Lipid Nanoparticles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

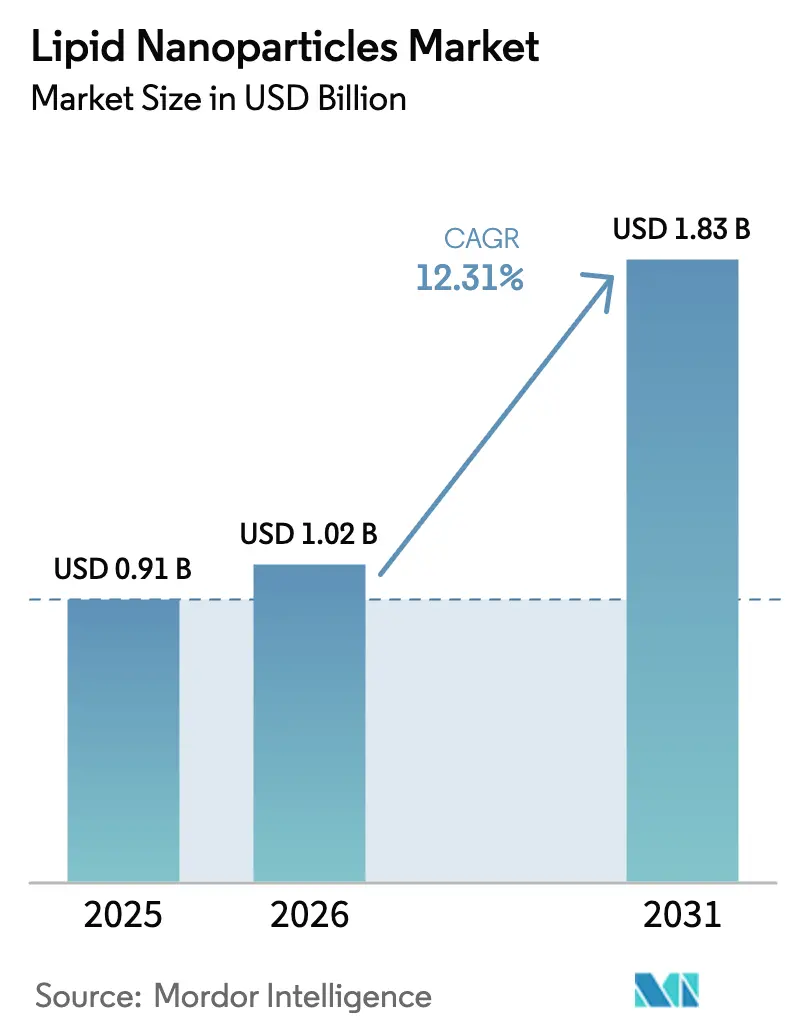

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 12.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lipid Nanoparticles Market Analysis by Mordor Intelligence

Lipid Nanoparticles market size in 2026 is estimated at USD 1.02 billion, growing from 2025 value of USD 0.91 billion with 2031 projections showing USD 1.83 billion, growing at 12.31% CAGR over 2026-2031. This solid mid-teens growth reflects the technology’s evolution from an emergency vaccine vehicle to a versatile carrier for gene therapy, cancer immunotherapy and rare-disease therapeutics. Robust clinical data on in-vivo CAR T cell programming, successful extrahepatic tissue-targeted delivery and continuous-manufacturing productivity gains attract sustained venture and strategic investment. Further momentum comes from the FDA’s 2024 guidance that clarifies non-clinical expectations for oligonucleotide-based products and thereby reduces approval uncertainty for next-generation formulations. Scale-up capacity additions by global CDMOs, especially in Asia-Pacific, are aligning manufacturing throughput with pipeline demand, while artificial-intelligence-designed ionizable lipids expand the therapeutic window across multiple tissue types.

Key Report Takeaways

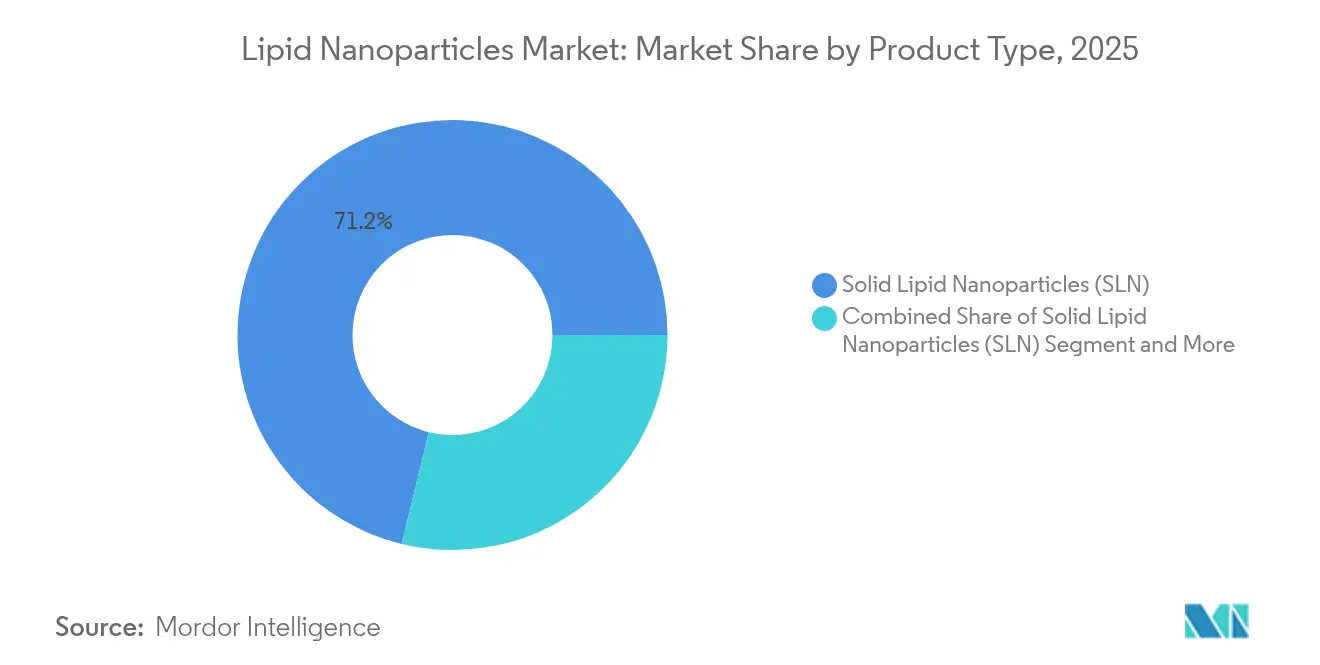

- By product type, solid lipid nanoparticles led with 71.20% of lipid nanoparticles market share in 2025; nanostructured lipid carriers are forecast to expand at a 13.04% CAGR through 2031.

- By application, therapeutic use captured 59.60% of the lipid nanoparticles market size in 2025, while research applications are advancing at a 13.12% CAGR between 2026 and 2031.

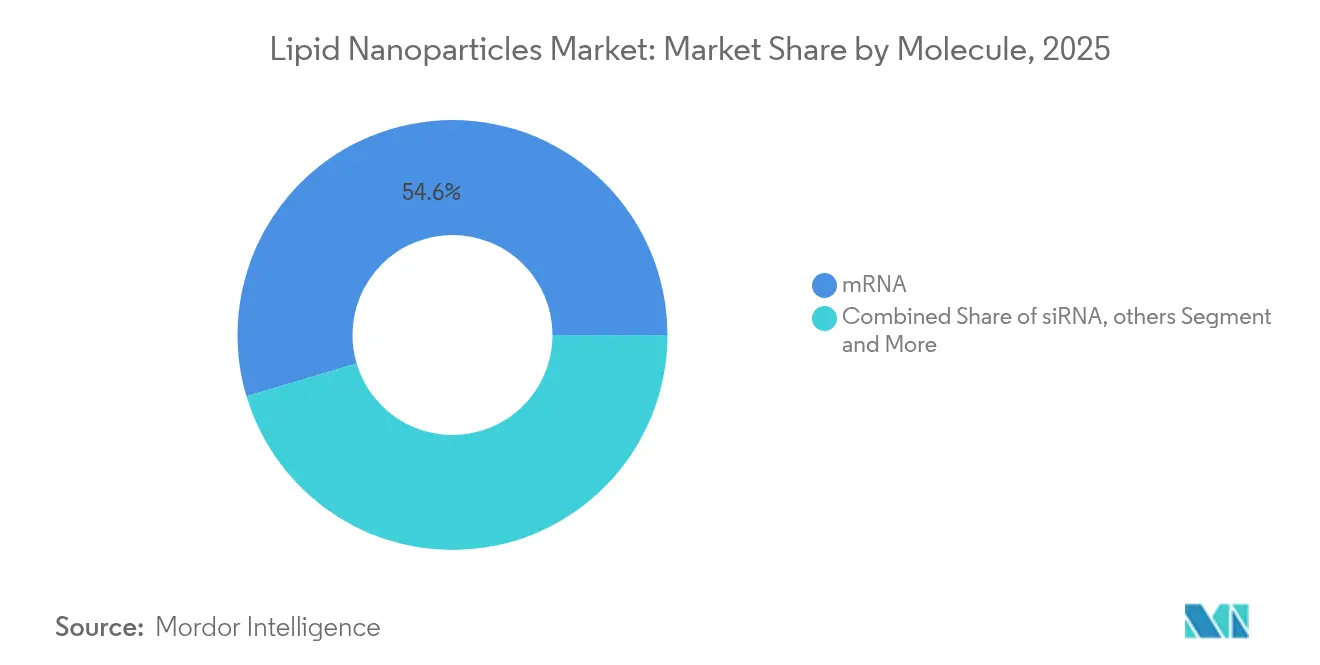

- By molecule, mRNA accounted for 54.60% of the lipid nanoparticles market size in 2025; siRNA molecules are projected to grow at an 11.35% CAGR to 2031.

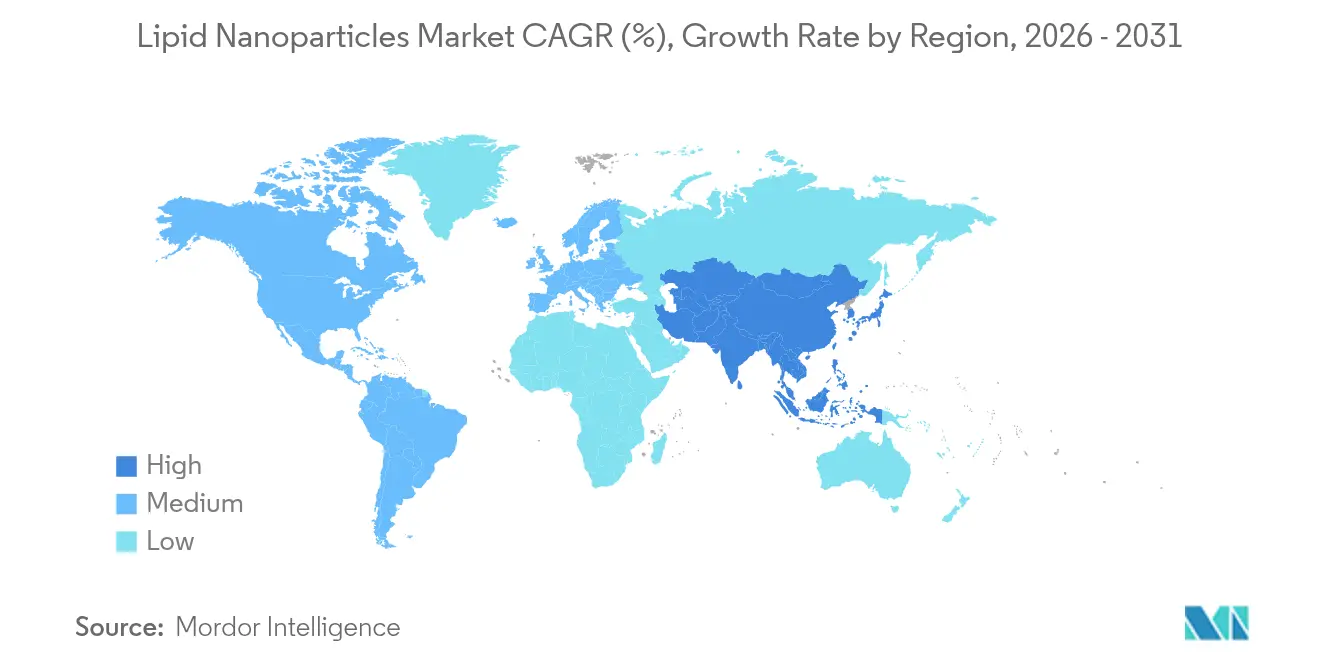

- By geography, North America dominated with 37.90% lipid nanoparticles market share in 2025, whereas Asia-Pacific is set to grow at a 13.78% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lipid Nanoparticles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic and rare diseases | +2.1% | Global, North America & Europe focus | Long term (≥ 4 years) |

| Explosive mRNA-vaccine pipeline beyond COVID-19 | +2.3% | Global, led by North America, expanding to Asia-Pacific | Medium term (2–4 years) |

| Large-scale government pandemic-prep stockpiling | +1.8% | North America & EU dominant, Asia-Pacific emerging | Short term (≤ 2 years) |

| Expansion of CDMO lipid-mixing capacity in Asia-Pacific | +2.0% | Core in Asia-Pacific, spill-over to Middle East & Africa | Medium term (2–4 years) |

| AI-designed ionizable lipids enabling tissue targeting | +2.4% | Global, early adoption in North America | Long term (≥ 4 years) |

| Micro-fluidics-based continuous manufacturing | +1.9% | Global, hubs in North America & Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic and Rare Diseases

Oncology, metabolic and neurological disease burdens are rising worldwide, creating sustained demand for precision delivery platforms that bypass physiological barriers. Lipid nanoparticle-enabled cancer vaccines such as mRNA-4157 combined with pembrolizumab achieved a 44% reduction in tumor recurrence during Phase II studies.[1]Source: Matthias Magoola and Sarfaraz Niazi, “Current Progress and Future Perspectives of RNA-Based Cancer Vaccines: A 2025 Update,” Cancers, mdpi.com More than 120 active clinical trials now evaluate lipid nanoparticle formulations for pancreatic, glioblastoma and monogenic disorders, underscoring the modality’s versatility. The approach is particularly compelling in rare diseases where small populations make conventional bioprocessing economically challenging, yet lipid nanoparticles can deliver DNA-encoded biologics with scalable manufacturing footprints. Sustained research funding in North America and Europe underpins stable long-term demand.

Explosive mRNA-Vaccine Pipeline Beyond COVID-19

COVID-19 validated mRNA technology and compressed development timelines from nine weeks to less than four weeks through continuous-manufacturing adoption, setting a new speed benchmark. As a result, firms now pursue prophylactic and therapeutic mRNA vaccines for influenza, RSV, cytomegalovirus and multiple cancer antigens. First commercial approvals for non-COVID mRNA vaccines are forecast before 2029, supported by improved cold-chain stability and higher-payload nanostructured lipid carriers. Artificial-intelligence pipelines shorten antigen selection cycles, further reinforcing the lipid nanoparticles market growth prospects.

Large-Scale Government Pandemic-Prep Stockpiling

Agencies such as BARDA finance domestic active pharmaceutical ingredients and finished vaccine reserves to avoid shortages experienced in previous years. Funding extends to ionizable lipids, mixing equipment, and microfluidics skids, creating predictable baseline volumes that derisk private capacity expansion. The strategy also pushes suppliers to meet stringent quality documentation requirements, indirectly raising industry standards.

Expansion of CDMO Lipid-Mixing Capacity in Asia-Pacific

Regional contractors in Singapore, South Korea and India add microfluidics lines dedicated to lipid nanoparticle assembly, leveraging local raw-material supply chains to compress lead times and reduce cost. Wacker and CordenPharma both commissioned specialized facilities in 2024 that offer end-to-end formulation to commercial fill-finish services. Flexible capacity attracts Western biopharma clients seeking diversified supply networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent CMC and immunogenicity data requirements | -2.1% | Global, strictest in North America & EU | Long term (≥ 4 years) |

| High-purity ionizable lipid price volatility | -1.7% | Global, supply concentration in North America & EU | Short term (≤ 2 years) |

| Environmental footprint of solvent-heavy processes | -1.5% | EU primary, expanding to North America & Asia-Pacific | Medium term (2–4 years) |

| Loading-capacity ceiling of legacy SLN platforms | -1.9% | Global, affecting established manufacturers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent CMC and Immunogenicity Data Requirements

Post-emergency regulatory pathways now demand full chemistry, manufacturing and controls packages including long-term immunogenicity monitoring, histopathology and off-target biodistribution studies. The FDA’s November 2024 draft guidance on oligonucleotide therapeutics formalized extensive toxicology expectations that extend development timelines, especially for small biotechnology firms with limited regulatory infrastructure.[2]Source: Food and Drug Administration, “Nonclinical Safety Assessment of Oligonucleotide-Based Therapeutics; Draft Guidance for Industry,” federalregister.gov The need for chronic-toxicity studies and comparative impurity profiling increases cost hurdles.

High-Purity Ionizable Lipid Price Volatility

A handful of qualified suppliers control the majority of pharmaceutical-grade ionizable lipid output. During pandemic surges, list prices for proprietary lipids tripled as demand outpaced capacity. Lot-to-lot variability also forces buyers to institute extensive incoming quality testing, adding both time and expense. This volatility motivates strategic partnerships, vertical integration and larger safety-stock holdings, yet near-term margin pressure persists. This supply constraint has prompted pharmaceutical companies to diversify supplier networks and invest in backward integration strategies to secure reliable raw material access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: SLN Dominance Faces NLC Innovation

Solid lipid nanoparticles held 71.20% market share in 2025 on the strength of validated manufacturing know-how and an installed base of filling lines. Yet nanostructured lipid carriers are forecast to post a 13.04% CAGR through 2031, reflecting higher drug-loading ceiling and improved colloidal stability which directly translate to lower dose volumes and extended shelf life. As oncology programs escalate dose requirements, NLC formulations become attractive despite higher raw-material cost. The lipid nanoparticles market therefore shows a gradual shift in revenue mix toward NLC as sponsors favor performance over cost. Suppliers co-locate NLC skids with existing SLN infrastructure, maintaining throughput flexibility while leveraging common raw materials and quality systems.

Process innovation further narrows cost differentials. Continuous microfluidics yields consistent NLC particle-size distributions that rival or exceed SLN homogeneity. Hybrid constructs that blend solid and liquid lipids appear in exploratory studies targeting intracellular organelles, expanding formulation toolkits. Lipid liquid-crystalline nanoparticles also gain traction for membrane-protein delivery, highlighting the industry’s pivot from single-molecule payloads to complex multimodal cargos. As intellectual-property roofs expire, generic SLN entrants could pressure pricing, further encouraging differentiation through NLC.

By Application: Therapeutics Lead While Research Accelerates

Therapeutic use retained 59.60% of 2025 revenue and remains the principal investor draw given multiple late-stage clinical programs. Oncology, infectious disease and cardiology drive near-term commercial volumes, with pipeline breadth signaling persistent demand. However, research applications are set to grow 13.12% annually to 2031 as standardized nanoparticle kits simplify lab adoption. The lipid nanoparticles market benefits from this dual flywheel: research spending uncovers new indications, while clinical proof reallocates venture capital into translational projects.

Academic demand spikes due to grant support for extrahepatic delivery exploration, including pulmonary and ocular targets. Off-the-shelf starter kits from CordenPharma democratize formulation access, and cloud-based design tools guide lipid choices in silico. As equipment miniaturizes and costs fall, start-ups leverage desktop microfluidic systems to generate GMP-ready toxicology batches, accelerating pre-clinical timelines. The virtuous cycle of discovery, validation and commercialization supports sustained pipeline depth.

By Molecule: mRNA Dominance Challenged by siRNA Growth

mRNA cargos captured 54.60% of lipid nanoparticles market size in 2025 due to pandemic vaccine revenues and expanding cancer vaccine trials. Although growth moderates from the exceptional 2020-2023 period, oncology and infectious disease pipelines keep unit volumes elevated. siRNA is projected to climb at an 11.35% CAGR, buoyed by cardiovascular candidates such as lepodisiran targeting lipoprotein(a) where Phase II data show significant lowering of the pathogenic particle. Delivery breakthroughs that enable sustained extrahepatic silencing further improve clinical feasibility.

DNA plasmids and CRISPR components remain niche today but present upside as editing specificity issues resolve. Successful delivery of 10 kb DNA templates in mice demonstrates the lipid nanoparticles industry’s expanding payload envelope. The market therefore anticipates a diversified mix where multiple nucleic-acid classes coexist, each requiring tailored lipid chemistry.

By End User: Pharma Leads While Academia Drives Innovation

Pharmaceutical and biotechnology companies generated 57.80% of revenue in 2025, deploying internal GMP suites or outsourcing to dedicated CDMOs for commercial batches. Their focus is regulatory compliance, scale and product-life-cycle management. Academia and research institutes are projected to expand fastest at 13.52% CAGR through 2031, riding increased grant allocations and kit-based entry solutions. This group drives early-stage hypothesis testing and unearths novel delivery paradigms such as in-vivo CAR T cell reprogramming pioneered by Capstan Therapeutics.

CDMOs occupy a bridging role, offering formulation screening, analytical characterization and fill-finish support to both early-stage inventors and Big Pharma. Danaher’s 2024 buyout of Precision NanoSystems signaled escalating strategic interest in owning platform capabilities, foreshadowing further consolidation among service providers. Other end users such as veterinary health and agro-biotech emerge, though revenue remains immaterial today.

Geography Analysis

North America remained the largest regional contributor with 37.90% revenue in 2025 owing to mature biopharmaceutical infrastructure, deep venture funding pools and clear regulatory precedents. The United States maintains a robust pipeline of oncology and rare-disease programs, and BARDA’s strategic stockpiling guarantees baseline demand. Canada benefits from policy incentives such as the Strategic Innovation Fund, which subsidizes domestic mRNA vaccine facilities located in Quebec and British Columbia.

Europe holds the second-largest share, supported by Germany’s and the United Kingdom’s manufacturing expansions. The European Medicines Agency harmonizes with FDA guidelines yet imposes additional environmental and solvent-emission requirements that foster greener production technology. France’s Grand-Est region offers tax credits for lipid nanoparticle research, luring start-ups and multinational R&D centers. Cross-border collaboration via Horizon Europe funds projects on targeted lipid design and GMP microfluidic scale-up, strengthening the regional knowledge base.

Asia-Pacific is the fastest-growing territory with a forecast 13.78% CAGR to 2031 thanks to aggressive CDMO capacity build-outs, competitive pricing and supportive government funding. Singapore’s Tuas biomedical hub houses continuous-manufacturing lines capable of both clinical and commercial run rates. South Korea’s BioKorea policy grants tax holidays on equipment imports, accelerating installation of solvent-recovery modules necessary for green compliance. Japan’s Pharmaceuticals and Medical Devices Agency streamlines priority review for nucleic-acid therapeutics, reducing time-to-market. China’s local players focus on generic mRNA vaccines, yet intellectual-property uncertainty hampers Western outsourcing despite attractive cost structures. Middle East and Africa register nascent activity focused on pandemic-preparedness technology transfer agreements, while South America sees sporadic academic programs. These regions remain future expansion frontiers as healthcare budgets and biomanufacturing policies mature.

Competitive Landscape

The lipid nanoparticles market is moderately fragmented with a mix of vaccine powerhouses, specialized formulation vendors and disruptive start-ups. Acuitas Therapeutics licenses GenVoy technology to multiple collaborators, underpinning broad platform adoption. Danaher’s Precision NanoSystems deal consolidated key microfluidic lipid-mixing IP and added a Vancouver-based GMP site to its Cytiva network, illustrating strategic convergence between equipment and service businesses.

Competition now centers on lipid chemistry innovation rather than solely manufacturing scale. AI-assisted design accelerates discovery of ionizable lipids with bespoke pKa values, biodegradability and tissue specificity. Capstan Therapeutics raised USD 175 million to advance in-vivo CAR T cell programming, eliminating ex-vivo cell-processing bottlenecks and potentially unlocking autoimmune indications. Emerging suppliers such as Entos Pharmaceuticals pursue fusogenic lipid architectures that promise higher endosomal escape efficiency.

Partnerships dominate go-to-market strategies. Bayer collaborates with Acuitas on liver-targeted RNA payloads, while AstraZeneca secures CDMO slots in Singapore to hedge capacity risk. Venture funding remains healthy, yet inflated lipid prices temper near-term margins, prompting co-development agreements that share raw-material exposure. Intellectual-property battles over proprietary ionizable lipids intensify, with several lawsuits pending in United States federal courts.

Lipid Nanoparticles Industry Leaders

Merck KGaA

Arcturus Therapeutics, Inc.

Ascendia Pharmaceuticals

Acuitas Therapeutics

Croda International Plc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: A Cornell University team unveiled “stealthy” lipid nanoparticles that replace a commonly used component likely to trigger innate immune responses, enhancing mRNA vaccine tolerability.

- February 2024: CordenPharma introduced Lipid Nanoparticle Starter Kits aimed at accelerating lab-scale formulation of mRNA therapeutics.

- June 2023: Bayer AG partnered with Acuitas Therapeutics to deploy GenVoy lipid nanoparticle technology for in-vivo gene-editing programs targeting liver diseases.

Global Lipid Nanoparticles Market Report Scope

Lipid-based nanoparticles (LNPs) are a highly adaptable class of nanocarriers that have gained widespread usage in medical research and pharmacology. They encapsulate various therapeutic agents for multiple applications, including small molecules, nucleic acids, and monoclonal antibodies. These engineered nanocarriers hold the potential to overcome significant limitations of traditional therapeutic products, such as inadequate efficacy, susceptibility to enzymatic degradation, low bioavailability, and off-target side effects.

The lipid nanoparticles market is segmented into type, application, end user, and geography. By type, the market is segmented into solid lipid nanoparticles, nanostructured lipid carriers, and other types. By application, the market is segmented into research and therapeutics. By end-user, the market is segmented into pharmaceutical and biotechnology companies, contract development and manufacturing organizations, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report also offers the market size and forecasts for 13 countries across the region. The report offers the value (USD) for the above segments.

| Solid Lipid Nanoparticles (SLN) |

| Nanostructured Lipid Carriers (NLC) |

| Other Types |

| Research |

| Therapeutics |

| siRNA |

| mRNA |

| Others |

| Pharmaceutical and Biotechnology Companies |

| Contract Development & Manufacturing Organizations |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Solid Lipid Nanoparticles (SLN) | |

| Nanostructured Lipid Carriers (NLC) | ||

| Other Types | ||

| By Application | Research | |

| Therapeutics | ||

| By Molecule | siRNA | |

| mRNA | ||

| Others | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Contract Development & Manufacturing Organizations | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the lipid nanoparticles market?

The lipid nanoparticles market size reached USD 1.02 billion in 2026 and is forecast to grow to USD 1.83 billion by 2031.

Which product type holds the largest share?

Solid lipid nanoparticles dominated with 71.20% share in 2025, though nanostructured lipid carriers are growing faster at a 13.04% CAGR.

Which geographic region is expanding most quickly?

Asia-Pacific is projected to record a 13.78% CAGR between 2026 and 2031 due to strong CDMO investments and supportive government policies.

What molecule class leads current applications?

MRNA payloads account for 54.60% of revenue, yet siRNA is the fastest-rising molecule class with an 11.35% CAGR outlook.

How are AI tools influencing lipid nanoparticle development?

Artificial-intelligence platforms design ionizable lipids with targeted biodistribution profiles, enabling delivery to organs beyond the liver and expanding clinical possibilities.

What manufacturing innovation is most transformative?

Microfluidics-based continuous manufacturing improves batch consistency, reduces solvent usage and shortens production cycles, supporting rapid clinical supply.

Page last updated on: