Nitinol Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 4.77 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

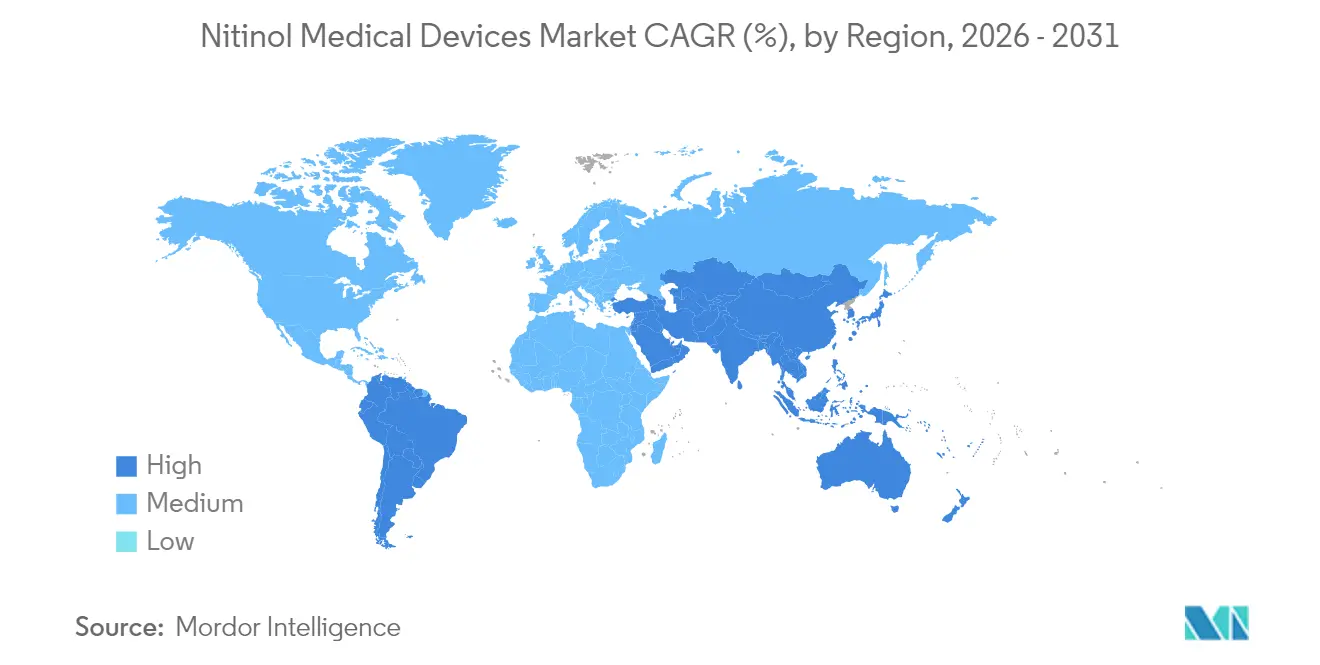

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nitinol Medical Devices Market Analysis by Mordor Intelligence

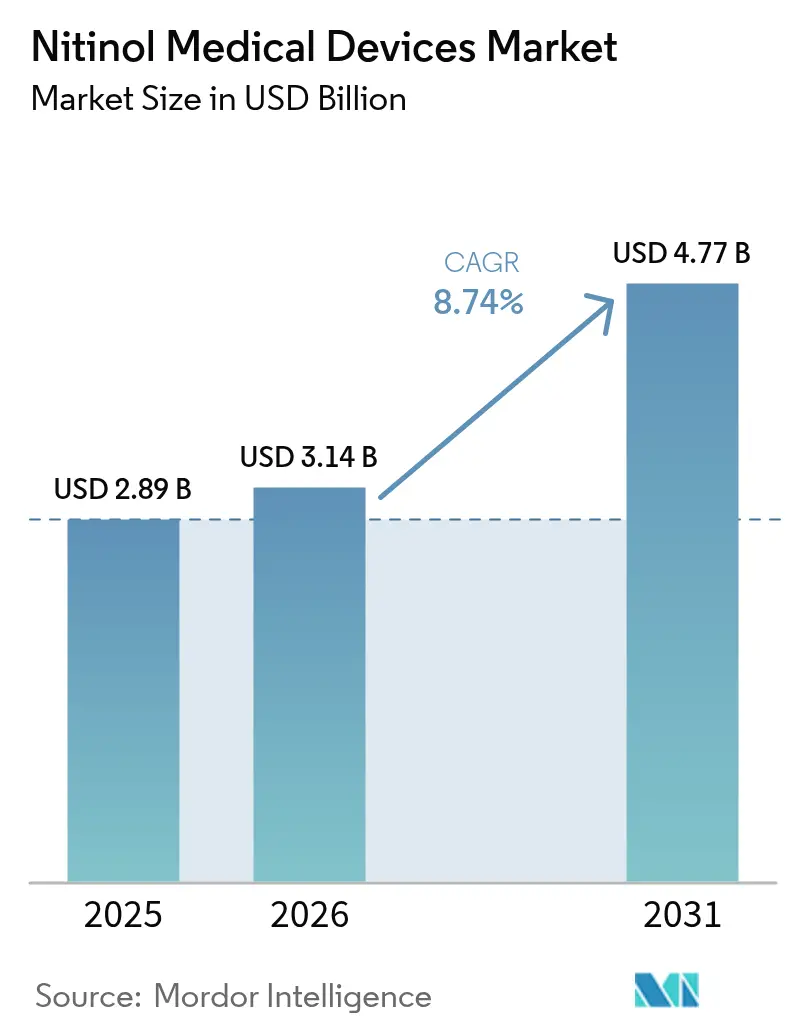

The Nitinol Medical Devices Market size is expected to grow from USD 2.89 billion in 2025 to USD 3.14 billion in 2026 and is forecast to reach USD 4.77 billion by 2031 at 8.74% CAGR over 2026-2031.

Robust demand stems from the convergence of aging populations, rising chronic disease prevalence, and the continual push toward less-invasive care pathways that exploit nitinol’s superelasticity and shape-memory behavior. Material suppliers are scaling melting and tubing capacity to keep pace with orders for miniaturized components that navigate previously inaccessible anatomies. Hospitals remain the primary customers, yet ambulatory surgical centers are winning procedures as reimbursement incentives reward day-care interventions that lower total treatment costs. At the same time, geographic momentum is shifting toward Asia-Pacific, where local manufacturing initiatives and wider healthcare access are accelerating device approvals and adoption.

Key Report Takeaways

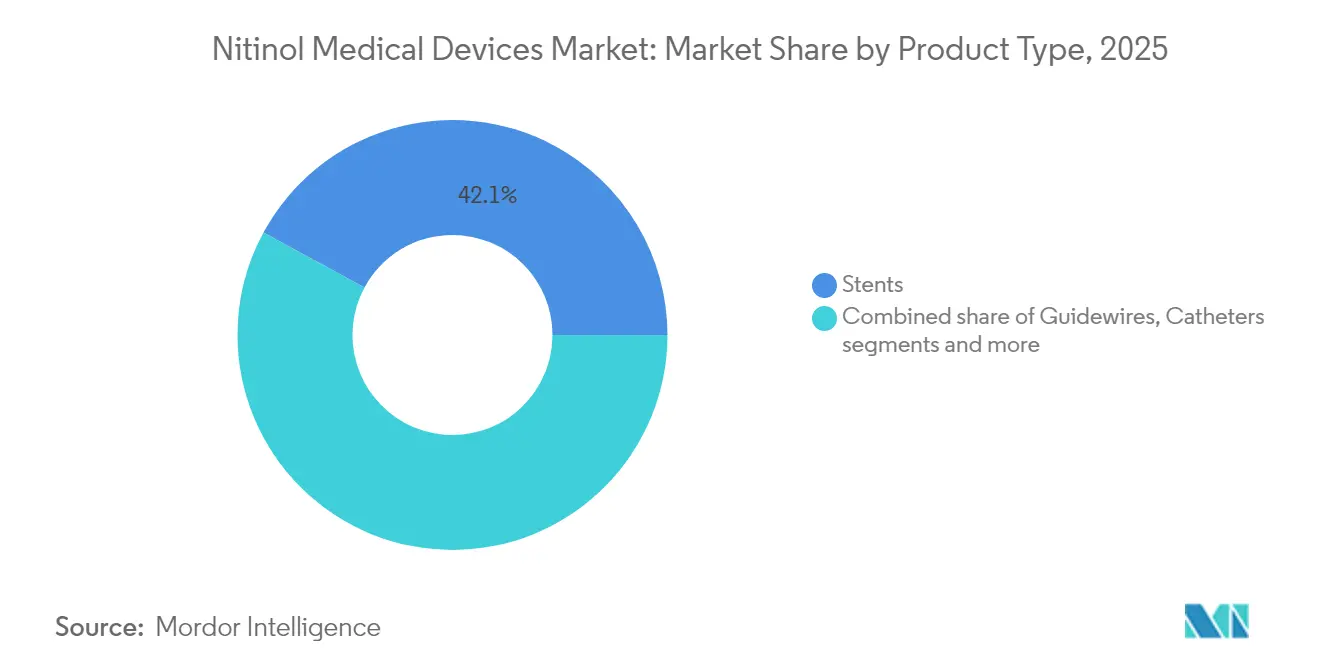

- By product type, stents led with 42.10% of the nitinol medical devices market share in 2025, while filters and occlusion devices are projected to expand at an 10.55% CAGR to 2031.

- By application, cardiovascular interventions held a 64.85% share of the nitinol medical devices market in 2025; gastroenterology applications are forecast to rise at a 11.32% CAGR through 2031.

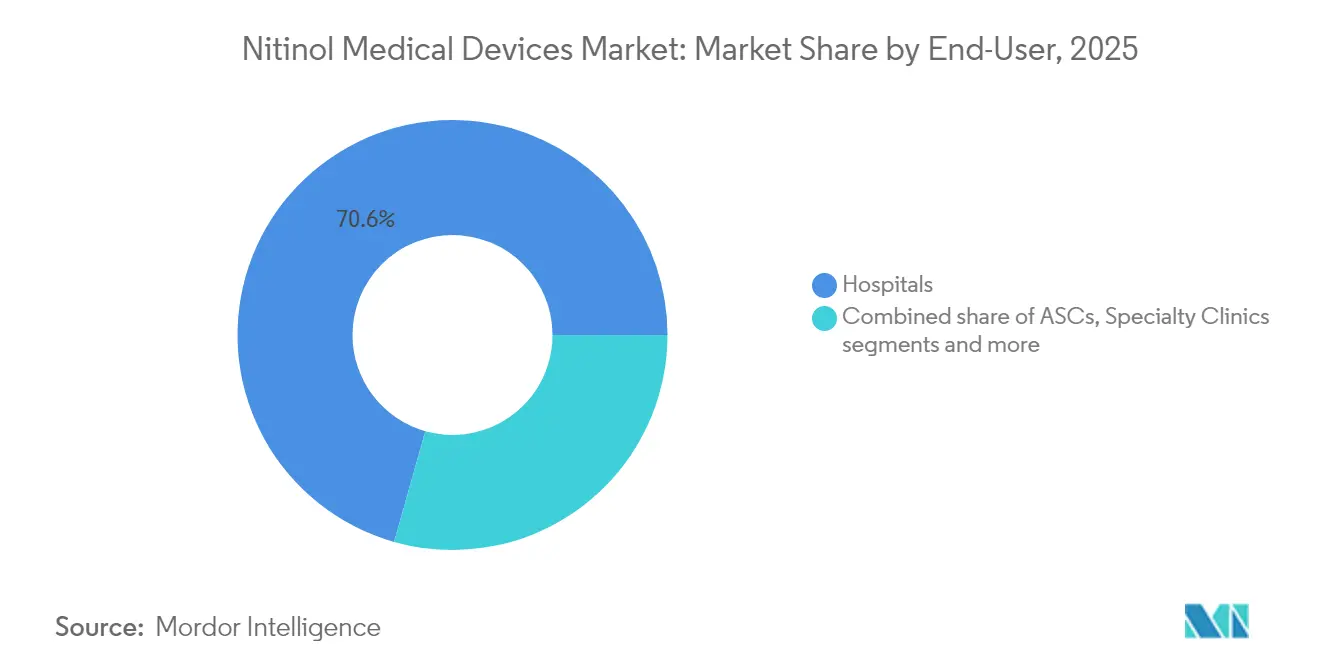

- By end-user, hospitals held 70.62% of the nitinol medical devices market size in 2025, whereas ambulatory surgical centers are advancing at a 9.98% CAGR to 2031.

- By geography, North America dominated with a 43.10% revenue share in 2025; Asia-Pacific is set to register the highest regional CAGR of 10.98% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nitinol Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating chronic-care interventional procedures | +2.1% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Growing adoption of super-elastic alloys to miniaturize devices | +5.2% | Global, with innovation centers in North America, Europe, and Japan | Long term (≥ 4 years) |

| Shift toward day-care minimally-invasive surgeries | +1.8% | North America, Europe, and developed APAC | Medium term (2-4 years) |

| Expanding reimbursement coverage for implantable devices | +1.4% | North America, with gradual adoption in Europe and select APAC countries | Short term (≤ 2 years) |

| Increasing clinical evidence boosting physician confidence | +1.1% | Global | Medium term (2-4 years) |

| AI-assisted imaging and robotics boosting precision and success rates of nitinol interventions | +1.6% | North America, Europe, and developed APAC markets with advanced imaging infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Chronic-Care Interventional Procedures

Cardiovascular disease continues to claim 17.9 million lives each year, propelling steady demand for nitinol stents that navigate tortuous vasculature and sustain high patency rates. A single-center study[1]B. Lukic et al., “Endovascular Treatment of Femoro-Popliteal Disease with the Supera Stent,” Journal of Clinical Medicine, doi.org of the Supera interwoven device reported 95.6% primary patency at 1 month and 77.7% at 24 months in femoropopliteal lesions. Beyond the heart, interventional gastroenterology and neurology are shifting away from open surgery, embracing nitinol-based systems that shorten recovery, reduce infection risk, and support outpatient workflows. Aging demographics magnify these trends as older patients benefit most from low-trauma therapies compatible with comorbidities.

Growing Adoption of Super-Elastic Alloys to Miniaturize Devices

Device engineers now routinely specify wall thicknesses below 50 µm, leveraging nitinol’s capacity to recover up to 8% strain without plastic deformation. Suppliers such as Fort Wayne Metals doubled their melting output[2]Fort Wayne Metals, “Fort Wayne Metals Expands Nitinol Melting Capabilities to Meet Growing Medical Device Industry Demand,” fwmetals.com from 2022 to 2024 and plan another doubling during 2025 to reach 1 million lb annual capacity. Miniaturization opens neurovascular and pediatric markets where compact catheters and self-expanding frames create clinical options that stainless steel cannot match. High success rates for devices like the Alpha stent, which achieved 97.1% technical success in wide-neck intracranial aneurysms,[3]J. Kim, “Safety and Efficacy of the Novel Alpha Stent for the Treatment of Intracranial Wide-Necked Aneurysm,” Nature Scientific Reports, nature.com validate the engineering push toward thinner, more flexible solutions.

Shift Toward Day-Care Minimally-Invasive Surgeries

Global health systems are migrating procedures from inpatient wards to ambulatory settings to control costs and free hospital beds. The United States finalized a 2.9% payment increase for outpatient services in 2025, alongside expanded pass-through payments for device-intensive cases. Ambulatory surgical centers typically deliver 35-50% cost savings to payers, making nitinol-enabled techniques financially attractive. Dedicated CPT codes for innovations such as the iTind implant for benign prostatic hyperplasia remove coding ambiguity and accelerate scheduling in outpatient theatres.

Expanding Reimbursement Coverage for Implantable Devices

Coverage wins spur wider adoption. U.S. private insurers now reimburse FDA-cleared nitinol stents for peripheral artery disease and chronic mesenteric ischemia, acknowledging superior performance versus bare-metal alternatives. Europe is following with iterative updates that compensate hospitals for device-driven value, particularly where randomized evidence shows lower re-intervention rates. In Asia-Pacific, Japan’s favorable device reimbursement and China’s volume-based procurement pilots are starting to balance affordability with quality, expanding the addressable population for nitinol implants

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of nitinol-based implants | -1.2% | Global, with higher impact in price-sensitive markets | Medium term (2-4 years) |

| Complex thermo-mechanical processing requirements | -0.9% | Global, with manufacturing concentrated in North America, Europe, and Japan | Short term (≤ 2 years) |

| Risk of nickel hypersensitivity in susceptible patients | -0.3% | Global | Long term (≥ 4 years) |

| Uncertain long-term biocompatibility data related to nickel ion release | -0.7% | Global, with higher regulatory scrutiny in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing of Nitinol-Based Implants

Raw nitinol ingot prices rose during 2024 as demand tightened supply, widening the cost gap with stainless steel by 30-40%. Budget-constrained hospitals in emerging economies often defer adoption until alternative funding emerges. Value-based contracting that shares savings from lower readmission rates partly offsets premiums, yet widespread acceptance in low-income regions will depend on localized production and streamlined logistics that trim landed cost.

Complex Thermo-Mechanical Processing Requirements

Shape-set accuracy, oxidation control, and micro-machining tolerances demand specialized know-how, limiting the number of qualified suppliers. Variations in surface finish can influence corrosion resistance and nickel ion release, forcing OEMs to audit partners rigorously. Resonetics acquired gun-drilling assets in 2025 to internalize critical tubing steps and shrink lead-times for high-precision components. While such investments gradually boost capacity, the learning curve and capital intensity restrain smaller entrants and slow high-volume scale-up for novel geometries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stents Lead While Filters Accelerate

Stents generated the largest revenue pool, capturing 42.10% of the nitinol medical devices market share in 2025 by virtue of their proven efficacy in challenging vasculature. Consistent radial force and kink resistance give nitinol stents a clinical edge, reflected in 24-month patency rates exceeding 77% in peripheral arteries. Guidewires, catheters, and orthodontic archwires follow, each exploiting the alloy’s torqueability and pseudoelastic properties to reduce procedure time and improve patient comfort.

Filters & occlusion devices represent the fastest-growing segment, expanding at an 10.55% CAGR as physicians embrace retrievable vena cava filters, embolic protection systems, and implantable hemodynamic monitors. Phraxis’ EndoForce Connector, integrating a flexible nitinol segment, reached a 92% patency rate at six months, illustrating how hybrid devices address longstanding graft complications. Diagnostic sensors such as the FIRE1 IVC platform further enlarge the addressable space by enabling remote monitoring of chronic heart failure, a capability unattainable with rigid metallic materials.

By Application: Cardiovascular Dominance Meets Gastroenterology Growth

Cardiovascular indications commanded 64.85% of revenue in 2025, underscoring nitinol’s irreplaceable role in vascular reconstruction. Drug-eluting, self-expanding frames cut restenosis risk while small-profile delivery catheters curtail procedural trauma. Urology, orthopedics, dentistry, and neurology form the secondary tier, yet each shows sustained pipeline activity supported by the alloy’s fatigue endurance and biocompatibility.

Gastroenterology delivers the highest upside with a 11.32% forecast CAGR. Researchers engineered polyurethane-silicone coated nitinol stents loaded with 5-fluorouracil that release cytotoxic concentrations for up to 150 days in esophageal cancer models. Such combination devices address tumor obstruction and drug delivery simultaneously, reducing re-intervention frequency. Endoscopists also leverage nitinol’s flexibility to traverse tight colonic strictures, broadening indications for minimally invasive palliation.

By End-User: Hospitals Lead While ASCs Gain Momentum

Hospitals held 70.62% of revenue in 2025, as complex neurovascular, structural heart, and peripheral interventions still gravitate to tertiary centers with hybrid theatres and advanced imaging. These centers also host multidisciplinary panels required for novel device credentialing. The segment’s growth reflects organic volume growth and incremental adoption in emerging nations.

Ambulatory surgical centers (ASCs) record the fastest expansion at a 9.98% CAGR. Predictable procedure times and reduced infection rates make ASCs ideal for peripheral angioplasty, urologic implants, and gastrointestinal stent placements that rely on nitinol delivery systems. Payment reforms that equalize device-intensive reimbursement with hospital outpatient departments reinforce the shift. Specialty clinics and academic institutes contribute minor, yet strategically important, volumes through focused expertise and first-in-human trials that de-risk next-generation products.

Geography Analysis

North America retained a commanding 43.10% share in 2025 as extensive clinical infrastructure, broad reimbursement, and a cohesive supply chain reinforced leadership in the nitinol medical devices market. Fort Wayne Metals’ capacity expansion exemplifies the regional commitment to secure raw alloy availability for OEMs. The United States continues to issue pass-through payments for breakthrough implants, supporting a steady 8.27% regional CAGR through 2031. Canada and Mexico post single-digit growth, focused on metropolitan centers, integrating advanced endovascular programs.

Asia-Pacific is the fastest-growing region with 10.98% CAGR. Japan’s mature interventional cardiology market anchors early adoption, while China scales domestic manufacturing and broadens device listing under national insurance. India targets a medical devices market jump to USD 50 billion by 2030, buoyed by production-linked incentives and dedicated industrial parks that ease entry barriers for nitinol component fabrication. South Korea nurtures proprietary designs like the Alpha stent, demonstrating regional innovation capacity.

Europe ranks second, driven by Germany, France, and the United Kingdom, where hospital networks value the lower re-intervention profile of nitinol technology. Regional CAGR stands at 8.72%, based on expectations of wider adoption in lower-limb artery revascularization and emerging neurovascular procedures. The Middle East & Africa and South America collectively represent a relatively smaller chunk of global revenue today, but show double-digit compound growth. Private hospitals in the Gulf and Brazil implement complex structural heart and neurovascular programs that depend on nitinol’s performance advantages. Government tenders increasingly accept value-based bids, creating openings for cost-optimized devices supplied from Asia.

Competitive Landscape

The nitinol medical devices market presents a moderate concentration. Multinational device manufacturers dominate cardiovascular, neurovascular, and structural heart niches, yet specialized component firms wield influence through proprietary tubing, laser-cutting, and shape-setting knowledge. Vertical integration is intensifying: Resonetics’ 2025 purchase of gun-drilling assets assures internal control of precision lumen creation vital for microcatheters, while Fort Wayne Metals scales ingot supply to safeguard alloy purity across the value chain.

White-space potential lies in gastroenterology, remote hemodynamic monitoring, and transcatheter valve repair, where nitinol’s fatigue resistance and conformability create differentiated therapy options. Surface engineering is another competitive frontier; low-temperature plasma oxidation yields uniform titanium dioxide layers that cut nickel ion release and boost endothelialization. Companies pairing such coatings with drug-elution technology may capture premium positioning as payers emphasize durability and patient safety.

Mergers and acquisitions are reshaping portfolios. Medical Device Components completed the Lighteum takeover in 2024 to access femtosecond laser processing for high-complexity implants, and Edwards Lifesciences added J-Valve to strengthen its transcatheter regurgitation offering built on nitinol frames. Competition in neurovascular markets remains fierce, highlighted by Penumbra’s ACCESS25 launch that complements stent retrievers with agile delivery tooling designed around nitinol kink resistance.

Nitinol Medical Devices Industry Leaders

Arthrex, Inc.

B. Braun Melsungen AG

Boston Scientific Corporation

Terumo Corporation

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Phraxis Inc. gained FDA clearance for the EndoForce Connector, a flexible ePTFE-covered nitinol device that improves dialysis graft patency, achieving 92% patency at six months.

- February 2025: Penumbra introduced the ACCESS25 Delivery Microcatheter to enhance aneurysm access with nitinol-reinforced construction.

- November 2024: Medical Device Components completed the acquisition of Lighteum, adding femtosecond laser nitinol processing to its portfolio.

- October 2024: Edwards Lifesciences won FDA approval for the Evoque TTR system featuring a self-expanding nitinol frame, while Abbott’s TriClip awaited reimbursement review.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global nitinol medical devices market as the annual sales value of finished therapeutic or diagnostic products, such as self-expanding stents, guidewires, filters, and shape-memory implants, whose primary load-bearing component is the nickel-titanium alloy nitinol, valued at end-user transfer price before distributor mark-ups. Devices that merely contain trace nitinol additives without performance reliance are out of scope.

Scope exclusion: industrial actuators, orthodontic archwires sold to dental labs, and raw nitinol tubing or wire are excluded from this sizing.

Segmentation Overview

- By Product Type

- Stents

- Guidewires

- Catheters

- Filters & Occlusion Devices

- Baskets & Retrieval Devices

- Orthodontic Archwires

- Other Nitinol Implants

- By Application

- Cardiovascular

- Urology

- Orthopedics & Trauma

- Dental

- Gastroenterology

- Neurology

- Other Applications

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Institutes

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with interventional cardiologists, purchasing managers at large hospital chains, and senior engineers at contract manufacturers across North America, Europe, and Asia-Pacific. These conversations clarified real-world adoption rates, ASP erosion curves, and regional reimbursement shifts that rarely surface in public literature, letting us verify and fine-tune secondary findings.

Desk Research

We gathered baseline metrics from open datasets such as United States International Trade Commission DataWeb, OECD Health Statistics, UN Comtrade shipment codes for nickel-titanium devices, and regulatory filings posted by the US FDA and European Medicines Agency. Trade association white papers from MedTech Europe and the Advanced Medical Technology Association provided hospital procedure volumes and device ASP benchmarks. D&B Hoovers supplied private-company revenue splits that helped us apportion nitinol lines within broader portfolios. This list is illustrative; dozens of additional public sources fed our screens.

Market-Sizing & Forecasting

A top-down reconstruction started with nitinol device import-export flows and hospital procedure counts, which were then matched with triangulated average selling prices to build the 2025 demand pool. Select bottom-up cross-checks, supplier roll-ups and sampled distributor audits, flagged outliers and guided minor adjustments. Key model inputs include elective coronary stent volumes, endovascular aneurysm repair prevalence, geriatric population growth, and nitinol raw-material price trends. Multivariate regression, anchored to those predictors and validated by expert consensus, produced the 2025-2030 outlook. Gaps where shipment data were thin were bridged using moving-average imputation benchmarked against adjacent material classes.

Data Validation & Update Cycle

Outputs pass a three-level review covering variance checks against historical series, peer review by domain specialists, and management sign-off. We refresh every twelve months, with interim updates when regulatory or supply shocks materially alter assumptions, ensuring clients always receive the latest vetted view.

Why Mordor's Nitinol Medical Devices Baseline Commands Confidence

Published market values often diverge because firms pick different device lists, price bases, and refresh cadences. According to Mordor Intelligence, our 2025 baseline of USD 2.89 billion relies on a strictly medical, finished-product lens, annual ASP audits, and transparent variable tracking.

Key Gap Drivers include whether archwire and raw-material sales are bundled, the point in the channel at which revenue is booked, inflation translation choices, and the frequency of assumption refresh.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.89 bn (2025) | Mordor Intelligence | - |

| USD 4.10 bn (2024) | Global Consultancy A | Includes orthodontic archwires and raw nitinol stock, uses factory-gate prices |

| USD 4.66 bn (2024) | Industry Journal B | Bundles industrial actuators, five-year refresh; exchange rates fixed at 2020 average |

| USD 14.50 bn (2023) | Regional Consultancy C | Adds orthopedic staples and dental wires, applies list prices without volume discounts |

The comparison shows that scope breadth and pricing assumptions explain most gaps. Our disciplined device list, verified ASPs, and annual refresh cadence together make Mordor's baseline the dependable starting point for strategic planning.

Key Questions Answered in the Report

How does device miniaturization influence adoption of nitinol-based interventions?

Thinner nitinol components allow delivery through smaller catheters, enabling procedures in tortuous or previously inaccessible anatomies and improving patient eligibility for minimally invasive care.

Why are ambulatory surgical centers increasingly choosing nitinol devices?

Nitinol’s flexibility supports same-day, low-trauma procedures that align with outpatient workflows, helping centers cut recovery times and meet payer incentives for cost-efficient care.

What role do surface-modification techniques play in the competitive landscape?

Advanced coatings such as low-temperature plasma oxidation reduce nickel ion release and enhance endothelialization, giving manufacturers a differentiation lever based on long-term biocompatibility.

Which clinical evidence most strongly persuades physicians to switch to nitinol implants?

Real-world studies showing high patency and occlusion success rates—especially in complex cardiovascular and neurovascular cases—boost confidence in nitinol’s durability versus conventional alloys.

How are supply-chain strategies evolving among nitinol component suppliers?

Firms are vertically integrating melting, tubing, and gun-drilling capabilities to secure raw alloy availability and shrink lead times, positioning themselves as reliable partners for OEMs.

How is reimbursement influencing adoption?

Expanded Medicare pass-through payments and new CPT codes for nitinol implants reduce financial hurdles, accelerating clinical uptake across multiple specialties.

Page last updated on: