Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

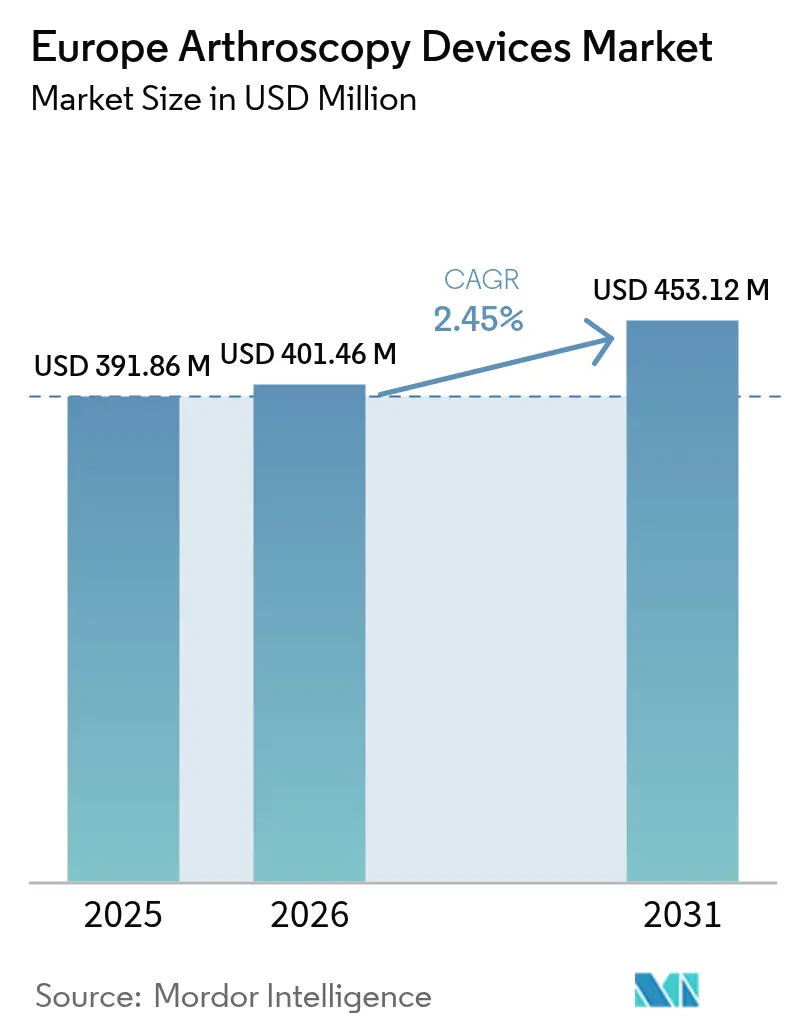

| Base Year Market Size (2025) | USD 391.86 Million |

| Market Size (2026) | USD 401.46 Million |

| Market Size (2031) | USD 453.12 Million |

| Growth Rate (2026 - 2031) | 2.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Arthroscopy Devices Market Analysis by Mordor Intelligence

The Europe arthroscopy devices market size is expected to grow from USD 391.86 million in 2025 to USD 401.46 million in 2026 and is forecast to reach USD 453.12 million by 2031 at 2.45% CAGR over 2026-2031. Demand is sustained by the simultaneous rise in sports-related trauma and degenerative joint disease, even as reimbursement reforms tighten margins and temper headline growth. Population aging keeps osteoarthritis procedures on hospital calendars, while widening sports participation broadens the pool of injuries treated with minimally invasive techniques. Device makers that streamline workflow for same-day discharge win share because European payers now reimburse outpatient arthroscopy more favorably than inpatient care. At the same time, EU-MDR compliance costs deter smaller entrants, allowing incumbents with regulatory scale to channel resources into 4K/8K visualization, biologic implants, and single-use kits that shorten turnover time in high-volume ambulatory surgical centers.

Key Report Takeaways

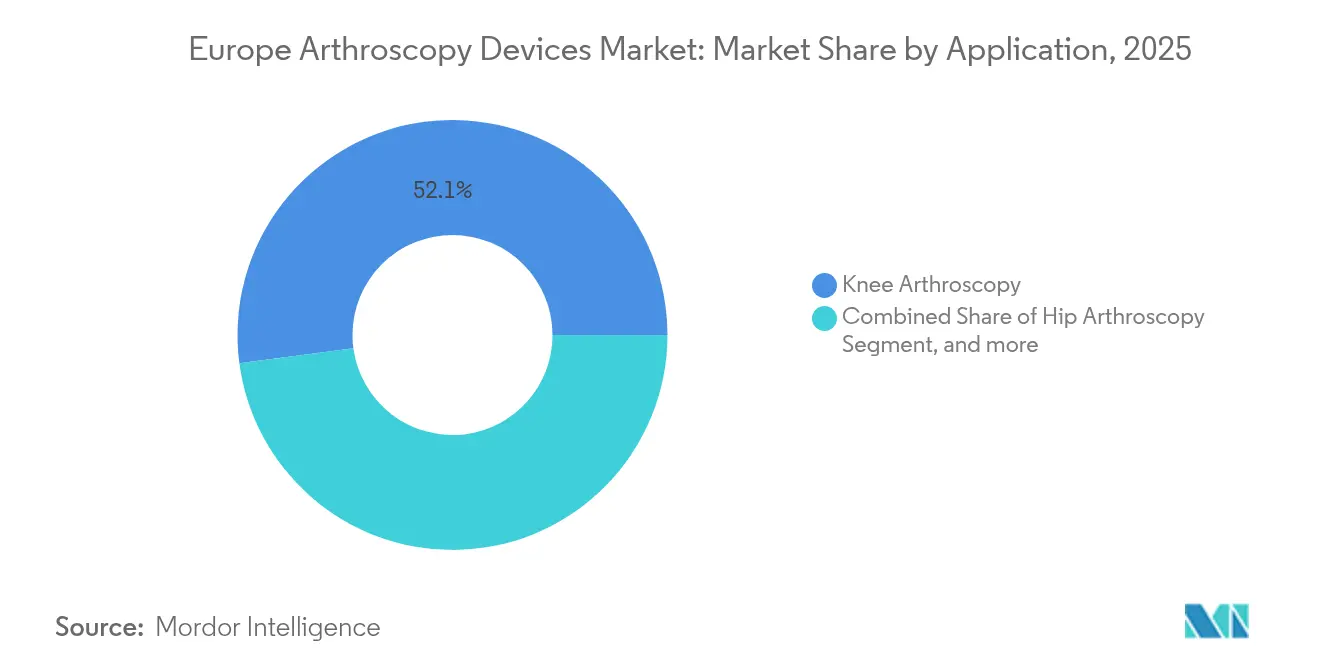

- By application, knee procedures held 52.10% of Europe arthroscopy devices market share in 2025; hip arthroscopy exhibits the fastest expansion at a 4.34% CAGR through 2031.

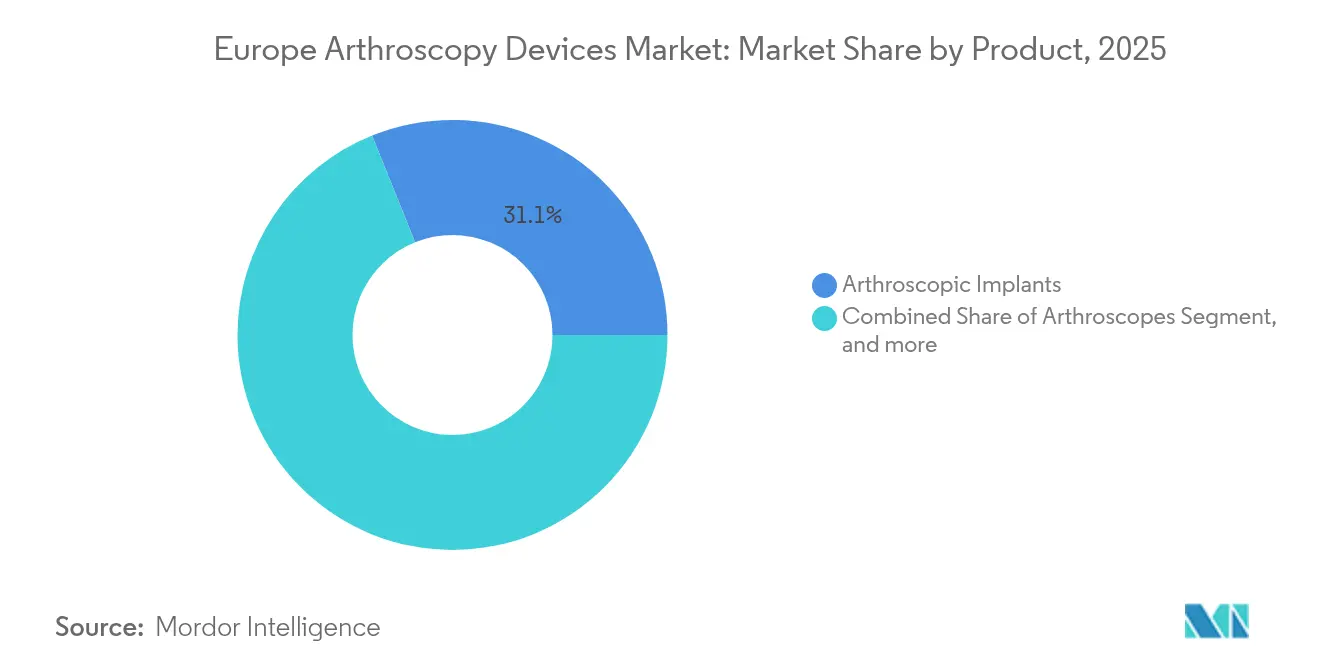

- By product, implants accounted for 31.10% of the Europe arthroscopy devices market size in 2025, whereas radio-frequency and energy systems deliver the quickest growth at 4.28% CAGR to 2031.

- By end user, hospitals captured 55.00% revenue in 2025, while ambulatory surgical centers post the highest 4.55% CAGR through 2031.

- By country, Germany dominated with a 33.85% share of the Europe arthroscopy devices market size in 2025; Spain leads the growth league at a 3.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Arthroscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating sports-injury incidence | +0.4% | Pan-European, strongest in Germany, UK, France | Medium term (2-4 years) |

| Rapid growth of same-day arthroscopy centres | +0.6% | Western Europe, expanding to Central & Eastern Europe | Short term (≤ 2 years) |

| Ageing population with osteoarthritis | +0.5% | All Europe, acute in Germany and Italy | Long term (≥ 4 years) |

| Mini-robotic & needle-scope adoption | +0.4% | Technology-leading markets: Germany, Netherlands, Switzerland | Medium term (2-4 years) |

| MDR post-market-surveillance upgrade cycle | +0.2% | EU-wide | Short term (≤ 2 years) |

| AI-assisted 4K/8K visualisation uptake | +0.3% | Germany, Netherlands, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Sports-Injury Incidence

European participation in organized recreation keeps trending upward, and the injury burden follows. UEFA surveillance reports an anterior cruciate ligament injury rate of 0.09 per 1,000 exposure hours in women’s football, translating into high knee arthroscopy volumes[1]European Society for Sports Traumatology, Knee Surgery & Arthroscopy, "UEFA Injury Surveillance Report," esska.org . National cohort studies show sports-related knee injuries running 300-400% above baseline in football, basketball, and skiing demographics, which dovetail with Europe’s leisure interests. Clinical consensus now favors meniscal preservation, boosting demand for repair anchors, biologic augmentation, and premium implants over basic debridement tools. Because return-to-sport protocols require anatomic restoration, surgeons lean on higher-priced fixation systems that promise faster healing. Together these factors lift procedure value even as overall case counts rise modestly.

Rapid Growth of Same-Day Arthroscopy Centers

Ambulatory surgical centers capture arthroscopy volume as payers pay close attention to cost per case. Switzerland already completes 67% of surgeries on an outpatient basis, and Hungary stands at 58%[2]Organisation for Economic Co-operation and Development, "Health Statistics 2024," oecd.org . Germany’s 2025 DRG catalog unlocks new outpatient codes, tilting reimbursement in favor of same-day knee and hip scopes. The shift pressures suppliers to design single-use shavers, sealed optics, and self-contained fluid pumps that bypass central sterilization bottlenecks. Fast-setup integrated towers support compressed turnover times and lower staffing ratios, a critical benefit as Europe faces a 1.8 million healthcare-worker shortfall. Vendors able to validate workflow savings win ASC tenders despite the sector’s small but fast-growing base.

Aging Population with Osteoarthritis

Western Europe posts age-standardized osteoarthritis prevalence of 3,500–4,000 per 100,000 residents, and incidence climbs in lockstep with population aging. Arthroscopy remains part of the therapeutic pathway—often preceding viscosupplementation or joint replacement particularly for degenerative meniscal tears and multifocal cartilage damage. German health systems, sitting at Europe’s demographic epicenter, consequently consume the largest share of scopes, implants, and visualization stacks. EUROVISCO’s 2024 guidance underscores patient clusters for which arthroscopy plus injection therapy outperforms either treatment alone, sustaining volume despite the rise of non-operative modalities[3]Cartilage Journal, "EUROVISCO 2024 Consensus Guidelines," cartilagejournal.org. Complex multi-compartment pathology common in older adults propels interest in advanced suture systems and multichannel pumps that keep fields clear during prolonged procedures.

AI-Assisted 4K/8K Visualization Uptake

Ultra-high-definition optics paired with real-time AI decision support redefine intra-articular assessment. German surgeons report measurably shorter operative times and lower revision rates after adopting AI-enhanced 4K towers. Algorithms highlight micro-tears invisible on standard HD, auto-generate operative notes, and flag optimal portal placement, easing cognitive load for overstretched surgical teams. EU-MDR offers software-as-a-medical-device validation pathways that move faster than hardware approvals, encouraging device makers to bundle AI modules with cameras and endoscopes. Facilities implementing 8K towers embark on staged replacement cycles that lift capital equipment budgets even amid reimbursement pressures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of fellowship-trained arthroscopists | -0.3% | Pan-European, acute in Eastern Europe | Long term (≥ 4 years) |

| Pan-EU price ceilings & tenders | -0.4% | EU-wide, strongest impact in public systems | Short term (≤ 2 years) |

| Lengthy EU-MDR recertification backlog | -0.3% | EU-wide | Short term (≤ 2 years) |

| Post-pandemic OR staffing deficits | -0.2% | Pan-European, severe in Italy and Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Fellowship-Trained Arthroscopists

Europe’s orthopedic pipeline cannot keep pace with demand, and experienced arthroscopists migrate westward for better pay and resources. Fellowship programs add one to two years beyond residency, lengthening the path to competence and capping immediate capacity. Eastern European hospitals feel the pinch most acutely as talent exits for Germany and the Netherlands. As a result, high-complexity meniscal repairs and hip scopes often face scheduling backlogs, slowing premium device pull-through. Medical schools are enlarging sports-medicine cohorts, yet the early-career wave will not materialize before the late 2020s. This human-capital bottleneck eats into revenue potential even where patient queues are long.

Pan-EU Price Ceilings & Tenders

Centralized procurement is the rule in Europe’s tax-funded systems, and recent DRG revisions in Germany impose implicit cost caps on arthroscopic consumables. Italy’s delayed tariff update further muddies outlook, and hospitals respond with aggressive volume-based tenders that squeeze margins. The European Commission’s scrutiny of device prices under the EU4Health initiative portends wider adoption of reference pricing. Value-based awards, in which functional outcomes trump bells and whistles, disadvantage breakthrough products that carry high R&D amortization. Consequently, suppliers must document clear cost offsets—shorter OR time, fewer complications—before commanding any price premium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Knee Procedures Drive Volume Growth

Knee cases captured 52.10% of Europe arthroscopy devices market share in 2025, underscoring the joint’s vulnerability to contact and pivoting sports as well as degenerative wear. Hip scopes, while newer in routine practice, chart a 4.34% CAGR to 2031, paced by growing diagnoses of femoroacetabular impingement in younger, athletic adults. ESSKA’s 2024 consensus advocating meniscal repair over resection elevates per-case implant count and aligns with the premiumization trend. The Europe arthroscopy devices market size linked to knee interventions benefits from broader instrument trays, biologic scaffolds, and high-flow pumps that maintain visibility during complex repairs. Shoulder and elbow indications remain steady, driven by cuff disease in aging workers, while ankle and wrist scopes get a lift from instrument miniaturization suited to small-joint anatomy. As procedure coding standardizes across the bloc, surgeons leverage unified training modules that further entrench knee and hip techniques at the top of the case-mix hierarchy.

Surgeons performing knee scopes increasingly prefer all-inside repair systems that cut tunnel drilling time and facilitate outpatient workflows. Hip-specific portals have matured, enabling labral preservation that delays arthroplasty and justifies adoption in younger cohorts. The Europe arthroscopy devices industry also sees rising use of biologic augmentation—PRP, bone-marrow concentrate—inside the joint capsule, layering consumable sales onto base hardware. Because national registries, such as the UK’s NJR, now track re-intervention rates, facilities gravitate toward implants with long-term data, reinforcing brand stickiness among leading vendors. Collectively these trends lock knee procedures into the volume leader’s seat while empowering hip scopes to deliver the strongest incremental growth.

By Product: Implants Lead Despite Energy System Innovation

Implants held 31.10% of the Europe arthroscopy devices market size in 2025, reflecting their pivotal role in definitive tissue fixation. Smith+Nephew’s rollout of the AGILI-C cartilage implant and REGENETEN scaffold typifies a shift toward biologic solutions that combine mechanical stability with regenerative cues. Radio-frequency probes and plasma wands post a 4.28% CAGR on the promise of precise tissue modulation, reduced bleeding, and faster turnover, making them attractive in the ambulatory setting. Arthroscopes themselves now adopt chip-on-tip sensors and disposable sheaths, but replacement cycles remain linked to optical advances rather than volume spikes.

Power shavers compete with energy devices, yet the best outcomes often rely on a hybrid setup, preserving demand for both lines. Fluid management consoles integrate suction, inflow, and pressure regulation under touchscreen control, an appealing value proposition to staff-constrained ORs. Visualization towers move from HD to 4K and soon to 8K, establishing a capital equipment replacement curve that cushions suppliers against soft consumables pricing. With EU-MDR raising the bar for re-approvals, larger companies capitalize on breadth of catalog to cross-sell implants, pumps, and scopes as bundled solutions, deepening account penetration across Europe.

By End User: ASCs Accelerate Amid Hospital Dominance

Hospitals retained a 55.00% revenue share of the Europe arthroscopy devices market in 2025, buoyed by legacy infrastructure, trauma call coverage, and the complexity of revision work. Yet, ambulatory surgical centers are the undisputed growth engine, expanding at a 4.55% CAGR and winning reimbursement uplifts from payers keen to lower per-case expenses. Switzerland’s outpatient penetration of 67% shows what mature ASC ecosystems can achieve, and Germany’s 2025 coding reform opens similar pathways. The Europe arthroscopy devices market size tied to ASCs grows not just through higher case counts but through premium for single-use shavers, pre-sterile implant caddies, and all-in-one visualization carts that reduce turnaround time.

Office-based settings remain niche, limited to diagnostic needle arthroscopy and minor debridement due to sterility and anesthesia constraints. Hospitals increasingly reserve operating room blocks for complex reconstructions, while straightforward meniscal or labral repairs migrate to ASCs. Device vendors tailor packaging color-coded trays, RFID tracking to fit lean ASC staffing, enhancing traceability and speeding counts. Over the forecast horizon, any product that trims minutes off room occupancy or obviates re-sterilization can price at a premium, even under Europe’s tight tender rules.

Geography Analysis

Germany commanded 33.85% of Europe arthroscopy devices market share in 2025, a product of strong orthopedic training, broad insurance coverage, and DRG pathways that reimburse both hospital and ambulatory cases. The country’s adoption of AI-guided 4K towers sets a technology benchmark others emulate. Spain, while smaller, registers the fastest advance at 3.42% CAGR, propelled by health-system modernization, sports-medicine investment, and expanded ASC capacity in Madrid and Catalonia. The United Kingdom remains sizable but navigates post-Brexit regulatory divergence that complicates CE-mark transitions.

France leverages centralized procurement to standardize implant selection, while Italy's delayed tariff update creates reimbursement uncertainty that constrains premium adoption. The Europe arthroscopy devices market size in Nordic countries benefits from value-based frameworks that reward documented outcomes over acquisition cost. Medartis's 17% EMEA growth, anchored by German expansion, illustrates how distributors can capitalize on geographic variation in adoption curves. Regulatory harmonization under EU-MDR creates a more uniform compliance landscape, yet reimbursement remains stubbornly national, requiring country-specific market-access strategies.

Competitive Landscape

Germany's 34.11% share of the Europe arthroscopy devices market in 2024 reflects its triple advantages: demographic scale, healthcare sophistication, and regulatory leadership. The country's aging population drives osteoarthritis volume, while its robust sports culture generates trauma cases across all age brackets. Germany's 2025 DRG catalog expansion specifically accommodates outpatient arthroscopy, creating payment pathways that reward same-day discharge. As the EU-MDR regulatory nerve center, German approval often precedes broader European rollout, giving local hospitals first access to compliant technologies. Medartis's expansion of its Umkirch distribution hub to 1,100 square meters underscores the country's pivotal role in European device logistics, supporting the company's 17% EMEA growth trajectory.

Spain's 3.56% CAGR through 2030 outpaces the regional average, driven by healthcare modernization and expanded surgical capacity. The country's investment in ambulatory infrastructure aligns with European trends toward outpatient care delivery, while its aging population sustains demand for joint preservation. Spanish procurement increasingly emphasizes value-based purchasing that rewards documented outcomes over marketing claims. The national sports medicine infrastructure, particularly around football and basketball academies, generates steady arthroscopic volume that complements age-related degenerative pathology. As Spanish centers adopt advanced visualization and energy-based tissue management, per-procedure device consumption rises even as case counts grow modestly.

The United Kingdom, France, and Italy represent mature markets with established practice patterns and procurement relationships. Post-Brexit, the UK navigates a distinct regulatory path that adds complexity for manufacturers but preserves access to advanced arthroscopic technologies. France's centralized purchasing leverages volume discounts while standardizing clinical protocols, and Italy's delayed tariff implementation creates reimbursement uncertainty that constrains premium adoption. Across Northern Europe, including the Netherlands, Switzerland, and Nordic countries, advanced healthcare systems prioritize patient outcomes and technological innovation, creating receptive markets for devices that demonstrate clear clinical value. The Europe arthroscopy devices market size varies substantially by country, yet the underlying trend toward ambulatory care, biologic augmentation, and workflow optimization transcends national boundaries.

Europe Arthroscopy Devices Industry Leaders

-

Johnson & Johnson (DePuy Synthes)

-

Arthrex Inc.

-

Conmed Corporation

-

Richard Wolf GmbH

-

Karl Storz GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Smith+Nephew expanded its Sports Medicine portfolio with the CARTIHEAL AGILI-C cartilage repair implant and REGENETEN Bioinductive Implant for tendon augmentation. The CARTIHEAL system, which received FDA Breakthrough Device designation, demonstrated double the pain reduction compared to standard microfracture in multicenter randomized trials.

- January 2024: The da Vinci Single-Port robotic system obtained CE mark for European market entry. Its 25mm single-shaft design houses three multi-jointed instruments, representing significant miniaturization for minimally invasive procedures with potential applications in small-joint arthroscopy.

Europe Arthroscopy Devices Market Report Scope

As per the scope of the report, arthroscopy devices are used to examine the bone joints for specific conditions, such as osteoarthritis, rheumatoid arthritis, tendinitis, and bone tumor.

The European Arthroscopy Devices Market is Segmented by by Application (Knee Arthroscopy, Hip Arthroscopy, Spine Arthroscopy, Shoulder and Elbow Arthroscopy, Other Arthroscopy Applications), Product (Arthroscopes, Arthroscopic Implants, Powered Shavers & Resection Systems, Fluid Management Systems, Radio-frequency & Energy Systems, Visualisation & Imaging Systems, Other Products), End User (Hospitals, Ambulatory Surgical Centres, Office-based Settings), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The report offers the market size and forecasts in value (USD million) for the above segments.

By Application

| Knee Arthroscopy |

| Hip Arthroscopy |

| Spine Arthroscopy |

| Shoulder and Elbow Arthroscopy |

| Other Arthroscopy Applications |

By Product

| Arthroscopes |

| Arthroscopic Implants |

| Powered Shavers & Resection Systems |

| Fluid Management Systems |

| Radio-frequency & Energy Systems |

| Visualisation & Imaging Systems |

| Other Products |

By End User

| Hospitals |

| Ambulatory Surgical Centres (ASCs) |

| Office-based / In-clinic Settings |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Application | Knee Arthroscopy |

| Hip Arthroscopy | |

| Spine Arthroscopy | |

| Shoulder and Elbow Arthroscopy | |

| Other Arthroscopy Applications | |

| By Product | Arthroscopes |

| Arthroscopic Implants | |

| Powered Shavers & Resection Systems | |

| Fluid Management Systems | |

| Radio-frequency & Energy Systems | |

| Visualisation & Imaging Systems | |

| Other Products | |

| By End User | Hospitals |

| Ambulatory Surgical Centres (ASCs) | |

| Office-based / In-clinic Settings | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe arthroscopy devices market by 2031?

The market is forecast to reach USD 453.12 million by 2031, expanding at a 2.45% CAGR from its 2026 base of USD 401.46 million.

Which joint procedure is expected to grow the fastest over the next five years?

Hip arthroscopy leads the growth chart with a 4.34% CAGR, driven by wider recognition of femoroacetabular impingement and rising demand for labral preservation techniques.

How are outpatient surgery centers influencing purchasing decisions for arthroscopy equipment?

Ambulatory surgical centers favor single-use instruments, integrated 4K towers, and pre-sterile implant sets that speed turnover time and support same-day discharge, enabling vendors with workflow-optimized portfolios to win tenders.

Why does Germany account for the largest share of device sales in this field?

Germany combines a large aging population, strong sports participation, and progressive reimbursement codes that encourage outpatient arthroscopy, together claiming 33.85% of regional revenues in 2025.

Which technology upgrades are most likely to replace legacy arthroscopes?

AI-assisted 4K/8K visualization systems are gaining traction because they enhance diagnostic accuracy, shorten operative time, and integrate automated documentation features for over-burdened surgical teams.

How does the shortage of trained arthroscopists affect device adoption across Europe?

Limited availability of fellowship-trained surgeons slows uptake of complex repair tools and premium implants, especially in Eastern Europe, even though patient demand and technology readiness remain high.

Page last updated on: