Non-thermal Pasteurization Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

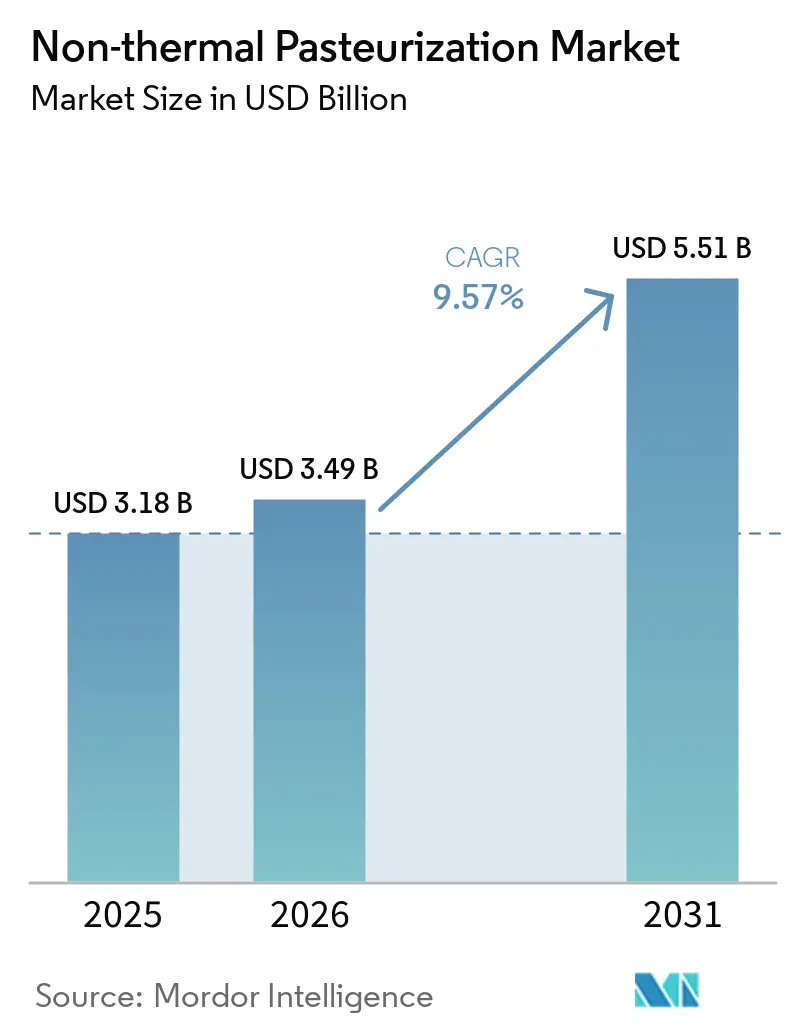

| Market Size (2026) | USD 3.49 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 9.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-thermal Pasteurization Market Analysis by Mordor Intelligence

The non-thermal pasteurization market size was valued at USD 3.18 billion in 2025 and estimated to grow from USD 3.49 billion in 2026 to reach USD 5.51 billion by 2031, at a CAGR of 9.57% during the forecast period (2026-2031). The non-thermal pasteurization market encompasses equipment, contract processing services, and tolling operations for HPP, PEF, MVH, ultrasonic processing, and irradiation, serving food and beverage manufacturers, pharmaceutical producers, and nutraceutical companies. Demand in the non-thermal pasteurization market is being shaped by the shift toward clean-label, minimally processed products, as many premium categories can no longer tolerate the quality loss associated with heat treatment. HPP remained the leading technology in the non-thermal pasteurization market in 2025, helped by its established role in U.S. food safety practice, where FDA and USDA-FSIS recognition has made commercial adoption easier in juices, seafood, and ready-to-eat meat applications. North America led the non-thermal pasteurization market because it has the deepest installed HPP base and the broadest tolling access, while Asia-Pacific is set to grow the fastest as China formalizes equipment standards and product-level requirements for HPP processing. The non-thermal pasteurization market is also gaining support from tighter pathogen-control expectations, wider use of tolling and Equipment-as-a-Service models, and rising interest from pharmaceutical and nutraceutical manufacturers that need microbial control without heat damage to sensitive compounds.

Key Report Takeaways

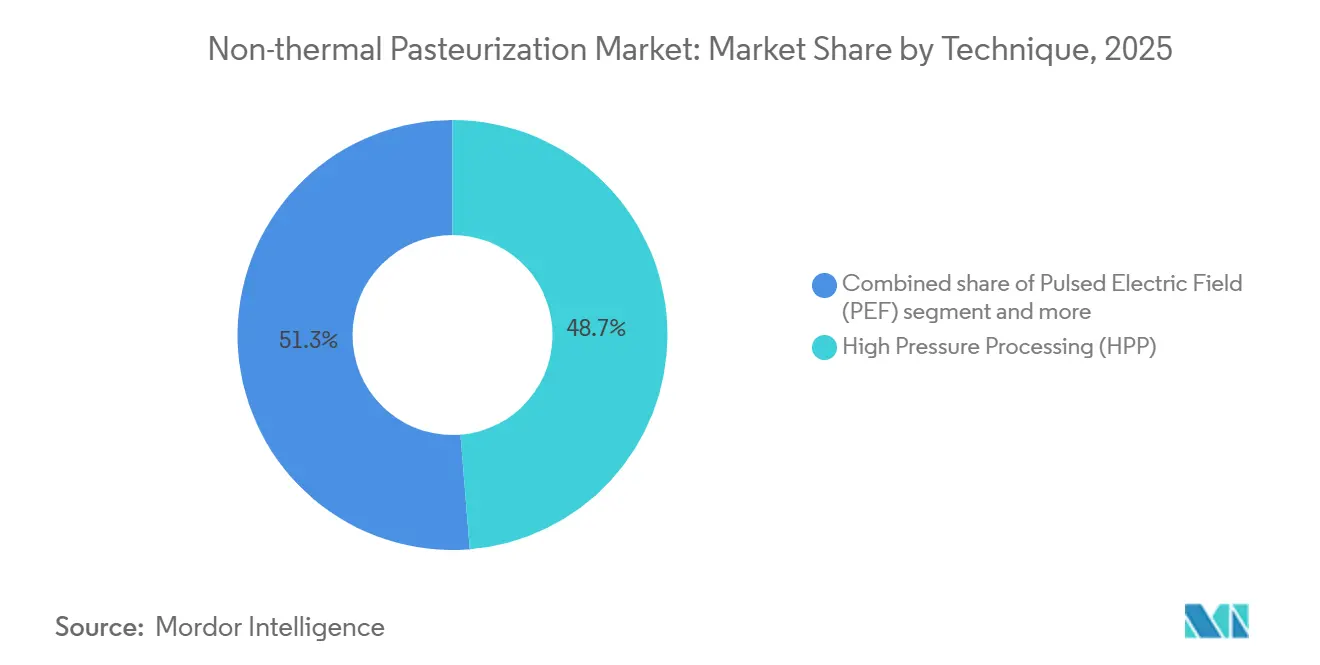

- By technique, High Pressure Processing (HPP) retained 48.73% share in 2025, whereas Pulsed Electric Field (PEF) is forecast to expand at a 10.67% CAGR through 2031.

- By form, liquid led the non-thermal pasteurization market with a 62.56% share in 2025, while semi-solid is anticipated to register the fastest CAGR of 10.37% during 2026-2031.

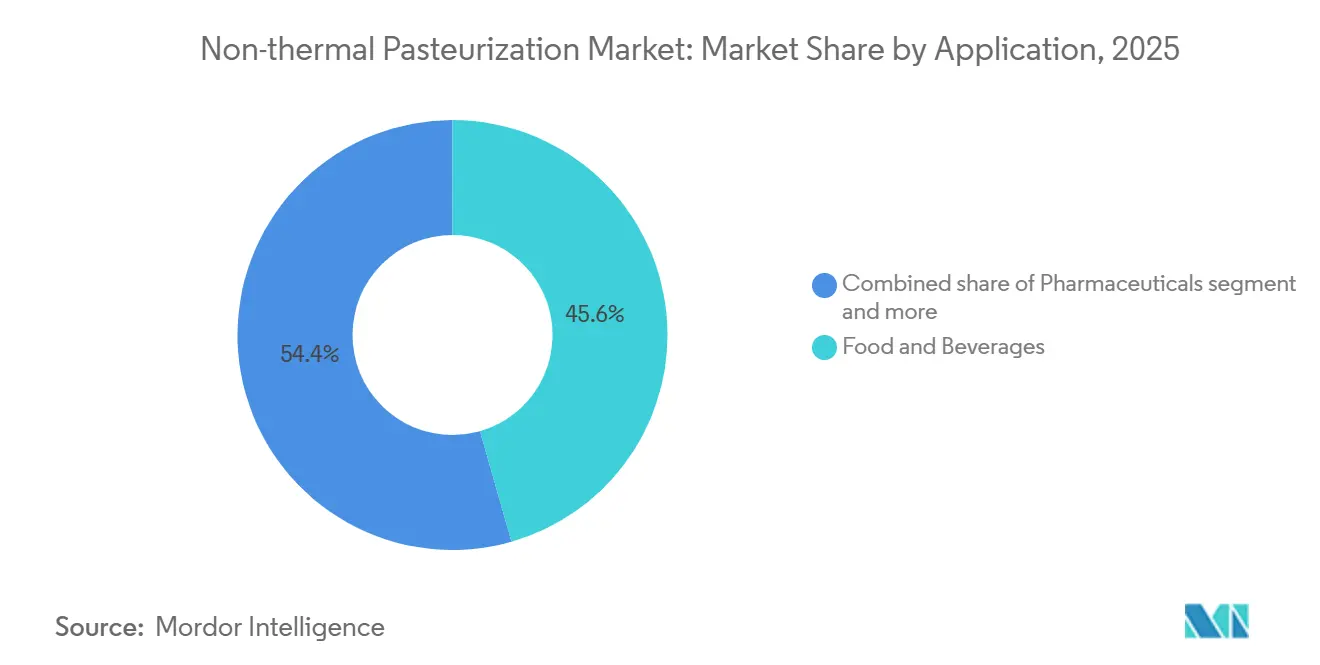

- By application, food and beverages held 45.58% of 2025 revenue, but pharmaceuticals are expected to grow fastest at 10.86% through 2031.

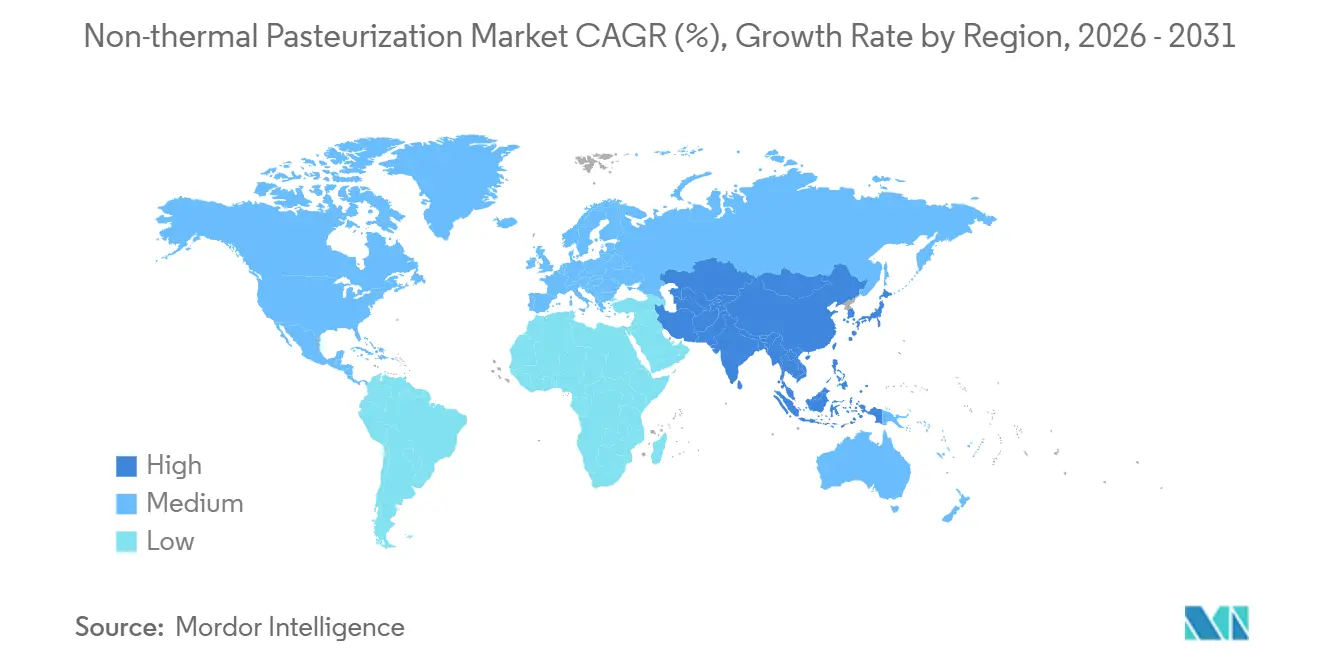

- By geography, North America accounted for the largest share of the non-thermal pasteurization market, at 32.36% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 11.38% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non-thermal Pasteurization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Clean-Label and Minimally Processed Foods | +2.1% | Global, led by North America and Western Europe, with growing pull in APAC urban centers | Medium term (2-4 years) |

| Shelf-Life Extension Without Thermal Damage | +1.8% | Global, strongest in APAC cold-chain expansion markets and South America export corridors | Long term (≥ 4 years) |

| Food Safety Compliance and Pathogen Control Pressure | +1.6% | North America and Europe, with regulatory formalization emerging in Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Cold-Chain Premium Beverage Formats | +1.2% | North America, Western Europe, and East Asia | Medium term (2-4 years) |

| Equipment-as-a-Service Models Lowering Adoption Barriers | +0.9% | North America core, expanding to Europe, Asia-Pacific, and South America | Short term (≤ 2 years) |

| Rising Use of HPP in Meat and Seafood Processing | +1.0% | North America, South America, and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label, minimally processed foods

Consumer-led pressure on ingredient transparency is acting as a structural tailwind for the non-thermal pasteurization market in a way that traditional food safety economics alone cannot explain. A 2025 survey by the International Food Information Council (IFIC) found that the share of US consumers defining "healthy food" as "minimally or no processing" increased from 20% in 2022 to 28% in 2025, with "limited or no artificial ingredients or preservatives" rising from 18% to 25% over the same period[1]Source: Penn State Extension, “Food Trends 2026,” Penn State Extension, extension.psu.edu. This shift has direct commercial consequences: HPP and PEF-processed products command retail price premiums that offset the processing cost premium, improving unit economics at scale. The critical but under-appreciated insight here is that clean-label demand is not a homogeneous consumer trend; it is being reinforced by institutional buyers, including foodservice operators and retailers, who are imposing clean-label supplier specifications, creating a B2B pull that reaches further into the supply chain than consumer surveys suggest. Lyras A/S's UV-based pasteurization technology, which saves 60-90% in energy and 60-80% in water use compared to thermal pasteurization, has been adopted by Novozymes, a global industrial enzyme leader, precisely because its clean, non-thermal processing profile aligns with corporate sustainability claims. The knock-on effect is visible in PEF research output, where publications in peer-reviewed journals examining PEF's ability to produce preservative-free plant-based milks and beverages nearly doubled between 2019 and 2025.

Shelf-life extension without thermal damage

Shelf-life extension through non-thermal processing offers a materially different value proposition than conventional preservation, as it eliminates the trade-off between food safety and sensory quality. HPP applied at pressures of 400-600 MPa inactivates vegetative pathogens without triggering the Maillard reaction or degrading heat-sensitive enzymes and vitamins, enabling the production of products with shelf lives 3 to 6 times longer than untreated equivalents while retaining a fresh-like profile. The strategic implication is that non-thermal pasteurization effectively expands the addressable geographic market for premium perishable goods by closing the logistics gap that previously made long-haul or export distribution of fresh products uneconomical. JBT Marel's Avure Technologies published research findings in February 2025 confirming that HPP processing preserves bioactive compounds, including heat-sensitive vitamins and phytonutrients, at levels significantly higher than those achieved with thermal treatment across multiple produce categories. For retail and foodservice buyers operating on just-in-time replenishment cycles, extended shelf life without additives is a direct inventory management benefit that reduces food waste and write-down risk. The secondary commercial effect, less remarked upon, is that shelf-life extension through HPP allows manufacturers to enter cold-chain markets in APAC and South America that lack the infrastructure density for rapid inventory turnover.

Food safety compliance and pathogen control pressure

Tightening regulatory enforcement is proving to be the single fastest-acting driver for HPP adoption in North America's RTE meat and poultry sector. In December 2024, USDA-FSIS announced that, effective January 2025, it would expand its Listeria testing protocols to include all Listeria species, not just L. monocytogenes, across RTE products, food contact surfaces, and environmental samples[2]Source: U.S. Department of Agriculture Food Safety and Inspection Service, “FSIS Announces Stronger Measures to Protect the Public From Listeria Monocytogenes,” USDA FSIS, fsis.usda.gov. Crucially, the agency simultaneously announced prioritized Food Safety Assessments for facilities that rely exclusively on sanitation measures to control Listeria, creating a direct regulatory incentive to implement a validated post-lethality treatment such as HPP, which qualifies under Alternative 1 or Alternative 2 of the Listeria Rule (9 CFR Part 430). This enforcement shift materially changes the risk calculus for RTE meat processors: the cost of an FSIS-initiated Food Safety Assessment and associated compliance exposure now compares unfavorably to the cost of HPP adoption, particularly when tolling services eliminate the capex requirement. The regulatory drag from the Boar's Head Listeria outbreak review, which prompted the National Advisory Committee on Microbiological Criteria for Foods (NACMCF) to begin examining existing Listeria policy with recommendations expected in 2026, indicates that regulatory stringency is likely to intensify rather than ease. For equipment suppliers and HPP tollers, this enforcement cycle effectively functions as a demand stimulus that is government-generated and time-bound.

Expansion of cold-chain premium beverage formats

The premium beverage segment, cold-pressed juices, functional shots, plant-based milks, and kombucha-adjacent fermented drinks, has become the single largest source of new HPP equipment installations globally, accounting for 37% of Hiperbaric's 2025 machine installations by sector. This is not simply volume growth; it represents a category-level transformation in how beverage manufacturers position non-thermal processing as a brand attribute rather than merely a food safety intervention. The Cold Pressure Council, the industry standardization body convened by PMMI, The Association for Packaging and Processing Technologies, has formalized the "High Pressure Certified" mark as the sector's primary third-party consumer-facing claim, with member brands deploying it across North American, European, South American, and Asian markets. Beverage producers in South Korea, Singapore, Japan, and Australia are among the fastest-growing adopters, leveraging HPP to meet both domestic and export market clean-label requirements simultaneously. A less visible but commercially significant development is that major foodservice chains are beginning to specify HPP for fresh-pressed juices and premium sauce ingredients as part of supply-chain food-safety requirements, converting what was previously a retail-sector demand pattern into an institutional procurement requirement. The emerging tension between HPP-processed beverage positioning and the FDA prohibition on labelling HPP-pasteurised juices as "fresh" in the United States remains an unresolved regulatory blind spot that constrains marketing optionality for US operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity for HPP and PEF Installations | -1.5% | Global; most acute in emerging markets (APAC, MEA, South America) and among SME food manufacturers | Long term (≥ 4 years) |

| Validation, Packaging, and Line-Integration Complexity | -0.9% | Global; particularly challenging for small producers in APAC and South America lacking in-house food science capability | Medium term (2-4 years) |

| Regulatory Uncertainty for Irradiation and Cross-Border Labeling | -0.6% | EU (Novel Food Regulation EU 2015/2283), Southeast Asia, Middle East | Medium term (2-4 years) |

| High Energy and Maintenance Cost Concerns | -0.8% | Global; most impactful for high-throughput operations without optimised batch scheduling | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital intensity for HPP and PEF installations

Capital barriers represent the most persistent structural constraint on the expansion of the non-thermal pasteurization market, particularly in middle-income and emerging market geographies where access to equipment financing is limited. Industrial-scale HPP and PEF systems entail high procurement costs, creating a significant financing hurdle for small- and mid-size food manufacturers that lack the processing volume to justify dedicated equipment ownership. The challenge is compounded by the need for pressure-flexible packaging materials, which must withstand approximately 15% volume reduction during pressurization and therefore incur procurement and reformulation costs beyond equipment acquisition. The EaaS model and tolling network expansion are partially addressing this constraint in North America, where Hiperbaric's global tolling network, which includes newly established facilities in North Carolina and Pennsylvania as of 2025, provides access to HPP on a per-pound or per-batch basis without a capex commitment. However, in APAC, South America, and MEA, tolling infrastructure density remains low, meaning that manufacturers in these regions must absorb the full capital cost of equipment or forgo HPP adoption entirely. PEF adoption specifically faces a compounded barrier: unlike HPP, which has a mature equipment market with established service networks, PEF systems require more technical expertise to operate and validate, limiting the pool of qualified operators.

Regulatory uncertainty for irradiation and cross-border labeling

Irradiation and certain emerging non-thermal techniques face a fragmented, sometimes contradictory global regulatory landscape that delays commercial deployment and undermines investment confidence. In the European Union, HPP products derived from animal-origin foods require pre-market authorisation under the Novel Food Regulation (EU) 2015/2283, with safety assessment by the European Food Safety Authority (EFSA); an EFSA opinion from 2022 backed HPP's safety record while raising specific concerns about its application as an alternative to thermal pasteurisation of raw milk, illustrating the nuanced risk appetite of EU regulators[3]Source: European Food Safety Authority, “Novel Food,” EFSA, efsa.europa.eu. For irradiation, the disparity is sharper: the Codex Alimentarius Commission has approved food irradiation broadly, but national implementations vary, with the EU requiring specific labeling of irradiated foods and several Asian markets maintaining restrictions on irradiated product imports that effectively close export channels for North American and South American producers using irradiation as a phytosanitary or microbial-reduction treatment. Cross-border labeling standards for HPP-processed products also remain unharmonized; what constitutes permissible HPP marketing claims in the US (where "cold pressure" labeling is actively promoted by the Cold Pressure Council) differs from EU requirements, forcing exporters to maintain parallel label versions. The compliance cost of managing multi-jurisdictional label variants and novel food authorisation timelines structurally favours large multinational operators over the smaller regional producers that HPP's tolling model was designed to serve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique / Technology: HPP Dominates, PEF Crosses the Industrial Threshold

HPP held 48.73% of the non-thermal pasteurization market share in 2025, maintaining a clear lead over all other techniques. Its lead comes from a long commercial history, clear food safety acceptance, and broad fit across beverages, ready-to-eat meat, seafood, sauces, and premium refrigerated foods. PEF is the fastest-growing technique, with a projected CAGR of 10.67% through 2031, indicating that the non-thermal pasteurization market is expanding beyond HPP into technologies that can serve large-volume, continuous processing lines. MVH, ultrasonic processing, and irradiation make up the remaining share, and each serves narrower use cases where rapid volumetric heating, enhanced mass transfer, or targeted microbial reduction is the main priority.

The Others category includes technologies that still have smaller commercial footprints but can matter in very specific liquid applications within the non-thermal pasteurization market. Lyras has positioned raslysation as a UV-C-based solution for opaque liquids, and the company states that the system can reduce energy use by 60% to 90% and water use by 60% to 80% compared with thermal pasteurization. Its installation at Mjólkursamsalan in Iceland shows that niche alternatives can enter dairy systems where water, hygiene, and product quality are all important. HPP still has the strongest structural position in the non-thermal pasteurization market because it works after packaging and lowers the chance of post-process contamination, which remains a major advantage in high-safety chilled foods.

By Form: Liquid Formats Anchored by Beverage Growth, Semi-Solid Set to Outpace

Liquid held a 62.56% share of the non-thermal pasteurization market in 2025, supported by demand for juices, smoothies, dairy beverages, plant-based drinks, liquid egg products, and liquid pharmaceutical formulations. This form has remained central to the non-thermal pasteurization market because beverages often offer processors the clearest returns on quality retention, shelf-life extension, and cleaner-label positioning. Semi-solid is the fastest-growing form, with a 10.37% CAGR through 2031, helped by strong uptake in guacamole, hummus, premium spreads, baby food purees, and similar chilled products where preservatives are being reduced or removed. Solid foods also remain important, especially in ready-to-eat meat and seafood, where HPP has regulatory value as a recognized post-lethality treatment that can be built into HACCP-based food safety programs.

Growth in semi-solid formats is broader than the early HPP story around guacamole, and that matters for the future shape of the non-thermal pasteurization market. Clean-label nut butters, protein-rich pastes, refrigerated bakery spreads, and plant-based filling systems are expanding the range of uses where heat can alter oils, enzymes, and flavor notes in ways manufacturers want to avoid. Consumer interest in protein-rich foods also moved up between 2022 and 2025, which supports the product pipeline for chilled spreads and nutrient-dense semi-solid products that fit well with non-thermal preservation. The tolling model also supports these categories in the non-thermal pasteurization market because many semi-solid SKUs do not need enough throughput to justify a dedicated machine, but they still benefit from the process economics of outsourced capacity.

By Application: Food and Beverages Remains the Core, Pharmaceuticals Signals the Emerging Frontier

Food and beverages accounted for 45.58% of the non-thermal pasteurization market in 2025, underscoring that this remains the core application area. Demand covers beverages, fresh produce, dairy, sauces, dips, ready-to-eat meals, meat, and seafood, with each category using non-thermal methods to achieve a slightly different balance of safety, shelf life, and quality retention. Ready-to-eat meat and poultry now carry added importance because tighter USDA-FSIS Listeria expectations make validated post-lethality treatments more attractive for processors that previously relied solely on sanitation. Dairy and dairy alternatives also support the non-thermal pasteurization market, as additive-free positioning and fresh-like sensory qualities are becoming increasingly important in cultured products and premium milk alternatives.

Pharmaceuticals are the fastest-growing application in the non-thermal pasteurization market, with a projected CAGR of 10.86% through 2031. This part of the non-thermal pasteurization market is different from food use because the main value lies in microbial control without damaging biologics, liquid vaccines, therapeutic proteins, probiotics, and other heat-sensitive ingredients. Nutraceuticals follow a similar pattern, since manufacturers want to preserve bioactive compounds in botanical extracts, enzyme-active products, and high-value functional preparations that lose value when exposed to heat. The Others category also captures cosmetic and personal care applications where microbial stability is needed but product actives are sensitive, which gives the non-thermal pasteurization market a wider long-term demand base than food alone.

Geography Analysis

North America retained the largest share of the non-thermal pasteurization market, accounting for 32.36% in 2025. The United States anchors this lead because it combines the most mature installed HPP base with the broadest tolling network, which lowers entry barriers for both large brands and smaller processors in the non-thermal pasteurization market. U.S. adoption has also benefited from a clearer regulatory path, as FDA and USDA-FSIS have already established the role of HPP in food safety applications relevant to juices, oysters, and ready-to-eat meat systems. The USDA-FSIS December 2024 Listeria announcement added further momentum, as processors using sanitation-only approaches now face a more stringent compliance environment from January 2025 onward. Canada and Mexico add regional support to the non-thermal pasteurization market, while Latin American rollout history, starting with Chile in 2005, shows how export-oriented food sectors can become the first practical route for commercial HPP expansion.

Europe remained the second-largest geography in the non-thermal pasteurization market, with Germany, Spain, the Netherlands, and the UK forming the most established base outside North America. A major regional strength is the service infrastructure around technology validation, and thyssenkrupp’s Centre of Excellence in Quakenbrück offers toll processing, product development, microbiological testing, and validation support that reduce adoption risk for new users. Europe also has a more cautious regulatory path in parts of the non-thermal pasteurization market, especially where novel food review affects commercialization timelines for some animal-origin applications under EU rules. That difference slows some product launches, but it also pushes suppliers to build stronger documentation and validation capabilities, which benefits larger and more technically prepared operators. South America is still an emerging part of the non-thermal pasteurization market, but Brazil, Chile, Colombia, and Peru stand out as the main adoption hubs, with meat, seafood, and juice exports driving demand for technologies that preserve quality while meeting importer food safety expectations.

Asia-Pacific is the fastest-growing region in the non-thermal pasteurization market, and the Asia-Pacific non-thermal pasteurization market size is projected to expand at 11.38% CAGR through 2031. China is the region’s most important turning point, because JB/T 15299-2025 formalized equipment specifications and China Agricultural University backed a broader group standard effort that extends from processing equipment into product-level categories such as NFC juice, vegetable juice, tea beverages, and coffee liquids. India, Japan, South Korea, Australia, Singapore, and Indonesia are also building relevance in the non-thermal pasteurization market as premium packaged food demand rises and food processing infrastructure improves. The Middle East and Africa remain early-stage, but the UAE and South Africa have started to emerge as initial centers where premium beverage, dairy, and meat applications can support first-wave deployment in the non-thermal pasteurization market.

Competitive Landscape

The non-thermal pasteurization market has a concentration profile that is neither highly concentrated nor highly fragmented, leaving room for both global leaders and specialist technology providers. JBT Marel, Hiperbaric, thyssenkrupp, Elea Technology, and Lyras are the most visible names in the non-thermal pasteurization market because they combine equipment capabilities with application support, validation, or service access, rather than relying solely on machine sales. Hiperbaric has built one of the clearest commercial models in the non-thermal pasteurization market by using its tolling ecosystem to widen customer access and reduce the capital burden for food manufacturers that cannot justify ownership from the start. thyssenkrupp stands apart through high-pressure thermal processing and through its integrated support model in Germany, where tolling, development, testing, and validation are offered together instead of as separate services. This means competition in the non-thermal pasteurization market depends as much on post-installation support, process validation, and customer readiness as it does on equipment specifications.

White-space opportunities in the non-thermal pasteurization market remain strongest in pharmaceutical-grade processing, regional tolling infrastructure outside North America, and better digital process monitoring. Lyras is one of the more interesting challengers because it is targeting dairy and fermentation liquid streams with raslysation, which offers a different value proposition based on lower energy and water use rather than on HPP’s in-pack pressure model. Its deployment at Iceland’s largest dairy company shows that the non-thermal pasteurization market still has room for smaller technology plays that solve narrow industrial problems well. China’s local equipment base is also becoming more relevant as standards mature, and domestic suppliers are likely to compete more aggressively on price and service response inside Asia-Pacific. The Cold Pressure Council adds another layer to competition in the non-thermal pasteurization market because its certification mark helps HPP users turn process choice into a visible market claim, which indirectly strengthens the ecosystem around established HPP suppliers.

Strategic moves in the non-thermal pasteurization market show that suppliers are trying to build practical adoption pathways rather than only selling hardware. Hiperbaric has pushed the tolling model to expand user access, which allows processors to enter the non-thermal pasteurization market without committing to full equipment ownership at the first step. thyssenkrupp has tied its equipment proposition to a broader technical service platform, which helps customers move from trials to regulatory validation and commercial production within one regional system. Lyras has advanced through focused deployment in dairy brine treatment, showing that the non-thermal pasteurization market can still reward specialized solutions when they address water use, energy use, hygiene control, and product quality in one application.

Non-thermal Pasteurization Industry Leaders

JBT Marel Corporation

Hiperbaric S.A.

thyssenkrupp AG

Elea Technology GmbH

Lyras A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Elea Technology showcased its new compact PEF Advantage B Micro system (up to 1.7 t/h) and its AI-driven PiCon inline automation and control platform at SnackEx 2026 in Cologne, targeting small-line snack producers seeking advanced PEF processing without the footprint or investment of full-scale industrial systems.

- February 2026: American Pasteurization Company (APC) installed a new Hiperbaric 525 HPP system at its Milwaukee, Wisconsin, facility, expanding tolling capacity to serve a growing base of clean-label food and beverage customers.

- January 2026: Nordion (Canada) Inc. (a Sotera Health company), Westinghouse Electric Company, and PSEG Nuclear LLC announced key milestones toward the first commercial-scale production of Cobalt-60 in US Pressurized Water Reactors, with the US Nuclear Regulatory Commission reviewing a License Amendment Request and the parties targeting implementation in 2026.

- November 2025: Hiperbaric announced a partnership with Sunrise Logistics, Inc., part of The Four Seasons Family of Companies, to integrate HPP tolling services with comprehensive cold chain logistics at a facility in Ephrata, Pennsylvania.

Global Non-thermal Pasteurization Market Report Scope

Non-thermal pasteurization refers to food preservation techniques that use alternative processing methods to eliminate harmful microorganisms while maintaining the nutritional quality, flavor, texture, and freshness of products without relying on traditional heat-based pasteurization. The non-thermal pasteurization market is segmented by technique/technology, product type, application, and geography. By technique/technology, the market includes High Pressure Processing (HPP), Pulsed Electric Field (PEF), Microwave Volumetric Heating (MVH), ultrasonic, irradiation, and other technologies. Based on product type, the market covers liquid, solid, and semi-solid products. By application, the market is segmented into food and beverages, pharmaceuticals, nutraceuticals, and other applications. The food and beverages segment includes beverages, fruits and vegetables, meat and seafood, dairy and dairy alternatives, ready-to-eat meals, and sauces and dips. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| High Pressure Processing (HPP) |

| Pulsed Electric Field (PEF) |

| Microwave Volumetric Heating (MVH) |

| Ultrasonic |

| Irradiation |

| Others |

| Liquid |

| Solid |

| Semi-Solid |

| Food and Beverages | Beverages |

| Fruits & Vegetables | |

| Meat & Seafood | |

| Dairy & Dairy Alternatives | |

| Ready-to-eat Meals | |

| Sauces & Dips | |

| Pharmaceuticals | |

| Nutraceuticals | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Technique / Technology | High Pressure Processing (HPP) | |

| Pulsed Electric Field (PEF) | ||

| Microwave Volumetric Heating (MVH) | ||

| Ultrasonic | ||

| Irradiation | ||

| Others | ||

| By Form | Liquid | |

| Solid | ||

| Semi-Solid | ||

| By Application | Food and Beverages | Beverages |

| Fruits & Vegetables | ||

| Meat & Seafood | ||

| Dairy & Dairy Alternatives | ||

| Ready-to-eat Meals | ||

| Sauces & Dips | ||

| Pharmaceuticals | ||

| Nutraceuticals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in non-thermal pasteurization through 2031?

Growth is being supported by clean-label demand, longer shelf life without heat damage, stronger food safety enforcement, and rising use in pharmaceuticals. The sector is projected to grow at a 9.57% CAGR through 2031.

Which technology leads current adoption?

HPP is the leading technique, with 48.73% share in 2025, because it has the strongest installed base and the clearest commercial acceptance across food safety applications.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific is forecast to expand at 11.38% CAGR through 2031, helped by China’s formal equipment standards and broader product-level standard development for HPP processing.

Which application area remains the core revenue base?

Food and beverages held 45.58% share in 2025, making it the largest application area across beverages, meat, seafood, dairy, sauces, dips, and ready-to-eat foods.

Why are pharmaceutical companies interested in these technologies?

Non-thermal methods help control microbes without damaging heat-sensitive biologics, liquid vaccines, proteins, probiotics, and other high-value formulations. Pharmaceuticals are the fastest-growing application at 10.86% CAGR through 2031.

Page last updated on: