Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

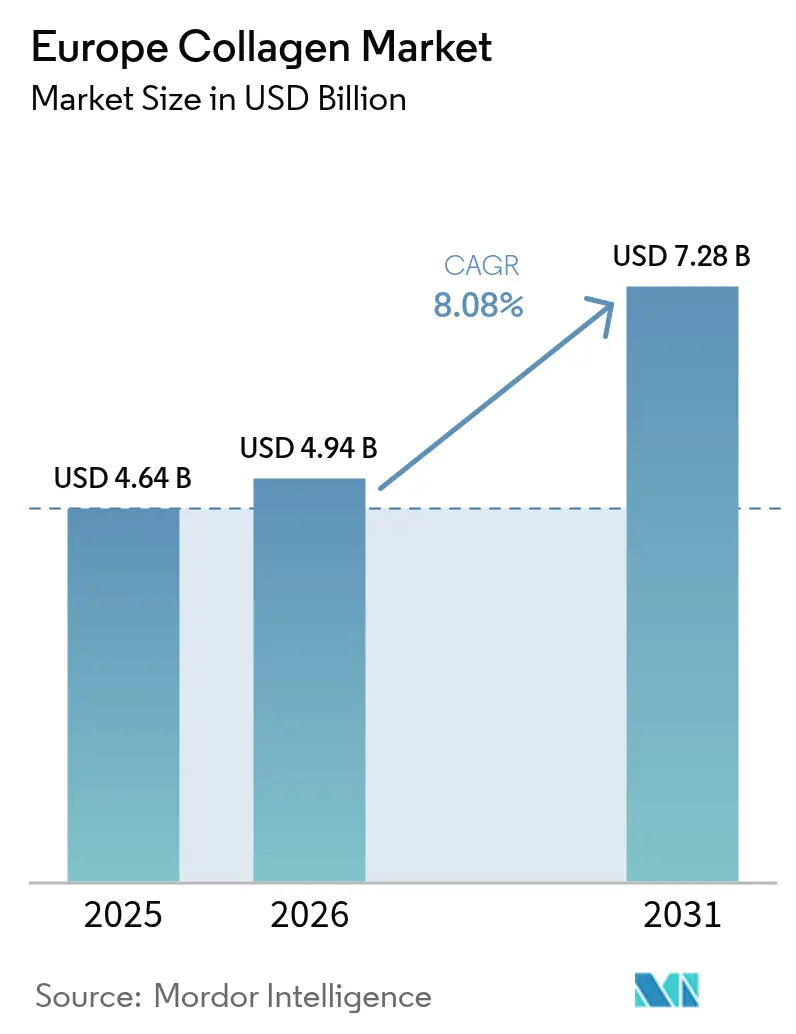

| Base Year Market Size (2025) | USD 4.64 Billion |

| Market Size (2026) | USD 4.94 Billion |

| Market Size (2031) | USD 7.28 Billion |

| Growth Rate (2026 - 2031) | 8.08% CAGR |

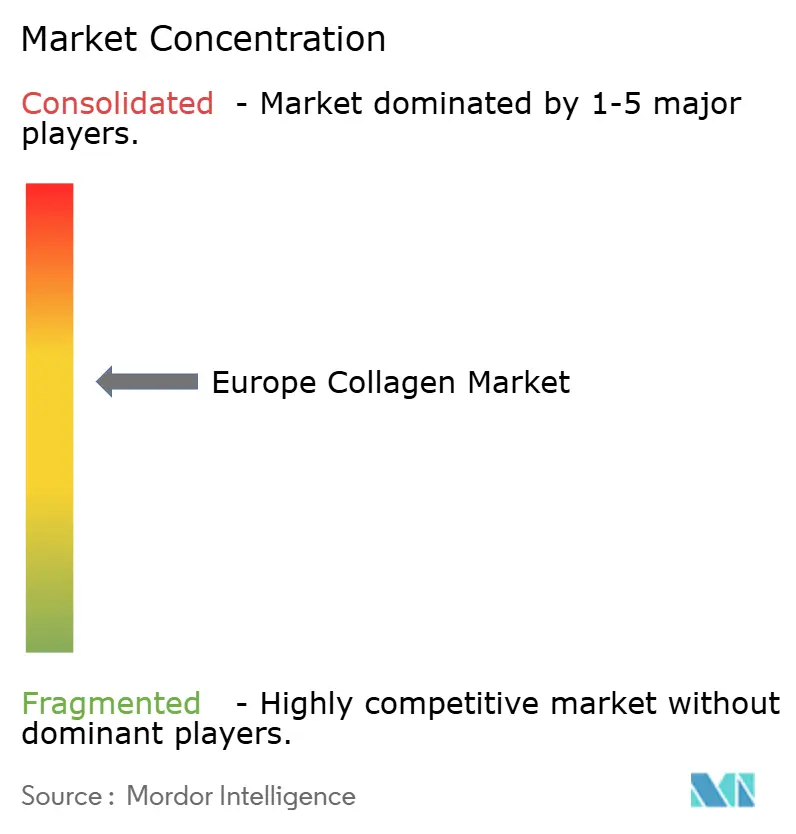

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Collagen Market Analysis by Mordor Intelligence

The Europe collagen market size is projected to be USD 4.64 billion in 2025, USD 4.94 billion in 2026, and reach USD 7.28 billion by 2031, growing at a CAGR of 8.08% from 2026 to 2031.European consumers are increasingly transitioning from reactive pharmaceutical solutions to preventive nutricosmetic routines that combine dermatology with nutrition science, which is driving demand for ingestible collagen across various age groups. Clinical evidence highlighting benefits for joint health and skin elasticity, along with a preference for clean-label products, is encouraging manufacturers to focus on traceable raw materials and smaller molecular weight peptides with improved absorption rates. Consolidation among major producers is intensifying as companies aim to achieve economies of scale in bovine and porcine collagen sourcing, while marine-based and precision-fermentation alternatives are gaining popularity due to sustainability considerations. Liquid formats utilizing liposomal or colloidal delivery systems are experiencing faster adoption compared to powders, despite their higher production costs. This shift is further supported by the growing consumer awareness of the 20% to 30% higher bioavailability offered by these advanced delivery systems, which enhances their effectiveness and appeal. Additionally, the focus on traceability and sustainability aligns with the increasing demand for transparency in sourcing and production processes, further strengthening consumer trust in these products.

Key Report Takeaways

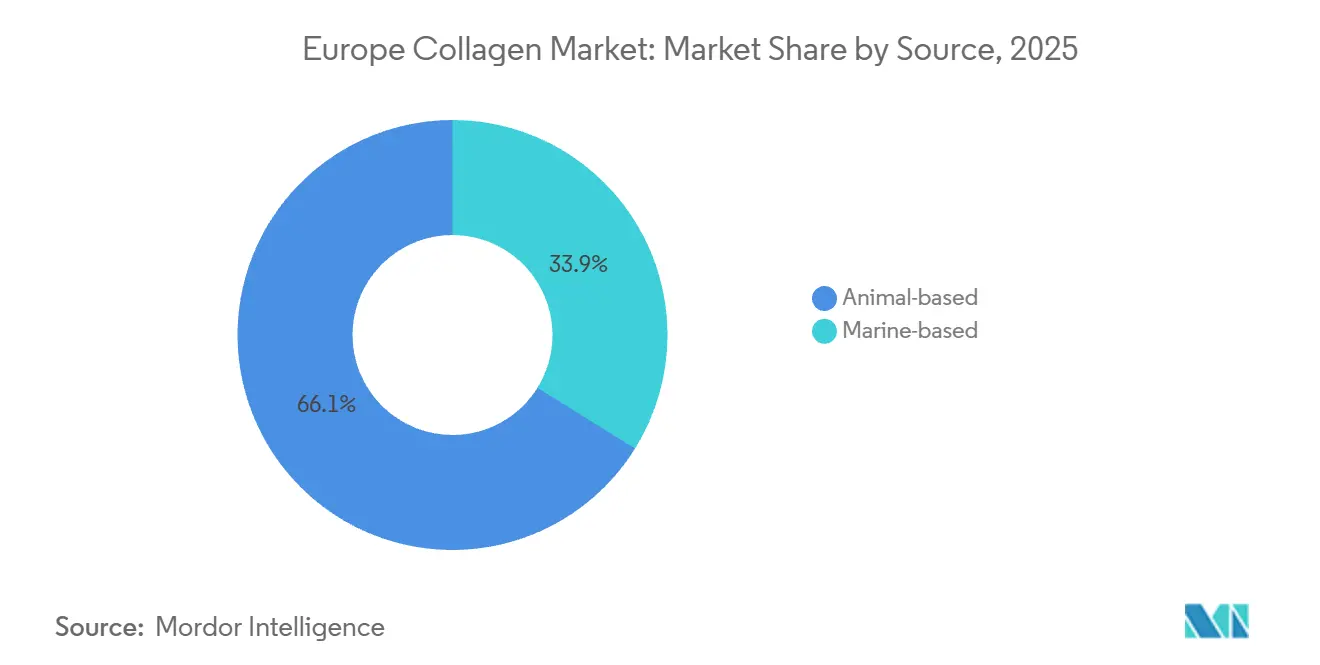

- By source, animal-based collagen held 66.14% of the Europe collagen market share in 2025, whereas marine collagen is forecast to post the quickest 9.32% CAGR to 2031.

- By form, powders commanded 81.12% of Europe collagen market share in 2025, and liquids are projected to grow at an 8.89% CAGR through 2031.

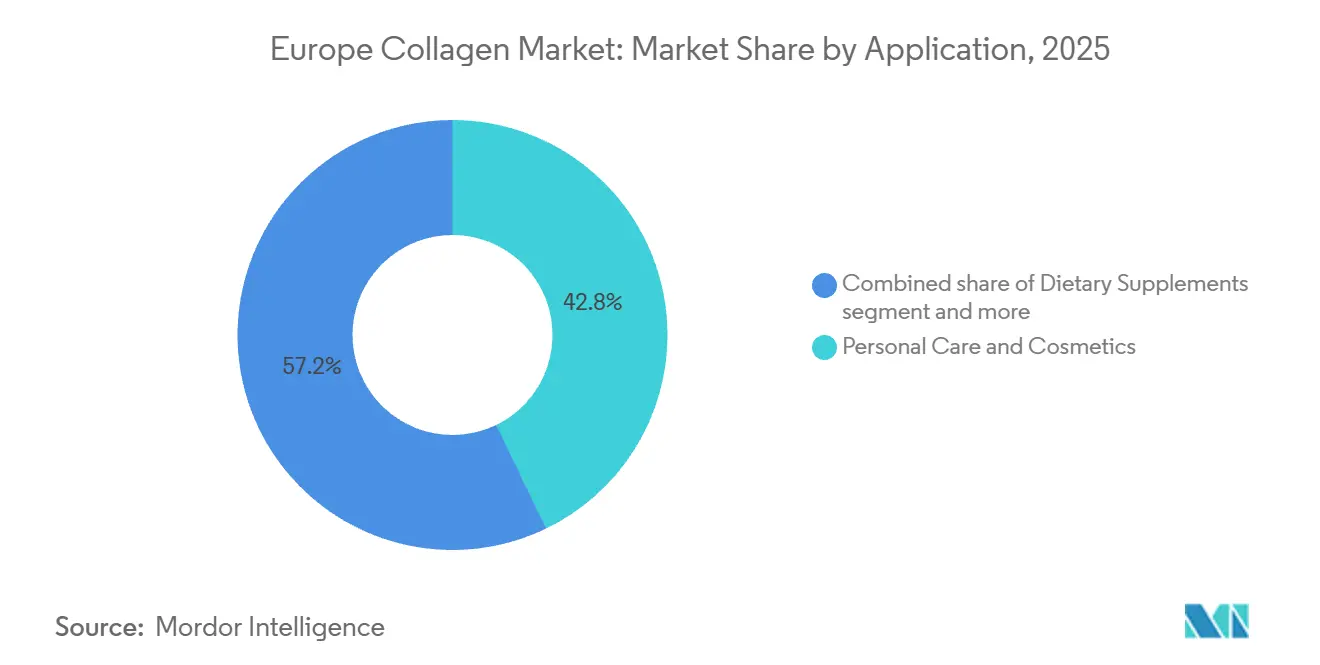

- By application, personal care and cosmetics captured 42.83% revenue share of the Europe collagen market in 2025; dietary supplements are projected to expand at a 9.33% CAGR through 2031 across the region.

- By geography, Germany led with 33.82% of the Europe collagen market size in 2025, while Spain is expected to log the fastest 9.32% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Collagen Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population seeking joint care, skin, bone, and hair health solutions | +1.8% | Pan-European, concentrated in Germany, Italy, France | Long term (≥ 4 years) |

| Shift toward preventive healthcare and holistic wellness approaches | +1.5% | Western Europe (Germany, UK, Netherlands), expanding to Iberia | Medium term (2-4 years) |

| Growing preference for beauty-from-within nutricosmetics | +1.3% | France, Italy, Spain, Germany | Medium term (2-4 years) |

| Rising popularity of clean-label and natural products | +1.1% | Nordic countries (Sweden), Germany, Netherlands, UK | Short term (≤ 2 years) |

| Advancements in collagen bioavailability and peptide technology | +1.0% | Germany (Evonik, Gelita), France (Weishardt), Netherlands (DSM-Firmenich) | Medium term (2-4 years) |

| Shift to sustainable marine collagen sources with higher absorption | +0.9% | Coastal nations (Spain, Italy, France, UK), Nordic region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging population seeking joint care, skin, bone, and hair health solutions

Europe's demographic shift, characterized by the rapid growth of the 60-plus age group compared to the working-age population, is influencing supplement demand. The focus is shifting from multivitamins to targeted functional ingredients. According to data from the World Health Organization (WHO), by 2030, the global population aged 60 or older will reach 1.4 billion, representing a 34% increase from 2019 [1]Source: World Health Organization, “Ageing and health,” who.int. Europe is contributing significantly to this trend due to low fertility rates and increased life expectancy. Joint-health formulations containing Type II collagen peptides are gaining popularity as orthopedic specialists increasingly recommend them to reduce reliance on non-steroidal anti-inflammatory drugs. In February 2024, Evonik plans to launch Vecollage Fortify L, a liquid collagen peptide aimed at improving joint mobility. This launch is supported by clinical evidence showing that a daily intake of 10 grams of hydrolyzed collagen can enhance cartilage synthesis markers within 12 weeks. Claims related to skin elasticity and dermal hydration are particularly appealing to the 50-plus female demographic, who view collagen as a non-invasive alternative to cosmetic procedures. While applications for hair and bone health are still emerging, they are attracting research and development investments, especially in formulations combining collagen with biotin, silica, and vitamin D3 for synergistic benefits.

Shift toward preventive healthcare and holistic wellness approaches

National health systems in Germany, France, and the Netherlands are evaluating reimbursement models for preventive nutrition interventions. These regulatory developments support collagen supplements positioned for wellness maintenance rather than disease treatment. This shift is driven by financial pressures, as chronic musculoskeletal conditions place a significant burden on European healthcare systems. Policymakers are increasingly focusing on preventive measures to delay the onset of such conditions. Consumers are also adopting holistic wellness routines that integrate collagen with probiotics, adaptogens, and plant-based proteins. This trend signifies a move from single-ingredient supplementation to multi-functional product combinations. Gelita highlighted this development by presenting OPTIBAR and PeptENDURE at Food Ingredients Europe (Fi Europe) in December. These collagen peptides are tailored for sports nutrition and recovery, addressing the intersection of performance enhancement and preventive care. Furthermore, the expansion of telemedicine and personalized nutrition applications is enabling direct-to-consumer brands to offer collagen products alongside DNA-based dietary recommendations. This strategy bypasses traditional retail channels, allowing brands to achieve higher profit margins.

Growing preference for beauty-from-within nutricosmetics

France and Italy, which have traditionally been strong markets for topical skincare, are now seeing a shift toward ingestible beauty products. This change is supported by dermatological studies that link oral collagen peptides to measurable improvements in skin hydration and wrinkle reduction. A 2024 study published in Frontiers in Nutrition found that a daily intake of 2.5 grams of collagen peptides over 12 weeks increased dermal collagen density by 9% in women aged 45 to 65, offering clinical evidence that appeals to evidence-focused consumers. DSM-Firmenich's April 2025 launch of SYN-COLL CB peptide, a bioactive ingredient designed to stimulate collagen synthesis at the cellular level, highlights the industry's transition from commodity gelatin to precision peptides with proven efficacy. Nutricosmetics are also gaining traction through social media, where influencers aged 25 to 40 share visible skin improvement results, encouraging trial among previously skeptical demographics. Additionally, regulatory clarity under European Union (EU) Regulation 1924/2006 on nutrition and health claims has allowed brands to promote specific benefits, such as "supports skin elasticity," without risking enforcement actions. This reduced compliance risk has further encouraged investment in the category.

Rising popularity of clean-label and natural products

Nordic consumers, particularly in Sweden and Denmark, are increasingly prioritizing transparency in sourcing and processing. They prefer collagen derived from grass-fed bovine or wild-caught marine species over conventionally farmed alternatives. Lapi Gelatine's focus on European production and certifications, such as International Organization for Standardization (ISO) 22000, Food Safety System Certification (FSSC) 22000, Aquaculture Stewardship Council, and Friend of the Sea, highlights the importance of third-party validation in the premium segment. Clean-label requirements now extend beyond ingredient origin to include processing methods. Enzymatic hydrolysis is favored over acid or alkaline extraction due to its ability to avoid chemical residues and preserve native peptide structures. This trend is pressuring suppliers who cannot ensure traceability to the farm or fishery level, while benefiting vertically integrated companies that manage the supply chain from raw materials to finished peptides. Additionally, the United Kingdom's Food Safety Act 1990 and the Informed Sport certification program are establishing de facto standards that are being adopted by other European markets [2]Source: Food Standard Agency, “Key regulations,” food.gov.uk. This creates a regulatory framework that advantages large manufacturers capable of ensuring compliance.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical concerns over animal-derived collagen welfare and sourcing | -0.7% | Western Europe (Germany, UK, Netherlands, Sweden) | Medium term (2-4 years) |

| Allergenic risks from bovine, porcine, or marine sources | -0.5% | Pan-European, heightened in UK, Germany, France | Short term (≤ 2 years) |

| Stringent regulatory compliance and novel food approval | -0.6% | EU-wide, particularly Germany, France, Netherlands | Long term (≥ 4 years) |

| Taste, odor, and texture issues in supplements | -0.4% | Southern Europe (Spain, Italy, Portugal), Eastern Europe (Poland) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ethical concerns over animal-derived collagen welfare and sourcing

Animal-welfare advocacy groups in Germany and the United Kingdom (UK) are urging retailers to audit collagen supply chains for compliance with European Union (EU) Directive 98/58/EC on livestock protection. This has created reputational risks for brands unable to demonstrate humane slaughter practices. Bovine collagen sourced from cattle raised in intensive feedlots is facing boycotts from ethically conscious consumers, who prefer grass-fed or organic certifications despite their higher costs. Porcine collagen faces additional challenges due to religious and cultural restrictions, as Muslim and Jewish populations avoid porcine-derived products, limiting its market penetration in diverse urban centers such as London, Paris, and Berlin. Technological advancements, such as precision fermentation and recombinant collagen technologies, exemplified by Gelita's collaboration with Geltor, present opportunities for animal-free alternatives that replicate identical amino-acid sequences. However, as of 2026, commercial-scale production remains cost-prohibitive. Transparency initiatives, including blockchain-enabled traceability from farm to finished product, are emerging as competitive advantages. Nevertheless, the high implementation costs pose challenges for smaller suppliers. The ethical considerations surrounding collagen sourcing are becoming increasingly significant as younger consumers (aged 18 to 35) prioritize sustainability and animal welfare over price. This demographic shift is expected to influence sourcing strategies through 2031.

Allergenic risks from bovine, porcine, or marine sources

Collagen peptides, even after hydrolysis, retain allergenic epitopes that may trigger immune responses in sensitized individuals. Marine collagen presents specific risks for consumers with shellfish or fish allergies, and European Union (EU) Regulation 1169/2011 requires clear allergen labeling, which can discourage initial purchases [3]Source: European Union, “Food Information to Consumers Regulation,” eur-lex.europa.eu. Bovine collagen carries a residual risk of prion contamination, although no cases have been reported in collagen supplements. This risk contributes to consumer hesitancy in regions with a history of bovine spongiform encephalopathy outbreaks. Porcine collagen is generally well-tolerated but may cause cross-reactivity in individuals allergic to pork proteins. Clinical data on collagen allergenicity remain limited, with most reported adverse events involving gastrointestinal discomfort rather than severe allergic reactions like anaphylaxis. However, the lack of large-scale safety studies restricts widespread physician recommendations. Manufacturers are focusing on developing hypoallergenic formulations, such as extensively hydrolyzed peptides with molecular weights below 1,000 Daltons, which are believed to lower immunogenic potential. Regulatory bodies have not yet established standardized allergen testing protocols for collagen, leaving brands to self-regulate and assume liability risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Gains as Sustainability Trumps Cost

Animal-based collagen is projected to account for 66.14% of the European market volume in 2025, supported by well-established bovine and porcine supply chains and cost advantages ranging from 30% to 50% compared to marine alternatives. Bovine collagen, which is rich in Type I and Type III collagen, dominates applications in joint health and sports nutrition. Meanwhile, porcine collagen, known for its high glycine content, is preferred in cosmetic formulations aimed at improving skin elasticity. Marine-based collagen is anticipated to grow at a compound annual growth rate (CAGR) of 9.31% through 2031, driven by sustainability requirements and its perceived superior absorption due to smaller peptide sizes and a high concentration of Type I collagen.

Coastal nations such as Spain, Italy, and France are utilizing byproducts from the fishing industry to produce marine collagen, thereby reducing waste and adhering to certifications like the Aquaculture Stewardship Council and Friend of the Sea. These certifications enable premium pricing opportunities in Northern European markets. Emerging technologies, including precision fermentation and recombinant collagen production, represent a potential third category of collagen sources. Although still in the early stages of commercialization, these technologies could disrupt the traditional animal-versus-marine dichotomy by offering identical amino acid profiles without relying on animal inputs. For instance, Gelita's collaboration with Geltor highlights advancements in this area.

By Form: Liquid Formats Leverage Bioavailability Science

Powder collagen accounted for 81.12% of European revenue in 2025, driven by its cost efficiency, extended shelf life, and compatibility with existing supplement manufacturing processes. This format's dominance is particularly evident in Germany and the United Kingdom, where consumers prioritize value and are accustomed to incorporating supplements into beverages or smoothies. Meanwhile, liquid collagen is projected to grow at a compound annual growth rate (CAGR) of 8.89% through 2031, supported by advancements in liposomal encapsulation and colloidal delivery systems, which enhance absorption rates and bioavailability. For instance, Evonik's February 2024 launch of Vecollage Fortify L, a liquid peptide designed to improve joint mobility, leverages clinical evidence showing that liquid formats bypass gastric degradation more effectively than powders, allowing for lower dosages to achieve similar efficacy. Additionally, ready-to-drink collagen beverages are gaining popularity in France and Italy, where they are perceived as functional alternatives to traditional skincare routines, merging nutrition with cosmetics.

Powder formulations face challenges related to taste and texture, such as a gritty mouthfeel and residual odor, which can reduce consumer appeal. However, advancements in flavor-masking technologies, including microencapsulation and co-formulation with fruit extracts, are addressing these issues. Liquid collagen formats, while resolving sensory concerns, require preservatives and stabilizers to ensure shelf life, which can conflict with clean-label preferences and increase production costs. The growing shift toward liquid formats is also influenced by direct-to-consumer brands that utilize subscription models and premium pricing strategies to offset these higher costs. Capsule and tablet formats, though not separately segmented in the approved metrics, represent a third category that combines the stability of powders with the convenience of liquids, particularly for on-the-go consumption. For example, Gelita's EASYSEAL capsule technology, showcased at Fi Europe 2025, underscores the industry's focus on delivery innovations as a means of differentiation in a competitive market.

By Application: Dietary Supplements Outpace Cosmetics on Clinical Evidence

In 2025, personal care and cosmetics accounted for 42.83% of European collagen revenue, reflecting the sector's historical emphasis on topical anti-aging formulations and the influence of French and Italian beauty conglomerates. However, dietary supplements are projected to grow at a compound annual growth rate (CAGR) of 9.33% through 2031, driven by peer-reviewed studies linking oral collagen peptides to measurable improvements in skin hydration, joint mobility, and bone density. DSM-Firmenich's April 2025 launch of SYN-COLL CB peptide, a bioactive ingredient targeting collagen synthesis at the cellular level, illustrates the shift from commodity gelatin to precision peptides with documented efficacy. This trend is accelerating the adoption of dietary supplements among evidence-driven consumers. Food and beverages represent an emerging but high-potential application, with collagen-fortified products such as protein bars, coffee creamers, and functional waters gaining traction in mainstream retail markets in Germany and the Netherlands. Pharmaceutical applications remain niche, focusing on wound-healing matrices and tissue-engineering scaffolds, but are attracting research and development (R&D) investment as advancements in regenerative medicine continue. Animal nutrition, the smallest segment, is experiencing growth as pet food manufacturers incorporate collagen peptides into joint-health formulations for aging pets, mirroring trends observed in human supplements.

The growth of dietary supplements is further supported by telemedicine platforms and personalized nutrition apps, which bundle collagen with DNA-based dietary recommendations. These platforms bypass traditional retail channels, enabling brands to capture higher margins. Regulatory clarity under European Union (EU) Regulation 1924/2006 on nutrition and health claims has allowed brands to communicate specific benefits such as "supports skin elasticity" or "maintains joint flexibility" without triggering enforcement actions. This has reduced compliance risks that previously deterred investment in the segment. Personal care and cosmetics applications face challenges from the "beauty-from-within" movement, which promotes ingestible collagen as more effective than topical formulations. This perspective emphasizes the systemic delivery of peptides.

Geography Analysis

Germany accounted for 33.82% of European collagen revenue in 2025, supported by the manufacturing presence of Gelita and Evonik, along with a consumer base that emphasizes clinical evidence and quality certifications. Germany's market dominance is attributed to vertical integration, with Gelita managing bovine sourcing, gelatin production, and peptide hydrolysis within a single supply chain, enabling cost efficiency and faster innovation cycles. Evonik's February 2024 partnership with Jland Biotech to co-develop collagen peptides for the Asian market highlights a strategic focus on export-led growth, though European operations remain the primary profit center. The Netherlands benefits from the presence of DSM-Firmenich's headquarters and a population inclined toward preventive health measures, while Belgium and Sweden, while smaller markets in absolute terms, demonstrate high per-capita consumption due to clean-label preferences and strong regulatory frameworks ensuring product safety.

Spain is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.32% through 2031, driven by increasing disposable incomes, the integration of collagen-fortified functional foods into the Mediterranean diet, and a growing nutricosmetics culture influenced by French and Italian beauty trends. Spain's rapid growth is fueled by a wellness culture driven by tourism and the rise of direct-to-consumer brands leveraging social media to target younger demographics. France and Italy, traditionally strong in topical skincare, are shifting toward ingestible beauty products as dermatologists publish peer-reviewed studies linking oral collagen peptides to improvements in skin hydration and wrinkle depth. France's nutricosmetics market, valued at over EUR 500 million annually, is transitioning from niche to mainstream as pharmacy chains allocate shelf space to ingestible beauty products. Italy's collagen market remains fragmented, with regional players such as Italgel and Lapi Gelatine competing against multinational companies, though consolidation is expected as distribution efficiencies favor larger players.

The United Kingdom, despite regulatory changes following Brexit, remains a key market due to high supplement penetration rates and the influence of Informed Sport certification, which appeals to fitness-focused consumers. Poland's growth, though constrained by lower per-capita incomes, is accelerating as Western European brands expand into Eastern Europe. The Rest of Europe category, which includes Eastern European markets like the Czech Republic, Romania, and Hungary, is expanding from a low base as disposable incomes increase and Western supplement brands establish distribution partnerships with local retailers. These markets are witnessing gradual growth as consumers adopt preventive health measures and collagen-based products. Overall, the European collagen market reflects diverse growth dynamics, with established markets focusing on innovation and emerging markets benefiting from rising incomes and increased product availability.

Competitive Landscape

The Europe collagen market is moderately fragmented, with established gelatin producers such as Gelita, Rousselot (Darling Ingredients), and Weishardt competing alongside specialized peptide innovators like Evonik and precision-fermentation startups exploring animal-free recombinant collagen. The market is witnessing consolidation, as highlighted by the December 2025 definitive merger agreement between Darling Ingredients and Tessenderlo Group. This merger combines Rousselot and PB Leiner into a USD 1.5 billion entity with an annual capacity of 200,000 metric tons and 22 facilities across Europe and North America. This consolidation reflects the strategic focus on securing bovine and porcine supply chains amid volatile raw material pricing.

Vertical integration remains a dominant strategy in the market. By controlling sourcing, extraction, hydrolysis, and peptide formulation within a single enterprise, companies achieve cost leadership and can respond swiftly to regulatory changes. For instance, Evonik's September 2025 launch of VECOLLAN clinical-grade collagen peptides, optimized for pharmaceutical applications, demonstrates how incumbents are leveraging proprietary enzymatic processes to target high-margin segments that traditional gelatin suppliers have not pursued. Additionally, technology adoption is accelerating, with innovations such as liposomal encapsulation, nanoemulsions, and hydrogel matrices enhancing bioavailability and supporting premium pricing for liquid collagen formats.

White-space opportunities in the market include precision fermentation for animal-free collagen, collagen peptides tailored for glycemic control or gut-health applications, and geographic expansion into Eastern Europe, where supplement penetration remains below Western European averages. Emerging disruptors like Geltor, in partnership with Gelita to commercialize recombinant collagen, are challenging the traditional animal-sourcing paradigm. However, as of 2026, commercial-scale production of recombinant collagen remains cost-prohibitive. Smaller players, such as Lapi Gelatine, are differentiating themselves through a focus on European production and third-party certifications such as International Organization for Standardization (ISO) 22000, Food Safety System Certification (FSSC) 22000, Aquaculture Stewardship Council, and Friend of the Sea. These certifications appeal to clean-label advocates and command price premiums, particularly in Nordic markets.

Europe Collagen Industry Leaders

Gelita AG

Darling Ingredients Inc.

PB Leiner

Italgel S.r.l.

Nippi Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Darling Ingredients announced a USD 1.5 billion collagen ingredients venture, capitalizing on the growing health and wellness market demand for functional collagen products. This strategic investment positioned the company to expand production capacity and develop innovative collagen applications across food, pharmaceutical, and cosmetic segments.

- October 2024: Darling Ingredients introduced Nextida GC, a collagen peptide that reduced post-meal glucose spikes by an average of 42% based on clinical trials. The product represented a new category of collagen-based solutions targeting metabolic health applications.

- February 2024: Evonik partnered with Jland Biotech to market vegan collagen for cosmetic applications, investing through its Venture Capital group to commercialize fermentation-based collagen production. The collaboration aimed to provide commercial quantities of vegan collagen for skincare products, including anti-aging and hydrating formulations.

Europe Collagen Market Report Scope

Collagen is an essential structural protein found in the skin, tendons, and bones of vertebrates, providing numerous nutritional, skin, and health benefits. The collagen market in Europe is categorized based on source, form, application, and geography. The market is divided into two primary sources: animal-based collagen and marine-based collagen. By form, the market is segmented into powder and liquid collagen. Collagen is applied across several industries, including food and beverages, dietary supplements, personal care and cosmetics, pharmaceuticals, and animal nutrition. Additional applications include medical care, biomaterial research, and packaging. Geographically, the market is segmented into Germany, France, the United Kingdom, Russia, Italy, Spain, and the rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Source

| Animal-based |

| Marine-based |

By Form

| Powder |

| Liquid |

By Application

| Food and Beverages |

| Dietary Supplements |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Animal Nutrition |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Source | Animal-based |

| Marine-based | |

| By Form | Powder |

| Liquid | |

| By Application | Food and Beverages |

| Dietary Supplements | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Animal Nutrition | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large will European demand for collagen be by 2031?

It is forecast to reach USD 7.28 billion by 2031, expanding at an 8.08% CAGR from 2026 to 2031.

Which country contributes the most revenue?

Germany led with 33.82% of regional revenue in 2025, supported by vertically integrated manufacturers.

What segment is growing fastest?

Dietary supplements are projected to rise at a 9.33% CAGR on the back of strong clinical validation.

Are marine sources overtaking bovine collagen?

Marine collagen is still smaller in absolute terms but is set to grow at 9.31% CAGR, faster than animal-based formats.

Why are liquid collagen products gaining popularity?

Liposomal and colloidal delivery systems boost bioavailability, enabling lower dosages and convenient ready-to-drink formats.

Page last updated on: