Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

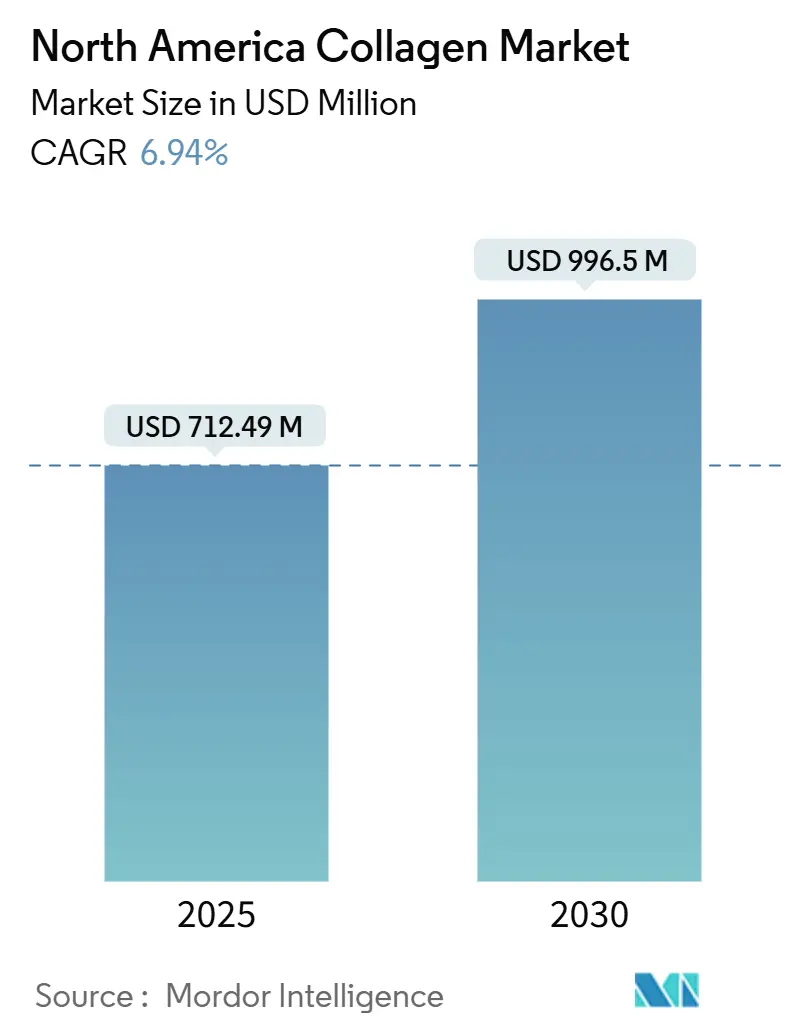

| Market Size (2025) | USD 712.49 Million |

| Market Size (2030) | USD 996.5 Million |

| Growth Rate (2025 - 2030) | 6.94% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Collagen Market Analysis by Mordor Intelligence

The North America collagen market size stood at USD 712.49 million in 2025 and is projected to reach USD 996.5 million by 2030, reflecting a 6.94% CAGR during the forecast period. The expansion traces back to the region’s rising population of adults aged 65 years and older, sustained regulatory support for new dietary ingredients, and steady investments in functional food fortification. Robust consumer awareness around joint mobility, skin health, and postoperative recovery programs further stimulates category penetration across multiple retail channels. Supply-side factors such as integrated slaughterhouse by-product collection, growing marine waste valorization, and fermentation innovation reinforce volume availability while enabling continuous cost optimization. Competitive strategies now emphasize backward integration into raw material streams, branded consumer engagement through e-commerce, and clinical substantiation that earns premium pricing.

Key Report Takeaways

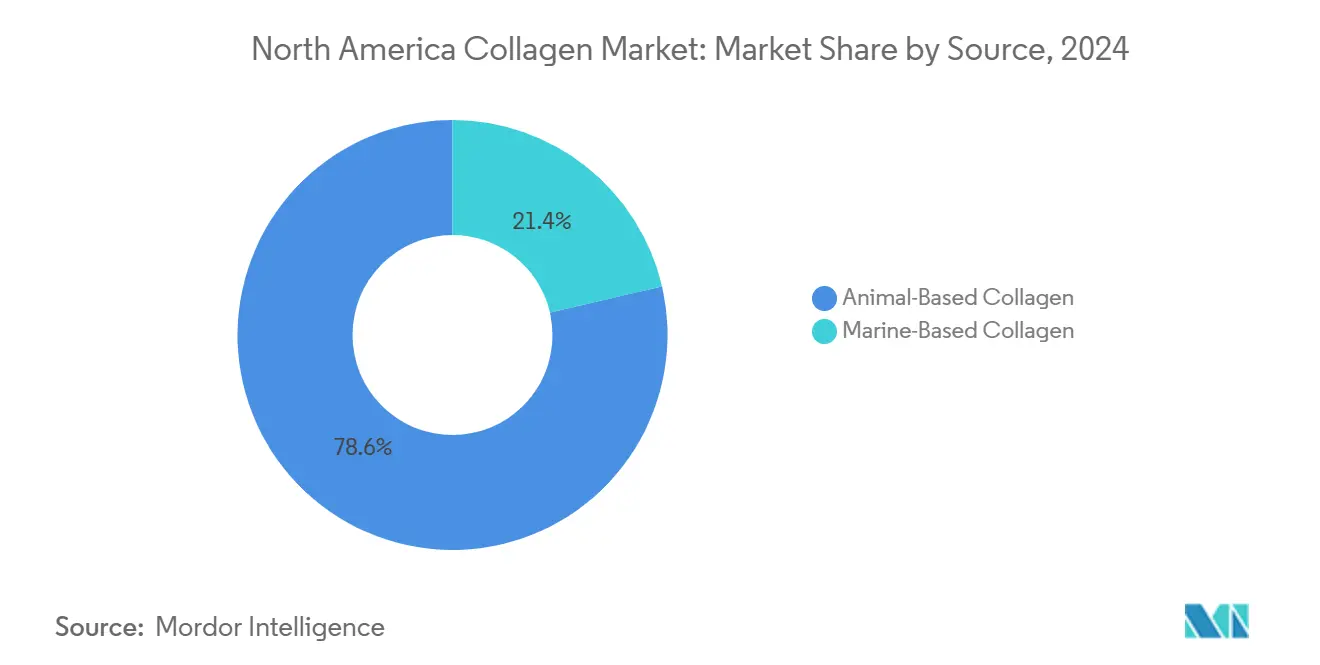

By source, animal-based collagen captured 78.62% of the North America collagen market share in 2024, and Marine collagen is advancing at an 8.2% CAGR through 2030.

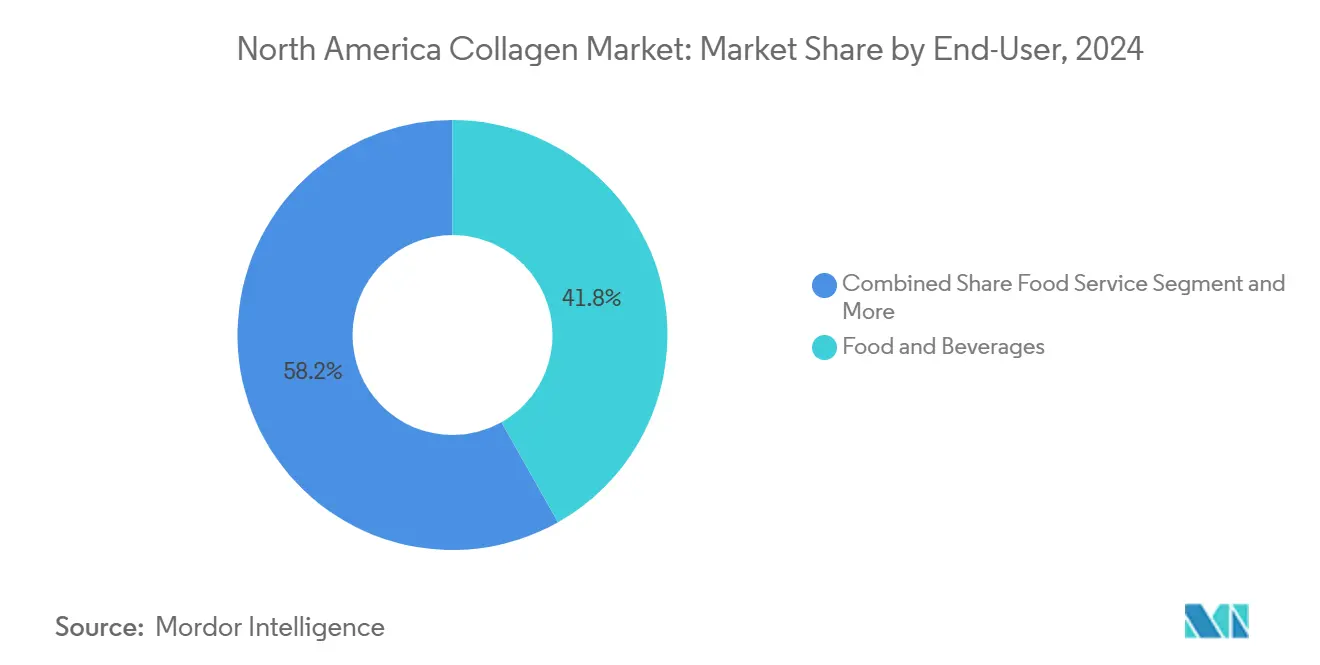

By end-user, food and beverage accounted for 41.84% share of the North America collagen market size in 2024, and Biomedical uses are projected to expand at a 9.73% CAGR to 2030.

By geography, the United States held 73.28% of the North America collagen market size in 2024, and Mexico is tracking the fastest growth at an 8.38% CAGR through 2030.

North America Collagen Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and increasing joint-health focus | 1.2% | North America-wide, concentrated in US and Canada | Long term (≥ 4 years) |

| Surging innovations in nutricosmetic and dietary supplements | 0.8% | US-led with Canadian spillover | Medium term (2-4 years) |

| Functional food and beverage fortification boom | 1.1% | North America-wide, Mexico emerging | Medium term (2-4 years) |

| Clean-label collagen use in meat processing | 0.6% | US and Canada primarily | Short term (≤ 2 years) |

| Sustainable marine collagen from invasive species | 0.4% | Coastal regions, Great Lakes area | Long term (≥ 4 years) |

| Eased Canadian regulatory pathway for peptides | 0.3% | Canada with cross-border implications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Increasing Joint-Health Focus

Demographic fundamentals drive sustained collagen demand as North America's 65-plus population expands by 3.2% annually, creating a cohort predisposed to joint degradation and mobility concerns. The CDC reports 32.5 million US adults currently manage osteoarthritis, with projections indicating 635,000 hip replacements and 1.28 million knee replacements by 2030[1]Centers for Disease Control and Prevention. "Osteoarthritis Data and Statistics." Accessed September 8, 2025. https://www.cdc.gov/arthritis/data_statistics/osteoarthritis.html. Canada's osteoarthritis burden will triple from 4 million to 12 million by 2040, establishing collagen supplementation as a preventive intervention before surgical thresholds. This demographic shift transforms collagen from cosmetic enhancement to medical necessity, supporting premium pricing and insurance reimbursement discussions. The aging cohort's willingness to invest in preventive health measures creates sustained revenue streams independent of economic cycles.

Surging Innovations in Nutricosmetic and Dietary Supplements

Technological advances in peptide bioavailability unlock new consumer segments as companies develop targeted formulations for specific health outcomes. Neutrogena's Collagen Bank utilizes micro-peptide technology for enhanced skin penetration, while BioCell Technology's ERP ingredient has demonstrated measurable improvements in skin hydration in clinical trials. The nutricosmetics category benefits from crossover appeal between beauty and wellness consumers, expanding the total addressable market beyond traditional supplement users. Vital Proteins' launch of colostrum capsules in February 2025 exemplifies category expansion, targeting gut health while maintaining collagen brand equity. Innovation cycles accelerate as brands seek differentiation through novel delivery formats and innovative ingredient combinations.

Functional Food and Beverage Fortification Boom

Collagen integration into mainstream food products removes consumption barriers while expanding market reach beyond supplement-conscious consumers. Pretty Tasty's collagen-infused tea and Collagenx's marine collagen energy drinks demonstrate successful product diversification that captures impulse purchases and routine consumption patterns. Food manufacturers leverage collagen's clean-label positioning to enhance protein content without artificial additives, addressing consumer demand for recognizable ingredients. The functional beverage segment particularly benefits from collagen's neutral taste profile and mixability, enabling incorporation into existing product lines without reformulation challenges. Retail placement in beverage aisles rather than supplement sections increases consumer exposure and trial rates.

Clean-Label Collagen Use in Meat Processing

Meat processors adopt collagen as a natural binding agent and protein enhancer, replacing synthetic additives while improving nutritional profiles. Devro and ViskoTeepak's collagen casings enable clean-label claims for processed meats, while Nitta Casings develops specialized applications for premium sausage products. This application leverages existing meat processing infrastructure and supplier relationships, reducing adoption friction compared to new ingredient categories. Clean-label positioning commands premium pricing while addressing consumer concerns about artificial preservatives and binding agents. The meat processing application also provides volume stability for collagen suppliers, balancing the seasonal fluctuations common in supplement markets.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bovine supply volatility (disease risk) | -0.9% | US and Canada cattle regions | Short term (≤ 2 years) |

| Rise of vegan/plant-based alternatives | -0.5% | Urban centers, West Coast concentration | Medium term (2-4 years) |

| FDA draft heavy-metal limits raising costs | -0.4% | US manufacturing facilities | Short term (≤ 2 years) |

| Mexico cold-chain gaps for marine collagen | -0.3% | Mexico, cross-border trade | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bovine Supply Volatility (Disease Risk)

BSE concerns and regulatory restrictions on specified risk materials create supply chain vulnerabilities that threaten cost stability and production continuity. ANSES guidance from April 2024 reinforces precautionary measures for collagen and gelatin production, while FDA and USDA restrictions on bovine materials over certain ages limit raw material availability[2]ANSES. "ANSES Issues Guidance on BSE Precautions for Collagen/Gelatin." April 2024. https://www.anses.fr/en/content/anses-issues-guidance-bse-precautions-collagen-gelatin-april-2024. Darling Ingredients' SEC filings reveal supply chain concentration risks, with top 10 suppliers accounting for 36% of raw materials, creating potential bottlenecks during disease outbreaks. Raw material competition from the expanding biofuel industry further constrains bovine by-product availability, driving cost inflation that pressures margin-sensitive applications. Supply diversification toward marine and synthetic sources becomes a strategic necessity rather than a preference.

Rise of Vegan/Plant-Based Alternatives

Fermentation-based and plant-derived collagen alternatives challenge traditional animal-sourced products, particularly among environmentally conscious consumers in urban markets. VeCollal's biomimetic vegan collagen and Vegetology's Vollagen amino acid complex demonstrate the technical feasibility of plant-based alternatives that replicate collagen's functional benefits[3]TCI Bio. "VeCollal® a Vegan Collagen Alternative." March 4, 2025. https://www.tci-bio.com/technology/vecollal/. These alternatives target the 6% of North American consumers following plant-based diets while appealing to flexitarians concerned about animal welfare and environmental impact. Vegan alternatives currently command premium pricing due to production complexity, but scaling manufacturing could achieve cost parity with animal-derived products. The threat intensifies as major food companies invest in alternative protein technologies and consumer acceptance of novel ingredients increases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Innovation Challenges Bovine Dominance

Animal-based collagen maintains 78.62% market share in 2024, leveraging North America's position as the world's largest beef producer to enable cost-effective mass production of bovine collagen peptides. The segment benefits from established supply chains, processing infrastructure, and consumer familiarity with bovine-derived supplements, while porcine and poultry sources provide alternative options for specific dietary requirements. Bovine collagen's amino acid profile closely matches human collagen composition, supporting efficacy claims for joint health and skin benefits that drive consumer adoption. However, supply chain concentration creates vulnerability to disease outbreaks and regulatory changes, as evidenced by ANSES guidance reinforcing BSE precautionary measures for collagen production. The segment's dominance faces pressure from sustainability concerns and religious dietary restrictions that limit market expansion.

Marine-based collagen emerges as the fastest-growing segment, driven by sustainability initiatives that convert fish processing waste and invasive species into premium peptides with superior bioavailability profiles. DeepMarine's Canadian operations and Ajinomoto's Indigo Marine Collagen demonstrate successful commercialization of North Atlantic fish waste, while jellyfish-derived collagen from Certified Nutraceuticals targets brain health applications through unique amino acid compositions. Marine sources command premium pricing due to perceived purity and environmental benefits, offsetting higher processing costs and supply chain complexity. The segment benefits from regulatory support for sustainable sourcing and growing consumer awareness of ocean conservation issues.

By End-User: Biomedical Applications Accelerate Beyond Food Dominance

Food and beverage manufacturers captured 41.84% market share in 2024, leveraging collagen's neutral taste profile and clean-label positioning to enhance protein content across diverse product categories. The segment encompasses dietary supplements, functional foods and beverages, and meat processing applications, with companies like Pretty Tasty and Collagenx demonstrating successful product diversification into mainstream consumer goods. Retail placement in food aisles rather than supplement sections increases consumer exposure and trial rates, while functional beverage integration captures impulse purchases and routine consumption patterns. The segment's growth depends on continued innovation in delivery formats and combination ingredients that expand appeal beyond traditional supplement users.

Biomedical applications represent the fastest-growing end-user segment at 9.73% CAGR through 2030, driven by expanding adoption in wound care and tissue engineering applications where collagen's biocompatibility and regenerative properties provide clinical advantages. Advanced wound dressings incorporating collagen peptides demonstrate superior healing outcomes compared to traditional materials, while tissue engineering applications leverage collagen scaffolds for organ repair and regeneration. Clinical validation studies support reimbursement discussions with healthcare payers, potentially transforming collagen from consumer supplement to medical device component. The segment benefits from aging demographics that increase demand for advanced wound care solutions and surgical interventions requiring tissue repair materials.

Geography Analysis

North America's collagen market showcases distinct demographic and infrastructural nuances across its three key players. The U.S., bolstered by a vast beef infrastructure and well-established pharmacy and grocery supplement sectors, stands out as the dominant force. With 32.5 million adults grappling with osteoarthritis, the demand is evident. Furthermore, the U.S. sees a flourishing of direct-to-consumer models, thanks to widespread internet access and secure payment systems. This environment has birthed subscription-based programs, effectively evening out revenue fluctuations throughout the year. While Canada may not boast the largest market value, its regulatory decisions wield significant influence. A case in point: Health Canada's nod to VERISOL peptides in 2025 not only validated certain skin-health assertions but also catalyzed a wave of investments from global suppliers into thorough clinical trials. Meanwhile, processors along Canada's coasts are turning the region's plentiful salmon and cod by-products into marine peptides. These products, enjoying tariff-free passage into the U.S., bolster regional supply security.

Mexico stands at the cusp of a burgeoning opportunity. The introduction of pharmaceutical-grade cold storage facilities is a game-changer, ensuring the delicate logistics of marine collagen are met with precision. Retail pharmacy chains are now placing single-serve collagen sachets at checkout counters, positioning them as impulse buys, akin to energy shots. With public-sector campaigns spotlighting musculoskeletal health, households are increasingly willing to invest in preventive supplementation. Additionally, Mexico's geographical proximity to U.S. manufacturing plants reduces freight costs and fosters co-packing arrangements, effectively shortening lead times and enhancing supply chain efficiency

Competitive Landscape

In North America, a handful of vertically integrated players dominate the collagen market, overseeing everything from raw material sourcing and hydrolysis to branded consumer distribution. Gelita, with its multi-species extraction sites, has bolstered its marine line share as a buffer against bovine market fluctuations. Meanwhile, Darling Ingredients is streamlining operations by directly channeling hides and bones from its rendering arm's slaughterhouse sources into high-purity peptide production. In a strategic move, the company joined forces with Tessenderlo Group in May 2025, merging their raw material scale with European processing expertise to fast-track their North American growth. Emerging mid-tier players are leveraging recombinant technology to produce animal-free collagen alternatives. By licensing strain libraries and outsourcing fermentation to bio-manufacturers, they sidestep the hefty investments typically required for extraction facilities. Collaborations with beverage firms not only pave their market entry but also secure offtake agreements, mitigating risks associated with scaling up. To stand out, these brands emphasize traceable sourcing, clinical validation, and innovative, convenient product formats.

Recent patenting trends highlight advancements in enzymatic fractionation for precise bioactivity and encapsulation methods that enhance stability during ultra-high-temperature beverage processing. Brands harness e-commerce insights for optimal bundle pricing and replenishment timings, with loyalty initiatives boosting repeat purchases to over 60%. Sustainability is a key focus, with brands showcasing their commitment through carbon-footprint labels, recycled packaging efforts, and contributions to third-party ocean clean-up projects.

North America Collagen Industry Leaders

-

Nitta Gelatin, NA Inc.

-

Weishardt

-

Tessenderlo Group

-

Gelita AG

-

Darling Ingredients Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Darling Ingredients announced a joint venture with Tessenderlo Group to accelerate expansion in the collagen-based health, wellness, and nutrition sector. The partnership combines Darling's raw material sourcing capabilities with Tessenderlo's processing expertise to enhance market position in North America and globally.

- February 2024: Evonik has launched Vecollage™ Fortify L, a biotech-based vegan collagen ingredient for the beauty and personal care market that is identical to the collagen found in human skin. Developed through fermentation technology in partnership with Modern Meadow Inc., Vecollage™ Fortify L offers dual benefits by preventing age-related collagen degradation and stimulating the skin’s own collagen production.

North America Collagen Market Report Scope

By source, North Americacollagen market is segmented as animal-based collagen and marine-based collagen. By applications, the market is segmented as dietary supplements, meat processing, food, cosmetics & personal care, and other applications, where other applications includebeverages, medical care, biomaterial research,and packaging.

By Source

| Animal-based Collagen | Bovine |

| Porcine | |

| Poultry | |

| Marine-based Collagen | Fish Skin & Scales |

| Jellyfish |

By End-User Industry

| Food and Beverage Manufacturers | Dietary Supplements |

| Functional Foods and Beverages | |

| Meat Processing and Analogues | |

| Biomedical | |

| Cosmetics and Personal Care | |

| Food Service |

By Country

| United States of America |

| Canada |

| Mexico |

| Rest of North America |

| By Source | Animal-based Collagen | Bovine |

| Porcine | ||

| Poultry | ||

| Marine-based Collagen | Fish Skin & Scales | |

| Jellyfish | ||

| By End-User Industry | Food and Beverage Manufacturers | Dietary Supplements |

| Functional Foods and Beverages | ||

| Meat Processing and Analogues | ||

| Biomedical | ||

| Cosmetics and Personal Care | ||

| Food Service | ||

| By Country | United States of America | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the projected value of the North America collagen market in 2030?

It is forecast to reach USD996.5 million by 2030, reflecting a 6.94% CAGR between 2025 and 2030.

Which source segment is growing fastest in the region?

Marine collagen is expanding at an 8.2% CAGR as processors upcycle fish waste and invasive species into high-purity peptides.

How large is the food and beverage share within the regional collagen space?

Food and beverage applications accounted for 41.84% of 2024 revenue, making them the leading end-user category.

What key regulatory change impacted collagen marketing claims in 2025?

Health Canada’s approval of VERISOL peptides with verified skin-health benefits created a benchmark for evidence-based labeling across the continent.

Page last updated on: