Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

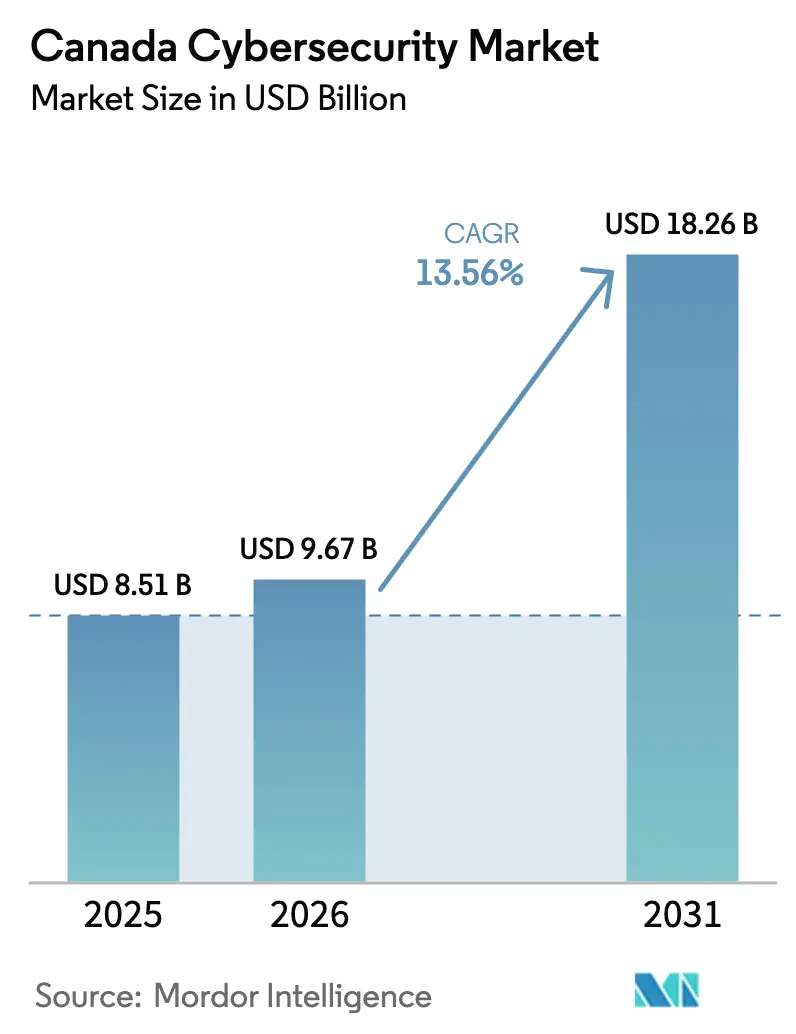

| Base Year Market Size (2025) | USD 8.51 Billion |

| Market Size (2026) | USD 9.67 Billion |

| Market Size (2031) | USD 18.26 Billion |

| Growth Rate (2026 - 2031) | 13.56% CAGR |

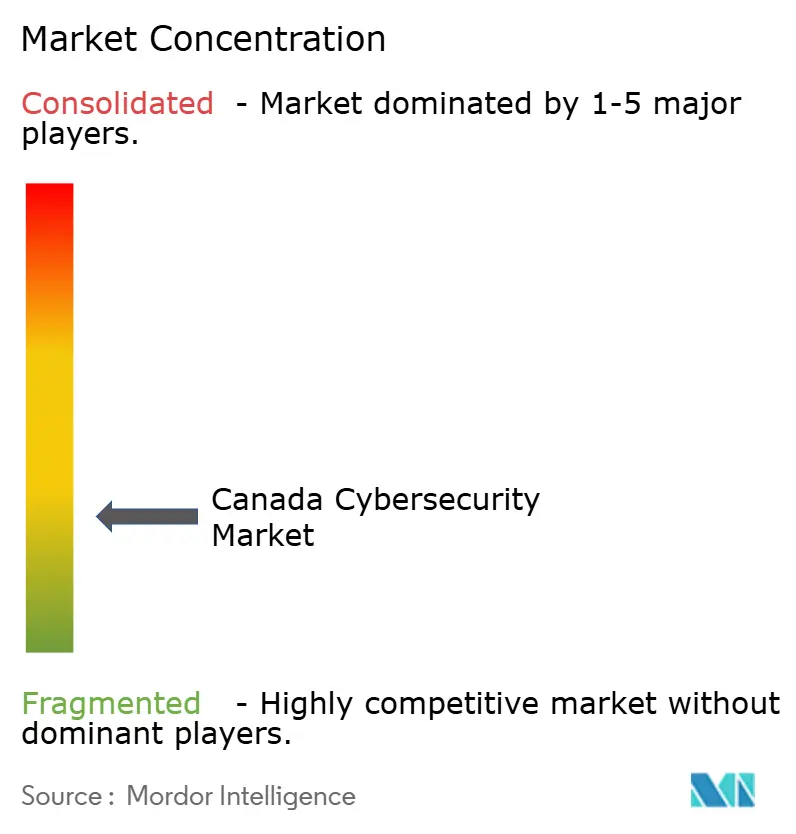

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Cybersecurity Market Analysis by Mordor Intelligence

The Canada Cybersecurity Market size was valued at USD 8.51 billion in 2025 and is estimated to grow from USD 9.67 billion in 2026 to reach USD 18.26 billion by 2031, at a CAGR of 13.56% during the forecast period (2026-2031). Growing ransomware sophistication, stricter federal breach-notification rules, and accelerated cloud adoption among small and medium enterprises are converging to push security from a one-time purchase to a continuous operational discipline. Vendors able to bundle threat intelligence, detection, and response into integrated platforms are gaining ground as boards seek unified visibility over expanding attack surfaces. Fragmented provincial mandates create additional demand for compliance-automation tools, while sovereign-data requirements give Canadian-born providers a competitive wedge against multinational rivals. Intensifying competition, rising incident costs, and sizable public-sector investments position the Canada cybersecurity market for sustained double-digit growth through the forecast horizon.

Key Report Takeaways

- By offering, solutions led with a 62.73% revenue share of the Canada cybersecurity market in 2025, while services are forecast to expand at a 15.22% CAGR through 2031.

- By deployment mode, cloud architectures captured 63.84% of the Canada cybersecurity market share in 2025 and will accelerate at a 15.32% CAGR to 2031.

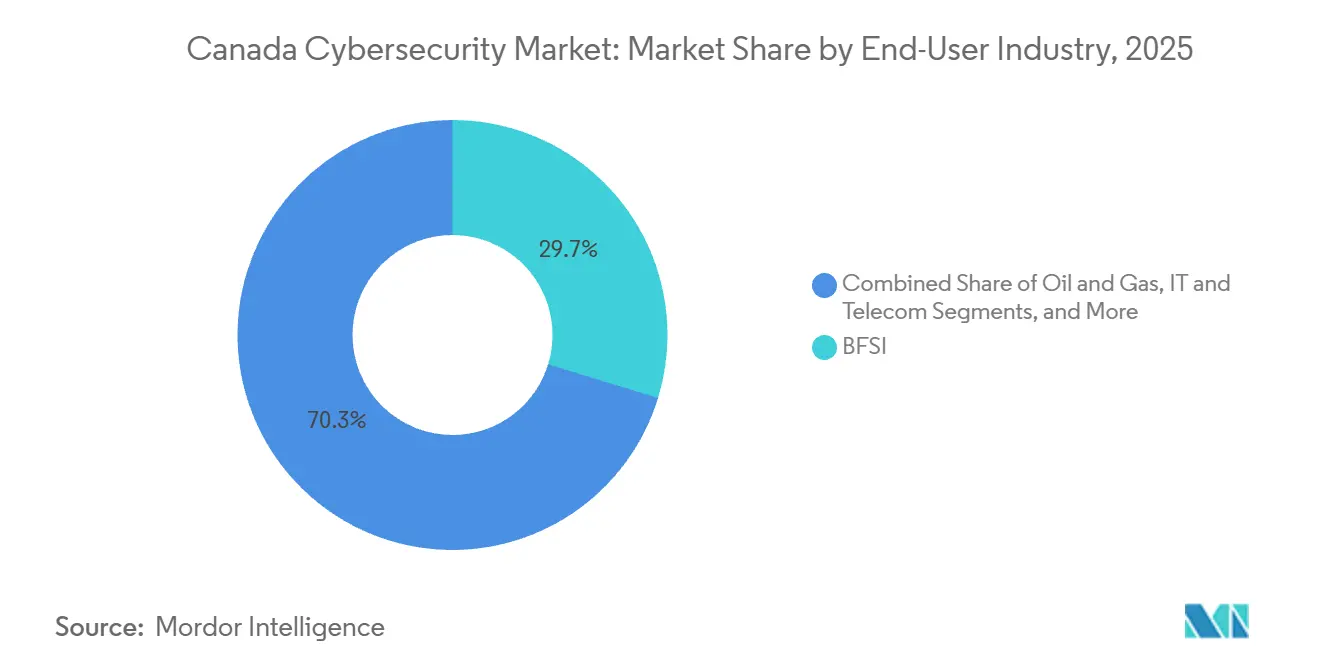

- By end-user industry, banking, financial services, and insurance held a 29.73% revenue share of the Canada cybersecurity market in 2025; healthcare is projected to post the fastest 14.66% CAGR through 2031.

- By enterprise size, large organizations accounted for 61.74% of 2025 spending of the Canada cybersecurity market, whereas small and medium enterprises will rise at a 15.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency and cost of ransomware incidents | +2.8% | National, pronounced in healthcare and municipal services | Short term (≤ 2 years) |

| Tightening federal regulation (Bill C-26 and CCSPA) | +3.2% | National, sector-specific enforcement in BFSI, telecom, energy, transportation | Medium term (2-4 years) |

| Accelerated cloud migration by Canadian SMEs | +2.4% | National, higher adoption in Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Public-sector digital-service expansion and Zero-Trust mandates | +2.1% | Federal agencies and provincial digital-service teams | Medium term (2-4 years) |

| Province-specific critical-infrastructure mandates | +1.5% | Ontario, Quebec, Alberta, British Columbia | Long term (≥ 4 years) |

| “Buy Canadian Cyber” federal procurement platform | +1.2% | Federal procurement and downstream public contracts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Frequency and Cost of Ransomware Incidents

High-profile attacks demonstrate that total recovery costs far exceed ransom payments, encompassing system rebuilds, legal counsel, and reputational remediation. The CAD 5.7 million (USD 4.2 million) paid by the City of Hamilton in February 2024 highlights how multi-stage extortion cripples essential services and triggers public scrutiny. Healthcare suffered a major blow when 326,800 patient records were exposed during the TransForm incident, which spurred a CAD 480 million (USD 355 million) class-action lawsuit. Retail vulnerability was illustrated by London Drugs, which closed 79 stores for a week and faced employee-notification expenses. Statistics Canada noted that 16% of businesses endured a cyber event in 2023, with combined recovery and prevention outlays surpassing USD 9 billion. The National Cyber Threat Assessment 2025-2026 singles out ransomware-as-a-service ecosystems as the leading threat vector, pushing boards to classify cyber risk as an enterprise-continuity issue.[1] Statistics Canada, “Cybersecurity and Cybercrime Survey, 2023,” statcan.gc.ca

Tightening Federal Regulation (Bill C-26 and CCSPA)

Parliament has compressed incident-reporting windows and elevated cybersecurity oversight to the board level. Bill C-26 obliges critical-infrastructure operators to implement formal security programs, submit to audits, and face penalties for non-compliance. The Canadian Consumer Privacy Act imposes a 72-hour notification rule and grants the Privacy Commissioner order-making power, prompting enterprises to adopt automated detection and response workflows. Guideline B-13 from the banking regulator requires board-level cyber-risk governance and annual penetration testing, embedding cybersecurity in prudential oversight. The 2025 National Cyber Security Strategy earmarks USD 28 million for threat-intelligence collaboration, while Budget 2024 allocates USD 678.5 million over five years to Zero-Trust pilots across federal agencies. Collectively, these measures heighten compliance pressure and accelerate platform consolidation.

Accelerated Cloud Migration by Canadian SMEs

Small and medium enterprises are moving workloads to hyperscale platforms that provide built-in encryption, identity management, and threat analytics. Cloud deployment held 63.84% share in 2025 and is projected to outpace on-premise growth at a 15.32% CAGR. Federal cloud-first guidance has set a procurement benchmark replicated by provinces and municipalities. Managed detection and response subscriptions bundle endpoint, SIEM, and analyst triage into one monthly fee, giving resource-constrained firms 24/7 coverage without capital expenditure. CyberSecure Canada certification supplies vetted provider lists, lowering search costs and reinforcing cloud uptake among the long-tail of businesses.

Public-Sector Digital-Service Expansion and Zero-Trust Mandates

Government digitization programs are replacing perimeter-based defenses with identity-centric controls. Treasury Board funding supports Zero-Trust pilots that authenticate every user and device before granting access. Bill C-72 forces healthcare networks to enable cross-provincial data exchange, necessitating robust encryption and breach-detection capabilities. Ontario requires privacy-impact assessments within 24 hours of an incident, while British Columbia offers subsidized assessments to small and medium enterprises. Public-sector standards thus cascade into private-sector procurement criteria, spurring demand for identity and access management and micro-segmentation tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute mid-level cyber-talent shortage | -2.1% | National hot spots in Toronto, Montreal, Vancouver | Medium term (2-4 years) |

| High TCO of advanced XDR/Zero-Trust architectures | -1.8% | National, heaviest on SMEs and mid-market firms | Short term (≤ 2 years) |

| Compliance overlap drives audit costs | -1.2% | BFSI and healthcare face multi-agency oversight | Medium term (2-4 years) |

| SME budget fatigue and MDR subscription churn | -1.0% | Retail, hospitality, professional services | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Mid-Level Cyber-Talent Shortage

Canada requires thousands of additional analysts who can triage alerts, conduct forensics, and refine detection rules. Universities are not producing enough graduates with three to seven years of experience, causing salary inflation that erodes security-operations budgets. The gap is widest for small and medium enterprises, which must rely on managed services because they cannot match the compensation packages offered by financial institutions and technology firms. Government workforce-development programs aim to expand talent pipelines, yet the shortage will persist through the medium term and temper adoption of complex security architectures.[2]Innovation, Science and Economic Development Canada, “Quantum-Safe Cryptography Report,” ic.gc.ca

High TCO of Advanced XDR/Zero-Trust Architectures

Licensing alone understates the full expense of extended detection and response and Zero-Trust frameworks. Organizations must inventory assets, rewrite access policies, and retrain staff, consuming as much as 30% of annual security budgets before measurable risk reduction appears. Small and medium enterprises struggle with subscription fatigue as endpoint, email, identity, and SIEM services add recurring fees. This cost pressure slows migration to integrated platforms and sustains demand for bundled managed services that shift integration burdens to providers.[3]Canadian Centre for Cyber Security, “National Cyber Threat Assessment 2025-2026,” cyber.gc.ca

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Solutions as Security Turns Operational

Solutions represented 62.73% of 2025 revenue, yet services are poised to expand faster than solutions sales, advancing at a 15.22% CAGR through 2031 as organizations view protection as a continuous discipline rather than a capital purchase. Managed detection and response dominates services growth, particularly among firms lacking dedicated security staff. Professional services consulting, integration, and training rise when enterprises deploy Zero-Trust or extended detection and response platforms that demand policy overhauls.

The installed base of firewalls, endpoint agents, and identity platforms ensures solutions retain a sizeable footprint, but growth clusters around cloud security and identity and access management as workloads migrate and authentication replaces perimeter defenses. Application-layer protection gains momentum amid heightened software-supply-chain attacks, while integrated risk-management dashboards help boards monitor compliance. This operational tilt underscores that the Canada cybersecurity market is shifting from isolated tools to outcome-based services that merge technology and talent.

By Deployment Mode: Cloud Architectures Cement Leadership

Cloud deployments held 63.84% Canada cybersecurity market share in 2025 and are projected to rise at a 15.32% CAGR, propelled by hyperscalers’ embedded threat analytics and economies of scale. Federal and provincial cloud-first mandates create clear procurement pathways, and Microsoft’s USD 5.5 billion data-center expansion underscores provider confidence in sovereign-cloud demand. Small and medium enterprises benefit from pay-as-you-go models that compress implementation timelines and outsource maintenance.

On-premise installations persist in sectors governed by strict data-sovereignty or operational-technology constraints, notably banking, energy, and critical infrastructure. Hybrid strategies that pair local data stores with cloud-based analytics balance control and scalability. Telecommunications carriers such as Bell Canada are capitalizing on the trend by reselling managed cloud security, cementing their role as intermediaries between hyperscalers and risk-averse customers. Over the forecast horizon, pure on-premise rollouts will decline, but hybrid architectures will keep local data centers relevant within the broader Canada cybersecurity market.

By End-User Industry: Healthcare Surges While BFSI Retains Scale

Banking, financial services, and insurance held 29.73% of 2025 outlays, buoyed by regulator-mandated board oversight, annual penetration testing, and ISO-aligned response plans. Guideline B-13 compels institutions to treat cyber risk on par with credit exposure, keeping budgets robust. Healthcare, conversely, is expected to record a 14.66% CAGR as Bill C-72 mandates interoperable electronic records, heightening liability for breaches and fueling demand for encryption and identity tools.

Government entities accelerate spending by modernizing citizen services and imposing 24-hour reporting windows, while energy and utilities protect sprawling operational-technology estates that adversaries view as high-value targets. Retail and consumer sectors invest in business-continuity tools after headline-grabbing outages. Across segments, managed detection and response bridges talent gaps, underscoring why services will outrun solutions within the Canada cybersecurity market size forecast.

By Enterprise Size: SMEs Embrace Managed Detection and Response

Large enterprises accounted for 61.74% of 2025 revenue through sizable security operations centers and multilayered platforms. However, small and medium enterprises are forecast to grow at 15.42% annually through 2031, propelled by subscription-based offerings that bundle endpoint protection, SIEM, and expert triage. Rising cyber-insurance premiums and stricter underwriting standards now require evidence of continuous monitoring, nudging SMEs toward certified providers listed under the CyberSecure Canada program.

Sovereign-data residency plays to domestic vendors’ strengths. Firms such as eSentire, Arctic Wolf, and Field Effect compete successfully against multinational platforms by combining rapid incident response with Canadian storage and aligning with customer compliance needs. As board-level scrutiny spreads from large corporations to mid-market firms, SMEs will allocate a larger share of their IT budgets to security, propelling the services-led growth engine of the Canada cybersecurity market.

Geography Analysis

Ontario, Quebec, British Columbia, and Alberta account for the bulk of the Canada cybersecurity market, yet each province enforces distinct mandates that shape local demand. Ontario’s Bill 194 requires privacy-impact assessments for all public-sector digital services and imposes a 24-hour incident-reporting window, spurring rapid procurement of automation tools. Quebec’s Bill 82 established the Ministry of Cybersecurity and Digital Affairs and introduced mandatory notification for private-sector breaches, while launching a cross-provincial digital-identity framework. Alberta’s 2024 strategy emphasizes quantum readiness and public-private information sharing, positioning the province as a hub for post-quantum cryptography research. British Columbia’s CyberBC program subsidizes assessments for small and medium enterprises, broadening the addressable market for managed service providers.

Provincial fragmentation complicates compliance for national enterprises but creates opportunities for vendors offering multi-jurisdictional reporting dashboards. Federal initiatives mitigate disjointed rules, the National Cyber Security Strategy funds threat-intelligence exchange, and Budget 2024 backs Zero-Trust pilots across agencies. Treasury Board allocations accelerate identity-centric controls that will ripple through provincial procurement templates. Together, these programs elevate baseline expectations for incident detection and reporting across Canada cybersecurity market stakeholders.

Toronto, Montreal, and Vancouver anchor the vendor ecosystem, hosting headquarters for eSentire, CGI, and 1Password and benefiting from proximity to financial hubs and research universities. Calgary leverages its energy sector to drive operational-technology security contracts. Even smaller provinces feel the impact of rising threat activity. Saskatchewan faced a healthcare breach that compromised thousands of patient files, underscoring that geographic scale offers no immunity. Overall, spending correlates with economic weight, but targeted provincial incentives ensure that growth opportunities proliferate nationwide, reinforcing the diversified geography of the Canada cybersecurity market size.

Competitive Landscape

The Canada cybersecurity market is fragmented, with no single player exceeding a 10% share. Multinational platforms Microsoft, Cisco, Palo Alto Networks compete alongside Canadian specialists such as eSentire, Arctic Wolf, Field Effect, and BlackBerry Cybersecurity, whose local data residency and rapid incident response resonate with compliance-minded buyers. Arctic Wolf’s USD 160 million purchase of BlackBerry’s Cylance endpoint business integrates artificial-intelligence prevention with managed detection and response, illustrating the rush toward unified visibility.

Systems integrators are also active. CGI’s December 2025 acquisition of OBS augments its managed services and positions the firm to bundle security with digital-transformation engagements. Telecommunications carriers are expanding into security through partnerships and acquisitions, capitalizing on existing network footprints. White-space opportunities persist in operational-technology defense, compliance automation, and software supply-chain assurance, niches that firms such as Cybeats and Magnet Forensics are addressing through specialized tooling.

Investment momentum supports continued innovation. Microsoft’s USD 5.5 billion sovereign-cloud build-out, IBM’s USD 155 million semiconductor research infusion, and 1Password’s USD 75 million funding round all underscore confidence in domestic growth potential. Against this backdrop, managed detection and response vendors are best positioned to capture share as clients shift from point solutions to outcome-based subscriptions. Competitive intensity is expected to rise, yet the diverse mix of global and local players ensures vibrant choice for buyers across the Canada cybersecurity market.

Canada Cybersecurity Industry Leaders

IBM Canada Ltd.

Cisco Systems Canada Co.

Microsoft Canada Inc.

Check Point Software Technologies Ltd.

Palo Alto Networks (Canada) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microsoft Canada announced a CAD 7.5 billion (USD 5.5 billion) investment to expand AI and cloud infrastructure, with capacity scheduled for H2 2026.

- December 2025: CGI acquired OBS to deepen cybersecurity and digital-transformation capabilities.

- November 2025: IBM Canada committed CAD 210 million (USD 155 million) to semiconductor R&D supporting quantum computing and advanced cryptography.

- November 2025: Field Effect was named a Leader in managed detection and response by a leading analyst firm.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canada cybersecurity market as all business-to-business spending in Canada on software, dedicated security appliances, and fee-based security services that actively prevent, detect, or respond to unauthorized digital access. Revenues are recorded at vendor invoice level and converted to U.S. dollars using the average 2024 CAD-USD rate.

Scope Exclusions: Pure physical security devices and discretionary consumer antivirus packages are not covered.

Segmentation Overview

- By Offering

- Solutions

- Application Security

- Cloud Security

- Data Security

- Network Security

- Endpoint Security

- Infrastructure Protection

- Integrated Risk Management

- Identity and Access Management (IAM)

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premise

- By End-user Industry

- BFSI

- Government and Public Sector

- Oil and Gas

- IT and Telecom

- Retail, E-commerce and Consumers

- Manufacturing and Industrial

- Energy and Utilities

- Healthcare

- Other End-user Industries

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with CISOs, managed security providers, policy makers, and channel partners across Ontario, Québec, Alberta, and British Columbia. The discussions confirmed license renewal cycles, zero-trust adoption rates, and median spend per endpoint, tightening key model coefficients and closing data gaps revealed during desk work.

Desk Research

We began by mapping the regulatory and threat landscape through open data from the Canadian Centre for Cyber Security, Public Safety Canada, Statistics Canada, and the Canadian Internet Registration Authority, which clarified enterprise counts, incident rates, and IT outlays. Public company filings, provincial tender databases, and reputable press further revealed contract values and pricing shifts. Subscription tools such as Dow Jones Factiva and D&B Hoovers supplemented vendor financial trails. The sources cited illustrate our approach and are not exhaustive; many additional documents informed data collection, validation, and clarification.

A second pass drew on ITU telecom indicators, Chartered Professional Accountants of Canada surveys, and peer-reviewed journals to obtain cloud-workload penetration, breach costs, and SME digitization indices. These metrics anchored segment shares and driver trend lines ahead of model build.

Market-Sizing & Forecasting

We first applied a top-down approach that scales national IT expenditure by security-spend ratios, then corroborated totals through selective bottom-up checks, sampled vendor revenue roll-ups, channel ASP × volume, and capacity-utilization data. Core variables include connected-enterprise counts, average breach cost, cloud workload share, endpoint density, regulatory penalty ceilings, and cybersecurity wage inflation. A multivariate regression projects each driver through 2030, with an ARIMA overlay smoothing near-term volatility. Divergences beyond five percent trigger iterative reconciliation to the most reliable stream.

Data Validation & Update Cycle

Outputs flow through three-level analyst review, variance testing against external indices, and anomaly flags in our internal dashboard. Mordor refreshes figures annually and issues interim updates after material legislative or macro events. A final sense-check occurs just before publication.

Why Mordor's Canada Cybersecurity Baseline Commands Reliability

Published estimates often diverge because research firms widen or narrow scope, apply different CAD-USD conversions, or refresh on uneven schedules. Mordor's disciplined definition, annual cadence, and dual-path modeling make our baseline both transparent and repeatable.

Key Gap Drivers: some external publishers bundle physical security hardware, project growth without incorporating Bill C-26 compliance costs, or assume uniform price erosion across all solution tiers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.37 B (2025) | Mordor Intelligence | |

| USD 14.05 B (2024) | Regional Consultancy A | Includes hardware firewalls and cameras; pre-Bill C-26 assumption |

| USD 8.00 B (2024) | Global Consultancy B | Excludes managed security services; mixed currency reporting |

| USD 13.80 B (2024) | Industry Forecasting Firm C | Extends CAGR to 2035 without recent field validation |

Mordor Intelligence therefore delivers a balanced, evidence-backed figure that decision-makers can trace to named drivers and repeatable steps, ensuring dependable planning.

Key Questions Answered in the Report

What is the projected value of the Canada cybersecurity market by 2031?

The market is forecast to reach USD 18.26 billion by 2031, growing at a 13.56% CAGR.

Which deployment model is expanding the fastest in Canada?

Cloud-based security leads growth, projected to rise at a 15.32% CAGR through 2031.

Why is healthcare spending on cybersecurity accelerating?

Bill C-72’s interoperability rules and recent ransomware attacks are driving a 14.66% CAGR in healthcare security budgets.

How are small and medium enterprises addressing talent shortages?

SMEs are increasingly adopting managed detection and response subscriptions that bundle technology and analyst expertise into predictable monthly fees.

Which provinces have introduced notable cybersecurity legislation recently?

Ontario enacted Bill 194, Quebec passed Bill 82, Alberta updated its Cybersecurity Strategy, and British Columbia expanded the CyberBC program.

Page last updated on: