Neuromodulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.22 Billion |

| Market Size (2031) | USD 10.93 Billion |

| Growth Rate (2026 - 2031) | 8.65% CAGR |

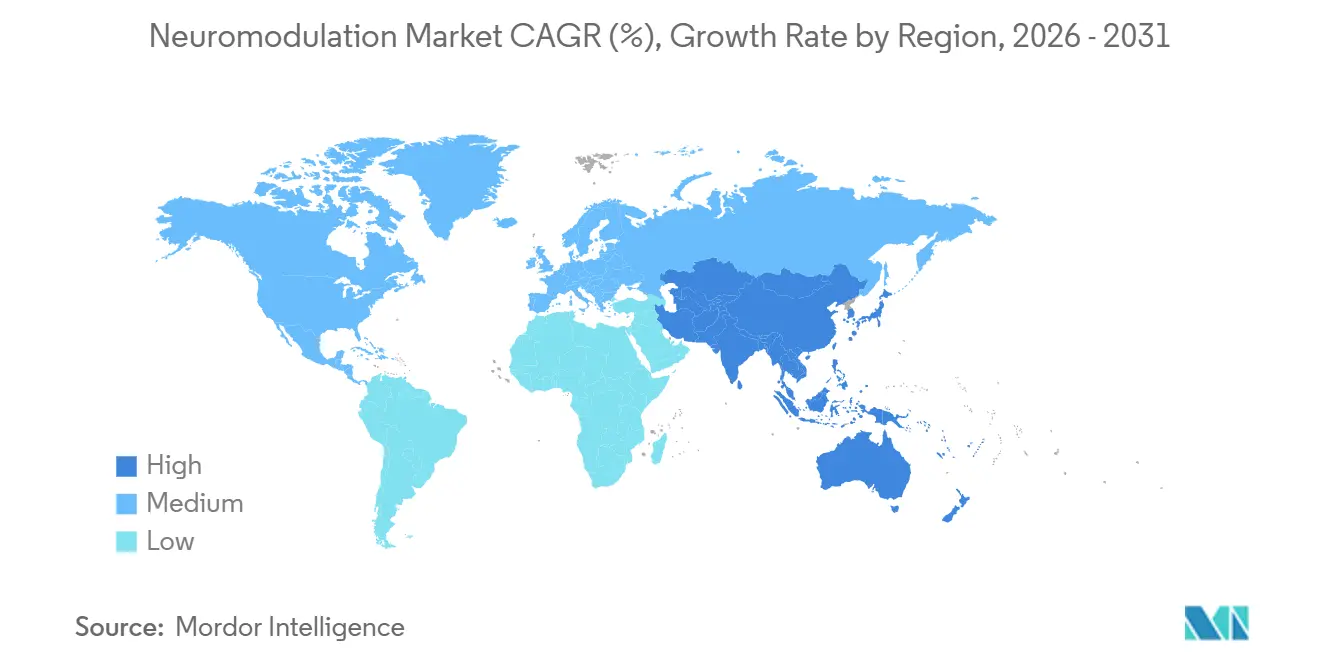

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neuromodulation Market Analysis by Mordor Intelligence

The Neuromodulation Market size is projected to expand from USD 6.67 billion in 2025 and USD 7.22 billion in 2026 to USD 10.93 billion by 2031, registering a CAGR of 8.65% between 2026 to 2031.

Three structural forces underpin this outlook: growing populations of drug-resistant patients with chronic pain and movement disorders, regulators expanding approved indications, and the rapid maturation of closed-loop stimulation algorithms. Mature reimbursement pathways for spinal cord and deep brain stimulation, particularly in the United States and Western Europe, maintain resilient capital equipment spending even when hospital budgets are tightened. Meanwhile, consumer-grade wearable stimulators are broadening the entry funnel by familiarizing patients with neuromodulation long before surgery is considered, creating a virtuous cycle of awareness, early adoption, and referral volume. Competitive dynamics are intensifying as incumbents bundle hardware, software, and data platforms to defend share against venture-backed disrupters targeting white-space indications and home-use devices. Finally, new cybersecurity mandates add compliance costs that favor scale manufacturers, who are able to amortize quality-system upgrades across large installed bases.

Key Report Takeaways

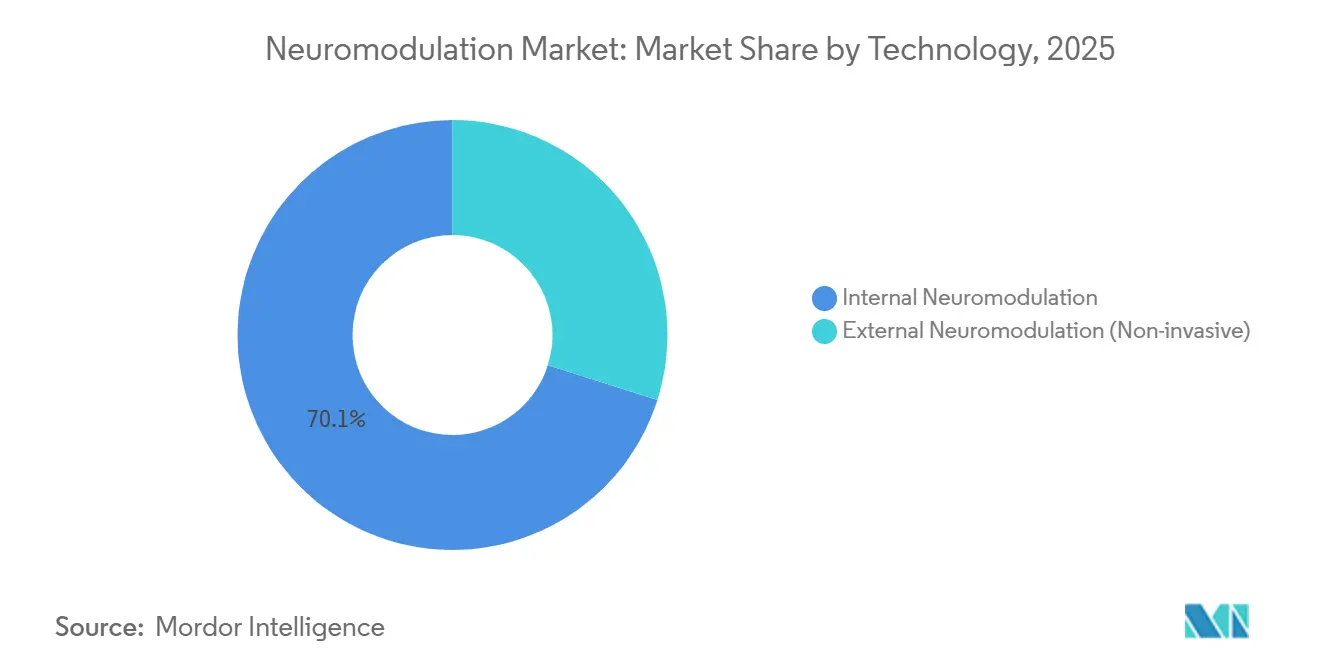

- By 2025, internal neuromodulation technologies captured a 70.12% revenue share; external, non-invasive systems are forecasted to advance at a 10.23% CAGR through 2031.

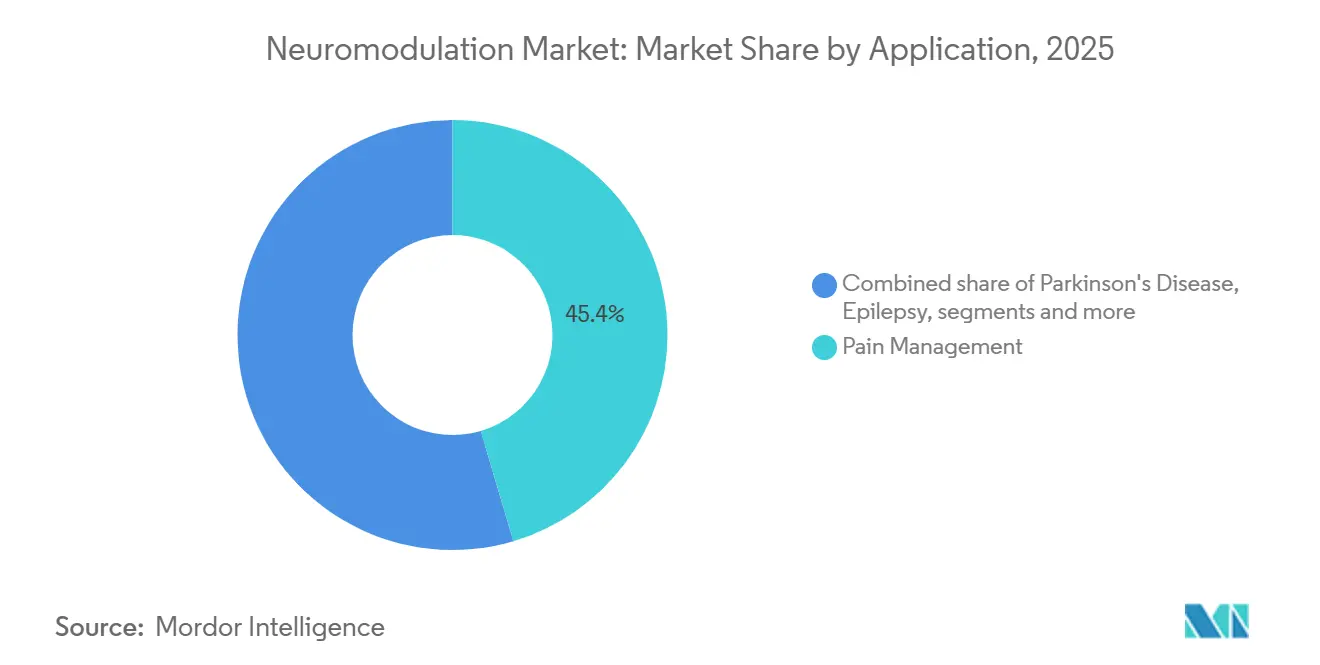

- By application, pain management retained 45.43% of 2025 revenues, while Parkinson’s disease applications are set to grow at a 10.56% CAGR to 2031.

- By end-user, hospitals and ambulatory surgical centers secured 60.32% of end-user turnover in 2025; clinics and physiotherapy centers are poised for 11.45% CAGR expansion.

- By geography, North America led with a 45.21% share in 2025, whereas the Asia-Pacific region is projected to exhibit the fastest growth of 9.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neuromodulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Burden Of Chronic Pain And Neurological Disorders | +2.1% | Global, with highest intensity in North America and Europe | Long term (≥ 4 years) |

| Continuous Advancements In Closed-Loop And High-Frequency Stimulation Technologies | +1.8% | North America and Europe lead adoption, APAC lags 2-3 years | Medium term (2-4 years) |

| Expansion Of Approved Clinical Indications And Reimbursement Coverage | +1.5% | United States, Europe, selective APAC markets | Medium term (2-4 years) |

| Increasing Investments, M&A Activity, And Strategic Partnerships Across Neurotechnology Ecosystem | +1.3% | Global, concentrated in North America venture capital and European strategic buyers | Short term (≤ 2 years) |

| Emergence Of AI-Powered Personalized Neuromodulation Algorithms | +1.2% | North America and Europe early adopters, APAC contingent on regulatory clarity | Medium term (2-4 years) |

| Growth Of Wearable, Non-Invasive Neuromodulation For Home-Based Care | +0.9% | Global, fastest uptake in North America consumer wellness and European physiotherapy channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Chronic Pain and Neurological Disorders

Chronic pain affects 1.5 billion people, and drug-resistant cases represent up to 30%, establishing a durable treatment pool. Disability-adjusted life years attributable to neuropathic pain and migraine climbed 12% between 2020 and 2024, partly from post-COVID neuropathies. Parkinson’s prevalence could double to 17 million by 2040 as populations age across Asia, where access to levodopa is uneven. Epilepsy remains refractory in 30% of 50 million global patients; 2024 FDA clearance of responsive neurostimulation for adolescents widened the U.S. eligible pool by roughly 200,000 candidates. Health-system moves toward bundled payments heighten interest in one-time device expenditures that offset recurring costs of drugs and emergency visits within five years.

Continuous Advancements in Closed-Loop and High-Frequency Stimulation Technologies

FDA clearance of Medtronic’s Percept RC in 2024 introduced adaptive deep brain stimulation, which titrates therapy against real-time beta-band biomarkers, reducing daily “off” time by 2.6 hours in Parkinson’s patients. Ten-kilohertz spinal cord stimulation, pioneered by Nevro and adopted by Abbott and Boston Scientific, avoids paresthesia and delivers 70% responder rates in failed-back-surgery syndrome trials. Neuros Medical’s high-frequency peripheral device received 2024 clearance for phantom-limb pain, signaling broader use in diabetic neuropathy. Such innovations shorten product life cycles and push manufacturers toward modular hardware capable of software upgrades over the air.

Expansion of Approved Clinical Indications and Reimbursement Coverage

U.S. Medicare issued a national determination for dorsal root ganglion stimulation in 2024, unlocking coverage for about 40,000 beneficiaries annually. Germany’s G-BA funded closed-loop DBS contingent on registry participation the same year. NeuroPace’s indication was lowered to age 12 in 2024, aligning with EMA guidance and enlarging pediatric access. Each regulatory green light builds a cumulative evidence base, quickening subsequent reviews and payer negotiations.

Increasing Investments, M&A Activity, and Strategic Partnerships

Venture funding for neurotechnology touched USD 1.8 billion in 2024, buoyed by Synchron’s USD 75 million Series C and Precision Neuroscience’s USD 93 million Series B. Abbott bought Neurovalens to fuse vestibular stimulation with its pain-portfolio channels. Boston Scientific’s acquisition of Farapulse demonstrates cross-vertical synergies that amortize R&D across cardiac and neuro portfolios. Medtronic partnered with Rune Labs to weave StrivePD data into Percept devices, cutting clinic visits by 40% in pilot programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Maintenance Costs Of Implantable Systems | -1.4% | Global, most acute in emerging APAC and U.S. self-pay segments | Long term (≥ 4 years) |

| Stringent And Divergent Global Regulatory Approval Requirements | -1.1% | EU (MDR transition), China (NMPA mandates), Japan | Medium term (2-4 years) |

| Cybersecurity And Data-Privacy Risks In Connected Neurostimulators | -0.6% | North America and Europe due to FDA and GDPR enforcement | Short term (≤ 2 years) |

| Limited Long-Term Clinical Evidence For Novel Indications | -0.8% | Global, particularly psychiatric and cognitive applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Implantable Systems

Implantable stimulators range from USD 20,000 to USD 50,000, outpacing total annual per-capita health spending in most countries. Non-rechargeable battery replacements add USD 8,000–12,000 every 3–5 years and carry 2–5% infection risk[1]. Medicare’s flat diagnosis-related payments since 2020 have squeezed hospital margins, while China reimburses only 70% of the DBS device cost, leaving sizable co-pays. Manufacturers are responding with lower-priced “value” systems; however, thinner margins may slow the development of next-generation features.

Stringent and Divergent Global Regulatory Approval Requirements

The EU Medical Device Regulation now requires clinical investigations for even predicate devices, extending approval cycles to approximately 36 months[2]. China’s NMPA calls for 100 local patients in pivotal neuromodulation trials, adding USD 5–10 million in costs and two-year delays. Japan’s PMDA requires local validation despite FDA and CE marks, dissuading mid-tier firms from simultaneous multi-region launches. New FDA cybersecurity rules add USD 2–5 million per product line, a burden smaller innovators struggle to absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Implantables Maintain Leadership as Non-Invasive Devices Accelerate

Internal platforms accounted for a 70.12% neuromodulation market share in 2025, supported by decades of evidence in spinal cord and deep brain applications. Medtronic’s sensing-enabled Percept RC shortens symptom “off” periods by up to 30% compared with open-loop predecessors. Abbott’s Eterna generator utilizes a 10-year rechargeable cell, alleviating patient concerns about frequent recharges. Dorsal root ganglion systems gained momentum after U.S. national coverage in 2024, broadening pain-care options for Medicare beneficiaries.

External, non-invasive modalities are projected to post a 10.23% CAGR through 2031, driven by home-use clearances and consumer adoption of wellness products. Neurovalens launched a USD 500 vestibular-nerve headset that delivers physician-grade therapy without the need for surgery. FDA cleared at-home transcranial magnetic stimulators in 2024, reducing the access hurdle posed by 36-session clinic regimens. Evidence remains mixed - Cochrane reviews show only modest pain reduction for transcutaneous electrical nerve stimulators - but bundling devices with telehealth coaching is improving adherence and outcomes[3].

By Application: Pain Dominates Revenue while Parkinson’s Drives Growth

Pain therapies accounted for 45.43% of the 2025 turnover and remain the economic anchor of the neuromodulation market. High-frequency waveforms now achieve 70% responder rates and reduce paresthesia, thereby enhancing patient satisfaction. New U.S. payer policies extend first-line coverage to spinal cord stimulation for complex regional pain, accelerating implant volumes.

Parkinson’s disease is set for a 10.56% CAGR through 2031, topping overall neuromodulation market growth. Adaptive DBS platforms such as Boston Scientific’s Vercise Genus and Medtronic’s Percept RC offer 20–30% superior motor control in recent trials. NeuroPace’s responsive cranial stimulator, now cleared for adolescents, expands epilepsy device reach, while LivaNova’s vagus therapy opens a measured but sizable opportunity in treatment-resistant depression.

By End-User: Hospitals Lead but Outpatient Sites Gain Momentum

Hospitals and ambulatory surgery centers captured 60.32% of 2025 neuromodulation market revenue, reflecting the surgical complexity of implant procedures. CMS added spinal cord stimulator implantation to its outpatient list in 2024, enabling same-day discharges that reduce facility costs by 30–40%. Device makers, in turn, released simplified anchoring systems that cut operating-room time and support high-throughput ambulatory centers.

Clinics and physiotherapy centers, however, are forecast to expand at an 11.45% CAGR as non-invasive devices migrate into community settings and European physiotherapists gain prescribing authority. Germany reimburses home-use vagus stimulators, adding 500,000 chronic-pain patients to the addressable pool. In the United States, direct-access prescribing rights for physical therapists have been implemented in 12 states, nudging device distribution away from durable-equipment suppliers and toward clinic-based channels.

Geography Analysis

North America contributed 45.21% of 2025 revenues, driven by established reimbursement pathways, a concentrated clinical-trial infrastructure, and FDA programs that accept single-arm data for breakthrough devices. CMS’s national determination for dorsal root ganglion stimulation immediately opened coverage to roughly 40,000 Medicare lives, while private insurers removed prior authorization hurdles for candidates with documented opioid use disorder. Canada has added NeuroPace to its roster of assistive devices, supporting expected double-digit implant growth through 2027.

Europe delivered roughly one-third of global sales, led by Germany, the United Kingdom, and France. Germany’s registry-linked funding model for closed-loop DBS sets a template for value-based adoption, even as EU MDR rules lengthen device approval cycles. In 2024, NICE guidance affirmed the cost-effectiveness of spinal cord stimulation within accepted thresholds, thereby cementing its place as a standard intervention for failed-back-surgery syndrome. Uptake in Southern and Eastern Europe remains limited by budget and staffing shortages.

The Asia-Pacific region is the fastest-growing, with a projected 9.90% CAGR to 2031. China cleared Medtronic’s closed-loop DBS in 2024, but 30% patient cost-sharing still restricts implants to wealthier urban areas. Japan approved Boston Scientific’s latest DBS platform, yet maintains price caps 20% below U.S. levels; such margins discourage premium launches. India saw fewer than 500 spinal cord stimulators placed in 2024 because private insurance penetration is still low.

The Middle East, Africa, and South America collectively accounted for less than 7% of 2025 sales, but exhibit isolated hotspots. The United Arab Emirates has added spinal cord stimulation to its list of essential benefits, and Brazil’s private insurers reimburse neuromodulation at rates comparable to those in Southern Europe, although public-sector access remains limited.

Competitive Landscape

Medtronic, Abbott, and Boston Scientific command roughly 65–70% of the neuromodulation market revenue, leveraging broad portfolios, data-rich platforms, and global service networks. Abbott’s take-over of Neurovalens attaches vestibular wellness devices to its chronic-pain channel, diversifying reach beyond surgically implanted generators. Medtronic’s partnership with Rune Labs embeds remote-monitoring software, creating clinician switching costs and greater algorithmic lock-in. Boston Scientific’s Farapulse acquisition underscores the convergence between cardiac and neural electroceuticals, offering manufacturing economies of scale.

Mid-tier firms focus on differentiated niches to stay competitive. Nevro’s 10 kHz high-frequency system achieves a 70% responder rate, allowing for premium pricing in U.S. commercial contracts. NeuroPace maintains a first-mover advantage in responsive cranial stimulation, with nine-year durability data showing a 75% median seizure reduction. LivaNova secured a CE-mark extension for depression therapy, opening a new psychiatric frontier.

Competitive pressure also comes from innovators of brain-computer interfaces. Synchron’s endovascular implant entered pivotal trials under FDA breakthrough designation and could present a less-invasive alternative to conventional DBS if efficacy proves comparable. Patent filings grew 25% year-over-year in 2024; incumbents emphasize proprietary algorithms and cybersecurity compliance as defensible moats.

Neuromodulation Industry Leaders

Medtronic PLC

Abbott

Boston Scientific Corporation

LivaNova PLC

Nevro Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Swedish neurotech startup Flow Neuroscience received FDA approval for its first brain stimulation device designed for home use to treat depression. This regulatory milestone allows patients to access treatment conveniently outside clinical settings. The innovation could have a significant impact on the mental health market, which is expected to reach USD 540 billion by 2030.

- October 2025: Boston Scientific Corporation entered into a definitive agreement to acquire Nalu Medical, Inc. Nalu Medical specializes in minimally invasive solutions for chronic pain, including its wireless, battery-free neurostimulation system. The acquisition aims to expand Boston Scientific's pain management portfolio with targeted peripheral nerve stimulation technology.

- February 2025: Nevro Corp. announced the acquisition of Globus Medical. The merger will create a global leader in medical technology with approximately USD 3 billion in annual sales. Both companies are dedicated to developing innovative solutions for patients with chronic pain worldwide.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the neuromodulation market as the worldwide sales revenue generated by implantable and external systems that deliver targeted electrical or chemical pulses to modulate neural activity for therapeutic benefit. These systems include spinal cord, deep brain, vagus, sacral, gastric, and transcranial stimulators, as well as peripheral external stimulators, accessories, and programmer units.

Scope Exclusion. The analysis omits radio-frequency ablation generators, general electro-therapy devices, and disposable pain patches, which do not provide programmable neuromodulatory output.

Segmentation Overview

- By Technology

- Internal Neuromodulation

- Spinal Cord Stimulation (SCS)

- Deep Brain Stimulation (DBS)

- Vagus Nerve Stimulation (VNS)

- Sacral Nerve Stimulation (SNS)

- Gastric Electrical Stimulation (GES)

- Other Internal Neuromodulation

- External Neuromodulation (Non-Invasive)

- Transcutaneous Electrical Nerve Stimulation (TENS)

- Transcranial Magnetic Stimulation (TMS)

- Other External Neuromodulations

- Internal Neuromodulation

- By Application

- Pain Management

- Parkinson's Disease

- Epilepsy

- Depression

- Dystonia

- Other Applications

- By End-User

- Hospitals & Ambulatory Surgical Centers

- Clinics & Physiotherapy Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple semi-structured interviews and survey pulses with neurosurgeons, pain specialists, reimbursement consultants, and procurement heads across North America, Europe, and Asia-Pacific sharpened adoption curves, average selling prices, and replacement timelines. These conversations let us test secondary assumptions, calibrate regional weightings, and refine scenario parameters before locking the model.

Desk Research

Mordor analysts started by mapping the market space with publicly available sources such as the US FDA 510(k) database, the European CE marking register, and reimbursement fee schedules from the US Centers for Medicare and Medicaid Services. Epidemiology updates from the World Health Organization, prevalence dashboards from the Global Burden of Disease study, and surgical-volume records held by the International Neuromodulation Society helped us set disease pools and procedure counts. Company 10-Ks, investor decks, and clinical-trial registries then supplied shipment signals and pipeline clues, which were cross-checked against news archives in Dow Jones Factiva and financial snapshots in D&B Hoovers. The list above is illustrative; many additional open datasets were reviewed to validate figures and narrative context.

Market-Sizing & Forecasting

A top-down demand pool was built by multiplying treated-patient cohorts derived from chronic pain incidence, Parkinson's and epilepsy prevalence, and surgical eligibility ratios by device penetration and replacement rates. Selective bottom-up roll-ups of major supplier revenues and sampled ASP × unit data served as a reasonableness check. Key variables include:

Annual spinal-cord stimulator implant counts,

Share of non-invasive TMS sessions per pain case,

Average selling price shifts as rechargeable IPGs grow,

National reimbursement coverage milestones,

Device longevity improvements influencing replacement cycles.

Multivariate regression, using GDP per capita and neurology workforce density as predictors, generated country-level growth coefficients that feed an ARIMA overlay for near-term shocks.

Data gaps in small markets were bridged by geographic proxies, then adjusted through expert feedback.

Data Validation & Update Cycle

Outputs pass three-layer reviews: analyst, senior analyst, and research manager to flag anomalies. Variance greater than two percentage points versus independent procedure tallies triggers re-contact with respondents. Models refresh annually; interim revisions occur after material regulatory approvals or product withdrawals.

Why Mordor's Neuromodulation Baseline Commands Confidence

Published values often differ because firms pick unique product baskets, currency years, and refresh rhythms.

Key gap drivers include divergent inclusion of disposable leads, differing ASP deflators, and whether external TENS is bundled with implantables. Mordor's disciplined scope alignment, annual model rebuild, and dual-stream validation keep our baseline balanced.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.64 B (2025) | Mordor Intelligence | |

| USD 6.81 B (2025) | Global Consultancy A | Counts radio-frequency ablation consoles and bundles service contracts |

| USD 6.37 B (2025) | Research Publisher B | Applies average USD-EUR 5-year FX rate instead of current-year spot |

| USD 9.07 B (2025) | Trade Journal C | Adds peripheral neuromodulation biomaterials and estimates ex-factory rather than end-user prices |

Taken together, the comparison shows that once inconsistent scopes and price bases are stripped away, Mordor's methodology delivers a transparent, repeatable view that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What was the neuromodulation market size in 2026 and how fast is it growing?

The neuromodulation market size reached USD 7.22 billion in 2026 and is forecast to expand at an 8.65% CAGR to 2031.

Which technology segment dominates current device revenues?

Implantable platforms, including spinal cord and deep brain stimulators, held 70.12% share in 2025 due to mature reimbursement and long clinical track records.

Which therapeutic area is projected to grow fastest through 2031?

Parkinson's disease applications are expected to clock a 10.56% CAGR, outperforming other indications because of adaptive deep brain stimulation gains.

Why are clinics and physiotherapy centers becoming important sales channels?

Non-invasive stimulators clear regulatory hurdles for outpatient use, and European payers now cover devices prescribed directly by physiotherapists, driving an 11.45% CAGR in these settings.

What regions will contribute most to future market expansion?

Asia-Pacific, led by China's accelerated approvals and local manufacturing scale-up, is projected to post the fastest 9.90% CAGR through 2031 despite current reimbursement gaps.

How are leading companies maintaining competitive advantage?

Incumbents bundle hardware with proprietary algorithms, pursue vertical integration via M&A, and invest in cybersecurity compliance to meet new FDA requirements while smaller firms focus on niche indications.

Page last updated on: