Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

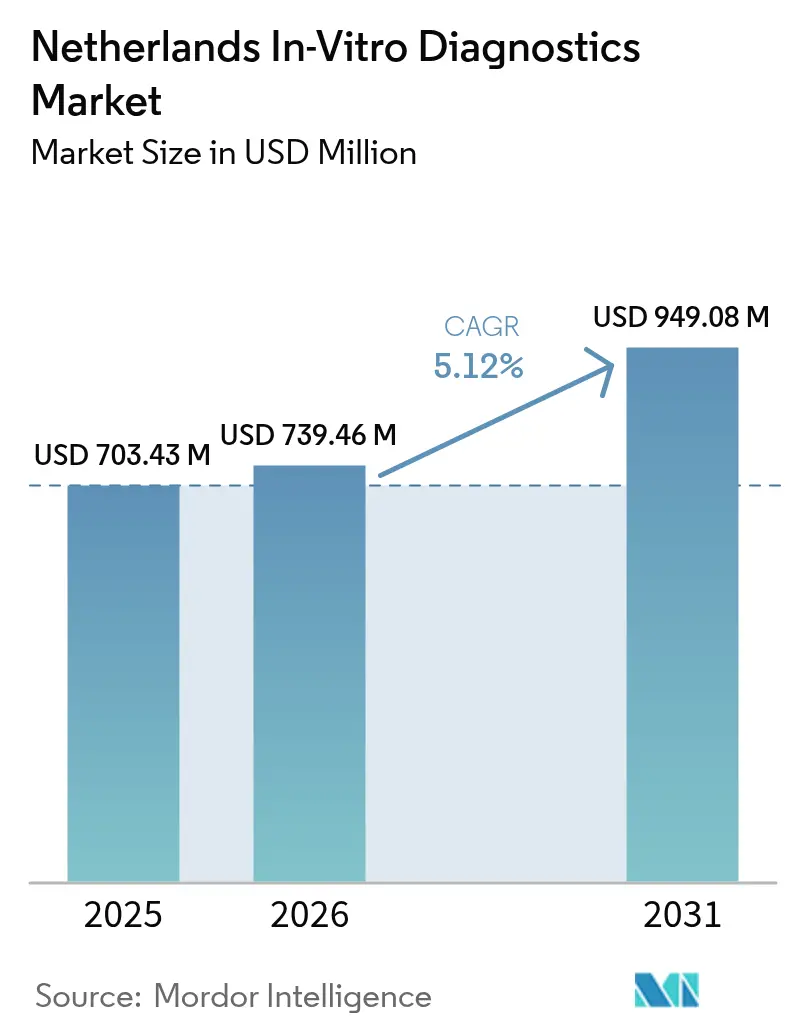

| Base Year Market Size (2025) | USD 703.43 Million |

| Market Size (2026) | USD 739.46 Million |

| Market Size (2031) | USD 949.08 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

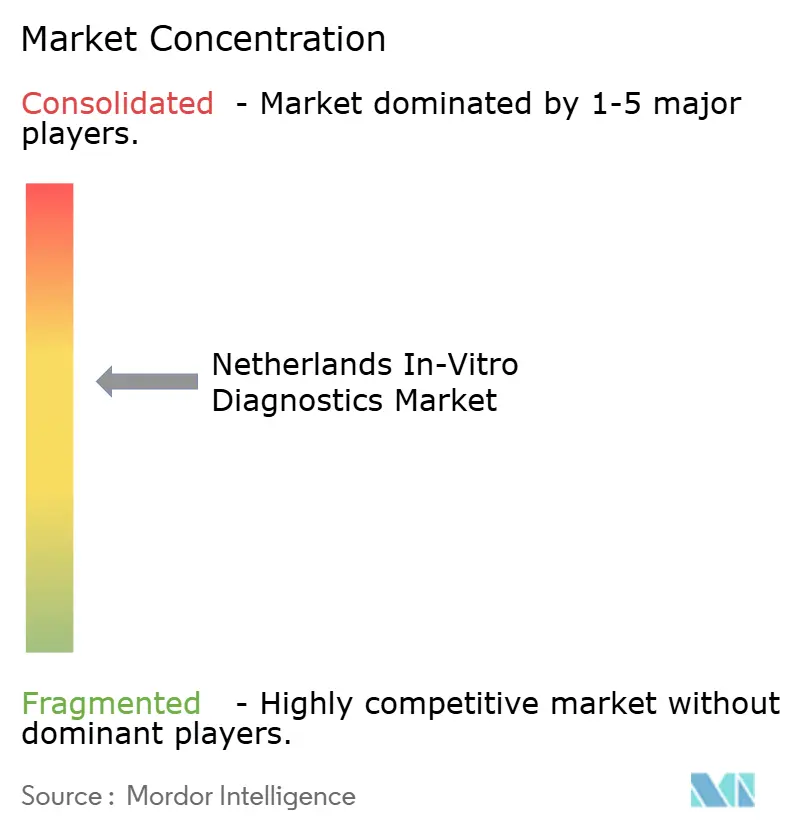

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Netherlands in-vitro diagnostics market size is expected to grow from USD 703.43 million in 2025 to USD 739.46 million in 2026 and is forecast to reach USD 949.08 million by 2031 at 5.12% CAGR over 2026-2031. Structural tailwinds include the country’s 10.7% allocation of health spending to medical goods, growing dependence on molecular assays for oncology and infectious diseases, and the strategic role the Netherlands already plays in the EUR 160 billion European med-tech arena. EU IVDR implementation is reshaping product portfolios and quality-management investments, especially for high-risk class D assays whose grace period ends May 2025. Demand is also supported by a reimbursement scheme that bundles in-hospital tests into DRGs yet pays primary-care requests fee-for-service, preserving laboratory volumes while encouraging point-of-care expansion. The Netherlands in-vitro diagnostics market continues to benefit from the Triple-Helix innovation model that tightens links among academia, industry and government.

Key Report Takeaways

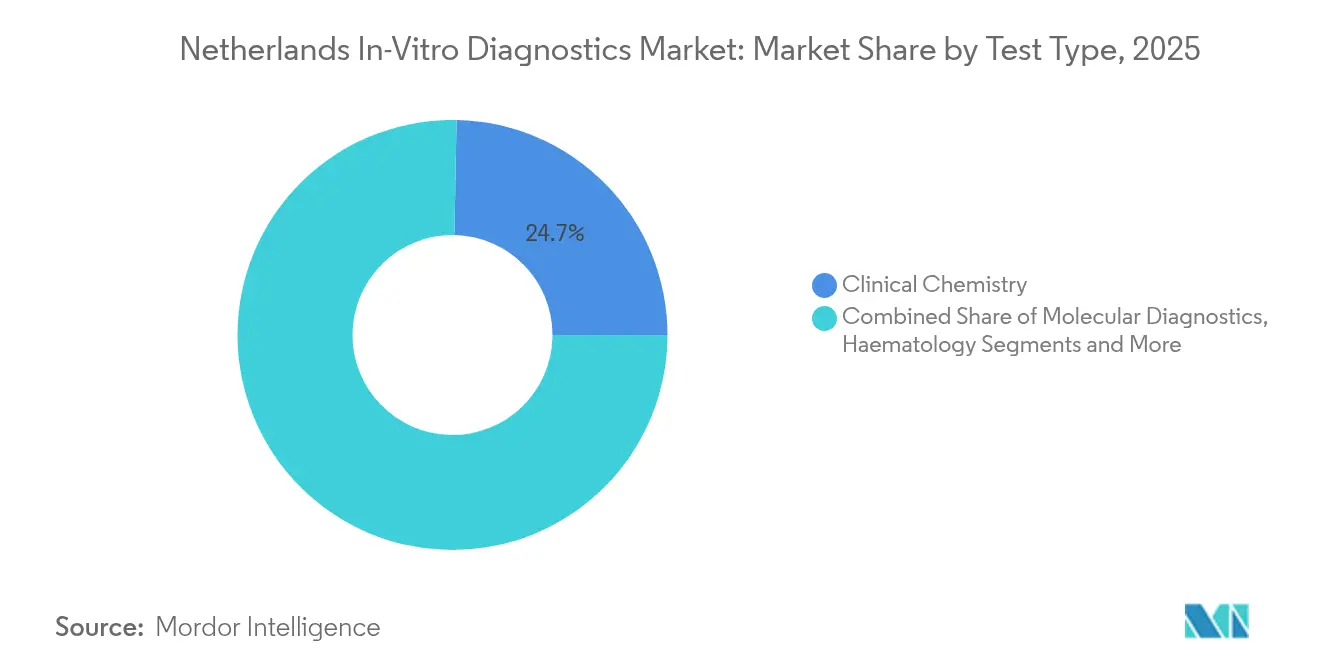

- By test type, Clinical Chemistry led with a 24.70% revenue share of the Netherlands in-vitro diagnostics market in 2025, while Molecular Diagnostics is poised for the fastest 9.22% CAGR through 2031.

- By product, reagents accounted for 70.40% of the Netherlands in-vitro diagnostics market size in 2025 and instruments are projected to post an 7.95% CAGR during 2026-2031.

- By usability, reusable systems retained 62.30% share in 2025; disposable devices are expanding at a 10.35% CAGR to 2031.

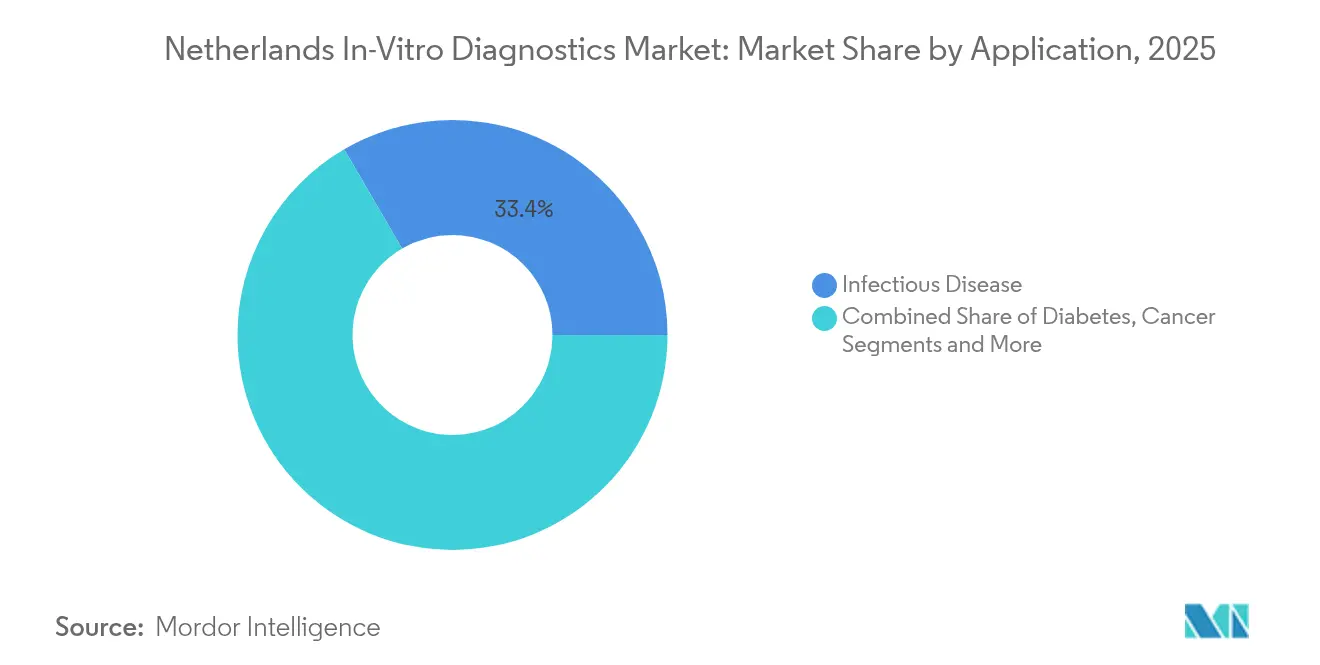

- By application, infectious-disease testing captured 33.40% of the Netherlands in-vitro diagnostics market share in 2025, whereas cancer/oncology assays will advance at an 10.92% CAGR over the forecast horizon.

- By end user, diagnostic laboratories held 51.20% share in 2025, while hospital-based testing is projected to grow 7.12% annually to 2031.

- By mode of testing, central laboratories processed 77.30% of testing volumes in 2025, yet point-of-care testing is slated to rise at a 12.05% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & lifestyle diseases in ageing population | +1.3% | National, higher in urban centers | Long term (≥ 4 years) |

| e-Health & tele-monitoring policies accelerating home-based PoC testing | +1.1% | National, early adoption in major cities | Medium term (2-4 years) |

| Reimbursement of companion diagnostics under Dutch Health Insurance Act | +0.8% | National | Short term (≤ 2 years) |

| Health-Valley clusters fueling IVD start-up commercialization | +1.0% | East Netherlands | Medium term (2-4 years) |

| Adoption of AI-enabled digital pathology | +0.6% | Academic medical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Lifestyle Diseases in Ageing

Population ageing is steadily raising the incidence of diabetes and cardiovascular illnesses, prompting healthcare providers to prioritize early diagnostic interventions. The WHO has catalogued cardiac and metabolic assays as essential technologies for managing these conditions[1]World Health Organization, “Priority Medical Devices for CVD and Diabetes,” who.int. Dutch hospitals, which receive the bulk of health-care funds, are directing larger shares to laboratory budgets so they can offer higher-throughput chemistry, immunoassay and molecular panels. Demand for personalized testing—particularly HbA1c, lipid panels and high-sensitivity troponin—is climbing as clinicians focus on risk stratification. These shifts underpin persistent reagent consumption, reinforcing the recurring-revenue structure that supports the Netherlands in-vitro diagnostics market. In parallel, pay-for-performance schemes emphasize outcomes, encouraging earlier screening as a means of reducing downstream costs, thereby sustaining long-range test-volume growth.

e-Health & Tele-Monitoring Policies Accelerating Home-Based PoC Testing

Government incentives for digital health are dismantling barriers to near-patient diagnostics. Evidence shows point-of-care panels can shave roughly 40 minutes off clinical decision time compared with central laboratory workflows. Dutch primary-care teams already turn to C-reactive protein assays to differentiate bacterial from viral infections, curbing antibiotic over-prescription. Familiarity among practitioners and proven cost-effectiveness drive rapid uptake, bolstering forecast volumes for compact readers, single-use cartridges and digital connectivity platforms. As reimbursement parity between PoC and laboratory tests is extended, manufacturers expect a broader deployment of HbA1c, UACR and rapid molecular instruments, further enlarging the Netherlands in-vitro diagnostics market.

Reimbursement of Companion Diagnostics under Dutch Health Insurance Act

The Dutch Healthcare Institute (ZIN) runs a transparent HTA pathway that generally completes within 18-30 months, enabling novel companion diagnostics to enter the basic benefit package swiftly. Oncology assays that select therapies for lung, breast and colorectal cancers have gained coverage, stimulating investment in clinical-validation studies. Predictable reimbursement has pulled multinational kit makers and local genomics start-ups toward the Dutch market. The Netherlands in-vitro diagnostics market therefore enjoys an early-adopter profile for precision-medicine tools, translating into double-digit growth in molecular reagents and digital sequencing workflows.

Health-Valley Clusters Fueling IVD Start-Up Commercialisation

East Netherlands hosts a dense innovation corridor, coupling Radboud University, University of Twente and Wageningen University with Noviotech Campus and Mercator Science Park[2]Oost NL, “Health Valley Cluster,” oostnl.com. The ecosystem supplies shared wet-lab space, clinical validation partners and grant programs, compressing time-to-market for biosensors, microfluidics and AI-software ventures. Government-industry-academia synergy—the Triple Helix—helps small firms offset IVDR compliance costs through pooled regulatory expertise. As these start-ups translate prototypes into ISO-13485-compliant products, they expand the competitive base of the Netherlands in-vitro diagnostics market and diversify technology offerings across oncology, infectious disease and chronic-care segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance costs for SMEs under EU IVDR conformity assessments | -0.8% | National, higher for small players | Short term (≤ 2 years) |

| Shortage of qualified lab technicians | -0.6% | National, acute in rural areas | Medium term (2-4 years) |

| Consolidation of hospital labs reducing supplier pricing power | -0.5% | Urban hospital networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Compliance Costs for SMEs under EU IVDR Conformity Assessments

IVDR stipulates that about 80% of assays now require notified-body review, a four-fold jump from the prior directive. With notified-body capacity still tight, Dutch SMEs face consulting, biocompatibility and QMS expenses that divert capital from R&D. Article 16(4) further obliges relabelers and distributors to secure certification, layering complexity onto supply chains. While larger multinationals absorb these costs more easily, smaller innovators risk delayed launches or portfolio pruning, constraining product diversity in the Netherlands in-vitro diagnostics market during the next two years.

Shortage of Qualified Lab Technicians

Europe’s estimated deficit of 1.2 million healthcare workers includes critical shortages in clinical chemistry and molecular labs[3]OECD, “Health at a Glance Europe 2024,” oecd.org. Dutch pathology services already rely on multi-professional teams, yet workforce planning data remain patchy, limiting strategic hiring initiatives. Vacancy gaps push overtime costs upward and can extend sample-to-result times, tempering throughput gains from automation. Laboratories therefore accelerate investment in robotics and AI, but interim staffing gaps still curb near-term expansion of the Netherlands in-vitro diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Redefines Cancer Care

In 2025 clinical chemistry generated 24.70% of Netherlands in-vitro diagnostics market revenue, anchored by routine metabolic, hepatic and renal panels. The Netherlands in-vitro diagnostics market size attributable to molecular assays is smaller but climbing at a 9.22% CAGR as oncologists adopt next-generation sequencing to guide therapy selection. Whole-genome sequencing identified actionable targets in 71% of metastatic cases at a Dutch cancer center. Tumor-agnostic companion tests plus multiplex PCR for respiratory pathogens are broadening coverage lists under ZIN, reinforcing reagent demand. Immunodiagnostics maintains relevance for allergy and autoimmune evaluations, while haematology continues to supply hospitals with CBCs and coagulation panels at stable volumes. Europe-wide underutilization of NGS—only 10% patient penetration—illustrates upside potential once reimbursement norms mature. The Netherlands in-vitro diagnostics market thus remains poised for over-performance in precision oncology, infectious-disease surveillance and inherited-mutation screening.

The competitive field is tilting toward high-multiplex systems capable of liquid-biopsy, minimal-residual-disease and antimicrobial-resistance panels. Start-ups nested in Health Valley are co-developing bioinformatics pipelines that feed hospital electronic-record platforms, streamlining clinician adoption. As IVDR high-risk deadlines approach, notified-body throughput constraints could momentarily slow product approvals, but larger entities such as Roche and Illumina retain capacity to shepherd assays through conformity assessments quickly. Consequently, molecular suppliers anticipate share gains while laboratories recalibrate capital budgets to accommodate sequencers and automated nucleic-acid extractors.

By Product: Reagents Sustain Recurring Revenue Streams

Reagents supplied 70.40% of Netherlands in-vitro diagnostics market sales in 2025, reflecting the razor-razorblade business logic where instrument installs translate into annuity consumables. Established ISO-13485 plants meet tight lot-to-lot tolerances essential for clinical accreditation. Meanwhile, instruments, although accounting for a smaller initial revenue slice, are on an 7.95% annual growth trajectory as older chemistry analyzers and immunoassay lines require replacement. Siemens Healthineers predicts a diagnostics-unit rebound in fiscal 2025 as coronavirus-testing drag recedes and core-lab automation cycles return. Integrated track systems that consolidate haematology, chemistry and serology on one belt are gaining popularity for high-volume Dutch hospitals. Software, middleware and quality-control materials emerge as value-added differentiators as IVDR stresses traceability. Sustainability mandates are beginning to drive R&D toward reduced-plastic cassettes and energy-efficient incubators, themes likely to influence procurement criteria through 2031.

At smaller medical-center labs, reagent-rental agreements lower entry barriers by bundling analyzers without upfront capital. Yet as procurement consortia expand, price transparency tightens margins, prompting suppliers to enhance technical-service contracts and digital-analytics dashboards that predict reagent inventory needs. This after-sales ecosystem reinforces customer lock-in, cementing reagent revenues in the Netherlands in-vitro diagnostics market.

By Usability: Disposable Devices Gain Momentum

Reusable analyzers and slide systems still manage 62.30% share but face growing scrutiny over infection-control and cleaning overheads. COVID-19 normalized the expectation of single-use swabs, cartridges and lateral-flow strips, catalyzing a 10.35% CAGR for disposable formats between 2026 and 2031. New European guidelines require justification when carcinogenic or endocrine-disrupting phthalates exceed 0.1% by weight, steering manufacturers toward safer polymers. Product-design teams are therefore adopting cyclo-olefin copolymers and biodegradable substrates for casings and microfluidic chips. Comparative usability studies of four CRP PoC devices demonstrated marked variations in hands-on steps, influencing adoption beyond price alone. Hospitals with robust sterilization units will sustain a baseline demand for reusable plates and pipettes, yet growth belongs to single-use cartridges and strip-based immunoassays that fit home-monitoring kits, amplifying decentralization within the Netherlands in-vitro diagnostics market.

By Application: Cancer Diagnostics Leads Growth Trajectory

Infectious-disease tests held 33.40% share of the Netherlands in-vitro diagnostics market in 2025, thanks to ongoing surveillance for respiratory, sexually transmitted and nosocomial pathogens. Molecular PoC devices are cutting diagnosis-to-therapy intervals, crucial for antimicrobial stewardship. Oncology applications, fuelled by the national cancer plan unveiled November 2023, will compound at 10.92% through 2031. Liquid-biopsy panels for ctDNA, multigene NGS panels and PD-L1 immunohistochemistry all stand to benefit from reimbursement clarity. Diabetes monitoring retains relevance, especially as primary-care centers integrate A1C and UACR PoC devices to catch chronic kidney disease early. Cardiology diagnostics leverage high-sensitivity troponin-T and NT-proBNP to triage emergency-department chest-pain cases, while nephrology markers such as NGAL gain research footing. Collectively, diversified applications anchor steady double-digit volume escalations for the Netherlands in-vitro diagnostics market.

By End User: Diagnostic Laboratories Maintain Leadership

Reference and hospital-affiliated labs processed 51.20% of IVD revenue in 2025, capitalizing on economies of scale, accreditation status and broad test menus. Automation tracks and LIS-middleware integration enable same-day reporting, incentives that sustain send-in volumes from physician offices. Hospitals and clinics themselves exhibit a 7.12% CAGR outlook as they embrace rapid-response labs, STAT chemistry islands and blood-gas PoC instruments to shorten inpatient stays. Studies confirm that PoC deployment trims discharged-patient stay by 34 minutes compared with central pathways, easing ED overcrowding. Home-care and tele-monitoring programs are fledgling but accelerating on policy pushes for self-management in chronic conditions. Academic centers double as early-adopter sites for AI pathology and NGS, channeling grant funding into cutting-edge platforms. Each cohort underpins the Netherlands in-vitro diagnostics market by amplifying test-volume elasticity and spurring tailored kit configurations.

By Mode of Testing: Point-of-Care Disrupts Traditional Models

Central labs still control 77.30% of test throughput, leveraging batch processing, dedicated phlebotomy routes and established quality-management systems. Nevertheless PoC formats—handheld readers, single-use cassettes and near-patient PCR—are growing at 12.05% annually. CRP PoC is close to universal in Dutch general practice, where clinicians report higher trust and availability than peers in the United Kingdom or Germany. Molecular PoC devices face hurdles around cold-chain logistics and lot-verification, yet their role in outbreak containment and emergency diagnosis is undisputed. As connectivity improves and EHR-integration APIs mature, decentralized analyzers will feed real-time surveillance databases, aligning with government antibiotic-reduction targets. Consequently, the Netherlands in-vitro diagnostics market accommodates a dual-track model where central and decentralized sites co-exist, each reinforced by evolving reimbursement levers.

Geography Analysis

Dutch IVD demand concentrates around densely populated Randstad provinces, where academic medical centers such as Amsterdam UMC, Erasmus MC and UMC Utrecht spearhead technology adoption. The national reimbursement framework—DRG for inpatient tests and fee-for-service for GP-ordered assays—encourages steady lab utilization across the territory. East Netherlands’ Health-Valley cluster accelerates device translation by pooling engineering talent and offering regulatory incubators. Northern regions participate in the Health Data Valley initiative, anchoring secure data-sharing infrastructures that benefit decentralized testing programs. Transport logistics across the compact geography preserve same-day courier routes, supporting the central-lab dominance in the Netherlands in-vitro diagnostics market. At the same time, high broadband penetration aids tele-monitoring, cementing a fertile ground for connected PoC roll-outs. Government co-funding of AI health projects, channelled through Health Holland, ensures uniform tech diffusion beyond urban centers, minimizing geographic disparities in diagnostic access.

Regulatory Landscape

In the Netherlands, in-vitro diagnostics are governed by the EU In Vitro Diagnostic Regulation (IVDR, Regulation (EU) 2017/746), applicable since 26 May 2022, with national implementation via the Medical Devices Act (Wet medische hulpmiddelen) and related decrees and regulations. The Health and Youth Care Inspectorate (Inspectie Gezondheidszorg en Jeugd, IGJ) is the primary supervisory authority overseeing MDR/IVDR compliance, including market surveillance, vigilance, and enforcement actions aligned to its intervention policy approach.

For market access, lifecycle compliance is increasingly decisive, particularly robust post-market surveillance and technical documentation suited to notified-body scrutiny (a step-up versus the prior directive). Economic operators are also facing tightened administrative obligations linked to EU-wide systems such as EUDAMED registration, alongside traceability expectations. For some product categories and workflows, Dutch requirements such as NOTIS registration for custom-made devices add to the overall compliance burden.

Competitive Landscape

Global majors—Roche, Abbott and Danaher Corporation—command the major share of instrument placements and reagent annuities, using multiyear contracts and middleware integration to anchor accounts. Roche’s Cobas Pro integrated chemistry-immuno lineup and Abbott’s Alinity systems slot easily into automated tracks, easing technician workloads. Siemens anticipates a rebound for its diagnostics unit in FY 2025 as routine testing normalizes post-pandemic. Bruker’s EUR 870 million acquisition of ELITechGroup (USD 957 million) in 2024 signalled intent to scale molecular capabilities and could strengthen competition within mid-size hospital niches. Becton Dickinson’s plan to spin off its diagnostics portfolio by 2026 may create a new specialized contender focused on microbiology and PoC cardiac markers.

White-space innovation stems from AI algorithms for digital pathology, smartphone-linked lateral-flow readers and blood-based multi-cancer early-detection assays. SMEs in Nijmegen and Enschede exploit Health-Valley resources yet must navigate IVDR costs that disproportionately strain limited budgets. Newly recognized notified bodies such as DNV are expected to ease certification bottlenecks, favoring first movers with complete technical files. Hospital-lab consolidation increases negotiating power, compelling vendors to bundle hardware, reagents and service with cloud-analytics dashboards that flag pre-analytical errors. The resulting competitive equilibrium keeps market concentration moderate while sustaining innovation velocity inside the Netherlands in-vitro diagnostics market.

Netherlands In-Vitro Diagnostics Industry Leaders

F. Hoffmann-La Roche AG

Abbott Laboratories

Bio-Rad Laboratories Inc.

Thermo Fisher Scientific Inc.

Danaher Corporation (Beckman Coulter, Cepheid)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace centers on helping laboratories and manufacturers manage the higher administrative and traceability load created by IVDR and the staged rollout of EUDAMED. In February 2026, a Dutch law amended the Wet medische hulpmiddelen to implement EU measures on medical-device delivery interruption notifications and the EUDAMED rollout. This change is creating demand for compliance tooling and services aimed at strengthening supply continuity, UDI readiness, and documentation completeness across manufacturers, importers, and distributors.

Decentralized testing and connected diagnostics continue to create parallel opportunities alongside the regulatory shift. Dutch e-health and tele-monitoring policies support wider use of point-of-care platforms and home-adjacent testing pathways, while the Dutch Healthcare Institute (ZIN) maintains a defined HTA route that supports companion diagnostics entering coverage lists. Vendors that combine IVDR-compliant assays with connectivity, workflow automation, and evidence packages aligned to Dutch reimbursement decision-making can sell to both central laboratories and primary-care settings, without depending only on traditional core-lab menu expansion.

Recent Industry Developments

- July 2026: Roche announced the launch of the cobas Hepatitis D Virus (HDV) test as a fully automated solution for HDV diagnostics. The update supports automated virology workflows in European laboratories and extends Roche's menu strategy under IVDR-driven portfolio prioritization.

- April 2026: Beckman Coulter Diagnostics (Danaher) received a CE 2797 mark under IVDR for the Access MeMed BV assay, designed to differentiate bacterial vs viral infections in about 20 minutes. Rapid host-response testing supports antimicrobial stewardship pathways and strengthens near-patient and emergency-department value for IVDR-compliant immunoassay platforms.

- May 2024: QIAGEN received EU IVDR certification for QIAGEN Clinical Insight Interpret, its clinical decision support software for oncology and hereditary diseases. Certification for software used in diagnostic interpretation supports wider deployment of integrated molecular workflows that combine wet-lab testing with compliant, traceable reporting.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers in vitro diagnostic (IVD) products used in the Netherlands to test human samples outside the body, where results support screening, diagnosis, and treatment monitoring in clinical settings.

Scope exclusions: We exclude therapeutic drugs, imaging systems, and general hospital services, and we also do not count routine lab labor costs that are billed as standalone services.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Molecular Diagnostics

- Immuno-Diagnostics

- Haematology

- Other Test Types

- By Product

- Instruments

- Reagents

- Other Products

- By Usability

- Disposable IVD Devices

- Reusable IVD Devices

- By Application

- Infectious Disease

- Diabetes

- Cancer / Oncology

- Cardiology

- Nephrology

- Other Applications

- By End User

- Diagnostic Laboratories

- Hospitals & Clinics

- Other End Users

- By Mode of Testing

- Central Laboratory Testing

- Point-of-Care Testing

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand base for testing in the Netherlands and then tying it to how labs and care sites procure IVD products. We mainly relied on public health and reimbursement context from sources such as the Dutch National Institute for Public Health and the Environment, the Dutch Central Bureau of Statistics, the European Commission medical device and IVDR resources, and OECD health statistics.

To keep the model grounded, we also reviewed public tender and procurement notices, peer reviewed clinical and laboratory medicine journals, and association or laboratory network publications where available. We used company annual reports, investor presentations, and reputable press to understand product mix shifts and pricing direction, and a paid subscription covering company financials and news helped validate the scale and timing of major portfolio moves. The desk research sources listed above are not exhaustive, and other public references were used to collect data, cross-check assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with IVD manufacturers and distributors, laboratory decision makers, and selected healthcare providers that influence test selection and usage patterns. Because this is a country market, discussions were focused on the Netherlands, and they were used to close gaps around product mix, point-of-care adoption, average selling price movement, and the practical split between central lab and near-patient testing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 18% | |

| Mid tier: 40% | Functional/Unit leaders: 27% | |

| Smaller Players: 22% | Managers: 55% |

Market-Sizing & Forecasting

For sizing, the main build is a top-down demand reconstruction, where published healthcare and lab activity signals are translated into an addressable testing pool and then converted into IVD spend by applying mix and pricing assumptions. In parallel, we run selective bottom-up checks, such as sampled price per test by category multiplied by estimated test volumes, and supplier and channel conversations that help adjust totals when the first pass looks off.

The model uses a small set of market fingerprints that are practical to validate, including diagnostic testing volumes by setting, the split between central laboratory and point-of-care usage, reagent to instrument spending ratios, utilization patterns linked to infectious disease and chronic disease monitoring, and expected price changes from menu expansion and automation. When data is missing for a narrow category, we handle the gap using proxy shares from similar European settings, then pressure-test it with local interviews until the resulting mix looks realistic.

Forecasts are built using scenario analysis supported by trend smoothing on the key demand drivers, and assumptions are reviewed with primary respondents so the base case reflects how procurement cycles and guideline-driven testing are expected to evolve over the next few years.

Data Validation & Update Cycle

Validation is done in layers so unusual jumps are caught early and explained before numbers are finalized. Model outputs are compared against independent signals like healthcare spending direction, diagnostic activity trends, and procurement visibility, and then followed by variance checks at category level to spot mix errors.

Before sign-off, analyst reviews challenge assumptions and recalculate results, and respondents are re-contacted when the range looks too wide or when a major input changes. Reports are refreshed annually, with interim updates triggered by material events such as regulatory shifts, reimbursement changes, or large product launches, and then a final freshness check is completed right before delivery so clients receive the most current view.

Mordor Intelligence's Vitro Diagnostics Netherlands Market Size Versus Other Published Estimates

Published numbers for the Netherlands IVD space can look far apart, even when the market name is the same, because the counting rules are not consistent. Differences usually come from what is treated as IVD spend, which year is used as the base, and how prices and test mix are carried forward.

The benchmark table shows a clear spread that is mostly explained by scope and measurement choices, and in Mordor Intelligence's model the value is anchored to IVD products used for testing and it is split by central laboratory versus point-of-care rather than folding in broader lab service revenue or adjacent medical technology spending. When other estimates assume faster menu expansion, apply different currency timing, or treat software and services as a larger bundle, the total will move quickly even if test demand is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 703.43 M (2025) | |

| Global Consultancy A | USD 3.80 B (2024) | Uses an earlier base year and appears to apply a broader IVD definition that can bundle software and related services more aggressively, which lifts the value even before forecasting assumptions are applied. |

| Industry Publisher B | USD 0.96 B (2023) | Uses a different base year and may mix in adjacent categories or apply higher average selling price assumptions across test types, and the forecast window and CAGR setup differs from a 2025 anchored view. |

Looking across the three figures, most of the gap is not about demand direction, it is about what gets counted and when. By keeping the inputs tied to observable testing settings, product mix, and practical price movement, the estimate stays traceable to a few repeatable steps that can be rechecked as new data and interview feedback comes in.

Key Questions Answered in the Report

How large is the Netherlands in-vitro diagnostics market in 2026?

The Netherlands in-vitro diagnostics market size stands at USD 739.46 million in 2026 with a projected CAGR of 5.12% through 2031.

Which test type is expanding fastest within Dutch diagnostics?

Molecular diagnostics leads growth with an expected 9.22% CAGR as oncologists and infectious-disease specialists adopt next-generation sequencing and rapid PCR assays.

What share of Dutch IVD revenues come from reagents?

Reagents contribute 70.40% of total sales, underscoring the consumable-driven revenue model that characterizes laboratory testing.

How quickly is point-of-care testing growing in the Netherlands?

Point-of-care platforms are forecast to rise at a 12.05% CAGR, fueled by e-health policies and demonstrated clinical value in primary care.

What impact does IVDR have on small Dutch IVD companies?

IVDR compliance costs reduce SME growth by an estimated 0.8 percentage points on CAGR because most assays now require notified-body review and full QMS certification.

Which region supports start-up commercialization in Dutch diagnostics?

The Health-Valley cluster in East Netherlands integrates universities, labs and incubators, accelerating IVD start-up scale-up and market entry.

Page last updated on: