Regenerative Thermal Oxidizer (RTO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

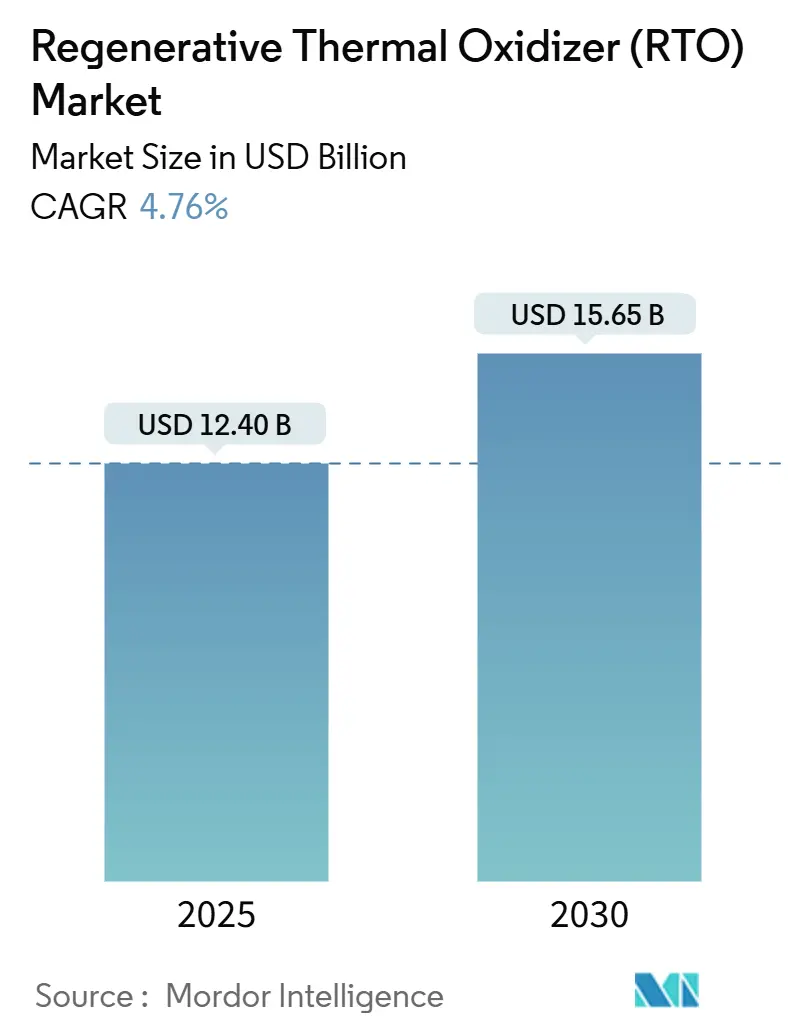

| Market Size (2025) | USD 12.40 Billion |

| Market Size (2030) | USD 15.65 Billion |

| Growth Rate (2025 - 2030) | 4.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Regenerative Thermal Oxidizer (RTO) Market Analysis by Mordor Intelligence

The regenerative thermal oxidizer market size stands at USD 12.40 billion in 2025 and is forecast to reach USD 15.65 billion by 2030, reflecting a 4.76% CAGR over the period. Tightening volatile organic compound (VOC) emission limits across OECD and BRICS economies, coupled with industrial decarbonization mandates, underpin steady capital expenditure despite macro-economic cycles.[1]U.S. Environmental Protection Agency, “Ethylene Oxide Emissions Standards for Sterilization Facilities,” epa.gov Continuous emission-monitoring rules have transformed thermal oxidizers from optional add-ons into mandatory compliance infrastructure, anchoring resilient equipment replacement cycles. Competitive differentiation centers on heat-recovery efficiencies, modular construction, and digital monitoring suites, while natural gas price volatility and technician shortages temper near-term installation rates. Over the forecast horizon, the regenerative thermal oxidizer market will benefit from petrochemical and semiconductor capacity investments in Asia-Pacific, brown-to-green refinery retrofits in North America and Europe, and tax incentives for energy-efficient technologies in major economies.[2]European Commission, “Fit for 55 Package,” europa.eu

Key Report Takeaways

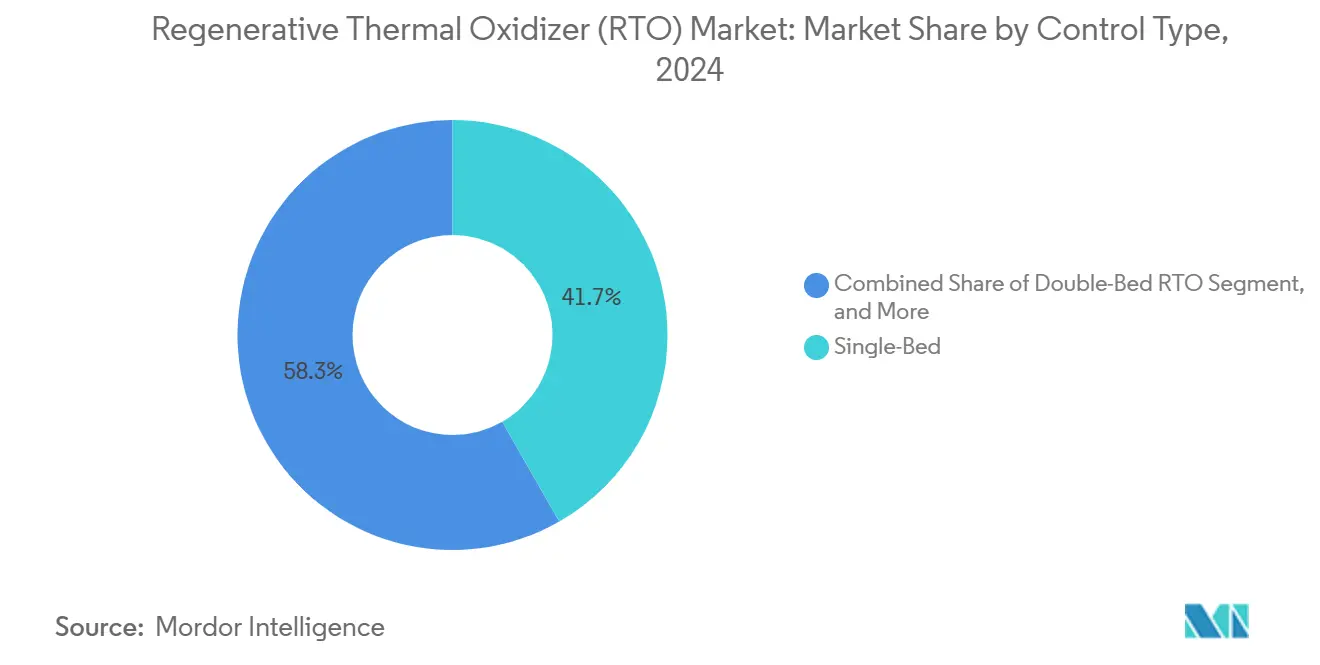

- By control configuration, single-bed units led with 41.72% of the regenerative thermal oxidizer market share in 2024, whereas double-bed systems are expected to record the highest 5.55% CAGR to 2030.

- By product type, rotary designs held 46.73% in 2024; compact modular packages are projected to expand at a 5.78% CAGR through 2030.

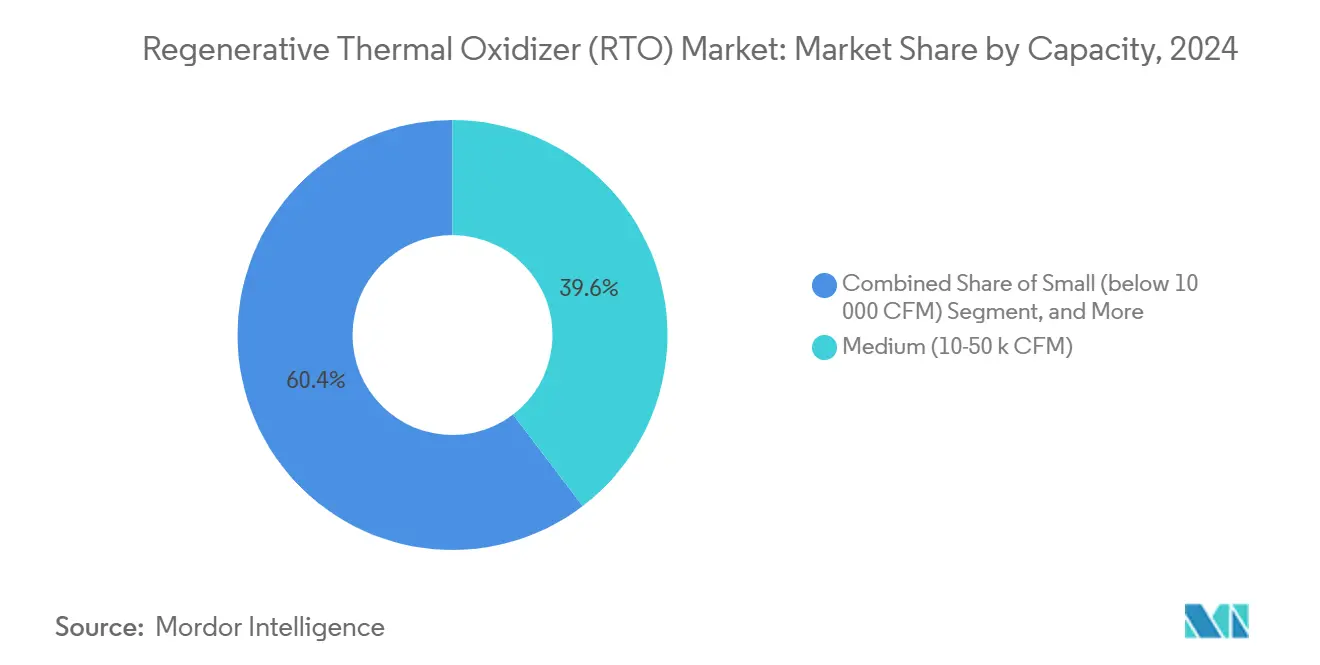

- By capacity, medium units (10,000–50,000 CFM) accounted for 39.64% of the regenerative thermal oxidizer market size in 2024, while installations over 50,000 CFM should advance at 5.43% CAGR.

- By end-use, chemical manufacturing captured 42.93% share of the regenerative thermal oxidizer market size in 2024; semiconductor and electronics applications are poised for the fastest 5.60% CAGR.

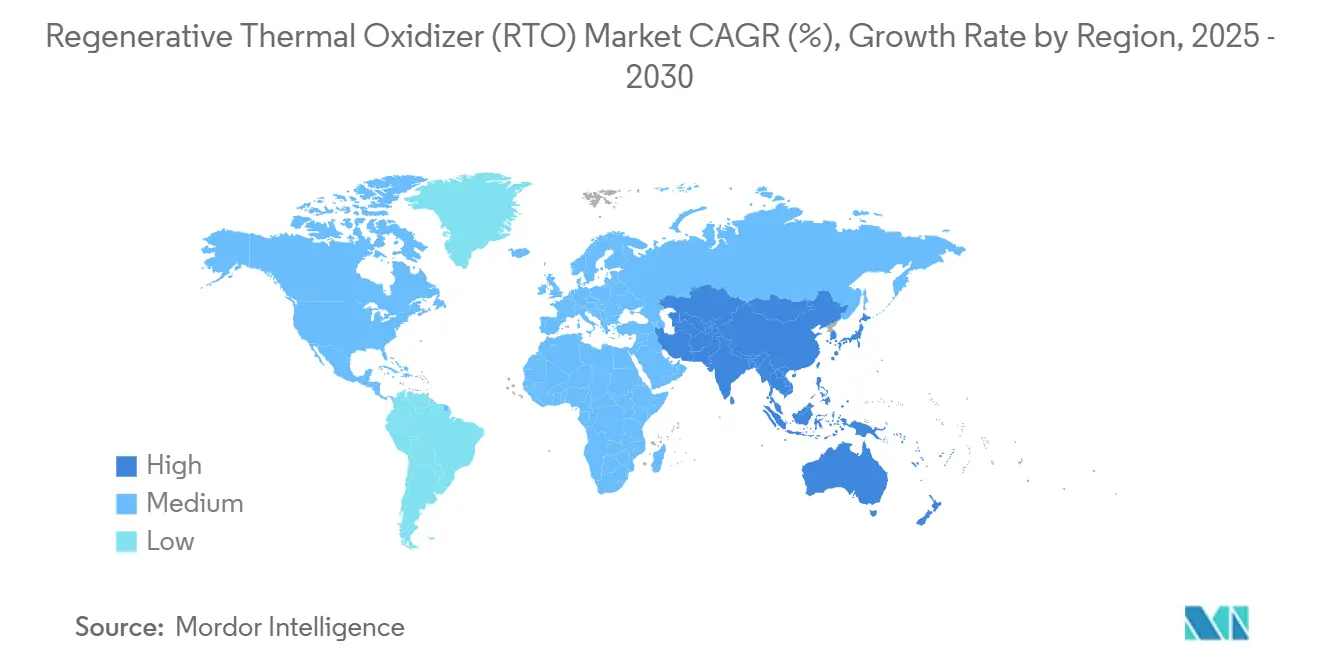

- By geography, North America commanded 39.83% in 2024; Asia-Pacific is forecast to log the highest 5.66% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Regenerative Thermal Oxidizer (RTO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC/HAP emission limits in OECD and BRICS economies | +1.1% | Global, with early enforcement in EU and North America | Medium term (2-4 years) |

| Petro-chemical and semiconductor fab build-outs in APAC | +0.8% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Brown-to-green refinery retrofits replacing flares with RTOs | +0.7% | North America and EU, emerging in BRICS | Medium term (2-4 years) |

| Mandatory continuous emission-monitoring (CEM) data transparency | +0.6% | OECD countries, expanding to emerging markets | Short term (≤ 2 years) |

| Tax incentives for heat-recovery systems (EU Fit-for-55, US IRA) | +0.5% | EU and North America primarily | Medium term (2-4 years) |

| Modular, IoT-ready RTO packages for SME batch manufacturers | +0.4% | Global, with concentration in industrial clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening VOC/HAP Emission Limits Drive Compliance Investment

Regulatory tightening across OECD and BRICS jurisdictions mandates destruction efficiencies of 99% or higher, effectively locking in budget allocations for new and replacement systems. Vietnam’s QCVN 19:2024 cap of 50 mg/Nm³ VOC forces rapid migration from basic scrubbers to regenerative oxidation, while EU Industrial Emissions Directive amendments require continuous monitoring for plants emitting over 10 t/year VOCs. Standard two- to three-year compliance windows provide clear procurement schedules, and the shift from periodic to real-time reporting removes operational work-arounds, turning thermal oxidizers into compulsory plant infrastructure.

Semiconductor Fabrication Expansion Accelerates APAC Demand

Advanced node fabs require ceramic heat exchangers and corrosion-resistant internals that withstand fluorinated solvents while achieving 99.9% destruction efficiency. Projects such as TSMC’s USD 40 billion Arizona complex and Samsung’s USD 17 billion Texas facility demonstrate how equipment specifications are frozen 18–24 months before tool move-in, securing predictable orders for triple-bed designs that support 24/7 operation. Similar investments across China, South Korea, and India support the region’s 5.66% CAGR leadership.

Brown-to-Green Refinery Retrofits Replace Legacy Flares

European carbon pricing and North American decarbonization roadmaps spur adoption of regenerative thermal units that recover waste heat while meeting Scope 1 targets. Integrated designs linking oxidizers to steam networks deliver energy savings that shorten project payback, and modular skids minimize shutdown duration during tie-ins.

Mandatory CEM Data Transparency Eliminates Compliance Gaps

Rules requiring cloud-based emission uploads make deviations instantly visible, ending reliance on manual stack testing. Plants adopt systems with embedded analytics and predictive maintenance dashboards to avoid fines, benefiting vendors offering hardware-software bundles that streamline permit audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital outlay and payback anxiety for SMEs | -0.9% | Global, particularly in emerging markets and industrial clusters | Short term (≤ 2 years) |

| Scarcity of skilled O&M technicians in emerging markets | -0.6% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Competition from low-CAPEX biofilters and scrubbers at <5 g/Nm³ VOC | -0.6% | Emerging markets and low-concentration applications globally | Medium term (2-4 years) |

| Volatile natural-gas prices eroding OPEX savings | -0.3% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Outlay Creates SME Adoption Barriers

Typical turnkey costs of EUR 12.8 - 34.83 (USD ~15.0 - 40.8) per m³ h⁻¹ airflow stretch SME budgets, and three- to five-year paybacks compete with revenue-generating investments. Limited in-house expertise prolongs decision cycles and raises dependence on third-party consultants, inflating total project expense.

Low-CAPEX Alternatives Challenge RTO Economics

Biofilters achieving 95–98% VOC removal at roughly half the capital cost draw interest from plants processing ≤ 5 g/Nm³ streams, while wet scrubbers reduce outlay for water-soluble emissions. These options, however, lack high-temperature capabilities and energy-recovery benefits that justify regenerative thermal solutions in energy-intensive settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Control Type: Double-Bed Systems Drive Efficiency Gains

In 2024 single-bed equipment held 41.72% of regenerative thermal oxidizer market share, yet double-bed designs are set for a 5.55% CAGR through 2030 as operators target 15–20% fuel savings and uninterrupted switchover performance. This energy advantage grows more compelling as natural gas prices fluctuate and carbon costs escalate.[3]Dürr AG, “Thermal Oxidation Portfolio,” durr.com

Double-bed installations increasingly feature digital combustion control that fine-tunes valve sequencing to maintain ≥ 99% destruction efficiency across variable flows. Single-beds still retain cost advantages for small batch operations, sustaining their role in niche segments of the regenerative thermal oxidizer market.

By Product Type: Modular Solutions Accelerate Market Penetration

Rotary machinery dominated the regenerative thermal oxidizer market size with 46.73% revenue in 2024, prized for handling fluctuating flow regimes in refining and chemical processing. Nonetheless modular fixed-bed packages are expected to outpace at 5.78% CAGR by shortening project cycles from 12–18 months to 6–9 months and reducing site labor exposure.

Factory acceptance testing provides plug-and-play assurance, while standardized heat-recovery cores unlock economies of scale. Maintenance simplicity favors fixed-beds over rotary seals in capacity bands below 40,000 CFM, widening access for mid-tier manufacturers.

By Capacity: Large Systems Capture Industrial Expansion

Facilities consolidating emissions at central stacks propel units above 50,000 CFM toward a projected 5.43% CAGR, even as medium systems claimed the largest 39.64% share of the regenerative thermal oxidizer market size in 2024. Scale leverages larger ceramic media beds that lift thermal efficiency and slash per-CFM costs.

Process industries integrate these large oxidizers with cogeneration loops, extracting steam for in-house demand and elevating project return profiles. Redundancy via modular cells within a single housing enables staged maintenance without production loss.

By End-Use Industry: Semiconductor Growth Outpaces Chemical Dominance

Chemical producers remained top customers at 42.93% share in 2024 owing to continuous solvent handling requirements, yet semiconductor fabs will log a 5.60% CAGR on the back of megaprojects in East Asia and the U.S. Southwest. Cleanroom uptime standards necessitate triple-bed or rotary solutions that permit maintenance while lines stay active.

Electronics coaters adopt compact packages with high turn-down ratios that manage recipe changes without efficiency drift. Cross-industry technology transfer is sharpening oxidizer metallurgy and control logic, benefiting broader applications such as pharmaceuticals and food processing.

Geography Analysis

North America led with a 39.83% share in 2024 thanks to mature refinery and petrochemical complexes subject to stringent EPA rules. The United States drives brown-to-green retrofits, while Canada’s oil sands and Mexico’s nearshoring manufacturing corridors add incremental demand.

Asia-Pacific is projected to eclipse regional peers at a 5.66% CAGR, fueled by China’s environmental clamp-downs, South Korean fab expansions, and India’s chemicals build-out. Vietnam’s new VOC norms pull forward smaller batch plant purchases, and Japan’s energy-efficiency grants tilt buyers toward high-recovery designs.

Europe remains a steady adopter as Fit-for-55 and the Industrial Emissions Directive embed energy-efficiency yardsticks into permit renewals. Retrofit activity emphasizes modular skids that slide into crowded brownfield plots without lengthy shutdowns. Carbon pricing in the EU Emissions Trading System further incentivizes heat-recovery integrations that shave Scope 1 footprints.

Competitive Landscape

The regenerative thermal oxidizer market features medium concentration, with the top five vendors supplying roughly 45% of global revenue. Dürr leverages its EcoRevo platform to pair oxidizers with digital twins that predict media bed fouling and schedule just-in-time service. John Zink Hamworthy emphasizes rotary solutions for high-throughput refinery clients, while CECO Environmental positions hybrid scrubber-oxidizer packages to secure multi-pollutant tenders.

Emergent challengers deliver electric or hydrogen-heated chambers aimed at sites targeting methane-free operations. Patenting intensity centers on staggered-port valve designs that slash pressure drop and on AI-enabled control loops optimizing fuel trim in real time. Vendors with regional fabrication hubs and regulatory advisory arms gain edge, as local content and compliance consulting increasingly sway award decisions.

Financial investors favor platform plays integrating air and water treatment portfolios, encouraging bolt-on acquisitions of smaller oxidizer specialists by larger environmental technology groups. This trend could lift portfolio synergies but also compress margins as scale buyers push for component cost reductions.

Regenerative Thermal Oxidizer (RTO) Industry Leaders

-

Dürr Aktiengesellschaft

-

John Zink Hamworthy Combustion LLC

-

CECO Environmental Corp.

-

Taikisha Ltd.

-

Anguil Environmental Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Worley released a refinery decarbonization roadmap that spotlights thermal oxidation as a primary pathway for 35% CO₂ cuts by 2030.

- August 2024: The U.S. EPA finalized ethylene oxide NESHAP requiring 99% destruction efficiency at sterilization facilities, triggering immediate retrofit activity.

- July 2024: TSMC confirmed USD 40 billion investment in an Arizona fab with emission specs mandating ultra-pure regenerative oxidizers.

- June 2024: Samsung broke ground on a USD 17 billion semiconductor plant in Texas, specifying triple-bed oxidizers for 24/7 uptime.

Global Regenerative Thermal Oxidizer (RTO) Market Report Scope

| Single-Bed RTO |

| Double-Bed RTO |

| Triple-Bed RTO |

| Rotary RTO |

| Compact / Modular RTO |

| Small (below 10 000 CFM) |

| Medium (10 000–50 000 CFM) |

| Large (above 50 000 CFM) |

| Chemical Manufacturing |

| Coating and Painting |

| Semiconductor and Electronics |

| Oil and Gas / Refining |

| Pharmaceutical |

| Food and Beverage |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Control Type | Single-Bed RTO | ||

| Double-Bed RTO | |||

| Triple-Bed RTO | |||

| By Product Type | Rotary RTO | ||

| Compact / Modular RTO | |||

| By Capacity | Small (below 10 000 CFM) | ||

| Medium (10 000–50 000 CFM) | |||

| Large (above 50 000 CFM) | |||

| By End-Use Industry | Chemical Manufacturing | ||

| Coating and Painting | |||

| Semiconductor and Electronics | |||

| Oil and Gas / Refining | |||

| Pharmaceutical | |||

| Food and Beverage | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the regenerative thermal oxidizer market?

The regenerative thermal oxidizer market size is USD 12.40 billion in 2025.

How fast will demand for regenerative thermal oxidizers grow through 2030?

The market is projected to expand at a 4.76% CAGR, reaching USD 15.65 billion by 2030.

Which region is expected to experience the fastest adoption of regenerative thermal oxidizers?

Asia-Pacific is forecast to post the highest 5.66% CAGR due to semiconductor and petrochemical investments.

Why are double-bed designs gaining popularity in emission control projects?

Double-bed units deliver 15–20% fuel savings and maintain ≥ 99% destruction efficiency without halting operations, making them attractive under volatile energy prices.

How do tax incentives influence regenerative thermal oxidizer procurement?

U.S. investment tax credits and EU Fit-for-55 grants cut capital costs by up to 30%, improving payback for heat-recovery-equipped systems.

Page last updated on: