Medical And Pharmaceutical-Grade Polymers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

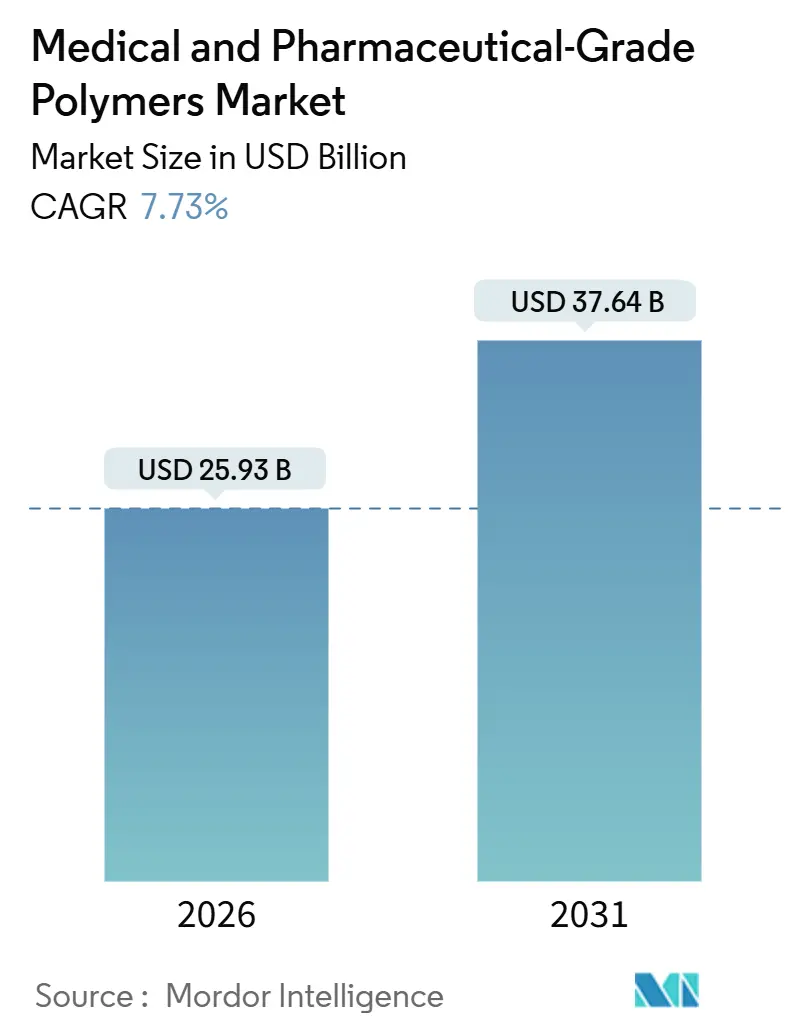

| Market Size (2026) | USD 25.93 Billion |

| Market Size (2031) | USD 37.64 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

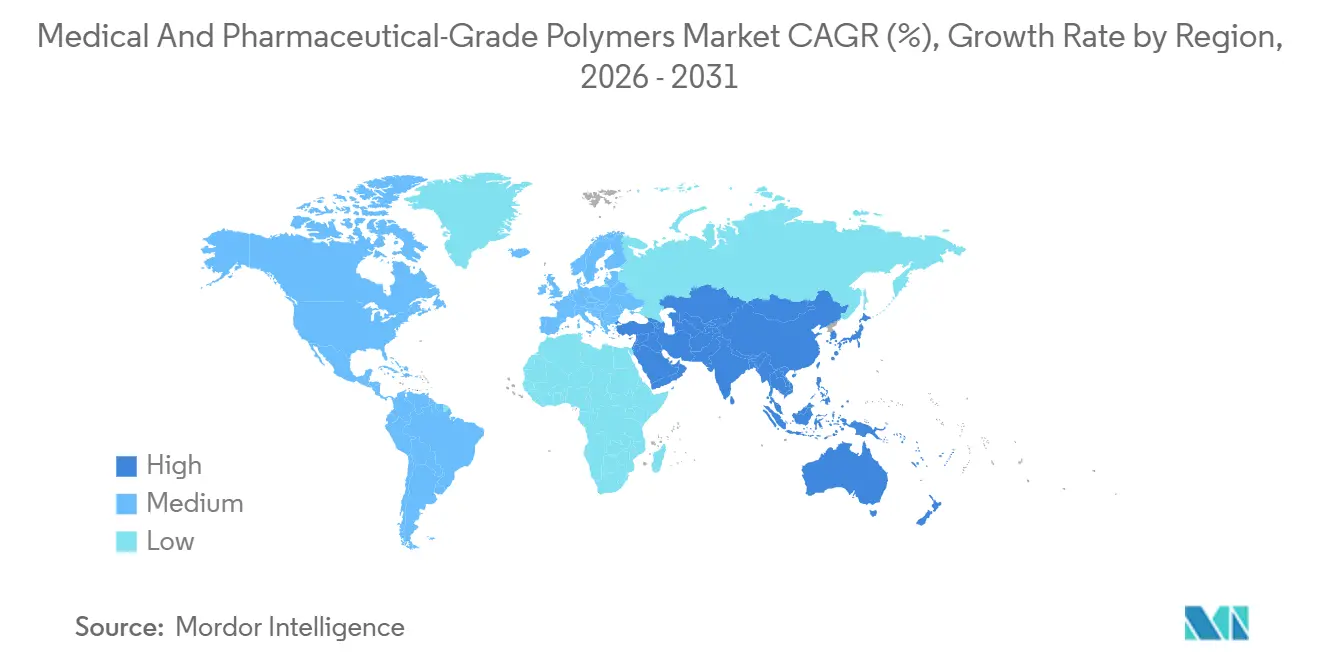

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical And Pharmaceutical-Grade Polymers Market Analysis by Mordor Intelligence

The Medical And Pharmaceutical-Grade Polymers Market size is estimated at USD 25.93 billion in 2026, and is expected to reach USD 37.64 billion by 2031, at a CAGR of 7.73% during the forecast period (2026-2031).

Hospitals are phasing out reusable instruments in favor of single-use sterile sets; point-of-care diagnostics require ultra-pure resins that meet ISO 10993 and USP Class VI standards; and regulators worldwide are restricting endocrine-disrupting additives. Device makers are therefore accelerating shifts toward phthalate- and BPA-free, bio-based feedstocks to limit Scope 3 emissions. Demographic aging in North America, Europe, and Japan is driving demand for implantable and wearable drug-delivery platforms made from high-performance thermoplastics and biodegradable polyesters. Meanwhile, patent activity for AI-optimized 3D printing is expanding the addressable base of patient-specific implants that leverage lattice geometries impossible to replicate via molding.

Key Report Takeaways

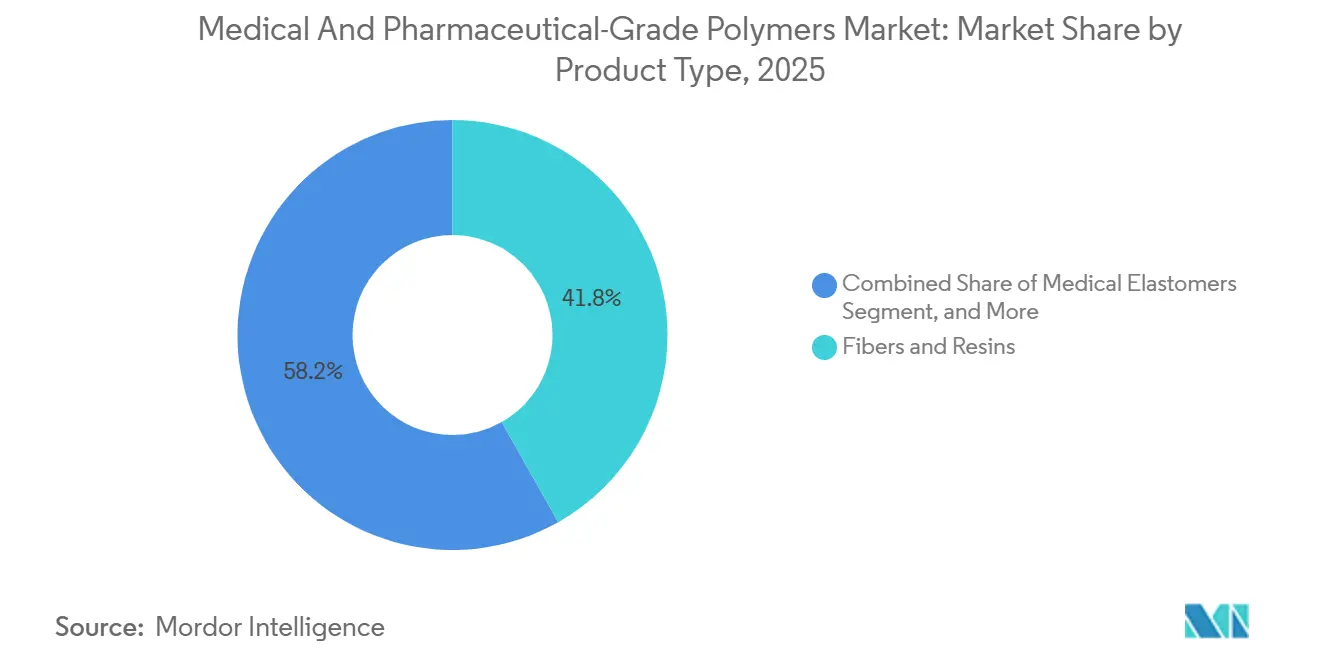

- By product type, fibers and resins led the medical and pharmaceutical grade polymers market with 41.81% share in 2025, while biodegradable polymers are advancing at a 9.26% CAGR through 2031.

- By application, medical devices accounted for 48.07% of revenue in 2025, but drug-delivery systems are projected to expand at an 8.36% CAGR through 2031.

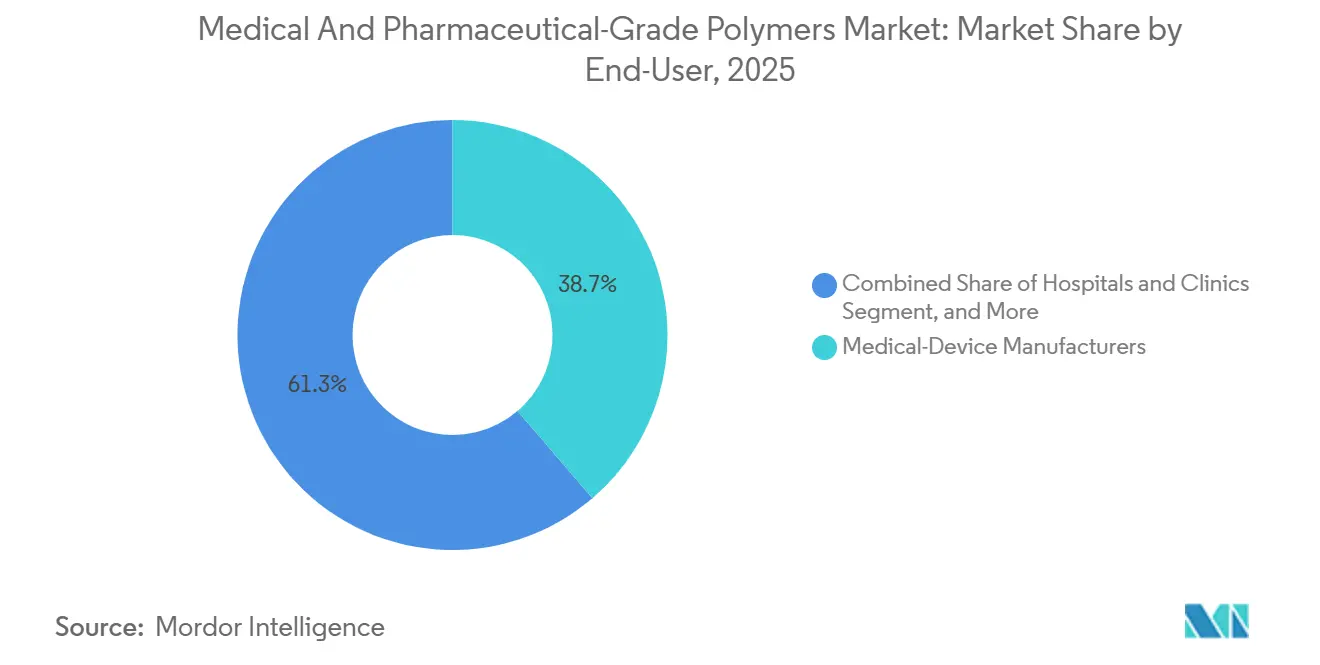

- By end user, medical device manufacturers held 38.72% of the value in 2025; contract manufacturing organizations are growing at a 10.41% CAGR during 2026-2031.

- By geography, North America dominated with a 41.83% share in 2025; Asia-Pacific is forecast to post an 11.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical And Pharmaceutical-Grade Polymers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic Shift to Chronic-Disease and Aging Care | +1.8% | Global, especially North America, Western Europe, Japan | Long term (≥ 4 years) |

| Point-of-Care Device Boom Demanding High-Purity Polymers | +1.5% | Global, led by North America, Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Single-Use Sterile Systems to Curb HAIs | +1.4% | North America, Europe, spillover to MEA | Short term (≤ 2 years) |

| Regulatory Push for DEHP-Free & BPA-Free Formulations | +1.2% | Europe, North America, China | Medium term (2-4 years) |

| Bio-Feedstock & CO₂-Capture Routes Lowering Scope-3 Footprint | +0.9% | Europe, North America | Long term (≥ 4 years) |

| AI-Enabled Polymer 3D Printing for Patient-Specific Implants | +0.7% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demographic Shift to Chronic-Disease and Aging Care

Rising life expectancy is swelling the global population aged 65 and above to 1.03 billion by 2030, from 771 million in 2022. Chronic disorders such as diabetes, heart failure, and osteoarthritis, therefore, require long-lived implants formed from polyether ether ketone, polysulfone, and ultra-high-molecular-weight polyethylene that resist in vivo protein fouling. Japan recorded a 22% increase in hip-replacement surgeries among citizens aged 70 and older during 2023-2025, driving demand for ultraclean acetabular liners.[1]Ministry of Health, Labour and Welfare Japan, “Orthopedic Surgery Statistics 2025,” mhlw.go.jp At-home chronic-disease management also favors hypoallergenic silicone elastomers certified to ISO 10993-10.

Point-of-Care Device Boom Demanding High-Purity Polymers

The U.S. FDA cleared 47 point-of-care molecular tests in 2025, up from 24 in 2023, sharply increasing the need for cyclic olefin copolymer cartridges with sub-10-ppm extractables. Celanese opened a 15,000-ton COC plant in Texas to serve rapid-diagnostics customers.[2]Celanese Corporation, “COC Capacity Expansion Texas,” celanese.com Rural clinics in India and sub-Saharan Africa now deploy ambient-stable reagent strips in polystyrene cassettes, widening geographic uptake.

Shift Toward Single-Use Sterile Systems to Curb HAIs

Healthcare-associated infections afflict 1 in 31 U.S. patients each day.[3]Centers for Disease Control and Prevention, “Healthcare-Associated Infections Progress Report,” cdc.gov Disposable surgical kits, IV sets, and breathing circuits made of polypropylene and thermoplastic elastomers minimize reprocessing missteps. WHO’s 2024 infection-prevention guidance ratified the adoption of gamma-sterilizable polymers. European hospitals cut central-line infections 31% between 2023 and 2025 by switching to antimicrobial polyurethane catheters.

Regulatory Push for DEHP-Free & BPA-Free Formulations

ECHA added four phthalates to the REACH Candidate List in January 2025, and the U.S. FDA advised neonatal devices to avoid ortho-phthalates altogether. China’s revised GB 15593 halves DEHP migration limits. Device OEMs are reformulating IV bags and feeding tubes with polyolefin films and thermoplastic polyurethane that require no plasticizer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Petro-Feedstock Pricing & Supply-Chain Shocks | -1.1% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Stringent ISO 10993 / USP <88> Biocompatibility Hurdles | -0.8% | North America, Europe | Medium term (2-4 years) |

| Hospital Zero-Waste Mandates Targeting Single-Use Plastics | -0.6% | Europe, California, select APAC cities | Medium term (2-4 years) |

| Talent Shortage in GMP-Grade Polymer Compounding | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Feedstock Pricing & Supply-Chain Shocks

Brent crude averaged USD 82 per barrel in 2025 but spiked by 15% in Q3 amid Middle East disruptions, squeezing resin margins. Hurricane-related force majeures on the U.S. Gulf Coast lifted polypropylene spot prices by 22%, delaying syringe production. Smaller Asian compounders that import 70% of feedstock faced currency hedging costs that eroded profits.

Stringent ISO 10993 and Biocompatibility Hurdles

The 2020 revision of ISO 10993-18 added extractable thresholds that many labs cannot test in-house. A single polymer grade can require USD 1 million and 24 months of evaluations. FDA’s 2025 draft guidance on long-term implants now calls for in vivo carcinogenicity studies, adding USD 400,000 and two years. Mid-tier suppliers, therefore, hesitate to introduce novel bio-based or recycled resins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biodegradables Outpace Legacy Resins

Fibers and resins retained a 41.81% share in 2025, anchoring syringe barrels and IV tubing built from polypropylene, polyethylene, and polyvinyl chloride. Yet biodegradable grades are posting the fastest 9.26% CAGR into 2031 as resorbable sutures, stents, and drug-delivery matrices migrate to polylactic acid, polyglycolic acid, and polycaprolactone. FDA cleared nine bioresorbable vascular scaffolds in 2025, more than doubling the number of approvals from 2023. Evonik’s RESOMER line captured 18% of global demand for implantable bioresorbable materials in 2025, demonstrating a first-mover advantage.

Premium high-performance polymers such as polyether ether ketone, polysulfone, and liquid-crystal polymers are used in spinal fusion cages, dialysis membranes, and miniature connector housings, leveraging their chemical inertia and sustained mechanical strength. Medical elastomers silicone, thermoplastic polyurethane, styrenic block copolymers enable catheter balloons, wound dressings, and wearable sensors that require steam-sterilizable elasticity. Other product types, including medical foams and pressure-sensitive adhesives, remain subscale today but are finding niches in negative-pressure wound therapy and multi-day transdermal patches.

By Application: Drug Delivery Gains on Devices

Medical devices accounted for 48.07% of 2025 revenue, driven by diagnostic instruments, surgical tools, and patient monitors that require dimensionally stable housings. However, drug-delivery systems are logging an 8.36% CAGR through 2031 as biologics migrate into self-injector pens and wearable pumps that boost adherence. Cyclic olefin polymer vials and cartridges reduce protein adsorption, commanding a 25% premium over glass.

Implants and prosthetics use high-performance polymers with decades of fatigue resistance. The American Academy of Orthopaedic Surgeons tallied 1.2 million hip and knee arthroplasties in 2025, and ultra-high-molecular-weight polyethylene liners represented 80% of bearings. Pharmaceutical and biologics packaging also grows steadily as serialization mandates under the U.S. Drug Supply Chain Security Act drive demand for tamper-evident polypropylene caps baked with RFID labels.

By End-User: CMOs Capture Outsourcing Wave

Medical-device OEMs accounted for 38.72% of end-user value in 2025, vertically integrating compounding and molding to protect intellectual property and ensure uninterrupted resin supply. Yet contract manufacturing organizations are expanding 10.41% annually to 2031 as mid-tier innovators outsource non-core processing. FDA-registered CMOs in Malaysia, Thailand, and Vietnam offer ISO 13485-certified cleanrooms at 20-30% lower conversion costs, spurring the relocation of tubing, catheter, and diagnostic-kit production. The medical-grade polymers industry benefits from that shift because CMOs typically source specialty grades in higher annual volumes than device OEMs operating single-site plants.

Hospitals and clinics shape resin choices through value-analysis committees that balance infection control with sustainability budgets. Pharma and biotech companies are investing in polymer characterization labs; Eli Lilly inaugurated a 50,000-square-foot center in Indiana during 2025, de-risking primary packaging qualification. Academic and veterinary end users form a fragmented tail that prefers off-the-shelf catalog compounds, offering stable baseline demand.

Geography Analysis

North America accounted for 41.83% of 2025 revenue, supported by the United States’ USD 4 trillion healthcare outlay and FDA programs that prioritize domestic production with Certificate-of-Foreign-Exports. The Inflation Reduction Act’s manufacturing tax credits, extended through 2026, subsidize cleanroom extruders and injection presses, prompting Eastman to add 8,000 tons of Tritan copolyester capacity in Tennessee. Canada’s harmonized device rules unlock cross-border flows, while Mexico’s maquiladora factories assemble IV-therapy kits using U.S.-sourced resins duty-free. Hospital consolidation and Medicare price pressures nevertheless squeeze device margins, forcing resin suppliers to emphasize total cost of ownership arguments.

Asia-Pacific is forecast to expand at an 11.03% CAGR to 2031, the fastest worldwide. China’s National Medical Products Administration approved 142 Class III devices in 2025, including polymer-based heart valves and degradable screws, thereby reducing reliance on imports. India’s Production-Linked Incentive scheme offers a 5% rebate on incremental device sales, catalyzing local compounding by Poly Medicure and Hindustan Syringes & Medical Devices. Japan’s super-aged population channels procurement toward home-care devices such as portable oxygen concentrators with polycarbonate shells, and South Korea’s fast-track digital-health approvals spur uptake of flexible-film substrates.

Europe remains shaped by the Medical Device Regulation (MDR) and the In Vitro Diagnostic Regulation (IVDR), which have tightened post-market surveillance. Notified-body bottlenecks delayed 40% of legacy recertifications in 2024, creating intermittent shortages that continued in 2025. Germany hosts BASF, Covestro, and Evonik prime suppliers of thermoplastic polyurethane and engineering-resin grades while France and Italy focus on single-use sterile tubing for biologics. The United Kingdom’s dual CE/UKCA regime forces suppliers to carry duplicate inventories until 2029. The Middle East and Africa are growing off a small base; Saudi Arabia’s SFDA approved 89 devices in 2025, encouraging regional distributors to stock ISO 10993-certified resins. South America’s expansion is concentrated in Brazil, but currency volatility and import tariffs weigh on margins.

Competitive Landscape

The medical and pharmaceutical grade polymers market is moderately fragmented. Their competitive edge rests on legacy biocompatibility files, vertically integrated feedstocks, and sustainability roadmaps. Teknor Apex, Lubrizol Life Sciences, and Raumedic differentiate by offering rapid prototyping, antimicrobial masterbatches, and customer-specific tack modifiers within eight-week lead times. WIPO logged 340 additive-manufacturing patent filings in 2025, up 40% year-on-year, led by Evonik, Arkema, and DSM Engineering Materials for antimicrobial fibers and bio-based polyamides.

Strategic moves illustrate consolidation and capacity acceleration. Dow commissioned a USD 180 million silicone-elastomer plant in Zhangjiagang, China, in March 2025 to serve catheter-balloon and wearable-sensor markets. BASF and Sinopec inaugurated a bio-based polybutylene succinate joint venture in Nanjing, targeting 30,000 tons per year, in November 2025. Saint-Gobain acquired a Singapore-based silicone-tubing specialist in 2025, strengthening its reach in the biologics supply chain.

White-space opportunities center on flexible electronics for continuous glucose monitors and smart wound dressings that demand stretchable thermoplastic polyurethane and silicone-polycarbonate copolymers. Less than a dozen suppliers can mass-produce substrates that survive cyclic bending without conductivity loss. AI-driven inline spectroscopy is now differentiating leaders that achieve six-sigma quality; laggards relying on batch-release testing experience 15-20% scrap.

Medical And Pharmaceutical-Grade Polymers Industry Leaders

-

BASF SE

-

W. L. Gore & Associates

-

Celanese Corporation

-

Evonik Industries AG

-

Fresenius SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BASF and Sinopec formed a joint venture to produce bioattributed polybutylene succinate at 30,000 tons per year in Nanjing.

- March 2025: Dow inaugurated a USD 180 million silicone-elastomer plant in Zhangjiagang, China, with a capacity of 25,000 tons for catheter balloons and wearables.

Global Medical And Pharmaceutical-Grade Polymers Market Report Scope

The Medical & Pharmaceutical-Grade Polymers Market is the global industry that encompasses the production, supply, and commercialization of high-performance, biocompatible, and regulatory-compliant polymer materials, specifically engineered and certified for use in medical devices, pharmaceutical applications, drug delivery systems, and healthcare products.

The Medical & Pharmaceutical-Grade Polymers Market Report is Segmented by Product Type (Fibers & Resins, Medical Elastomers, Biodegradable Polymers, High-Performance Polymers, Other Product Types), Application (Medical Devices, Pharmaceutical & Biologics Packaging, Drug-Delivery Systems, Implants & Prosthetics, Other Applications), End-User (Medical-Device Manufacturers, Hospitals & Clinics, Pharma & Biotech Companies, Contract Manufacturing Organizations, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Fibers & Resins |

| Medical Elastomers |

| Biodegradable Polymers |

| High-Performance Polymers |

| Other Product Types |

| Medical Devices |

| Pharmaceutical & Biologics Packaging |

| Drug-Delivery Systems |

| Implants & Prosthetics |

| Other Applications |

| Medical-Device Manufacturers |

| Hospitals & Clinics |

| Pharma & Biotech Companies |

| Contract Manufacturing Organizations |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Fibers & Resins | |

| Medical Elastomers | ||

| Biodegradable Polymers | ||

| High-Performance Polymers | ||

| Other Product Types | ||

| By Application | Medical Devices | |

| Pharmaceutical & Biologics Packaging | ||

| Drug-Delivery Systems | ||

| Implants & Prosthetics | ||

| Other Applications | ||

| By End-User | Medical-Device Manufacturers | |

| Hospitals & Clinics | ||

| Pharma & Biotech Companies | ||

| Contract Manufacturing Organizations | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical and pharmaceutical grade polymers market?

The market is valued at USD 25.93 billion in 2026.

How fast is the medical-grade polymers market expected to grow?

It is projected to register a 7.73% CAGR through 2031.

Which product type is expanding the quickest?

Biodegradable polymers are rising at a 9.26% CAGR due to resorbable sutures and implants.

Which region will see the fastest growth?

Asia-Pacific is forecast to post an 11.03% CAGR between 2026 and 2031.

Why are contract manufacturing organizations gaining share?

Mid-tier device firms are outsourcing compounding and molding to ISO 13485-certified CMOs to trim costs and speed market entry.

Page last updated on: