Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

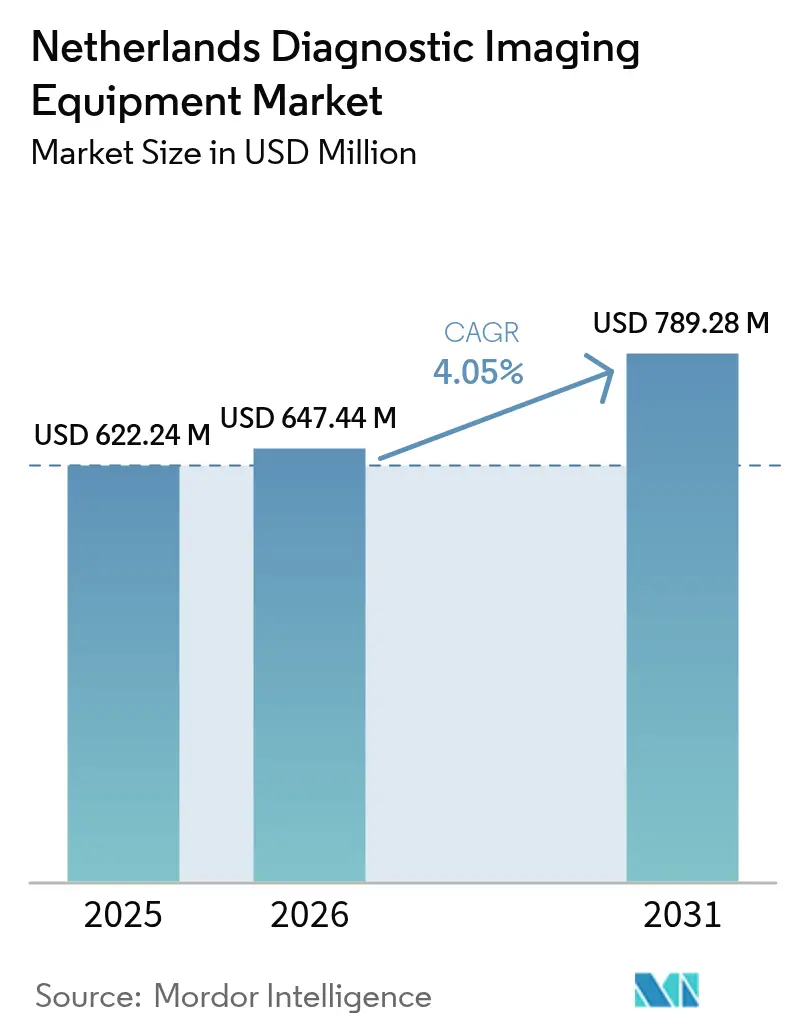

| Base Year Market Size (2025) | USD 622.24 Million |

| Market Size (2026) | USD 647.44 Million |

| Market Size (2031) | USD 789.28 Million |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

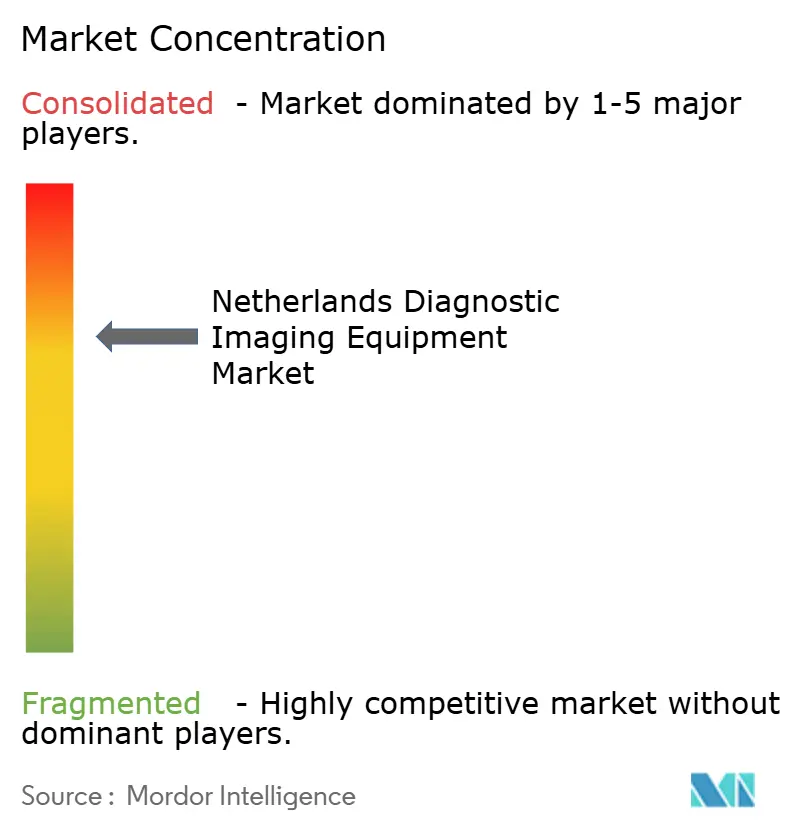

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The Netherlands Diagnostic Imaging Equipment Market size was valued at USD 622.24 million in 2025 and estimated to grow from USD 647.44 million in 2026 to reach USD 789.28 million by 2031, at a CAGR of 4.05% during the forecast period (2026-2031). Robust public spending—healthcare outlays rose 8.1% in 2024 to EUR 5,871 per capita—gives hospitals and specialist centers scope to refresh ageing fleets and pilot AI-ready platforms.[1]Source: Centraal Bureau voor de Statistiek, “Uitgaven gezondheidszorg stegen in 2024 met 8,1 procent,” cbs.nl A EUR 1.7 billion Digital Europe allocation for AI, data and cloud (2025-2027) is already funnelling grants to university medical centers, accelerating early adoption of photon-counting CT, helium-free MRI and autonomous X-ray suites.[2]Source: Rijksoverheid, “Nederland trekt financiering voor AI, data, cloud en cybersecurity innovatie aan,” rijksoverheid.nl High utilisation rates underscore entrenched demand from oncology screening, cardiac follow-up and precision-medicine protocols. Meanwhile, workforce shortages and stricter sustainability rules spur interest in portable, low-dose and energy-efficient systems, giving vendors that bundle AI workflow tools and helium-saving designs a competitive edge.

Key Report Takeaways

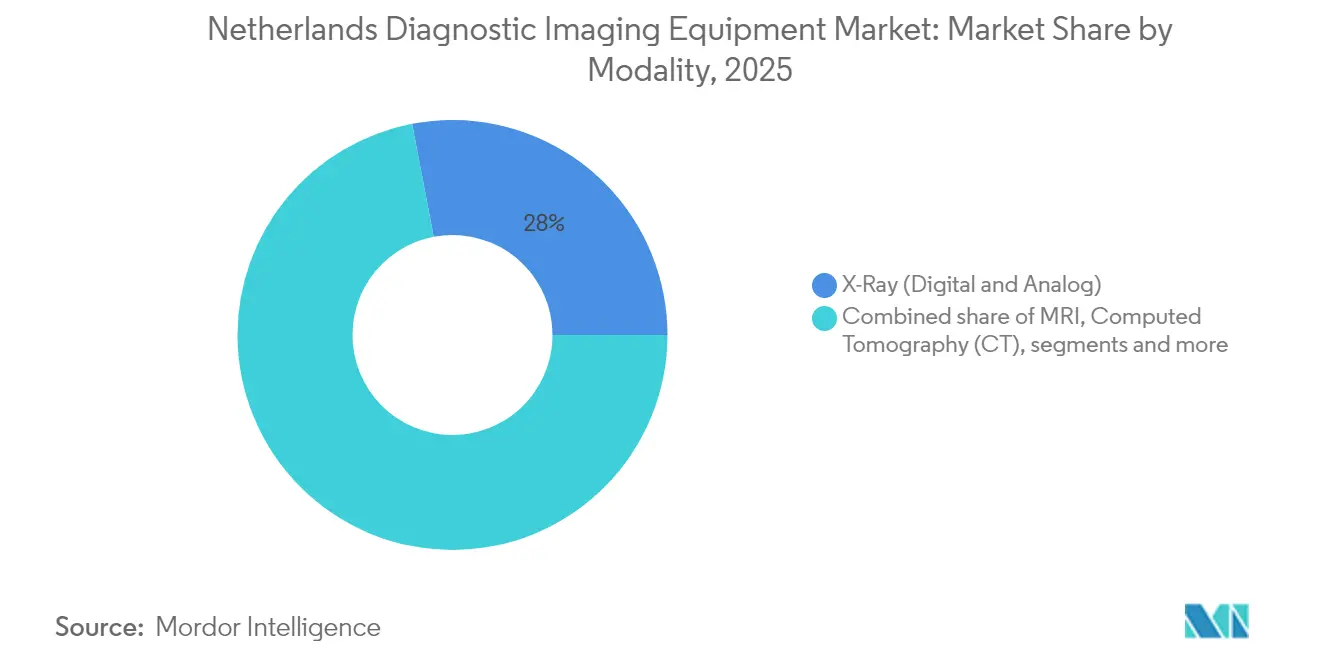

- By modality, X-ray equipment led with 28.01% revenue share in 2025, while MRI is projected to expand at a 5.95% CAGR to 2031.

- By portability, fixed systems accounted for 81.15% of the Netherlands diagnostic imaging equipment market share in 2025; mobile and handheld systems record the fastest 5.62% CAGR through 2031.

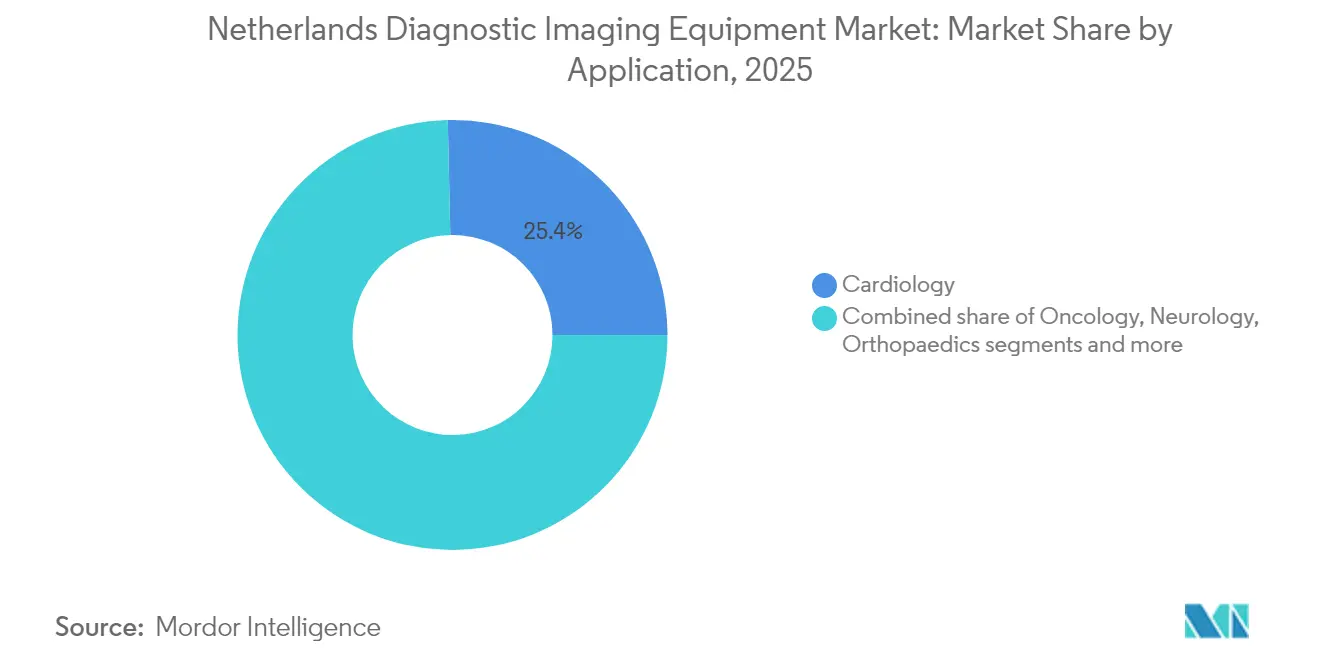

- By application, cardiology captured 25.35% of the Netherlands diagnostic imaging equipment market size in 2025 and oncology imaging is set to grow at a 5.73% CAGR to 2031.

- By end-user, hospitals commanded 69.45% share in 2025, whereas diagnostic imaging centers post the quickest 5.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Rise in prevalence of chronic diseases | +1.2% | National, with concentration in urban centers | Long term (≥ 4 years) |

| Technological advancement in imaging modalities | +0.9% | National, with early adoption in academic medical centers | Medium term (2-4 years) |

| Rapidly ageing population demanding early diagnosis | +0.8% | National, with higher impact in rural areas | Long term (≥ 4 years) |

| Shift toward low-dose protocols & radiation-free modalities | +0.6% | National, with regulatory compliance focus | Medium term (2-4 years) |

| Dutch government's AI-for-Health stimulus grants | +0.5% | National, with priority for university medical centers | Short term (≤ 2 years) |

| Expansion of national cancer-screening programs | +0.4% | National, with systematic rollout across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Prevalence of Chronic Diseases

Cardiovascular and oncologic illnesses jointly cause 51% of deaths, and the Netherlands performs 49.9 MRI plus 70.7 CT scans per 1,000 residents yearly, surpassing most EU peers. Outpatient pharmaceutical spending jumped 7% in 2024, mirroring a pivot to targeted drugs that require frequent imaging to monitor efficacy. Precision-medicine regimens make advanced modalities indispensable for tracking lesion response and drug toxicity. An ageing demographic magnifies repeat-scan volumes as chronic conditions progress. Policy shifts toward early detection channel a sizeable share of the EUR 109.4 billion health budget into imaging capacity upgrades.

Technological Advancement in Imaging Modalities

Thirty-six percent of Dutch radiology chiefs have operational AI tools and another 35% will deploy them by 2028. Photon-counting CT halves radiation while enhancing contrast, matching the patient-safety ethos embedded in national guidelines. Helium-free MRI such as the Magnetom Flow uses under 1% of legacy cryogen volumes, trimming running costs and aligning with green procurement targets. Deep-learning reconstruction cuts CT dose by 91.2% for lung-nodule programmes, and GE HealthCare’s tie-up with NVIDIA is pushing autonomous X-ray and ultrasound units onto Dutch trial sites. Together, these advances raise throughput, counteract radiologist shortages and improve diagnostic confidence.

Rapidly Ageing Population Demanding Early Diagnosis

Women aged 50-75 receive biennial breast exams that uncover about 14,000 invasive cancers each year. Contrast-enhanced mammography and dedicated breast CT are gaining favour as cost-sensitive alternatives to MRI. Forecast models show imaging demand climbing 27% over three decades, while radiologist head-count lags. Multi-morbid seniors increasingly need multimodal imaging—cardiac CT, spinal MRI and dual-energy X-ray—in single visits, driving hospitals to integrate cross-platform worklists and shared AI analytics. Portable scanners backed by teleradiology broaden access in regions with fewer specialists, keeping wait times manageable.

Shift Toward Low-Dose Protocols & Radiation-Free Modalities

AI-driven optimisation trims CT exposure by up to 80% and has become a marketable feature for procurement teams. RIVM monitoring intensifies provider accountability, prompting widespread adoption of iterative reconstruction and long-axial PET/CT systems that push fetal dose below 0.5 mGy. Emerging 0.5 T MRI units now substitute for CT in sinus studies, offering radiation-free pathways. Vendors able to supply complete dose-management dashboards—alerts, audit trails and predictive maintenance—win tender points as hospitals aim to satisfy both patient-safety and environmental metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expensive procedures & equipment | -0.7% | National, with higher impact on smaller hospitals | Long term (≥ 4 years) |

| Side-effects of certain contrast agents & radiation | -0.4% | National, with regulatory oversight focus | Medium term (2-4 years) |

| Lengthy device certification under EU MDR 2027 | -0.3% | EU-wide, with Netherlands compliance focus | Short term (≤ 2 years) |

| Radiologist workforce shortages limit throughput | -0.5% | National, with acute impact in rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expensive Procedures & Equipment

Hospital capital budgets continue to tighten even as overall health expenditure grows, forcing boards to stretch replacement cycles. Monthly insurance premiums hit EUR 156 in 2025, sparking public scrutiny of big-ticket MRI or PET investments. Consequently, facilities increasingly favour pay-per-scan leases and multi-vendor service contracts. Philips’ renewed deal with Isala Hospital showcases a shift toward outcome-based pricing tied to uptime and dose metrics.[3]Source: Royal Philips, “Philips and Dutch Isala Hospital renew long-term partnership focused on innovation and affordable, sustainable healthcare,” philips.com Rental and managed-service models now cover USD 545 million of European imaging, rising 7% annually, underscoring a broader move from capital to operational spend.

Radiologist Workforce Shortages Limit Throughput

Forecasts indicate a mismatch between a 27% jump in scan volumes and radiologist supply through 2055. Rural hospitals contend with vacancies that delay reporting and strain screening programmes; breast-cancer outreach already reports scheduling backlogs. AI decision-support claims a potential 451% ROI over five years, yet deployment requires upfront training and workflow redesign that can slow productivity short-term. Teleradiology mitigates gaps, but cross-border credentialing within the EU remains complex, limiting rapid scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: MRI Momentum Builds Inside an X-Ray-Led Portfolio

X-ray systems captured 28.01% of the Netherlands diagnostic imaging equipment market size in 2025, cementing their role for trauma and bedside exams. MRI, however, is advancing at a 5.95% CAGR, buoyed by helium-free magnets, silent sequences and AI-assisted motion correction that shorten table times. Photon-counting CT gains share for oncology staging and paediatric cases, delivering ultra-low-dose clarity prized by regulators committed to patient safety. Ultrasound adoption widens with handheld probes that sync to cloud PACS, enabling immediate consults. Nuclear-medicine platforms retain a foothold in theranostic oncology, while AI-guided mammography raises breast-screening sensitivity. Together, these shifts diversify revenue streams yet keep X-ray at the core of high-volume workflows.

Sustainability pressures steer hospitals toward energy-efficient hardware, making Siemens’ Magnetom Flow—using just 7 litres of helium—an attractive MRI upgrade. GE HealthCare’s manganese-based contrast agent pipeline addresses environmental concerns over gadolinium, potentially opening new MRI indications. Vendors embedding deep-learning reconstruction across CT, MRI and PET benefit from dose cuts and faster scans, enabling throughput gains critical amid staffing constraints. As such, modality mix decisions weigh image quality, sustainability compliance and AI readiness alongside cost.

By Portability: Mobile Systems Surge While Fixed Suites Retain Primacy

Fixed installations held 81.15% of the Netherlands diagnostic imaging equipment market share in 2025, reflecting hospitals’ need for high-spec scanners that integrate with surgical and intensive-care workflows. Mobile and handheld units, though smaller in absolute revenue, expand at 5.62% CAGR as point-of-care protocols become mainstream. The pandemic normalised bedside ultrasound and corridor CT, prompting procurement teams to allocate budget for portable complements rather than replacements. Ambulatory surgery centres now deploy mobile C-arms to sidestep limited booking slots in central radiology.

Evolving reimbursement models that reward same-day discharge further fuel demand for nimble imaging. Philips’ Zenition 90 C-arm exemplifies premium features in a roll-in format that supports orthopaedic and vascular interventions. Start-ups like Chipiron target community sites with low-field portable MRI that shares images via cloud PACS, trimming travel for elderly patients. Combined with AI-powered auto-positioning and dose alerts, mobile systems promise productivity boosts that justify higher per-scan fees.

By Application: Oncology Ascends Against Cardiology’s Established Base

Cardiology commanded 25.35% of the Netherlands diagnostic imaging equipment market in 2025 thanks to mature reimbursement for echocardiography, coronary CT angiography and stress MRI. Yet oncology exhibits the swiftest 5.73% CAGR as precision therapies demand tight imaging follow-up. Multi-cancer screening pilots, boosted by national breast and colorectal programmes, bolster CT, MRI and PET volumes. Radiomics tools now extract prognostic markers from routine mammograms, edging imaging into decision-support territory once reserved for lab tests. Neurology leverages head-only 3.0 T MRI to study dementia and stroke, while orthopaedics benefits from AI-based fracture detection that trims reading time. Obstetrics increasingly uses low-dose CT alternatives such as 0.5 T MRI for sinus assessment during pregnancy. Across applications, vendors that bundle modality-specific AI algorithms with cloud analytics position themselves to capture incremental scan demand as disease-management pathways evolve.

By End-User: Specialist Centers Erode Hospital Lead

Hospitals retained 69.45% control of the Netherlands diagnostic imaging equipment market in 2025, underpinned by emergency care and comprehensive service mandates. Diagnostic imaging centers, however, post a brisk 5.48% CAGR, capitalising on price transparency, short wait times and extended hours. Value-based healthcare contracts steer insurers to funnel elective scans to high-efficiency out-of-hospital sites that achieve same-week appointments.

Hospitals retained 69.45% control of the Netherlands diagnostic imaging equipment market in 2025, underpinned by emergency care and comprehensive service mandates. Diagnostic imaging centers, however, post a brisk 5.48% CAGR, capitalising on price transparency, short wait times and extended hours. Value-based healthcare contracts steer insurers to funnel elective scans to high-efficiency out-of-hospital sites that achieve same-week appointments.

Geography Analysis

The Netherlands ranks among Europe’s most image-intensive health systems. High per-capita spending (EUR 5,871 in 2024) ensures funding for next-generation scanners, while a EUR 1.7 billion Digital Europe envelope earmarked for AI cements policy backing. University medical centers in Amsterdam, Groningen and Utrecht serve as test beds where vendors pilot photon-counting CT, autonomous ultrasound and zero-helium MRI before country-wide rollout. Philips’ long-standing partnership with Zwolle’s Isala Hospital illustrates how public-private co-development accelerates nationwide adoption.

Rural provinces rely on mobile imaging trucks and portable ultrasound to mitigate radiologist shortages. Teleradiology networks link these outposts to specialists in academic hubs, aided by the Health-RI initiative’s FAIR data blueprint that harmonises image formats and reporting templates. National cancer-screening programmes reach 70.6% participation in colorectal and cover all eligible women for biennial breast exams, distributing imaging workload evenly across the country. The new National Health Information System strategy targets a unified cloud repository by 2035, paving the way for AI models trained on diversified datasets.

Cross-border collaboration through the European Health Data Space grants Dutch centres access to large image repositories, expediting algorithm validation for rare diseases. Local suppliers such as Tromp Medical, recently backed by Gilde Healthcare, leverage regional service teams to maintain uptime across peripheral hospitals, reinforcing decentralised care delivery. Together, cohesive policy, mature infrastructure and innovation clusters sustain the Netherlands diagnostic imaging equipment market as a launchpad for European-wide product introductions.

Competitive Landscape

Global majors—Philips, Siemens Healthineers and GE HealthCare—dominate tender lists through broad modality portfolios and established service footprints. Philips pairs hardware with enterprise cloud informatics, evidenced by its CE-marked SmartCT suite that automates neurovascular reconstructions. Siemens’ helium-saving Magnetom Flow speaks to sustainability clauses-in tenders, while GE HealthCare’s NVIDIA partnership positions it at the forefront of autonomous imaging. Compliance with EU Medical Device Regulation, whose deadlines for high-risk devices stretch to December 2027, favours these multinationals capable of sustaining lengthy certification.

Mid-tier challengers—Canon, FUJIFILM, Esaote and Samsung—differentiate via niche innovations such as hybrid CT-fluoroscopy or AI-enhanced handheld ultrasound. Distributors Tromp Medical, PI Medical and Delft Imaging Systems maintain market access by bundling multi-brand equipment with rapid on-site support, a critical criterion for small hospitals outside the Randstad. Chipiron’s USD 17 million raise for portable MRI underscores emergent competition that targets price-sensitive outpatient settings.

Vendor strategy increasingly hinges on demonstrating concrete ROI. Sustainability metrics—energy draw, helium use, and recyclability—enter scoring matrices alongside image quality. As a result, incumbents race to embed low-dose protocols, circular-economy design and predictive maintenance, while start-ups exploit niche use-cases overlooked by giants. The net effect is a moderately consolidated market with rapid technology turnover and high service expectations.

Netherlands Diagnostic Imaging Equipment Industry Leaders

FUJIFILM Holdings Corporation

Koninklijke Philips N.V.

Canon Medical Systems Corporation

GE HealthCare

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Dutch National Growth Fund awarded EUR 101.7 million to the Polaris RF consortium—including Philips—to bolster domestic MRI-grade RF component manufacturing.

- October 2023: Royal Philips, a health technology company based in the Netherlands, introduced its Philips CT 3500. This state-of-the-art CT system is designed to address the demands of routine radiology and high-volume screening programs. By leveraging AI-powered workflow enhancements and advanced image reconstruction capabilities, the Philips CT 3500 ensures increased productivity and first-time-right imaging, thereby improving the speed and accuracy of diagnoses.

- August 2023: GE HealthCare launched the Vscan Air SL handheld ultrasound device at the European Society of Cardiology (ESC) Congress in Amsterdam, Netherlands. This FDA-cleared device features sector and linear arrays, allowing for seamless cardiac and vascular assessments at the point of care.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Netherlands diagnostic imaging equipment market as the value of new capital equipment, MRI, CT, ultrasound, digital X-ray, nuclear imaging, fluoroscopy, mammography, and C-arms installed in Dutch care settings for diagnostic uses across cardiology, oncology, neurology, orthopedics, gastro-urology, and women's health.

We exclude replacement parts, picture-archiving software, service contracts, and refurbished systems.

Segmentation Overview

- By Modality

- MRI

- Computed Tomography (CT)

- Ultrasound

- X-Ray (Digital & Analog)

- Nuclear Imaging (PET / SPECT)

- Mammography

- Fluoroscopy and C-arms

- By Portability

- Fixed Systems

- Mobile and Hand-held Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopaedics

- Obstetrics and Gynaecology

- Gastro-Urology

- Other Applications

- By End-User

- Hospitals

- Diagnostic Imaging Centres

- Ambulatory Surgery Centres

- Speciality Clinics and Others

Detailed Research Methodology and Data Validation

Primary Research

We speak with Dutch radiologists, biomedical engineers, hospital procurement leads, and local distributors, which helps validate average selling prices, replacement triggers, and modality-specific backlog times. These conversations fill information gaps and guide final assumptions that Mordor analysts embed in the model.

Desk Research

We begin by pooling device import-export codes from Eurostat Comext, yearly modality stock from OECD Health Statistics, and procedure counts issued by the Dutch Health and Youth Care Inspectorate, and then match them with reimbursement tariffs from the Dutch Healthcare Authority. Next, we review white papers from the Radiological Society of the Netherlands, clinical-trial registers, and peer-reviewed articles in European Radiology to follow technology shifts, while D&B Hoovers and Dow Jones Factiva provide vendor revenue splits that anchor price corridors. The sources named are illustrative, not exhaustive, and many additional references inform data capture, validation, and clarification.

Market-Sizing & Forecasting

Our top-down "procedure-volume anchored demand pool" multiplies national scan counts by equipment densities and calibrates results against capacity-utilization norms before being filtered through sampled shipment rolls and channel checks. Key variables include MRI and CT exams per thousand residents, typical equipment life cycles, hospital capital-budget growth, statutory tariff revisions, and AI-enabled upgrade premiums. Five-year forecasts rely on multivariate regression linking modality demand with aging-index shifts, chronic-disease incidence, and real health-expenditure growth, with scenario analysis for currency swings resolving residual gaps.

Data Validation & Update Cycle

Model outputs are compared with independent trade data and historical trends. Analysts investigate variances beyond five percent, re-contact sources, and only then sign off. Reports refresh annually, with interim updates when material events (for instance, new reimbursement codes) occur, so clients receive the latest view.

Why Mordor's Netherlands Diagnostic Imaging Equipment Baseline Commands Reliability

Published estimates often diverge because research groups choose different modality baskets, apply varied euro-to-dollar rates, or roll secondary figures straight into forecasts without field checks.

The sharpest gaps usually stem from unchecked assumptions around average selling-price drift and scan-volume growth.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 622 million (2025) | Mordor Intelligence | - |

| USD 930 million (2024) | Global Consultancy A | Includes service contracts and refurbished units; lacks primary ASP validation |

| USD 657 million (2025) | Industry Association B | Converts euros at a flat rate and relies solely on import tallies, ignoring domestic production credits |

The comparison shows that Mordor's disciplined scope, mixed-method modeling, and annual refresh deliver a balanced, transparent baseline that decision-makers can retrace to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Netherlands diagnostic imaging equipment market?

The Netherlands Diagnostic Imaging Equipment Market size is estimated at USD 647.44 million in 2026, and is expected to reach USD 789.28 million by 2031.

What compound annual growth rate (CAGR) is forecast for the Netherlands diagnostic imaging equipment market between 2026 and 2031?

The market is projected to expand at a 4.05% CAGR through 2031.

Which imaging modality held the largest share of the Netherlands diagnostic imaging equipment market in 2025?

X-ray systems led with 28.01% revenue share in 2025.

How much does the Netherlands spend per capita on healthcare, and why is this relevant for imaging equipment suppliers?

Dutch outlays reached EUR 5,871 per resident in 2024, giving hospitals and specialty centers ample budget headroom to procure next-generation scanners and AI upgrades.

Which regulatory milestone dominates vendor planning cycles?

EU Medical Device Regulation deadlines now require high-risk imaging devices to be fully certified by December 2027, prompting buyers to favor vendors with proven compliance.

Which end-user segment is growing fastest, and at what pace?

Diagnostic imaging centers are advancing at a 5.48% CAGR through 2031, outpacing hospitals as outpatient models gain favor.

Page last updated on: