E-Bike Battery Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

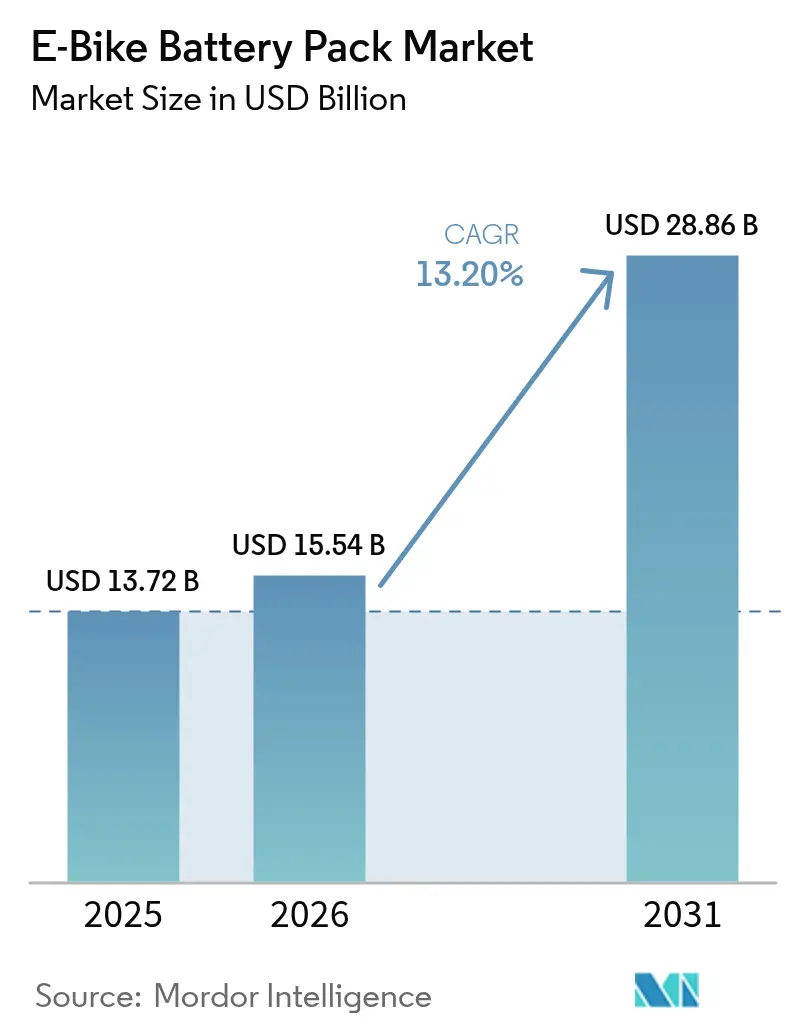

| Market Size (2026) | USD 15.54 Billion |

| Market Size (2031) | USD 28.86 Billion |

| Growth Rate (2026 - 2031) | 13.20% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-Bike Battery Pack Market Analysis by Mordor Intelligence

The e-bike battery pack market size in 2026 is estimated at USD 15.54 billion, growing from 2025 value of USD 13.72 billion with 2031 projections showing USD 28.86 billion, growing at 13.2% CAGR over 2026-2031. Rising urban population density, falling lithium-ion cell costs, and supportive purchase incentives in more than 40 countries together widen the addressable customer base. Sodium-ion pilot lines scheduled for large-scale output from 2025 onward add a low-cost chemistry pathway that could broaden access in price-sensitive regions. Commercial fleet electrification further accelerates demand by favoring high-cycle-life packs over pure energy density gains. At the same time, supply-chain domination by China introduces geopolitical risk, and tightening urban fire-safety rules impose new certification hurdles.

Key Report Takeaways

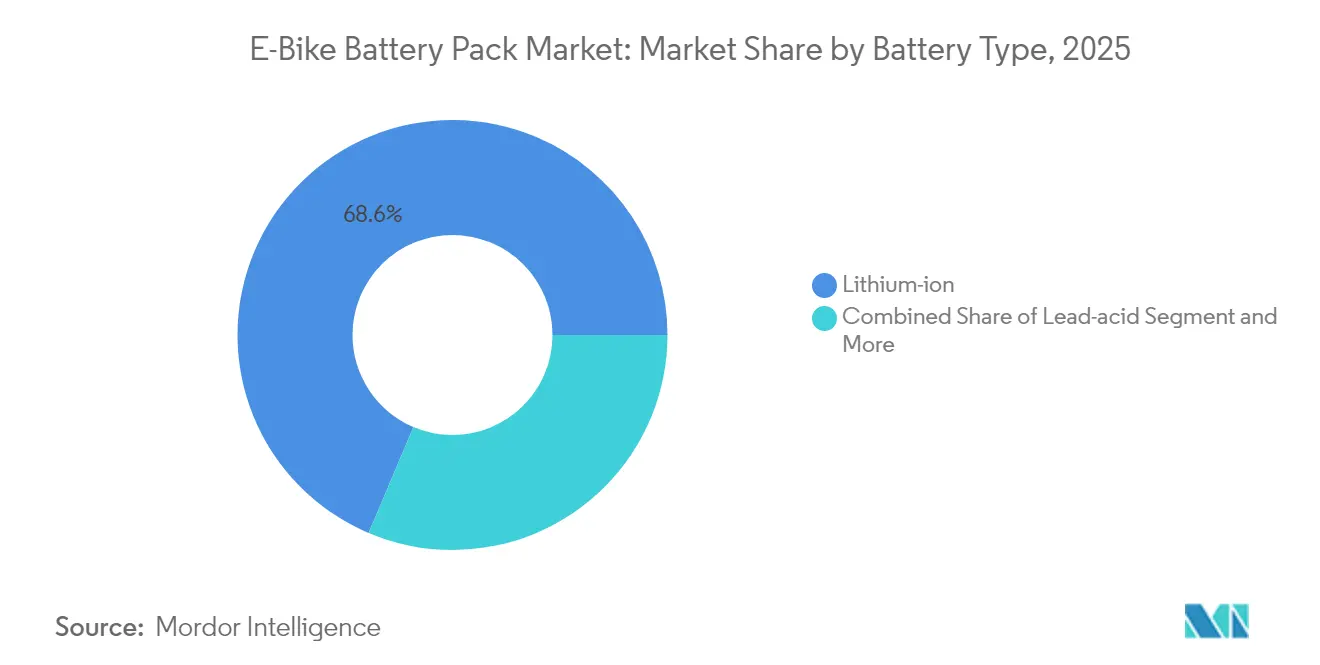

- By battery type, lithium-ion commanded 68.62% of e-bike battery market share in 2025, and is projected to register the fastest 14.87% CAGR through 2031.

- By battery pack position, down-tube solutions led with 70.45% revenue share in 2025; rear-carrier packs are forecast to grow at a 14.05% CAGR to 2031.

- By voltage class, less than/equal to 36 V systems accounted for 52.64% of the e-bike battery market size in 2025, whereas above 48 V systems are advancing at 15.12% CAGR through 2031.

- By end-use application, urban commuter bikes held 61.73% share of the e-bike battery market size in 2025 and cargo/delivery bikes are progressing at a 15.74% CAGR through 2031.

- By distribution channel, OEM-integrated batteries represented 72.58% revenue share in 2025; aftermarket replacements record the highest 14.42% CAGR to 2031.

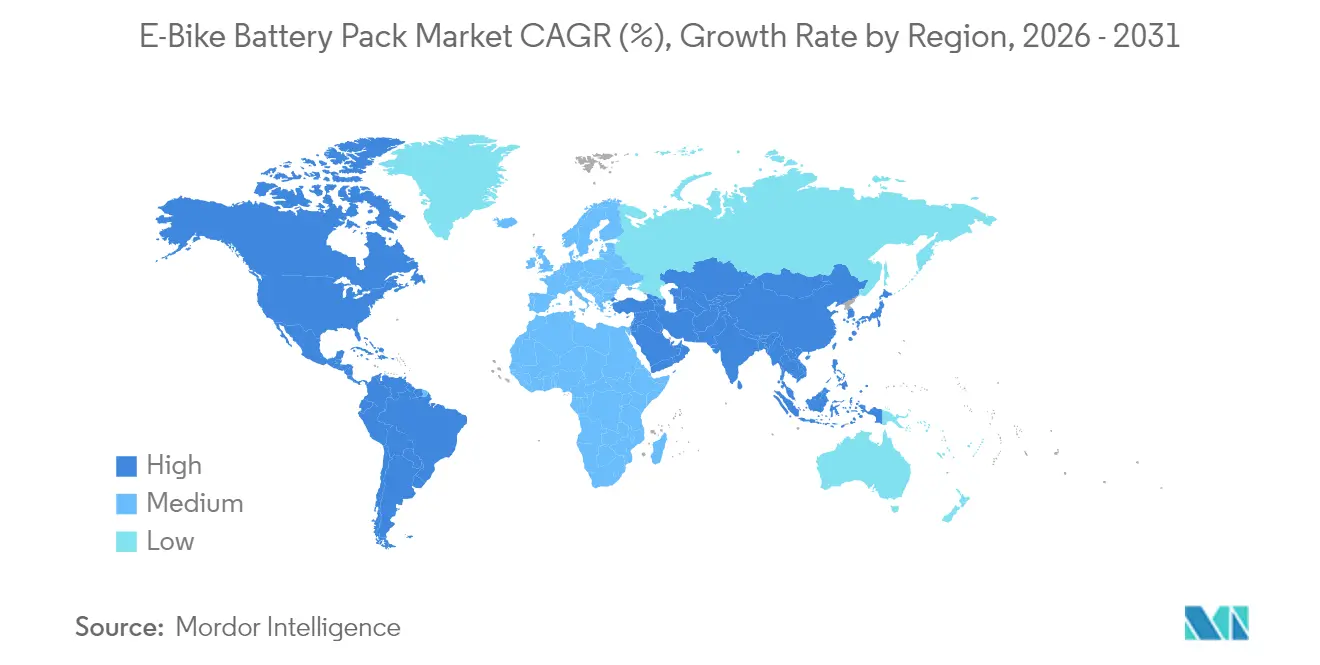

- By geography, Asia-Pacific retained 56.60% of the e-bike battery market share in 2025, while South America exhibits the strongest 16.55% regional CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-Bike Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Down Trend in Li-ion | +2.2% | Global, strongest in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Urban Delivery Fuels High-Cycle Packs | +1.8% | North America and EU core; growing in Asia-Pacific | Medium term (2-4 years) |

| Government Purchase Incentives | +1.5% | Europe and North America lead; emerging South America | Medium term (2-4 years) |

| Battery as a Service Models | +1.3% | Asia-Pacific core; pilots in Europe and North America | Long term (≥ 4 years) |

| Fast-Charge Cylindrical Formats | +0.9% | Global; early premium adoption | Short term (≤ 2 years) |

| Sodium-Ion Low-Cost Entry Bikes | +0.7% | China-centric; expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Down Trend in Li-ion Cells

Lithium-ion pack prices fell 20% in 2024, reaching USD 115 per kWh at the pack level, while cell costs also slid. These declines stem from gigafactory scale economies, optimized NMC and LFP cathode chemistries, and streamlined logistics between cathode producers and pack assemblers. Lower pack prices let brands offer extended-range models without raising retail tags, drawing cost-sensitive buyers into the e-bike battery market. Vertical integration strategies from cell to module adopted by major Asian suppliers stabilize margins despite raw-material volatility. Western manufacturers instead differentiate via UL 2849 certifications and longer warranties, reflecting diverging competitive postures. Raw-material spikes or fresh tariffs could slow the deflationary curve, yet the structural cost advantage of larger plants remains intact.

Urban-Last-Mile Delivery Boom Fuels High-Cycle Packs

Commercial operators now demand packs that withstand more than 1,000 cycles each year, far exceeding the 50-100 cycles typical for leisure riders. UPS has deployed over 10,000 low-emission vehicles, including e-bikes worldwide, to cut downtown delivery emissions, pushing suppliers toward LFP chemistry valued for its cycle life [1]“UPS expands global e-bike fleet,” UPS, ups.com. Food-delivery apps subsidize e-bike purchases for couriers, generating aggregated volumes that justify fit-for-purpose battery lines. High-cycle duty elevates the role of battery-management software capable of optimally throttling charge rates and monitoring cell temperatures. The e-bike battery market thus segments into consumer-range packs and commercial-grade solutions, each carrying distinct value propositions. Advanced telemetry further lowers lifetime cost per kilometer for fleet managers by predicting swap or service windows.

Government Purchase Incentives in More Than 40 Countries

France’s EUR 4,000 (~USD 4,696) grant for cargo e-bikes and Germany’s company-bike leasing tax benefits, combine to trim effective purchase prices [2]“Cargo-bike purchase subsidy,” French Ministry for Ecological Transition, gouv.fr. Forty-plus national programs share a policy logic that views e-bikes as congestion-relief tools, not discretionary gadgets. Many schemes earmark larger battery capacities for cargo or adaptive bikes, indirectly lifting watt-hour demand even when unit sales plateau. Funding continuity depends on annual budgets, so suppliers diversify go-to-market plans rather than anchor forecasts to subsidies alone. Early adopters in South America emulate European models, signaling policy diffusion that could unlock fresh volume corridors across Bogotá, São Paulo, and Santiago.

Battery-as-a-Service (BaaS) Models for Shared Fleets

Hero MotoCorp’s VIDA program decouples vehicle and battery ownership, charging riders a subscription that includes guaranteed swaps and technology upgrades. The model lowers upfront expense, improves residual values, and builds annuity revenue for providers. Integrating grid-interactive platforms such as Nuvve’s helps operators earn ancillary income by exporting power during peak demand, potentially offsetting subscription fees. BaaS demands dense swap infrastructure and accurate state-of-health analytics to meet consumer convenience benchmarks. Successful pilots in Asia broaden investor appetite for similar offerings in Europe’s shared mobility fleets. Over time, BaaS could lift the e-bike battery market by shortening replacement cycles, thereby raising cumulative cell demand.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small-Pack Premium vs EV | -1.8% | Global; highest in cost-sensitive regions | Medium term (2-4 years) |

| Fire-Safety and Insurance Restrictions | -1.2% | North America & EU urban centers; rising APAC | Short term (≤ 2 years) |

| China-Centric Cell Supply Risk | -0.9% | Global chains; largest impact on West | Medium term (2-4 years) |

| Warranty Gap Limits Cost Parity | -0.7% | Global; acute in commercial fleets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Small-Pack USD/kWh Premium vs. EV (Above 40%)

E-bike packs cost more than 40% per kWh above auto-grade batteries because each design must fit unique frame geometries and meet small-scale certification hurdles. Fixed costs for BMS hardware, enclosure tooling, and UN 38.3 transport testing weigh heavier when spread across modest watt-hour volumes. Suppliers respond with modular platforms that share cells and electronics across multiple models, yet the dilution effect remains limited. While the premium strains entry-level affordability, premium commuters absorb it in favor of lighter weight. Convergence with automotive cylindrical formats could narrow the gap, but only if e-bike frame makers align mounting standards and achieve higher lot sizes.

Fire-Safety and Insurance Restrictions in Dense Cities

A rise in lithium-ion incidents led New York City to require UL 2849 certification for any e-bike sold after September 2023 and prompted Transport for London to ban uncertified devices from the underground network [3]“Lithium-ion battery incident statistical report,” New York City Fire Department, nyc.gov. Property insurers follow suit, imposing storage surcharges that lift total ownership costs. Pack builders now integrate thermal-runaway barriers, shutdown separators, and cell-level fusing, which incrementally raise bill-of-materials expense. Smaller brands lacking in-house testing capabilities risk market exit, accelerating consolidation. Nonetheless, stringent rules also elevate consumer trust and could unlock pent-up demand once certification coverage becomes universal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Cost Leadership Meets Chemistry Diversification

Lithium-ion technology held 68.62% of e-bike battery market share in 2025. The segment is projected to grow at a 14.87% CAGR, supported by falling NMC and LFP costs that reinforce the overall e-bike battery market. Entry-level manufacturers keep lead-acid alive for its ultra-low sticker price, yet weight and cycle-life penalties confine its role to niche rural geographies. Sodium-ion’s 2025 commercial release illustrates how lower-density chemistries can unlock fresh consumer layers without government subsidies. Over the forecast period, lithium-ion will remain the anchor of the e-bike battery industry, but cost-driven segments shift toward sodium-ion once pack volumes cross economic break-even thresholds.

Competitive dynamics differ by chemistry. CATL’s TECTRANS lifetime-extension coating promises durability for LFP packs, a decisive advantage in high-cycle fleets. On the other hand, Yadea leverages sodium-ion’s cold-weather resilience to broaden sales in northern China, Russia, and Scandinavia. Premium brands chase NMC811 cathodes for extended range, but commercial fleets increasingly adopt LFP to minimize replacement downtime. The coexistence of multiple chemistries supports a layered supply ecosystem, mitigating single-technology dependence risk within the e-bike battery market.

By Battery Pack Position Type: Accessibility Versus Integration

Down-tube packs commanded 70.45% of 2025 revenue, favored for balanced weight distribution and sleek aesthetics that mirror conventional bike silhouettes. Rear-carrier modules are set to expand 14.05% annually as cargo and family bikes require higher capacities that cannot fit within slender down tubes. Manufacturers of commercial delivery bikes choose rack-top positioning to enable quick swaps without dismantling frame covers, a feature that directly lowers courier downtime. Integrated in-frame cavities attract premium urban commuters who value theft resistance and weather sealing, even if servicing becomes more labor-intensive.

Regulatory changes that mandate battery removability for apartment storage complicate full integration strategies. Bosch’s digital Battery Lock seeks to square the circle by allowing user-controlled unlock via a phone app when removal is required for indoor charging. Platform designers now offer modular rails that accept both down-tube and rear-carrier packs, granting OEMs flexibility to serve multiple customer personas while ordering common cells. The debate will ultimately center on maintenance convenience versus visual appeal, keeping both approaches relevant inside the e-bike battery market.

By Voltage Class: Performance Scaling Within Regulatory Limits

Systems rated less than/equal to 36 V held 52.64% of 2025 sales because many jurisdictions cap assisted-speed classes at this voltage, allowing riders to avoid motorcycle licensing rules. Yet configurations above 48 V will post the fastest 15.12% CAGR as performance-oriented consumers demand stronger hill-climb torque and cargo operators seek greater payload capability. Intermediate 37-48 V systems split the difference, especially in regions where 45 km/h speed-pedelec categories sit in regulatory gray zones. Samsung SDI’s forthcoming 46-series cylindrical cells increase volumetric energy, enabling builders to hit 55 Nm torque targets without enlarging pack footprints.

Voltage unfamiliarity among bike shops and emergency responders remains a barrier, prompting OEMs to integrate clearer labeling and automatic discharge circuitry for maintenance safety. Over the forecast window, harmonization of UL and EN standards is expected to streamline compliance across voltage tiers, smoothing cross-border sales for global brands. As a result, a tiered structure will persist, but upward migration in performance segments will lift average pack watt-hours, amplifying the overall e-bike battery market size.

By End-Use Application: Commercial Demand Redefines Specifications

Urban commuters absorbed 61.73% of market revenue in 2025, reflecting household adoption for work journeys under 10 km. Logistics firms, however, turn cargo and delivery bikes into the prime growth engine at 15.74% CAGR, driving innovation beyond pure range metrics. UPS’s 10,000 fleet confirms that pack durability and rapid-charge capability trump ultra-high density in daily operations. Food-delivery platforms follow suit by co-financing bikes that guarantee 1,200 charge cycles, catalyzing demand for LFP and forthcoming sodium-ion chemistries less sensitive to deep discharges.

Mountain and trekking bikes retain a loyal enthusiast base, but they contribute smaller absolute volumes owing to higher entry costs and a preference for seasonal usage. Folding bikes gain momentum in megacities where apartment storage restrictions limit full-size frames. This widening array of use cases forces cell suppliers to broaden product catalogs, ensuring that the e-bike battery industry meets differentiated cycle-life, power, and weight targets without straining manufacturing economics.

By Distribution Channel: OEM Control Meets Aftermarket Flexibility

OEM-fitted batteries made up 72.58% of 2025 shipments as brands pursued end-to-end quality assurance and integrated service offerings. Aftermarket replacements are growing 14.42% annually, fueled by capacity upgrades once original packs degrade and by DIY retrofits of legacy pedal bicycles. Standardized rail systems such as EnergyBus facilitate safe cross-brand compatibility, but leading OEMs restrict BMS firmware to prevent unauthorized packs from pairing with their controllers. Independent pack assemblers counter by offering price advantages and higher watt-hours, appealing to budget-minded consumers even at the expense of warranty loss.

The channel competition sharpens as right-to-repair legislation in the EU and certain U.S. states gives consumers more freedom to source batteries outside brand networks. Yet insurers and fleet managers often specify UL-certified OEM packs to reduce liability exposure, preserving the OEM channel’s dominance in commercial segments. Hybrid approaches emerge where manufacturers sell upgrade kits through authorized dealers, blending control with customer choice while sustaining recurring revenue within the e-bike battery market.

Geography Analysis

Asia-Pacific held 56.60% of global 2025 revenue, with China exporting electric motorcycles and e-bikes exceeded 40 billion yuan (USD 5.5 billion) that year. Korea and Japan contribute advanced cell R&D that trickles into premium European brands, while India’s e-two-wheeler unit sales in FY 2025 underscore latent demand in value-driven segments. Despite its dominance, the region’s dependency on domestic lithium processing invites tariff risk, pushing some suppliers to establish satellite assembly in Vietnam and Hungary for tariff-neutral shipping into the West.

South America will clock a 16.55% CAGR through 2031. Bogotá’s CicloRUTA expansion, São Paulo’s low-interest e-bike loans, and Brazilian tax rebates create fertile ground for both commuter and cargo models. Supply-chain gaps—chiefly in certified service centers and battery recycling—could temper adoption, prompting governments to court foreign direct investment in localized pack assembly. Regional growth accelerates once sodium-ion packs cut initial vehicle prices and mitigate range loss under tropical temperatures.

Europe and North America represent relatively mature arenas yet still promise mid-single-digit growth as policy measures intensify. France’s cargo-bike grants and Germany’s company-bike leasing encourage larger battery formats, prolonging replacement cycles yet raising aggregate watt-hour demand. The EU Battery Regulation will mandate digital passports by 2027, adding administrative overhead that larger suppliers can absorb more easily. In the United States, a federal tax credit plus California’s voucher stack together to drive suburban uptake beyond core urban centers. Fire-safety rules tightening in New York and San Francisco may momentarily slow momentum, but improved certification compliance is expected to restore growth by 2026.

Competitive Landscape

Competition is moderately fragmented. Samsung SDI has accelerated production of 46-series fast-charge cylindrical cells specifically for micro-mobility, leveraging automotive scale for cost leadership. CATL’s commercial sodium-ion roll-out targets value bikes and utility fleets, diversifying away from lithium dependence and buffering against LFP price swings. Bosch eBike Systems integrates 21700 cells into its PowerTube line, coupling hardware with sophisticated software that enhances dealer-level diagnostics.

Strategic moves extend beyond chemistry. Yamaha acquired Brose’s e-bike drive unit in 2025 to bundle motors, controllers, and batteries under one roof, signaling vertical integration as a route to margin defense. Panasonic and LG Energy Solution explore cell-leasing partnerships with European shared-bike operators, aspiring to steady second-life value streams. Start-ups such as Anod pivot to hybrid super-capacitors that promise ultra-fast charging, albeit with energy-density trade-offs. Incumbents answer by investing in solid-state R&D, hedging against a long-term leap in performance standards.

Midsize players in Europe and North America carve out niches in UL 2849-certified premium packs where customers pay for enhanced safety and longer warranty coverage. However, escalating certification costs and warranty liabilities pressure thin operating margins, raising the prospect of consolidation. Overall, brands capable of married hardware-software portfolios and diversified chemistry pipelines are best positioned to navigate evolving regional rules and user requirements within the e-bike battery industry.

E-Bike Battery Pack Industry Leaders

Samsung SDI Co., Ltd.

Panasonic Industry

Shimano Inc.

BMZ GmbH

LG Energy Solution, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: French start-up Anod unveiled an e-bike that runs on hybrid super-capacitors instead of lithium-ion cells, promising faster charging and longer cycle life.

- December 2024: The United Kingdom issued statutory guidance obligating businesses that manufacture or distribute lithium-ion e-bike batteries to integrate enhanced safety mechanisms addressing fire-hazard risks.

Global E-Bike Battery Pack Market Report Scope

An E-bike battery pack is a rechargeable battery pack used to power e-bikes. Batteries vary according to the voltage, total charge capacity (amp hours), weight, the number of charging cycles before performance degrades, and ability to handle over-voltage charging conditions.

The E-Bike Battery Pack Market is Segmented by Battery Type (Lithium-ion Battery, Lead Acid Battery, and Other Battery Types), Battery Pack Position Type (Rear Carrier, Down Tube, and In-tube Battery Pack), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers market size and forecast in value (USD million) for all the above segments. The report also offers the market dynamics, latest trends, size, share, and industry overview.

| Lithium-ion | NMC |

| LFP | |

| Lead-acid | |

| Other Chemistries (Ni-MH, Na-ion) |

| Rear Carrier |

| Down Tube |

| In-Frame / Integrated |

| Less than/equals 36 V |

| 37-48 V |

| Above 48 V |

| Urban Commuter |

| Cargo / Delivery |

| Mountain / Trekking |

| Folding / Micro-mobility |

| OEM-fitted |

| Aftermarket Replacement |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Type | Lithium-ion | NMC |

| LFP | ||

| Lead-acid | ||

| Other Chemistries (Ni-MH, Na-ion) | ||

| By Battery Pack Position Type | Rear Carrier | |

| Down Tube | ||

| In-Frame / Integrated | ||

| By Voltage Class | Less than/equals 36 V | |

| 37-48 V | ||

| Above 48 V | ||

| By End-use Application | Urban Commuter | |

| Cargo / Delivery | ||

| Mountain / Trekking | ||

| Folding / Micro-mobility | ||

| By Distribution Channel | OEM-fitted | |

| Aftermarket Replacement | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the global e-bike battery market in 2031?

The e-bike battery market is projected to reach USD 28.86 billion by 2031, registering a 13.2% CAGR from 2026.

Which chemistry holds the largest share in e-bike batteries today?

Lithium-ion commands 68.62% of 2025 sales due to its superior energy density and mature supply chain.

Why are cargo e-bikes driving battery innovation?

Cargo and delivery bikes need packs that withstand more than 1,000 annual cycles and accept fast charging, pushing suppliers toward long-life chemistries such as LFP.

Which region is the fastest-growing market for e-bike batteries?

South America leads in growth with a 16.55% CAGR through 2031, supported by urban congestion policies and emerging incentive schemes.

Page last updated on: