Nasal Polyps Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

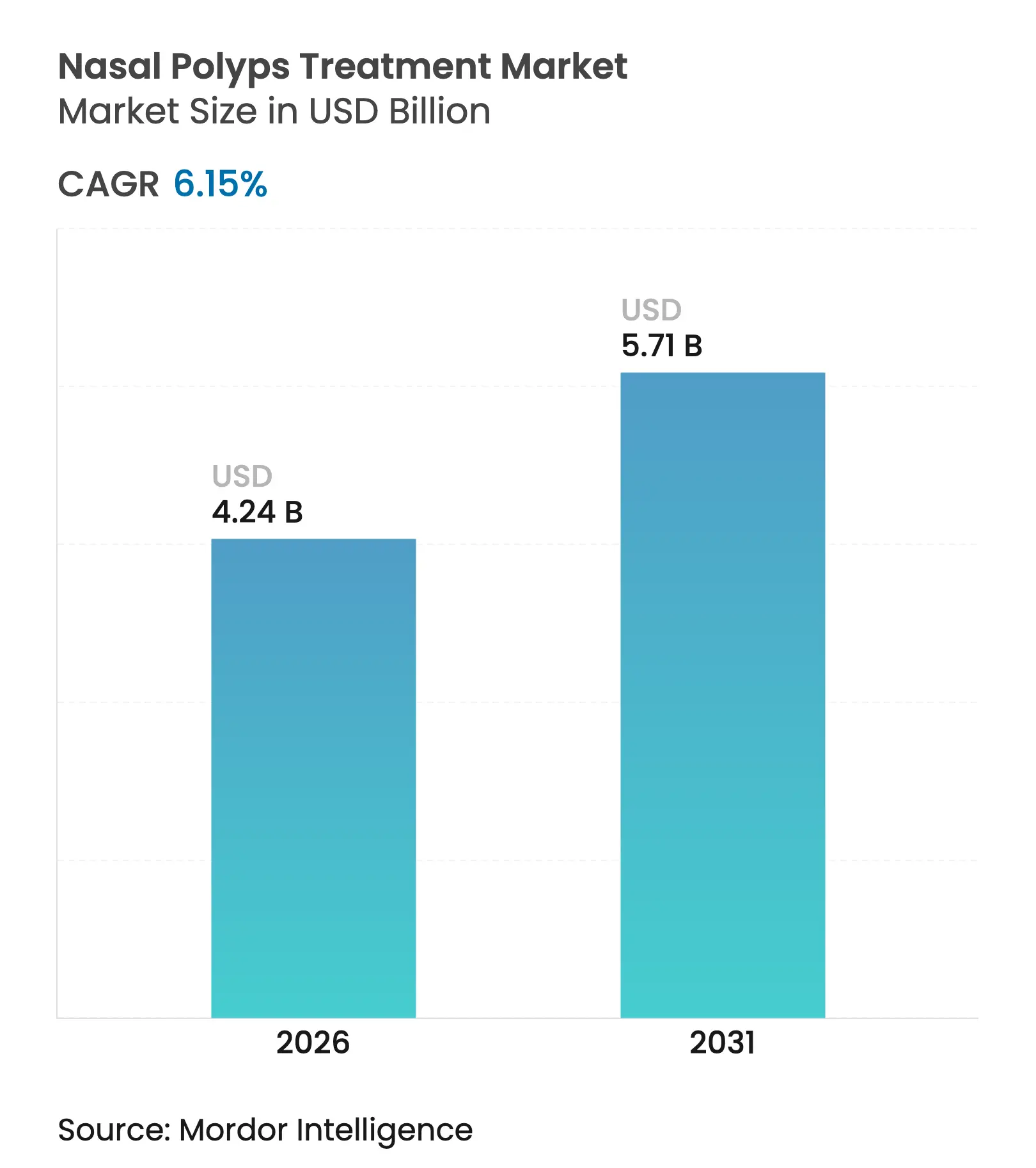

| Market Size (2026) | USD 4.24 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 6.15 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Nasal Polyps Treatment Market Analysis by Mordor Intelligence

The nasal polyps treatment market size is expected to grow from USD 3.99 billion in 2025 to USD 4.24 billion in 2026 and is forecast to reach USD 5.71 billion by 2031 at 6.15% CAGR over 2026-2031. Demand is rising as physicians shift from broad corticosteroid use toward precision biologics that interrupt interleukin-4, -5 and -13 signaling pathways. Growth is reinforced by the high coexistence of asthma and chronic rhinosinusitis with nasal polyps (CRSwNP), the expansion of fast-track biologic approvals, and steady uptake of minimally invasive delivery systems that improve intranasal drug deposition. Competition intensifies as large pharmaceutical groups protect market positions through life-cycle management and co-promotion agreements, while smaller biotechnology companies target under-served patient segments through differentiated mechanisms of action. Digital pharmacy channels, broader ENT specialist networks, and favorable reimbursement pilots in developed markets further expand patient access, although cost containment policies in price-sensitive regions remain a headwind.

Key Report Takeaways

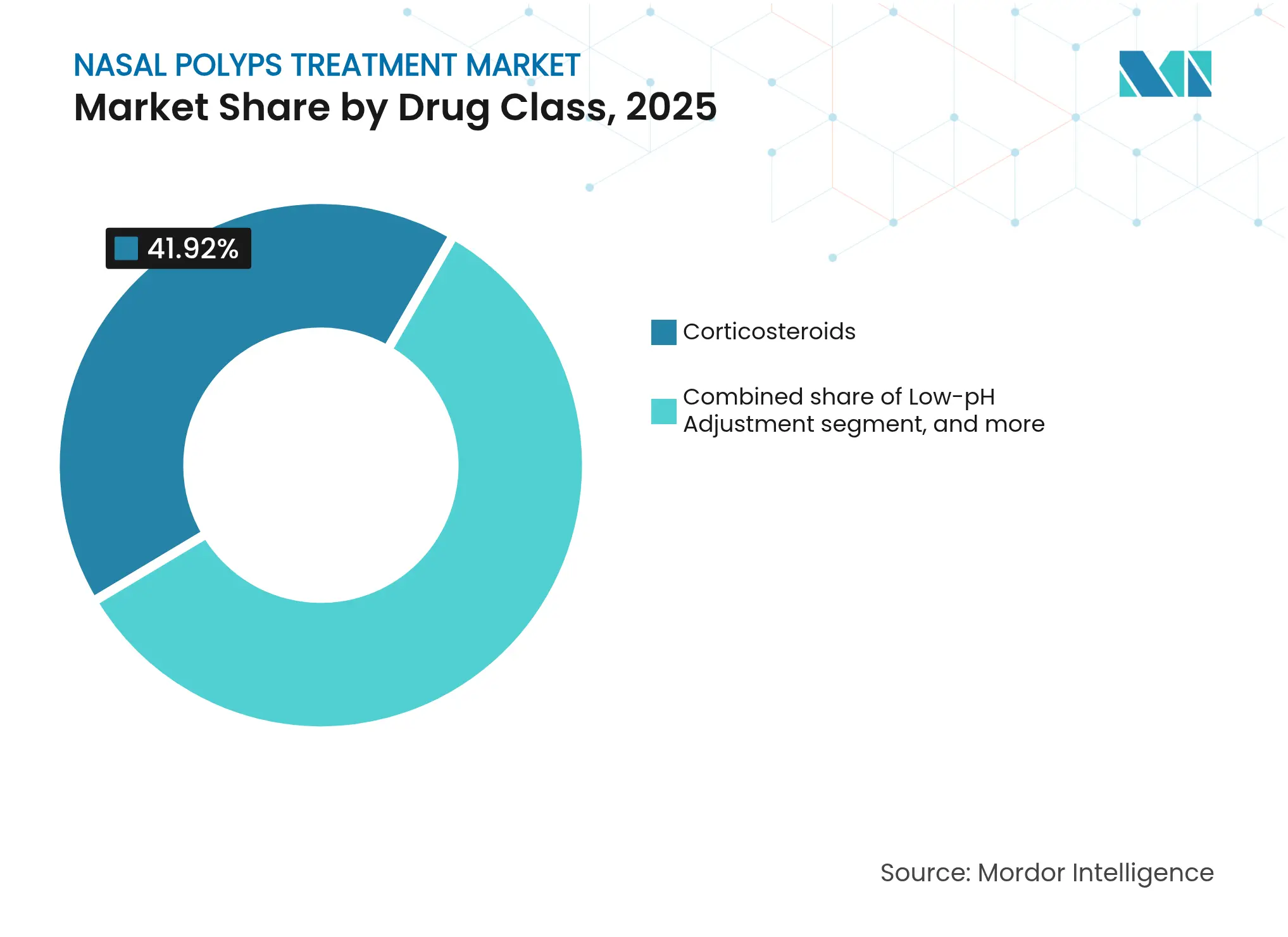

- By drug class, corticosteroids led with 41.92% of the nasal polyps treatment market share in 2025, while the biologics-dominated “Other Drug Class” segment is projected to expand at an 8.22% CAGR through 2031.

- By route of administration, nasal sprays commanded 48.01% revenue share in 2025; exhalation delivery systems are forecast to grow at an 8.35% CAGR over the same period.

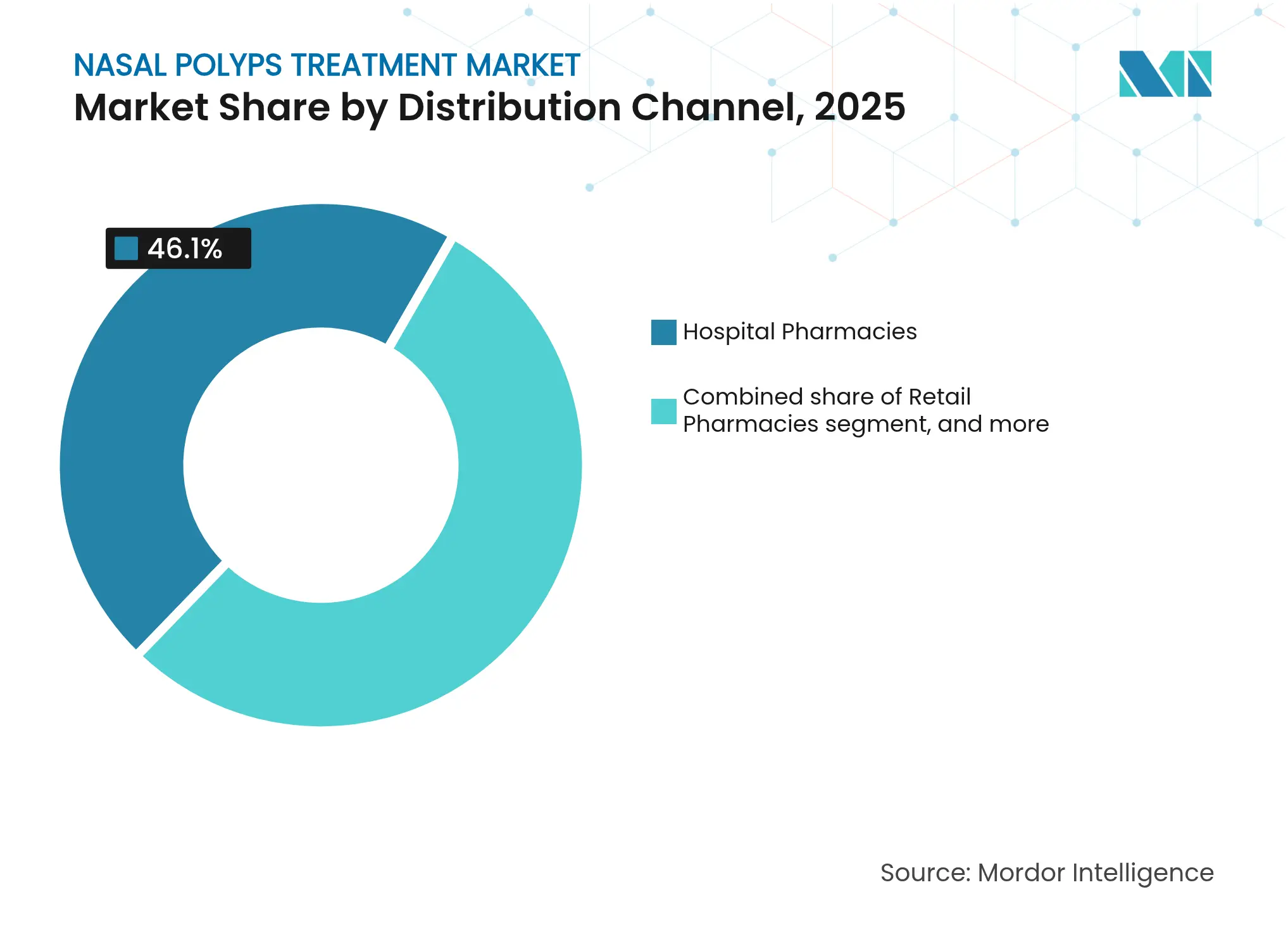

- By distribution channel, hospital pharmacies held 46.10% share of the nasal polyps treatment market size in 2025, whereas online pharmacies are set to rise at a 9.08% CAGR to 2031.

- By end user, hospitals accounted for 50.74% share in 2025, with ENT clinics advancing at a 9.21% CAGR on the back of specialized diagnostics.

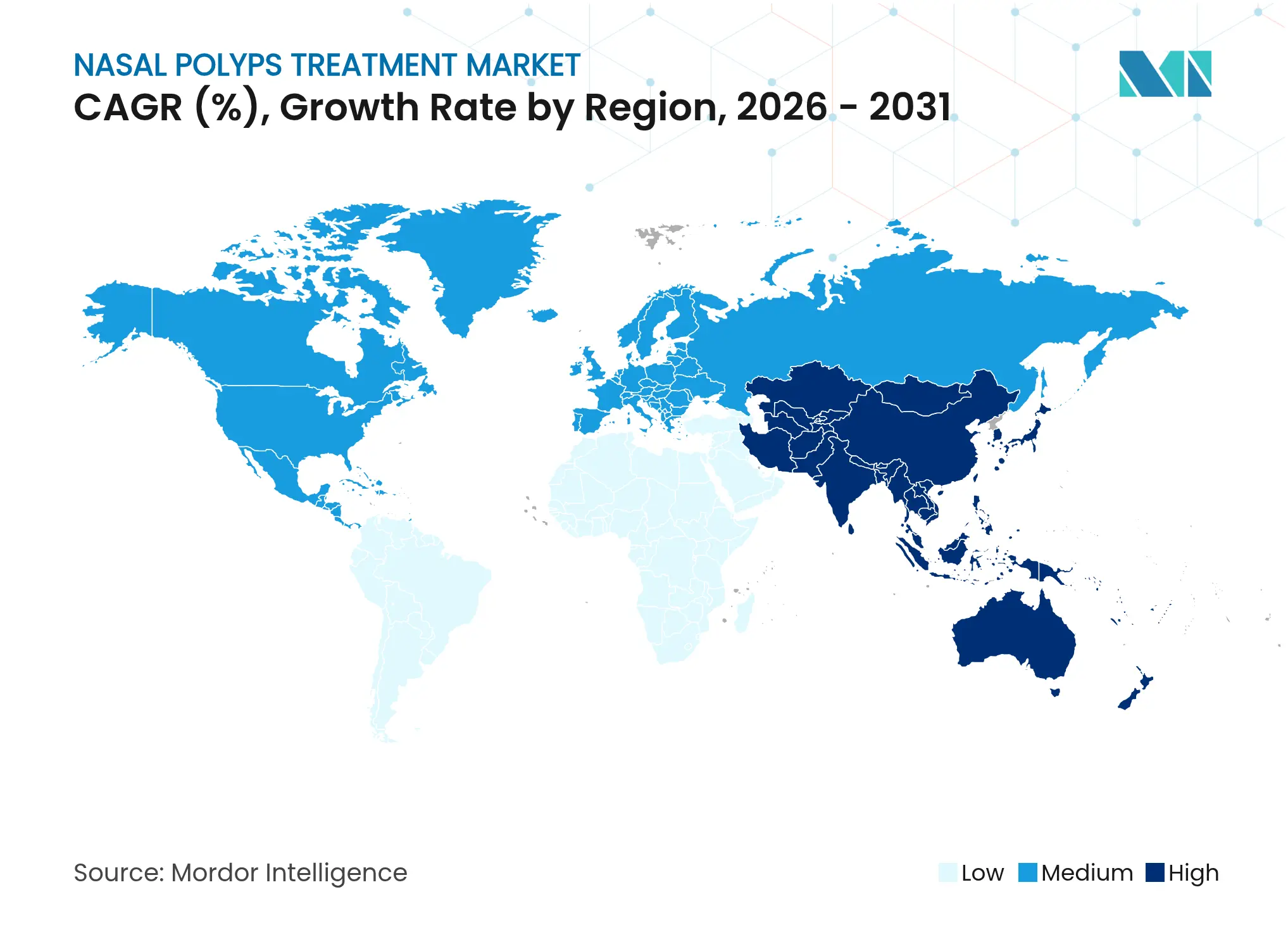

- By geography, North America contributed 42.02% market share in 2025, while Asia-Pacific is the fastest-growing region at a 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nasal Polyps Treatment Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing prevalence of chronic rhinosinusitis with nasal polyps Growing prevalence of chronic rhinosinusitis with nasal polyps | +1.8% | Global (highest in North America & Europe) | Medium term (2-4 years) | % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global (highest in North America & Europe) | Impact Timeline:Medium term (2-4 years) |

Increasing adoption of biologic therapies in treatment protocols Increasing adoption of biologic therapies in treatment protocols | +2.1% | North America & EU leading, APAC emerging | Short term (≤ 2 years) | |||

Rising healthcare expenditure and access to ENT surgical care Rising healthcare expenditure and access to ENT surgical care | +1.2% | Asia-Pacific core, spill-over to Middle East & Africa | Long term (≥ 4 years) | |||

Favorable regulatory approvals and fast-track designations for novel drugs Favorable regulatory approvals and fast-track designations for novel drugs | +1.4% | Global, with regulatory precedence in US & EU | Short term (≤ 2 years) | |||

Expansion of Tele-ENT consultations and remote prescription fulfillment Expansion of Tele-ENT consultations and remote prescription fulfillment | +0.9% | North America & Asia-Pacific | Short term (≤ 2 years) | |||

Integration of AI-based diagnostic tools enhancing early detection rates Integration of AI-based diagnostic tools enhancing early detection rates | +1.0% | North America & Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Prevalence of Chronic Rhinosinusitis With Nasal Polyps

Global CRSwNP prevalence is climbing as environmental pollutants, urban allergens, and ageing populations converge, raising disease incidence to roughly 4% of adults worldwide[1]American Academy of Allergy, Asthma & Immunology, “Rhinosinusitis Prevalence and Asthma Comorbidity,” aaaai.org. Diagnosis rates improve in developed markets thanks to widespread endoscopic screening, but limited ENT capacity in emerging regions delays detection. About 60% of CRSwNP patients also have asthma, compounding morbidity and increasing the need for combination therapies that deliver longer-lasting symptom remission. North American and European payers already recognize the economic burden of recurrent surgeries and systemic steroid use, prompting policy discussions around earlier biologic intervention. In Asia-Pacific, rapid industrial expansion intensifies air-quality issues, which, together with the build-out of tertiary hospitals, is generating a pronounced uptick in patient volumes.

Increasing Adoption of Biologic Therapies in Treatment Protocols

Targeted biologics such as dupilumab, tezepelumab, and stapokibart ease nasal obstruction, reduce polyp grade, and lower surgery rates, prompting guideline updates that prioritize their use in refractory CRSwNP. Dupilumab’s 2024 adolescent approval broadened the eligible U.S. cohort by about 9,000 patients, while tezepelumab’s Phase III WAYPOINT trial reported a 98% cut in surgical interventions, positioning it as a competitive benchmark. Physicians increasingly combine biologics with topical corticosteroids to consolidate control, and payers reward documented improvements in work productivity and reduced emergency visits. China’s stapokibart authorization in 2024 signaled a strategic move toward local innovation, setting the stage for wider Asia-Pacific penetration of premium biologics. Ongoing head-to-head trials will likely refine positioning by endotype, driving incremental share shifts within the biologics segment.

Rising Healthcare Expenditure and Access to ENT Surgical Care

Asia-Pacific medical technology spend is forecast to reach USD 140 billion in 2025, equipping hospitals with advanced endoscopes, navigation systems, and postoperative care platforms. However, India still fields only one ENT surgeon per 28,000 residents, underlining resource gaps that favor non-surgical biologic routes. Tele-ENT services mitigate distance barriers and feed digital prescription channels that ship maintenance sprays direct to homes. Meanwhile, global otorhinolaryngology device sales, at USD 13.99 billion in 2026, illustrate healthy capital expenditure on minimally invasive instruments that shorten operating times and accelerate recovery. This dual investment in surgery and medical management broadens the therapeutic toolkit and sustains overall market expansion.

Favorable Regulatory Approvals and Fast-Track Designations for Novel Drugs

Regulators have accelerated review pathways to close the treatment gap in CRSwNP, granting fast-track and breakthrough tags to multiple monoclonal antibodies. GSK’s depemokimab received FDA submission acceptance in March 2025, underscoring momentum around IL-5 blockade. The March 2024 approval of XHANCE for chronic rhinosinusitis without nasal polyps created a precedent for label expansion in adjacent rhinosinusitis phenotypes. Harmonization between FDA, EMA and China’s NMPA lowers duplicative trial requirements, speeding global launches. Pediatric indications command high public-health priority and further justify priority review vouchers, effectively shortening time-to-market and maintaining the innovation cycle.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High treatment costs and limited reimbursement for biologics High treatment costs and limited reimbursement for biologics | -1.6% | Global (strongest in emerging markets) | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.6% | Geographic Relevance:Global (strongest in emerging markets) | Impact Timeline:Medium term (2-4 years) |

Stringent regulatory and safety requirements for nasal implants Stringent regulatory and safety requirements for nasal implants | -0.8% | United States & European Union | Long term (≥ 4 years) | |||

Low awareness and diagnosis rates in emerging markets Low awareness and diagnosis rates in emerging markets | -1.1% | Africa, South Asia & Latin America | Medium term (2-4 years) | |||

Competition from alternative therapies and over-the-counter remedies Competition from alternative therapies and over-the-counter remedies | -0.7% | North America & Europe | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Treatment Costs and Limited Reimbursement for Biologics

Annual dupilumab therapy exceeds USD 30,000 in the United States, placing pressure on commercial payers to deploy prior-authorization hurdles that elongate treatment timelines[2]Tufts Medical Center Institute for Clinical and Economic Review, “Coverage Policies for Biologics in CRSwNP,” tuftsmedicalcenter.org. Cost-effectiveness studies show biologics outperform systemic steroids in quality-adjusted life-years, yet budget impact for health plans remains substantial, particularly when layered on top of expanding specialty drug pipelines. In lower-middle-income economies, biologic usage is often limited to self-pay urban elites, widening equity gaps. Biosimilar entry after 2028 may ease price tension, but payers will still negotiate steep rebates to curb specialty spending growth. Ancillary costs, including injection training and pharmacovigilance, further complicate universal coverage in stewardship-driven reimbursement systems.

Stringent Regulatory and Safety Requirements for Nasal Implants

Implantable corticosteroid or absorbable scaffold devices must prove biocompatibility, non-migration, and long-term mucosal safety in heterogeneous anatomies, extending development timelines. FDA post-market surveillance rules add incremental cost layers for smaller device innovators, often diverting resources toward orthopedic or cardiovascular programs with clearer reimbursement uplifts. Divergent EU MDR clauses around reusable device reprocessing and traceability complicate pan-European rollouts. Manufacturing controls demand high-purity polymer inputs and particle-free cleanrooms, resulting in steep fixed costs that dissuade new entrants. Consequently, pipeline activity tilts toward drug-device combination sprays that face a more predictable regulatory path, delaying adoption of high-potential implants in many regions.

Segment Analysis

By Drug Class: Biologics Drive Premium Segment Growth

Corticosteroids retained 41.92% share of the nasal polyps treatment market in 2025 on the back of favorable pricing and wide prescriber familiarity. Yet biologic therapies within the “Other Drug Class” bracket are expanding at an 8.22% CAGR, propelled by robust real-world effectiveness and multi-cohort label extensions. Antibiotic usage is falling as mechanistic focus shifts from infectious to type 2 inflammatory drivers. Leukotriene modifiers remain niche, serving patients with comorbid asthma yet limited standalone benefit in polyp regression.

The competitive tide is evident in hospital formularies, where biologic utilization in high-surgery-risk cohorts is rising quarter-on-quarter. Dupilumab’s adolescent indication, tezepelumab’s near-approval status, and China’s stapokibart launch intensify attention on disease-modifying results that reduce revision surgeries and cumulative systemic steroid exposure. Payer scrutiny is tightening but long-term cost offsets from fewer operating-room episodes and productivity gains strengthen the biologic value narrative. Post-2028 biosimilar waves should gradually unlock fuller access while sustaining innovation incentives for next-generation cytokine targets.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Targeted Delivery Systems Gain Traction

Nasal sprays delivered 48.01% revenue share in 2025, benefiting from patient-friendly formats and over-the-counter steroid options that manage mild-to-moderate symptoms. Exhalation delivery systems, led by XHANCE’s closed-palate mechanism, are on track for an 8.35% CAGR by 2031 as studies confirm deeper sinus penetration and better polyp shrinkage scores. Oral and injectable routes remain relevant for systemic treatments, especially during acute exacerbations or for biologic dosing every 2–8 weeks. Implantable devices, exemplified by SINUVA and LATERA, occupy an early-adopter niche awaiting further long-term safety data.

Emerging solutions combine handheld battery-assisted atomizers with sensors that log dosing compliance to cloud portals, supporting remote physician oversight. Stryker’s LATERA absorbable implant reportedly saves USD 2,200 per patient compared with functional endoscopic sinus surgery in suitable lateral wall collapse cases. Uptake of such implants remains country-specific, hinging on specialist skill sets and reimbursement scheduling. As device makers refine ergonomics and integrate digital guidance, payers may favor these technologies for their potential to lower intensive surgical episodes.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies represented 46.10% of the nasal polyps treatment market size in 2025, reflecting centralized biologic inventories, cold-chain controls, and immediate post-infusion monitoring services. Online pharmacies are growing at a 9.08% CAGR, underpinned by e-prescription laws and patient expectations for doorstep specialty medication delivery with adherence apps. Retail chains hold steady volumes via intranasal sprays, while specialty clinics increasingly manage biologic dispensing under coordinated care agreements.

Health systems integrate tele-ENT consultation portals, enabling remote diagnosis, e-consult coding, and synchronized pharmacy shipments, especially across rural catchments in Asia-Pacific. National regulators now allow electronic prior authorizations and temperature-controlled courier models, sustaining biological integrity to the patient’s refrigerator. Pharmacy benefit managers expand nurse-navigator programs for biologic titration, supporting home-administration paradigms that lower infusion-center overheads and broaden regional reach.

Note: Segment shares of all individual segments available upon report purchase

By End User: ENT Clinics Emerge as Specialized Care Centers

Hospitals accounted for 50.74% revenue share in 2025, backed by superior imaging suites, integrated surgical theaters, and multidisciplinary allergy-pulmonology collaboration. ENT clinics are the fastest, at a 9.21% CAGR, as high-definition endoscopes, cone-beam CT scanners, and biologic inventory financing give single-specialty centers comparable capabilities at lower fixed-cost bases. Ambulatory surgery centers add volume for less complex procedures, such as polypectomy with balloon sinuplasty, while home care garners interest for biologic maintenance in stable patients.

The Global Otolaryngology-Head and Neck Surgery Initiative’s equipment minimums empower emerging-market clinics to perform reliable diagnostics, thereby capturing patient loyalty. AI-driven decision-support platforms filter endoscopic images to grade polyp severity and recommend evidence-based treatment plans, raising clinic throughput. Pay-for-performance models tie reimbursement to patient-reported outcomes, rewarding centers that minimize repeat surgeries and systemic steroid bursts, thus favoring specialized ENT environments.

Geography Analysis

North America led the nasal polyps treatment market in 2025 with 42.02% share, underpinned by strong prescribing of FDA-cleared biologics, widespread insurance coverage for specialty drugs, and active patient advocacy groups that facilitate early diagnosis. The United States accounts for the bulk of regional revenue, leveraging real-time benefits checks and manufacturer copay programs that offset high list prices. Canada’s provincial drug plans steadily add biologics to formularies following health-technology assessments, while Mexico’s growing private insurance pool is accelerating corticosteroid spray and balloon sinuplasty uptake. Ongoing payer negotiations create heterogeneous access, yet steady commercial uptake has cemented the region’s leadership.

Europe shows balanced growth, supported by centralized EMA reviews that streamline multinational launches. Germany and the United Kingdom anchor clinical research networks and employ stringent cost-effectiveness thresholds, accelerating tender competition and risk-sharing contracts for biologic reimbursement. France and Italy benefit from specialist training programs and universal coverage, keeping surgery queues short and biologic adoption steady. Spain, with upgraded tertiary ENT hubs and improving macroeconomics, is emerging as a significant volume contributor. EU aging demographics and stringent workplace wellness mandates sustain long-term demand.

Asia-Pacific is projected to achieve the fastest 7.18% CAGR through 2031 as healthcare spending expands, infrastructure modernizes, and patient awareness rises. China’s stapokibart approval marked a milestone in domestic innovation and opened the door for locally produced monoclonals at regionally competitive price points. Japan’s robust innovation funding and single-payer insurance framework support high biologic penetration, while Australia and South Korea mirror Western adoption curves. India’s ENT workforce shortfall remains a constraint, though tele-medicine and policy emphasis on noncommunicable diseases could unlock latent demand later this decade. Urban–rural disparities will persist, but incremental expansion of public hospital capacity and private insurance penetration is set to widen treatment access.

Competitive Landscape

Market Concentration

The nasal polyps treatment market is moderately concentrated, with the top five biopharma players collectively responsible for more than 60% of segment revenue. Sanofi-Regeneron’s dupilumab maintains first-mover advantages through broad age-range indications, real-world evidence, and physician familiarity. AstraZeneca-Amgen’s tezepelumab has demonstrated exceptional surgery-avoidance efficacy, potentially shifting prescribing for severe CRSwNP cases once approved. GSK’s depemokimab aims to exploit IL-5 biology, while Keymed Biosciences represents regional challenger momentum following stapokibart’s Chinese launch.

Litigation over cytokine patent breadth and profit-sharing arrangements, as seen in Regeneron-Sanofi transparency disputes, underscores the strategic stakes. Device makers, including Stryker, Medtronic, and Acclarent (now part of Integra LifeSciences), compete on absorbable implants and navigation platforms that complement pharmacotherapy. Integra’s USD billion-sized ENT portfolio acquisition cements its presence in sinus surgery consumables. Partnership models—such as co-promotions between biologic firms and diagnostics startups that supply rapid-assay biomarker kits—illustrate convergence across therapeutics, devices, and digital health. Real-world studies comparing surgery-first versus biologic-first sequencing will likely dictate competitive share allocations in the next five years.

Nasal Polyps Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GSK received FDA acceptance of depemokimab applications for asthma with type 2 inflammation and CRSwNP, reinforcing the IL-5 pathway race.

- March 2025: AstraZeneca and Amgen announced that TEZSPIRE met all primary endpoints in the Phase III WAYPOINT trial, cutting surgery need by 98% and strengthening tezepelumab’s clinical positioning.

- January 2025: Lyra Therapeutics reported positive safety and efficacy results for LYR-210 in a Phase 3 extension study for chronic rhinosinusitis, demonstrating sustained benefits beyond 32 weeks.

- December 2024: Keymed Biosciences gained Chinese NMPA approval for stapokibart, extending IL-4Rα blockade options in Asia.

- September 2024: Sanofi secured FDA approval to extend dupilumab to adolescents aged 12–17 with CRSwNP, enlarging the U.S. treatable population.

Table of Contents for Nasal Polyps Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope Of The Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Prevalence of Chronic Rhinosinusitis With Nasal Polyps

- 4.2.2Increasing Adoption of Biologic Therapies In Treatment Protocols

- 4.2.3Rising Healthcare Expenditure and Access to ENT Surgical Care

- 4.2.4Favorable Regulatory Approvals and Fast-Track Designations For Novel Drugs

- 4.2.5Expansion of Tele-ENT Consultations and Remote Prescription Fulfillment

- 4.2.6Integration of AI-Based Diagnostic Tools Enhancing Early Detection Rates

- 4.3Market Restraints

- 4.3.1High Treatment Costs and Limited Reimbursement for Biologics

- 4.3.2Stringent Regulatory and Safety Requirements For Nasal Implants

- 4.3.3Low Awareness and Diagnosis Rates in Emerging Markets

- 4.3.4Competition From Alternative Therapies and Over-The-Counter Remedies

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat Of New Entrants

- 4.5.2Bargaining Power Of Buyers

- 4.5.3Bargaining Power Of Suppliers

- 4.5.4Threat Of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Drug Class

- 5.1.1Corticosteroids

- 5.1.2Antibiotics

- 5.1.3Leukotriene Inhibitors

- 5.1.4Other Drug Class

- 5.2By Route Of Administration

- 5.2.1Nasal Sprays

- 5.2.2Oral Tablets & Suspensions

- 5.2.3Injectable / IV

- 5.2.4Exhalation Delivery Systems

- 5.2.5Implantable Devices

- 5.3By Distribution Channel

- 5.3.1Hospital Pharmacies

- 5.3.2Retail Pharmacies

- 5.3.3Online Pharmacies

- 5.3.4Specialty Clinics

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2ENT Clinics

- 5.4.3Ambulatory Surgery Centers

- 5.4.4Home-Care Settings

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1Sanofi S.A.

- 6.3.2Regeneron Pharmaceuticals Inc.

- 6.3.3GlaxoSmithKline Plc

- 6.3.4OptiNose Inc.

- 6.3.5Intersect ENT Inc.

- 6.3.6Teva Pharmaceutical Industries Ltd.

- 6.3.7Merck & Co., Inc.

- 6.3.8F. Hoffmann-La Roche AG

- 6.3.9Novartis AG

- 6.3.10Pfizer Inc.

- 6.3.11AstraZeneca Plc

- 6.3.12Allakos Inc.

- 6.3.13Lyra Therapeutics Inc.

- 6.3.14Medtronic Plc

- 6.3.15Stryker Corporation

- 6.3.16Amgen Inc.

- 6.3.17Bristol Myers Squibb

- 6.3.18Takeda Pharmaceutical Co. Ltd.

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Drug Class

- Corticosteroids

- Antibiotics

- Leukotriene Inhibitors

- Other Drug Class

- Corticosteroids

- By Route Of Administration

- Nasal Sprays

- Oral Tablets & Suspensions

- Injectable / IV

- Exhalation Delivery Systems

- Implantable Devices

- Nasal Sprays

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Clinics

- Hospital Pharmacies

- By End User

- Hospitals

- ENT Clinics

- Ambulatory Surgery Centers

- Home-Care Settings

- Hospitals

- Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Nasal Polyps Treatment Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 3.99 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 3.65 B (2025) | Global Research Firm A | Excludes implantable devices and relies on 2023 prevalence ratios without mid-period refresh | ||

USD 5.68 B (2025) | Industry Journal B | Adds surgical procedure revenues and applies a single global ASP that inflates biologic spend |