Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

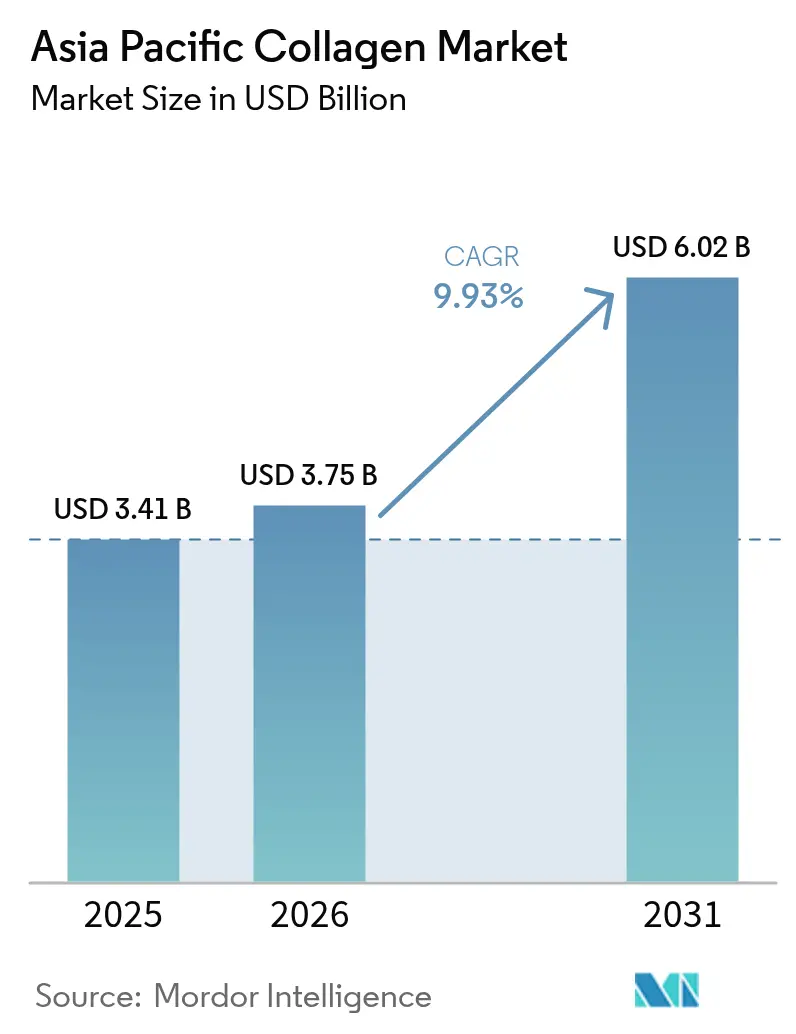

| Base Year Market Size (2025) | USD 3.41 Billion |

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia Pacific Collagen Market Analysis by Mordor Intelligence

The Asia Pacific collagen market size was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.75 billion in 2026 to reach USD 6.02 billion by 2031, at a CAGR of 9.93% during the forecast period (2026-2031). This robust growth, driven by a 10.02% CAGR, is attributed to several key factors, including demographic shifts, rising disposable incomes, and an increasing focus on preventive health and beauty-from-within consumption patterns. The region is emerging as the global hub for collagen supply and demand, leveraging China's manufacturing economies of scale alongside India's rapidly growing demand. The market is witnessing advancements in extraction technologies, such as enzymatic hydrolysis and acid-soluble collagen methods, which are improving production efficiency and output. Marine-based sourcing initiatives, including the use of fish skin and scales, are gaining popularity due to their sustainability and superior bioavailability. Furthermore, the expansion of regulatory frameworks, including harmonized standards across countries, is fostering innovation and facilitating cross-border trade within the region. Despite these positive developments, the market faces certain challenges. Competition from alternative proteins, such as plant-based and lab-grown options, is intensifying. Additionally, rising raw material costs are exerting pressure on profit margins, posing short-term hurdles for manufacturers. Nevertheless, the long-term outlook for the Asia Pacific collagen market remains optimistic, supported by technological advancements and evolving consumer preferences.

Key Report Takeaways

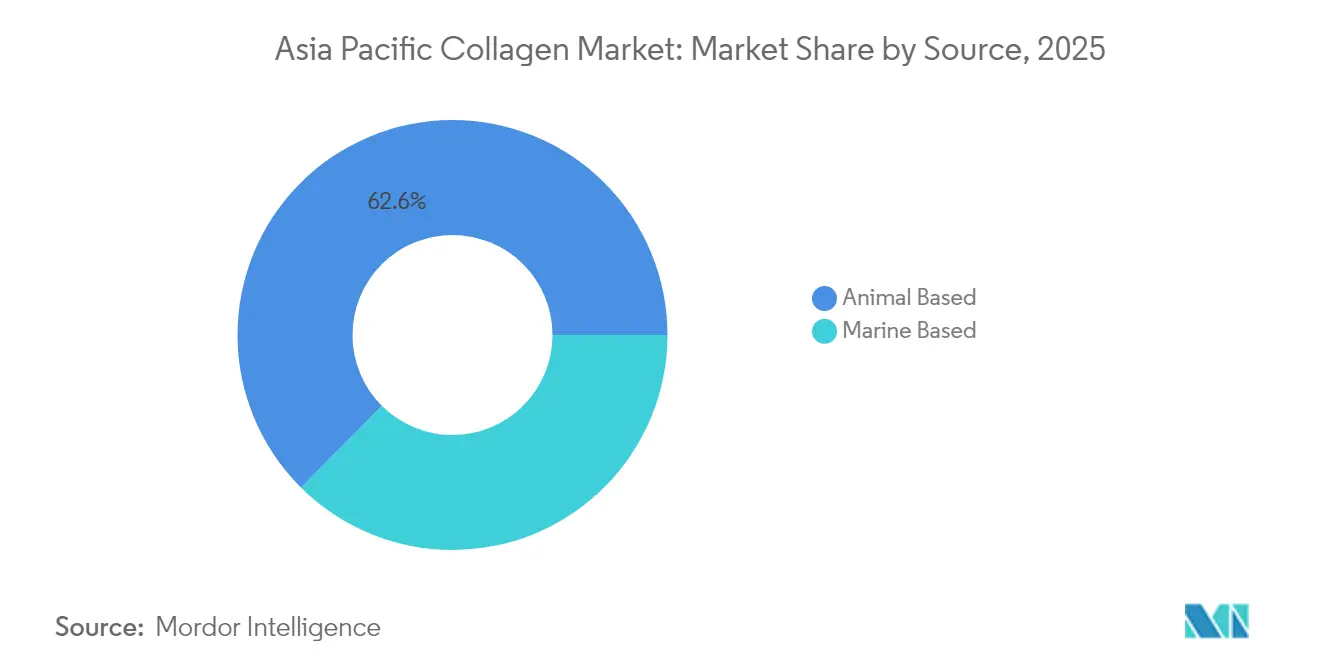

- By source, animal-based collagen captured 62.55% of the Asia Pacific collagen market share in 2025, whereas marine-based variants are forecast to grow at a 10.28% CAGR between 2026 and 2031.

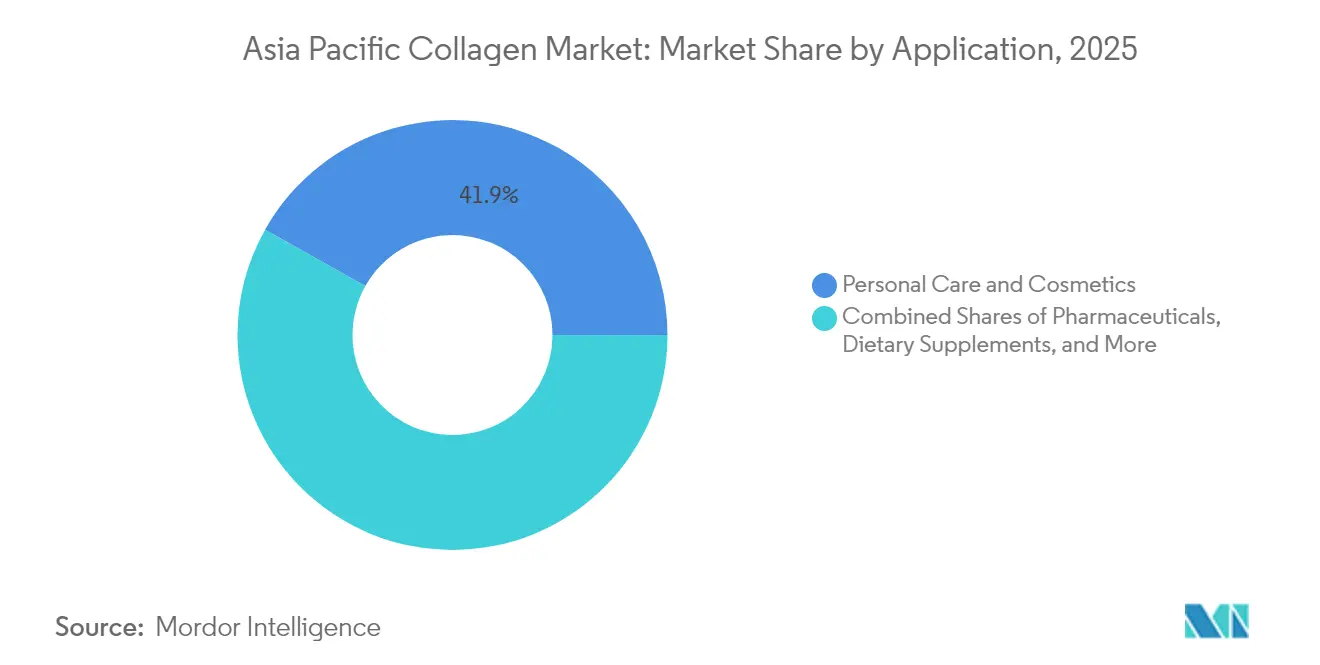

- By application, personal care and cosmetics led revenue with a 41.85% share in 2025, while dietary supplements are expected to record the highest 11.07% CAGR through 2031.

- By geography, China contributed 34.11% of 2025 regional sales, and India is poised to advance at an 11.38% CAGR in the same forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Collagen Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer demand for health and wellness products | +1.8% | APAC core, strongest in China and India | Medium term (2-4 years) |

| Ageing population seeking joint-care solutions | +1.6% | Japan, Australia, South Korea with spillover to China | Long term (≥ 4 years) |

| Rising Applications in Anti-Aging Creams and Other Beauty Products | +1.4% | Global, with premium segments in Japan and South Korea | Short term (≤ 2 years) |

| Technological advancements in extraction, processing, and formulation | +1.2% | Manufacturing hubs in China, innovation centers in Japan | Medium term (2-4 years) |

| Shift toward sustainable marine collagen sources | +0.9% | Coastal economies: Thailand, Indonesia, Vietnam | Long term (≥ 4 years) |

| Rising Innovation in research and production | +0.8% | R&D centers in Japan, China, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Demand for Health and Wellness Products

As the wellness economy continues to expand across the Asia Pacific region, collagen is increasingly being utilized in functional nutrition, extending its applications beyond traditional beauty-related uses. Furthermore, per capita income in the region is expected to grow significantly, rising from USD 17,440 in 2024 to a projected USD 23,260 by 2029. This economic growth is driving a shift toward preventive health investments, creating a strong foundation for the adoption of premium collagen products. These products are specifically designed to address key health concerns such as joint health, skin elasticity, and bone density maintenance. Consumers are demonstrating a growing willingness to pay higher prices for collagen formulations that are supported by robust scientific evidence. This trend offers substantial margin expansion opportunities for suppliers who can effectively demonstrate the clinical efficacy of their products through peer-reviewed research and ensure compliance with regulatory health claims.

Ageing Population Seeking Joint-Care Solutions

As developed APAC markets experience significant demographic shifts, the demand for joint-care collagen applications continues to grow steadily. According to the World Bank[1]World Bank, "Population ages 65 and above (% of total population) - Japan", www.data.worldbank.org data from 2024, 30% of people in Japan were above the age of 65. Japan, characterized by its advanced aging society, serves as a pivotal market for testing and developing innovative solutions. For instance, Rohto Pharmaceutical's MOCOLA brand has introduced a unique combination of 20ml collagen drinks and vitamin tablets, effectively addressing the consumption preferences of elderly consumers. This approach highlights the importance of format innovation in catering to the aging population. Beyond Japan, similar trends are emerging in China and South Korea, where aging baby boomers are becoming key drivers of market growth. These consumers, equipped with substantial accumulated wealth and a strong focus on health and wellness, are fostering the development of premium market segments. The demand for clinically-validated joint health formulations in these regions underscores the growing importance of addressing the specific needs of this demographic group.

Rising Applications in Anti-Aging Creams and Other Beauty Products

As consumer preferences increasingly lean towards holistic anti-aging solutions, the beauty industry is accelerating the incorporation of collagen into its formulations. This trend emphasizes the combination of topical and ingestible products to address aging concerns comprehensively. In April 2025, DSM-Firmenich introduced SYN-COLL CB tripeptide, a groundbreaking innovation in eco-conscious, high-performance peptides. This product is derived from 99% natural origins and has undergone clinical validation across diverse ethnic groups, highlighting its efficacy and inclusivity. The Asia Pacific cosmetics market, which accounts for over one-third of the global market share, offers a significant growth opportunity for collagen-infused beauty products. Additionally, sustainability is becoming a critical factor for brands, serving as a key differentiator in the competitive landscape while ensuring compliance with evolving regulatory requirements.

Technological Advancements in Extraction, Processing, and Formulation

Companies like Glanbia Nutritionals are driving significant advancements in collagen technology by introducing high-potency tripeptides. These tripeptides offer 4x faster absorption and 10x greater efficacy compared to traditional peptides, all while requiring just one-tenth of the dosage. Additionally, breakthroughs in enzymatic hydrolysis have enabled precise control over molecular weight, enhancing peptide functionality for specific health applications. This not only improves the effectiveness of collagen-based products but also reduces production costs, making them more accessible. These technological innovations have broadened collagen's use across various product formats, including ready-to-drink beverages, gummies, and functional foods. By addressing consumer preferences for convenience, these developments are facilitating collagen's penetration into mass-market channels, thereby expanding its market reach and potential.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative proteins | -0.7% | Global, with innovation centers in China and Japan | Short term (≤ 2 years) |

| Stringent regulatory compliance and certification requirements | -0.5% | Regulatory-intensive markets: Japan, Australia, South Korea | Medium term (2-4 years) |

| Concerns over allergenicity and religious dietary restrictions | -0.3% | Muslim-majority markets: Indonesia, Malaysia | Long term (≥ 4 years) |

| High costs of sourcing and processing high-quality collagen raw materials | -0.2% | Raw material importing countries: Japan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Proteins

Companies like Rawga are driving significant innovation in collagen sourcing by developing VC-H1, a vegetable collagen derived from plant cell wall extensin. This product is specifically designed to replicate the tripeptide structure and molecular weight of animal collagen, offering a plant-based alternative that closely mimics its natural counterpart. At the same time, Evonik is making strides in precision fermentation through substantial investments and advancements in biotechnology. These efforts are creating scalable and sustainable alternatives to traditional collagen, addressing growing concerns about environmental impact and dietary restrictions. Additionally, these technologies hold the potential to reduce production costs when implemented at scale, making them economically viable. Consequently, traditional collagen suppliers are facing mounting pressure to adapt. They are focusing on differentiating their offerings by emphasizing superior bioavailability, securing clinical validation, and targeting specialized applications. These areas highlight the unique advantages of natural collagen, particularly its complex matrix properties, which synthetic alternatives have yet to fully replicate.

Stringent Regulatory Compliance and Certification Requirements

Regulatory complexities across APAC markets significantly hinder market entry and escalate compliance costs for businesses. In Japan, the Consumer Affairs Agency has introduced mandatory Good Manufacturing Practices (GMP) requirements and adverse event reporting protocols for Foods with Function Claims, particularly in tablet and capsule formats. These measures aim to enhance consumer safety but impose additional regulatory obligations on companies. Similarly, in China, the government is tightening its regulatory framework with evolving cross-border e-commerce regulations and proposed stricter labeling requirements for pre-packaged foods. These changes create a more intricate compliance landscape, favoring established players who possess the regulatory expertise and financial resources necessary to manage the diverse requirements across multiple jurisdictions. Smaller suppliers and new entrants, however, face significant challenges in meeting these stringent standards, which could lead to a consolidation of market share among larger, compliant incumbents who are better equipped to navigate these regulatory hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Sustainability Drives Premium Positioning

Marine-based collagen accelerates at a 10.28% CAGR through 2031, outpacing the animal-based segment's market-leading 62.55% share in 2025, reflecting consumer preference shifts toward sustainable and hypoallergenic alternatives. Thai Union's marine collagen investments and circular economy initiatives demonstrate how fishing industry byproducts create value-added revenue streams while addressing sustainability concerns, according to the University of Florida IFAS EDIS. Animal-based collagen maintains dominance through established supply chains and cost advantages, particularly in price-sensitive market segments where functional benefits outweigh sustainability premiums.

The marine collagen segment benefits from technological advances in fish skin processing and decellularization techniques that enhance bioavailability while reducing allergenicity risks compared to bovine and porcine alternatives. Regulatory frameworks increasingly favor marine sources due to lower disease transmission risks and reduced religious dietary restrictions, particularly in Muslim-majority markets like Indonesia and Malaysia. However, marine collagen faces supply chain constraints from fishing industry regulations and seasonal availability, creating price volatility that limits mass-market penetration compared to consistently available animal-based alternatives.

By Application: Personal Care and Cosmetics Lead the Market

Personal care and cosmetics applications command 41.85% market share in 2025, yet dietary supplements emerge as the fastest-growing segment at 11.07% CAGR, indicating consumer behavior evolution toward preventive health approaches. The consumption of personal care and cosmetics is increasing in the region, owing to which, the use of collagen in various products is increasing. According to the METI (Japan) data from 2023, the production volume of makeup in Japan was 2.22 million kilograms. Darling Ingredients' development of Nextida GC collagen peptides targeting post-meal glucose spikes demonstrates application diversification beyond traditional beauty and joint health into metabolic wellness. Food and beverages represent emerging opportunities as manufacturers integrate collagen into functional foods, protein bars, and ready-to-drink formats targeting convenience-oriented consumers.

Pharmaceutical applications maintain steady growth through wound healing, orthopedic, and regenerative medicine applications, while animal nutrition segments benefit from pet humanization trends driving premium pet food formulations. The application diversification reduces market concentration risk and creates cross-selling opportunities for suppliers with comprehensive product portfolios. Regulatory approvals for new health claims, such as China's proposed joint health support function, could accelerate dietary supplement adoption and expand addressable market segments across multiple application categories.

Geography Analysis

In 2025, China holds a leading 34.11% share of the Asia Pacific collagen market, leveraging its position as a cost-efficient manufacturing hub and a rapidly growing consumption center. China's extensive raw material processing capabilities and well-developed supply chains drive cost advantages, enabling competitive pricing in global markets. Darling Ingredients' operations in China, generating USD 238.06 million in Food Ingredients revenue for 2024, underscore the market's scale and importance for global collagen suppliers. The country's shift toward stricter regulations, including enhanced labeling requirements and substantiation of health claims, creates challenges for smaller players while benefiting established suppliers with expertise in compliance and robust financial resources.

India is the fastest-growing market in the region, with a projected CAGR of 11.38% through 2031. This growth is driven by increasing disposable incomes, greater health awareness, and a growing middle class. India's youthful population and rising focus on preventive healthcare contribute to strong long-term demand for collagen-based dietary supplements and functional foods. However, the country's complex regulatory environment for nutraceutical classifications and import requirements poses challenges, encouraging businesses to adopt local manufacturing and partnership strategies. India's traditional medicine practices and consumer preference for natural health solutions foster acceptance of collagen products marketed as wellness enhancers rather than pharmaceutical solutions.

Japan and Australia are established, premium-focused markets where regulatory frameworks support science-based health claims, and consumers are willing to pay for clinically-validated products. Japan's "Foods with Function Claims" system facilitates evidence-based marketing, while Australia's Therapeutic Goods Administration enhances regulatory credibility, supporting regional market growth. These developed markets act as innovation hubs for new product formats and delivery systems, with successful launches often expanding to other APAC countries. In the broader Asia Pacific region, including Southeast Asian countries like Thailand, Indonesia, and Vietnam, opportunities exist for marine collagen sourcing and cost-effective manufacturing. These emerging markets, characterized by a growing middle class and increasing health awareness, present significant potential for collagen product consumption.

Competitive Landscape

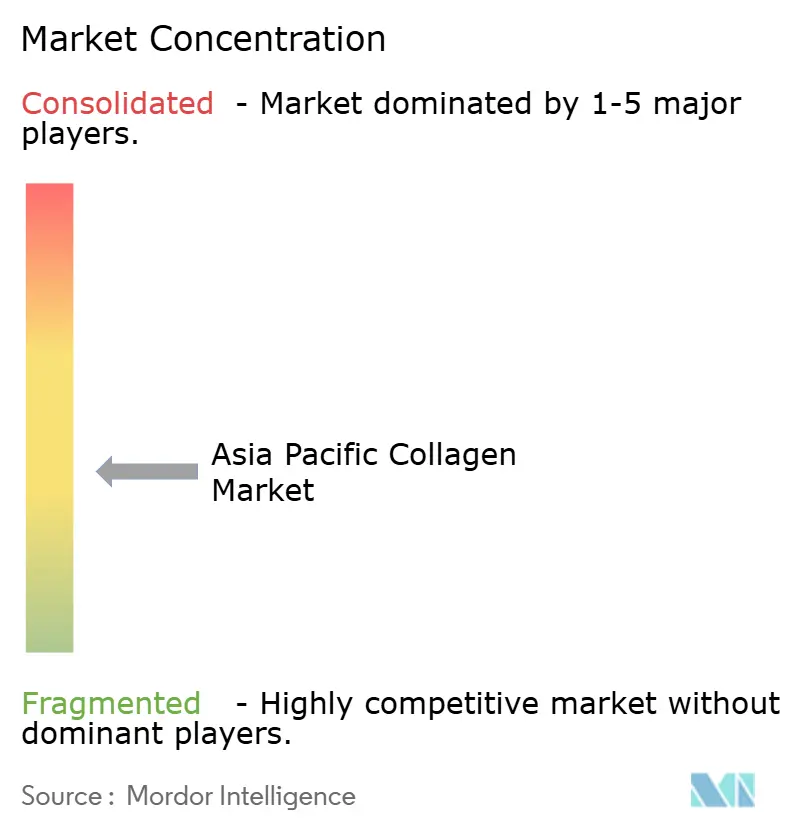

The Asia Pacific collagen market, with a concentration score of 4 out of 10, indicates moderate fragmentation and highlights significant opportunities for consolidation among players with scale advantages and advanced technological capabilities. Leading suppliers like Darling Ingredients maintain strong market positions through vertical integration strategies that encompass raw material sourcing, processing, and distribution across various geographies.

Companies with diverse product portfolios, covering multiple applications and source materials, hold a competitive edge by enabling cross-selling opportunities and reducing reliance on single market segments. As precision fermentation and alternative protein companies disrupt traditional sourcing models, technology-driven differentiation becomes increasingly critical. Strategic partnerships and joint ventures are driving market expansion. For instance, Darling Ingredients' May 2025 partnership with Tessenderlo Group aims to establish a new company focused on collagen-based health, wellness, and nutrition applications.

Innovation-centric companies utilize proprietary peptide profiles and targeted health applications to secure premium pricing and strengthen their competitive position through intellectual property protections. Untapped opportunities lie in personalized nutrition, sustainable sourcing initiatives, and penetration into emerging markets. Additionally, strong regulatory compliance capabilities provide a competitive advantage in highly-regulated markets such as Japan and Australia.

Asia Pacific Collagen Industry Leaders

-

Hangzhou Nutrition Biotechnology Co. Ltd .

-

Jiangxi Cosen Biochemical Co., Ltd.

-

Nitta Gelatin, NA Inc.

-

Gelita AG

-

Tessenderlo Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Chiyoda Corporation successfully launched Japan's first "Plant Biofoundry" in Yokohama as a demonstration platform for plant bio-manufacturing. This facility was developed under a NEDO initiative to enable large-scale, animal-free production of useful proteins—including the world's first human type II collagen produced in tobacco plants.

- May 2025: Darling Ingredients and Tessenderlo Group announced formation of a new joint company to accelerate growth in collagen-based health, wellness, and nutrition sectors, combining complementary capabilities and market access to expand addressable market opportunities across multiple application segments.

- June 2024: Glanbia Nutritionals launched Collameta high-potency collagen tripeptide ingredient in partnership with Jellice Co., offering 4x faster absorption and 10x efficacy compared to traditional collagen peptides at one-tenth the dosage for enhanced product formulation flexibility.

Asia Pacific Collagen Market Report Scope

Collagen is a major structural protein found in the skin, tendons, and bones of vertebrates and has multiple nutritional, skin, and health benefits.

The Asia-Pacific collagen market is segmented into source, application, and geography. By source, the market is segmented into animal-based collagen and marine-based collagen. By applications, the market is segmented into dietary supplements, meat processing, food, cosmetics & personal care, and other applications, where other applications include beverages, medical care, biomaterial research, and packaging. By geography, the market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific.

The report offers the market size in value terms in USD and volume terms in tons for all the above-mentioned segments.

By Source

| Animal-based |

| Marine-based |

By End User / Application

| Food & Beverages |

| Dietary Supplements |

| Personal Care & Cosmetics |

| Pharmaceuticals |

| Animal Nutrition |

By Geography

| Japan |

| China |

| India |

| Australia |

| Rest of Asia Pacific |

| By Source | Animal-based |

| Marine-based | |

| By End User / Application | Food & Beverages |

| Dietary Supplements | |

| Personal Care & Cosmetics | |

| Pharmaceuticals | |

| Animal Nutrition | |

| By Geography | Japan |

| China | |

| India | |

| Australia | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia Pacific collagen market in 2031?

The region is expected to reach USD 6.02 billion by 2031, up from USD 3.75 billion in 2026.

Which source category is growing fastest in regional collagen demand?

Marine-based collagen is forecast to post a 10.28% CAGR between 2026-2031 due to sustainability and hypoallergenic positioning advantages.

Which country shows the highest growth momentum for collagen products?

India is projected to grow at an 11.38% CAGR, powered by expanding middle-class incomes and preventive-health adoption.

Which application currently generates the largest revenue?

Personal care and cosmetics command the largest share at 41.85% of 2025 regional revenue.

Page last updated on: