Agricultural Robots Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

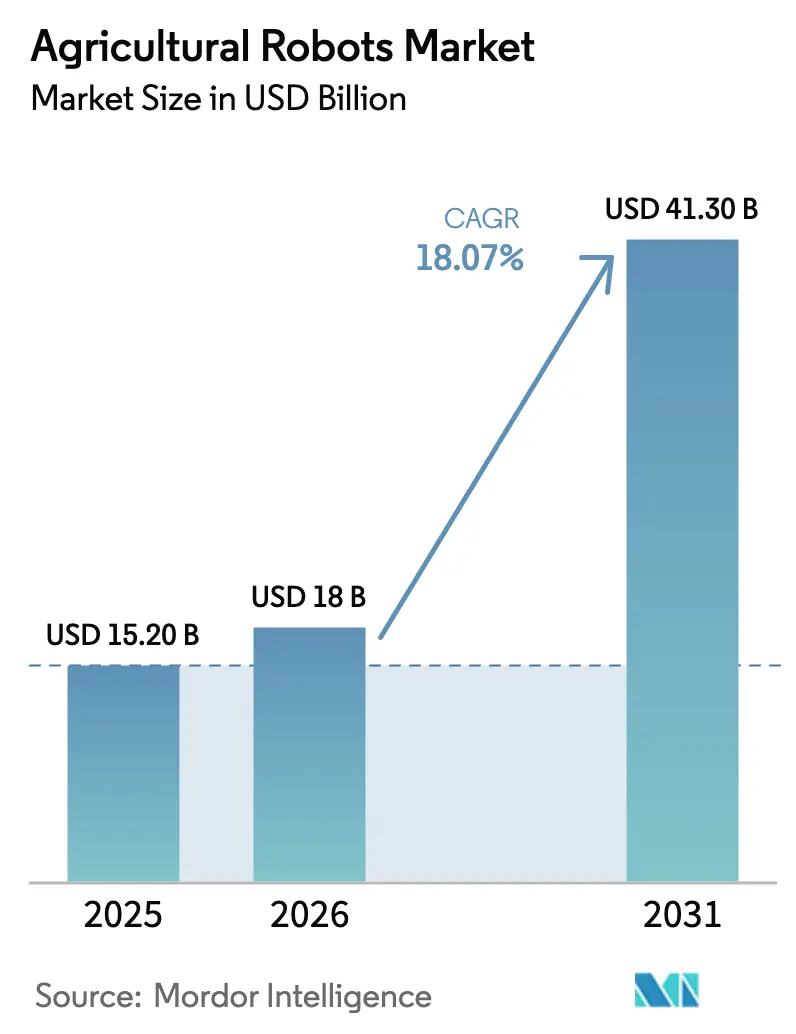

| Market Size (2026) | USD 18 Billion |

| Market Size (2031) | USD 41.30 Billion |

| Growth Rate (2026 - 2031) | 18.07% CAGR |

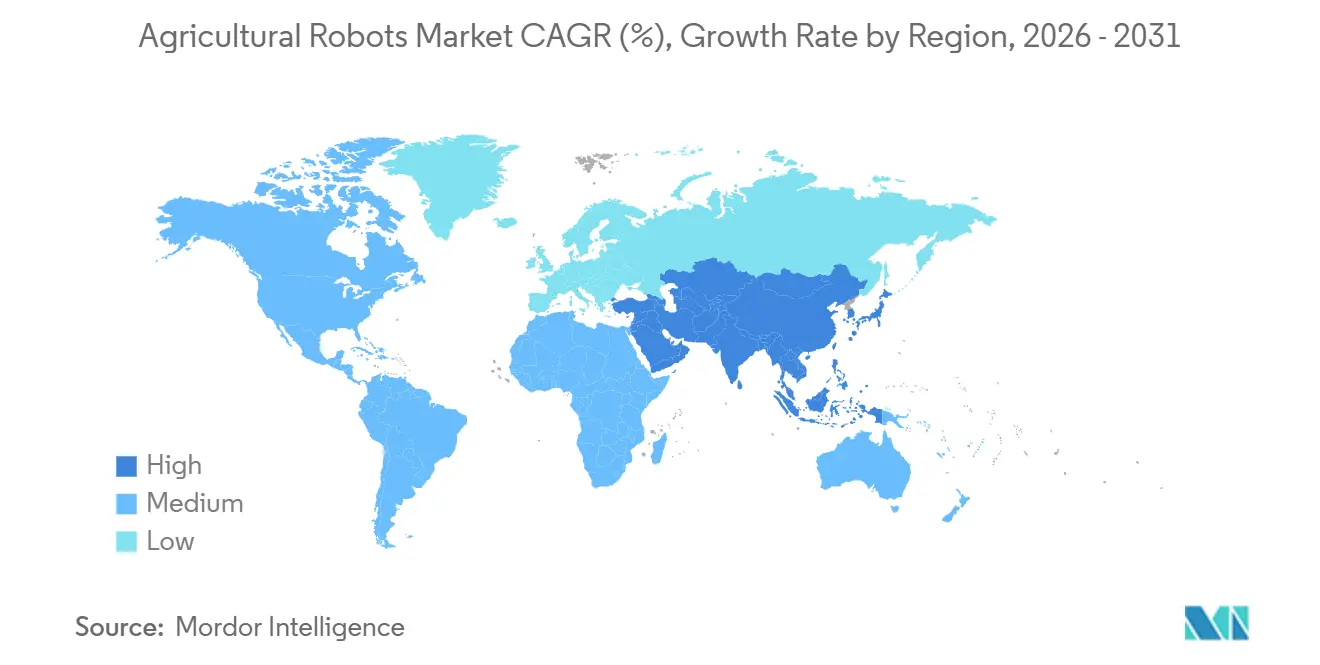

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Robots Market Analysis by Mordor Intelligence

The agricultural robots market is projected to expand from USD 15.2 billion in 2025 and USD 18.0 billion in 2026 to USD 41.3 billion by 2031, registering a CAGR of 18.07% between 2026 to 2031. Factors such as escalating labor costs, decreasing sensor prices, and the rise of subscription-based robotics-as-a-service models are making autonomous equipment more accessible to mid-tier farms. This shift is accelerating the commercialization of these technologies across row-crop, specialty-crop, and dairy operations. Between 2022 and 2025, over USD 1 billion was funneled into harvesting and weeding start-ups, underscoring a robust supply of mature technology products poised to fill the gap left by seasonal labor shortages. Advancements in hardware, like LiDAR systems priced under USD 1,000 and affordable machine-vision cameras, are driving down material costs and expediting design processes. Government incentives, ranging from eco-schemes by the European Commission to precision-agriculture grants in the United States, are promoting verifiable reductions in chemical inputs. These incentives particularly favor robots that can produce audit-ready data. Collectively, these dynamics are steering value towards software and data analytics. Fleet-management platforms are emerging as pivotal tools, transforming machines into continuous sources of agronomic insights.

Key Report Takeaways

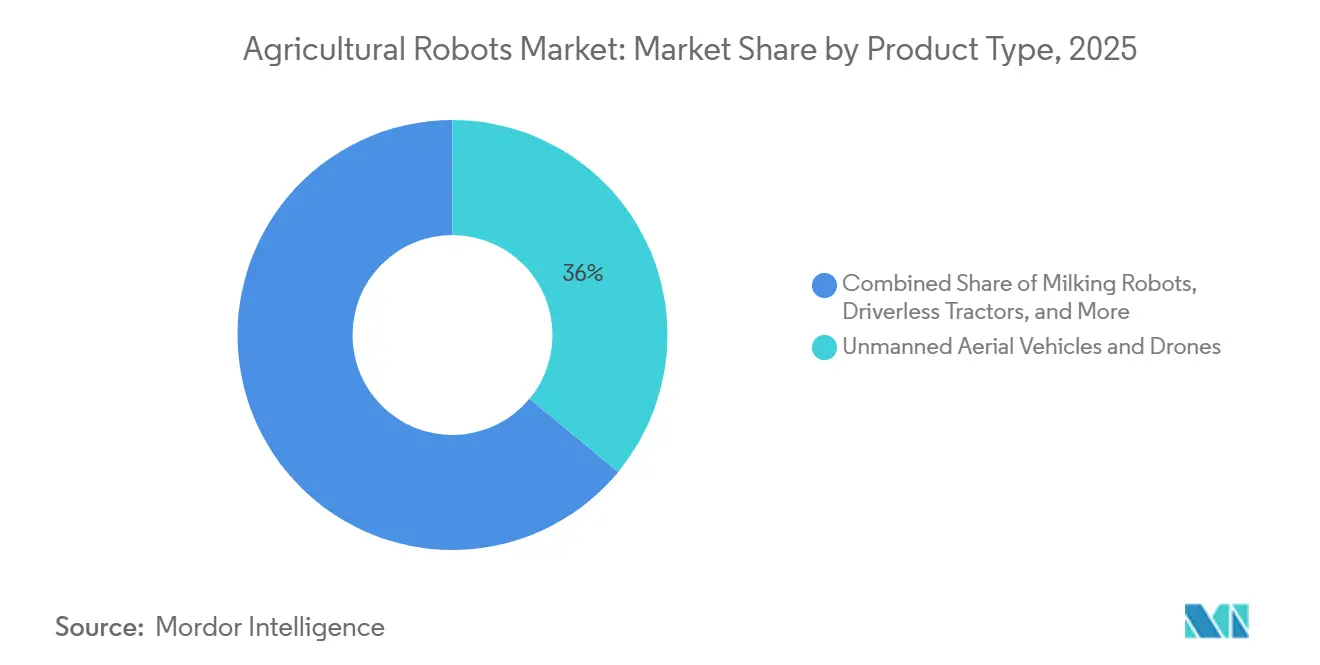

- By product type, unmanned aerial vehicles and drones led with 36.0% revenue share in 2025, while harvesting and picking robots are forecast to expand at a 18.9% CAGR through 2031.

- By application, crop farming accounted for 44.0% of the agricultural robots market share in 2025, and greenhouse farming is projected to advance at a 17.4% CAGR through 2031.

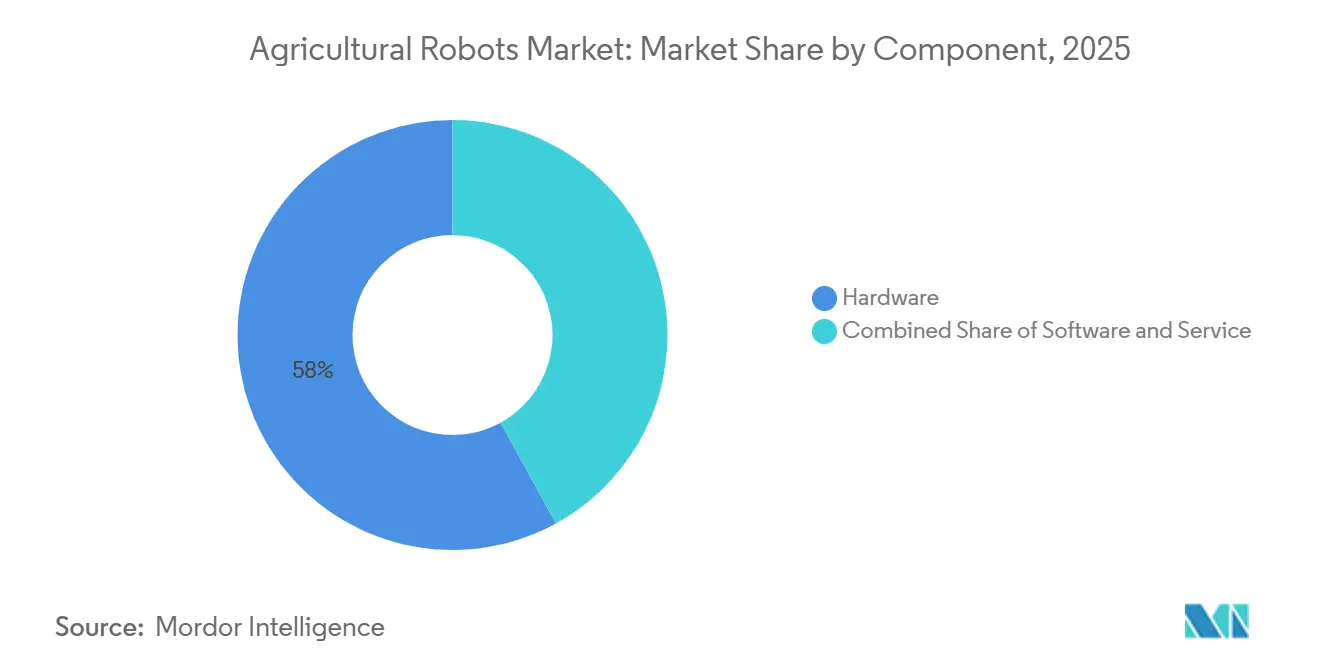

- By component, hardware captured 58.0% of the agricultural robots market size in 2025, whereas software is anticipated to grow at a CAGR of 16.7% between 2026 and 2031.

- By geography, North America accounted for 33.0% of the revenue in 2025, whereas the Asia-Pacific region is anticipated to grow at a CAGR of 14.8% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agricultural Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating labor shortages in industrialized farming nations | +4.2% | North America, Europe, Japan | Medium term (2-4 years) |

| Declining price of machine-vision cameras and LiDAR | +3.1% | Global | Short term (≤ 2 years) |

| Policy incentives for sustainable and precision farming | +2.8% | Europe, North America, China | Long term (≥ 4 years) |

| Venture-capital influx into autonomous harvesting start-ups | +2.3% | North America, Europe | Medium term (2-4 years) |

| Synergistic use of agricultural robots with carbon-credit platforms | +1.7% | Europe, North America, Australia | Long term (≥ 4 years) |

| Ag-robot subscription models boosting SME affordability | +2.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Labor Shortages in Industrialized Farming Nations

Farm labor scarcity is reshaping capital-allocation priorities across the United States, Europe, and Japan. In the United States, only 637,000 hired crop workers were counted in April 2025, despite the temporary worker visa program issuing 310,676 visas in 2023, indicating that guest-worker inflows cannot fully offset domestic labor exits[1]Source: UK Department for Environment, Food and Rural Affairs, “Improving Farm Productivity Grant Guidance,” gov.uk. Japan projects that its farmer population will plunge below one million by 2030, with an average age surpassing 68 years, and similar demographic pressures are also haunting Germany, France, and the Netherlands. Specialty crops such as strawberries and apples, which still depend on hand-picking, face the greatest risk because scheduling errors or sudden worker shortages can wipe out full-season profits. Autonomous harvesters that replicate repetitive human motions offer an economic breakeven once hourly labor costs exceed USD 18, a threshold already surpassed in California and Western Europe, as growers redesign orchards and row spacing to accommodate machines. Labor savings compound over multiple seasons. Because a full crop cycle is needed to embed new practices, the impact on market growth is concentrated in the medium term.

Declining Price of Machine-Vision Cameras and LiDAR

Rapid cost deflation in sensors is lowering entry barriers for both equipment makers and growers. Solid-state LiDAR units, which cost USD 10,000 in 2020, dropped below USD 1,000 by late 2024, a 90% reduction driven by economies of scale in the automotive sector. Camera modules with onboard inference chips decreased in price from USD 500 to under USD 150 per unit between 2022 and 2025. Deere integrated Nvidia Jetson edge-AI boards into its See and Spray Ultimate platform to process 20 images per second and trigger nozzles within 50 milliseconds, slashing herbicide volumes by up to 80%. Lower sensor bills shorten product development cycles, encourage modular designs, and open doors for regional manufacturers that could not previously afford expensive research and development. The affordability gains materialize immediately upon shipment, resulting in a significant short-term growth contribution.

Venture-Capital Influx into Autonomous Harvesting Start-Ups

Capital availability has swung from scarcity to abundance. Carbon Robotics, maker of laser-based weeders, raised USD 70 million in October 2024 and plans to scale manufacturing to 500 units by 2025. Orchard Robotics secured USD 22 million in September 2025 for fruit-intelligence analytics that guide robotic pickers. FarmWise has closed a USD 45 million round in 2022 to expand its per-acre weeding service. Funding accelerates hiring, tooling, and dealer-network build-out, compressing the timeline from prototype to commercial availability. Because hardware field validation and farmer onboarding require at least two seasons, the contribution to market growth peaks in the medium term.

Synergistic use of Agricultural Robots with Carbon-Credit Platforms

Agricultural robots are evolving into data engines for soil-carbon programs operated by companies such as Nori and Indigo Ag. Robots’ embedded sensors produce timestamped, geotagged records of tillage, cover crops, and fertilizer placement that manual logs cannot replicate. Deere’s Operations Center exports machine-generated data directly to credit registries, helping growers capture payments of USD 13 to USD 20 per metric ton of carbon in Australia’s Emissions Reduction Fund. The emerging revenue stream defrays leasing fees and strengthens the business case for automation. As market rules continue to harmonize, growth acceleration is anticipated to unfold over the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-operability gaps among multi-vendor farm platforms | -1.9% | Global | Medium term (2-4 years) |

| Low internet-of-things (IoT) coverage in rural zones | -1.6% | South America, Africa, rural Asia-Pacific | Long term (≥ 4 years) |

| High up-front retro-fitting cost for legacy implements | -1.3% | Europe, North America | Short term (≤ 2 years) |

| Cyber-security concerns around GNSS spoofing of ag-robots | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inter-Operability Gaps Among Multi-Vendor Farm Platforms

Most equipment brands maintain proprietary data formats that prevent seamless coordination across mixed fleets. Deere Operations Center, CNH Industrial Raven Autonomy, and AGCO Fuse each apply unique message protocols, forcing growers either to standardize on one supplier or invest in middleware integration. The Agricultural Industry Electronics Foundation has published ISO 11783 standards. However, vendors often add private extensions to protect their competitive moats. Farmers who attempt cross-brand automation confront data silos, incompatible map layers, and duplicative subscriptions. Integration consulting can inflate the total cost of ownership and slow project rollouts. Because standards adoption historically stretches over five to seven years, the restraint’s drag on market growth is classified as medium-term.

Low Internet of Things Coverage in Rural Zones

Autonomous equipment relies on continuous connectivity for real-time monitoring and fleet coordination, yet broadband gaps persist. The Federal Communications Commission reported that rural areas in the United States still lack 25/3 megabit broadband, and 5G coverage remains spotty outside urban centers[2]Source: Federal Communications Commission, “2024 Broadband Deployment Report,” fcc.gov. In sub-Saharan Africa and rural South America, internet penetration is below 30%. Robots can operate offline using edge processing, but growers lose the ability to update missions, receive alerts, or push data to carbon platforms. Satellite and low-power wide-area networks offer partial solutions but come with subscription fees. Because tower construction and fiber backhaul build-outs require multi-year investments, the restraint’s impact extends into the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unmanned Aerial Vehicles and Drones Lead

Unmanned aerial vehicles and drones captured 36.0% of the agricultural robots market share in 2025 as growers embraced their dual ability to scout fields and spray inputs with centimeter-accurate targeting. The DJI Agras T50 drone carries a 40-kilogram payload and covers 20 hectares per hour, trimming application time by 60% compared to ground sprayers[3]Source: DJI, “Agras T50 Specifications,” dji.com. The large-scale adoption of aerial robots in rice and wheat paddies across China and Southeast Asia highlights the ease of integrating them into existing workflows. Notably, data gathered by drones feeds into variable-rate fertilizer models, linking equipment spending to tangible yield gains. Hardware manufacturers are layering subscription-based analytics on top of one-time drone sales, turning flight data into recurring revenue streams. As satellite imagery improves, drones continue to hold an edge in spatial resolution and flexible deployment windows, thereby preserving their leadership across various crop types.

Harvesting and picking robots are projected to grow at a CAGR of 18.9% between 2026 and 2031, the fastest trajectory in the agricultural robots market. Orchard platforms that once moved workers now carry robotic arms to pick apples, peaches, and berries. Soft-grip end-effectors and machine-vision cameras track fruit ripeness, while laser targeting reduces bruising and boosts pack-out rates. Laser weeding systems from Carbon Robotics already demonstrate field-ready durability, removing 5,000 weeds per minute. Venture funding is accelerating commercial pilots across California, Washington, and New South Wales, with service providers guaranteeing per-acre cost parity with seasonal labor by the third season. As controlled-environment agriculture expands, robots tailored to greenhouse tomatoes, cucumbers, and leafy greens will further diversify revenue, driving the category’s out-performances.

By Application: Crop Farming Leads, Greenhouse Farming Accelerates

Crop farming commanded a 44.0% market share of agricultural robots in 2025, as growers of corn, soybeans, and wheat leveraged autonomous tractors and spray drones to cover broad acreages with centimeter-level precision. The scale and uniformity of these row-crop fields enable robots to log long duty cycles and generate high-quality data sets that refine variable-rate prescriptions season after season. Livestock management accounted for a significant share in 2025, driven by robotic milking, health-monitoring collars, and automated feeding systems that enable dairy operators to reduce labor hours by half while enhancing yield consistency. Dairy-specific solutions, such as the Lely Astronaut A5, can handle up to 60 cows a day, freeing workers for higher-value herd-health tasks and validating payback timelines of fewer than four years.

Greenhouse farming is forecast to expand at a 17.4% compound annual growth rate through 2031, the fastest trajectory within the application mix, because controlled-environment layouts make vision-guided robots immediately productive. Vertical-farm operators in North America and Western Europe now rely on robotic transplanters and harvesters to operate around the clock in facilities where human labor costs exceed and ergonomic risks rise quickly. Technologies first proven in open-field weeding, such as Naïo Technologies Oz platform, are now adapted for greenhouse tomatoes and cucumbers, enabling precise blade control that avoids delicate stems. As urban agriculture scales, continuous production cycles feed a steady data stream into artificial-intelligence engines, raising the strategic worth of robots beyond labor substitution and helping boost the overall agricultural robots market size.

By Component: Hardware Dominates, Software Gains Momentum

Hardware delivered 58.0% of revenue in 2025, as each autonomous tractor or dairy robot embeds USD 100,000 to USD 150,000 worth of mechanical and electronic parts, ranging from ruggedized frames to multispectral cameras. The cost of these components still dictates initial purchase decisions, particularly for growers evaluating whether to retrofit or replace aging fleets.

Software, however, is projected to grow at 16.7% annually through 2031, the quickest component pace, because edge-artificial-intelligence algorithms now deliver real-time weed recognition, yield estimation, and route optimization without cloud latency. Deere See and Spray Ultimate processes twenty images per second on Nvidia Jetson boards, triggering nozzles within fifty milliseconds and cutting herbicide volumes by up to 80%. As update cycles shorten to quarterly over-the-air releases, subscription fees linked to performance gains drive gross margins higher than those from hardware sales alone. Consequently, software value capture is shifting the revenue center of the agricultural robots market size toward data analytics and predictive decision support.

Geography Analysis

North America held a 33.0% share in 2025, bolstered by large row-crop farms in the Midwest and high-value specialty crop operations in California, where the average hourly wage for hired labor was USD 19.52. The serial production of the Deere autonomous 8R tractor in 2024 provided corn and soybean growers with a commercial path to full-season driverless operation. Canada’s Prairie provinces introduced provincial rebate programs covering up to 30% of autonomous upgrades, increasing adoption in the wheat and canola sectors. Despite robust dealer networks, interoperability barriers among major brands temper growth because growers hesitate to lock into single-vendor ecosystems.

The Asia–Pacific region is projected to grow at a rate of 14.8% per year through 2031, the fastest regional pace. Japan faces a rapid demographic contraction, with the average age of farmers exceeding 68 years. To address this, the Ministry of Agriculture, Forestry, and Fisheries subsidizes autonomous rice transplanters capable of planting 10 hectares daily. China’s plan to achieve 30% smart-farming coverage by 2025 channels funds into domestic manufacturers such as FJDynamics, which shipped its five-thousandth autonomous mower, at a rate equivalent to the average hourly wage for the fastest-performing region in the Asia-Pacific region, enhancing collective autonomy. Australia leverages robotic weeders to counter herbicide-resistant ryegrass, and Carbon Robotics deployed 20 LaserWeeder units across Queensland and New South Wales in 2024.

In Europe, Germany, the Netherlands, and France together installed more than 10,000 Lely, DeLaval, and GEA milking robots in 2024, cutting labor hours by half and improving yield consistency. The Middle East and Africa, though comparatively smaller, are piloting robots in hydroponic greenhouses where water scarcity and heat stress limit human labor.

Regulatory Landscape

Safety, conformity, and data or repair rules are becoming more explicit for autonomous agricultural machinery, which increases the value of documented risk assessment and validation in global product rollouts. ISO published ISO 18497-4:2024 (July 2024), which sets verification methods and validation principles for partially automated, semi-autonomous, and autonomous agricultural machinery and tractors, supporting OEM and integrator efforts to formalize safety cases for field robots and driverless tractors.

In Europe, Regulation (EU) 2023/1230 (consolidated text updated May 2026) defines machinery safety obligations and includes provisions relevant to autonomous mobile machinery and machine-learning driven behavior. This shapes design controls, documentation, and conformity assessment planning ahead of its mandatory application date (20 January 2027). In the United States, the EPA (February 2026) clarified that the Clean Air Act does not restrict farmers and equipment owners from making their own repairs on nonroad diesel equipment, including units with advanced emissions controls, supporting fleet uptime for robotic and autonomous platforms deployed in time-sensitive field windows.

Competitive Landscape

The agricultural robots market exhibits moderate concentration, with the top five players, Deere & Company, DJI, CNH Industrial N.V., AGCO Corporation, and Lely, accounting for the majority of global revenue in 2025. Deere leverages a network of 1,500 dealers across North America to bundle autonomy upgrades with agronomic advisory, anchoring its ecosystem around the Operations Center cloud platform. DJI transfers consumer-drone scale efficiencies into agricultural models, claiming a 70% share of global ag-drone shipments in 2024. CNH Industrial integrated Raven Industries' guidance software after a USD 2.1 billion acquisition, deepening vertical control over hardware and telematics. Patent filings emphasize computer-vision algorithms and sensor fusion. Deere alone holds more than 200 active patents for precision spraying and autonomous navigation.

Start-ups remain vital in specialty niches. FarmWise and Naïo Technologies offer per-acre service models for high-density vegetable plots, providing flexibility that large equipment vendors currently lack. EcoRobotix’s solar-powered ARA robot cuts herbicide use by 95%, attracting European vegetable growers subject to strict pesticide regulations. Consolidation is anticipated to intensify as incumbents absorb niche innovators, mirroring Deere’s prior acquisition of Blue River Technology and AGCO’s purchase of Precision Planting.

Agricultural Robots Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Lely

DJI

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is forming around service-led deployment models and retrofit autonomy that reduce adoption friction for mid-tier farms that cannot justify full fleet replacement. Solinftec reported a sharp expansion of its US operational footprint in February 2026, including deployment of over 100 Solix autonomous robots and the debut of a commercial-ready autonomous Refill Station designed for continuous field operation, pointing to demand for end-to-end robotics systems that bundle hardware, software, and field logistics.

Public programs and targeted innovation funding are also widening pathways for robotics pilots and scaled procurement, especially where labor constraints and sustainability compliance intersect. The UK Defra added GBP 53 million (June 2026) to the Farming Innovation Programme with funding rounds that include agricultural robotics, and India added a state-level policy lever when the Government of Maharashtra approved the Automated Systems Policy-2026 (June 2026) to incentivize drones and robots in agriculture alongside training initiatives. On the product side, DJI Agriculture introduced the Agras T55 and T100 dual-battery spraying systems (July 2026), and these higher-throughput platforms support recurring analytics, fleet management, and input-reduction workflows that can produce audit-ready data for eco-schemes and precision-agriculture grant requirements.

Recent Industry Developments

- February 2026: Deere & Company announced its 2026 Startup Collaborator Program participants, including TorqueAGI and Aerobotics, to accelerate integrations spanning AI foundation models, autonomous robotics, and drone-based precision insights. The program expands Deere's partner pipeline for software and sensing capabilities that can be embedded into farm operations platforms, supporting faster commercialization across mixed task workflows.

- November 2025: AGCO highlighted new smart farming and autonomous solutions around Agritechnica 2025, including updates under its Fendt portfolio that reinforce autonomy and precision crop-care positioning. The announcements strengthened AGCO's automation-ready platform positioning and created additional touchpoints for bundling hardware with digital agronomy and autonomy toolchains.

- October 2024: Carbon Robotics raised USD 70 million in a Series D round led by NVentures and outlined plans to ramp production of its LaserWeeder platform that uses computer vision and CO2 lasers to eliminate weeds without chemicals. The funding enabled scaling of manufacturing capacity and field deployments for non-chemical weed control, aligning with tightening pesticide constraints and labor availability challenges.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers robots and closely linked control software used to automate on-farm work such as seeding, spraying, weeding, harvesting support, field scouting, and dairy automation. The market value is tracked as the annual revenue generated from these systems and related services across key farming regions.

Scope exclusions: Systems used only for post-harvest warehousing and pack-house material handling are excluded from this market sizing.

Segmentation Overview

- By Product Type

- Driverless Tractors

- Unmanned Aerial Vehicles and Drones

- Milking Robots

- Harvesting and Picking Robots

- Weeding Robots

- Others

- By Application

- Crop Farming

- Livestock Management

- Dairy Management

- Aquaculture

- Greenhouse Farming

- By Component

- Hardware

- Software

- Services

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on farming activity, labor constraints, and mechanization intensity, because these signals indicate where automation can scale. We mostly use public sources such as USDA datasets, FAOSTAT, Eurostat, and International Labour Organization series to anchor crop areas, farm labor availability, wages, and output trends.

To keep the model realistic by region, we also review sources such as customs and trade statistics portals, national agriculture ministries, and university extension publications that describe adoption barriers and operating practices, including spraying cycles and harvesting windows. Company filings, investor decks, patent databases, and reputable press are used to cross-check product roadmaps, pricing direction, and shipment momentum, and paid subscriptions for company financials and news are used where needed. This list is not exhaustive, and many other public references were reviewed to collect inputs, validate results, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk signals cannot fully explain, especially real-world utilization, price realization, and replacement cycles for different robot types. We speak with a mix of robot makers, component suppliers, dealers, farm operators, and service partners across APAC, EMEA, and the Americas, so assumptions can be checked across both open-field and controlled-environment farming.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 48% |

| Mid tier: 58% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 15% | Managers: 44% | Americas: 22% |

Market-Sizing & Forecasting

For the core sizing, we use a top-down build where the demand pool is reconstructed using mechanization intensity and task-level automation feasibility by region, then mapped to robot categories used on farms. After the regional totals are formed, we apply selective bottom-up approximations as a cross-check. This includes sampled price points times estimated unit volumes for key categories like UAVs, driverless tractors, and milking robots, followed by channel feedback to adjust outliers.

The model is guided by practical inputs such as cropped area under key crops, farm labor cost trends, dairy herd size and milking-parlor replacement cycles, average operating hours per season, and the share of farms using precision tools that make robots easier to deploy. Pricing is handled with a blended ASP logic by robot type and region, then refined using interview feedback on discounting, service attachments, and robotics-as-a-service contracts. When the bottom-up check has gaps, such as missing unit visibility in smaller regions, totals are balanced using proxy indicators like farm equipment spending growth and regional adoption curves.

Forecasts are produced using scenario analysis supported by a light multivariate regression, with adoption linked to labor cost pressure, farm income direction, and policy support signals. Assumptions are discussed with practitioners so the base case reflects what is actually being planned for procurement and deployment over the next few seasons.

Data Validation & Update Cycle

Validation is done through several checks so the final numbers do not depend on one data stream. We compare outputs against independent signals like agriculture equipment spending trends, regional crop and dairy activity, and import patterns where relevant, then investigate variances that look too high or too low.

Before sign-off, the model and its key assumptions go through internal analyst review, and follow-up calls are triggered when pricing, adoption, or regulatory cues change the story in a meaningful way. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery review is completed so clients receive the most current view.

Mordor Intelligence's Agricultural Robots Market Size Versus Other Published Estimates

Published market values for agricultural robots often do not match because scope lines are drawn differently, and the pricing math is handled differently across studies. The year chosen for currency conversion, the treatment of service revenue, and how fast average selling prices are allowed to move can each shift the total.

In practice, the biggest gaps come from whether UAV-related services are counted, whether robot software and support are bundled into the headline value, and whether estimates assume aggressive adoption in smaller regions without enough field checks. By keeping FX conversion timing consistent, refreshing ASP ranges with recent channel feedback, and rechecking totals against farm labor and mechanization indicators, Mordor Intelligence reduces drift that can build up when older price points and one-time assumptions are carried forward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.2 B (2025) | |

| Global Consultancy A | USD 17.09 B (2025) | This estimate appears to apply broader inclusion of offerings and may embed higher near-term price realization for hardware and software, which can lift the 2025 value even if unit adoption is similar. |

| Industry Publisher B | USD 18.52 B (2025) | The total likely assumes faster ASP progression and wider inclusion of controlled-environment and supporting revenue lines, and the longer forecast horizon can also encourage more aggressive early-year scaling assumptions. |

The table shows that even when the same year is cited, differences in pricing treatment, what is bundled into the market value, and how assumptions are refreshed can move the headline number by several billions. Our approach keeps the estimate traceable to a defined on-farm demand pool, with practical checks that help align pricing and adoption to what stakeholders report in the field.

Key Questions Answered in the Report

How large is the agricultural robots market in monetary terms in 2026?

The agricultural robots market size reached USD 18.0 billion in 2026.

What annual growth rate is anticipated for agricultural robots through 2031?

The market is projected to expand at an 18.07% compound annual growth rate, reaching USD 41.3 billion by 2031.

Which product class currently dominates sales of agricultural robots?

Unmanned aerial vehicles and drones lead with 36.0% revenue share in 2025 due to widespread use in scouting and precision spraying.

Which geographic region is forecast to be the fastest growing?

Asia-Pacific is set to grow at a CAGR of 14.8% through 2031, spurred by Japanese and Chinese government subsidies and labor shortages.

What business model is gaining traction among smaller farms?

Robotics-as-a-service, which converts capital cost into subscription payments, is accelerating adoption by small and mid-sized growers.

Page last updated on: