Neuroendoscopy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 4.7 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neuroendoscopy Market Analysis by Mordor Intelligence

The neuroendoscopy market size is expected to grow from USD 3.45 billion in 2025 to USD 3.63 billion in 2026 and is forecast to reach USD 4.7 billion by 2031 at 5.30% CAGR over 2026-2031. This expansion reflects rising preference for minimally invasive procedures that shorten recovery while preserving neurological function. Momentum is sustained by cross-fertilization between high-definition optics, navigation software, robotics and artificial-intelligence-driven image analysis, which together broaden the applications of endoscopic neurosurgery and elevate procedural accuracy. Disposable instruments—though still a minority—are capturing share as infection-control priorities intensify, and the growing installed base of navigation-integrated towers lowers barriers to clinical adoption. Competitive dynamics remain moderately concentrated: large multinationals leverage global distribution and R&D scale, yet specialized entrants are making headway in single-use devices and pediatric-specific platforms. Headwinds persist where hospitals struggle to fund capital equipment and where the steep learning curve slows surgeon uptake, especially outside tier-one centers.

Key Report Takeaways

- By application, transcranial procedures expanded at a 9.12% CAGR to 2031 while intraventricular techniques retained a 42.30% revenue share in 2025.

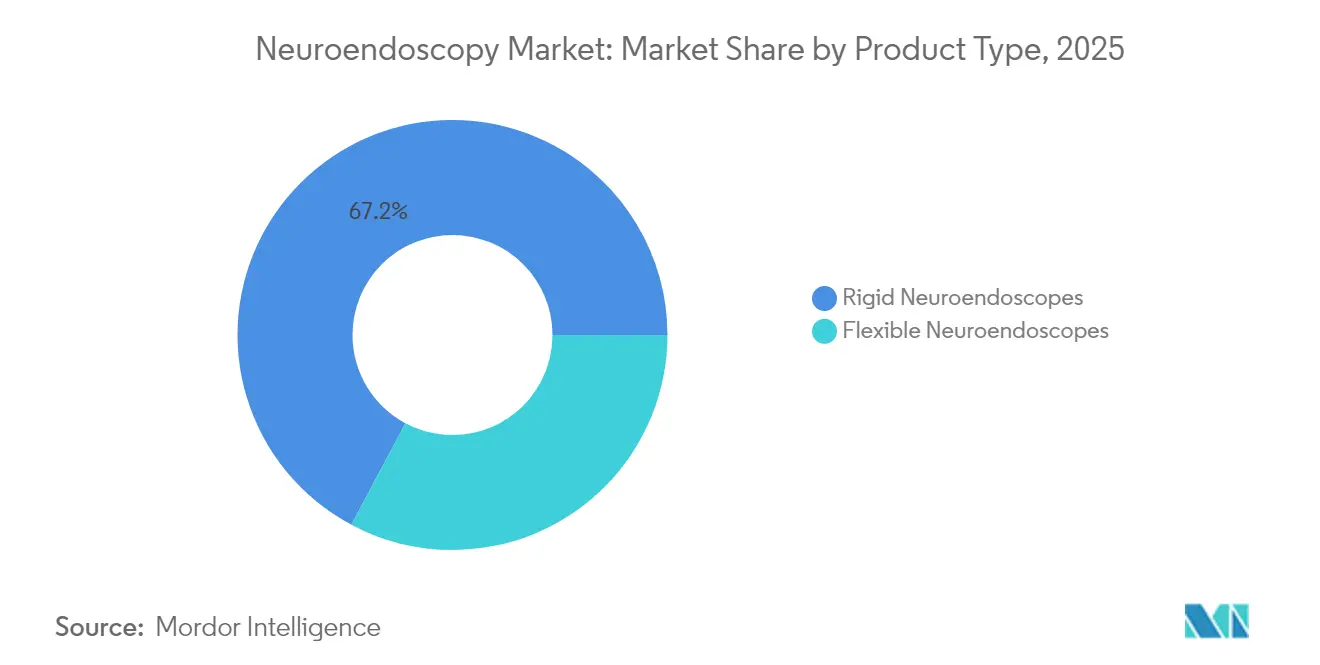

- By product type, rigid scopes held 67.20% of the neuroendoscopy market share in 2025; flexible scopes are projected to climb at an 8.06% CAGR through 2031.

- By usability, reusable instruments commanded 66.25% share of the neuroendoscopy market size in 2025; the disposable category is tracking a 7.62% CAGR to 2031.

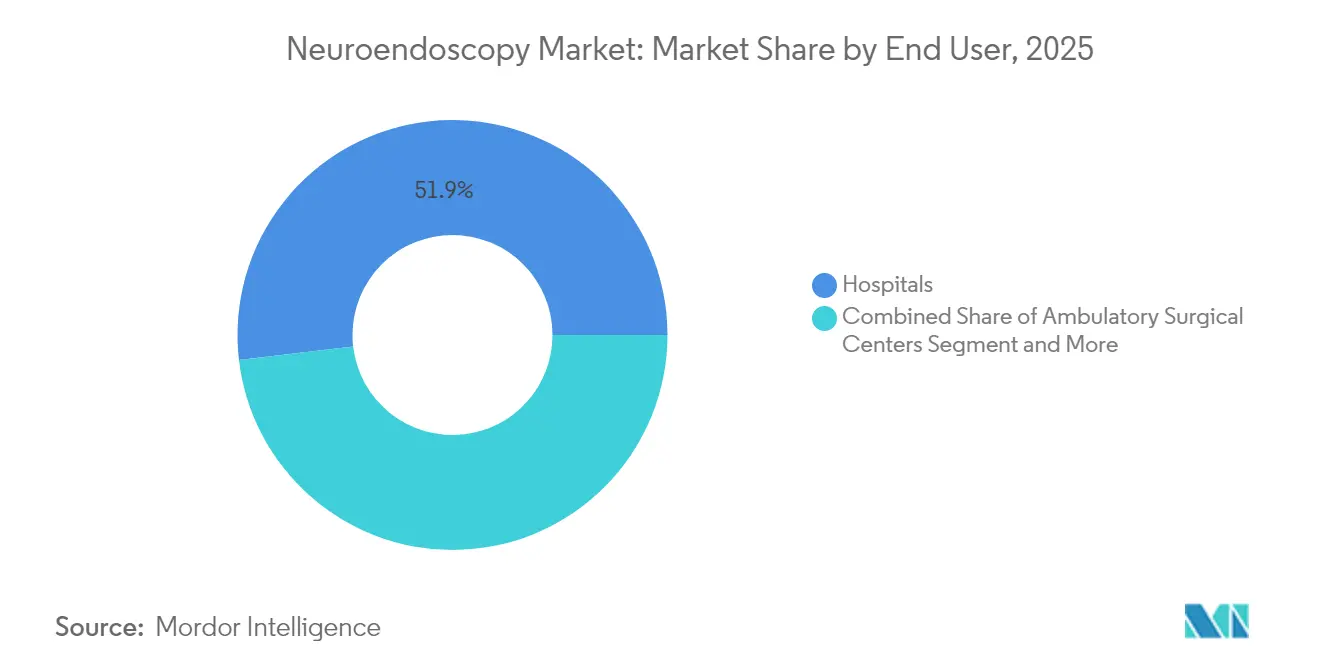

- By end user, hospitals controlled 51.85% of the neuroendoscopy market size in 2025, whereas ambulatory centers are set to post an 7.74% CAGR between 2026-2031.

- By patient demographics, adults accounted for 69.10% share of the market size in 2025 and the pediatric cohort is expanding at a 7.28% CAGR through 2031.

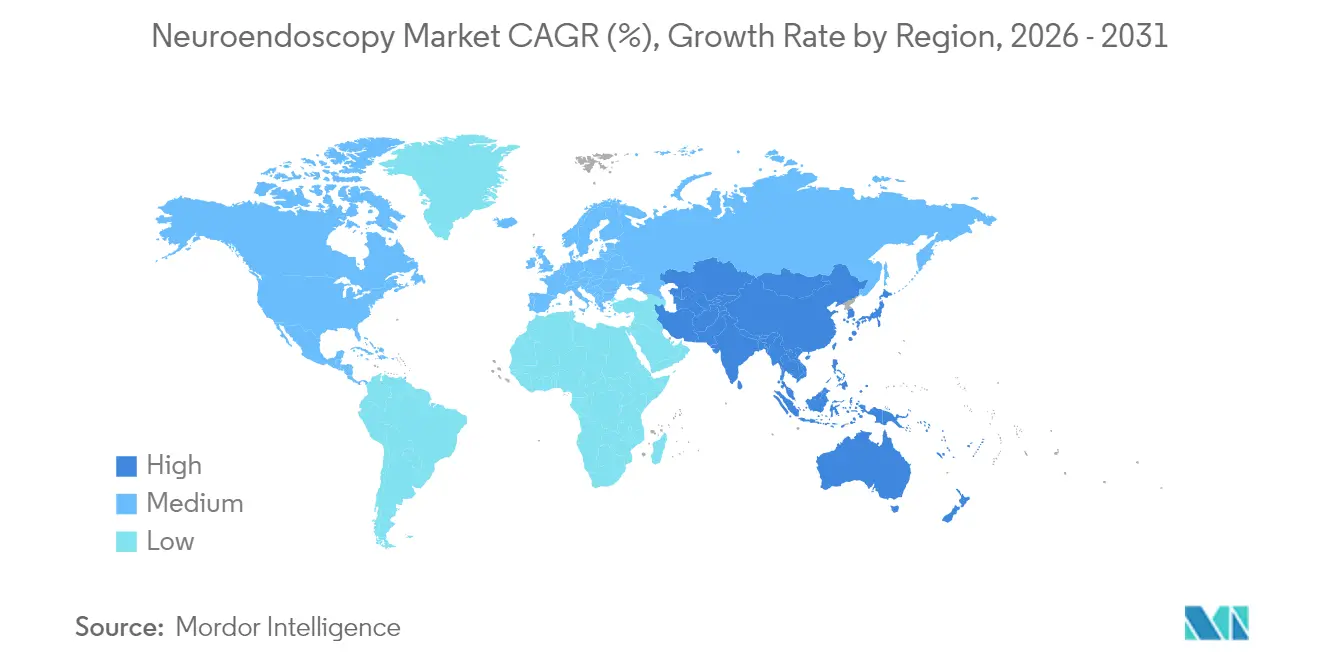

- By geography, North America dominated with 37.40% revenue in 2025; Asia-Pacific records the fastest regional CAGR at 8.83% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neuroendoscopy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Burden of Brain & Skull-Base Tumors Increasing Demand for Minimally Invasive Neuroendoscopy | +1.8 | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Technological Advancements in Optics, Visualization, and Navigation Enhancing Clinical Outcomes | +1.2 | North America, Europe, and advanced APAC markets | Medium term (2-4 years) |

| Expanding Healthcare Infrastructure and Neurosurgery Capacity in Emerging Economies | +1.5 | APAC core (China, India), with spill-over to MEA | Long term (≥ 4 years) |

| Favorable Regulatory and Reimbursement Policies Supporting Adoption of Neuroendoscopic Devices | +0.9 | North America and Europe | Short term (≤ 2 years) |

| Aging Population Susceptibility to Neurological Disorders Stimulating Procedure Volumes | +1.1 | Global, with higher impact in Japan, Europe, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Brain & Skull-Base Tumors Increasing Demand for Minimally Invasive Neuroendoscopy

The global prevalence of nervous-system disorders affects 3.8 billion people, and central-nervous-system tumors impose growing morbidity. Glioblastoma multiforme remains difficult to manage, spurring surgeons to adopt approaches that reduce cortical disruption while achieving maximal safe resection. Clinical studies published in 2024 show neuroendoscopic resections require craniotomy areas up to 70% smaller than conventional microsurgery, with comparably high extirpation rates and lower complication incidence. These outcomes reinforce the shift toward minimally invasive techniques as caseloads climb.

Technological Advancements in Optics, Visualization, and Navigation Enhancing Clinical Outcomes

Real-time 3D reconstruction paired with neuroendoscopy has improved shunt placement accuracy for hydrocephalus, cutting malposition complications in recent multicenter trials. Purpose-built robotic arms stabilize instrumentation in narrow corridors and provide sub-millimetric tremor filtration, extending reach to previously inaccessible lesions. Together, these advances lift surgeon confidence and are shortening operating times in early adopter sites.

Expanding Healthcare Infrastructure and Neurosurgery Capacity in Emerging Economies

China and India are allocating record capital budgets to neurosurgery suites, and domestic vendors are launching competitively priced single-use scopes that undercut imports. India’s Sri Sathya Sai Institute has demonstrated that a no-cost-to-patient model can deliver 34,000 neurosurgeries over two decades with modern endoscopic platforms, highlighting feasibility for volume expansion in resource-constrained contexts[1]Sumit Thakar et al., “Value-Based, No-Cost-To-Patient Neurosurgery …,” LWW.COM, lww.com.

Favorable Regulatory and Reimbursement Policies Supporting Adoption of Neuroendoscopic Devices

A 2024 cost-effectiveness analysis comparing MR-guided laser therapy with open craniotomy for radiation necrosis reported an incremental cost-effectiveness ratio of –USD 183,464 per QALY owing to lower length of stay and complication rates. Evidence that minimally invasive routes reduce outlays is feeding into payer coverage decisions in the United States and Europe, accelerating capital procurement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs of Advanced Neuroendoscopic Systems Restricting Uptake in Resource-Constrained Settings | -1.2 | Global, with higher impact in developing regions | Medium term (2-4 years) |

| Steep Learning Curve and Limited Surgeon Training Affecting Procedure Adoption Rates | -0.8 | Global, with higher impact in regions with fewer specialized training centers | Short term (≤ 2 years) |

| Concerns Over Device Reprocessing, Sterility, and Associated Litigation | -0.6 | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Advanced Systems Restricting Uptake

Procurement of neuronavigation-ready towers, high-resolution cameras and rigid scopes often exceeds a department’s annual equipment budget in low-income settings. Ongoing calibration and service contracts further strain finances, widening the gap between high-income and middle-income facilities where neurosurgical needs are surging.

Steep Learning Curve and Limited Surgeon Training Affecting Adoption Rates

Endoscopic neurosurgery demands finesse in bimanual manipulation within cramped fields. Surveys show nearly one-third of surgeons hesitate to adopt due to insufficient training opportunities and perceived risk of complications during early cases[2]“Australian Spine Surgeons’ Perspectives on Endoscopic Spine Surgery,” E-NEUROSPINE.ORG, e-neurospine.org. Program directors are expanding simulator-based curricula, yet capacity remains inadequate relative to global demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid Dominates While Disposables Gain Momentum

Rigid scopes captured 67.20% of 2025 revenue, underpinning the neuroendoscopy market share advantage of systems offering crystal-clear optics suited to intraventricular and skull-base corridors. Flexible scopes are accelerating at an 8.06% CAGR from 2026 to 2031. Manufacturers are shrinking distal tip diameters below 4 mm and integrating chip-on-the-tip cameras that rival reusable counterparts in resolution. Augmented-reality overlays now project anatomic landmarks directly onto surgeon displays, a capability under evaluation in multicenter trials.

Advances in polymer optics and recyclable packaging aim to mitigate environmental concerns cited by hospital sustainability boards. Early lifecycle assessments suggest carbon-neutral production of selected single-use models is achievable if renewable-energy inputs exceed 60% of total manufacturing consumption. As pricing narrows between premium reusable kits and turnkey disposable sets, hospitals are recalibrating value analyses that consider downtime due to scope damage or decontamination backlog.

By Usability: Reusable Instruments Face Sustainability Challenges

Reusable units comprise 66.25% of the 2025 neuroendoscopy market size thanks to amortization over hundreds of procedures. Decontamination protocols, however, require multistep workflows that raise labor and chemical costs while exposing facilities to compliance lapses. NICE has cautioned that single-use scopes can be cost-ineffective when high-throughput reprocessing infrastructure exists, yet it also acknowledges reprocessing failures as a litigatory flashpoint.

Industrial design changes—detachable light cables, scratch-resistant sapphire windows and reinforced angulation mechanisms—are extending reusable scope lifespans beyond 2,000 cycles, bending cost curves in favor of retention. Parallel work on biodegradable polymers for single-use channels signals an eventual convergence where clinical, economic and environmental metrics can be met simultaneously.

By Application: Transcranial Approaches Expand Procedural Horizons

Intraventricular surgeries, led by endoscopic third ventriculostomy, held 42.30% of 2025 revenue. The neuroendoscopy market size for transcranial techniques is rising quickest, charting a 9.12% CAGR as supraorbital keyhole entries permit access to aneurysms, meningiomas and craniopharyngiomas while limiting bone removal to an average 3.77 cm opening. Clinical series document 81% favorable outcomes for aneurysm clipping with this hybrid approach and 89% for space-occupying lesions.

Endonasal routes remain pivotal for pituitary adenomas; randomized cohorts that incorporated a reserved gastric tube during resection logged lower postoperative nausea, reduced sore-throat scores and shorter inpatient stays. Diversification into cerebrovascular bypass assistance and spinal intradural cyst fenestration underscores broadening utility, positioning neuroendoscopy market growth across multiple subspecialties.

By End User: Ambulatory Centers Drive Procedural Migration

Hospitals retained 51.85% of 2025 revenues as complex tumor resections and acute hydrocephalus cases demand ICU backup. Yet ambulatory surgical centers are registering an 7.74% CAGR to 2031, propelled by payers steering elective biopsies and low-risk cyst fenestrations to lower-cost venues. Workflow efficiencies—including same-day discharge and bundled pricing—enhance patient satisfaction and free inpatient beds for higher acuity care. Specialty clinics devoted to skull-base pathology or pediatric hydrocephalus are also emerging, leveraging focused expertise to shorten waitlists.

Academic institutes continue to generate technique innovation and maintain steady but smaller procedure counts; their influence on guidelines and surgeon training amplifies downstream adoption across community facilities.

By Patient Demographics: Pediatric Applications Show Accelerated Growth

Adults account for 69.10% of 2025 procedures, yet pediatric cases are climbing at a 7.28% CAGR given neuroendoscopy’s ability to spare developing neural tissue. Endoscopic third ventriculostomy with choroid plexus cauterization now rivals shunting in infants, delivering reduced infection and revision rates. Up to 56.7% of pediatric brain-tumor patients present with hydrocephalus, making ventricular endoscopy integral to multidisciplinary care. Case reports detail its role in combined treatment for disseminated medulloblastoma, further validating the modality’s versatility.

Miniaturized scopes—outer diameters below 2 mm—and flexible biopsy forceps tailored to smaller ventricles have improved safety profiles. Pediatric-centric device launches therefore represent a strategic growth frontier for manufacturers seeking differentiation.

Geography Analysis

North America led with 37.40% revenue in 2025, supported by advanced hospital networks, rapid FDA clearance pathways and high neurosurgical training density. AI-augmented planning platforms are increasingly integrated with navigation systems, sharpening resection margins and bolstering first-pass success rates.

Asia-Pacific is the fastest-growing region at 8.83% CAGR to 2031. Japan’s aging population, coupled with universal coverage, drives robust equipment refresh cycles. China’s domestic producers, such as Scivita Medical Technology, are challenging foreign incumbents, signaling a shift in vendor mix. India’s public–private hospital expansion is widening access to endoscopic suites, while training exchanges with global centers raise procedural competency levels.

Europe maintains meaningful share as national health systems encourage minimally invasive strategies to trim lengths of stay. The Middle East and Africa are witnessing targeted investments in tertiary centers within the Gulf Cooperation Council and South Africa. In Latin America, Brazil and Argentina lead adoption, underpinned by academic partnerships and charitable outreach; the Neurosurgery Outreach Foundation has demonstrated scalable impact through 1,985 surgeries conducted across low-resource settings.

Competitive Landscape

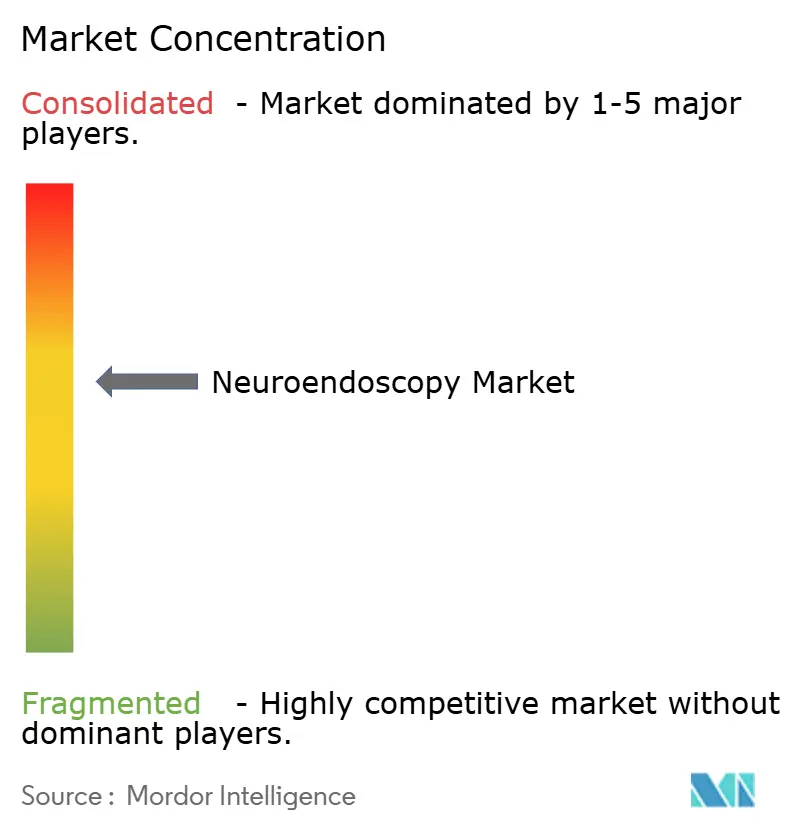

Market concentration is moderate: Medtronic, KARL STORZ and Olympus draw on global reach, but specialized firms are narrowing gaps via focused R&D. Medtronic’s 2024 FDA nod for asleep deep-brain stimulation underscores its leadership in integrated platforms that dovetail with neuroendoscopy towers. KARL STORZ broadened its single-use visualization line in April 2025, targeting infection-control-sensitive segments. ClearPoint Neuro has invested in MRI-guided stereotactic systems compatible with endoscopic ports, enhancing real-time trajectory monitoring.

Patent filings spotlight instrument-tracking algorithms that auto-recognize tool type and orientation, promising to curtail wrong-site deployments and streamline digital surgical logs. Regional challengers concentrate on lower-price tiers and pediatric indications. Opportunities remain to design greener single-use scopes, integrate fluorescence imaging and develop portable towers for field neurosurgery missions.

Neuroendoscopy Industry Leaders

Adeor Medical AG

B. Braun Melsungen AG

Clarus Medical

KARL STORZ SE & Co. KG

Machida Endoscope Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Karl Storz debuted the Slimline C-MAC S single-use video laryngoscope for neurosurgical visualization.

- January 2024: EndoSound secured FDA 510(k) clearance for its EndoSound Vision System, enabling high-resolution ultrasound guidance during neuroendoscopic procedures.

Global Neuroendoscopy Market Report Scope

As per the scope of the report, neuroendoscopy is a minimally invasive surgical procedure in which the neurosurgeon removes the tumor through small holes in the skull or through the mouth or nose. The neuroendoscopy market is segmented by product (rigid neuroendoscopes and flexible neuroendoscopes), application (transnasal neuroendoscopy, intraventricular neuroendoscopy, and transcranial neuroendoscopy), usability (reusable neuroendoscopes and disposable neuroendoscopes), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report offers the value (in USD million) for the above segments.

| Rigid Neuroendoscopes | Videoscopes |

| Fiberscopes | |

| Flexible Neuroendoscopes |

| Reusable Neuroendoscopes |

| Disposable / Single-Use Neuroendoscopes |

| Transnasal Neuroendoscopy |

| Intraventricular Neuroendoscopy |

| Transcranial Neuroendoscopy |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Research & Academic Institutes |

| Adult |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Rigid Neuroendoscopes | Videoscopes |

| Fiberscopes | ||

| Flexible Neuroendoscopes | ||

| By Usability | Reusable Neuroendoscopes | |

| Disposable / Single-Use Neuroendoscopes | ||

| By Application (Surgery Type) | Transnasal Neuroendoscopy | |

| Intraventricular Neuroendoscopy | ||

| Transcranial Neuroendoscopy | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Research & Academic Institutes | ||

| By Patient Demographics | Adult | |

| Pediatric | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the neuroendoscopy market in 2026?

The neuroendoscopy market size stands at USD 3.63 billion in 2026 and is projected to reach USD 4.7 billion by 2031.

Which neuroendoscopy application is growing fastest?

Transcranial procedures are expanding at a 9.12% CAGR, reflecting wider adoption for skull-base and aneurysm cases.

What region will post the strongest growth to 2031?

Asia-Pacific is set to grow at 8.83% CAGR, led by China, Japan and India, thanks to infrastructure investment and domestic device production.

Why are disposable neuroendoscopes gaining traction?

Single-use scopes reduce cross-contamination risk and simplify workflow, driving an 7.62% CAGR despite environmental concerns.

What is the key barrier to wider neuroendoscopy adoption?

High capital costs and a steep surgeon learning curve remain the primary obstacles, especially in resource-constrained hospitals.

Which companies lead innovation in neuroendoscopy?

Medtronic, KARL STORZ and Olympus leverage integrated imaging and navigation platforms, while specialists like Scivita focus on cost-efficient single-use devices.

Page last updated on: