost of ownership for legacy fleets.

Restraints Impact Analysis of Automotive 3D Printing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Metal Printers | -2.4% | Global, greatest in emerging markets | Short term (≤ 2 years) |

| Material-Qualification Gaps | -1.8% | Regulated sectors worldwide, notably aerospace & medical | Medium term (2-4 years) |

| Energy-Intensive Laser Systems | -1.5% | Regions with high energy tariffs | Medium term (2-4 years) |

| IP-Security Concerns | -1.2% | Defense and aerospace verticals globally | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

High Cost of Metal Printers

Industrial SLS printers list between USD 12,000 and USD 33,000, while specialty metal powders average USD 300–600 per kg, limiting adoption among cost-sensitive suppliers. Helium-atomized powder production offers the most sustainable route, yet capital outlays remain steep. Lifecycle analyses show powder-bed fusion is economical for high-complexity components, but up-front capital still deters wide deployment. Lower-cost metal-filament processes mitigate entry barriers but add post-processing complexity, reducing the Automotive 3D printing market CAGR by 2.4 percentage points

Material-Qualification Gaps

Safety-critical industries require certified datasets for additive-specific alloys, which takes 3–5 years per material. Incomplete mechanical-property databases delay design approval, especially in aerospace, medical, and automotive applications. Academic consortia and standards bodies are accelerating test-protocol harmonization, yet the qualification backlog dampens adoption by 1.8 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive 3D Printing Market Segment Analysis

By Technology Type:

FDM Dominance Challenged by SLS InnovationFDM accounted for 37.74% of the Automotive 3D printing market share in 2025, owing to low system costs and broad material selection. SLS is projected to grow at an 18.02% CAGR through 2031 as desktop powder-bed systems below USD 3,000 democratize high-performance nylon and composite printing. Advances in nanoscale photopolymerization have pushed stereolithography resolution to 100 nm at 100 µm per second, extending its use into microfluidic and optics applications. Digital Light Processing (DLP) increasingly supports jewelry and dental models, while electron-beam melting serves aerospace titanium parts. The Automotive 3D printing market size for SLS-based parts is forecast to expand sharply as EV manufacturers adopt durable nylon gears and under-hood components.

Hybrid manufacturing that blends additive and subtractive techniques is gaining ground. FDM toolpaths integrate continuous-fiber reinforcement, improving tensile strength without secondary operations. Holographic volumetric printing demonstrates up-to-20-fold speed gains by curing entire layers simultaneously, holding promise for high-volume automotive interiors. Continual improvements in process simulation software reduce trial iterations, ensuring FDM retains relevance even as the SLS installed base rises.

By Component Type:

Software Growth Outpaces Hardware ExpansionHardware captured 56.61% of 2025 revenue, encompassing printers, post-processing stations, and scanners. However, software is expanding at 18.21% CAGR as machine-learning algorithms cut defect rates and orchestrate multi-factory fleets. Manufacturing operations platforms deployed at Baker Hughes trimmed monitoring time by 98% and scrap by 18%. Service bureaus flourish when automakers outsource specialty materials or small production runs that do not justify capital spending.

AI-driven build-parameter engines reduce engineering labor by 80%, contributing to a rising software share within the Automotive 3D printing market. Browser-based collaboration suites allow design iterations across continents, enabling simultaneous engineering and rapid release to production. As cloud connectivity scales, subscription revenue offers vendors a high-margin annuity, shifting the competitive balance from machines to digital ecosystems

By Material Type:

Metal Printing Accelerates Despite Polymer LeadershipPolymers maintained a 47.12% share of total revenue in 2025, supported by biocompatible resins and high-temperature composites for under-hood applications. Nonetheless, metal printing is growing at 19.05% CAGR to 2031, propelled by iron–silicon powder for EV motors and aluminum-scandium alloys for structural parts. The Automotive 3D printing market size for metal components is projected to exceed USD 4 billion by the end of the decade.

Powder reuse rates surpass 85% in selective-laser-melting processes, reducing material overhead and environmental impact. Ceramic formulations address thermal-barrier requirements for turbocharger housings, while carbon-fiber-reinforced composites decrease vehicle mass without exotic metals. Sustained R&D into recycled polymers and bio-based feedstocks aligns additive manufacturing with circular-economy objectives.

By Application Type:

Production Surge Transforms Industry DynamicsPrototyping commanded 43.12% revenue in 2025, yet production parts are growing fastest at 25.11% CAGR as design-for-additive principles mature. The Automotive 3D printing market size for series parts is expected to match prototyping by 2028. Tooling and fixtures benefit from conformal cooling, achieving 30% cycle-time reductions. GE Aerospace’s USD 1 billion commitment to domestic additive capacity underscores the shift to end-use production.

Medical-grade PEEK cranial implants, cleared by the FDA, exemplify high-value patient-specific components produced on industrial printers. Automotive OEMs now integrate additively manufactured brackets, ducts, and interior trims directly into assembly lines, reducing part counts and accelerating vehicle personalization. As certification barriers diminish, spare-parts printing will reshape after-sales supply chains for legacy models.

Geography Analysis

North America Automotive 3D Printing Market

North America leads the Automotive 3D printing market with a 38.02% share in 2025, supported by the United States’ dominant aerospace and EV supply chains. GE Aerospace’s USD 1 billion investment in additive facilities signals long-term confidence in domestic productio. Reshoring initiatives combined with the Inflation Reduction Act incentivize localized manufacturing, accelerating printer installations across automotive tiers. Canada and Mexico contribute through lightweight truck components and aerospace casting molds, leveraging cross-border trade frameworks.

APAC Automotive 3D Printing Market

Asia-Pacific is the fastest-growing region at a 18.96% CAGR through 2031, propelled by China’s manufacturing digitalization and India’s emerging bioprinting startups. Chinese five-year plans earmark additive manufacturing as a strategic pillar, spurring installation growth across automotive hubs and battery factories. India’s collaboration between EOS and Godrej accelerates aerospace applications, while public-private R&D centers foster skill development. Japan and South Korea push materials innovation, developing heat-resistant polymers tailored to hybrid-electric powertrains. Southeast Asian electronics clusters adopt 3D printing for tooling, aided by government tax incentives.

Europe, South America and Middle East Automotive 3D Printing Market

Europe holds a significant share, anchored by Germany where majority of manufacturers deploy additive processes. The region invests 30.6% of AM company turnover back into R&D, reinforcing leadership in metal-printer exports. France and Italy expand composite printing for supercars, while Scandinavia explores bio-based polymers for vehicle interiors. Regulatory alignment through ISO/ASTM standards supports cross-border qualification of printed parts, smoothing supply-chain flows. Emerging regions in South America and the Middle East pursue diversification; Saudi Arabia outfits SMEs with entry-level printers to decrease energy consumption in metal fabrication. Brazil pilots additive repair hubs for agricultural machinery, demonstrating the technology’s reach beyond high-income economies.

Regulatory Landscape

Automotive additive manufacturing is governed less by a single automotive-specific rulebook and more by a growing body of AM qualification, process-control, and machine-performance standards used in supplier audits and part approval. ISO/ASTM 52920:2023 establishes a common approach for manufacturing series and replacement parts with defined process-control criteria, while ISO/ASTM 52945:2023 defines methodologies and KPIs for evaluating laser powder bed fusion (PBF-LB/M) machine performance. Together, these standards support reproducibility requirements as AM moves from prototyping to production.

Policy attention is also shifting toward supply-chain sovereignty and digital compliance. In January 2026, U.S. Department of Defense provisions in the National Defense Authorization Act (NDAA) tightened restrictions on acquiring additive manufacturing equipment connected to covered nations, increasing equipment provenance and sourcing due diligence for AM platforms used across industrial ecosystems. In April 2026, ANSI's Additive Manufacturing Standardization Collaborative (AMSC) issued a progress update tracking work against dozens of standardization gaps, reinforcing continued progress toward clearer qualification and certification frameworks that affect automotive supplier readiness and cross-border part acceptance.

Value Chain Analysis

The automotive 3D printing value chain starts with hardware OEMs and platform providers (polymer and metal systems, post-processing, metrology) and extends through materials suppliers (polymers, metal powders, composites) and software layers that manage build preparation, traceability, and production workflows. Automotive OEMs and Tier suppliers increasingly operationalize AM through integrated toolchains rather than standalone printers, as illustrated by the January 2025 collaboration among 3D Systems, Daimler Truck, Daimler Buses, Oqton, and Wibu-Systems to enable remote spare-part printing with software-driven workflow control and digital rights management.

Downstream, service bureaus and certified print networks support low-volume production, tooling, and aftermarket spares, while distributed production reduces logistics and inventory exposure. Capability build-out at OEM and Tier sites is also becoming part of the chain: in April 2026, Toyota Kirloskar Motor and Wipro 3D signed an MoU to establish an additive manufacturing Centre of Excellence at the Toyota Technical Training Institute (Bidadi) focused on production aids and on-demand spare parts. At the high end of metal applications, Nikon SLM Solutions and Bosch Industry Consulting demonstrated large-format LPBF viability by printing a complete V8 engine block as a single piece (AlSi10Mg) on the NXG XII 600, highlighting how multi-laser platforms, parameter IP, and qualification know-how are becoming critical value-capture points alongside machines and powders.

Competitive Landscape

The Automotive 3D printing market displays moderate fragmentation. Top players collectively control significant chunk, yet consolidation is accelerating. Stratasys reinforced its balance sheet via a USD 120 million equity infusion from Fortissimo Capital to finance acquisitions and polymer-system R&D. Nano Dimension spent USD 179.3 million buying Desktop Metal and USD 116 million acquiring Markforged, forming a USD 200 million-revenue group with polymer, metal, and electronics capabilities. The combined entity rationalizes overlapping portfolios to capture in software and powder production.

Software differentiation is an intensifying battleground. 3D Systems’ Oqton platform secured large industrial wins after delivering 98% monitoring-time cuts at Baker Hughes. EOS integrates AI into its printer fleet, reducing parameter setup iterations by 80%. HP partners with Materialise to embed proprietary datasets into cloud toolchains, fostering closed-loop process control.

Niche disruptors target desktop SLS and resin systems. Formlabs’ acquisition of Micronics accelerates sub-USD 10,000 powder-bed units, extending the Automotive 3D printing market into design studios and service garages. Hybrid machine builders combine additive and five-axis milling to achieve surface finishes rivaling CNC at reduced cycle times. Patent filings concentrate on multi-material printheads and AI-generated lattice geometries, positioning innovators to license core technologies to automotive OEMs seeking mass-production scale.

Automotive 3D Printing Industry Leaders

Stratasys Ltd

3D Systems Corporation

EOS GmbH

HP Inc.

Materialise NV

- *Disclaimer: Major Players sorted in no particular order

Automotive 3D Printing Market Companies Covered in this Report

- Stratasys Ltd

- 3D Systems Corporation

- EOS GmbH

- HP Inc.

- Materialise NV

- GE Additive (Arcam AB)

- Desktop Metal (ExOne)

- Ultimaker BV

- Voxeljet AG

- Carbon Inc.

- Hoganos AB

- EnvisionTEC GmbH

- SLM Solutions Group AG

- Renishaw plc

- BASF Forward AM

- Markforged Inc.

- Sindoh Co. Ltd

- XYZprinting Inc.

- Moog Inc.

Market Opportunities and Future Outlook

Opportunities are expanding where additive shifts from prototype-only use to validated production and operational uptime use cases. Distributed, rights-managed spare-parts printing is one clear whitespace for automotive and commercial vehicles, supported by the January 2025 3D Systems, Daimler Truck, Daimler Buses, Oqton, and Wibu-Systems initiative to enable remote printing with IP protection. This direction targets faster part availability and lower inventory dependence. Factory-floor software and digital workflow orchestration also create room for scale deployments as fleets of printers move into manufacturing operations rather than staying within engineering labs.

Metal additive manufacturing for complex, consolidated parts is another active avenue, reinforced by supplier investments and demonstrators. Brose expanded metal AM capacity in March 2026 via a new laser beam powder bed fusion system (with Farsoon Technologies) aimed at increasing series-production output for complex metal components. In July 2026, Nikon SLM Solutions and Bosch Industry Consulting printed a complete V8 engine block as a single piece in AlSi10Mg on an NXG XII 600 system, underscoring the direction toward substituting casting tooling for highly complex architectures. In parallel, BMW Group has reported broad integration of 3D-printed components across its vehicle brands and has highlighted industrialization of wire-arc additive manufacturing for larger-format parts, pointing to continued opportunity in large tooling, production aids, and lightweight structures that connect emissions and circularity priorities with qualified materials and repeatable process control.

Recent Industry Developments in Automotive 3D Printing Market

- May 2026: The Cadillac Formula 1 Team deployed seven 3D Systems SLA printing systems to support wind-tunnel testing and production parts development for its 2026 Formula 1 debut. The deployment anchors high-throughput polymer additive manufacturing in a time-critical motorsport pipeline, increasing the need for repeatable materials, process control, and rapid iteration across aerodynamic and thermal management components.

- June 2025: General Motors confirmed that the Cadillac Celestiq will enter limited-series production with more than 130 additively manufactured parts, including the industry's largest 3D-printed aluminum structural component. The program moves additive manufacturing into production-intent applications and indicates stronger pull-through for qualified metal processes and automotive-grade quality assurance.

- March 2024: HP released HP 3D HR PA 12 S, a nylon material with an 85% reuse rate engineered for durable, lightweight car-interior parts. Higher powder reusability and performance stability support cost control and sustainability targets, helping accelerate qualification cycles for polymer series parts and tooling within automotive plants.

Automotive 3D Printing Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the automotive 3D printing market is defined as revenue generated from additive manufacturing used for automotive part design, prototyping, tooling, and production, including industrial equipment, qualified materials, software, and related services when tied to automotive use.

Scope exclusions: We exclude consumer or hobby-grade desktop printers and any material sales that cannot be reasonably linked back to automotive applications.

Segments Covered in This Report

- By Technology Type

- Selective Laser Sintering (SLS)

- Stereolithography (SLA)

- Digital Light Processing (DLP)

- Electron Beam Melting (EBM)

- Selective Laser Melting (SLM)

- Fused Deposition Modeling (FDM)

- By Component Type

- Hardware

- Software

- Service

- By Material Type

- Metal

- Polymer

- Ceramic

- Composite

- By Application Type

- Production

- Prototyping

- Tooling and Fixtures

- Spare-Parts / MRO

- Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping the automotive additive manufacturing value chain and identifying demand signals that can be checked outside interviews. We relied on public sources such as vehicle production statistics from agencies like OICA, trade and tariff line data from UN Comtrade, and safety and standards references from bodies such as ISO and SAE, because these help indicate where 3D printed parts can be adopted in automotive programs.

To ground assumptions, we reviewed patent databases for filing trends around additive manufacturing in vehicle components, along with peer-reviewed journals on material qualification and part performance. Company filings, investor presentations, and reputable press releases were used to track product launches and capacity additions. In a few cases, we used paid subscriptions for company financials, and separate paid access for news and financials, to cross-check revenue exposure and corporate activity. These are illustrative examples, and we also referenced other public and paid sources for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews focused on verifying what share of additive manufacturing spend is actually automotive-led, and where it is concentrated across printer and material stakeholders, prototype shops, tooling suppliers, and production programs. We conducted discussions with automotive manufacturing teams, service bureaus, and printer or material providers across APAC, EMEA, and the Americas, then used follow-up checks to confirm utilization levels, qualification timelines, and realistic pricing progression assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 27% | EMEA: 30% |

| Smaller Players: 17% | Managers: 58% | Americas: 26% |

Market-Sizing & Forecasting

Our sizing uses a top-down approach tied to automotive manufacturing activity and additive adoption signals. We start from vehicle build volumes and platform launches, then translate the addressable opportunities into additive printing needs across prototyping, tooling, and production parts. That demand pool is priced using unit-economics drivers, such as machine utilization, qualified material consumption rates, and the service share for outsourced builds, which we adjust based on application maturity.

To keep totals realistic, we run selective bottom-up checks, including roll-ups of revenue from a sampled set of suppliers, channel checks on service bureau throughput, and simple ASP-to-volume math for major process families. When a data point is missing, for example when service revenue is bundled, we fill the gap using peer ratios from interviews, then stress-test the outcome against what automotive programs can absorb in a given year.

Forecasts are built using scenario analysis supported by variable-level inputs from primary discussions. The largest drivers include vehicle production outlook by region, adoption of additive tooling versus conventional tooling, the shift toward metal printing for high-value components, material qualification lead times, and the pace of printer fleet additions at automotive-focused sites. Where adoption is lumpy, we apply short-term smoothing, then narrow the scenario ranges after re-checking with respondents.

Data Validation & Update Cycle

Validation is done through multiple passes that compare model outputs with independent signals, including automotive production trends, visible capacity expansion, and the relative split between prototyping and production use cases. When a variance shows up, we reopen the relevant assumption and verify it through targeted re-contacts and additional desk checks.

Before sign-off, the work is reviewed across analysts to keep the scope boundaries, conversion logic, and regional splits consistent and traceable. Reports are refreshed annually, with interim updates when material events occur, such as major regulatory shifts or step-changes in printer installations. Right before delivery, we complete a final refresh pass to ensure clients receive the latest updated view.

Mordor Intelligence's Automotive 3d Printing Market Sizing Compared With Other Published Estimates

Published market sizes for automotive 3D printing often differ because the market boundary is not treated the same way across sources, and build-up variables are not always aligned with how automotive programs purchase. Variances also come from the chosen anchor year, how services are counted, and whether revenue is limited to automotive-only use or includes spillover from general industrial additive.

By tracking automotive-linked equipment, qualified material usage, and service throughput checks, Mordor Intelligence keeps the total anchored to use cases that can be tied to vehicle programs, rather than counting all additive revenue that sits near the automotive supply chain.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.91 B (2025) | |

| Global Research Publisher A | USD 4.11 B (2025) | Uses a broader offerings structure and a faster adoption ramp that appears to count a larger share of general industrial service revenue as automotive, and it also anchors the series on a different base year with different currency timing assumptions. |

| Industry Research Publisher B | USD 5.95 B (2024) | Anchors on a 2024 base and extends the forecast horizon, and it blends motorcycles with automotive in some cuts, which shifts the demand pool and can change the implied split between prototyping, tooling, and production parts. |

The comparison shows that the spread is mostly explained by scope boundaries and how service and material revenue is attributed to automotive end use. When the demand pool is built from vehicle-program activity and then cross-checked with practical utilization and pricing inputs, the resulting number is easier to trace and repeat across updates.

Key Questions Answered in the Report

What is the current size of the Automotive 3D printing market?

The market is valued at USD 6.85 billion in 2026 and is projected to grow to USD 14.39 billion by 2031 at a 15.97% CAGR.

Which technology leads the Automotive 3D printing market?

Fused Deposition Modeling leads with a 37.74% market share in 2025, though Selective Laser Sintering is growing fastest at 18.02% CAGR.

How are software platforms shaping the Automotive 3D printing industry?

AI-enabled manufacturing-operations software can cut monitoring time by 98% and scrap by 18%, making software the fastest-growing component segment at 18.21% CAGR.

What restraints limit wider adoption of metal 3D printing in automotive applications?

High printer and powder costs, lengthy material-qualification cycles, and energy-intensive laser systems collectively reduce forecast CAGR.

Which companies are driving consolidation in the Automotive 3D printing market?

Nano Dimension, Stratasys, GE Aerospace, and Formlabs are leading acquisitions and strategic investments that reshape competitive dynamics.

Page last updated on: