Nanoparticle Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.90 Billion |

| Market Size (2031) | USD 10.10 Billion |

| Growth Rate (2026 - 2031) | 11.41% CAGR |

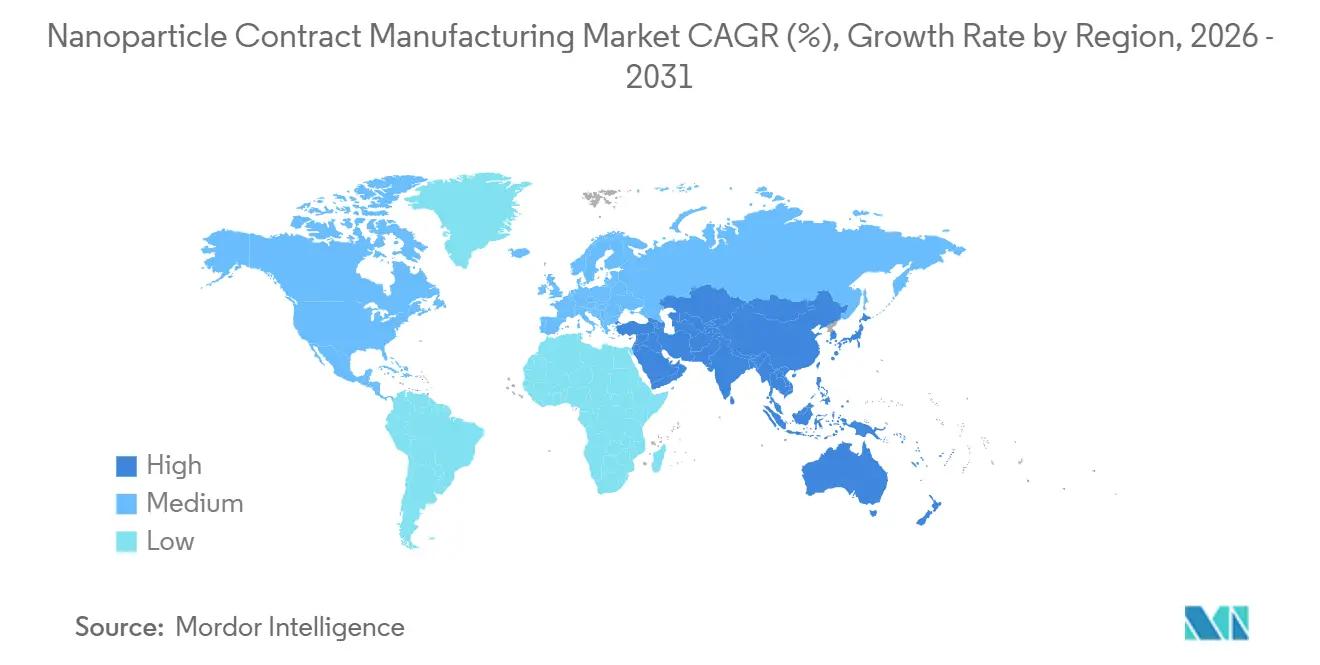

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nanoparticle Contract Manufacturing Market Analysis by Mordor Intelligence

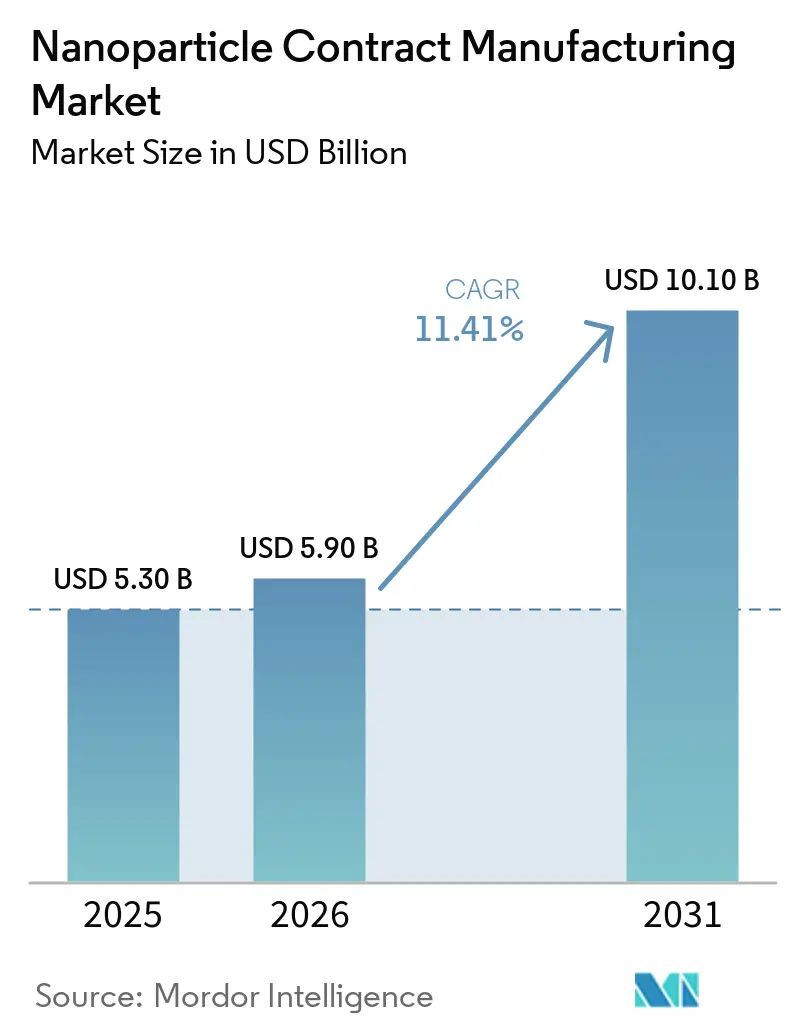

The Nanoparticle Contract Manufacturing Market size is expected to increase from USD 5.30 billion in 2025 to USD 5.90 billion in 2026 and reach USD 10.10 billion by 2031, growing at a CAGR of 11.41% over 2026-2031.

Rising demand for clinical- and commercial-grade lipid nanoparticles, capital-intensive GMP requirements, and growing regulatory clarity continue to pull sponsors toward specialized outsourcing partners. The COVID-19 vaccine experience proved that microfluidic mixing capacity and validated analytical methods are mission-critical, prompting large and emerging biotechs alike to lock in multi-year supply agreements. Oncology remains the biggest single application, but genetic and metabolic programs are scaling faster because gene-editing cargos require sub-100 nm precision and strict endotoxin controls. Regionally, North America dominates today, but Asia-Pacific shows the steepest growth curve as Chinese and Indian contractors add ionizable-lipid synthesis lines that meet ICH Q3D specifications. Across every service tier, sponsors favor CDMOs that bundle formulation, analytical, and aseptic fill-finish under one quality system because integrated workflows shorten time to clinic and reduce tech-transfer risk.

Key Report Takeaways

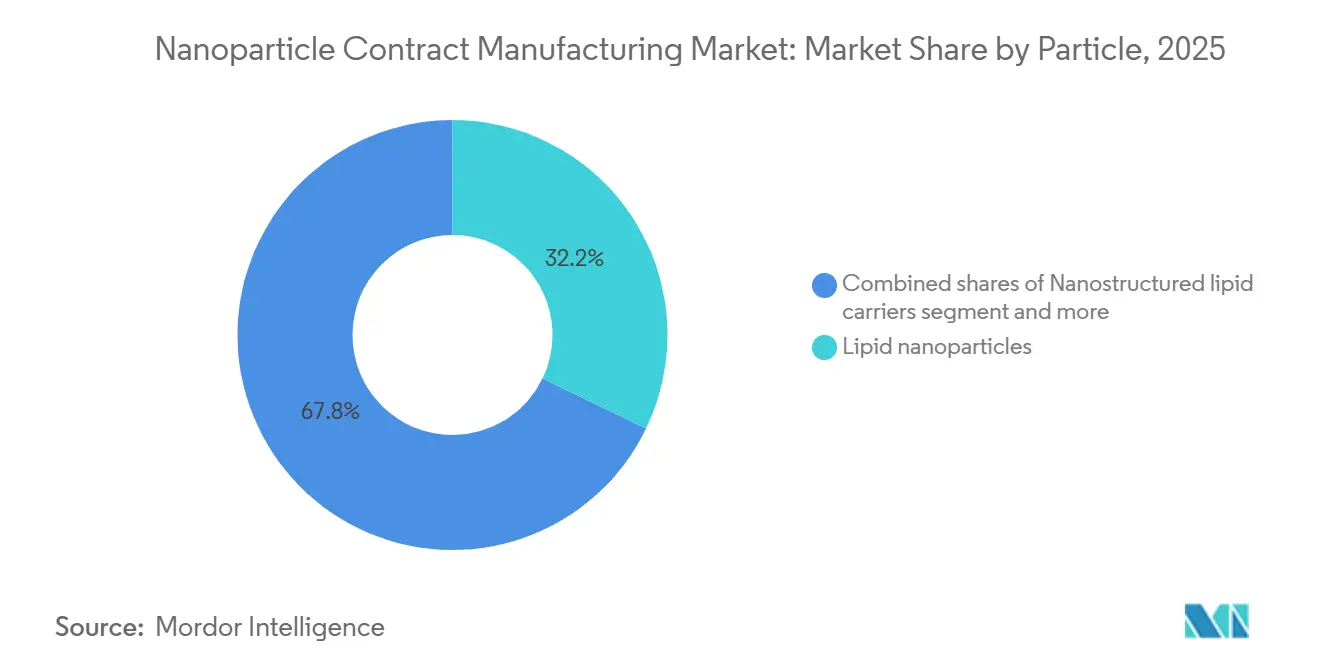

- By particle type, lipid nanoparticles led with 32.16% of the Nanoparticle Contract Manufacturing Market share in 2025, while polymeric nanoparticles are forecast to advance at an 11.98% CAGR to 2031.

- By modality, small-molecule payloads accounted for 28.13% of the Nanoparticle Contract Manufacturing Market size in 2025, and mRNA formulations will expand at an 11.89% CAGR through 2031.

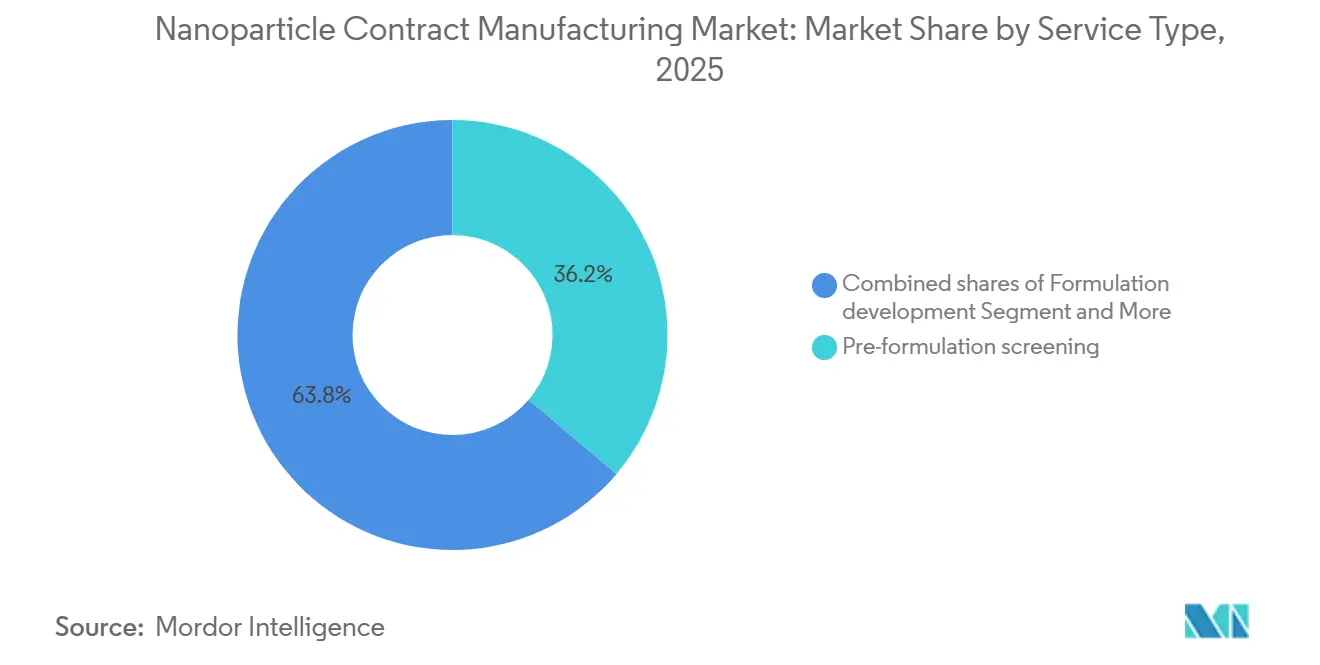

- By service type, pre-formulation screening accounted for 36.19% of the Nanoparticle Contract Manufacturing Market size in 2025, and aseptic fill-finish & lyophilization will expand at an 11.89% CAGR through 2031.

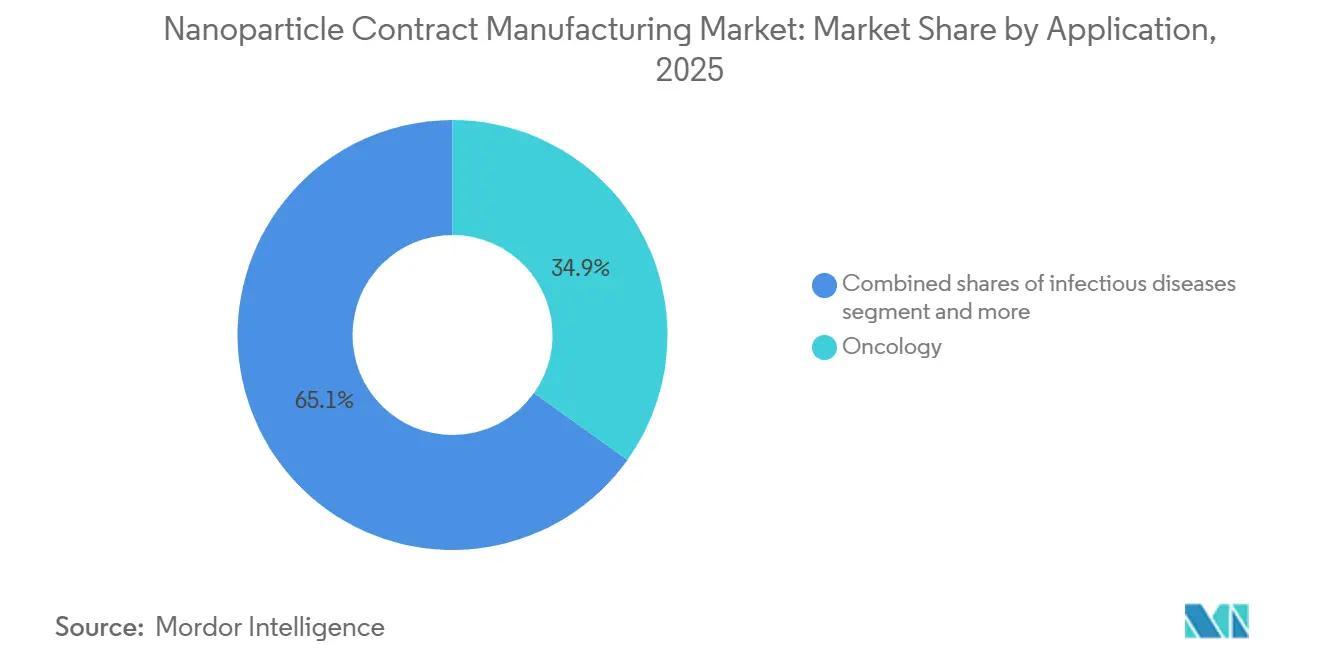

- By application, oncology captured 34.87% revenue share in 2025; genetic and metabolic disorders are projected to grow at a 12.05% CAGR toward 2031.

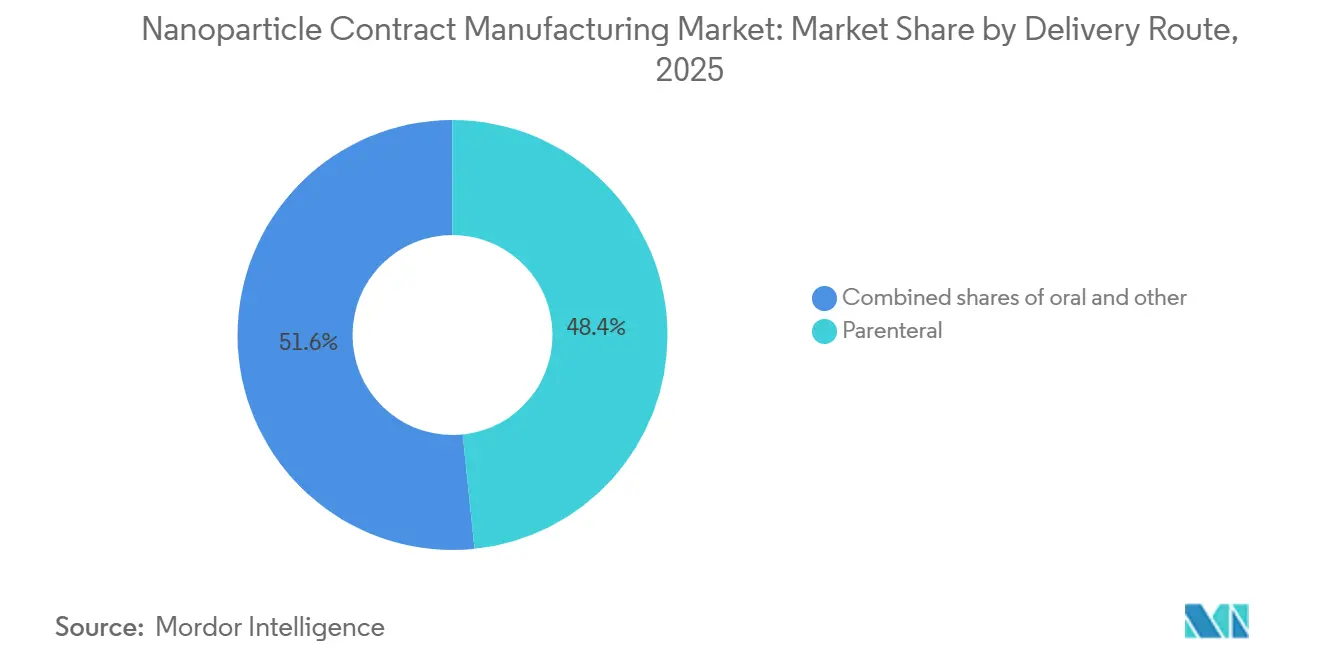

- By delivery route, parenteral formats represented 48.36% of 2025 revenue, and oral nanoparticle products are poised for an 11.76% CAGR through 2031.

- By client type, pharmaceutical and biotechnology companies commanded 56.18% of 2025 sales and will grow at an 11.93% CAGR over the forecast period..

- By geography, North America held 39.16% of 2025 revenue, whereas Asia-Pacific is set to post an 11.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nanoparticle Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of mRNA/siRNA pipelines requiring LNP-enabled CDMO capacity | +2.8% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Oncology nanomedicine adoption sustaining complex nanoparticle demand | +2.3% | North America, Europe, Asia-Pacific core markets | Long term (≥ 4 years) |

| Outsourcing acceleration due to capex, GMP, and analytics barriers | +2.1% | Global, particularly emerging biotechs in North America and the Asia-Pacific | Short term (≤ 2 years) |

| Regulatory clarity and evolving CMC expectations for nanomedicines | +1.6% | North America and Europe, spillover to the Asia-Pacific | Medium term (2-4 years) |

| Platformization of LNP/analytical toolkits reducing time-to-clinic | +1.4% | Global, with early adoption in North America | Short term (≤ 2 years) |

| saRNA/circRNA programs creating novel formulation demand | +1.2% | North America and Europe, and emerging in the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of mRNA/siRNA Pipelines Requiring LNP Capacity

Moderna disclosed in its 2025 10-K that eight of fifteen clinical programs rely on external lipid-nanoparticle formulation because in-house suites are reserved for COVID-19 boosters. Similar outsourcing by BioNTech and Arbutus shows a clear preference to deploy capital toward R&D rather than toward GMP bricks-and-mortar. New FDA guidance now requires ≥80% encapsulation efficiency and a polydispersity index ≤0.2, elevating the analytical bar and favoring CDMOs that already run AF4-MALS and cryo-TEM assays [1]U.S. Food and Drug Administration, “Guidance for Industry: Chemistry, Manufacturing, and Controls Information for mRNA Vaccines,” fda.gov. With platformized ionizable lipids cutting formulation timelines in half, sponsors can progress multiple pipeline assets concurrently.

Oncology Nanomedicine Adoption Sustaining Complex Particle Demand

Oncology held 34.87% revenue in 2025 on the back of PEGylated liposomes and polymeric carriers that temper systemic toxicity. Merck KGaA logged a significant jump in CDMO requests for antibody-drug conjugate cargos encapsulated in nanoparticles, confirming clinician preference for targeted delivery [2]Merck KGaA, “Annual Report 2025,” merckgroup.com. NCI studies show solid-lipid nanoparticles triple tumor accumulation for paclitaxel versus Cremophor formulations, underlining the clinical upside. Intratumoral injections of TLR agonists further show systemic immune activation without cytokine storms, broadening nanoparticle use cases.

Outsourcing Acceleration Tied to Capex and Analytics Barriers

Precision NanoSystems reported that the majority of surveyed startups outsource chiefly because of analytical complexity rather than capacity shortfalls. Recipharm’s 18 new European LNP contracts averaged USD 3.8 million each, signaling sponsor willingness to pay for risk transfer. ISPE benchmarking shows CDMOs deliver lower cost per gram than in-house builds, reinforcing the economic logic. High utilization rates, WuXi Biologics tracks the majority on its mixers—translate into faster slot access and fewer scheduling gaps.

Regulatory Clarity Around Nano-CMC Expectations

FDA and EMA draft guidances now enumerate particle size, zeta potential, and payload-to-lipid ratio as critical quality attributes, giving sponsors cleaner targets and reducing review cycles. Catalent noted IND timelines compressed by four months when its validated comparability protocols are accepted at Type C meetings. PDA technical reports recommend orthogonal sizing methods, which only tier-1 CDMOs routinely offer. Japan’s PMDA alignment with ICH Q5A extends this clarity into Asia, smoothing multi-regional submissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex, evolving nano-CMC characterization and comparability risk | -1.8% | Global, with heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| High cost, scale-up risk, and batch failure sensitivity | -1.5% | Global, particularly impacting emerging biotechs | Short term (≤ 2 years) |

| Lipid IP/licensing constraints and freedom-to-operate hurdles | -1.2% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Cold-chain and aseptic constraints for nano-DP/fill-finish | -1.0% | Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Nano-CMC Characterization and Comparability Risk

FDA’s 2024 Complete Response Letter to Translate Bio cited inadequate lipid-oxidation profiling, forcing a nine-month refile and underscoring regulatory stakes. Less than 20 CDMOs worldwide run validated AF4-MALS assays, narrowing sponsor choice and slowing tech transfer [3]Journal of Pharmaceutical Sciences, “Scale-Up Challenges in LNP Manufacturing,” jpharmsci.org. Cryo-EM costs USD 5,000–10,000 per sample, a heavy burden for seed-stage ventures. Switching vendors mid-program can shift particle size by 10–20 nm, triggering bridging studies that add 12–18 months.

High Cost, Scale-Up Risk, and Batch-Failure Sensitivity

Lonza documented an eight-month, USD 2 million exercise to move from 1-liter to 50-liter LNP batches because mixing energy profiles change non-linearly at scale. Pharmaceutical Technology reports 8%–12% batch failure rates for clinical-scale LNPs, triple that of monoclonal antibodies. GMP-grade ionizable lipids sell for USD 50,000–150,000 per kilogram, far above standard phospholipid costs, which magnifies budget blow-outs when batches fail.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Particle: LNPs Anchor Revenue, Polymeric Platforms Gain Momentum

Lipid nanoparticles secured 32.16% revenue in 2025 and remain the primary workhorse for RNA therapeutics across the Nanoparticle Contract Manufacturing Market. Polymeric systems will grow at an 11.98% CAGR because PLGA and chitosan carriers enable oral dosing and sustained release that lipids struggle to match. Liposomes retain a solid niche in small-molecule oncology, delivering extended half-life and reduced cardiotoxicity. Dendrimers stay in prototype status due to high synthesis cost. Other formats, such as nanostructured lipid carriers and solid lipid nanoparticles, serve dermatology and ophthalmology, while inorganic particles are largely confined to imaging studies.

Polymeric platforms capitalize on FDA-approved excipients, lowering toxicology hurdles and shortening IND review. Evonik’s Eudragit nanoparticles improved oral insulin bioavailability fourfold in Phase I, demonstrating how polymer chemistry can solve first-pass metabolism challenges. Samsung Biologics now lists six Phase II polymeric programs for diabetes and IBD, giving credibility to the segment. CDMOs offering both lipid and polymer lines can arbitrage demand swings and reduce capacity downtime, a tactical edge as the Nanoparticle Contract Manufacturing Market diversifies.

By Modality/Payload: Small Molecules Lead, mRNA Surges

Small-molecule cargos held 28.13% of 2025 revenue, powered by nanoparticle-solubilized oncology agents. mRNA projects, however, will post an 11.89% CAGR on the way to 2031, propelled by infectious-disease vaccines and emerging self-amplifying constructs that permit lower dosing. Gene-editing payloads such as CRISPR-Cas9 ribonucleoproteins require ultra-pure LNPs optimized for endosomal escape, pushing analytical demands higher. Peptide and protein therapies leverage pH-sensitive polymeric particles to prevent enzymatic degradation. Circular RNA, stable at room temperature for six months, offers new logistical advantages for the Nanoparticle Contract Manufacturing Market.

The modality mix now attracts a wider sponsor base. Moderna lists fifteen non-COVID mRNA programs spanning cardiology and oncology, each depending on external formulation suites. BioNTech’s melanoma neoantigen data showed objective response when delivered via customized LNPs, underscoring efficacy upside and fortifying outsourcing pipelines.

By Service Type: Formulation Development and GMP Manufacturing Dominate

Pre-formulation screening captured 36.19% of the 2025 service-type revenue share, reflecting strong sponsor demand for swift confirmation that candidate payloads remain stable across lipid, polymeric, and liposomal platforms before significant capital is committed to GMP campaigns. The service compresses decision cycles from 6 months to 6 weeks by running 20–50 formulation variants in parallel, giving emerging biotechs a practical hedge against clinical attrition across multiple nanoparticle designs. Demand for this early-screening step rose further after the FDA’s 2024 guidance required cryo-TEM and AF4-MALS data in every lipid nanoparticle (LNP) IND, prompting many sponsors to bundle analytical characterization with screening to streamline filings.

Aseptic fill-finish and lyophilization remain the fastest-growing offerings, projected to advance at an 11.89% CAGR through 2031 as commercial mRNA vaccines migrate from emergency-use authorizations to routine immunization schedules and must meet ICH Q1A stability targets for global distribution. These sterile operations increasingly rely on single-use systems that limit cross-contamination while supporting thermostable formats required for 18- to 24-month expiry dating at 2 °C to 8 °C. Sponsors pursuing mid-stage programs still outsource formulation development—optimizing lipid ratios, buffer pH, and mixing parameters yet revenue concentration is shifting toward GMP clinical and commercial manufacturing, where Phase II and Phase III batches demand multi-kilogram output and full CMC documentation

By Application: Oncology Leads, Genetic Disorders Surge

Oncology delivered 34.87% of 2025 revenue. However, genetic and metabolic disease programs grow fastest at 12.05% CAGR due to gene-editing breakthroughs for sickle-cell and lysosomal disorders. Infectious-disease vaccines moderate as pandemic volumes recede but still contribute a sizable baseline demand. Cardiometabolic payloads such as siRNA lipid-lowering drugs gain traction as payers accept the high cost in exchange for durable outcomes. Ophthalmology, CNS, and respiratory indications test advanced delivery routes, ocular, intrathecal, and inhalation, that only a handful of CDMOs can support.

BioNTech’s partnership with Genentech for neoantigen vaccines puts additional oncology demand in play, while CRISPR Therapeutics’ CTX001 approval validates the genetic-disorder segment and unlocks premium-priced therapies that rely on flawless LNP quality.

By Client Type: Pharma and Biotech Dominate

Pharma and biotech entities represent 56.18% of 2025 revenue and will remain the core clientele thanks to late-stage pipelines and commercial manufacturing needs. Academic labs contribute exploratory projects, often funded by NIH grants, but usually transfer to CDMOs before IND submission because universities lack GMP suites. Large pharma follows a hybrid approach, outsourcing non-core batches while reserving flagship lines in-house. Pfizer’s RSV vaccine work with Samsung Biologics exemplifies this flexible model.

Emerging biotechs, bolstered by USD 8 billion in 2024 venture inflows, remain the most agile and outsourcing-intensive client subset. Their preference for variable over fixed costs keeps the Nanoparticle Contract Manufacturing Market humming through capital cycles.

By Delivery Route: Parenteral Dominates, Oral Gains Traction

Parenteral formats commanded 48.36% revenue in 2025 as intravenous and intramuscular routes stayed central for vaccines and oncology infusions. Oral nanoparticles, however, will climb at 11.76% CAGR on the back of mucoadhesive coatings that dodge gastric pH and first-pass metabolism. Inhaled, intrathecal, ocular, and intratumoral routes remain niche but strategic, offering local action with minimal systemic exposure.

Evonik’s chitosan-coated oral insulin hit 15% bioavailability in Phase I, proving feasibility for complex biologics outside the injection paradigm. Intratumoral nanoparticles that combine checkpoint inhibitors with TLR agonists keep toxicity low while amplifying systemic immunity, a finding echoed in Bristol Myers Squibb’s Phase II trial updates.

Geography Analysis

North America dominated the Nanoparticle Contract Manufacturing Market with 39.16% revenue in 2025, supported by more than 30 GMP-certified lipid-nanoparticle suites across Boston, San Francisco, and the Research Triangle. FDA final guidance that now mandates cryo-TEM and AF4-MALS for all IND submissions further entrenches demand for advanced U.S. capacity. Canada subsidizes domestic outsourcing through NRC Montreal, while Mexico’s Toluca cluster offers near-shore cost arbitrage for early-stage U.S. sponsors.

Asia-Pacific is forecast to record an 11.84% CAGR, the fastest regional climb, as China’s NMPA cleared eight LNP products in 2024–2025 and Indian CDMOs invested USD 500 million in new mixing lines. Samsung Biologics’ USD 300 million expansion cements South Korea as a regional anchor. Australia leverages integrated Phase I units to woo local biotech trials, while Japan’s PMDA guidance convergence reduces export hurdles.

Europe sits between these poles, strong in specialized ionizable-lipid chemistry through players like Polymun Scientific and Evonik. EMA’s reflection paper harmonizes CMC demands, but the UK’s separate MHRA pathway offers a faster alternative for some sponsors. Spain’s Rovi facility secured Moderna’s European supply, and Swiss-based Lonza remains the go-to vendor for late-stage programs. Emerging demand in Middle East & Africa and South America is limited by cold-chain gaps, though Brazil’s Fiocruz and South Africa’s Biovac are investing in nanoparticle vaccine lines.

Competitive Landscape

Competition is moderately fragmented; the top five providers hold a significant share, leaving ample headroom for mid-tier specialists. Thermo Fisher, Catalent, Lonza, WuXi Biologics, and Samsung Biologics differentiate on inspection track records and integrated analytical suites. Polymun Scientific, Precision NanoSystems, and Vernal Biosciences capture niche demand for ionizable-lipid screening and microfluidic optimization, illustrating the importance of depth over scale in certain contracts.

Analytical breadth is a decisive factor. Catalent’s acquisition of Metrics added cryo-TEM and AF4-MALS, allowing end-to-end service under one quality system and justifying price premiums. AI-guided formulation has become a new frontier; Lonza’s patent claims a significant reduction in screening runs, cutting months off development calendars. Vertical integration into lipid synthesis, seen in Evonik’s 2024 German acquisition, secures feedstock and improves cost control. M&A remains selective but likely to accelerate as sponsors demand fewer touchpoints and single-service-level agreements.

CDMOs that successfully combine lipid, polymer, and oral-delivery competencies with digital process control will capture future growth. Meanwhile, freedom-to-operate disputes over ionizable-lipid IP from Acuitas and Genevant form a latent risk that could reshape alliances and licensing economics.

Nanoparticle Contract Manufacturing Industry Leaders

Thermo Fisher Scientific

Catalent Biologics

Lonza Group

WuXi Biologics

Samsung Biologics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Genprex shifted production of its diabetes gene-therapy candidate, GPX-002, from university laboratories to a coordinated network of contract development and manufacturing organizations, a move that positions the program for first-in-human trials planned for 2026.

- September 2025: Merck KGaA and Biocytogen agreed to co-develop antibody-linked lipid carriers for nucleic-acid drugs.

- January 2025: Evonik partnered with ST Pharm to integrate tailored nucleic acids with its LNP manufacturing services.

Global Nanoparticle Contract Manufacturing Market Report Scope

As per the scope of the report, nanoparticle contract manufacturing refers to the specialized outsourcing of nanoparticle production to external organizations, often called Contract Development and Manufacturing Organizations (CDMOs), that possess the high-level expertise and infrastructure required for these complex materials.

The nanoparticle contract manufacturing market is segmented by particle, modality, service, application, client type, delivery route, and geography. By particle, the market is segmented into lipid nanoparticles, nanostructured lipid carriers, dendrimers, liposomes, polymeric nanoparticles, nanoemulsions, solid lipid nanoparticles, polymeric micelles, and inorganic nanoparticles. By modality, the market is segmented into mRNA, small molecules, gene editing cargos, siRNA / ASO, peptides, vaccines, DNA, proteins, and therapeutic vaccines.

By service type, the market is segmented into pre-formulation screening, analytical & characterization, aseptic fill-finish & lyophilization, formulation development, GMP clinical manufacturing, tech transfer & comparability, process development & scale-up, GMP commercial manufacturing, stability & method validation.

By application, the market is segmented into oncology, infectious diseases, genetic & metabolic disorders, cardiovascular & metabolic, CNS, ophthalmology, respiratory, and immunology/inflammation. By client type, pharmaceutical and biotechnology companies, academic and research institutes, and contract research organizations. By delivery route, the market is segmented into intravenous, intramuscular, subcutaneous, inhalation, intratumoral, intrathecal, ocular, and oral.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Lipid nanoparticles |

| Nanostructured lipid carriers |

| Dendrimers |

| Liposomes |

| Polymeric nanoparticles |

| Nanoemulsions |

| Solid lipid nanoparticles |

| Polymeric micelles |

| Inorganic nanoparticles |

| mRNA |

| Small molecules |

| Gene editing cargos |

| siRNA / ASO |

| Peptides |

| Vaccines |

| DNA |

| Proteins |

| Therapeutic vaccines |

| Pre-formulation screening |

| Analytical & characterization |

| Aseptic fill-finish & lyophilization |

| Formulation development |

| GMP clinical manufacturing (DP) |

| Tech transfer & comparability |

| Process development & scale-up |

| GMP commercial manufacturing (DP) |

| Stability & method validation |

| Oncology |

| Infectious diseases |

| Genetic & metabolic disorders |

| Cardiovascular & metabolic |

| CNS |

| Ophthalmology |

| Respiratory |

| Immunology/Inflammation |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Contract Research Organizations |

| Intravenous (IV) |

| Intramuscular (IM) |

| Subcutaneous (SC) |

| Inhalation |

| Intratumoral |

| Intrathecal |

| Ocular |

| Oral |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Particle | Lipid nanoparticles | |

| Nanostructured lipid carriers | ||

| Dendrimers | ||

| Liposomes | ||

| Polymeric nanoparticles | ||

| Nanoemulsions | ||

| Solid lipid nanoparticles | ||

| Polymeric micelles | ||

| Inorganic nanoparticles | ||

| By Modality / Payload | mRNA | |

| Small molecules | ||

| Gene editing cargos | ||

| siRNA / ASO | ||

| Peptides | ||

| Vaccines | ||

| DNA | ||

| Proteins | ||

| Therapeutic vaccines | ||

| By Service Type | Pre-formulation screening | |

| Analytical & characterization | ||

| Aseptic fill-finish & lyophilization | ||

| Formulation development | ||

| GMP clinical manufacturing (DP) | ||

| Tech transfer & comparability | ||

| Process development & scale-up | ||

| GMP commercial manufacturing (DP) | ||

| Stability & method validation | ||

| By Application | Oncology | |

| Infectious diseases | ||

| Genetic & metabolic disorders | ||

| Cardiovascular & metabolic | ||

| CNS | ||

| Ophthalmology | ||

| Respiratory | ||

| Immunology/Inflammation | ||

| By Client Type | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Contract Research Organizations | ||

| By Delivery Route | Intravenous (IV) | |

| Intramuscular (IM) | ||

| Subcutaneous (SC) | ||

| Inhalation | ||

| Intratumoral | ||

| Intrathecal | ||

| Ocular | ||

| Oral | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What will be the market size of Nanoparticle Contract Manufacturing Market in 2031?

The Nanoparticle Contract Manufacturing Market size is expected to increase from USD 5.30 billion in 2025 to USD 5.90 billion in 2026 and reach USD 10.10 billion by 2031, growing at a CAGR of 11.41% over 2026-2031.

Which region is projected to grow fastest in outsourced nanoparticle manufacturing?

Asia-Pacific is forecast to post an 11.84% CAGR thanks to large capital projects in China, India, and South Korea.

How do polymeric nanoparticles differ in commercial outlook from lipid systems?

Polymeric platforms will grow at an 11.98% CAGR because they enable oral dosing and controlled release that lipid particles rarely achieve without added complexity.

Why are emerging biotechs heavy users of CMO services?

Start-ups prefer to channel scarce capital toward clinical trials, so they outsource GMP suites and analytics that can cost USD 100 million to build in-house.

Page last updated on: