North America Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

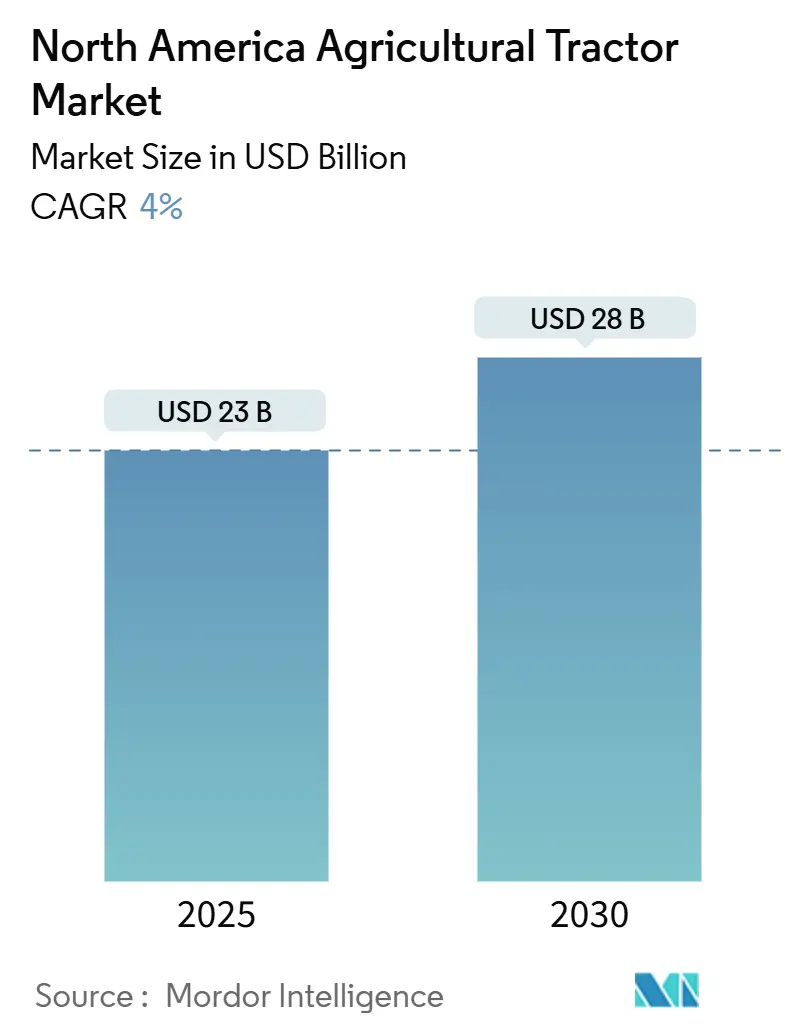

| Market Size (2025) | USD 23 Billion |

| Market Size (2030) | USD 28 Billion |

| Growth Rate (2025 - 2030) | 4.00% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Agricultural Tractor Market Analysis by Mordor Intelligence

The North America agricultural tractor market reached USD 23.0 billion in 2025 and is projected to grow to USD 28.0 billion by 2030, at a CAGR of 4.0%. Fleet replacement requirements, precision agriculture upgrades, and government financing initiatives help counterbalance cyclical market softening due to reduced commodity prices. Labor shortages in specialty and row-crop farming operations, along with equipment manufacturers' hardware-as-a-service options, maintain equipment demand despite increased interest rates. The United States holds the largest market share in 2024, while Mexico shows the highest growth potential through 2030, driven by a budget of USD 24.4 billion for PEC (Special Concurrent Program for Sustainable Rural Development) and USD 4.0 billion for SADER (Secretariat of Agriculture and Rural Development) in 2025 [1]Source: U.S. Department of Agriculture Economic Research Service, “Mexico: Policy,” ers.usda.gov. Market concentration remains high, though profitability faces pressure from increased warranty expenses related to connected and autonomous equipment.

Key Report Takeaways

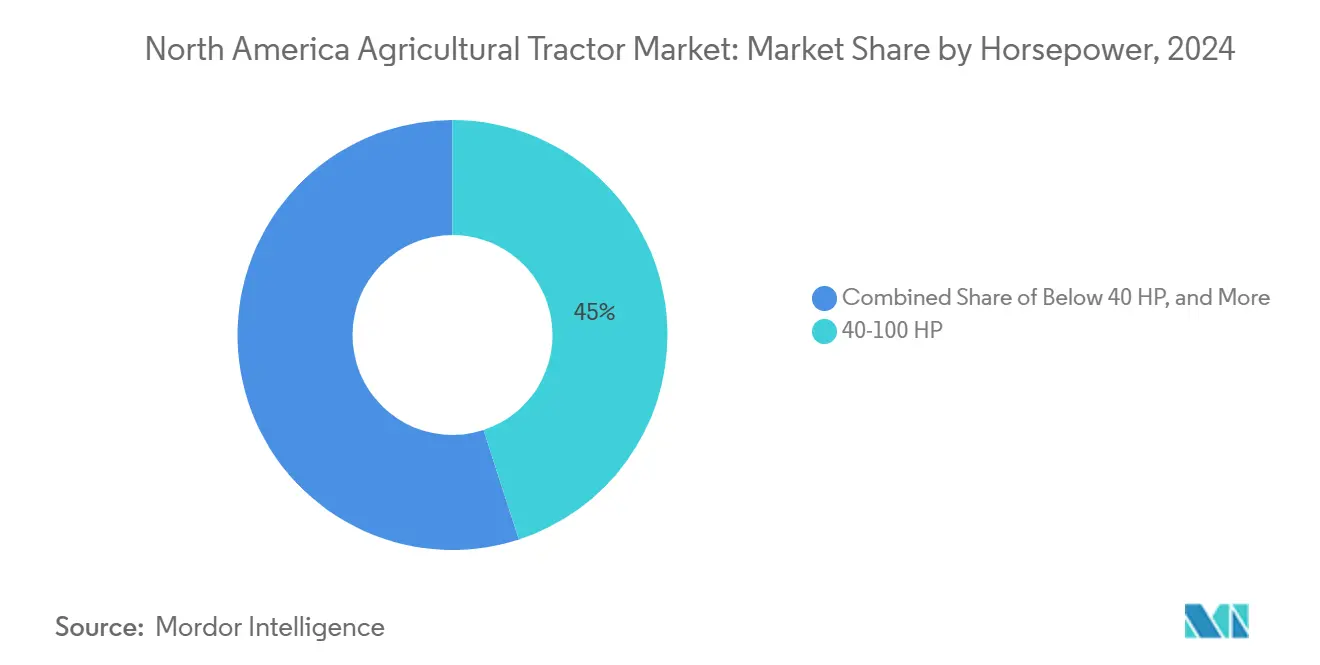

- By engine power, tractors with 40-100 HP dominated with 45% of the North America agricultural tractor market size in 2024, while tractors above 100 HP are growing at a 7.8% CAGR through 2030.

- By drive type classification, 2-wheel-drive tractors maintained 82% market share in 2024, with 4-wheel-drive variants growing at a 7.4% CAGR through 2030.

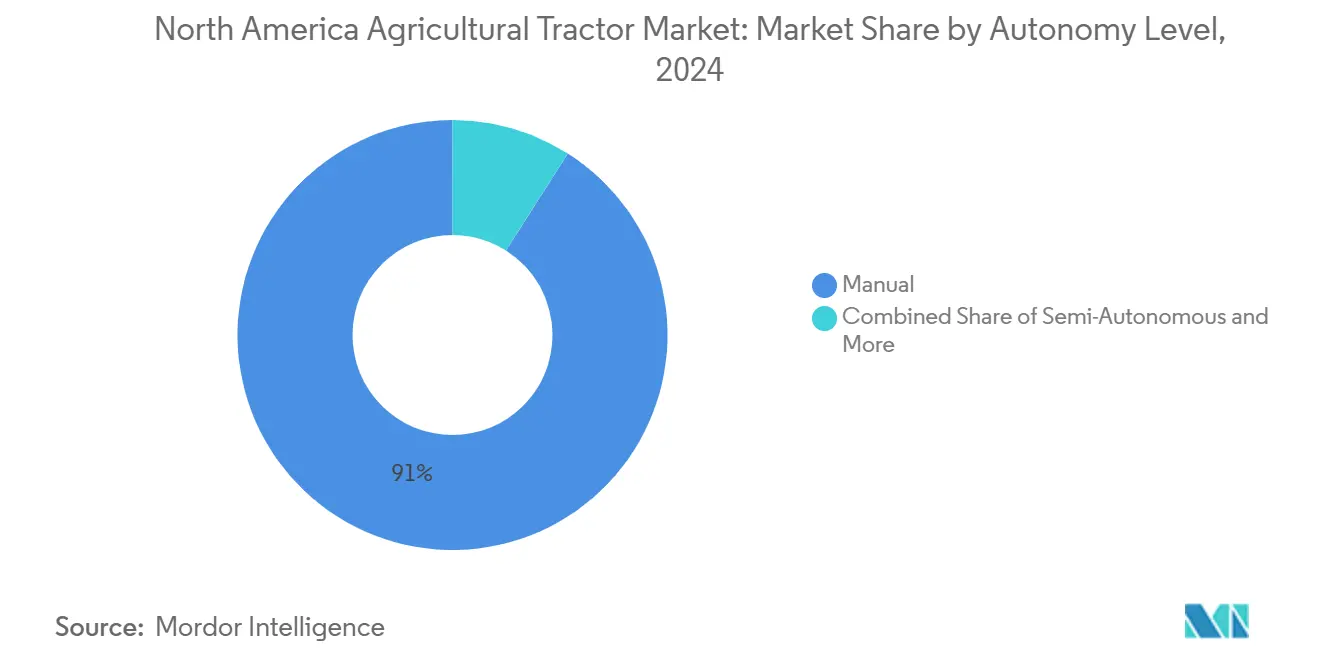

- By autonomy level, manual operation remains prevalent with 91% of the North America agricultural tractor market size in 2024, as fully autonomous systems demonstrate strong growth at 12.4% CAGR through 2030.

- By application, row-crop farming applications held a 58% share of the North America agricultural tractor market in 2024, with specialty and horticulture tractors growing at a 6.3% CAGR through 2030.

- By geography, the United States holds 75% of the North America agricultural tractor market size in 2024, with Mexico experiencing growth at a 5.7% CAGR through 2030.

North America Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Precision Agriculture and GPS-enabled Guidance | +0.8% | United States and Canada | Medium term (2-4 years) |

| Labor Shortage Accelerating Mechanization Uptake | +0.7% | North America | Short term (≤ 2 years) |

| Government Subsidies and Low-interest Equipment Loans | +0.5% | United States and Mexico | Medium term (2-4 years) |

| Surge in Demand for Higher-HP Tractors for Large Farms | +0.6% | United States and Canada | Long term (≥ 4 years) |

| OEM “Hardware-as-a-service” Subscription Models | +0.3% | North America | Long term (≥ 4 years) |

| Farm-data Monetization Driving Connected Tractor Sales | +0.4% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Precision Agriculture and GPS-enabled Guidance

Precision agriculture continues to expand, though significant portions of farms operate without advanced guidance systems. Recent investments from public and private sectors are reducing the technology adoption gap, particularly for farmers seeking to enhance yields and control input costs [2]Source: U.S. Government Accountability Office, “Precision Agriculture: Benefits and Challenges,” gao.gov. Large-scale operations derive the most benefit, as guidance system installation facilitates the integration of additional technologies, including sensors and prescription planting equipment. California strawberry producers have implemented computer-vision sprayers to minimize chemical application. While implementation costs and data management remain concerns, integrated solutions and improved return-on-investment analysis tools are facilitating broader market adoption.

Labor Shortage Accelerating Mechanization Uptake

Agricultural producers face persistent labor shortages, increasing the shift toward mechanization. Rising wages and housing expenses impact operational margins and reduce manual labor viability. In response, farmers are implementing mechanical harvesters that offer extended operational hours and collect operational data for route optimization. The labor shortage extends to equipment maintenance, as dealerships face difficulties recruiting qualified technicians. Equipment manufacturers are responding by developing virtual-reality training programs and apprenticeships to develop technical service professionals capable of maintaining advanced agricultural machinery.

Government Subsidies and Low-interest Equipment Loans

Government loan programs support farm modernization by reducing financial barriers. These programs provide flexible financing options through commercial banks and direct lending channels, enabling new and small-scale farmers to acquire machinery. In Mexico, rural development initiatives increase tractor and equipment demand through direct payments and price guarantees. Agricultural finance institutions' credit guarantees reduce lending risks, encouraging banks to finance purchases of advanced equipment with autonomous navigation and efficient propulsion systems.

Surge in Demand for Higher-HP Tractors for Large Farms

Farm consolidation drives demand for high-horsepower tractors to manage expanded operations efficiently. These tractors accommodate wider implements, increasing operational coverage rates. Despite increased availability of used equipment, demand persists for new models equipped with smart technologies, including variable-rate seeding and fleet management systems. Equipment manufacturers' trade-in programs facilitate fleet upgrades. This market development reflects the agricultural sector's transition toward data-integrated, high-capacity equipment supporting large-scale precision farming operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Maintenance Expenditure | -0.9% | North America | Short term (≤ 2 years) |

| Seasonal Volatility in Farm Incomes | -0.8% | North America | Short term (≤ 2 years) |

| Cyber-security and Data-privacy Risks in Connected Tractors | -0.5% | United States, Canada | Medium term (2-4 years) |

| Dealer-technician Shortage for Advanced Machinery | -0.6% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Maintenance Expenditure

The cost of high-horsepower tractors has increased significantly over the years, making new equipment purchases challenging for farmers. Electric models require additional investments in infrastructure, such as on-farm charging systems. Combined with increasing costs of fertilizer and pesticides, these financial pressures are impacting farm budgets. Consequently, farmers are extending the use of their existing machinery and purchasing used equipment through auctions instead of investing in new units.

Seasonal Volatility in Farm Incomes

Agricultural income varies considerably year-over-year due to fluctuating crop prices and weather conditions. This variability complicates planning for major capital investments, particularly during periods of reduced income. Farmers are increasingly utilizing financing options with flexible payment terms and seasonal payment deferrals. While these financial arrangements help manage cash flow, they result in slower new equipment sales, which affects manufacturing backlogs and delays technological adoption in the agricultural sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine power: Large Farms Drive High-HP Uptake

The 40–100 HP category generated 45% of the North America agricultural tractor market size in 2024, reflecting its versatility on mixed-crop farms. Above-100 HP machines are accelerating at a 7.8% CAGR as consolidation creates mega-acre operations demanding faster field coverage. Dealers report that software-ready premium cabs, integrated guidance, and higher PTO ratings enable growers to pull 24-row planters in a single pass, mitigating high fuel costs per acre. Yet abundant off-lease inventory has depressed residual values, stirring a buyers’ market that rewards farms with healthy balance sheets.

Strong uptake in the high-HP cohort underscores a technology-first replacement rationale: growers prefer fewer but more productive units equipped with variable tire inflation and hydraulic downforce control. Consequently, component suppliers are developing higher-torque transmissions and dual-clutch drivelines to handle heavier seeding toolbars without sacrificing transport speed.

By Drive Type: 4WD Adoption Accelerates

Two-wheel-drive equipment maintains 82% of unit sales due to lower acquisition cost and simplicity. These machines are preferred by smallholders and mixed-use farms for their maintenance simplicity and adaptability across different terrains. Four-wheel-drive tractors are growing at a 7.4% CAGR, driven by midwestern grain producers aiming to reduce soil compaction and operate larger strip-till implements. This trend indicates increasing demand for high-horsepower equipment capable of managing heavier implements and extended operations while preserving field conditions.

Manufacturers are responding with enhanced features, including lighter articulated frames, improved ballasting systems, and hydraulic flow rates above 435 liters per minute to accommodate high-demand planters. Fleet managers indicate that 4WD models provide improved turn radii and enhanced tractive efficiency in wet spring conditions, reducing fuel consumption by up to 6% on heavy soils. In response, leasing companies have expanded residual-value tables for articulated machines, improving 4WD accessibility through operating leases.

By Autonomy Level: Manual Still Reigns, Full Autonomy Accelerates

Manual operation represents 91% of revenue share in 2024, while fully autonomous systems are growing at a 12.4% CAGR, supported by retrofit solutions for existing tractors. Manufacturers are integrating advanced sensors in new models and providing subscription-based navigation software.

Semi-autonomous features, including auto-steer and automated headland turns, serve as transitional technology. Farmers report reduced fatigue during spraying operations and improved precision in field coverage. Full adoption faces delays due to regulatory uncertainty regarding uncrewed heavy equipment operation, though field-specific operating zones and geofencing are addressing safety concerns.

By Application: Row Crops Anchor Demand, Specialty Crops Accelerate

Row crops account for 58% of the North America agricultural tractor market share in 2024, primarily from corn, soybean, and wheat production. The horticulture tractors are growing at a 6.3% CAGR through 2030 as increased labor costs and year-round produce demand drive adoption of compact, maneuverable tractors with autonomous spraying capabilities.

Manufacturers are developing narrow chassis and high-clearance frames for precision applications in drip-fertigation and plastic-mulch management. Specialty units see additional demand from landscape contractors and municipal users. Plantation segments remain small but may expand through manufacturer partnerships near Central American fruit export regions.

Geography Analysis

The United States accounts for 75% of North America agricultural tractor market share in 2024, supported by extensive corn-belt farming operations and well-established dealership networks. The market faces current challenges from increased used equipment inventory, which has affected new model pricing and order volumes. The United States farmers maintain their position at the forefront of autonomous technology adoption, influenced by tightening emissions standards and growing interest in alternative power systems [3]Source: Environmental Protection Agency, “Greenhouse Gas Standards for Heavy-Duty Vehicles,” epa.gov. The country's agricultural scale, infrastructure, and innovation adoption rates establish it as the region's technology leader.

Mexico demonstrates the region's highest growth rate at 5.7% CAGR, driven by governmental agricultural modernization initiatives and expanded credit access programs. With mechanization levels at approximately one-third of U.S. standards, significant growth potential exists. Mexican farmers prefer mid-horsepower, versatile tractors suitable for both field operations and transportation. The country's manufacturing capability is strengthening through increased collaboration between local assemblers and global OEMs for knock-down kit production, improving domestic supply chain stability. This development reflects Mexico's focus on enhanced agricultural productivity and mechanical efficiency.

Canada's agricultural tractor market, while smaller in volume, demonstrates high technological adoption rates and leads the region in 4WD tractor implementation. Prairie-based farmers select high-traction equipment for operating heavy implements such as air drills, particularly in challenging soil conditions. Provincial incentives for climate-smart agriculture support telematics adoption for fuel consumption monitoring. The country has prioritized cybersecurity, implementing federal standards for farm equipment encryption. Canada's emphasis on precision agriculture, environmental sustainability, and digital technology integration establishes its position as an innovator in advanced farming practices.

Competitive Landscape

The North America agricultural tractor market maintains a consolidated structure, with five major Original Equipment Manufacturers (OEMs) dominating the industry revenue. Despite recent volume declines causing profit reductions across manufacturers, Kubota Corporation maintained its revenue through successful compact tractor sales and strategic financing programs. The market dynamics are influenced by established brand loyalty, extensive dealer networks, and product specialization, with manufacturers adapting to economic challenges through targeted promotions and product line adjustments.

The Original Equipment Manufacturers (OEMs) are implementing cost control measures and flexible manufacturing processes to enhance profit margins through streamlined parts management and expanded digital services. AGCO Corporation has increased its investment in precision agriculture technologies, while New Holland has established retrofit partnerships. Deere & Company continues to develop its smart spraying platform, incorporating machine learning into subscription-based services. These developments indicate an industry transition from traditional hardware sales to software-enabled solutions, with digital platforms becoming essential for customer retention.

The North American agricultural tractor industry is adapting its operational strategy, with manufacturers optimizing workforce numbers and developing software licensing models for consistent revenue streams. Dealerships are expanding technician training programs to resolve service issues and increase parts revenue, utilizing proprietary diagnostic systems. Environmental regulations, particularly regarding emissions standards, are driving the development of hybrid and electric tractor models. Manufacturers are establishing battery supply chains and developing compliance strategies to meet environmental requirements and market demands.

North America Agricultural Tractor Industry Leaders

Deere & Company

AGCO Corporation

CNH Industrial N.V.

Kubota Corporation

Mahindra & Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AGCO Corporation expanded its dealer network by integrating Carter Agri-Systems into Utah and launching Mississippi’s first full-line Fendt and Massey Ferguson dealership through Delta Ag Equipment. This expansion strengthens AGCO’s presence in key farming regions, improving access to advanced machinery and support services for North American farmers.

- January 2025: Deere & Company launched the Autonomous 9RX Tractor, equipped with 16 high-resolution cameras for 360-degree vision and autonomous operation in large-scale farming. This innovation boosts productivity and labor efficiency in North America’s expansive agricultural operations, especially during peak tillage seasons.

North America Agricultural Tractor Market Report Scope

| Below 40 HP |

| 40 -100 HP |

| Above 100 HP |

| 2-Wheel Drive (2WD) |

| 4-Wheel Drive (4WD) |

| Manual |

| Semi-Autonomous |

| Fully Autonomous |

| Row-Crop Farming |

| Specialty / Horticulture |

| Plantation and Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Engine power | Below 40 HP |

| 40 -100 HP | |

| Above 100 HP | |

| By Drive Type | 2-Wheel Drive (2WD) |

| 4-Wheel Drive (4WD) | |

| By Autonomy Level | Manual |

| Semi-Autonomous | |

| Fully Autonomous | |

| By Application | Row-Crop Farming |

| Specialty / Horticulture | |

| Plantation and Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America agricultural tractor market in 2025?

The North America agricultural tractor size is USD 23.0 billion in 2025, with a 4.0% CAGR leading to USD 28.0 billion by 2030.

Which horsepower range sells the most units?

The 40-100 HP bracket leads with 45% share because it suits mixed-use operations while remaining price-competitive.

What segment is growing fastest?

Fully autonomous tractors post the highest growth at 12.4% CAGR due to labor shortages and OEM retrofit kits.

Why is Mexico expanding faster than the United States?

Mexico benefits from a USD 24.4 billion modernization budget and subsidized credit, producing a 5.7% CAGR through 2030.

Page last updated on: