New Zealand Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

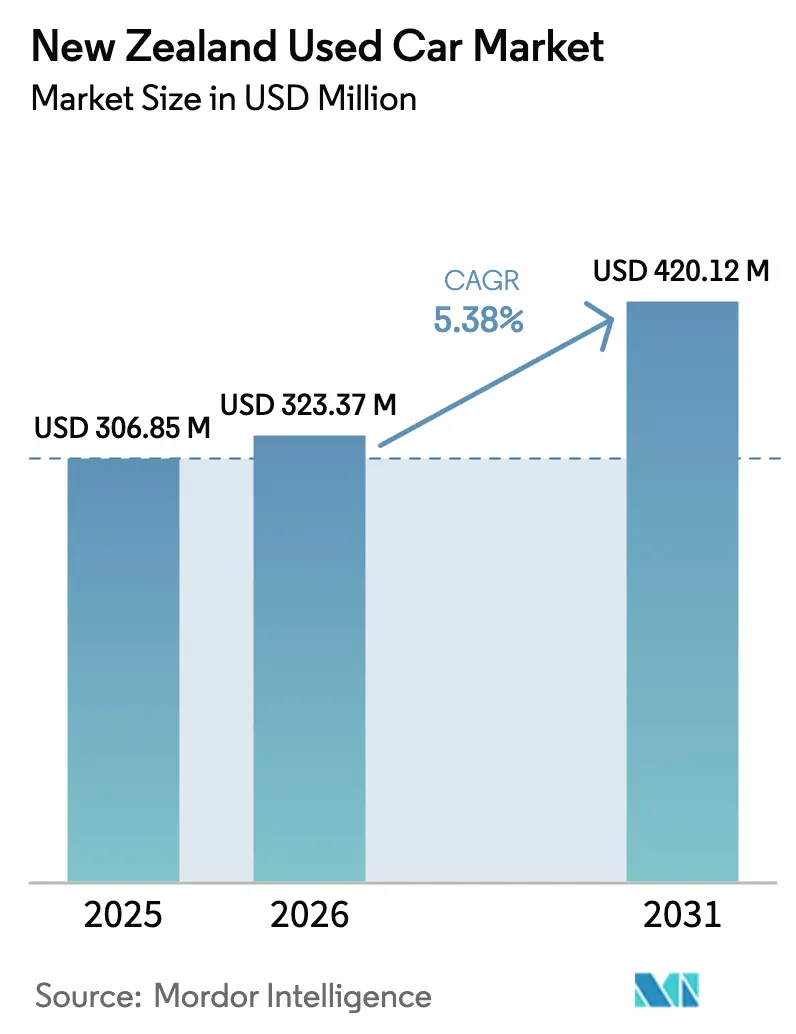

| Base Year Market Size (2025) | USD 306.85 Million |

| Market Size (2026) | USD 323.37 Million |

| Market Size (2031) | USD 420.12 Million |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

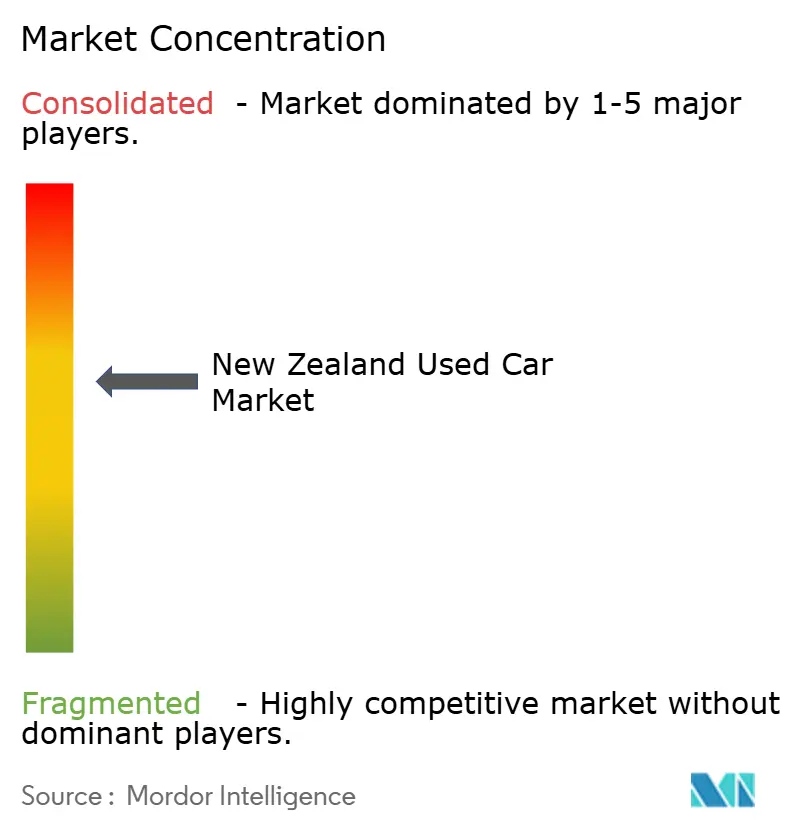

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand Used Car Market Analysis by Mordor Intelligence

The New Zealand used car market size is expected to grow from USD 306.85 million in 2025 to USD 323.37 million in 2026 and is forecast to reach USD 420.12 million by 2031 at 5.38% CAGR over 2026-2031. Demand remains resilient despite the 2023 end of the Clean Car Discount and the 2024 road-user charge for battery-electric vehicles, as buyers adapt to evolving policy settings [1] “Clean Car Standard Guidance, ”New Zealand Transport Agency, nzta.govt.nz. Growth is fueled by a decisive shift from yard-only shopping to digital-first journeys. Consumer appetite for versatile sport-utility vehicles stays strong, while a steady influx of competitively priced Japanese hybrid and electric imports, supported by a weak yen, broadens low-emission choices. These conditions create opportunities for dealers that blend omnichannel retailing, emissions-compliant inventory, and transparent vehicle histories to serve an expanding, tech-savvy customer base.

Key Report Takeaways

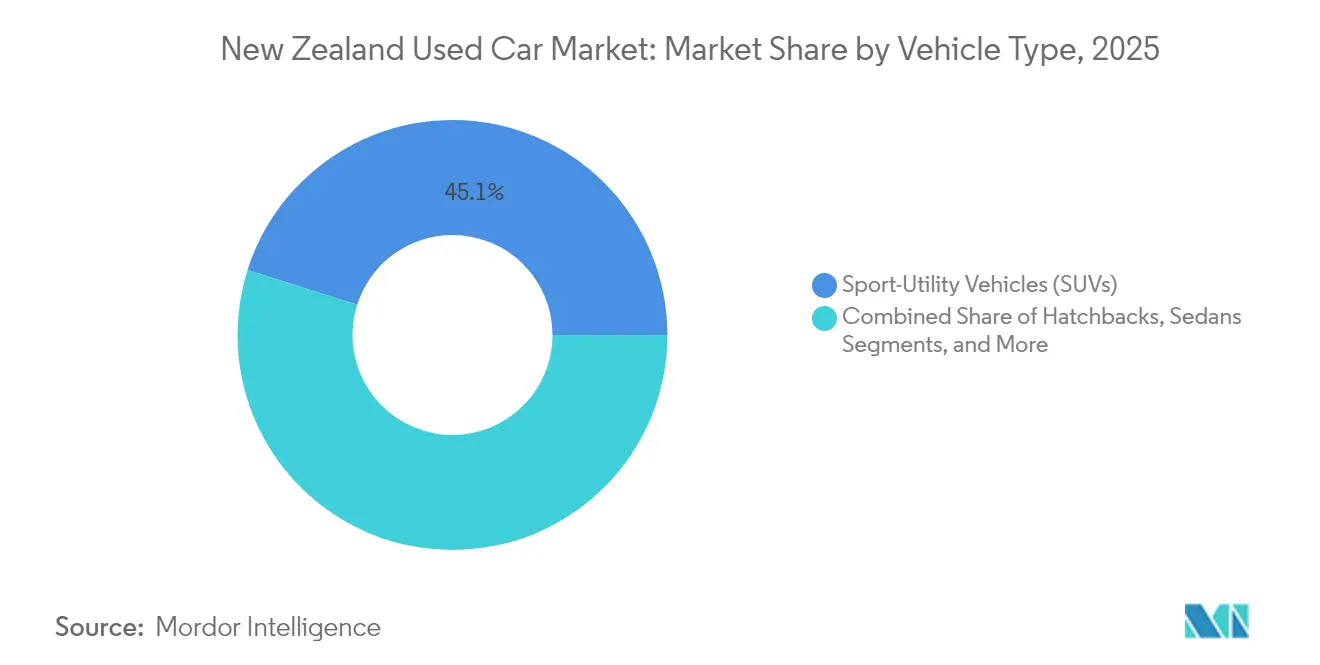

- By vehicle type, sport-utility vehicles held 45.12% of the New Zealand used car market share in 2025, and the segment is expanding at 5.88% CAGR through 2031.

- By vendor type, unorganized dealers captured 57.63% revenue of the New Zealand used car market in 2025, while the organized segment is advancing at 6.42% CAGR to 2031.

- By fuel type, petrol engines commanded a 63.45% share of the New Zealand used car market in 2025, while hybrid and electric cars recorded the fastest 13.78% CAGR, though 2031.

- By vehicle age, 6-8 year units accounted for 38.72% share of the New Zealand used car market in 2025, whereas 0-2 year vehicles are projected to grow at 6.85% CAGR through 2031.

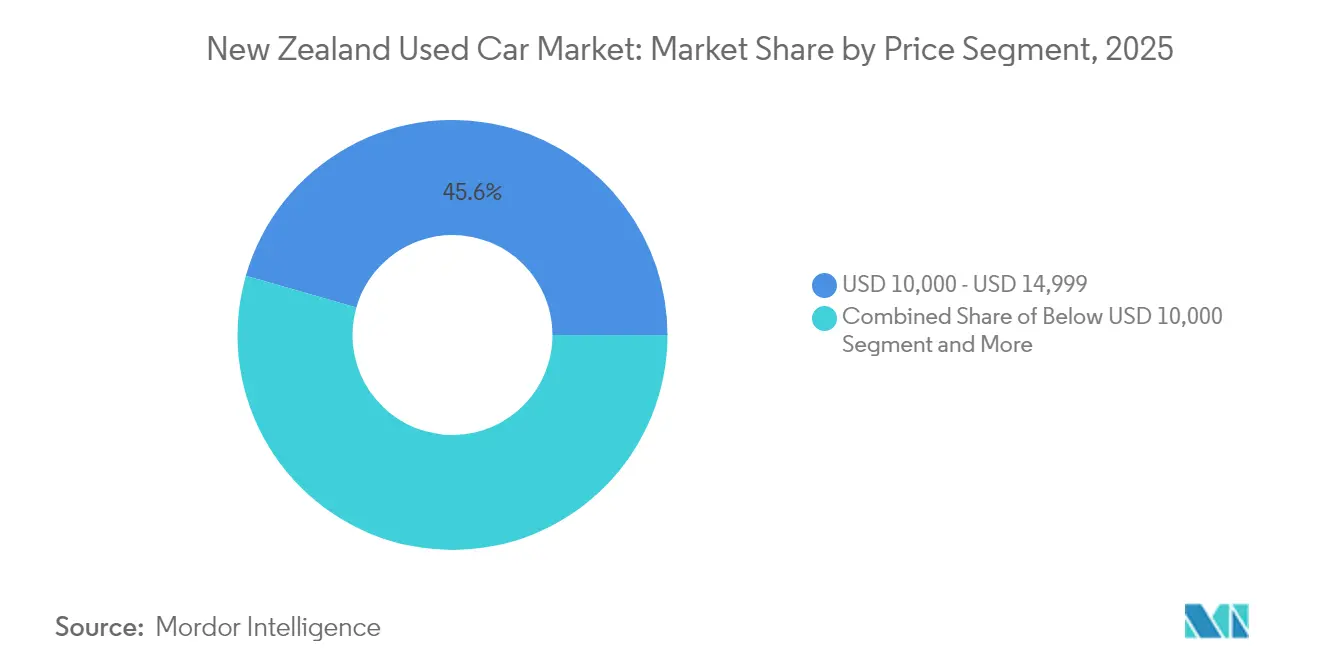

- By price segment, USD 10,000-14,999 cars led with 45.55% share of the New Zealand used car market in 2025, yet models priced above USD 30,000 are set to climb 6.12% CAGR through 2031.

- By sales channel, offline outlets retained 57.95% share of the New Zealand used car market in 2025, but online sales are increasing at 7.72% CAGR through 2031.

- By ownership, multi-owner listings represented 73.40% share of the New Zealand used car market in 2025, while first-owner cars are growing 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in New zealand includes both locally based firms and those operating across multiple regions. The market landscape in the global used car industry research shows how these players are arranged internationally.

New Zealand Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Clean Car Standard and rebate legacy effects | +1.2% | National | Medium term (2-4 years) |

| Surging supply of budget EV and hybrid ex-JDM imports | +0.9% | National, major ports | Medium term (2-4 years) |

| Accelerated online-to-offline retail integration | +0.8% | National, early gains in Auckland/Wellington/Christchurch | Short term (≤ 2 years) |

| Fleet-age reduction mandate proposed by NZTA | +0.7% | National, commercial fleets | Long term (≥ 4 years) |

| Rise of subscription car-as-a-service models | +0.6% | Urban centers, expanding regionally | Medium term (2-4 years) |

| Favorable FX (weak yen) boosting importer margins | +0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Clean Car Standard and Rebate Legacy Effects

Although the Clean Car Discount ended in 2023, importers still face NZD 22.50 per gram of CO₂ above fleet targets, so low-emission stock remains strategically valuable. Electric-vehicle registrations nearly doubled in early 2025 versus the prior year, confirming that underlying demand persists without direct rebates. The ongoing standard improves visibility for dealers until at least 2027, motivating higher import volumes of hybrids and electrics. Secondary-market buyers benefit from lower entry prices as first owners shoulder the steepest depreciation. Dealers who optimize emissions portfolios gain an edge when auctioning high-CO₂ inventory to overseas buyers, moderating compliance costs.

Surging Supply of Budget EV and Hybrid Ex-JDM Imports

Japan ships many used cars each month to New Zealand at an average landed cost of NZD 7,700 (USD 4,620), filling forecourts with value-priced hybrids and micro-EVs. Quality checks such as JEVIC inspections ensure units meet Euro 4 standards, sustaining buyer confidence even at lower price points. Import volumes center on the 3-5 year age bracket, directly contesting local trade-in pricing. Dealers with in-house compliance centers turn faster, while smaller yards absorb higher reconditioning times. The flow of electrified imports raises consumer exposure to EV ownership, accelerating repeat-purchase likelihood in the New Zealand used car market.

Accelerated Online-to-Offline Retail Integration

Consumers increasingly expect seamless digital journeys, prompting dealers to embed virtual showrooms, instant finance calculators, and remote paperwork into traditional processes. Around 18.72% of all big-ticket retail transactions already occur fully online, signaling cultural readiness for click-to-buy car purchases. The shift trims floorplan costs and widens national reach but requires investment in inventory-management systems and staff re-skilling. Smaller independents face margin pressure until platform fees normalize and scale economies emerge. As payment security and logistics partners mature, conversion rates on digital listings are expected to edge closer to traditional yards, giving the New Zealand used car market a durable omnichannel backbone.

Fleet-Age Reduction Mandate Proposed by NZTA

Policy debate now weighs fees on high-emission vehicles older than 12 years, a move aligned with the 2050 net-zero goal [2]“Net-Zero Roadmap,” Ministry of Transport, transport. govt.nz. Commercial fleets may be required to shorten replacement cycles, stimulating turnover toward younger, lower-maintenance stock. Parts distributors forecast 5-10% annual growth under a status-quo fleet, underscoring potential upside if forced retirement accelerates. Mandates would lift demand for late-model units yet risk stranding aged inventory that remains price-competitive for rural buyers. Stakeholders, therefore, lobby for phased rollouts with scrappage vouchers, cushioning transition pain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trust Gap in Odometer/Damage-History Data | -0.5% | National, higher-value deals | Long term (≥ 4 years) |

| Stricter Japanese Auction Sourcing Rules | -0.4% | National, import-dependent | Short term (≤ 2 years) |

| Volatile BEV Residual Values | -0.3% | Urban EV clusters | Medium term (2-4 years) |

| Insufficient Public Charging Outside Main Metros | -0.2% | Regional/Rural | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Trust Gap in Odometer/Damage-History Data

Claims disputes heard by the Motor Vehicle Disputes Tribunal underline lingering transparency issues around mileage rollbacks and past damage [3]“Motor Vehicle Disputes Tribunal Cases 2024,” consumerprotection.govt.govt.nz. Cost or effort deters some buyers from independent inspections, and requested price discounts compress dealer margins. Digital platforms now attach government-verified Consumer Information Notices to listings, yet authenticity doubts persist for imports lacking verified service records. Wider uptake of blockchain-based maintenance logs could narrow the gap, but critical mass remains distant. Until certainty improves, premium transactions will progress cautiously, tempering the New Zealand used car market’s velocity at the high end.

Stricter Japanese Auction Sourcing Rules

Japan’s domestic regulator is tightening export procedures to curb fraud and protect local buyers, which can cap New Zealand importer access to premium lanes or increase compliance expenses. Small importers lacking bundled shipping contracts face higher per-unit logistics charges, eroding landing-price advantages. Dealers may diversify to Singapore or UK auctions, but those channels carry different specs and right-hand-drive availability. In the short term, inventory scarcity on popular grades could lift domestic wholesale prices, transferring cost to consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUV Dominance Drives Market Evolution

Sport-utility vehicles captured 45.12% of the New Zealand used car market in 2025 and are projected to climb at a 5.88% CAGR through 2031. The segment enjoys strong resale values, supportive of trade-in flows that perpetuate inventory depth. Hatchbacks and sedans continue serving budget and fleet buyers but surrender share to higher-riding crossovers. Outdoor recreational culture, gravel roads, and unpredictable weather make all-wheel drive and elevated ground clearance practical advantages. The Clean Car Standard nudges OEMs toward hybrid and plug-in SUV variants, moderating future compliance penalties. Enthusiast body styles such as convertibles and coupes remain niche yet attract premium margins for specialty yards.

By Vendor Type: Organized Dealers Gain Ground

Unorganized sellers held 57.63% of the New Zealand used car market turnover in 2025, yet organized dealerships are expanding fastest at a 6.42% CAGR as buyers seek warranty cover and structured finance. First-tier dealers leverage certified reconditioning centers and nationwide logistics to shorten lead times and build brand trust. Unorganized sellers retain cost advantages yet struggle to match digital marketing spend and compliance sophistication. Expanding consumer-credit screening by banks favors licensed yards able to integrate instant approval engines. As transparency laws tighten, the New Zealand used car market is expected to keep reallocating volume toward the organized segment.

By Fuel Type: Electrification Accelerates Despite Policy Shifts

Petrol models held 63.45% share of the New Zealand used car market in 2025, but hybrids and electrics will post the fastest 13.78% CAGR as battery prices fall and consumer running-cost awareness rises. Many buyers experiment with hybrid technology first, comforted by ample Japanese import supply and familiar servicing. Road-user charges on EVs introduce a new cost line, yet total ownership calculations still favor BEVs for high-kilometer drivers under rising fuel prices. Diesel experiences gradual contraction as emissions scrutiny intensifies, and LPG/CNG remains minor owing to sparse refueling networks.

By Vehicle Age: Newer Vehicles Gain Preference

Units aged 6-8 years held a 38.72% share in 2025 within the New Zealand used car market, yet 0-2-year entries will rise at 6.85% CAGR as buyers prioritize up-to-date safety tech and connectivity. Lease returns from corporates provide a steady pipeline of such late-model cars. Older than 12 years stock faces looming policy risk and higher Warrant-of-Fitness-fail rates, nudging cost-aware consumers toward the younger 3–5-year bracket. Part suppliers still see healthy demand from legacy fleets, indicating a long tail of older-vehicle viability, particularly outside major cities.

By Price Segment: Premium Growth Amid Value Focus

Cars priced USD 10,000-14,999 controlled 45.55% of the New Zealand used car market in 2025, reflecting broad value hunting among mid-income households. However, units above USD 30,000 are forecast to grow at 6.12% CAGR, propelled by technology seekers and rising disposable incomes in dual-earner households. Sub-USD 10,000 choices face reliability concerns and limited finance support, while the USD 15,000-29,999 middle tiers act as gateways to advanced driver-assistance features. Dealers stocking premium near-new imports benefit from higher gross profit per unit, offsetting slower turn rates.

By Sales Channel: Digital Transformation Accelerates

Offline showrooms still processed 57.95% of the New Zealand used car market transactions in 2025, but online channels expanded at 7.72% CAGR as listing platforms add finance, inspection, and delivery plugins. Consumers increasingly pre-qualify for loans online, reducing time spent on-site. Physical yards adapt by offering click-and-collect services and virtual video tours. Auction houses maintain dealer-to-dealer relevance, though some pivot to livestreamed bidding to widen buyer circles. Omnichannel strategies emerge as baseline expectations rather than competitive differentiators.

By Ownership: First-Owner Vehicles Command Premium

First-owner listings grow at 7.18% CAGR against a dominant 73.40% share of the New Zealand used car market for multi-owner cars in 2025, signaling a willingness to pay a transparency premium. Verified service logs and extended warranties help close deals faster, especially on vehicles under five years old. Multi-owner stock keeps volume leadership by affordability, yet contends with the enduring odometer-history trust gap. Platforms investing in data analytics to validate ownership chronology can unlock latent value across this high-volume segment of the New Zealand used car market.

Geography Analysis

Auckland functions as the nation’s import hub, funneling Japanese arrivals through its ports and sustaining the country’s largest dealer network. Wellington’s steady government employment provides a resilient customer base that values late-model low-emission vehicles. Christchurch continues to refresh its fleet after earthquake-era write-offs, maintaining active demand.Secondary cities such as Hamilton, Tauranga, and Dunedin post above-average growth as population inflows and infrastructure upgrades lower distribution costs. Regional consumers often face inventory scarcity and longer test-drive logistics, creating pricing premiums. Electric-vehicle uptake maps closely to charging-point density; major urban corridors enjoy firm BEV demand, whereas regional areas lag pending the government’s 10,000-point 2030 infrastructure target. Meridian Energy’s highway installations are narrowing gaps, yet range anxiety still tempers rural BEV resale values.

Mordor Intelligence tracks the used car market across other major regions such as Africa, with additional country-level coverage spanning Sri Lanka, South Korea, South Africa, Myanmar, Switzerland, Belgium, Nigeria, and Kenya, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Turners Automotive Group leads with an integrated auction-retail-finance model that funds technology and nationwide branch expansion. Trade Me Motors dominates online eyeballs and deepens data-valuation capabilities following the full acquisition of AutoGrab in July 2024, sharpening pricing transparency for dealers.

Digital-only entrants offer subscription vehicles and doorstep delivery, unsettling traditional dealers who rely on foot traffic. Organized networks counter by bundling extended warranties, service contracts, and rapid finance approval to sweeten value propositions.

The unorganized segment stays relevant through low overheads and local relationships, yet concedes share as compliance regulations tighten. Overall, the New Zealand used car industry exhibits moderate concentration, leaving space for niche specialists such as rural-vehicle suppliers and classic-car restorers.

New Zealand Used Car Industry Leaders

AJ Motors Ltd

Turners Automotive Group

2Cheap Cars Group Limited

Trade Me Limited

Auto Trader Media Group Limited (Auto Trader)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Auto Trader, a leading online used car marketplace in New Zealand, has announced a notable resurgence. Supported by Japan's Optimus automotive group and the creative expertise of an Auckland-based agency, the company has expanded its facilities across New Zealand.

- January 2025: NZ Cheap Cars, a prominent player in the used car market, opened a national distribution center in Penrose, Auckland, to streamline nationwide stock rotation.

- December 2024: Only Cars launched an online listing platform catering to both used and new cars, which is designed with dealer feedback to reduce transaction pain points.

- July 2024: Trade Me acquired AutoGrab; through this acquisition, the company enhanced real-time used vehicle-pricing accuracy for the dealer community.

New Zealand Used Car Market Report Scope

A used car is a pre-owned vehicle that has previously had one or more retail owners. These cars are sold through a variety of outlets through independent dealers, online sales channels, and others.

New Zealand's used car market is segmented by vehicle type, vendor type, and fuel type. Based on the vehicle type, the market is segmented into hatchbacks, sedans, sports utility vehicles, and multi-purpose vehicles. Based on the vendor type, the market is segmented into organized and unorganized. Based on the fuel type, the market is segmented into gasoline, diesel, electric, and other fuel types.

For each segment, the market sizing and forecast have been done based on the value (USD).

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Others (Convertibles, Coupes, Crossovers, Sports Cars) |

| Organized |

| Unorganized |

| Petrol |

| Diesel |

| Hybrid and Electric |

| Others (LPG, CNG, etc.) |

| 0 - 2 Years |

| 3 - 5 Years |

| 6 - 8 Years |

| 9 - 12 Years |

| Above 12 Years |

| Below USD 10,000 |

| USD 10,000 - USD 14,999 |

| USD 15,000 - USD 19,999 |

| USD 20,000 - USD 29,999 |

| Greater than and Equals USD 30,000 |

| Online |

| Offline |

| First-owner Resale |

| Multi-owner |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| Sport-Utility Vehicles (SUVs) | |

| Multi-Purpose Vehicles (MPVs) | |

| Others (Convertibles, Coupes, Crossovers, Sports Cars) | |

| By Vendor Type | Organized |

| Unorganized | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid and Electric | |

| Others (LPG, CNG, etc.) | |

| By Vehicle Age | 0 - 2 Years |

| 3 - 5 Years | |

| 6 - 8 Years | |

| 9 - 12 Years | |

| Above 12 Years | |

| By Price Segment | Below USD 10,000 |

| USD 10,000 - USD 14,999 | |

| USD 15,000 - USD 19,999 | |

| USD 20,000 - USD 29,999 | |

| Greater than and Equals USD 30,000 | |

| By Sales Channel | Online |

| Offline | |

| By Ownership | First-owner Resale |

| Multi-owner |

Key Questions Answered in the Report

What is the current value of the New Zealand used car market?

The New Zealand used car market is valued at USD 323.37 million in 2026.

Which vehicle type leads the market?

Sport-utility vehicles lead with 45.12% share and are growing at a 5.88% CAGR through 2031.

How fast are hybrid and electric used-car sales growing?

Hybrid and electric models are the fastest-growing fuel category, advancing at a 13.78% CAGR to 2031.

Why are organized dealers gaining share?

Organized dealers offer warranties, financing, and digital services, enabling 6.42% CAGR growth while improving customer trust and convenience.

Page last updated on: