Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.51 Billion |

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 14.10 Billion |

| Growth Rate (2026 - 2031) | 16.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Cybersecurity Market Analysis by Mordor Intelligence

The ASEAN cybersecurity market size was valued at USD 5.51 billion in 2025 and estimated to grow from USD 6.44 billion in 2026 to reach USD 14.1 billion by 2031, at a CAGR of 16.95% during the forecast period (2026-2031). Rising digital uptake, stricter data-protection laws and expanding attack surfaces from cloud, IoT and 5G ecosystems underpin this growth. Singapore leads regional spending, Vietnam records the fastest incident growth, and managed service adoption accelerates across all member states as enterprises look to close skills gaps. Fragmented regulation, high ownership costs for multi-cloud SecOps and talent shortages temper the outlook, yet broad-based public-private investment in zero-trust, SASE and government-funded SOC programs continues to unlock new opportunities for both global providers and regional specialists.

Key Report Takeaways

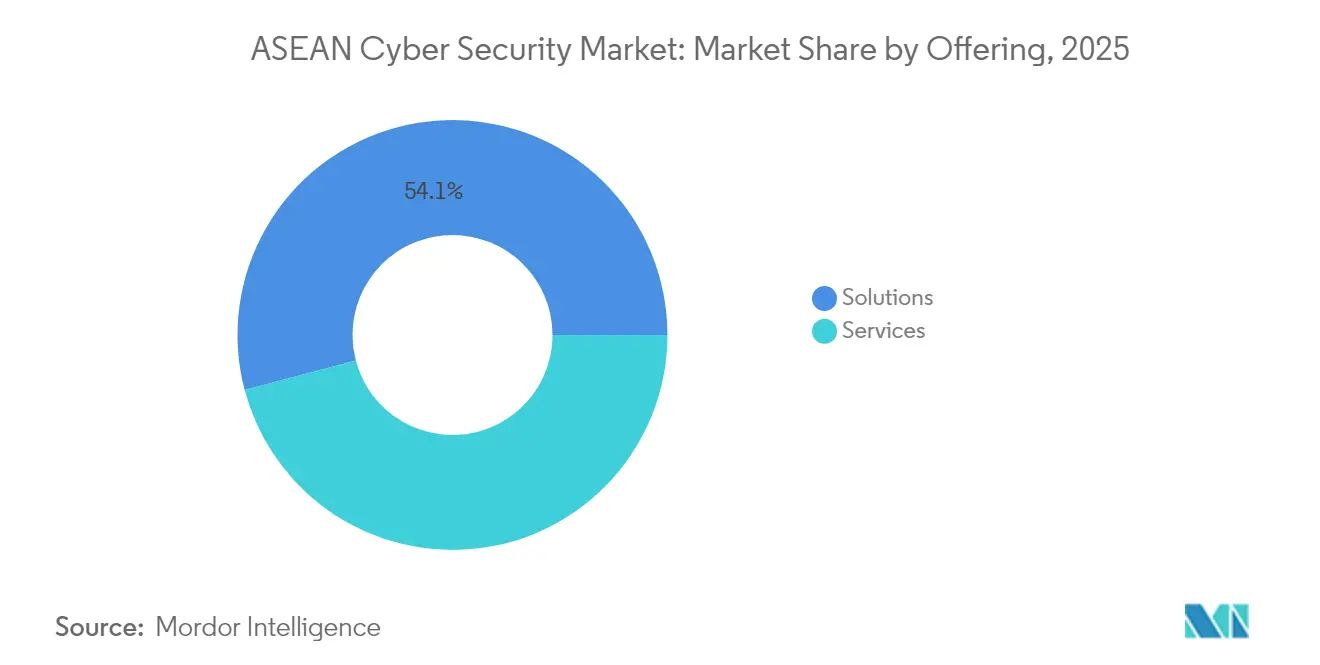

- By offering, solutions captured 54.12% of ASEAN cybersecurity market share in 2025, while managed services post the highest CAGR at 18.95% to 2031.

- By deployment mode, cloud held 57.34% of the ASEAN cybersecurity market size in 2025 and is advancing at a 19.88% CAGR through 2031.

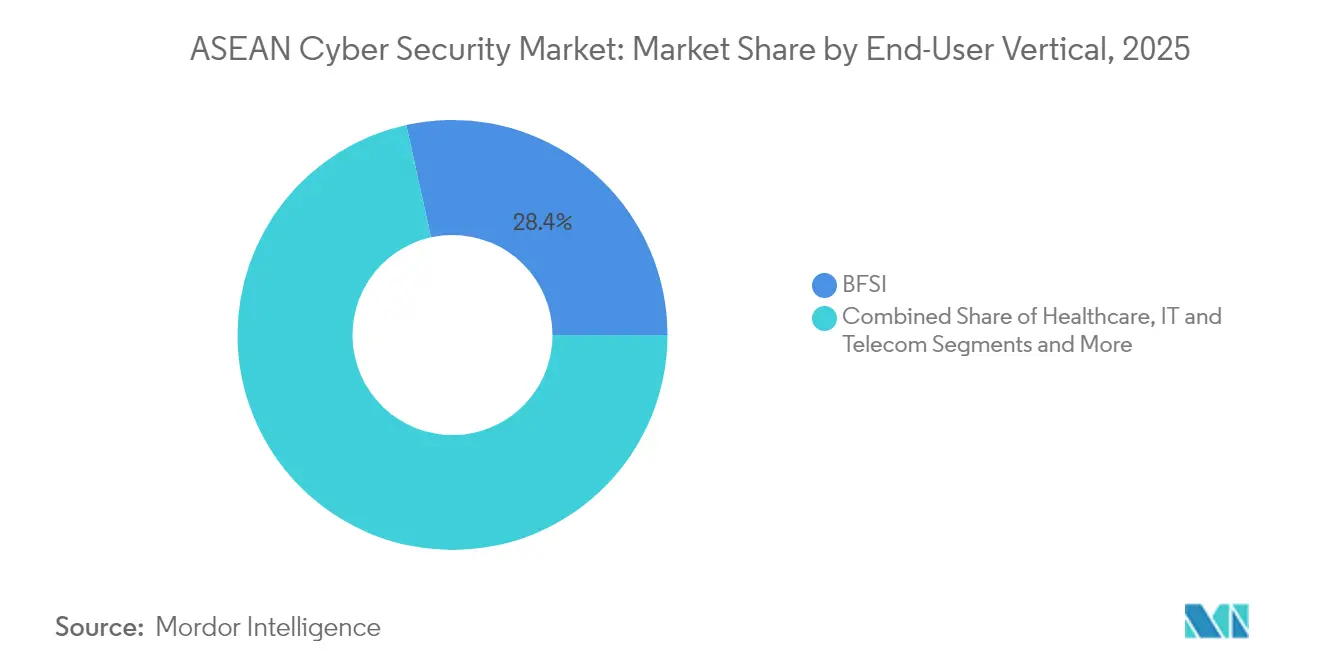

- By end-user vertical, BFSI led with 28.45% revenue share in 2025; healthcare is expanding at a 20.12% CAGR to 2031.

- By enterprise size, large enterprises commanded 62.05% share of the ASEAN cybersecurity market in 2025, whereas SMEs record the briskest 18.55% CAGR to 2031.

- By country, Singapore retained 26.22% share in 2025; Vietnam is forecast to grow fastest at 21.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying zero-trust adoption in Singapore-led BFSI sector | +3.2% | Singapore, Malaysia, Thailand | Medium term (2-4 years) |

| Explosive IoT-inflicted attack surface in Indonesian manufacturing & smart-cities | +2.8% | Indonesia, Thailand, Vietnam | Long term (≥ 4 years) |

| ASEAN government-funded SOC & CERT investments | +2.1% | Malaysia, Singapore, Thailand | Short term (≤ 2 years) |

| Rapid SASE roll-outs among Thai telcos to monetise 5G enterprise edge | +1.9% | Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| Growing cyber-insurance mandates for listed firms | +1.6% | Singapore, Malaysia | Short term (≤ 2 years) |

| Surging e-commerce data-leak fines under PDPA | +1.4% | Thailand, Philippines, Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Zero-Trust Adoption in Singapore-led BFSI Sector

Banks in Singapore accelerated zero-trust rollouts after the Monetary Authority updated its technology risk guidelines in 2024[1]Monetary Authority of Singapore, “Technology Risk Management Guidelines 2024,” mas.gov.sg. Financial institutions across Malaysia and Thailand now mirror the approach to secure open-banking APIs, mobile wallets and cloud cores. Globe’s GCash grew its internal cyber team five-fold to protect PHP 1 trillion in annual transactions, illustrating how headcount expansion parallels architectural change. Vendors gain from higher licence volumes for identity governance, micro-segmentation and continuous authentication, while service providers benefit from design and managed detection mandates. As regulators emphasise resilience tests, zero-trust has moved from best practice to baseline, underpinning sustained spending momentum in the ASEAN cybersecurity market.

Explosive IoT-Inflicted Attack Surface in Indonesian Manufacturing and Smart-Cities

Industry 4.0 pilots across Java and Sumatra add sensors, AGVs and edge gateways that were never hardened for hostile networks. Alliance Laundry Systems’ 5G-enabled line in Batam mirrors projects across ASEAN, with each plant hosting tens of thousands of unmanaged endpoints that demand network segmentation, NAC and anomaly analytics. Local system integrators partner global OEMs to retrofit OT-security, while insurers increasingly insist on asset-discovery audits before underwriting. Similar smart-city grids in Bangkok and Ho Chi Minh City amplify the region-wide call for IoT-centric threat modelling, sustaining double-digit growth in the ASEAN cybersecurity market.

ASEAN Government-Funded SOC and CERT Investments

Malaysia’s MyCERT 2.0 and Singapore’s national SOC roadmap collectively bring more than USD 150 million in new detection and response spending to market before 2026. NEC’s ICON facility in Johor delivers 24/7 triage across 10 Asian economies, demonstrating how private players monetize public funding. Early-warning data feeds, cyber-range exercises and graduate scholarships are scaling the home-grown talent pool, closing regional capability gaps that hindered adoption among SMEs. This push unlocks near-term demand for analytics platforms, SIEM upgrades and red-team retainers, fueling managed-service revenue in the ASEAN cybersecurity market.

Surging E-Commerce Data-Leak Fines Under PDPA

Thailand’s PDPA fines up to THB 5 million triggered a compliance rush among platforms and payment gateways, boosting adoption of tokenisation, database encryption and breach-notification workflows[2]Sangfor Technologies, “PDPA Compliance Costs in ASEAN,” sangfor.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total-cost-of-ownership for multi-cloud SecOps in SMEs | -2.3% | Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Fragmented data-protection regulations across 10 member states | -1.8% | ASEAN-wide | Long term (≥ 4 years) |

| Shortage of GIAC-certified professionals in emerging CLMV cluster | -1.5% | Cambodia, Laos, Myanmar, Vietnam | Long term (≥ 4 years) |

| Low cyber-resilience culture within family-owned conglomerates | -1.2% | Indonesia, Thailand, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total-Cost-of-Ownership for Multi-Cloud SecOps in SMEs

Only 11% of Vietnamese firms report incident preparedness despite facing 659,000 attacks in 2024. The need for dedicated tooling across AWS, Azure and Google Cloud drives licence duplication, complex integration and spiraling analyst workloads. Training, threat-intel feeds and 24/7 monitoring further elevate opex, forcing many SMEs to opt for baseline controls, widening the exposure gap inside the ASEAN cybersecurity market.

Fragmented Data-Protection Regulations Across 10 Member States

Divergent breach timelines, localization clauses and penalty thresholds oblige multinationals to build country-specific control stacks. Legal, audit and engineering hours multiply, inflating compliance budgets and delaying platform rollouts. Providers must customize product modules for every jurisdiction, slowing regional SKU launches and marginally suppressing growth in the ASEAN cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Lead Despite Services Acceleration

Solutions captured 54.12% of ASEAN cybersecurity market share in 2025, anchored by demand for integrated platforms that unify endpoint, network and cloud controls. Identity-and-access suites, next-generation firewalls and XDR stacks dominate initial purchase cycles, creating lock-in effects that fortify vendor renewals. Professional and managed services rise at 18.95% CAGR as enterprises confront skills shortages and regulatory audits that require continuous monitoring and bespoke compliance mapping. Malaysia’s plan to train 25,000 cyber defenders by 2025 underscores the services imperative.

The ASEAN cybersecurity market size attributable to services will likely reach mid-single-billion-dollar levels by 2031 as organizations outsource tier-one alert handling, purple-team simulations and compliance documentation. Regional MSSPs bundle advisory, integration and operations in outcome-based contracts, accelerating adoption among late-digitizing sectors such as manufacturing and utilities.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments held 57.34% of the ASEAN cybersecurity market size in 2025, rising on the back of SaaS adoption among SMEs and greenfield ventures. Prisma Cloud, GuardDuty and Defender for Cloud enable rapid threat-hunting, posture scoring and automated remediation without upfront capex, making them attractive in price-sensitive economies. Hybrid reference architecture remains for banks and healthcare groups bound by data-residency mandates, yet even these institutions extend visibility tooling to multi-cloud workloads.

The ASEAN cybersecurity market continues to record 19.88% CAGR in cloud-security spend as shift-left DevSecOps, container security and CNAPP platforms become default procurement. On-premise appliance refresh cycles stretch to five years or more, solidifying the structural tilt toward cloud-native controls.

By End-User Vertical: BFSI Leads While Healthcare Surges

BFSI generated 28.45% of regional revenue in 2025, reflecting layered defence strategies, SWIFT CSP obligations and continual red-team testing. Open-API ecosystems drive adoption of API gateways, fraud analytics and real-time threat-intelligence feeds. Healthcare outpaces all other verticals with 20.12% CAGR after high-profile data breaches and telemedicine expansion. Singapore’s SingHealth episode remains a cautionary benchmark that propels EMR encryption, micro-segmentation and identity-proofing mandates.

Retail, manufacturing and energy sectors broaden spend as ransomware crews pivot to supply-chain attacks and OT disruption. As every vertical integrates IoT and edge analytics, baseline cyber-hygiene evolves into mission-critical uptime insurance, cementing growth prospects for the ASEAN cybersecurity market.

By End-User Enterprise Size: SMEs Emerge as Growth Engine

Large organizations still account for 62.05% of revenue, yet outsized 18.55% CAGR among SMEs signals democratization of enterprise-grade protection. Cloud-delivered EDR, pay-as-you-go SIEM and incident-response retainers enable risk-based scaling without heavy capex. Public-sector voucher schemes in Thailand and Indonesia further subsidize SME onboarding, expanding addressable base for MSSPs and SaaS vendors.

As cyber-insurance carriers tighten underwriting, even micro-enterprises must evidence endpoint hardening, MFA and backup governance, embedding cybersecurity into baseline operational checklist. The ASEAN cybersecurity market therefore widens beyond top-tier conglomerates to encompass long-tail businesses that collectively employ the majority of the region’s workforce.

Geography Analysis

The ASEAN cybersecurity market remains geographically concentrated in Singapore, Malaysia and Thailand, yet growth velocity skews to Vietnam, Indonesia and the Philippines. Singapore’s 26.22% share is anchored by a sophisticated banking sector, sovereign digital initiatives and the Cybersecurity Agency’s prescriptive guidelines for AI, quantum and critical infrastructure defence. Deep talent pools and sovereign-cloud frameworks attract global SOC investments, reinforcing the city-state’s hub status.

Malaysia follows on the back of MyDIGITAL and MyCERT 2.0, which channel matching grants into SOC-as-a-service and skills pipelines. Johor’s ICON centre and Cyberjaya’s BlackBerry-backed academy exemplify federal-state industry alignment. Thailand leverages 5G roll-outs, EEC manufacturing corridors and PDPA enforcement to inject urgency into enterprise roadmaps.

Vietnam's cybersecurity 21.05% CAGR underscores its leapfrog trajectory from low-base spending to cloud-first deployments across fintech, e-commerce and smart-city pilots. Indonesia and the Philippines, with their vast consumer bases and super-app ecosystems, present substantial greenfield demand for cloud, identity and fraud-mitigation controls. Brunei, Cambodia, Laos and Myanmar remain nascent yet show accelerating project pipelines as digital government programmes take root.

Competitive Landscape

ASEAN’s cybersecurity landscape features a blend of global heavyweights, regional champions and niche innovators. Palo Alto Networks, Cisco and Fortinet defend incumbent shares through platform bundling and curated partner ecosystems. Ensign InfoSecurity and StarHub integrate connectivity, cloud and security into unified service stacks tailored for local compliance, gaining traction with mid-market clients[3]StarHub, “Modern Digital Infrastructure Press Release,” starhub.com .

Fragmentation endures as no vendor exceeds 15% regional revenue, yet ongoing consolidation—such as telcos acquiring MSSPs—nudges the market toward tighter concentration. AI-driven analytics, SOAR orchestration and attack-surface management represent key battlegrounds where disruptors challenge legacy appliances. Vendors differentiate through local SOC footprints, multilingual support and regulatory mapping accelerators that lower total compliance cost.

Strategic alliances with academia and government unlock grant funding while boosting reputation credentials. As talent scarcity persists, players offering training, certification sponsorships and career pathways gain competitive heft alongside technical portfolios.

ASEAN Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems, Inc.

Fujitsu Thailand Co., Ltd.

Red Sky Digital Ventures Ltd.

Info Security Consultants Co., Ltd. (INFOSEC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Palo Alto Networks expanded its Prisma Cloud security suite deployment across the Philippines, targeting enterprises migrating to cloud environments with automated risk identification and mitigation features.

- April 2025: StarHub established a dedicated Information Security Office and appointed a Chief Information Security Officer to strengthen data protection and cyber resilience capabilities.

- March 2025: Singapore’s Cyber Security Agency published comprehensive guidelines for securing Generative AI and Large Language Models, covering data privacy controls and secure code-generation practices.

- March 2024: NEC opened the Intelligent Center Operations of NEC (ICON) cybersecurity centre in Malaysia’s Johor state, offering 24/7 network monitoring across 10 Asian markets.

ASEAN Cybersecurity Market Report Scope

The market is defined by the revenue accrued from the sale of cybersecurity solutions offered by players operating in the market across the ASEAN region.

The ASEAN cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solutions] and services [professional services and managed services]), by deployment mode (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Services | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Country

| Singapore |

| Malaysia |

| Thailand |

| Indonesia |

| Philippines |

| Vietnam |

| Rest of ASEAN (Brunei, Cambodia, Laos, Myanmar) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Services | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Country | Singapore | |

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Philippines | ||

| Vietnam | ||

| Rest of ASEAN (Brunei, Cambodia, Laos, Myanmar) | ||

Key Questions Answered in the Report

What is the current value of the ASEAN cybersecurity market?

The market is valued at USD 6.44 billion in 2026, reflecting strong regional demand for security solutions.

How fast is the ASEAN cybersecurity market expected to grow?

It is forecast to expand at a 16.95% CAGR, reaching USD 14.1 billion by 2031.

Which country leads ASEAN cybersecurity spending?

Singapore holds the largest 26.22% share owing to its mature financial sector and proactive regulations.

Which vertical is growing fastest within the market?

Healthcare posts the highest 20.12% CAGR through 2031 as patient-data protection becomes critical.

Why are SMEs becoming a key growth segment?

Regulatory pressure, cyber-insurance requirements and cloud-based security subscriptions make enterprise-grade protection accessible to smaller firms, driving an 18.55% CAGR in SME spend.

Page last updated on: