North America Agricultural Drones Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

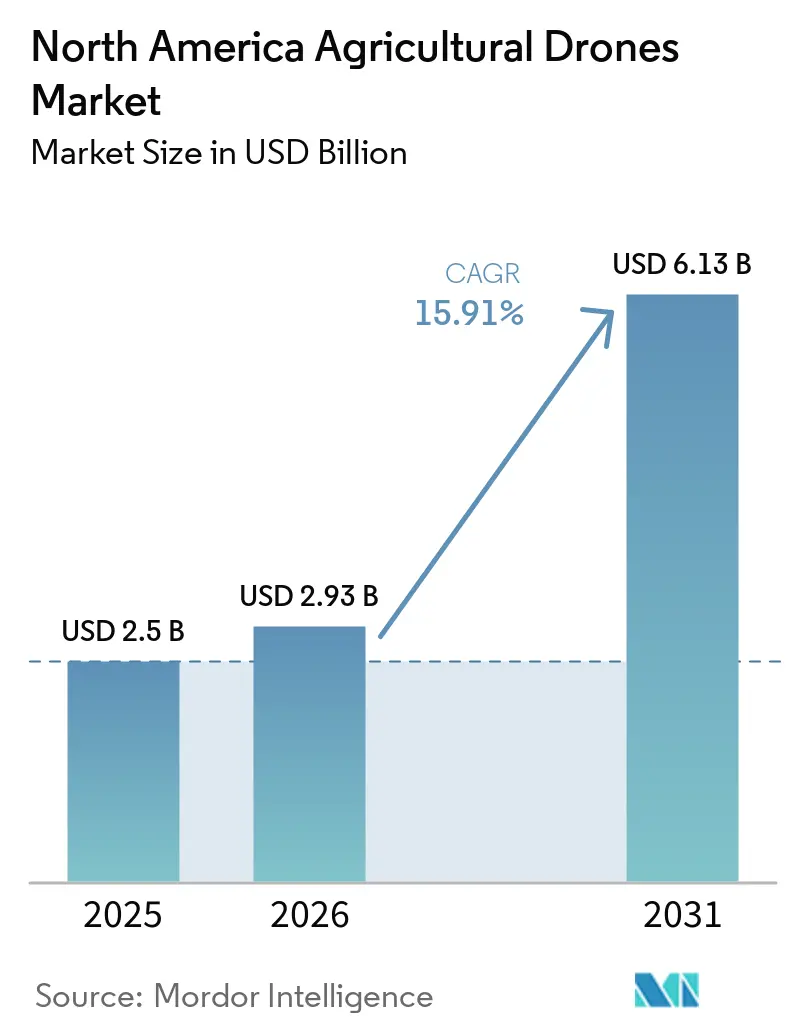

| Base Year Market Size (2025) | USD 2.5 Billion |

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 6.13 Billion |

| Growth Rate (2026 - 2031) | 15.91% CAGR |

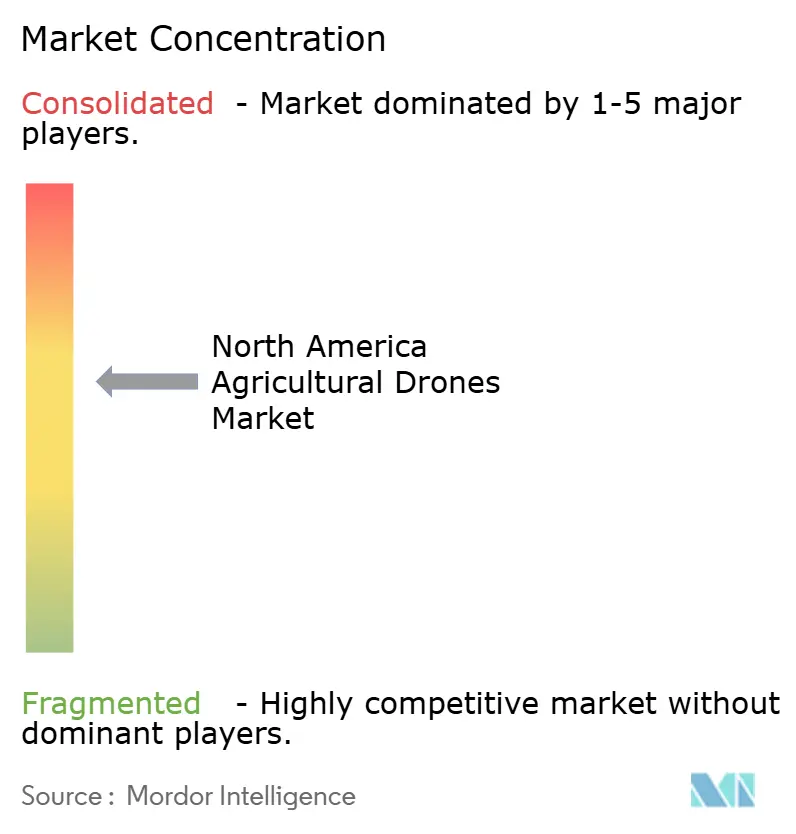

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Agricultural Drones Market Analysis by Mordor Intelligence

The North America agricultural drones market size is projected to grow from USD 2.50 billion in 2025 and USD 2.93 billion in 2026 to USD 6.13 billion by 2031, registering a CAGR of 15.91% between 2026 and 2031. Factors such as widespread labor shortages, rising input costs, and favorable beyond-visual-line-of-sight (BVLOS) exemptions from the Federal Aviation Administration (FAA) are driving the demand for unmanned aerial systems in large-acre row-crop and high-value specialty-crop operations. Declining hardware costs, enhanced payload capacities, and tariff-driven on-shoring of manufacturing are reducing adoption barriers for midsize farms. Additionally, Drone-as-a-Service providers are addressing the needs of fragmented smallholder farms. Software platforms capable of converting imagery into variable-rate prescriptions within 24 hours are creating new revenue opportunities and supporting recurring revenue models for vendors. Competitive intensity remains moderate to high, with domestic producers gaining market share following the Federal Communications Commission (FCC) decision to limit the entry of new foreign-made drones.

Key Report Takeaways

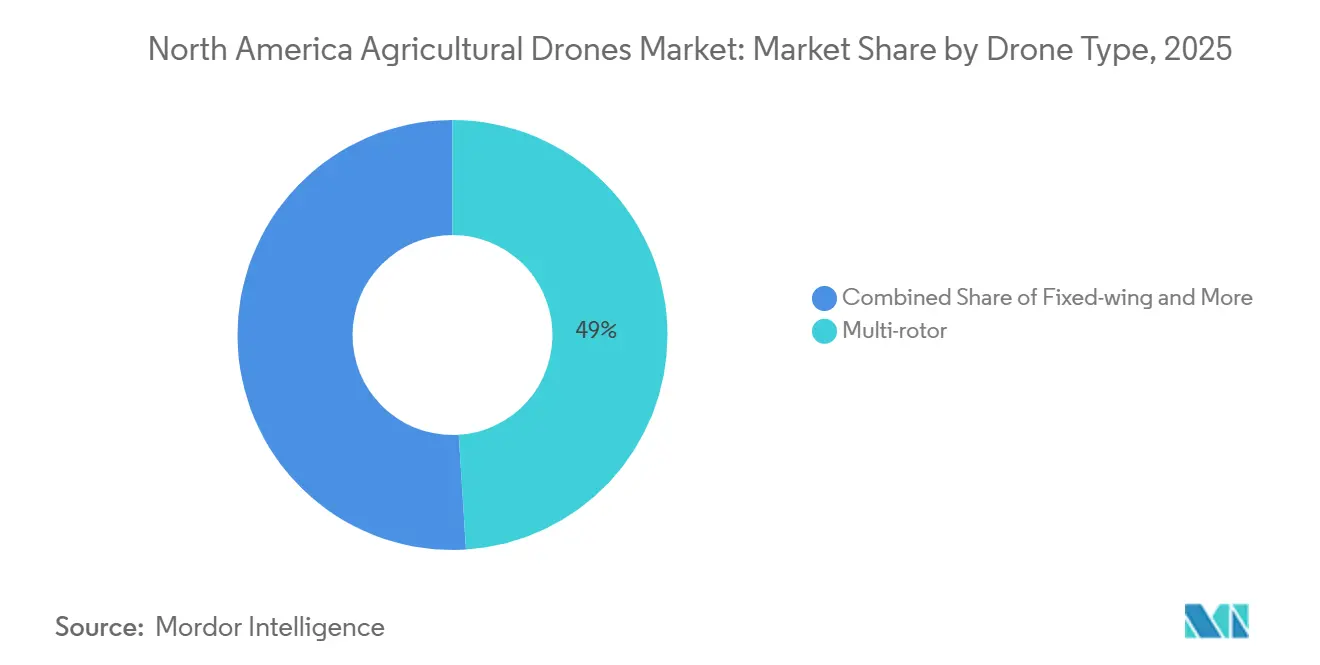

- By drone type, multi-rotor accounted for the largest 49.0% of the North America agricultural drones market share in 2025. In contrast, the North America agricultural drones market size for hybrid (VTOL) is projected to expand at the fastest 17.4% CAGR from 2026 to 2031.

- By application, crop monitoring and scouting held the largest 38.0% market share in 2025, whereas the North America agricultural drones market size for precision spraying and fertilization is projected to grow at the fastest 16.9% CAGR from 2026 to 2031.

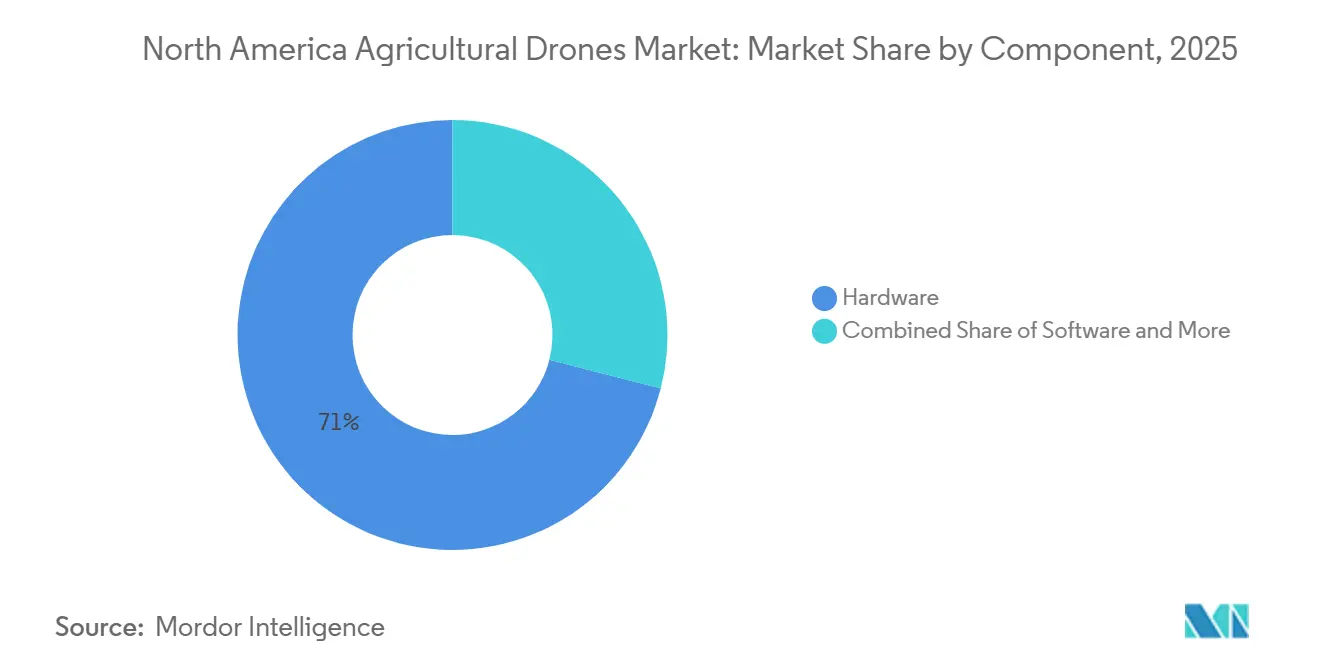

- By component, hardware captured the largest 71.0% of the North America agricultural drones revenue share in 2025, whereas software is projected to expand at the fastest 17.8% CAGR from 2026 to 2031.

- By autonomy level, semi-autonomous accounted for the largest 56.0% revenue share in 2025, whereas fully autonomous is projected to grow at the fastest 17.2% CAGR from 2026 to 2031.

- By geography, the United States commanded the largest 79.0% revenue share in 2025, whereas Mexico is projected to expand at the fastest 16.4% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Agricultural Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid precision-agriculture adoption across large United States and Canadian farms | +3.8% | United States Midwest and Great Plains, Canadian prairie provinces | Medium term (2–4 years) |

| Falling costs and better performance of multi-rotor and fixed-wing drones | +3.2% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Easier Federal Aviation Administration beyond visual line of sight (FAA BVLOS) approvals boosting acreage coverage | +4.1% | United States rural Class G airspace | Medium term (2–4 years) |

| Tariff-driven domestic drone assembly strengthening supply resilience | +2.6% | United States manufacturing hubs in Texas, Vermont, and Michigan | Long term (≥ 4 years) |

| Carbon-credit revenue from variable-rate input reduction | +1.4% | Conservation watersheds in United States and Canada | Long term (≥ 4 years) |

| Drone-as-a-Service expansion in Mexico’s specialty crop belt | +2.7% | Michoacán, Jalisco, Sinaloa, and Durango | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Precision-Agriculture Adoption Across Large United States and Canadian Farms

Large-scale farms in the United States and Canada are increasingly adopting digital farming technologies to enhance field efficiency, optimize input usage, and improve crop monitoring. According to the United States Department of Agriculture Economic Research Service report published in December 2024, guidance autosteering systems and other equipment were utilized on 70% of large-scale crop-producing farms in the United States. The expanding use of precision agriculture systems is fostering favorable conditions for the adoption of agricultural drones, particularly for applications such as multispectral imaging, crop scouting, and variable-rate application in major row-crop-producing regions across North America.

Falling Costs and Better Performance of Multi-Rotor and Fixed-Wing Drones

Declining drone costs, combined with significant advancements in payload capacity, battery efficiency, and field productivity, are driving the adoption of agricultural drones across North America. In February 2026, XAG launched the P150 Max agricultural drone in the United States, featuring a maximum payload capacity of 176 pounds and an average spraying productivity of 50–60 acres per hour [1]Source: XAG, “XAG P150 Max Agricultural Drone Comes to Unites States with Proven Efficiency and Reliability,” xa.com. Its swarm-control capability allows a single operator to manage two drones simultaneously. Furthermore, DJI Technology Co. Ltd.'s DB1560 Intelligent Flight Battery offers up to 1,500 charge cycles and nine-minute fast charging, minimizing downtime during critical application periods.

Easier Federal Aviation Administration Beyond Visual Line of Sight (FAA BVLOS) Approvals Boosting Acreage Coverage

In September 2025, the Federal Aviation Administration (FAA) Exemption No. 24815 granted Beyond Visual Line of Sight (BVLOS) relief to Bluebird Precision Ag, establishing an operator-certificate pathway under Part 137 regulations. Kansas allocated USD 3 million to statewide drone corridors and completed a long-range BVLOS delivery in August 2025, providing a reference model for rural drone operations. In March 2026, ResilienX obtained a 1,900-square-mile waiver by utilizing shared surveillance infrastructure, demonstrating that cooperative detect-and-avoid networks can enable routine BVLOS operations without the need for visual observers [2]Source: Starburst Aerospace, “ResilienX Receives FAA Certificate of Waiver for BVLOS Drone Operations,” starburst.aero.

Tariff-Driven Domestic Drone Assembly Strengthening Supply Resilience

A cumulative 170% tariff imposed in April 2025 in the United States increased the retail price of the DJI Mavic 3 Pro from USD 2,199 to approximately USD 4,750. This led to a decline in imports and encouraged local production [3]Source: AirSight, “Tariffs on Chinese Drones in 2025, Rising Prices and Impacts on the Unites States Market,” airsight.com. Additionally, the December 2025 FCC ruling further restricted the entry of new foreign drones, prompting companies such as Hylio, Ceres Air, and Exedy Drones to expand domestic production capacity. State-level procurement bans, such as the 2025 Kansas House Substitute for Senate Bill 9, emphasize domestic sourcing requirements. However, supply chain challenges persist for components such as motors, batteries, and LiDAR, which may necessitate temporary waivers in the near future.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-platform compatibility gaps with legacy machinery | −2.1% | United States and Canada mixed-vintage fleets | Short term (≤ 2 years) |

| High upfront and maintenance costs for small growers | −2.8% | Farms under 500 acres in United States and Mexico | Medium term (2–4 years) |

| Shortage of licensed remote pilots with agronomic analytics expertise | −1.9% | Rural United States and Canada | Medium term (2–4 years) |

| Stricter lithium-battery shipping regulations affecting field logistics | −1.2% | Cross-border supply chains in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Platform Compatibility Gaps With Legacy Machinery

Older tractors and sprayers from CNH Industrial, AGCO Corporation, and early John Deere series do not have built-in compatibility with drone-generated shapefiles, necessitating manual data transfers or expensive display upgrades. Middleware solutions like agrirouter are being introduced to enable automated synchronization between the John Deere Operations Center and third-party software. However, full bidirectional telemetry and prescription data exchange are not projected until late 2026. While AcreConnect currently supports exporting application maps compatible with DJI, XAG, and Exedy drones, many mixed fleets continue to depend on USB sticks, increasing the likelihood of errors.

High Upfront and Maintenance Costs for Small Growers

High acquisition and operating costs continue to hinder the adoption of agricultural drones among small and mid-sized farms in North America. According to the University of Missouri Extension’s 2025 analysis, the total application cost for a farmer using a DJI Agras T40 drone across 1,000 acres was estimated at USD 12.27 per acre, with battery expenses alone accounting for USD 1.72 per acre. The study also highlighted that drone ownership becomes economically viable only when annual application acreage exceeds approximately 980 acres. These cost challenges make it difficult for farms operating below this scale to justify investments in drone hardware, batteries, charging systems, and maintenance infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drone Type: Hybrid VTOL Gains Traction

Multi-rotor accounted for the largest 49.0% of the North America agricultural drones market share in 2025. This segment benefits from features such as vertical take-off capability, maneuverability in irregular field layouts, and suitability for targeted spraying and crop monitoring. Farmers in the United States Midwest and Canadian prairie provinces are increasingly adopting multi-rotor systems for applications like fungicide spraying, crop scouting, and nutrient assessment. These drones are favored for their simplified operation and compatibility with precision agriculture workflows.

The North America agricultural drones market size for hybrid (VTOL) is projected to expand at the fastest 17.4% CAGR from 2026 to 2031. This segment combines the cruising efficiency of fixed-wing drones with the vertical take-off flexibility of multi-rotor systems, making it ideal for large-acre farms requiring extended coverage and operational efficiency. Factors such as increasing interest in beyond visual line of sight (BVLOS) operations, advancements in battery charging speed, and swarm-control capabilities are driving the adoption of hybrid drones in broadacre farming.

By Application: Precision Spraying Accelerates

Crop monitoring and scouting held the largest 38.0% market share in 2025. Agricultural producers are increasingly utilizing drone-based imaging systems to detect nutrient deficiencies, pest infestations, irrigation inconsistencies, and crop stress conditions before visible damage occurs in the field. Multispectral and thermal imaging technologies play a critical role in precision farming by enabling growers to optimize fertilizer application, enhance yield forecasting, and monitor crop health across extensive farming areas. Adoption is particularly strong in regions producing corn, soybean, wheat, and specialty crops, where labor shortages and rising operational costs drive the use of automated aerial monitoring solutions for field management and agronomic assessments.

Precision spraying and fertilization are projected to grow at the fastest 16.9% CAGR from 2026 to 2031. This growth is driven by the increasing adoption of drone-based pesticide application, the rising use of variable-rate technologies, and the demand for reduced chemical wastage in commercial farming operations. Agricultural drones equipped with centrifugal atomizers and precision application systems are enhancing spray consistency, reducing input consumption, and minimizing field compaction. Regulatory approvals for multi-drone operations and the integration of prescription mapping technologies are further boosting demand for precision spraying services, particularly among large farms and agricultural contractors aiming to improve operational efficiency and reduce per-acre treatment costs.

By Component: Software Drives Margin Expansion

Hardware accounted for the largest 71.0% of the North America agricultural drones revenue share in 2025. The segment's dominance is driven by strong demand for airframes, propulsion systems, imaging sensors, batteries, and payload equipment. Agricultural producers are prioritizing drones that can carry larger spray loads, cover wider field areas, and operate for extended durations under diverse environmental conditions. The increasing use of fixed-wing and hybrid platforms for large-acre farming applications is further boosting investments in advanced hardware systems. Additionally, domestic manufacturing expansion and supply-chain localization initiatives in the United States and Canada are supporting the growth of hardware demand.

Software is projected to grow at the fastest CAGR of 17.8% from 2026 to 2031. The rising demand for analytics platforms capable of processing aerial imagery, generating prescription maps, and integrating field intelligence into precision agriculture ecosystems is driving this growth. Cloud-based software solutions are enhancing operational efficiency by enabling rapid image analysis, flight planning, automated reporting, and seamless integration with digital farm-management systems. As autonomous and semi-autonomous drone fleets become more prevalent, software platforms that support mission coordination, data interpretation, and variable-rate application workflows are projected to capture a larger share of industry spending. These platforms are also creating recurring subscription-based revenue opportunities for technology providers.

By Autonomy Level: Fully Autonomous Systems Emerge

Semi-Autonomous accounted for the largest 56.0% revenue share in 2025. The segment remains dominant because agricultural producers continue to prefer systems that combine automated flight paths with human supervision for spraying, scouting, and mapping operations. Semi-autonomous drones improve operational efficiency while allowing operators to maintain oversight during field missions, particularly in complex agricultural environments and varying weather conditions. Their compatibility with existing precision agriculture workflows, lower regulatory complexity, and reduced training requirements support widespread adoption across commercial farming operations in the United States, Canada, and Mexico. Demand also remains strong among agricultural contractors managing multiple farm locations and crop types.

Fully Autonomous is projected to grow at the fastest 17.2% CAGR from 2026 to 2031. Growth is supported by advances in artificial intelligence, detect-and-avoid systems, autonomous navigation, and edge-computing technologies that reduce the need for continuous operator intervention. Agricultural producers are increasingly evaluating autonomous platforms capable of continuous field monitoring, automated spraying, and real-time agronomic analysis to address labor shortages and improve operational scalability. Expanding regulatory support for beyond visual line of sight operations and multi-drone fleet management is also accelerating interest in fully autonomous agricultural systems designed for large-scale row-crop and specialty-crop farming environments across North America.

Geography Analysis

The United States accounted for the largest market share of 79.0% in 2025, driven by extensive cropland availability, strong adoption of precision agriculture, and supportive regulatory frameworks for commercial drone operations. Major farming states such as Iowa, Illinois, Kansas, and Nebraska are expanding drone usage for crop monitoring, spraying, and field analytics. The adoption of precision farming systems, along with increasing labor shortages and the demand for greater operational efficiency, is driving the use of drones on large-scale row-crop farms. Furthermore, advancements in beyond visual line of sight testing programs and rising investments in rural drone corridors are supporting the expanded deployment of commercial agricultural drones nationwide.

Mexico is projected to grow at the fastest CAGR of 16.4% from 2026 to 2031, driven by increasing demand for efficient crop management solutions in specialty-crop farming regions. Agricultural drone adoption is rising among producers of avocados, berries, and vegetables, as aerial spraying systems offer greater effectiveness across fragmented landholdings and uneven terrain compared to conventional ground equipment. The growing availability of drone-as-a-service providers is improving access to this technology for small and medium-sized growers who may find direct equipment ownership cost-prohibitive. Rising labor costs and increasing interest in precision farming practices are further supporting the demand for drone-assisted spraying, scouting, and fertilization operations in commercial farming regions.

Canada is experiencing a rise in agricultural drone adoption across prairie farming regions, driven by regulatory advancements that enhance commercial deployment opportunities. In 2025, Transport Canada announced new regulations permitting certain beyond visual line of sight (BVLOS) operations and medium-sized drone operations without the need for a Special Flight Operations Certificate. These regulations are effective from November 2025. This updated framework is anticipated to enhance operational scalability for agricultural drone operators engaged in activities such as crop scouting, nitrogen management, and field monitoring on wheat and canola farms. The growing regulatory support for autonomous and long-range drone operations is bolstering commercial confidence in precision agriculture technologies across rural Canada.

Competitive Landscape

The competition in the North America Agricultural Drone market remains moderately concentrated, with key players including DJI Technology Co. Ltd., Deere and Company, Trimble Inc., PrecisionHawk Inc., and DroneDeploy Inc. Domestic manufacturers, software developers, and precision agriculture technology providers are expanding their presence in commercial farming operations. Regulatory restrictions on foreign drone approvals are driving local assembly and increasing investments in domestically manufactured systems tailored for agricultural applications. Companies are focusing on enhancing payload capacity, operational endurance, autonomous capabilities, and integrated analytics to strengthen their competitive positioning.

Technology differentiation continues to influence competition, with manufacturers prioritizing productivity enhancements, faster charging systems, and improved fleet management capabilities. Software providers are expanding cloud-based analytics platforms to process aerial imagery and deliver actionable agronomic insights more efficiently. Agricultural contractors increasingly prefer interoperable systems that integrate seamlessly with existing farm-management platforms and precision agriculture infrastructure. Market participants are also investing in autonomous flight capabilities, detect-and-avoid technologies, and multi-drone coordination systems to enhance operational efficiency in large-scale commercial farming operations. These advancements are intensifying competition among hardware manufacturers, analytics providers, and integrated agricultural technology companies.

Strategic collaborations and technology partnerships are becoming more prevalent as companies aim to strengthen their product portfolios and accelerate deployment in commercial agriculture. For instance, in May 2025, Deere and Company acquired Sentera to integrate aerial field imagery into its precision spraying ecosystem, enhancing digital agronomy and automated application capabilities. Companies that can combine hardware manufacturing, aerial analytics, autonomous operations, and agronomic decision-support tools into a unified operational platform are projected to gain a competitive edge in the long term. Furthermore, increasing investments in artificial intelligence, autonomous navigation, and cloud-based analytics platforms are reshaping the competitive dynamics within North America's precision agriculture technology ecosystems.

North America Agricultural Drones Industry Leaders

DJI Technology Co. Ltd.

Deere and Company

Trimble Inc.

PrecisionHawk Inc.

DroneDeploy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: XAG Co. Ltd. introduced the P150 Max agricultural drone in the United States at the Spray Drone End User Conference held in Kansas City. The drone is equipped with a 176-pound payload capacity, swarm-control functionality, and a spraying efficiency of 50–60 acres per hour, aimed at enhancing large-scale precision farming operations.

- December 2025: The Federal Communications Commission included DJI Technology Co. Ltd. and other foreign-made drones on the Covered List, limiting future equipment authorizations for new drone models in the United States. This regulatory measure has increased demand for domestically produced agricultural drones.

- May 2025: Deere and Company acquired Sentera Inc. to incorporate aerial drone imagery and field analytics into its precision agriculture ecosystem. This acquisition enhanced the company’s See and Spray technology and autonomous crop management capabilities in North America.

North America Agricultural Drones Market Report Scope

Agricultural drones are unmanned aerial vehicles (UAVs) utilized in farming to enhance crop management, field monitoring, and precision agriculture practices. These drones assist farmers with tasks such as crop scouting, precision spraying, soil analysis, irrigation monitoring, and livestock surveillance, while minimizing labor needs, input costs, and operational time. The North America agricultural drones market report is segmented by drone type (multi-rotor, fixed-wing, and hybrid (VTOL)), by application (crop monitoring and scouting, precision spraying and fertilization, soil and field analysis, irrigation management, planting and seeding, and livestock monitoring), by component (hardware, software, and services), by autonomy level (remote-controlled, semi-autonomous, and fully autonomous), and by geography (United States, Canada, and Mexico). The market forecasts are provided in terms of value (USD).

| Multi-rotor |

| Fixed-wing |

| Hybrid (VTOL) |

| Crop Monitoring and Scouting |

| Precision Spraying and Fertilization |

| Soil and Field Analysis |

| Irrigation Management |

| Planting and Seeding |

| Livestock Monitoring |

| Hardware | Frame and Airframe |

| Propulsion System | |

| Batteries and Power | |

| Sensors and Payloads | |

| Software | Flight Planning and Control |

| Data Analytics and AI | |

| Fleet Management | |

| Services | Drone-as-a-Service |

| Training and Support | |

| Maintenance and Repair |

| Remote-Controlled |

| Semi-Autonomous |

| Fully Autonomous |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Drone Type | Multi-rotor | |

| Fixed-wing | ||

| Hybrid (VTOL) | ||

| By Application | Crop Monitoring and Scouting | |

| Precision Spraying and Fertilization | ||

| Soil and Field Analysis | ||

| Irrigation Management | ||

| Planting and Seeding | ||

| Livestock Monitoring | ||

| By Component | Hardware | Frame and Airframe |

| Propulsion System | ||

| Batteries and Power | ||

| Sensors and Payloads | ||

| Software | Flight Planning and Control | |

| Data Analytics and AI | ||

| Fleet Management | ||

| Services | Drone-as-a-Service | |

| Training and Support | ||

| Maintenance and Repair | ||

| By Autonomy Level | Remote-Controlled | |

| Semi-Autonomous | ||

| Fully Autonomous | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current value of the North America agricultural drones market?

The North America agricultural drones market size is at USD 2.93 billion USD in 2026.

How fast is the market projected to grow by 2031?

The market is projected to grow at 15.91% CAGR from 2026 to 2031.

Which drone type holds the largest share today?

Multi-rotor type drone captured the largest 49.0% of the market share in 2025.

Are domestic manufacturers gaining share?

Yes, the December 2025 FCC ruling restricting new foreign drones is prompting companies such as Hylio Inc. to expand local assembly, reshaping competitive dynamics.

Page last updated on: