Nanorobots In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

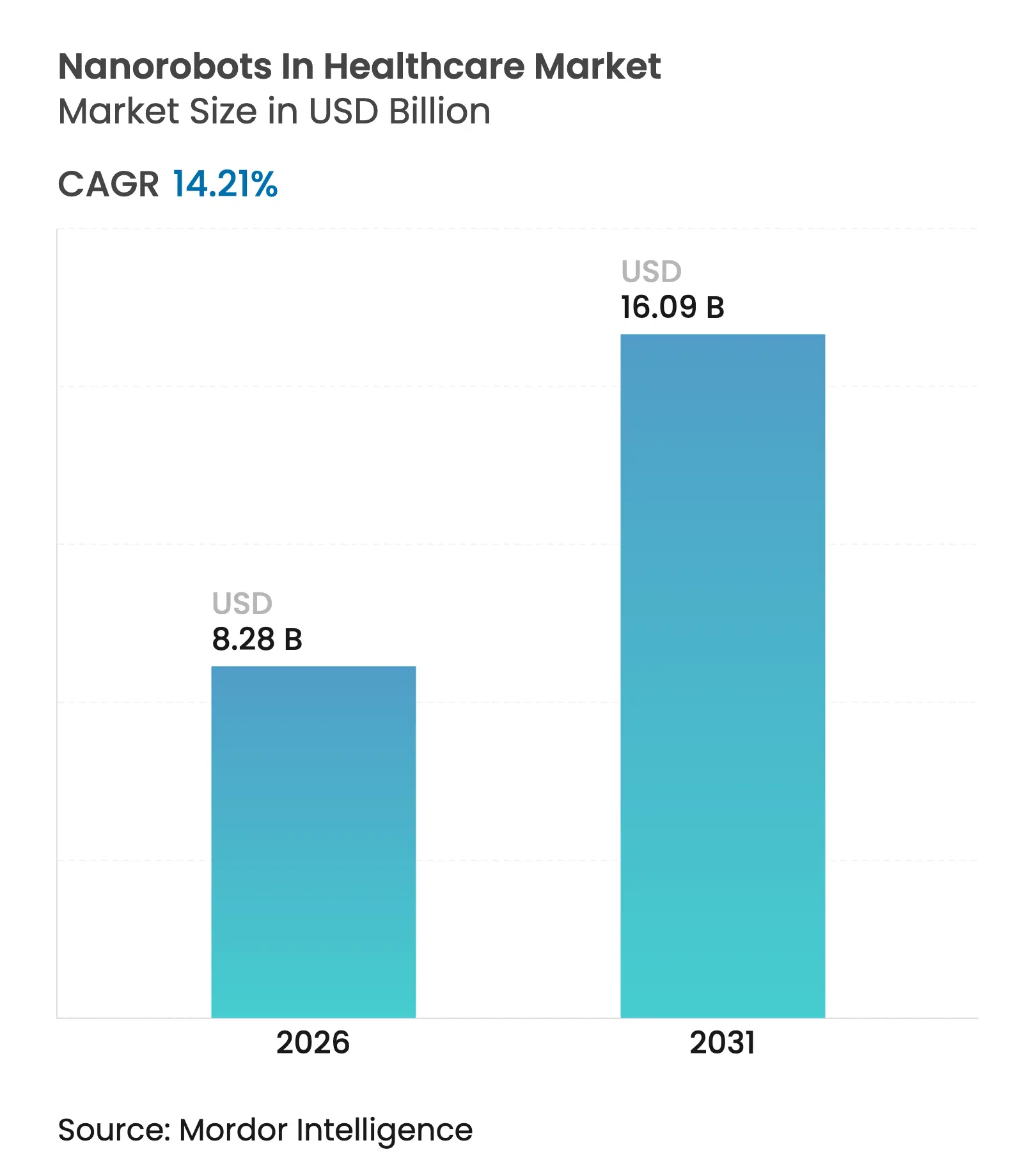

| Market Size (2026) | USD 8.28 Billion |

| Market Size (2031) | USD 16.09 Billion |

| Growth Rate (2026 - 2031) | 14.21 % CAGR |

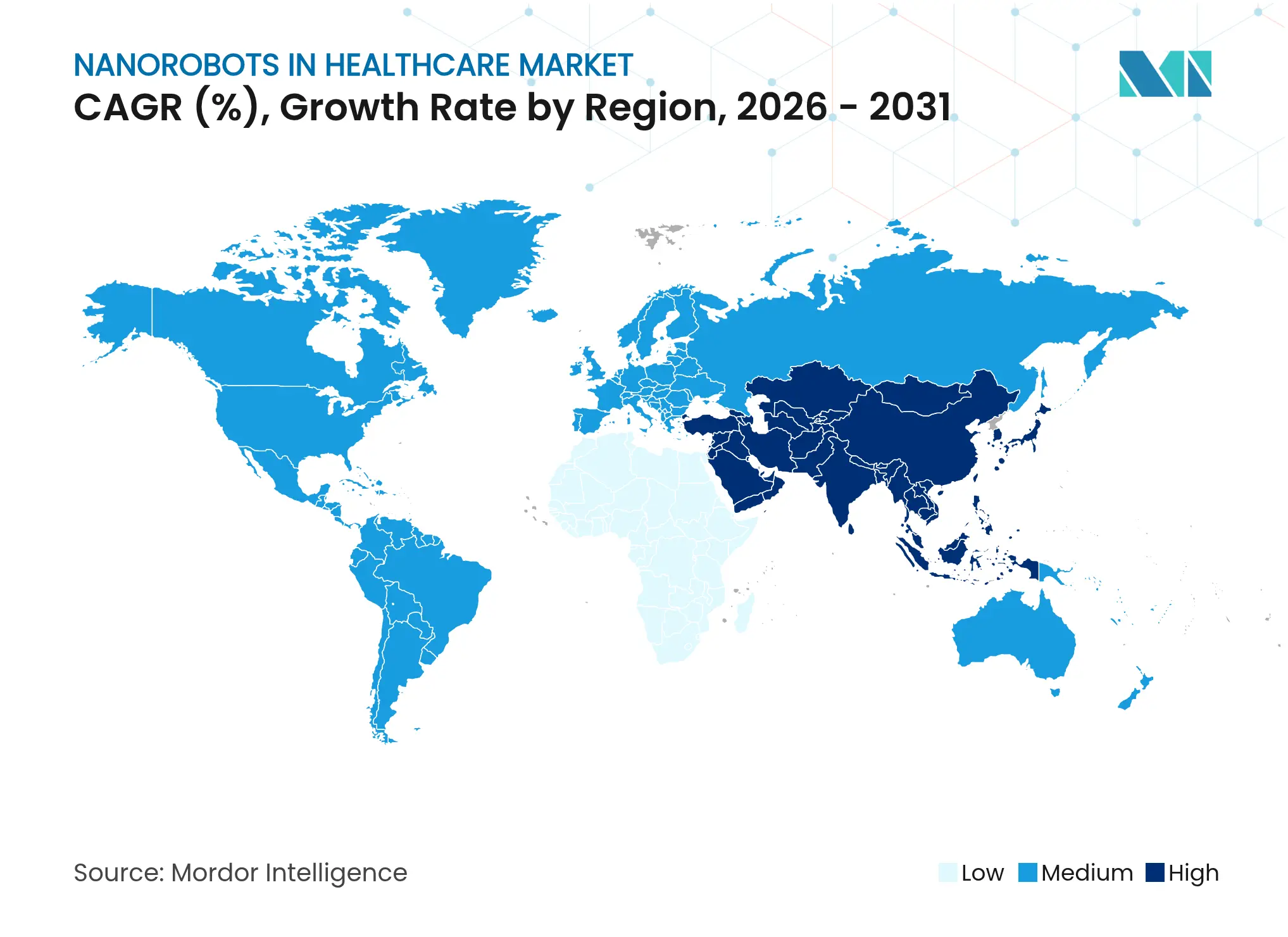

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

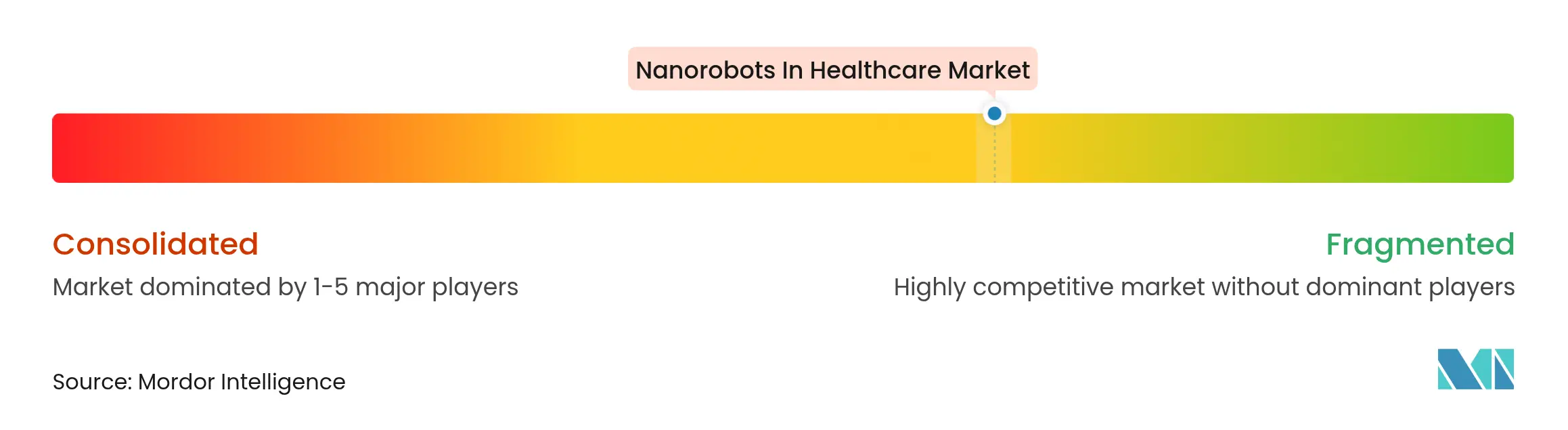

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Nanorobots In Healthcare Market Analysis by Mordor Intelligence

Nanorobots in healthcare market size in 2026 is estimated at USD 8.28 billion, growing from 2025 value of USD 7.25 billion with 2031 projections showing USD 16.09 billion, growing at 14.21% CAGR over 2026-2031. Uptake accelerates as precision medicine moves from theory to routine practice, prompting demand for nanoscale devices that can deliver or activate therapy at the single-cell level. Advances in magnetic propulsion coils, AI-assisted imaging, and biodegradable hydrogel bodies help manufacturers overcome earlier safety and navigation barriers. Chronic disease prevalence continues to climb, especially cancers and neurodegenerative disorders, making highly targeted drug delivery a clinical necessity. At the same time, defense-funded biothreat programs shorten regulatory timelines by underwriting early-stage trials and de-risking capital-intensive research.

Key Report Takeaways

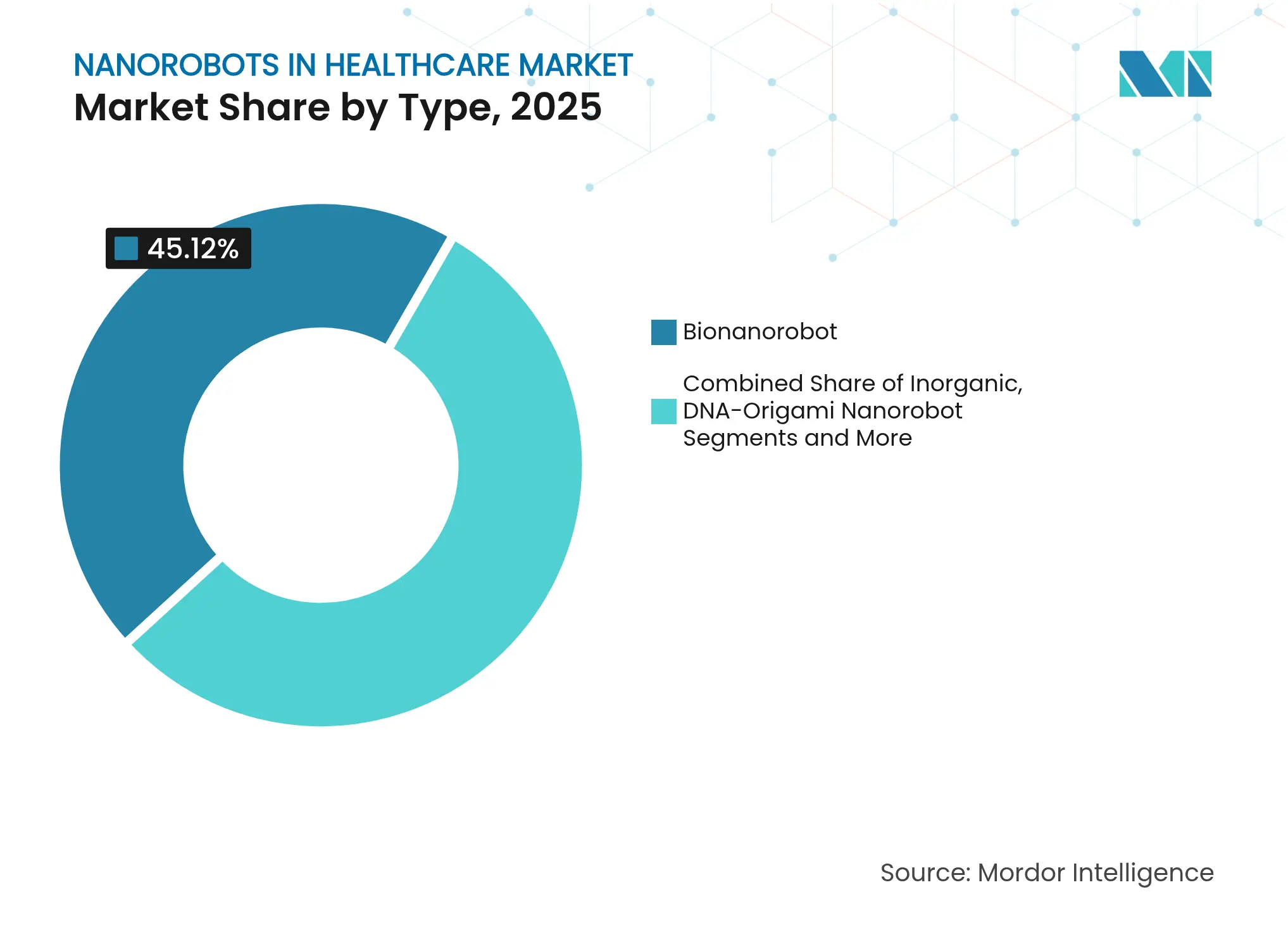

- By type, bionanorobots led with 45.12% share of the nanorobots in healthcare market in 2025; magnetically-guided nanorobots are projected to expand at an 18.12% CAGR through 2031.

- By application, drug delivery held 52.98% of the nanorobots in healthcare market size in 2025, while theranostics is on track for a 17.15% CAGR to 2031.

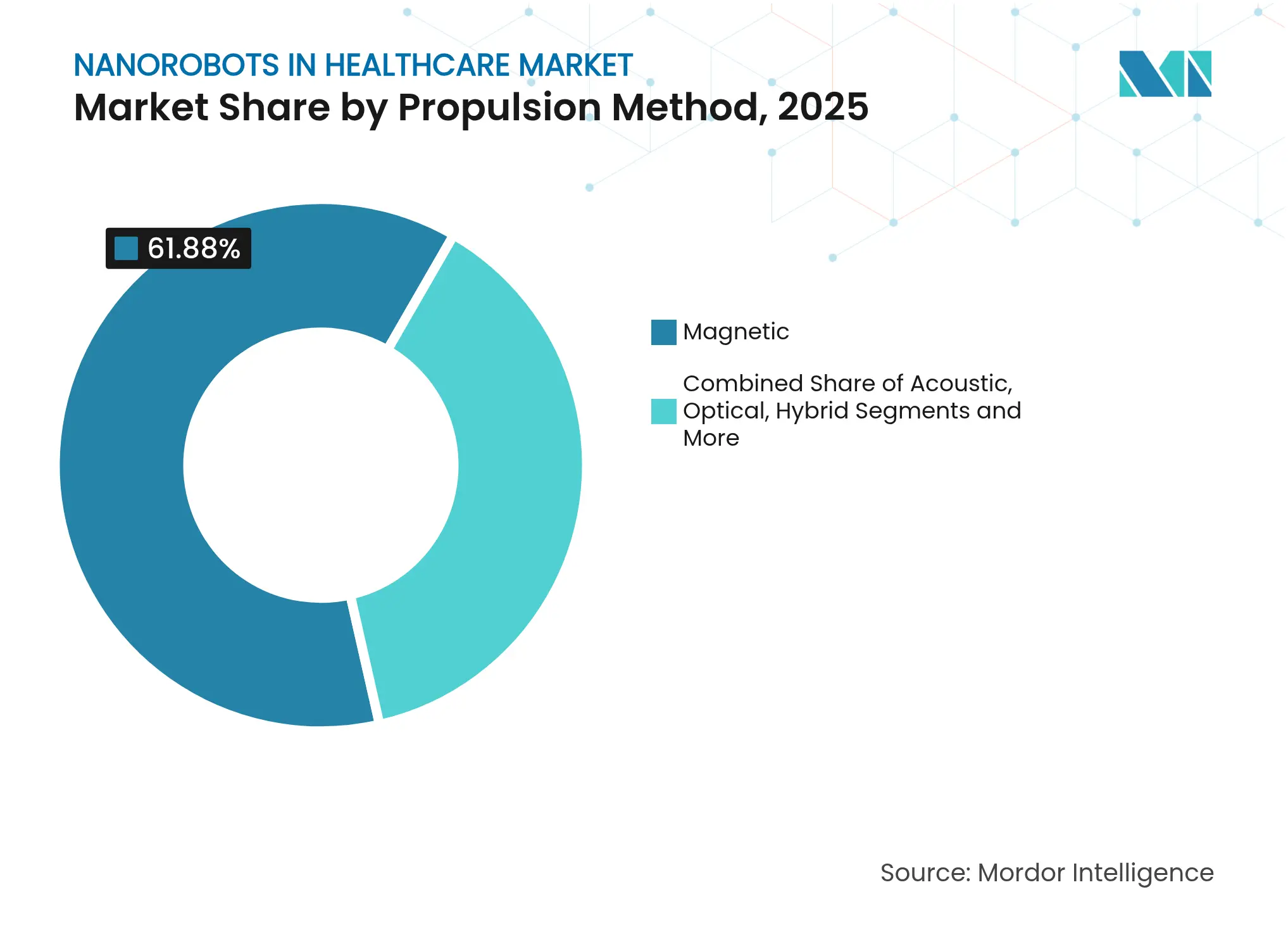

- By propulsion method, magnetic systems commanded 61.88% of the nanorobots in healthcare market share in 2025; hybrid propulsion is forecast to grow at a 17.71% CAGR.

- By end user, hospitals and ambulatory surgical centers accounted for 45.96% revenue in 2025, whereas pharmaceutical and biotechnology companies will post a 16.35% CAGR through 2031.

- By geography, North America captured 36.92% of the nanorobots in healthcare market in 2025; Asia Pacific is projected to climb at a 16.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nanorobots In Healthcare Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Advancement in precision medicine

Advancement in precision medicine

| +2.8% | Global, early gains in North America and EU | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:

+2.8%

|

Geographic Relevance

:

Global, early gains in North America

and EU

|

Impact Timeline

:

Medium term (2–4 years)

|

Growing R&D investments in

nanorobotics

Growing R&D investments in

nanorobotics

| +2.1% | APAC core, spill-over to North America | Long term (≥ 4 years) | |||

Rising chronic disease burden

Rising chronic disease burden

| +3.2% | Global | Short term (≤ 2 years) | |||

AI-enabled imaging and navigation

AI-enabled imaging and navigation

| +2.5% | North America and EU, expanding to APAC | Medium term (2–4 years) | |||

Biodegradable

magnetically-controlled hydrogels

Biodegradable

magnetically-controlled hydrogels

| +1.9% | Global, regulatory leadership in North America | Medium term (2–4 years) | |||

Defense-funded in-vivo biothreat

programs

Defense-funded in-vivo biothreat

programs

| +1.7% | North America, technology transfer to allied nations | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Advancement in Precision Medicine

Precision medicine’s shift toward cell-specific interventions places nanorobots at the center of personalized therapy. DNA-origami devices from Karolinska Institutet reduced tumor volumes by 70% in murine trials by activating only in acidic micro-environments, a proof that nanorobots can spare healthy tissue.[1]Karolinska Institutet, “Nanorobot With Hidden Weapon Kills Cancer Cells,” sciencedaily.com Falling genomic sequencing costs, richer biomarker libraries, and hospital investments in companion diagnostics further raise demand for programmable nanoscale carriers. Pharmaceutical firms now view autonomous nanorobots as essential adjuncts to biologics pipelines because conventional liposomes cannot meet the specificity required for gene therapies. National Institutes of Health grants also target nano-enabled vectors, ensuring steady public funding.

Growing R&D Investments in Nanorobotics

Venture capital and government grants converge on nanorobotics as a transformational platform. DARPA’s SHIELD program develops bloodstream “roomba-like” robots that neutralize pathogens before symptomatic infection, with anticipated civilian spin-offs. Polytechnique Montréal opened a dedicated NanoRobotics Laboratory that marries materials science with AI route-planning. Bionaut Labs raised USD 43.2 million to ready first-in-human trials, signaling investor confidence in clinical viability.

Rising Chronic Disease Burden

Global incidence of oncology and neuro-degenerative disorders climbs with aging populations. Self-propelled protein-bound magnetic nanobots cut bladder tumor size by 90% in preclinical studies, underscoring value where long-term systemic dosing is toxic. Hospitals look to nanorobot-enabled sustained release platforms to lower repeat admissions and adverse-event rates. Insurers support pilots that demonstrate reduced total treatment cost through localized therapy.

AI-Enabled Imaging and Navigation

Machine-learning algorithms now guide nanorobots through arterial branches in real time. University of Saskatchewan researchers built predictive flow models that improve route efficiency, unlocking longer mission windows in vivo. On-board sensors feed edge-computing units, allowing mid-course adjustment if biomarkers signal sub-optimal conditions. The convergence of 5G telemetry and cloud analytics gives surgeons dashboard-style oversight during procedures.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory challenges in clinical

applications

Regulatory challenges in clinical

applications

| -2.3% | Global, varying intensity by region | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:

-2.3%

|

Geographic Relevance

:

Global, varying intensity by region

|

Impact Timeline

:

Medium term (2–4 years)

|

High manufacturing cost and

scalability

High manufacturing cost and

scalability

| -1.8% | Global, acute in emerging markets | Long term (≥ 4 years) | |||

Public perception and bio-hacking

concerns

Public perception and bio-hacking

concerns

| -1.4% | North America and EU, spreading globally | Short term (≤ 2 years) | |||

Scarcity of rare-earth metals for

propulsion

Scarcity of rare-earth metals for

propulsion

| -1.1% | Global, supply chain concentration in China | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory Challenges in Clinical Applications

Current device frameworks struggle to classify autonomous, AI-enabled swarms. The US FDA issued nanotechnology guidance, yet firms must validate both hardware and learning algorithms, stretching approval cycles.[2]U.S. Food and Drug Administration, “Considering Whether an FDA-Regulated Product Involves Application of Nanotechnology,” fda.gov Multi-region trials duplicate effort because harmonized global standards do not exist, raising cost burdens on start-ups.

High Manufacturing Cost and Scalability

Atom-level assembly demands precision tooling and inline defect detection at molecular resolution. Continuous processing pilots highlight potential, but capital spending remains prohibitive for many developers.[3]VandenBerg Michael A. et al., “Continuous Manufacturing of Nanomaterials,” springeropen.com Hybrid designs further complicate production, as each propulsion module may require dissimilar material inputs.

Segment Analysis

By Type: Biocompatible Designs Capture Early Adoption

Bionanorobots secured 45.12% of the nanorobots in healthcare market in 2025 owing to their immune-friendly protein or lipid shells that blend seamlessly with human tissue. Magnetically-guided nanorobots remain the breakout sub-category, slated for an 18.12% CAGR through 2031 as external field generators achieve millimeter-scale precision. DNA-origami formats widen therapeutic index by folding strands into logic-gated cages that open only inside tumor micro-environments.

Clinical buyers now screen platforms for both efficacy and manufacturability. Biohybrid designs that merge cell membranes with synthetic cores illustrate compromise, delivering higher payloads without triggering macrophage response. Vendors scaling up biotemplated assembly plants position themselves for long-term contracts as payers demand cost parity with conventional biologics.

Note: Segment shares of all individual segments available upon report purchase

By Application: Drug Delivery Dominates, Theranostics Accelerates

Drug delivery owns 52.98% of the nanorobots in healthcare market size and remains hospitals’ first purchase line because localized dosing immediately lowers adverse-event rates. Yet theranostic suites, forecast to grow 17.15% annually, integrate diagnostic sensors and drug depots to close the feedback loop in oncology protocols. Multifunctional nanodisks from Korea diagnose tumor phenotype, trigger chemo release, and stimulate immune response in one trip.

Future revenue shifts toward adaptive devices that adjust dosing based on continuous biomarker feeds. Imaging-enabled swarms map vasculature in real time, helping surgeons plan micro-invasive procedures. Biosensing and environmental monitoring stay niche but offer upside in infection-control programs within intensive care units.

By Propulsion Method: Magnetic Systems Hold Ground, Hybrid Solutions Rise

Magnetic fields currently drive 61.88% of the nanorobots in healthcare market share by leveraging MRI-compatible coils already present in tertiary hospitals. Hybrid propulsion is the growth story at 17.71% CAGR because it layers acoustic or chemical actuators onto magnetic cores to negotiate tissue heterogeneity. Focused ultrasound platforms recently produced Newton-scale thrust, opening deep-organ use cases previously off-limits.

Design engineers now favor mode-switching firmware that toggles power sources to conserve battery and sidestep field shadowing behind bone structures. Supply-chain planners diversify rare-earth exposure with piezoelectric and enzymatic alternatives to mitigate long-term cost risk.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Lead, Pharma Firms Accelerate

Hospitals and ambulatory surgical centers account for 45.96% of 2025 revenue because capital budgets already cover advanced imaging suites required for nanorobot guidance. Pharmaceutical and biotechnology companies exhibit the highest growth at 16.35% CAGR as they embed nanoscale carriers into in-house drug discovery pipelines. Bionaut Labs’ partnership with Mayo Clinic illustrates cross-sector collaboration where device makers gain clinical insight and hospitals access frontier therapies.

Academic institutes remain pivotal, publishing early-stage breakthroughs that feed commercial licensing deals. Specialty clinics specialising in oncology or neurology start pilot programs to differentiate on outcomes in value-based care contracts.

Geography Analysis

North America leads with 36.92% share of the nanorobots in healthcare market in 2025. Federal agencies provide predictable funding streams and the FDA continues to refine review templates that cut time-to-market for bio-resorbable devices. University consortia link engineering schools with teaching hospitals, speeding translational research. Canada’s policy grants for precision medicine further widen laboratory capacity.

Asia Pacific posts the fastest 16.84% CAGR to 2031. China positions nanorobotics as a strategic sector, channeling large budgets into smart DNA carriers and in-vivo diagnostic swarms. Japan leverages precision manufacturing strengths to build micron-scale ultrasonic transducers, while South Korea’s semiconductor supply base provides on-chip AI controllers. Indian biotech clusters in Hyderabad and Bengaluru court venture funds, though regulatory frameworks still mature. The region also faces concentrated dysprosium supply, prompting government stockpile strategies.

Europe maintains balanced growth by pairing stringent safety rules with Horizon funding grants. DFKI in Germany spearheads molecular communication protocols that let nanorobots relay telemetry outside the body. Scandinavian hospitals run first-in-patient trials for bio-degradable magnetic hydrogel carriers. Smaller regions such as the Middle East sign bilateral MOUs to import FDA-cleared platforms, hoping to leapfrog into advanced oncology care.

Competitive Landscape

Market Concentration

Industry structure remains fragmented, with no single firm exceeding a high single-digit share. Academic spin-outs, med-tech start-ups, and big-pharma innovation units compete on propulsion algorithms, payload chemistry, and bio-compatibility coatings. Bionaut Labs stands out after securing USD 43.2 million to fund pivotal trials on brain-targeted micro-robots, signalling investor appetite for niche neuro-applications.

Large device manufacturers partner with AI software houses to embed predictive navigation that cuts mission times. Patent portfolios cluster around magnetic steering coils and DNA-origami release triggers. Firms able to scale continuous manufacturing at pharmaceutical-grade standards build long-term pricing power.

Strategic moves include joint ventures between chipmakers and catheter OEMs to embed edge processors in disposable launch capsules, and cross-licensing between hydrogel formulators and imaging specialists to integrate visibility markers. M&A activity is anticipated once early clinical successes de-risk platform-level prospects.

Nanorobots In Healthcare Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ImmunityBio, Inc. signed an MOU with Saudi partners to introduce the FDA-cleared Cancer BioShield nanorobot platform in the Middle East.

- April 2025: Satio and Nanowear partnered to merge at-home nanotechnology biomarkers with self-administered drug-delivery patches.

- November 2024: Theranautilus secured USD 1.2 million seed funding to commercialize healthcare nanorobotic solutions.

Table of Contents for Nanorobots In Healthcare Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Advancement in Precision Medicine

- 4.2.2Growing R&D Investments in Nanorobotics

- 4.2.3Increasing Prevalence of Chronic Diseases Requiring Targeted Drug Delivery

- 4.2.4Technological Convergence with AI-Enabled Imaging & Navigation

- 4.2.5Biodegradable Magnetically-Controlled Hydrogel Nanorobots Fast-Track Pathways

- 4.2.6Defense-Funded In-Vivo Biothreat Neutralization Programs

- 4.3Market Restraints

- 4.3.1Regulatory Challenges in Clinical Applications

- 4.3.2High Manufacturing Cost & Scalability Issues

- 4.3.3Public Perception & Bio-Hacking Concerns

- 4.3.4Scarcity of Rare-Earth Metals for Magnetic Propulsion

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Type

- 5.1.1Bionanorobot

- 5.1.2Inorganic Nanorobot

- 5.1.3DNA-Origami Nanorobot

- 5.1.4Magnetically-Guided Nanorobot

- 5.2By Application

- 5.2.1Drug Delivery

- 5.2.2Diagnosis & Imaging

- 5.2.3Surgery

- 5.2.4Theranostics

- 5.2.5Others

- 5.3By Propulsion Method

- 5.3.1Magnetic

- 5.3.2Chemical/Enzymatic

- 5.3.3Acoustic

- 5.3.4Optical

- 5.3.5Hybrid

- 5.4By End User

- 5.4.1Hospitals & ASCs

- 5.4.2Specialty Clinics

- 5.4.3Academic & Research Institutes

- 5.4.4Pharma & Biotech Companies

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Bionaut Labs

- 6.3.2DNA Nanobots LLC

- 6.3.3JEOL Ltd

- 6.3.4Nanobots Therapeutics

- 6.3.5NanoCube Health

- 6.3.6Nanovery Ltd

- 6.3.7Theranautilus

- 6.3.8Thermo Fisher Scientific Inc.

- 6.3.9Bruker Corporation

- 6.3.10BICO Group AB

- 6.3.11Brigham & Women’s Hospital (Wyss Institute)

- 6.3.12Max Planck Institute for Intelligent Systems

- 6.3.13Imina Technologies SA

- 6.3.14Vs Nanotech

- 6.3.15Cytosurge AG

- 6.3.16Park Systems Corp.

- 6.3.17KIMM (Korea Institute of Machinery & Materials)

- 6.3.18ETH Zürich Nanorobotics Lab

- 6.3.19Magnea Therapeutics

- 6.3.20NanoRobotics SAS

- 6.3.21SRI International

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Nanorobots In Healthcare Market Report Scope

As per the report's scope, nanorobots in healthcare, also known as nanorobotic systems or nanobots, are tiny robotic devices designed to operate at the nanoscale (typically ranging from 1 to 100 nanometers) for various medical applications, such as surgery and drug delivery.

The nanorobots in the healthcare market are segmented as type into bionanorobot and inorganic nanorobot. The market is segmented by application into drug delivery, diagnosis, surgery, and others. By geography the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.