Transfection Technologies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

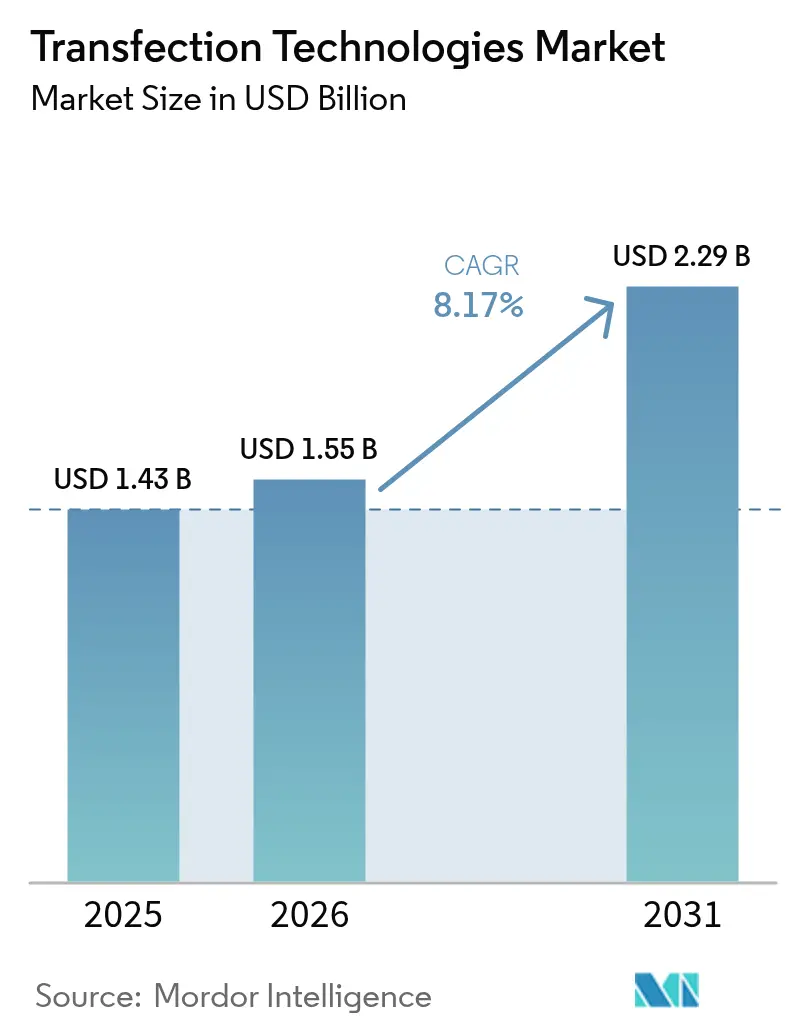

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 8.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transfection Technologies Market Analysis by Mordor Intelligence

Transfection Technologies market size in 2026 is estimated at USD 1.55 billion, growing from 2025 value of USD 1.43 billion with 2031 projections showing USD 2.29 billion, growing at 8.17% CAGR over 2026-2031. This trajectory reflects a rapid pivot from small-scale laboratory protocols toward scalable, cGMP-compliant platforms demanded by the gene and cell therapy sector. Uptake is paced by 37 FDA-approved gene therapy products that require high-efficiency, low-toxicity delivery of DNA, RNA, or protein cargos into primary cells.[1]Source: U.S. Food and Drug Administration, “Cellular and Gene Therapy Guidances,” fda.gov Instrument makers are automating electroporation, microfluidics, and lipid-nanoparticle workflows to satisfy commercial batch sizes that now exceed 200 billion cells. Top vendors differentiate through closed, single-use consumables that shorten validation cycles for mRNA vaccines, allogeneic CAR-T therapies, and in vivo CRISPR products. Regionally, United States and Canada maintain strong regulatory and manufacturing ecosystems, yet capital flows into Singapore, Japan, and China indicate a coming rebalance toward Asia-Pacific production hubs.

Key Report Takeaways

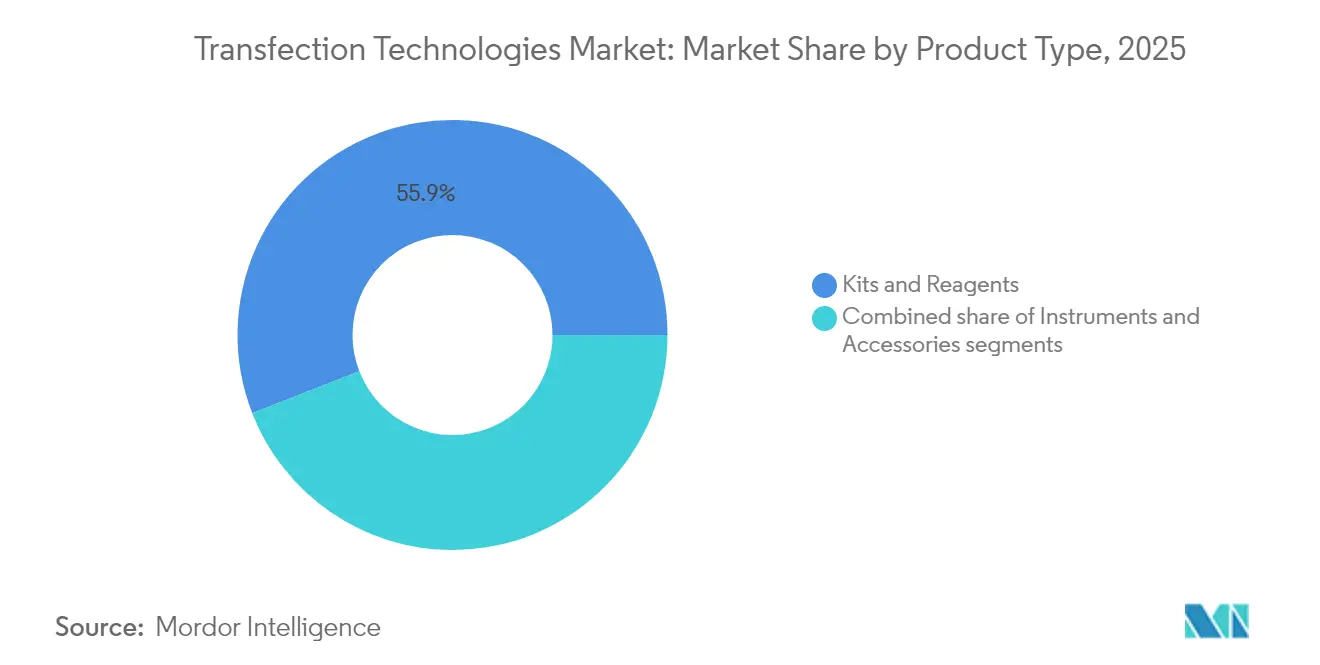

- By product type, kits and reagents led with 55.92% of transfection technologies market share in 2025, while instruments record the fastest 8.94% CAGR through 2031.

- By application, biomedical research held 43.10% revenue share in 2025; synthetic biology and genome engineering are projected to expand at a 9.28% CAGR.

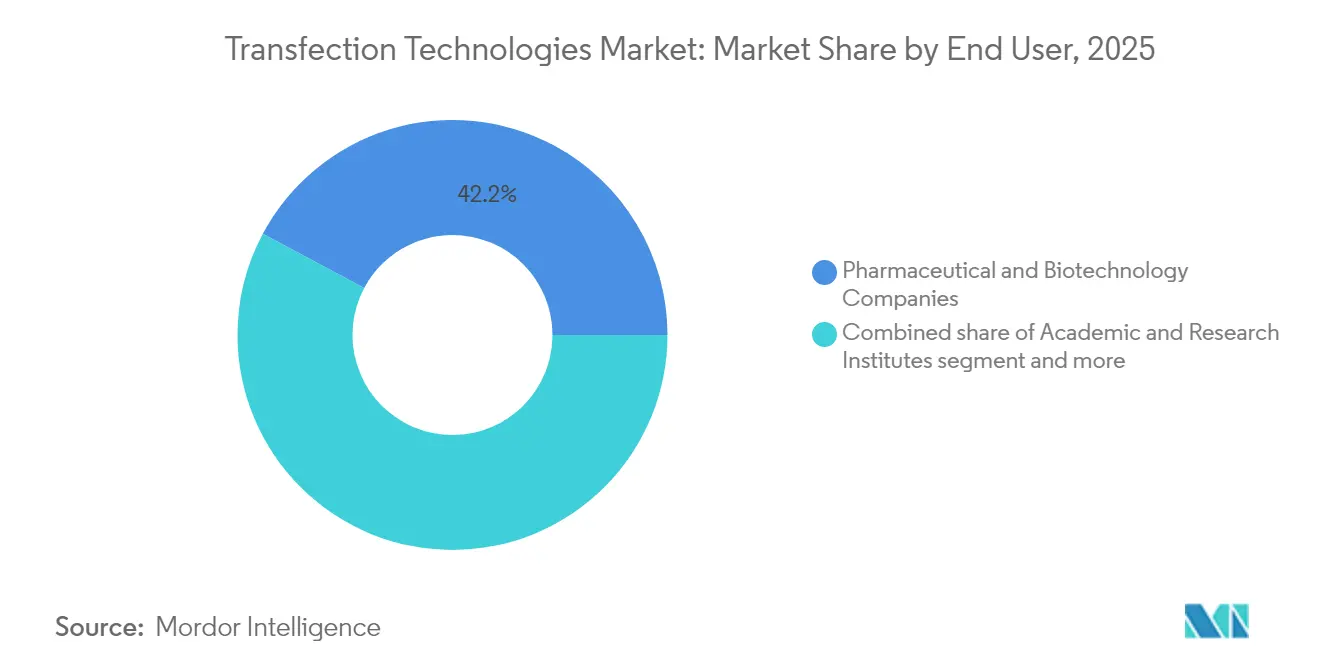

- By end user, pharmaceutical and biotechnology companies captured 42.20% of the transfection technologies market size in 2025, whereas academic institutes advance at a 9.46% CAGR.

- By geography, North America retained 38.40% of 2025 revenue, yet Asia-Pacific will outpace all regions with a 9.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transfection Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic diseases | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Expanding R&D in cell- & gene-based therapies | +2.1% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Growing demand for synthetic biology workflows | +1.5% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Government bio-foundry programmes | +1.2% | APAC core, with initiatives in North America | Long term (≥ 4 years) |

| mRNA-vaccine scale-up needs high-throughput transfection | +1.7% | Global, with early gains in US, Germany, Singapore | Short term (≤ 2 years) |

| Automation and standardization of manufacturing processes | +1.0% | Global, particularly North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Diseases

Cancer, neurological disorders, and inherited hematologic conditions are rising worldwide, pushing healthcare systems toward curative approaches based on gene transfer and genome editing. CAR-T pipelines alone require transfection platforms capable of 90% efficiency in primary T cells while maintaining ≥85% viability, a threshold now achieved with optimized electroporation buffers. Focused ultrasound-assisted CRISPR delivery is demonstrating precise in-brain editing without viral vectors, signalling new therapeutic frontiers. High treatment prices—CASGEVY lists at USD 2.2 million—justify capital investment in advanced instruments that compress production timelines from weeks to days.

Expanding R&D in Cell and Gene-Based Therapies

Global clinical activity exceeded 1,200 active trials in 2024, creating a robust funnel for commercial launches that rely on scalable, repeatable transfection protocols. Allogeneic cell banks magnify demand because a single manufacturing run can treat hundreds of patients, intensifying the focus on closed electroporation systems with process analytical technology. Long-term supply contracts—such as Lonza’s agreement to produce CASGEVY—illustrate how platform providers convert R&D momentum into multi-year revenue streams.

Growing Demand for Synthetic Biology Workflows

Bio-foundries automate design-build-test-learn cycles for organism engineering, generating high-throughput transfection needs across microbes, plant cells, and mammalian lines. The U.S. NSF committed USD 24 million to shared infrastructure in 2024, pooling robotics, analytics, and microfluidics that demand reagent optimization at scale.[2]Source: National Science Foundation, “BioFoundries Program,” nsf.gov Industrial players such as Ginkgo Bioworks outfit fermentation strains through multiplex genome edits that require consistent delivery across thousands of clones. With chemical manufacturing via synthetic biology projected to reach USD 39 billion by 2030, vendors that couple instruments with proprietary cationic-lipid chemistries gain early-mover advantage.

Government Bio-foundry Programmes

Strategic autonomy in biotechnology motivates nations to subsidize pilot plants and standardize regulatory pathways. The ARPA-H EMBODY program earmarked USD 50 million to automate cell-therapy production, specifically citing transfection bottlenecks.[3]Source: Advanced Research Projects Agency for Health, “EMBODY Program,” arpa-h.gov Singapore is funding self-amplifying mRNA platforms to secure domestic vaccine capacity, accelerating demand for high-throughput lipid-nanoparticle mixers. Such initiatives establish reference protocols that often become de facto industry standards, guiding vendor product roadmaps toward closed, disposable flow-cell architectures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of instruments | -1.4% | Global, particularly affecting smaller biotech firms | Medium term (2-4 years) |

| Cytotoxicity and low efficiency of legacy reagents | -1.1% | Global, with greater impact in cost-sensitive markets | Short term (≤ 2 years) |

| Complex cGMP plasmid supply chain bottlenecks | -0.9% | Global, with acute impact in North America & Europe | Medium term (2-4 years) |

| Regulatory scrutiny on gene-editing payloads | -0.8% | Global, led by North America & Europe regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Instruments

State-of-the-art electroporation skids exceed USD 500,000, placing advanced automation out of reach for many early-stage firms. Annual service contracts and single-use cartridges amplify total cost of ownership. Equipment-as-a-service models now spread that outlay over multi-year operating budgets, yet uptake remains modest. Contract development and manufacturing organizations relieve the burden, but slot constraints can delay IND filings by six months. Microfluidic chips fabricated through inexpensive laser engraving show promise to undercut capital costs while sustaining ≥90% transfection efficiency in suspension cells.

Cytotoxicity and Low Efficiency of Legacy Reagents

Widely used cationic-liposome systems often fall below 60% delivery efficiency in primary T cells and trigger apoptotic pathways that decimate yields. New ionizable lipids with optimized helper compositions reach 95% efficiency in hepatocytes, demonstrating translational potential for in vivo therapeutics. Acoustothermal and nanostraw approaches deliver similarly high performance while preserving membrane integrity, yet commercial adoption awaits consistent GMP manufacturing protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instruments Accelerate Automation

Kits and reagents maintained their dominant position with 55.92% market share in 2025, reflecting the recurring revenue nature of consumables and the specialized formulation requirements for emerging applications. However, instruments represent the fastest-growing segment at 8.94% CAGR through 2031, driven by automation imperatives in cell therapy manufacturing and the need for scalable platforms that can handle diverse cell types with consistent performance.

Industrial buyers evaluate platforms on cross-cell-type performance, integration with MES software, and validated cleaning protocols. Thermo Fisher’s 5 L DynaDrive bioreactor pairs with its neon electroporation device to form an end-to-end solution that trims process development time by 27%. As a result, the transfection technologies market size for instrument sub-segments is projected to expand faster than legacy reagent lines, capturing an incremental USD 445.3 million by 2031.

By Application: Synthetic Biology Reshapes Demand Curves

Biomedical research commanded 43.10% market share in 2025, yet synthetic biology and genome engineering applications post a 9.28% CAGR that will materially alter revenue composition. High-throughput design-build cycles in bio-foundries require platforms capable of transfecting 384-well plates in a single robotic run, spurring purchases of microfluidic flow-cell arrays. Transfection efficiency directly influences protein yield in transient expression systems, making delivery platforms a critical cost lever for contract protein producers.

The transfection technologies market size for synthetic biology workflows is on track to quadruple its 2024 baseline as CRISPR-Cas13 and base-editing modalities move into commercial pipelines. Diversification is visible in plant-cell engineering, where sonoporation with piezoelectric nanomaterials achieves 70% delivery efficiency, opening non-GMO crop traits that circumvent regulatory barriers. The breadth of emerging targets forces vendors to support both suspension and adherent cultures, microbial strains, and hard-to-transfect primary cells.

By End User: Academia Gains Momentum

Pharmaceutical and biotechnology firms command 42.20% of spending, motivated by submission-ready data packages that hinge on fully characterized transfection processes. Academic and research institutes, however, register a 9.46% CAGR as public funding programs equip shared facilities with next-generation delivery platforms. The transition matters because graduate students trained on a particular system often champion that brand when they migrate to industry, reinforcing platform lock-in.

Contract development organizations bridge capability gaps for virtual biotech start-ups; yet supply-chain turbulence, especially in GMP plasmids, can extend project timelines. The transfection technologies market share held by contract manufacturers will therefore rise modestly but remains capped by sponsor preference for intellectual-property control. Hospitals exploring ex vivo gene editing at the point of care create a nascent channel that favors compact, closed cartridges with minimal user intervention.

Geography Analysis

North America retained 38.40% of 2025 revenue thanks to strong venture investment, FDA guidance that clarifies chemistry-manufacturing-control expectations, and a network of specialized CDMOs. The region’s dominance in mRNA vaccine scale-up taught process engineers to apply lipid-nanoparticle formulations to therapeutic payloads beyond infectious disease. Nevertheless, labor shortages and high facility overheads sustain interest in lights-out manufacturing suites that reduce operator exposure.

Asia-Pacific is the fastest-growing territory, expanding at a 9.88% CAGR. Singapore’s Cell Therapy Facility offers subsidized GMP suites, while Japan’s Moonshot R&D program subsidizes electroporation studies that ensure higher delivery rates in induced pluripotent stem cells. China’s synthetic-biology parks push for 1,000-strain per month design capacity, driving bulk procurement agreements for lipid-nanoparticle reagents.

Europe remains a mature but cautiously expanding arena. Germany leverages messenger-RNA manufacturing expertise from its vaccine boom to pivot toward rare-disease therapeutics, while EMA guidance on genetically modified cells harmonizes quality expectations across member states. Stringent GMO regulations slow agricultural applications, yet attractive research funding offsets some regulatory friction.

Regulatory Landscape

Regulation of transfection technologies is framed around how reagents, instruments, and ancillary materials are qualified within cell and gene therapy (CGT) manufacturing, rather than stand-alone product approvals. In the United States, FDA oversight for CGT products sits primarily within CBER (including the Office of Tissues and Advanced Therapies), and CMC expectations for manufacturing changes and comparability shape how transfection-critical inputs are documented, controlled, and requalified across a product lifecycle. The market context includes 37 FDA-approved gene therapy products, which increases scrutiny of non-viral delivery steps and their associated raw materials used in commercial and late-stage supply.

In Europe, transfection reagents and related inputs are typically managed as ancillary or critical raw materials under the ATMP framework (including Regulation (EC) No 1394/2007) and GMP expectations in EudraLex, which puts emphasis on supplier qualification and traceability. Standardization is also advancing through ISO biotechnology workstreams, including ISO 23511:2026 (published June 2026) on cell line identification and cross-contamination testing, and ISO 20399-4 (ancillary materials CoA/CoO requirements) progressing through the DIS stage in April 2026. These developments support cGMP-aligned documentation (such as certificate of analysis and origin), tighter impurity and bioburden controls, and harmonized testing packages that reduce audit friction across global manufacturing footprints.

Value Chain Analysis

The value chain runs from raw material suppliers (lipids, polymers such as PEI, buffers, enzymes), to plasmid DNA and mRNA input providers, through to manufacturers of kits, reagents, instruments, and single-use consumables that enable delivery into primary and engineered cells. This upstream layer feeds end users and integrators, including pharmaceutical and biotechnology manufacturers, academic core labs and bio-foundries, and CRO/CDMO networks that operate cGMP suites for cell therapy and viral vector programs. Scale-up pushes buyers toward closed, disposable cartridges, validated electroporation assemblies, and standardized reagent packs that simplify change control and comparability as programs move from research to manufacturing.

Key constraints in the chain concentrate around cGMP plasmid availability and variability-sensitive transfection reagents. Plasmid DNA can represent a large share of raw-material spend, and instability of transfection complexes can propagate downstream into purification burdens and higher empty capsid loads. Industry responses include vertical integration and tighter supplier ecosystems, illustrated by the March 2026 strategic partnership between Porton Advanced and T&L Biotechnology to link upstream CGT raw materials with downstream CDMO execution. Regulatory-facing documentation strategies are also visible, such as Yeasen Biotechnology registering a GMP-grade UltraAAV transfection reagent in the FDA DMF system (July 2025). Distribution is dominated by direct-to-key-account sales for instruments and high-value reagents, supported by specialized life-science channel partners that extend reach for lab-scale adoption and recurring consumables pull-through.

Competitive Landscape

Competitive intensity is moderate, with platform strategies dictating share shifts. Merck KGaA’s USD 600 million acquisition of Mirus Bio underscores consolidation aimed at combining lipid-nanoparticle expertise with global distribution. MaxCyte holds 29 strategic platform licenses, covering oncology, regenerative medicine, and autoimmune indications, locking partners into royalty arrangements that extend to commercial sales.

Thermo Fisher and Cytiva compete on integrated bioprocess suites that combine transient expression bioreactors with automated electroporation skids. Polyplus, now under Sartorius, diversifies into helper plasmids that complement its reagent line, aiming to capture a larger slice of per-dose cost in AAV vector production. Start-ups such as Cellares and Terumo refine closed, modular systems that shorten end-to-end CAR-T production from 14 days to 36 hours.

Competitive differentiation now turns on real-time analytics, process digital twins, and turnkey cGMP documentation. Vendors that package software with hardware and consumables gain recurring revenues while easing customer audits. White-space opportunities persist in agricultural biotechnology and decentralized clinical settings, where small-footprint devices paired with lyophilized reagents could unlock new user segments. High-performance non-viral delivery chemistries and acoustothermal devices represent nascent threats to conventional electroporation leadership, but regulatory familiarity with electroporation sustains its near-term advantage.

Transfection Technologies Industry Leaders

Lonza Group

Bio-Rad Laboratories, Inc.

Thermo Fisher Scientific

Qiagen NV

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial CGT manufacturing is creating whitespace for transfection platforms that reduce reliance on transient methods while preserving development speed, and recent offerings reflect that shift. Lonza launched the Xcite AAV stable producer cell line platform (May 2026), highlighting a pathway to lower variability and simplify scale-up in AAV supply chains where transient transfection is a known bottleneck. Quality control and release testing are also becoming more closely tied to delivery workflows, as Bio-Rad Laboratories launched Vericheck ddPCR kits (July 2026) to address mycoplasma, empty-full capsid, and residual DNA quantification needs in cell and gene therapy manufacturing.

Method-level technology opportunity is expanding as well, especially for hard-to-transfect primary cells and multiplex payload delivery. Peer-reviewed 2026 research on microfluidic platforms for sequential delivery, including acoustic-electric shear orbiting poration and nanoparticle co-assembly strategies intended to improve serum stability and transfection in non-activated primary T cells, supports ongoing productization of higher-viability, high-efficiency non-viral delivery. Manufacturing-oriented workflows are also moving toward higher-density and more continuous operation, including perfusion-enabled transfection and increased use of process analytical technology in vector bioprocessing. This, in turn, increases demand for automated instruments, standardized consumables, and reagent lots with tighter performance windows across sites and programs.

Recent Industry Developments

- July 2026: Bio-Rad Laboratories launched a portfolio of Vericheck ddPCR kits compatible with the QX700 system, covering assays such as mycoplasma detection, empty-full capsid analysis, and residual DNA quantification for biopharma and cell and gene therapy workflows. The release strengthens in-process and release-testing toolkits around transfection-intensive manufacturing steps, increasing the need for integrated analytics alongside delivery platforms.

- May 2026: Lonza launched the Xcite AAV stable producer cell line platform to industrialize AAV manufacturing by reducing reliance on transient transfection. The platform supports a shift toward more repeatable vector output and tighter cost-of-goods control, shaping how manufacturers balance speed-to-clinic with long-run scalability.

- July 2025: Lonza announced the 4D-Nucleofector LV Unit PRO, a large-scale electroporation system using Nucleocuvette Cartridges PRO for GMP manufacturing, including T cell transfection use cases. The launch expands options for closed, manufacturing-oriented non-viral delivery, reinforcing the move from benchtop protocols to standardized production equipment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the global revenue generated from technologies used to introduce DNA or RNA into cells for lab research, bioprocess workflows, and therapeutic development, including reagents, kits, and related instruments.

Scope exclusions: We exclude general cell-culture plastics and consumables that are not specific to transfection work so totals do not get inflated by broader lab spend.

Segmentation Overview

- By Product Type

- Kits and Reagents

- Instruments

- Accessories

- By Application

- Biomedical Research

- Therapeutic Delivery

- Protein Production

- Synthetic Biology and Genome Engineering

- Other Applications

- By End User

- Academic and Research Institutes

- Pharmaceutical and Biotechnology Companies

- CROs and CMOs

- Hospitals and Clinical Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand story and to anchor assumptions that can be checked year after year. We relied on public science and health sources such as the NIH and NCBI (for publication volumes and research themes), the FDA and EMA (for therapy pipeline direction and approvals), the OECD and World Bank (for macro and R&D context), and trade bodies and standards groups that publish lab practice guidance and definitions.

To connect demand signals to revenues, we also reviewed company annual reports, investor presentations, product catalogs, and reputable press coverage around new launches and capacity expansions. Where needed, we referenced paid subscriptions for company financials and intelligence, patent databases, and an import-export shipment-level dataset to sense-check pricing and cross-border movement of specialized reagents and instruments. These sources are illustrative, and additional public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on experienced users and suppliers across the transfection value chain so that assumptions from desk research could be corrected with what is actually bought and used. We spoke with stakeholders from reagent and instrument providers, distributors, core labs, biopharma teams, and contract partners, and coverage was balanced across major regions to reflect differences in funding, adoption, and regulatory pace. Respondent input was used to confirm adoption by application, typical workflow mix, and how pricing shifts with scale and method.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 49% |

| Mid tier: 45% | Functional/Unit leaders: 33% | EMEA: 32% |

| Smaller Players: 16% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started with a top-down build where the total demand pool was reconstructed from research activity and bioprocess signals that directly drive transfection usage, and then translated into spend using price and workflow intensity assumptions. In practice, the model leans on indicators such as funded life-science research trends, cell and gene therapy pipeline momentum, growth in cell-line development programs, method shifts between chemical and physical transfection, and the mix between consumables and instruments (since recurring reagent purchases behave differently from capital equipment).

Those totals were then corroborated with selective bottom-up approximations, including supplier revenue benchmarks where available, sampled ASP times volume checks for common reagent categories, and channel feedback on instrument placements and replacement cycles. When an input could not be observed cleanly, we used a conservative range, tested it against interview feedback, and then tightened it only after the output aligned with multiple demand signals.

For forecasting, scenario analysis was used to reflect how the market moves under different adoption speeds for newer workflows, along with expected R&D funding direction and therapy pipeline conversion. The final yearly path was adjusted only when it remained consistent with the variables above and with what primary respondents described as realistic purchasing behavior.

Data Validation & Update Cycle

Validation was done through repeated cross-checks so that no single source drives the final number. Outputs were compared against independent signals like publication intensity, therapy pipeline changes, instrument placement trends, and pricing movement, and then reviewed for outliers by a second analyst before sign-off.

If a large variance appeared by region, product, or application, follow-up outreach was triggered to re-check the assumption that caused the swing. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, pricing shocks, or meaningful technology launches. Before delivery, we run a fresh review pass to ensure the latest publicly available updates are reflected.

Mordor Intelligence's Global Transfection Technologies Market Market Estimate Compared With Other Published Estimates

Published market sizes for transfection technologies do not always match because groups draw the line around different product baskets, treat viral-vector related spending differently, and apply different pricing and adoption curves when forecasting. Differences also come from how currency conversion is timed and whether the base year is refreshed using the newest pipeline, funding, and method-mix signals.

Viral vector manufacturing-only consumables sit outside Mordor Intelligence's scope, which explains why some totals look higher when adjacent gene delivery spend is blended into transfection line items. Another common gap is how instrument revenue is handled, since some estimates push more of the installed base into the current-year number without checking replacement cycles and utilization. We reduced these gaps by tying the model to observable demand drivers like research activity, bioprocess scale-up, and method adoption, and then stress-testing the output with interview-based pricing and workflow checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.43 B (2025) | |

| Industry Research Publisher A | USD 1.35 B (2025) | Uses a broader product taxonomy but appears to apply more conservative uptake for newer physical methods and keeps slower ASP progression, which pulls down the 2025 value even with similar base-year timing. |

| Industry Research Publisher B | USD 1.35 B (2025) | Does not clearly separate transfection-specific consumables from nearby gene delivery and vector-related workflows across all regions, and the slower growth path suggests a more cautious scenario set for therapy-driven demand. |

The table shows that the spread is mostly explained by what gets counted as transfection-specific spend and how fast method mix and pricing are assumed to move. By keeping inclusions clear, anchoring on repeatable demand indicators, and confirming the sensitive assumptions through primary checks, the market number stays easier to trace and re-run when new data arrives.

Key Questions Answered in the Report

What is the current size of the transfection technologies market?

The transfection technologies market is valued at USD 1.55 billion in 2026 and is projected to reach USD 2.29 billion by 2031.

Which product segment is growing fastest?

Instruments grow at 8.94% CAGR because automated electroporation and lipid-nanoparticle mixers streamline commercial cell-therapy manufacturing.

Which region will expand most rapidly?

Asia-Pacific leads growth with a 9.88% CAGR, driven by government-funded bio-foundries and mRNA manufacturing hubs.

How are high instrument costs being mitigated?

Equipment-as-a-service contracts, shared GMP suites, and emerging low-cost microfluidic devices help smaller firms access advanced technology without large upfront outlays.

What advances are reducing cytotoxicity in transfection?

Next-generation ionizable lipids, acoustothermal delivery, and nanostraw-based electroporation achieve efficiencies above 90% while maintaining high cell viability.

Page last updated on: