AI In Endoscopy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

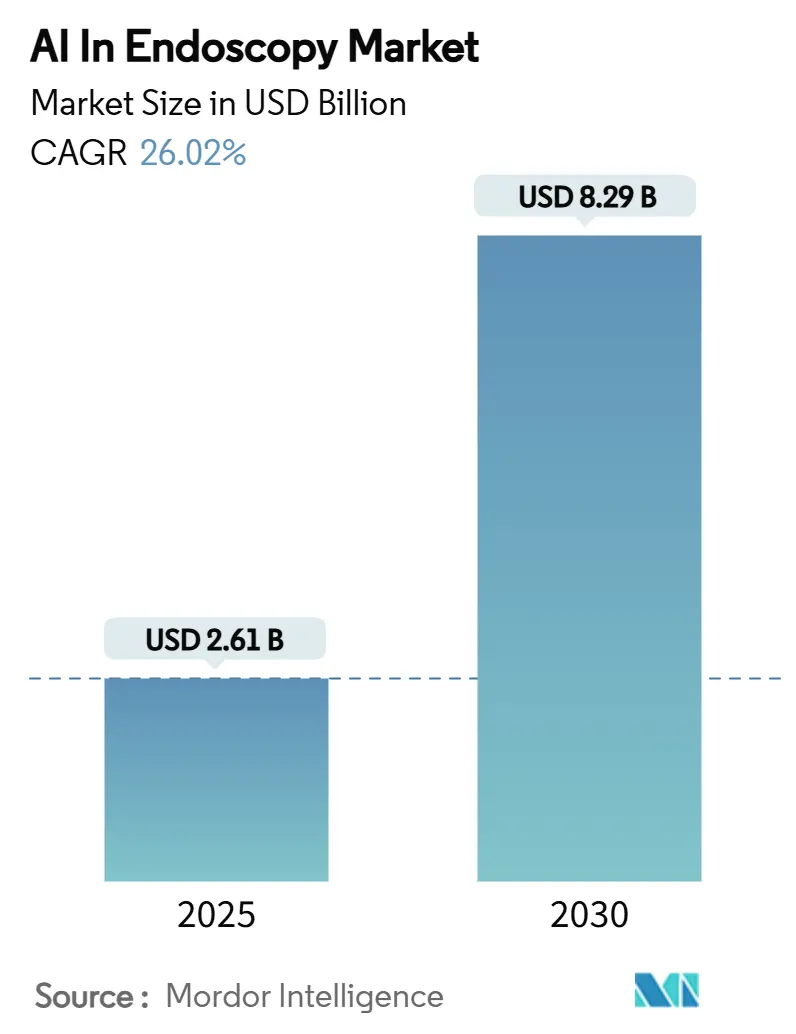

| Market Size (2025) | USD 2.61 Billion |

| Market Size (2030) | USD 8.29 Billion |

| Growth Rate (2025 - 2030) | 26.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

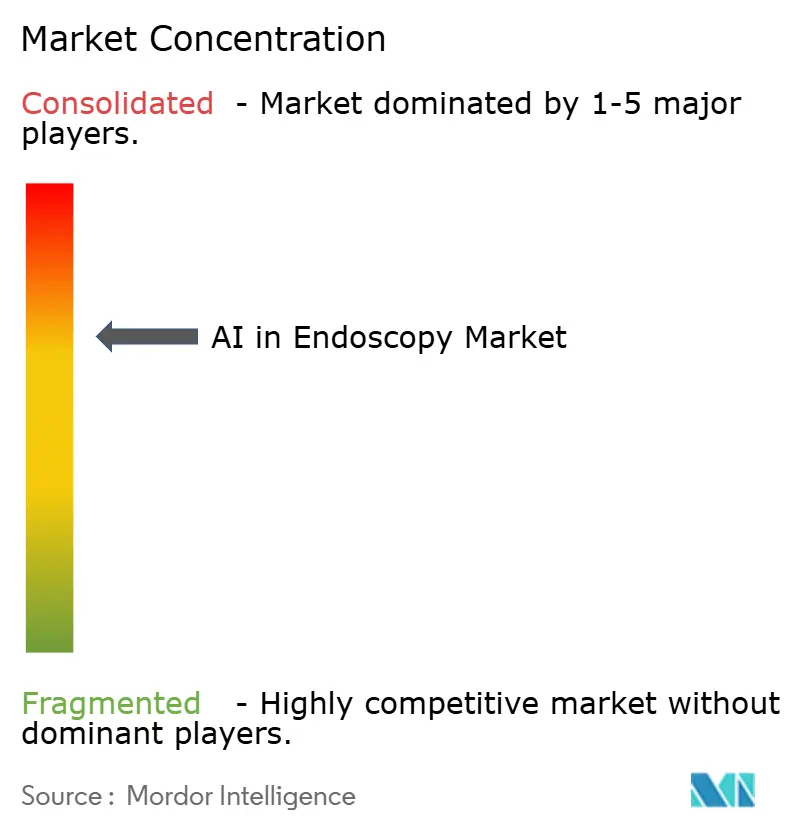

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Endoscopy Market Analysis by Mordor Intelligence

The AI in endoscopy market size stood at USD 2.61 billion in 2025 and is projected to climb to USD 8.29 billion by 2030, registering a 26.02% CAGR. Regulatory clarity from 21 CFR 876.1520 has shortened approval cycles, allowing computer-aided detection (CADe) systems to shift from pilot studies to routine clinical infrastructure.[1]U.S. Government, “21 CFR 876.1520 – Gastrointestinal Lesion Software Detection System,” ecfr.gov Mandatory adenoma detection rate (ADR) benchmarks, rising colorectal cancer incidence, and cloud delivery models continue to position AI as an indispensable productivity lever for hospitals and ambulatory centers. Hardware upgrades remain important, yet software dominance signals that algorithm performance, ease of integration, and pay-per-use contracts drive most purchase decisions. Intense competition between established endoscope makers and specialist AI vendors is compressing prices, spurring rapid product refreshes, and amplifying end-user bargaining power.

Key Report Takeaways

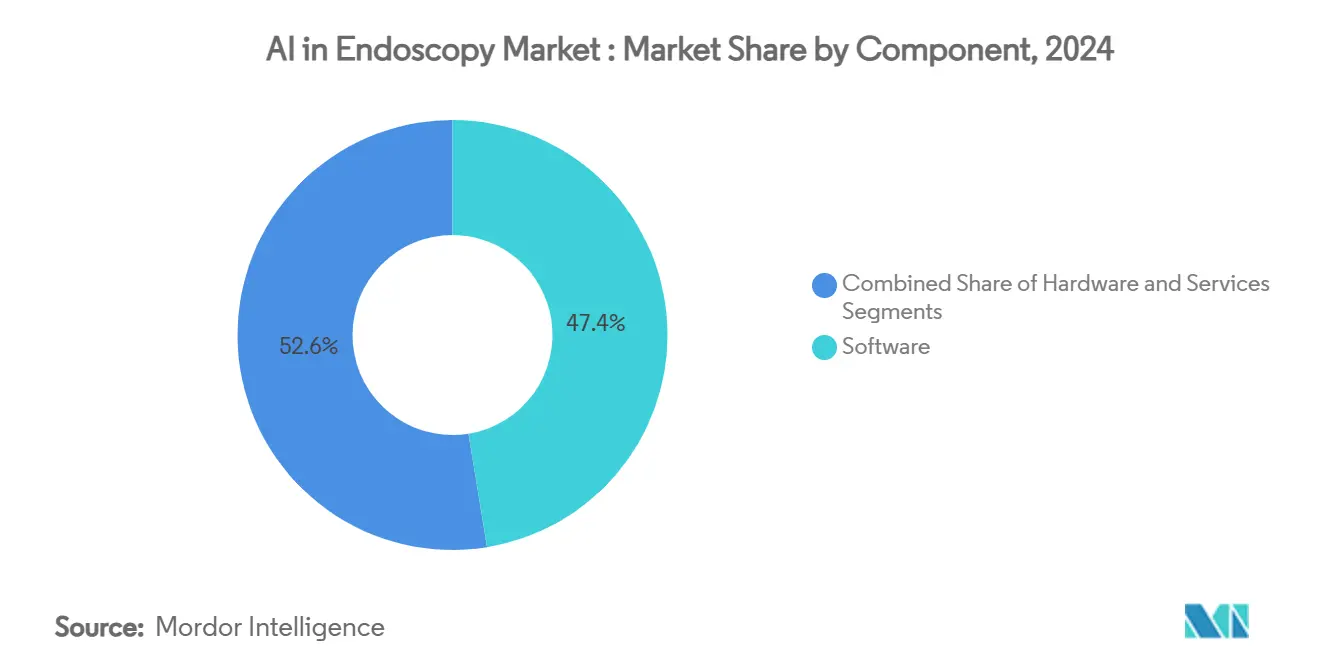

- By component, software held 47.43% of the AI in endoscopy market share in 2024; services are set to expand at a 29.35% CAGR through 2030.

- By algorithm type, deep learning captured 61.25% of the AI in endoscopy market size in 2024 and is poised for a 30.13% CAGR to 2030.

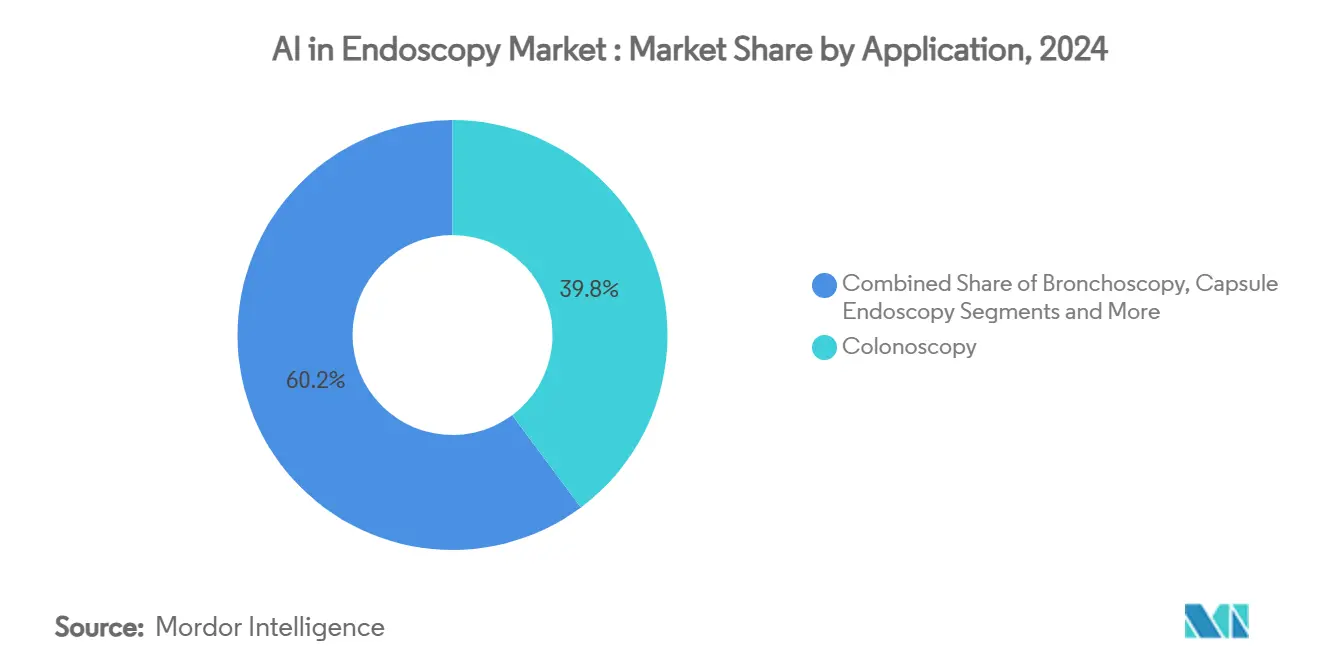

- By application, colonoscopy delivered 39.81% revenue in 2024, while bronchoscopy is advancing at a 28.24% CAGR to 2030.

- By end-user, hospitals controlled 64.51% of the AI in endoscopy market share in 2024; ambulatory surgical centers will grow at a 28.63% CAGR through 2030.

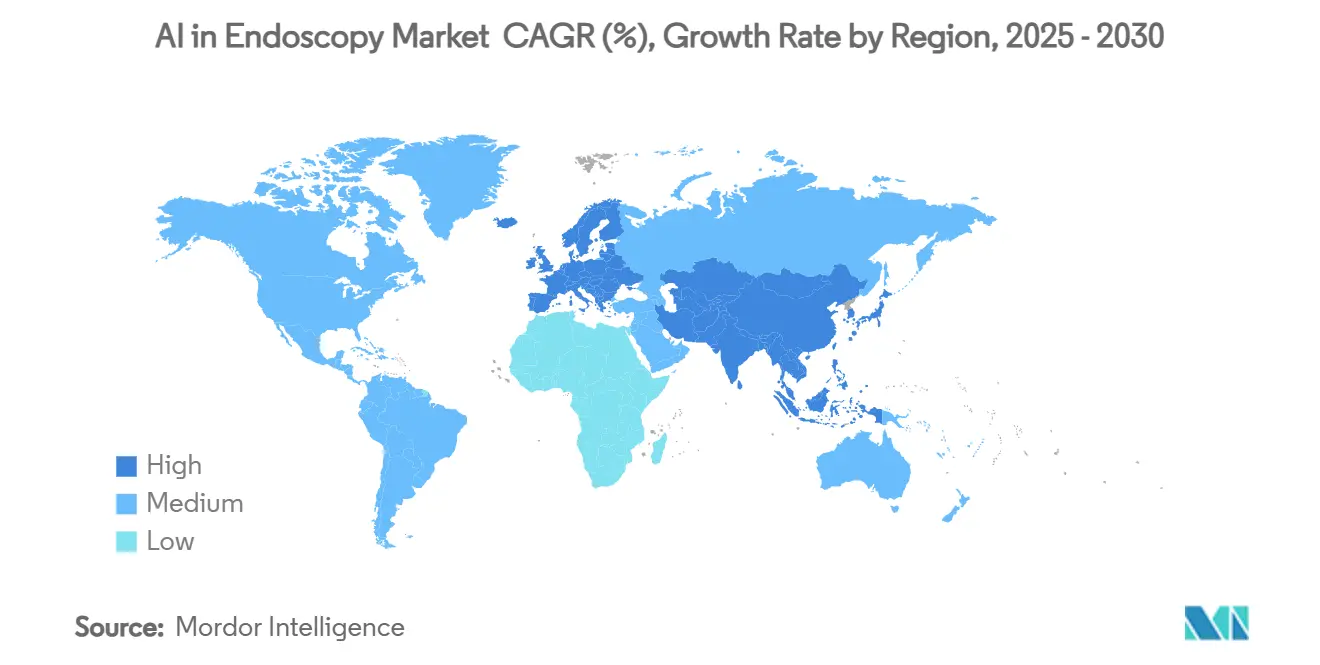

- By geography, North America generated 37.28% of 2024 revenue; Asia-Pacific is forecast to post a 29.06% CAGR to 2030.

Global AI In Endoscopy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA Approvals & Reimbursement For AI-Assisted Polyp Detection | + 4.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Mandatory ADR Quality Metrics Driving Adoption | + 3.8% | Global, with strongest enforcement in North America | Short term (≤ 2 years) |

| High-Speed Imaging Integrated With Edge AI Processors | + 3.1% | Global, led by technology-advanced markets | Medium term (2-4 years) |

| Incremental-Cost AI Add-Ons For Installed Endoscopy Stacks | + 2.9% | Global, particularly cost-sensitive markets | Short term (≤ 2 years) |

| APAC Government Digital-Health Subsidies For AI Endoscopy | + 2.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| SaaS Pay-Per-Use Analytics Models Boosting SME Uptake | + 2.4% | Global, strongest in fragmented healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FDA Approvals & Reimbursement For AI-Assisted Polyp Detection

Expedited FDA clearances for systems such as Olympus CADDIE and Fujifilm CAD EYE have reduced commercial launch times from years to months, creating a template other regulators now follow.[2]Olympus Corporation, “First Cloud-Based AI Endoscopy System for Colonoscopy Receives FDA Clearance,” olympus-global.com Parallel reimbursement moves—Japan added a CADe billing code in 2024—remove economic uncertainty and frame AI as quality infrastructure rather than optional add-on.[3]Misawa M., Kudo S., Mori Y., “Implementation of Artificial Intelligence in Colonoscopy Practice in Japan,” jmaj.jp Hospital buyers view these endorsements as risk mitigation that speeds budget sign-off while satisfying value-based payment contracts.

Mandatory ADR Quality Metrics Driving Adoption

Quality mandates elevate AI from competitive edge to operational must-have. Multi-center studies show ADR rising from 22.9% to 33.7% when CADe modes are engaged. Administrators see direct revenue protection because payer contracts increasingly penalize missed lesions. AI systems also narrow physician-to-physician variability, a key driver for networked health systems seeking uniform performance across sites.

High-Speed Imaging Integrated With Edge AI Processors

Platforms such as NVIDIA Holoscan cut maximum inference latency by 21–30%, enabling simultaneous polyp detection, anatomical tracking, and tissue characterization without cloud dependence. Real-time inference is critical during bronchoscopy and upper-GI procedures where milliseconds guide biopsy path selection. Edge architecture further limits outbound data traffic, lowering cyber-risk and easing compliance with stringent privacy laws.

Incremental-Cost AI Add-Ons For Installed Endoscopy Stacks

Medtronic GI Genius illustrates a plug-in model that overlays AI on existing towers, slashing acquisition cost from the high six figures to the low five figures. This modularity resonates with ambulatory centers and regional hospitals that prefer capital-light upgrades and minimal staff retraining. Vendors offering equipment-agnostic software capture wallet share without dislodging incumbents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Unclear ROI For Small Centers | -2.8% | Global, strongest impact in cost-sensitive markets | Short term (≤ 2 years) |

| Limited Annotated Datasets For Rare GI Pathologies | -2.1% | Global, particularly affecting specialized applications | Long term (≥ 4 years) |

| Cyber-Security Risks From Real-Time Video Streaming | -1.7% | Global, heightened in regulated healthcare environments | Medium term (2-4 years) |

| Multi-Jurisdiction AI Device Re-Validation Hurdles | -1.4% | Global, most complex in fragmented regulatory markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & Unclear ROI For Small Centers

Return-on-investment calculators for AI radiology promise 451% gains, yet comparable models for endoscopy remain scarce, prompting budget committees to defer purchases. Specialty clinics that rely on packaged fees struggle to monetize higher ADRs directly and increasingly seek vendor risk-sharing schemes that tie payments to quality improvements.

Cyber-Security Risks From Real-Time Video Streaming

Cloud-routed video streams expand attack surfaces and expose protected health information, with breach penalties that can eclipse equipment price. Institutions now require AES-256 video encryption, zero-trust access controls, and documented incident-response playbooks before signing multi-year software licenses. Edge inference addresses some concerns but does not eliminate vulnerability during firmware updates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Cloud Migration

Software accounted for 47.43% of 2024 revenue, underscoring provider demand for upgradeable algorithms that outlive hardware refresh cycles. Services will grow at a 29.35% CAGR as workflow redesign, data annotation, and continuous performance audits prove indispensable. Hospitals subscribe to cloud dashboards that benchmark ADR internally and against national registries, reinforcing a data-driven culture. Hardware growth remains steady because high-definition sensors and illumination must keep pace with algorithmic resolution requirements, yet margins compress as buyers prioritize total cost of ownership. The modular approach reduces downtime and allows staged rollouts that match capital budgets, a factor propelling the AI in endoscopy market across emerging economies.

Software-centric models also democratize advanced features: mid-tier hospitals can now activate capsule reading AI or Barrett’s esophagus modules via licence keys rather than forklift upgrades. This elasticity widens the AI in endoscopy market by enabling step-wise adoption that scales with procedure mix and reimbursement evolution. Vendors differentiate through continuous learning loops that incorporate de-identified footage from multiple hospitals, improving precision for underrepresented demographics.

By Algorithm Type: Deep Learning Maintains Technical Superiority

Deep learning captured 61.25% of the AI in endoscopy market share in 2024, with sensitivity above 90% for colorectal polyp detection. Convolutional neural networks excel at frame-level classification, powering real-time overlays that highlight lesions in under 33 milliseconds. Traditional machine learning retains niche roles in scheduling and workflow triage but lags in image interpretation accuracy. Natural-language-processing (NLP) engines automate report drafting, shaving documentation time and improving coding specificity. Hospitals often license a single platform that bundles CADe, NLP, and scheduling AI, simplifying procurement and cybersecurity audits. Cross-modality expansion—such as integrating fluoroscopy data during ERCP—will further cement deep learning’s share as multi-input models prove clinically superior.

Government grants aimed at rare disease datasets address blind spots where deep learning underperforms. Federated learning trials in Europe show promise, letting centers train shared models without exposing raw data, a safeguard likely to accelerate algorithm validation for pediatric and inflammatory bowel diseases. Such collaborations strengthen vendor access to diverse data, reinforcing network effects that perpetuate leadership positions.

By Application: Bronchoscopy Emerges as High-Growth Segment

Colonoscopy remained the workhorse, generating 39.81% of revenue in 2024; yet bronchoscopy is on track for a 28.24% CAGR as robotic platforms achieve >90% diagnostic yield for peripheral nodules. Integration of electromagnetic navigation, shape-sensing catheters, and AI route mapping reduces complication rates and shortens learning curves. Upper-GI modules targeting early gastric cancer use hyperspectral imaging with AI segmentation to flag sub-millimeter abnormalities. Capsule endoscopy benefits from reading-time cuts of up to 90%, bringing the modality into mainstream reimbursement schedules and expanding reach into rural screening programs. This broadening palette of clinical use cases diversifies revenue streams and buffers the AI in endoscopy market against procedure-specific slowdowns.

Patient experience considerations further favor bronchoscopy expansion: shorter anesthesia time and same-day discharge appeal to value-based care operators. Reimbursers increasingly bundle diagnostics and intervention, rewarding platforms that can guide biopsy and confirm margins within one session, a competitive trait now highlighted in vendor marketing.

By End-User: Ambulatory Centers Drive Adoption Acceleration

Hospitals commanded 64.51% of 2024 spend, leveraging their IT depth to integrate AI feeds into electronic health records and dashboard analytics. Yet ambulatory surgical centers (ASCs) exhibit a 28.63% CAGR as payers steer low-risk procedures to outpatient settings. AI ensures ADR compliance despite rotating physician rosters, supporting the ASC business model of high throughput with limited specialist availability. Specialty clinics differentiate by advertising AI-verified diagnostics to self-pay patients, attracting volumes that justify investment. Health-system consolidation also drives uniform equipment standards: large groups negotiate system-wide licences that cover both flagship hospitals and regional satellites, extending vendor footprints.

Operational metrics illustrate ASC momentum: AI-assisted colonoscopy cuts withdrawal time variability, enabling higher room turnover without compromising quality. Edge inference boxes mounted on existing towers allow quick deployments, aligning with ASC goals of minimal OR downtime. This dynamic enlarges the AI in endoscopy market pool while spreading revenues across diverse care settings.

Geography Analysis

North America generated 37.28% of 2024 revenue, underpinned by early FDA approvals, Medicare coverage for CADe add-ons, and stringent ADR targets. U.S. health systems bundle AI in capitated contracts, making performance dashboards a standard purchase condition. Canada and Mexico benefit from cross-border regulatory harmonization that simplifies import licenses, allowing vendors to scale North American marketing outlays. Asia-Pacific is the fastest-growing region at a 29.06% CAGR through 2030, propelled by Singapore’s USD 150 million AI healthcare fund and China’s multi-billion-dollar AI stimulus that sponsors domestic algorithm developers. Taiwan’s bias-mitigation registry and Japan’s CADe reimbursement code remove deployment hurdles, compressing adoption timelines and fueling local manufacturing partnerships.

Europe advances steadily as CE-mark processes align medical-AI rules with device regulations, enabling single-submission access to 27 markets. Germany’s GI-Insight programme, funded by the Bavarian Ministry of Science, demonstrates public-private collaboration that refines training datasets for under-served populations. Privacy-first cultures favor edge-based systems, driving demand for inference hardware that never exports raw video beyond facility firewalls. Middle East and Africa adopt incrementally, often through donation-backed projects that deploy cloud software atop refurbished towers. Latin America experiences sporadic uptake, with private insurers in Brazil and Chile piloting AI reimbursement as they transition to value-based models.

Regional policy gaps remain: the European AI Act will require real-world performance monitoring, creating a post-market workload that smaller vendors may struggle to fund, potentially reshaping market entrant profiles. Conversely, APAC subsidy programmes cushion early-stage risk, encouraging domestic startups that intensify competition for multinationals.

Competitive Landscape

The AI in endoscopy market features moderate concentration. Olympus, Fujifilm, and Medtronic together hold a sizeable installed base that anchors recurring software revenue. Olympus moved to acquire Odin Vision in 2025, signalling commitment to build full-stack digital offerings. KARL STORZ’s tie-up with Artisight underscores the growing weight of workflow analytics that extend beyond lesion detection. Pure-play developers such as Iterative Scopes and EndoTheia focus on algorithm innovation and device-agnostic cloud tools, often positioning as partners rather than direct hardware rivals.

Strategic moves highlight ecosystem play: Medtronic pairs GI Genius with Modernizing Medicine’s EHR to auto-populate pathology fields, lowering administrative burden and reinforcing customer lock-in. Fujifilm’s launch of CAD EYE leverages its optics know-how while committing to open APIs that let third-party AI integrate seamlessly. Price pressure intensifies as vendors shift from capital sales to annual software subscriptions, offering introductory tiers to penetrate ASCs. Patent landscapes converge around edge inference chips and multimodal fusion algorithms, suggesting litigation risk as portfolios mature.

Growth white spaces persist: paediatric GI, inflammatory strictures, and rare motility disorders lack labelled data, giving agile startups room to differentiate. In parallel, large manufacturers pursue turnkey service bundles—covering training, cybersecurity audits, and reimbursement consulting—that smaller firms struggle to replicate at scale. This duality keeps innovation cycles brisk while preventing monopolistic lock-in.

AI In Endoscopy Industry Leaders

Olympus Corporation

Fujifilm Holdings Corporation

Medtronic plc

Pentax Medical (Hoya Corp.)

Karl Storz SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus received FDA clearance for the EZ1500 extended-depth-of-field endoscopes, which integrate TXI, RDI, and NBI imaging modes to sharpen lesion visibility.

- January 2025: The ASGE AI Task Force issued consensus statements outlining practical AI integration steps for gastroenterology practice.

- October 2024: Olympus Europa secured CE approval for three cloud-based devices—CADDIE, CADU, and SMARTIBD—and confirmed a 2025 ecosystem launch.

Global AI In Endoscopy Market Report Scope

| Software |

| Hardware |

| Services |

| Traditional ML |

| Deep Learning |

| NLP & Others |

| Colonoscopy |

| Upper-GI Endoscopy |

| Bronchoscopy |

| Capsule Endoscopy |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Algorithm Type | Traditional ML | |

| Deep Learning | ||

| NLP & Others | ||

| By Application | Colonoscopy | |

| Upper-GI Endoscopy | ||

| Bronchoscopy | ||

| Capsule Endoscopy | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI in endoscopy market in 2025?

The AI in endoscopy market size is USD 2.61 billion in 2025 and is projected to reach USD 8.29 billion by 2030.

What CAGR is expected for global AI endoscopy spending?

Global spending is forecast to rise at a 26.02% CAGR from 2025 to 2030.

Which algorithm type leads adoption?

Deep learning holds 61.25% share and is growing at 30.13% CAGR due to superior real-time detection accuracy.

Why are ambulatory surgical centers adopting AI quickly?

ASCs seek higher throughput and consistent ADR compliance; AI reduces physician variability and supports outpatient volume growth at 28.63% CAGR.

Which region is expanding fastest?

Asia-Pacific is projected to post the highest regional CAGR of 29.06% between 2025 and 2030, supported by government AI subsidies and new reimbursement codes.

What drives revenue for service vendors?

Demand for workflow redesign, clinical training, and algorithm tuning underpins a 29.35% CAGR for services through 2030.

Page last updated on: