Lipid Nanoparticle CDMO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 419.13 Million |

| Market Size (2031) | USD 818.06 Million |

| Growth Rate (2026 - 2031) | 14.31% CAGR |

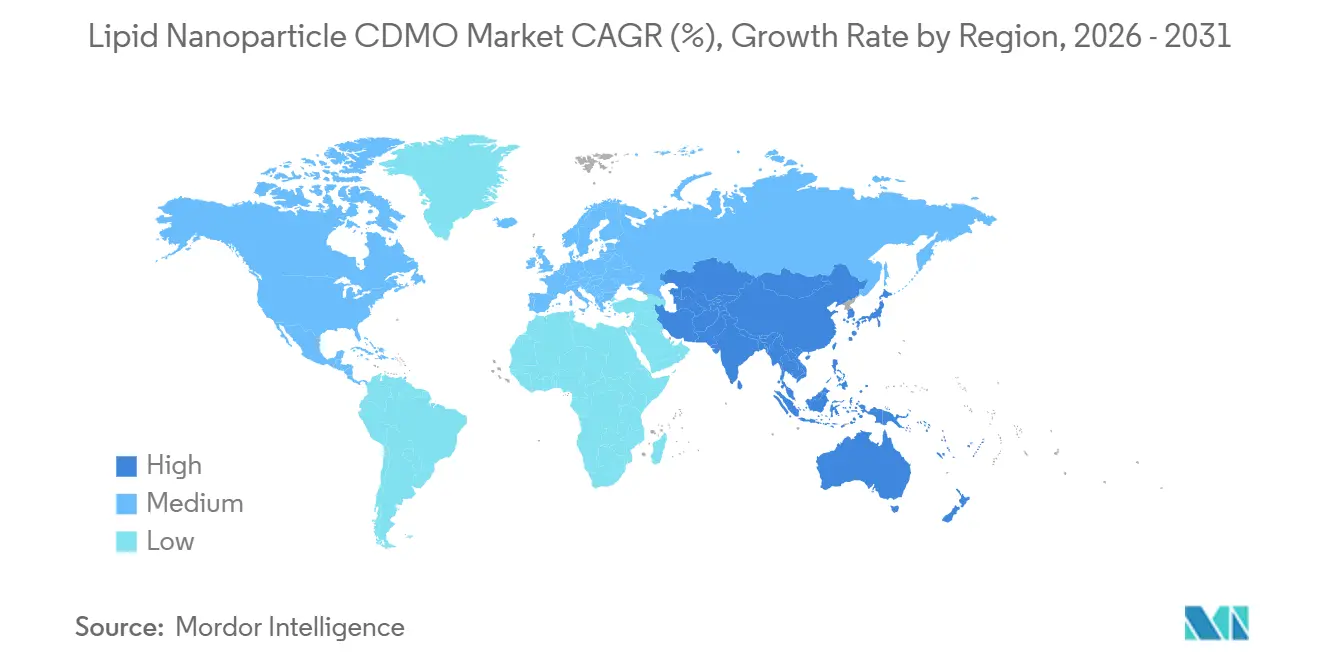

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

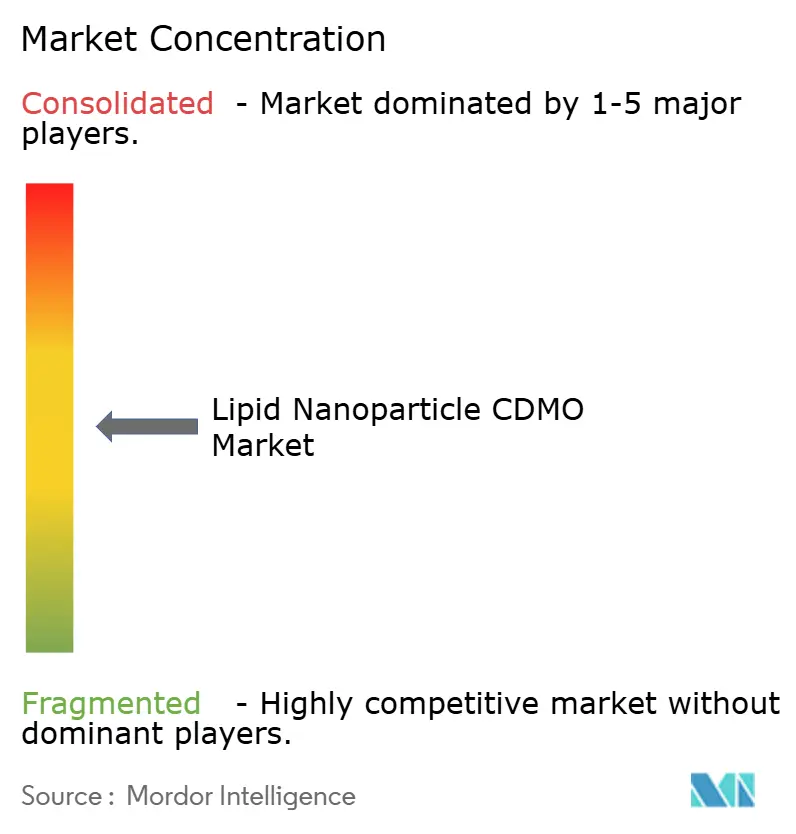

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lipid Nanoparticle CDMO Market Analysis by Mordor Intelligence

The Lipid Nanoparticle CDMO Market size was valued at USD 372.32 million in 2025 and is estimated to grow from USD 419.13 million in 2026 to reach USD 818.06 million by 2031, at a CAGR of 14.31% during the forecast period (2026-2031).

Sponsors are shifting toward outsourced expertise because formulation science, analytical method validation, and aseptic fill-finish all demand capital-intensive infrastructure and talent pools that few drug developers can justify building internally. Public-sector funding accelerates this trend; BARDA’s USD 150 million grant to Evonik’s Lafayette lipid hub in 2025 exemplifies sovereign efforts to secure domestic supply chains. Patent barriers are also easing, as the European Patent Office revoked Arbutus’s foundational EP 2279254 in 2026, widening technology access for contract manufacturers. At the same time, FDA guidance encouraging continuous processing and real-time release testing is nudging CDMOs toward microfluidic and modular systems that compress release timelines and reduce batch variability [1]U.S. Food and Drug Administration, “Guidance for Industry: Quality Considerations for mRNA Products,” fda.gov. Capacity build-outs in North Carolina, South Korea, and Australia signal that geographic footprints are expanding in lockstep with a diversified mRNA pipeline spanning oncology, rare disease, and pandemic-preparedness vaccines.

Key Report Takeaways

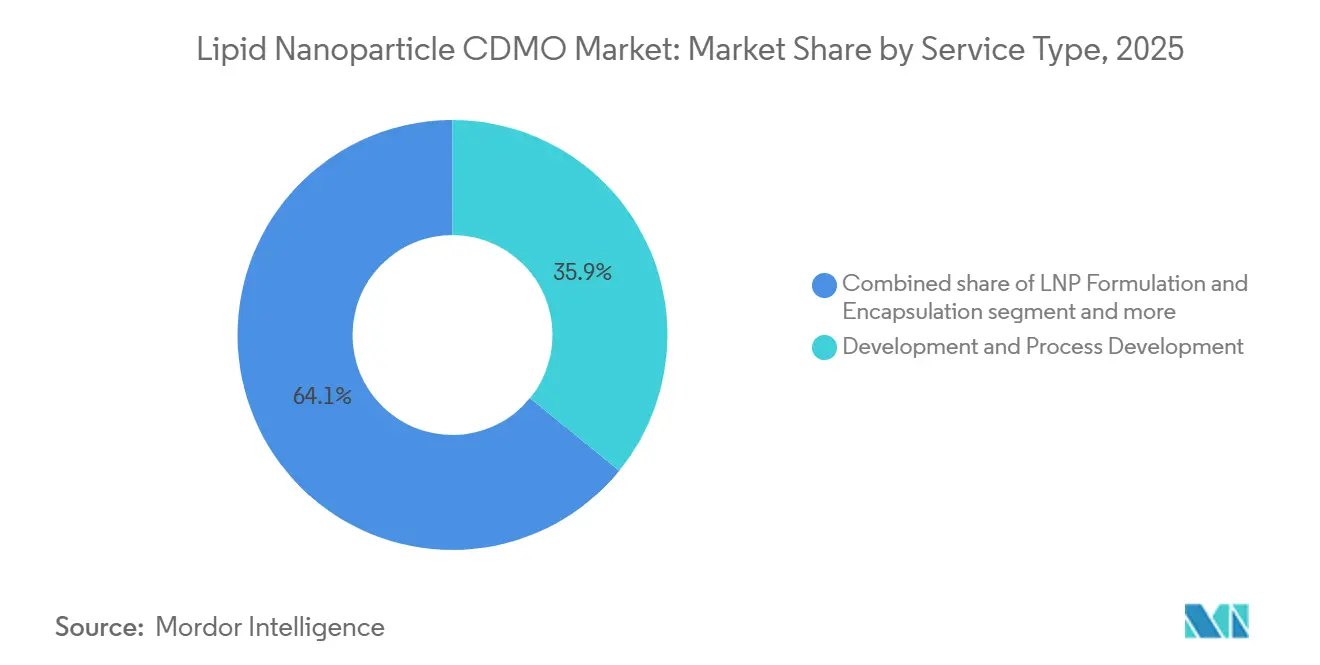

- By service type, Development and Process Development captured 35.9% of 2025 revenue while posting the fastest 15.18% CAGR to 2031, reflecting early-stage optimization needs that trigger repeat engagements.

- By application, oncology therapeutics led with 41.39% revenue share in 2025, whereas rare, genetic, and metabolic programs are advancing at a 14.86% CAGR through 2031.

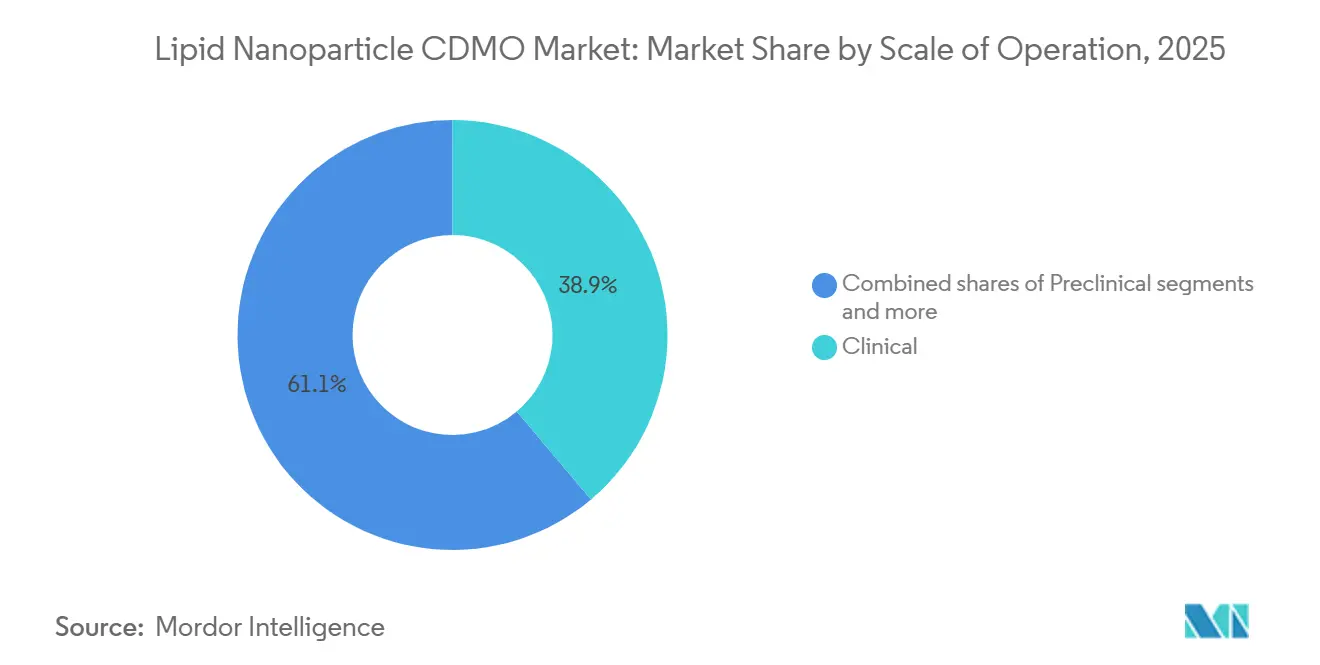

- By scale, commercial manufacturing is forecast to grow quickest at 15.70% annually even though clinical operations retained 38.87% share in 2025.

- By end user, large pharma held 58.28% of lipid nanoparticle CDMO market share in 2025, yet spending by small and mid-sized biotech is expanding at 14.75% CAGR.

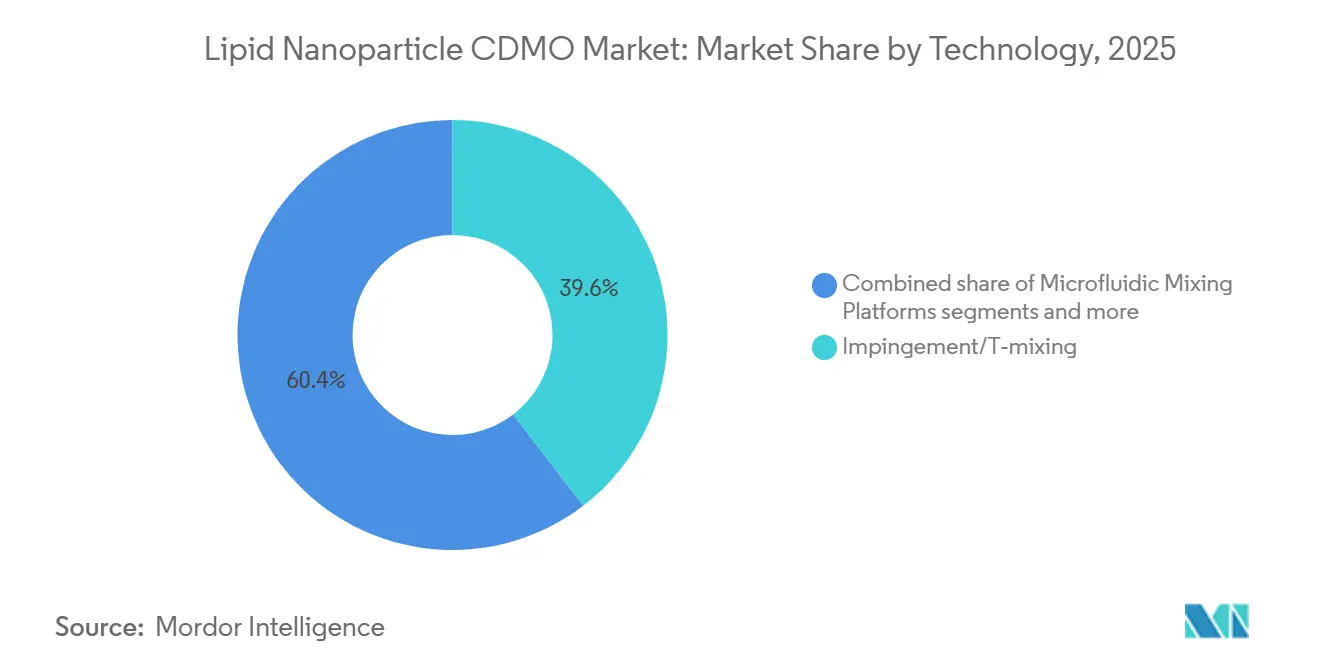

- By technology, continuous and modular LNP production platforms are rising at a 16.34% CAGR, outpacing impingement systems that still represented 39.60% of 2025 revenue.

- North America led with 46.75% revenue share in 2025; Asia-Pacific is the fastest-growing region at 15.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lipid Nanoparticle CDMO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pipeline expansion in mRNA vaccines and therapeutics | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Outsourcing of complex LNP formulation and fill-finish | +2.8% | Global | Short term (≤2 years) |

| Government-backed capacity investments | +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Scalable microfluidic and single-use platforms | +1.9% | Global, early adoption in North America and Europe | Long term (≥4 years) |

| Decentralized continuous manufacturing hubs | +1.6% | Africa, Latin America, Southeast Asia | Long term (≥4 years) |

| Lyophilized thermostable formulations | +1.4% | Global, priority in low-resource settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pipeline Expansion in mRNA Vaccines and Therapeutics

Dozens of late-stage oncology trials, including Moderna’s mRNA-4157 and BioNTech’s BNT122, are generating persistent demand for lipid ratio tuning, encapsulation-efficiency optimization, and particle-size control. Personalized vaccine workflows require CDMOs to compress manufacturing cycles from eight weeks to four, reinforcing multi-year service contracts. Rare-disease programs such as mRNA-3927 for propionic acidemia validate the platform’s versatility and extend the service horizon beyond seasonal vaccines. Regulatory familiarity with mRNA constructs, supported by FDA analytical guidance issued in 2024, shortens review timelines and emboldens sponsors to advance diversified pipelines [2]U.S. Food and Drug Administration, “Guidance for Industry: Quality Considerations for mRNA Products,” fda.gov. The broadened indication mix lengthens engagement periods and elevates the strategic value of CDMOs with integrated development-to-commercial capabilities.

Outsourcing of Complex LNP Formulation and Fill-Finish

Pharma innovators now view specialist CDMOs as partners for capabilities that are uneconomical to replicate internally. Lonza expanded its Stein and Geleen sites to bundle lipid synthesis through aseptic vial filling under one quality system. Analytical method development alone can exceed USD 10 million in capital outlay per lab, pushing small biotechs now growing at 14.75% CAGR toward external partnerships. Lyophilization expertise further differentiates suppliers, with Precision NanoSystems validating GenVoy-ILM for room-temperature storage in 2025. Continuous processing magnifies this outsourcing imperative because real-time analytics demand cross-functional talent pools that few sponsors maintain in-house.

Government-Backed Capacity Investments in Lipids and LNP

The United Kingdom’s GBP 520 million Biomanufacturing Fund, Canada’s CAD 200 million Resilience hub, and BARDA’s USD 150 million grant to Evonik are underwriting lipid and LNP infrastructure that would otherwise struggle to clear private hurdle rates. These subsidies accelerate time-to-capacity and improve regional supply resilience, thereby supporting demand growth across the lipid nanoparticle CDMO market. Sovereign involvement also incentivizes CDMOs to locate facilities closer to strategic stockpile programs, locking in long-term volume commitments.

Scalable Microfluidic and Single-Use Platforms

Recipharm’s CP1 line, built with USD 82 million in FDA funding, integrates inline sensors and closed-loop control that cut batch variability below 5%. Precision NanoSystems’ staggered-herringbone micromixers routinely achieve sub-100 nm particles with PDIs under 0.15, a benchmark that enhances cellular uptake. Single-use assemblies eliminate cross-contamination risk and shorten changeovers, advantages that resonate with personalized oncology programs. Although a GMP microfluidic suite costs roughly USD 25 million, the regulatory push for continuous processing positions these platforms as future industry standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LNP intellectual property litigation | −1.8% | Global, concentrated in US, EU, Asia | Short term (≤2 years) |

| GMP-grade lipid and component supply constraints | −1.5% | Global | Medium term (2-4 years) |

| Solvent handling and sustainability pressures | −0.9% | North America, Europe | Long term (≥4 years) |

| Talent shortages and Pharma 4.0 adoption gaps | −1.2% | Global, acute in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

LNP Intellectual Property Litigation and Licensing Complexity

Arbutus and Genevant sued Moderna across 30 jurisdictions in 2025, creating uncertainty over royalty stacking and freedom-to-operate for licensees. Although the EPO revoked EP 2279254 in 2026, overlapping patents on ionizable lipids still complicate contracting and extend negotiations by up to six months. Smaller sponsors bear higher risk premiums, dampening near-term demand growth within the lipid nanoparticle CDMO market.

GMP-Grade Lipid and Component Supply Constraints

Fewer than ten manufacturers supply GMP-grade ionizable lipids globally, and a single pandemic-scale campaign can consume up to 100 metric tons annually. Evonik’s Lafayette plant added 200 metric tons of capacity in 2025 yet leaves little buffer for therapeutics. Prolonged lead times force CDMOs to stockpile inventory, tying up working capital and elevating write-off risk if formulations evolve. Vertical integration is capital-intensive, so access remains uneven across the supply base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type Early-Stage Optimization Drives Repeat Engagement

Development and Process Development accounted for 35.9% of 2025 revenue and will post the fastest 15.18% CAGR to 2031, underscoring the strategic value of formulation screening and microfluidic parameter tuning. These studies cost USD 2 million to USD 5 million per program and typically precede multi-batch clinical campaigns. cGMP drug-product manufacturing remains the largest absolute pool as approved vaccines and therapeutics command contracts of USD 50 million to USD 200 million, yet its growth rate lags because revenues arrive episodically.

Analytical and quality control services are a rising high-margin niche because regulators expect orthogonal characterization via dynamic light scattering, cryo-EM, and reverse-phase HPLC. Fill-finish and lyophilization capabilities have become premium differentiators after GenVoy-ILM proved room-temperature stability in 2025. Integrated CDMOs that bundle these steps under performance-based contracts are winning share across the lipid nanoparticle CDMO market.

By Application Oncology Dominance Meets Rare-Disease Acceleration

Oncology therapeutics retained a 41.39% revenue share in 2025, reflecting personalized neoantigen vaccines that require bespoke mRNA sequences and rapid turnaround. Each patient-specific batch compresses timelines from eight weeks to four and drives ongoing demand for flexible capacity. Infectious-disease vaccines still anchor government stockpiles but no longer dominate revenues.

Rare, genetic, and metabolic disorders will expand fastest at 14.86% CAGR through 2031, supported by orphan-drug incentives and promising interim data from programs such as mRNA-3927. Other exploratory areas, including cardiometabolic and protein-replacement therapies, remain early-stage yet represent upside for CDMOs that develop tissue-targeted LNP chemistries.

By Scale of Operation Clinical Focus Shifts Toward Commercial Build-Out

Clinical production represented 38.87% share in 2025 because most mRNA programs remain in Phases 1 and 2. Batch sizes of 10 to 100 liters and iterative study designs keep utilization high. Preclinical volumes serve as a funnel for future revenue, ensuring that early relationships often persist through commercialization.

Commercial manufacturing will grow fastest at 15.70% CAGR to 2031 as late-stage assets secure approvals. Samsung Biologics’ modular Songdo campus illustrates how segregated suites handle 500- to 2,000-liter runs while minimizing cross-contamination. Early reservation deals and co-investment agreements have emerged to secure scarce large-scale slots, reflecting tightening supply across the lipid nanoparticle CDMO market.

By End User Biotech Agility Outpaces Pharma Incumbency

Large pharmaceutical firms controlled 58.28% of 2025 spending but often retain upstream operations internally, outsourcing mainly fill-finish and analytics. Small and mid-sized biotech companies are growing at 14.75% CAGR because they outsource nearly all manufacturing to conserve capital.

Government and academic programs, though smaller in value, catalyze technology diffusion through publicly funded research consortia and pandemic-preparedness contracts. The rise of virtual biotech models, which outsource every unit operation, further lifts demand for CDMOs that offer end-to-end integration under single quality systems.

By Technology or Process Continuous Platforms Disrupt Batch Incumbency

Impingement and T-mixing systems still delivered 39.60% of 2025 revenue thanks to regulatory familiarity. However, continuous and modular lines will grow at 16.34% CAGR as platforms like CP1 demonstrate sub-5% batch variability and real-time release. Microfluidic equipment such as NanoAssemblr enables sub-100 nm particles and precise lipid-to-mRNA ratios, supporting personalized oncology workflows.

Alternative non-viral nanoparticles remain exploratory, but interest is rising as sponsors seek chemistries that avoid PEG-related hypersensitivity. CDMOs investing early in continuous control architectures and diversified lipid portfolios are advantaged in securing long-term master-service agreements within the lipid nanoparticle CDMO market.

Geography Analysis

North America held 46.75% of 2025 revenue, supported by Thermo Fisher’s USD 650 million Greenville expansion and Evonik’s BARDA-funded lipid center in Indiana. Dense biotech clusters in Boston and San Francisco sustain early-stage pipeline flow, while regulatory familiarity with mRNA expedites approvals.

Europe accounted for roughly one-quarter of 2025 revenue. Germany’s Rhineland corridor links CordenPharma’s lipid synthesis, Rentschler’s formulation, and Evonik’s fill-finish capabilities, offering sponsors EU-GMP compliance without complex cross-border logistics [3]CordenPharma, “Plankstadt Lipid Expansion,” cordenpharma.com. The United Kingdom’s GBP 520 million biomanufacturing fund signals intent to reclaim post-Brexit competitiveness, though divergent regulations add documentation burdens.

Asia-Pacific is projected to grow fastest at 15.48% CAGR through 2031. Samsung Biologics’ Songdo facility, Moderna’s Melbourne build, and Chinese partnerships between Walvax, CSPC, and WuXi Biologics underscore regional momentum. India’s Gennova advanced GEMCOVAC-19 toward approval, showcasing ambitions for indigenous mRNA capacity. WHO’s technology-transfer hub extended to 15 countries by 2025, but uneven regulatory capacity limits immediate volume.

Competitive Landscape

The top five suppliers controlled a majority of 2025 revenue, producing a moderately concentrated structure within the lipid nanoparticle CDMO market. Integrated players such as Lonza and Thermo Fisher bundle mRNA plasmid production, lipid synthesis, formulation, analytics, and fill-finish under unified quality systems, easing tech-transfer risk for global sponsors. Samsung Biologics and WuXi AppTec leverage large campuses and cost advantages to court multinational pharma while adding proprietary continuous lines.

Specialists like Polymun Scientific and Precision NanoSystems compete on microfluidic technology and rapid process-development services, winning early-stage biotech contracts that favor speed and flexibility. Evonik’s vertical integration into ionizable lipid supply provides a hedge against raw-material shortages and positions the firm as a preferred partner for North American programs under domestic-content rules. Continuous-manufacturing pioneers such as Recipharm are building competitive moats by achieving real-time release profiles that batch systems struggle to match.

Litigation risks remain a wild card. The Arbutus and Genevant suit against Moderna could recalibrate licensing economics if royalties rise or chemistries shift. Mid-tier CDMOs lacking differentiated platforms or secured lipid supply are likely acquisition targets as leaders seek scale. Thermostable formulation, decentralized modular plants, and Pharma 4.0 analytics represent the next battlegrounds, and early movers stand to lock in multi-year government stockpile contracts that stabilize volume in the lipid nanoparticle CDMO market.

Lipid Nanoparticle CDMO Industry Leaders

Lonza

Thermo Fisher Scientific

Samsung Biologics

Polymun Scientific

WuXi AppTec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Acuitas acquired a majority stake in RNA Technologies & Therapeutics to broaden its RNA pipeline.

- October 2025: Evonik’s USD 220 million Lafayette lipid center became operational with BARDA support, adding 200 metric tons of annual capacity.

- September 2025: Biocytogen Pharmaceuticals reached an agreement with Merck KGaA to accelerate work on antibody-linked lipid carriers that can transport nucleic-acid drugs.

Global Lipid Nanoparticle CDMO Market Report Scope

As per the scope of the report, Lipid nanoparticle (LNP) Contract Development and Manufacturing Organizations (CDMOs) are specialized partners that provide end-to-end services for the development, formulation, and GMP-compliant manufacturing of advanced drug delivery systems.

The Lipid Nanoparticle CDMO Market is segmented by service type, applications, scale of operation, end-users, technology, and geography. By service type, it is segmented into development & process development, LNP formulation & encapsulation, analytical & quality control, CGMP drug product manufacturing, and fill-finish & lyophilization. By application, the market is segmented into infectious disease vaccines, oncology therapeutics, rare/genetic & metabolic disorders, and other therapeutics. By scale of operation, the market is divided into preclinical, clinical, and commercial. By end-users, the segmentation includes large pharma, small/mid biotech, and government/academic. By technology, the market is segmented into microfluidic mixing platforms, impingement/T‑mixing, continuous/modular LNP production, and alternative nonviral nanoparticles. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Development & Process Development |

| LNP Formulation & Encapsulation |

| Analytical & Quality Control |

| cGMP Drug Product Manufacturing |

| Fill-Finish & Lyophilization |

| Infectious Disease Vaccines |

| Oncology Therapeutics |

| Rare/Genetic & Metabolic Disorders |

| Other Therapeutics |

| Preclinical |

| Clinical |

| Commercial |

| Large Pharma |

| Small/Mid Biotech |

| Government/Academic |

| Microfluidic Mixing Platforms |

| Impingement/T‑mixing |

| Continuous/Modular LNP Production |

| Alternative Nonviral Nanoparticles |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Development & Process Development | |

| LNP Formulation & Encapsulation | ||

| Analytical & Quality Control | ||

| cGMP Drug Product Manufacturing | ||

| Fill-Finish & Lyophilization | ||

| By Application | Infectious Disease Vaccines | |

| Oncology Therapeutics | ||

| Rare/Genetic & Metabolic Disorders | ||

| Other Therapeutics | ||

| By Scale of Operation | Preclinical | |

| Clinical | ||

| Commercial | ||

| By End User | Large Pharma | |

| Small/Mid Biotech | ||

| Government/Academic | ||

| By Technology/Process | Microfluidic Mixing Platforms | |

| Impingement/T‑mixing | ||

| Continuous/Modular LNP Production | ||

| Alternative Nonviral Nanoparticles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the lipid nanoparticle CDMO market in 2026?

The lipid nanoparticle CDMO market size is estimated to reached USD 419.13 million in 2026.

What CAGR is projected for lipid nanoparticle CDMO services to 2031?

Market revenue is expected to grow at a 14.31% CAGR between 2026 and 2031.

Which service segment is expanding fastest?

Development and Process Development services are forecast to post the quickest 15.18% CAGR.

Why is Asia-Pacific the fastest-growing region?

Government subsidies, new modular plants in South Korea and Australia, and rising local biotech pipelines are driving a 15.48% regional CAGR.

What technological trend is disrupting traditional batch production?

Continuous and modular LNP lines with real-time analytics are outpacing legacy impingement systems as sponsors seek shorter release timelines.

Page last updated on: