Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

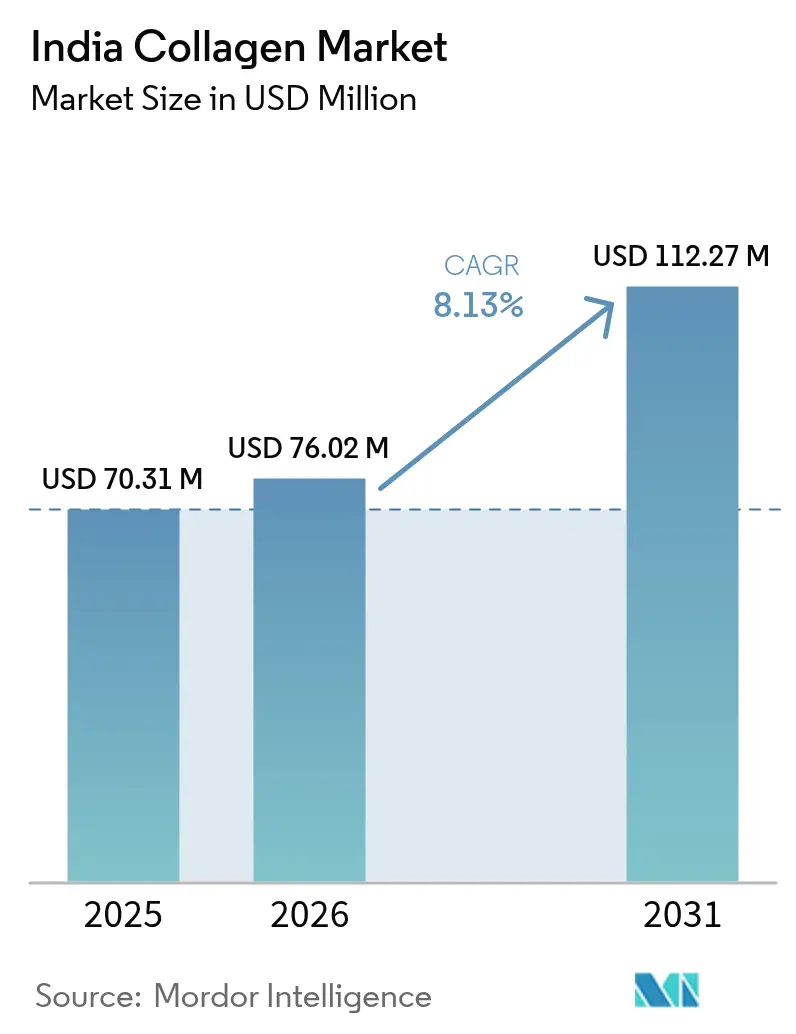

| Base Year Market Size (2025) | USD 70.31 Million |

| Market Size (2026) | USD 76.02 Million |

| Market Size (2031) | USD 112.27 Million |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Collagen Market Analysis by Mordor Intelligence

The India collagen market size is expected to grow from USD 70.31 million in 2025 to USD 76.02 million in 2026 and is forecast to reach USD 112.27 million by 2031 at 8.13% CAGR over 2026-2031. The market growth is driven by significant demographic changes, including an aging population and increased health consciousness among younger consumers, as well as rising disposable incomes across urban areas. Government regulations continue to enhance quality standards and promote domestic production through the implementation of manufacturing incentives and quality control measures. The expanding fitness culture, particularly in metropolitan cities, combined with the growing demand for functional foods and premium pet nutrition products, creates diverse opportunities for collagen-infused products across multiple segments. Recent regulatory developments include the Food Safety and Standards Authority of India (FSSAI) 2025 packaging amendment, which allows recycled PET usage to promote sustainable packaging solutions, and the potential transfer of nutraceutical oversight to the Central Drugs Standard Control Organization (CDSCO). This transfer indicates heightened compliance requirements and stricter quality control measures for manufacturers and importers in the collagen market.

Key Report Takeaways

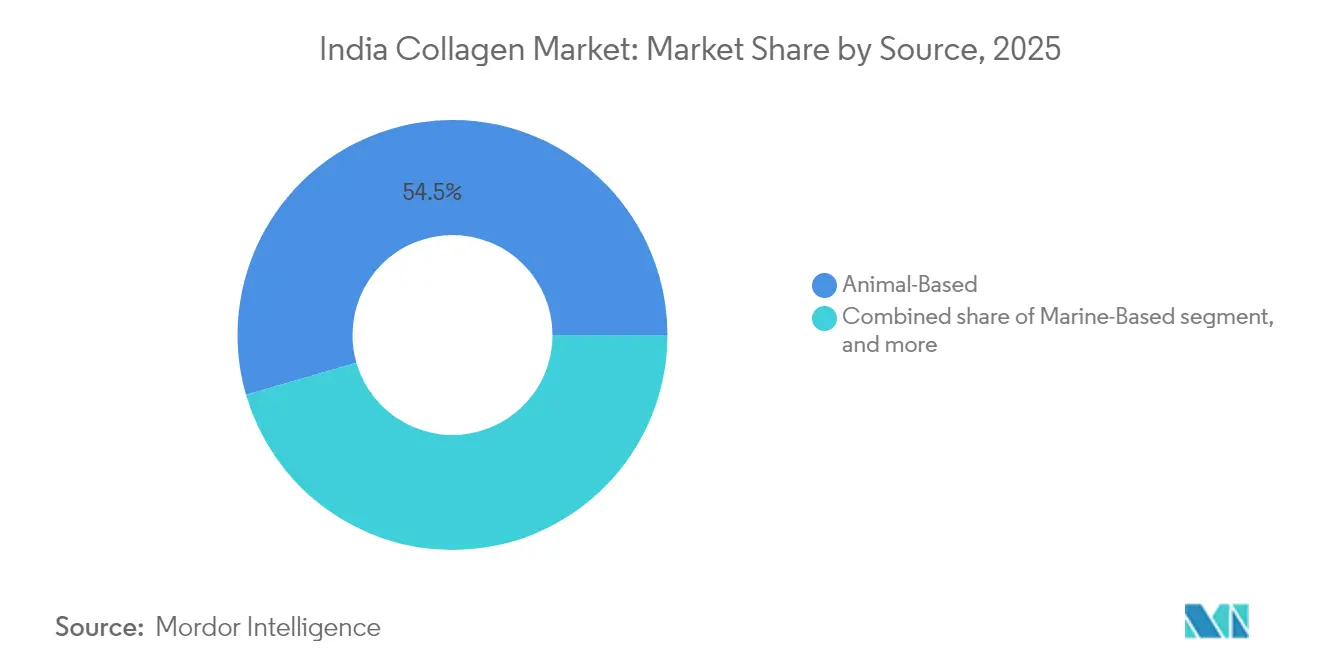

- By source, animal-based collagen led with 54.48% of India collagen market share in 2025; marine-derived collagen is projected to rise at a 9.05% CAGR from 2026–2031.

- By product type, gelatin commanded 48.05% of the Indian collagen market size in 2025, yet hydrolyzed collagen is expected to expand at an 8.64% CAGR.

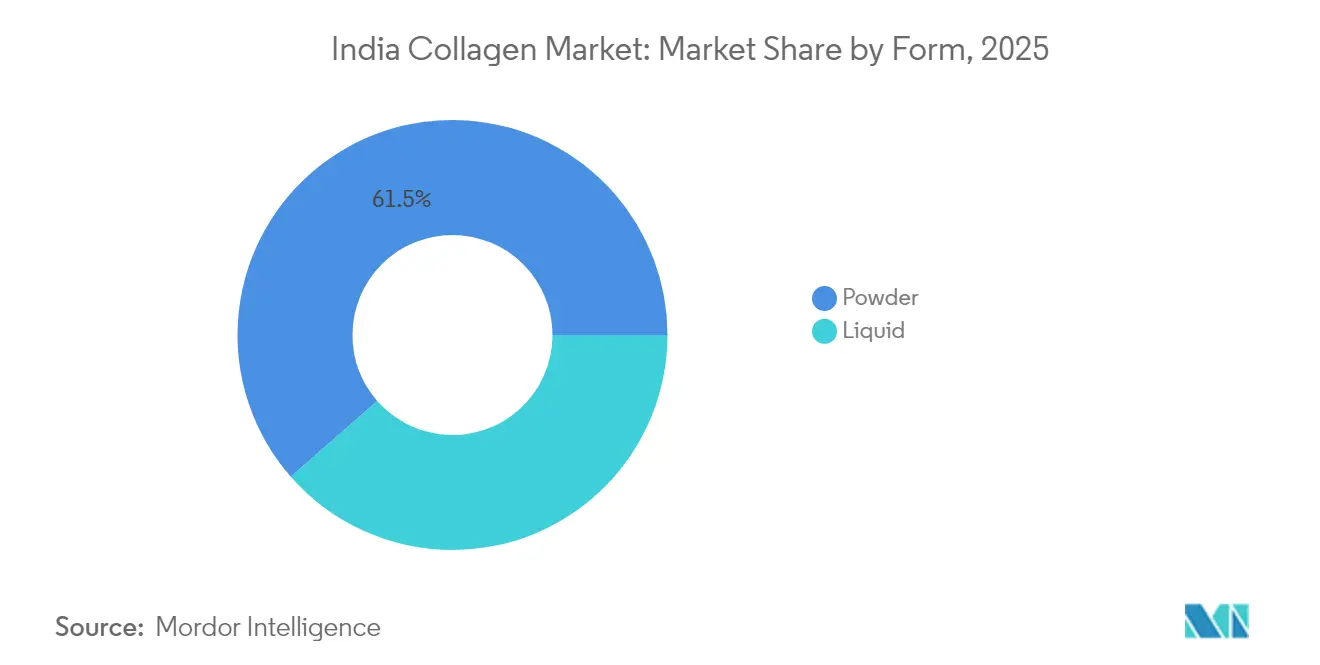

- By form, powder formats accounted for a 61.45% slice of the India collagen market share in 2025, while liquid formats are on track for an 8.53% CAGR.

- By application, dietary supplements captured 57.78% of the 2025 India collagen market size; cosmetics and personal care are forecast to grow the quickest at a 8.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Collagen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and beauty consciousness | +1.8% | National, with early gains in Mumbai, Delhi, Bangalore | Long term (≥ 4 years) |

| Sports and performance nutrition | +1.2% | Urban centers, Maharashtra, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| Expansion of functional food and beverage offerings | +1.0% | National, concentrated in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Pet health and animal nutrition | +0.8% | Metropolitan areas, Gujarat, Maharashtra, Delhi NCR | Long term (≥ 4 years) |

| Increasing vegan and specialty source options | +0.6% | Urban markets, South India, West Bengal | Medium term (2-4 years) |

| Product label transparency and clean-label demand | +0.4% | National, premium segment focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Beauty Consciousness

India's demographic transition presents distinct market opportunities for collagen products due to its large working-age population and accelerating aging trends. The country has the world's largest youth population, while its elderly segment is growing significantly. According to the United Nations Population Fund, the population aged 60 and above is expected to increase from 153 million in 2023 to 347 million by 2050[1]Source: The United Nations Population Fund, "India's ageing population: Why it matters more than ever," unfpa.org. This demographic shift generates demand across therapeutic and lifestyle enhancement applications, driven by increased aging awareness and beauty consciousness. Clinical evidence demonstrating collagen's benefits for joint health, skin elasticity, and bone mineral density over 12-month periods has helped address consumer skepticism and increase market acceptance[2]Source: International Journal of Orthopaedics Sciences, "Specific collagen peptides in osteoporosis management: Unraveling therapeutic potential through expert perspectives and scientific insights," orthopaper.com. The younger population segment increasingly uses collagen for preventive purposes, while older consumers focus on its therapeutic applications. States such as Kerala and Tamil Nadu, which are projected to reach peak population around 2040, are positioned to be early adopters of age-management products. While FSSAI regulations currently govern safety standards, potential oversight from the Central Drugs Standard Control Organization (CDSCO) may enhance quality requirements and lead to market consolidation.

Sports and Performance Nutrition

Sports and performance nutrition in India is experiencing significant growth due to increased government investment. The Ministry of Youth Affairs and Sports has allocated ₹3,790.50 crore for 2021-22 to 2025-26, expanding program coverage and improving sports infrastructure[3]Source: Ministry of Youth Affairs and Sports, "India’s Growing Focus on Youth and Sports," pib.gov. This enhanced support is promoting athletic participation, which increases the demand for advanced nutrition solutions, including collagen supplements, among professional athletes and fitness enthusiasts. The regulatory oversight of protein claims has enhanced the market position of collagen peptides, supported by their Generally Recognized as Safe (GRAS) status and proven benefits in diabetes management and joint health. The adoption of performance nutrition products is growing in metropolitan areas, driven by increased gym memberships and fitness awareness. Specialized formulations, such as Rousselot's Nextida GC, which demonstrates a 42% reduction in post-meal glucose spikes, expand the market beyond traditional joint health applications[4]Source: Darling Ingredients, "Darling Ingredients Introduces Nextida™ GC," darlingii.com. The Food Safety and Standards Authority of India's (FSSAI) strict protein supplement regulations present opportunities for compliant collagen manufacturers. Additionally, the younger demographic's preference for clean-label, scientifically validated nutrition products strengthens collagen's market position compared to synthetic alternatives.

Expansion of Functional Food and Beverage Offerings

Expansion of functional food and beverage offerings is becoming a major growth driver for the Indian collagen market as consumers increasingly seek products that deliver both nutritional value and lifestyle benefits. Collagen is being incorporated into a diverse range of formats from fortified dairy, protein bars, and ready-to-drink beverages to functional confectionery enabling brands to target multiple consumption occasions. The rising popularity of beauty-from-within products is merging with the wellness trend, encouraging manufacturers to blend collagen with complementary ingredients such as vitamins, antioxidants, and plant-based proteins to enhance appeal and efficacy. This convergence not only boosts product innovation but also expands collagen’s reach beyond niche supplement categories into mainstream retail and e-commerce shelves. The shift towards clean-label, premium-positioned functional products is particularly strong among urban millennials and Gen Z, who prioritize convenience, scientifically backed benefits, and sensory appeal. International brands and domestic players alike are launching collagen-enriched snacks and beverages tailored to Indian taste preferences while highlighting claims such as skin elasticity, joint support, and muscle recovery. With FSSAI regulations ensuring safety and transparency in ingredient labeling, the category benefits from rising consumer trust, paving the way for sustained market penetration and higher per capita collagen consumption.

Pet Health and Animal Nutrition

Pet health and animal nutrition segments present significant growth opportunities for the Indian collagen market, supported by increasing pet ownership and higher spending on premium animal care products. According to Agriculture and Agri-Food Canada, India recorded approximately 23 million households with pet dogs and 1.7 million with pet cats in 2023. The market recognizes collagen, especially in hydrolyzed and peptide forms, for its benefits in enhancing joint health, mobility, skin condition, and coat quality in pets. The combination of urbanization, higher disposable incomes, and nuclear family trends has increased pet adoption rates, leading owners to choose specialized nutrition products containing functional ingredients like collagen over generic feed. This shift creates opportunities for manufacturers to develop collagen-enriched treats, chews, and supplements that address both preventive and therapeutic requirements. The growth in this segment aligns with the expansion of India's livestock, aquaculture, and poultry sectors, where collagen-rich nutrition products improve growth performance, immunity, and overall animal health. The increasing awareness among veterinarians, pet food formulators, and livestock producers regarding collagen's benefits has led to greater incorporation of this ingredient in feed and supplement formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material supply limitations | -1.4% | National, coastal regions for marine sources | Medium term (2-4 years) |

| Religious and ethical dietary restrictions | -1.0% | National, concentrated in Muslim-majority regions | Long term (≥ 4 years) |

| Stability and shelf-life issues | -0.8% | Pan-India, acute in high-humidity regions | Short term (≤ 2 years) |

| Evidence gap and consumer skepticism on efficacy | -0.6% | Rural and semi-urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Supply Limitations

India's collagen supply chain faces structural constraints due to its dependence on imported raw materials for gelatin production. Marine collagen availability is restricted by seasonal fishing patterns and inadequate processing infrastructure. The concentration of seafood processing facilities in coastal states creates logistical challenges, while religious and cultural factors limit the availability of bovine and porcine raw materials. GELITA developed specialized technologies, such as RXL gelatin, to address processing constraints in the Asia-Pacific region, demonstrating industry recognition of infrastructure limitations. Marine-derived collagen prices fluctuate due to climate-related variations in fish catch volumes. The absence of an integrated cold-chain infrastructure between source locations and processing facilities increases raw material deterioration and operational costs. Manufacturers, especially smaller ones without long-term supply agreements, face supply security risks and currency exposure due to their reliance on imported specialized collagen.

Religious and Ethical Dietary Restrictions

Religious dietary laws affect collagen market growth through halal and kosher certification requirements, creating supply chain complexities for animal-derived products. The global market's reliance on pork-derived gelatin conflicts with Islamic dietary restrictions, while bovine-sourced products face limitations in Hindu markets. The challenges in authenticating halal and kosher gelatin affect consumer trust, as current detection methods cannot fully ensure compliance with religious dietary requirements. While biotechnology enables plant-based collagen alternatives, these lab-grown vegan options face higher production costs and consumer acceptance challenges. Marine collagen presents a religiously acceptable alternative but encounters supply constraints and higher prices. The diverse certification requirements across religious authorities create additional compliance challenges for manufacturers serving multiple consumer segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Sources Drive Sustainability Shift

Animal-based collagen holds a dominant market share of 54.48% in 2025, supported by well-established supply chains and cost advantages. Marine-based collagen is experiencing rapid growth with a 9.05% CAGR through 2031, driven by sustainability considerations and broader religious dietary acceptance. Bovine collagen leads the animal segment due to abundant raw materials and existing processing infrastructure. However, its market reach is limited in regions with significant Hindu populations. Porcine collagen faces market limitations due to Islamic dietary restrictions, creating distribution challenges for manufacturers. Marine collagen, despite higher prices, offers religious acceptability and environmental benefits that attract environmentally conscious consumers. The utilization of fish processing waste provides a cost-effective source for marine collagen production.

Biotechnology advancements have enabled the development of plant-based collagen alternatives. These include laboratory-produced vegan collagen, created by introducing human collagen genes into microorganisms. While these alternatives provide cruelty-free options, their production costs exceed traditional collagen sources. The combination of increasing sustainability demands and religious dietary considerations supports the continued growth of marine collagen, despite its premium pricing.

By Product Type: Hydrolyzed Formulations Gain Bioavailability Edge

Hydrolyzed collagen shows the highest growth rate at 8.64% CAGR through 2031, while gelatin maintains market dominance with a 48.05% share in 2025. Gelatin's market leadership position results from its widespread use in food and pharmaceutical applications, cost-effectiveness, and functional versatility across multiple end-uses. Native/undenatured collagen serves specific therapeutic segments, particularly in joint health applications where type II collagen's structural properties are essential and command premium prices.

Hydrolyzed collagen peptides are gaining increasing adoption in dietary supplements and cosmetics due to superior absorption rates, supported by clinical evidence. Manufacturers leverage advanced processing technologies to produce hydrolyzed collagen with specific molecular weights for different applications. For example, Rousselot's Nextida GC platform demonstrates the expanding applications of hydrolyzed collagen, achieving a 42% reduction in post-meal glucose levels and extending beyond traditional joint health markets.

By Form: Liquid Formats Capture Premiumization Trends

Liquid collagen formats accelerate at 8.53% CAGR through 2031, driven by consumer preference for convenient consumption and perceived absorption benefits, while powder formats maintain market dominance with a 61.45% share in 2025, supported by their cost-effectiveness and versatility in product formulations. The powder segment's leadership position stems from efficient manufacturing processes, longer shelf life, and established distribution networks, particularly in price-sensitive markets. While liquid formulations command higher prices due to convenience and marketed absorption benefits, scientific evidence supporting superior bioavailability compared to powder formats remains limited.

Urban consumers increasingly choose liquid formats for their ready-to-consume nature and convenience-focused lifestyle preferences. India's climate conditions present significant stability challenges for liquid collagen products, though technological solutions like GELITA's RXL address product degradation and crosslinking issues that affect product integrity. The requirements for specialized manufacturing processes and temperature-controlled distribution infrastructure restrict liquid format availability in rural areas, creating distinct market segments based on geographical accessibility and distribution capabilities.

By Application: Cosmetics Segment Accelerates Beauty-From-Within Trend

The cosmetics and personal care segment is projected to grow at a CAGR of 8.93% through 2031, while dietary supplements maintain market dominance with a 57.78% share in 2025. This growth reflects increasing consumer interest in beauty-from-within products and the premiumization trend in personal care. The cosmetics segment's growth is supported by higher profit margins, opportunities for brand differentiation, and consumer acceptance of premium pricing for beauty products. Dietary supplements maintain their market leadership position through established distribution networks, therapeutic positioning, and broad price accessibility.

The food and beverages segment presents growth opportunities as manufacturers integrate marine collagen into functional foods, exemplified by Dabur's introduction of marine collagen formulations in FMCG channels. FSSAI regulations require manufacturers to substantiate cosmetic health benefit claims, providing competitive advantages to companies with clinical validation. The integration of nutraceutical and cosmetic properties has resulted in hybrid products that expand market opportunities across both supplement and beauty categories. Additional applications in medical and veterinary segments, while smaller, provide specialized opportunities for manufacturers with appropriate regulatory compliance.

Geography Analysis

India's collagen market shows significant domestic growth potential, driven by demographic shifts, regulatory changes, and increasing health awareness in urban and semi-urban areas. The aging population, rising disposable incomes, and growing interest in preventive healthcare contribute to market expansion. The proposed transfer of nutraceutical oversight from FSSAI to CDSCO may enhance quality standards, improve product safety monitoring, and create consolidation opportunities for manufacturers who meet compliance requirements.

Metropolitan areas such as Mumbai, Delhi, and Bangalore lead market adoption due to higher disposable incomes, advanced healthcare infrastructure, and elevated health consciousness. The southern states, particularly Karnataka and Tamil Nadu, exhibit robust growth in manufacturing and consumption, supported by established pharmaceutical and biotechnology hubs, research institutions, and skilled workforce availability. Coastal regions have access to marine collagen raw materials from fish processing industries, but face processing infrastructure constraints that limit supply capacity. These limitations include inadequate cold storage facilities, processing technology gaps, and quality control challenges.

The government's BioE3 policy aims to strengthen biomanufacturing capabilities through infrastructure development, technology adoption incentives, and skill development programs. Rural markets face challenges in distribution networks, price sensitivity, and awareness gaps, though digital commerce expansion creates new access channels for collagen products. The limited healthcare infrastructure, inconsistent power supply, and seasonal accessibility issues further impact market penetration. However, government initiatives for rural development, increasing mobile connectivity, and the growth of telemedicine services present opportunities for market expansion in these regions.

Competitive Landscape

The Indian collagen market demonstrates moderate consolidation, with a 6 out of 10 rating. This market structure allows both established multinational companies and emerging domestic firms to gain market share through distinct strategies. Established companies such as GELITA use technological innovations, including RXL gelatin, to address regional climate challenges, particularly in maintaining product stability during storage and transportation.

Market opportunities exist in specialized segments like glucose management, collagen for diabetic patients, marine-based formulations derived from fish scales and skin, and pet nutrition supplements targeting the growing companion animal market, where regulatory requirements create competitive advantages. Companies that invest in bioavailability enhancement through peptide optimization, stability solutions for tropical climates using advanced encapsulation techniques, and sustainable sourcing methods such as traceable supply chains, gain advantages in premium market segments.

The Food Safety and Standards Authority of India (FSSAI) regulatory framework benefits established companies with robust quality systems, including Good Manufacturing Practice (GMP) certifications and quality testing protocols. Potential Central Drugs Standard Control Organisation (CDSCO) oversight may further consolidate the market by increasing entry barriers through stricter quality control requirements and documentation processes. New market entrants are developing plant-based alternatives using pea protein and biotechnology-derived collagen through recombinant protein expression, though high production costs and limited consumer acceptance currently restrict widespread adoption.

India Collagen Industry Leaders

-

Jellice Group

-

Nitta Gelatin Inc.

-

Gelita AG

-

Titan Biotech

-

Rousselot (Darling Ingredients)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nitta Gelatin India Ltd. (NGIL) announced a ₹200 crore expansion plan during its golden jubilee celebration. The plan includes a ₹60 crore collagen peptide production facility in Kerala, which will begin operations by mid-2025. This investment encompasses both gelatin and collagen peptide operations to address increasing global demand in the food and pharmaceutical sectors.

- December 2024: Lonza Capsules & Health Ingredients (CHI) implemented new manufacturing lines for hard gelatin capsules (HGCs) at its facilities in Rewari, India, and Suzhou, China. The expanded lines became operational in late 2024, with additional capacity planned for the third quarter of 2025. The capsules serve both pharmaceutical and nutraceutical applications, accommodating solid and liquid fills. The expansion improves regional supply capabilities with enhanced flexibility, quality control, and customization options for size and color.

- December 2024: Pioneer Jellice India Pvt. Ltd. and Ashok Matches & Timber Industries Pvt. Ltd. acquired a controlling stake in India Gelatine & Chemicals Ltd (IGCL). The acquisition began with a purchase of 39.42% of IGCL's shares through a Share Purchase Agreement (SPA), followed by an open offer to acquire an additional 26% from public shareholders.

India Collagen Market Report Scope

Collagen can be defined as the structural protein produced by the body. Collagen plays a crucial role in the structure & function of cartilage, connective tissue, skin, and bones.

India's collagen market is segmented by form and end-user. By form, the market is segmented into animal-based and marine-based. By end-user, the market is segmented into animal feed, personal care & cosmetics, food & beverages, and supplements. The food & beverages segment is further sub-segmented into the bakery, beverages, breakfast cereals, and snacks. Additionally, the supplement segment is further segmented into elderly nutrition and medical nutrition, and sport/performance nutrition.

The market sizing has been done in value terms in USD and for volume terms in volume in tons for all the abovementioned segments.

By Source

| Animal-Based |

| Marine-Based |

| Plant-Based |

By Product Type

| Gelatin |

| Hydrolyzed Collagen |

| Native/Undenatured Collagen |

By Form

| Powder |

| Liquid |

By Application

| Food and Beverages |

| Cosmetics and Personal Care |

| Dietary Supplements |

| Others |

| By Source | Animal-Based |

| Marine-Based | |

| Plant-Based | |

| By Product Type | Gelatin |

| Hydrolyzed Collagen | |

| Native/Undenatured Collagen | |

| By Form | Powder |

| Liquid | |

| By Application | Food and Beverages |

| Cosmetics and Personal Care | |

| Dietary Supplements | |

| Others |

Key Questions Answered in the Report

What is the projected value of the India collagen market in 2031?

The market is expected to reach USD 112.27 million by 2031, growing at an 8.13% CAGR over 2026-2031.

Which collagen source is expanding fastest in India?

Marine collagen is the fastest-growing source, forecast to post a 9.05% CAGR due to sustainability and religious neutrality advantages.

Why are hydrolyzed collagen products gaining popularity?

Hydrolyzed formats offer smaller peptides that absorb more efficiently, supporting joint, skin, and metabolic health claims and driving an 8.64% CAGR.

How is regulation shaping the India collagen space?

FSSAI labeling reforms and the possible shift of nutraceutical oversight to CDSCO are tightening quality controls, favoring manufacturers with GMP-grade facilities.

Page last updated on: