Native Collagen Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 252.57 Million |

| Market Size (2030) | USD 378.22 Million |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Native Collagen Market Analysis by Mordor Intelligence

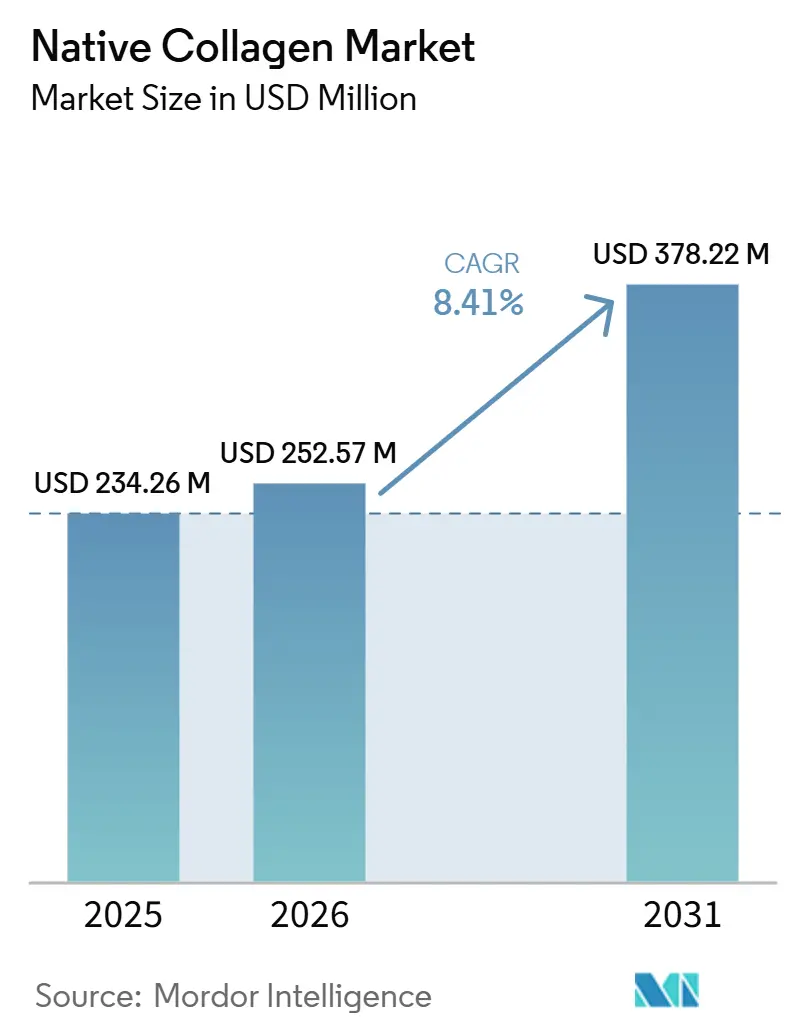

The native collagen market size is expected to grow from USD 234.26 million in 2025 to USD 252.57 million in 2026 and is forecast to reach USD 378.22 billion by 2031 at 8.41% CAGR over 2026-2031. Growth in the native collagen market is driven by its increasing use in nutraceutical, cosmetic, and pharmaceutical products, where intact triple-helix collagen supports tissue support, immune response, and dermal repair. Demand is also shifting away from hydrolyzed formats when formulators require higher structural integrity and more specific functional performance. The FDA’s 2024 GRAS acceptance of an Escherichia coli-derived recombinant collagen polypeptide widened the pathway for non-animal production and began easing a long-standing supply bottleneck. Cost pressure, biosafety scrutiny of animal-derived inputs, seasonal raw material limitations, and lower-cost peptide substitutes continue to affect adoption. However, the native collagen market still offers expansion opportunities as brands seek differentiated ingredients.

Key Report Takeaways

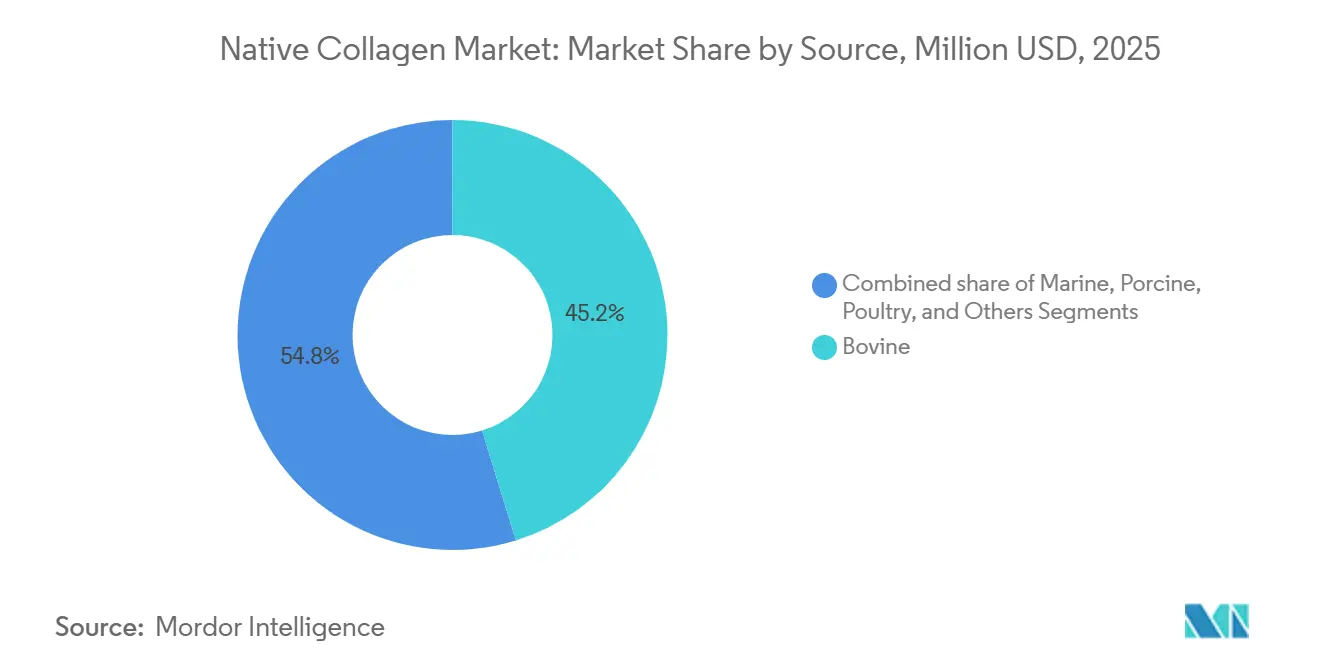

- By source, bovine collagen held 45.23% of the native collagen market share in 2025, while marine collagen is expected to expand at a 9.71% CAGR through 2031.

- By form, powdered products accounted for 51.54% of the native collagen market size in 2025; liquid formats are projected to grow fastest at a 10.78% CAGR through 2031.

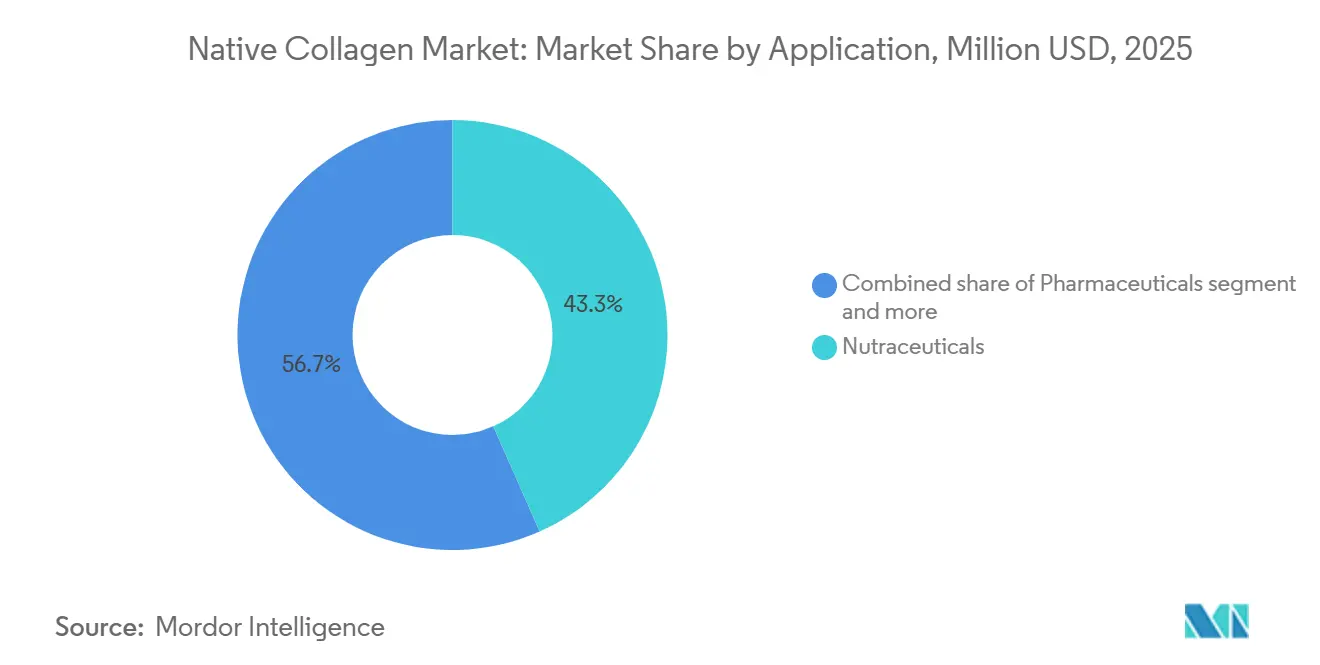

- By application, nutraceuticals generated 43.34% revenue in 2025, whereas cosmetics and personal care are advancing at a 10.21% CAGR through 2031.

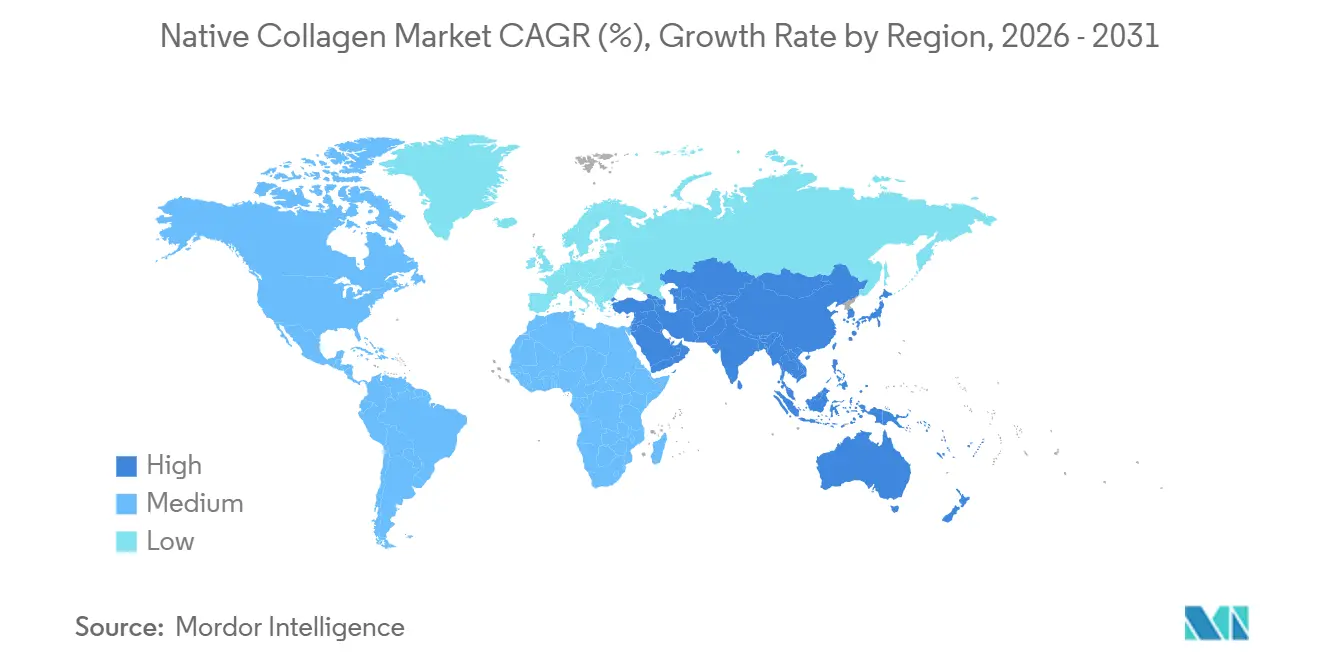

- By geography, North America commanded 34.76% revenue in 2025, while Asia-Pacific is poised for 9.89% CAGR growth through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Native Collagen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use in cosmetic and aesthetic treatments | +1.7% | Global, concentrated in North America, Europe, and Northeast Asia | Medium term (2-4 years) |

| Increasing demand for natural protein-based ingredients in nutraceuticals | +1.9% | Global, North America and Europe lead, Asia-Pacific is accelerating | Medium term (2-4 years) |

| Technological advancements in collagen extraction and purification | +1.3% | Global, Asia-Pacific leads production, North America and Europe lead research and development | Long term (≥ 4 years) |

| Expanding aging population driving demand for joint and skin health solutions | +1.2% | Global, concentrated in Asia-Pacific, Europe, and North America | Long term (≥ 4 years) |

| Rising prevalence of orthopedic and sports injury treatments | +0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Growing clinical acceptance of undenatured type II collagen for joint health | +1.1% | Global, with adoption concentrated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing use in cosmetic and aesthetic treatments

Increasing demand for cosmetic and aesthetic treatments is significantly expanding the use of native collagen in both topical and regenerative beauty applications. Native collagen is widely incorporated into premium skincare products, dermal matrices, wound-healing formulations, and aesthetic procedures due to its ability to support skin hydration, elasticity, and tissue regeneration. Growing consumer interest in anti-aging solutions and minimally invasive cosmetic treatments has encouraged manufacturers to develop advanced collagen-based products for skin rejuvenation and repair. The expanding medical aesthetics industry, coupled with rising disposable incomes and greater awareness of preventive skincare, is further strengthening product demand. In addition, advancements in biomaterials and regenerative medicine have increased the use of native collagen in facial reconstruction, tissue engineering, and post-procedure recovery applications.

Increasing demand for natural protein-based ingredients in nutraceuticals

Growing consumer focus on preventive healthcare and balanced nutrition is increasing the demand for natural protein-based ingredients in nutraceutical products. Native collagen has gained widespread acceptance due to its high biological functionality and its role in supporting joint health, bone strength, skin elasticity, muscle recovery, and overall wellness. The rising popularity of functional foods, dietary supplements, and healthy aging solutions has encouraged manufacturers to incorporate native collagen into capsules, powders, beverages, and protein-enriched formulations. Consumers are increasingly seeking clean-label, naturally sourced ingredients with scientifically supported health benefits, further strengthening market demand. In addition, expanding awareness of active lifestyles and age-related health management is driving the consumption of collagen-based nutritional products across diverse age groups.

Technological advancements in collagen extraction and purification

Continuous advancements in collagen extraction and purification technologies are enhancing the quality, functionality, and commercial value of native collagen across multiple industries. Modern extraction techniques are designed to preserve the natural triple-helix structure of collagen while improving purity, yield, and consistency, making the ingredient more suitable for nutraceutical, and cosmetic applications. Innovations in enzymatic processing, filtration, and purification methods have also reduced impurities and improved product safety without compromising biological activity. These technological improvements enable manufacturers to produce highly standardized collagen that meets stringent regulatory and quality requirements. In addition, enhanced processing efficiency helps optimize resource utilization and supports the sustainable use of animal and marine raw materials.

Expanding aging population driving demand for joint and skin health solutions

The expanding aging population is significantly increasing demand for native collagen-based products that support joint mobility, bone health, and skin wellness. According to World Bank data, people aged 65 years and older accounted for 30% of Japan's total population in 2025, highlighting the growing need for healthy aging solutions[1]Source: World Bank, “Population ages 65 and above (% of total population) - Japan”, data.worldbank.org. Older consumers are increasingly adopting collagen-based nutraceuticals to help maintain joint function, improve skin elasticity, and support overall musculoskeletal health. Clinical studies have demonstrated that undenatured collagen can reduce disease incidence by approximately 50% in collagen-induced arthritis models by leveraging oral immune tolerance mechanisms, reinforcing confidence in collagen-based joint health ingredients[2]BioCell Technology. "BioCell Collagen - BIOCELL TECHNOLOGY - Dairy-free - GRAS." 2025. www.knowde.com. In addition, commercially available ingredients such as BioCell Technology's GRAS-status collagen, sourced from chicken sternal cartilage, have expanded the availability of clinically supported collagen formulations for dietary supplements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and purification costs | -1.5% | Global, most acute for manufacturers in North America and Europe operating under GMP | Long term (≥ 4 years) |

| Risk of disease transmission from animal-derived collagen sources | -0.6% | Europe and North America, with acute regulatory pressure in the European Union | Medium term (2-4 years) |

| Limited availability of high-quality raw materials | -0.8% | Asia-Pacific and Europe, with supply fragility for bovine hides and poultry sternum cartilage | Medium term (2-4 years) |

| Competition from hydrolyzed collagen peptides | -1.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production and purification costs

High production and purification costs remain a significant challenge for the native collagen market, as preserving the protein's natural triple-helix structure requires sophisticated extraction and processing technologies. Manufacturers must employ carefully controlled purification methods to maintain biological activity while removing impurities and ensuring product safety. These advanced processes require specialized equipment, stringent quality control systems, and highly skilled personnel, resulting in elevated production expenses. In addition, compliance with pharmaceutical, medical device, and food-grade regulatory standards further increases manufacturing and validation costs. The sourcing of high-quality raw materials from bovine, porcine, marine, or poultry origins also adds to overall production expenditures, particularly when traceability and sustainability requirements must be met.

Risk of disease transmission from animal-derived collagen sources

Concerns regarding the potential transmission of animal-borne diseases continue to pose a challenge for the native collagen market, particularly for products derived from bovine and other ruminant sources. Manufacturers must comply with stringent sourcing, traceability, and processing regulations to ensure product safety and maintain consumer confidence. Although modern purification and quality control technologies have significantly reduced biological risks, safety concerns remain an important consideration for healthcare providers, regulators, and consumers. In July 2024, the EFSA BIOHAZ Panel concluded that oral exposure to collagen produced from ruminant bones would be expected to generate new BSE cases with a probability of 0 to 1% under standard manufacturing conditions, while also noting that commercial extraction from ruminant bones is not yet practiced[3]Source: European Food Safety Authority, “BSE risk posed by ruminant collagen and gelatine derived from bones”, efsa.europa.eu. While this assessment indicates an extremely low estimated risk under defined conditions, it also highlights the continued regulatory scrutiny surrounding animal-derived collagen.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Formats Disrupt A Bovine-Dominant Market

Bovine collagen accounted for the largest share of the native collagen market, representing 45.23% of total revenue in 2025, owing to its abundant availability, cost-effectiveness, and extensive commercial use. The segment benefits from a well-established raw material supply chain supported by the global meat processing industry, ensuring consistent production and competitive pricing. Native bovine collagen is widely utilized in dietary supplements, medical devices, tissue engineering, wound care products, and cosmetic formulations because of its high structural similarity to human collagen. Its favorable mechanical properties and broad regulatory acceptance have further strengthened its adoption across healthcare and personal care applications.

Marine collagen is projected to register the fastest CAGR of 9.71% through 2031, driven by rising consumer demand for sustainably sourced and highly bioavailable collagen ingredients. Extracted primarily from fish skin, scales, and other marine by-products, marine collagen has gained significant popularity in nutraceuticals, functional foods, and premium skincare products due to its excellent absorption characteristics and Type I collagen content. Growing consumer preference for pescatarian-friendly and non-bovine alternatives, coupled with concerns related to animal-derived ingredients, is accelerating market adoption.

By Form: Powder Holds Scale While Liquid Gains From Convenience

Powdered native collagen accounted for the largest share of the market, capturing 51.54% of total revenue in 2025, driven by its versatility, long shelf life, and ease of incorporation into a wide range of products. The powdered form is extensively used in dietary supplements, functional foods, medical nutrition products, and cosmetic formulations due to its excellent stability during storage and transportation. Manufacturers prefer powdered collagen because it offers greater flexibility in formulation, accurate dosage control, and compatibility with capsules, tablets, sachets, and beverage mixes. Its lower logistics costs and reduced risk of spoilage compared to liquid formulations further contribute to its widespread commercial adoption.

Liquid native collagen is projected to register the fastest CAGR of 10.78% through 2031, fueled by growing demand for ready-to-consume health and beauty products. Liquid formulations are gaining popularity due to their convenience, rapid absorption, and suitability for functional beverages, liquid dietary supplements, and premium skincare products. Consumers increasingly associate liquid collagen with enhanced bioavailability and ease of consumption, particularly among aging populations and wellness-focused individuals. Manufacturers are expanding their portfolios with flavored collagen drinks, beauty shots, and liquid nutraceutical products to meet evolving consumer preferences.

By Application: Nutraceuticals Lead While Cosmetics Builds Momentum

Nutraceuticals accounted for the largest share of the native collagen market, generating 43.34% of total revenue in 2025, driven by the growing global focus on preventive healthcare and nutritional supplementation. Native collagen is widely incorporated into dietary supplements aimed at improving joint health, bone strength, skin elasticity, muscle recovery, and overall wellness. Increasing consumer awareness of collagen's role in healthy aging and active lifestyles has significantly boosted demand for collagen-based capsules, powders, gummies, and functional beverages. The segment is also supported by rising healthcare expenditures, expanding aging populations, and the growing popularity of protein-enriched nutrition products.

Cosmetics and personal care are projected to register the fastest CAGR of 10.21% through 2031, fueled by increasing demand for anti-aging, skin-rejuvenating, and beauty-enhancing products. Native collagen is becoming a key ingredient in premium skincare formulations, facial serums, creams, masks, and hair care products due to its ability to support skin hydration, elasticity, and structural integrity. The growing popularity of beauty-from-within concepts, combined with rising consumer spending on premium cosmetic products, is accelerating adoption across both topical and ingestible beauty applications.

Geography Analysis

North America dominated the native collagen market in 2025, accounting for 34.76% of global revenue, supported by strong demand from the nutraceutical, biomedical, and cosmetic industries. The region benefits from high consumer awareness regarding preventive healthcare, healthy aging, and collagen supplementation, particularly in the United States and Canada. Well-established pharmaceutical and biotechnology sectors have accelerated the adoption of native collagen in regenerative medicine, wound care, tissue engineering, and medical devices. In addition, the presence of leading collagen manufacturers, advanced research capabilities, and stringent quality standards has strengthened the region's competitive position.

Asia-Pacific is projected to register the fastest CAGR of 9.89% through 2031, driven by expanding healthcare infrastructure, rising disposable incomes, and growing consumer awareness of health and beauty products. Countries such as China, Japan, South Korea, and India are witnessing rapid growth in the consumption of collagen-based nutraceuticals, cosmetics, and functional beverages. The region's thriving beauty and personal care industry, coupled with increasing demand for anti-aging skincare products, is creating significant opportunities for native collagen manufacturers. Expanding food processing and pharmaceutical industries are also incorporating native collagen into innovative formulations for health and wellness applications.

Europe, South America, and the Middle East and Africa contribute to the native collagen market expansion through evolving consumer preferences and broader industrial applications. In Europe, strong demand for clean-label nutraceuticals, premium cosmetics, and advanced biomedical products, along with stringent regulatory standards and a well-developed healthcare sector, supports market maturity. In South America, rising dietary supplement consumption, growing awareness of functional nutrition, and livestock-derived raw material availability drive steady growth. In the Middle East and Africa, rising healthcare investments, premium personal care demand, and growing interest in preventive wellness solutions support market emergence.

Competitive Landscape

The native collagen market remains moderately competitive, with a mix of multinational life science companies, specialized collagen manufacturers, and biotechnology firms competing across healthcare, nutraceutical, cosmetic, and research applications. Competition is driven by product quality, preservation of the native triple-helix structure, raw material sourcing, regulatory compliance, and technological expertise rather than price alone. Manufacturers are increasingly focusing on producing high-purity native collagen that meets the stringent requirements of pharmaceutical, biomedical, and premium personal care industries. Strong quality assurance systems, international certifications, and validated manufacturing processes have become key differentiators in securing long-term contracts with global customers.

Leading companies are investing significantly in research and development to improve extraction technologies, enhance collagen stability, and develop innovative products tailored for regenerative medicine, tissue engineering, wound care, dietary supplements, and advanced cosmetic formulations. Strategic initiatives such as capacity expansions, partnerships with biotechnology and healthcare companies, and collaborations with academic research institutions are becoming increasingly common. Companies are also expanding their portfolios by introducing collagen products derived from bovine, porcine, marine, and poultry sources to address diverse consumer preferences and regulatory requirements.

As global demand for functional nutrition, healthy aging solutions, and regenerative healthcare continues to increase, competition within the native collagen market is expected to intensify over the forecast period. Manufacturers are prioritizing product standardization, clinical validation, and scientific evidence to strengthen customer confidence and support premium product positioning. Advances in biotechnology, purification methods, and bioactive collagen formulations are creating new opportunities for product differentiation and higher-value applications.

Native Collagen Industry Leaders

-

SARIA SE & Co. KG

-

BIOFAC GROUP

-

Titan Biotech Limited

-

Lonza Group AG

-

BICO Group AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Holista Colltech Limited entered into a binding joint venture with Swang Chai Chuan Limited to establish an ovine nano-collagen production facility in Collie, Western Australia. The 50:50 joint venture will accelerate the commercialisation of Holista’s collagen technology, with the facility targeting high-value applications in nutraceuticals, food, cosmetics, and biomedical sectors.

- March 2026: Provenance Bio partnered with Artes Biotechnology to scale the commercial production of Col-01, a precision-fermented, animal-free hydroxylated collagen peptide. The collaboration combines Provenance Bio’s proprietary collagen technology with Artes Biotechnology’s expertise in microbial strain engineering and bioprocess development to enable large-scale, cost-effective manufacturing.

- May 2025: Nortian raised USD 41 million in funding at a USD 100 million valuation to expand operations and development of ultra-pure collagen production from hide through proprietary processing technologies, targeting supplements, food, and pharmaceutical industries with industrial facilities in Missouri.

Global Native Collagen Market Report Scope

Native collagen is a naturally occurring structural protein that retains its original triple-helix molecular structure, preserving its biological activity and functional properties. The native collagen market is segmented by source, form, application, and geography. Based on product type, the market is segmented into bovine, porcine, poultry, marine and others. Based on form, the market is segmented into powder and liquid. Based on application, the market is segmented into nutraceuticals, cosmetics and personal care, pharmaceuticals and food and beverages. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Bovine |

| Porcine |

| Poultry |

| Marine |

| Others |

| Powder |

| Liquid |

| Nutraceuticals |

| Cosmetics and Personal Care |

| Pharmaceuticals |

| Food and Beverages |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Source | Bovine | |

| Porcine | ||

| Poultry | ||

| Marine | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Nutraceuticals | |

| Cosmetics and Personal Care | ||

| Pharmaceuticals | ||

| Food and Beverages | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size outlook for native collagen through 2031?

The native collagen market size is projected to rise from USD 252.57 million in 2026 to USD 378.22 million by 2031 at an 8.41% CAGR.

Which source segment currently leads native collagen demand?

Bovine collagen led the source mix with 45.23% share in 2025 because supply chains are established and the material fits several end uses.

Which form is expanding the fastest?

Liquid collagen is forecast to grow at 10.78% CAGR through 2031, supported by ready-to-drink formats and functional beverages.

Why are nutraceuticals still the main outlet for native collagen?

Nutraceuticals held 43.34% share in 2025 because joint health, cartilage support, and clinically backed positioning remain core purchase drivers.

Which region offers the strongest near-term growth?

Asia-Pacific is the fastest-growing region with a projected 9.89% CAGR through 2031, supported by functional food demand and improving regulatory pathways.

Page last updated on: