Nano GPS Chipset Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 2.01 Billion |

| Growth Rate (2025 - 2030) | 12.38% CAGR |

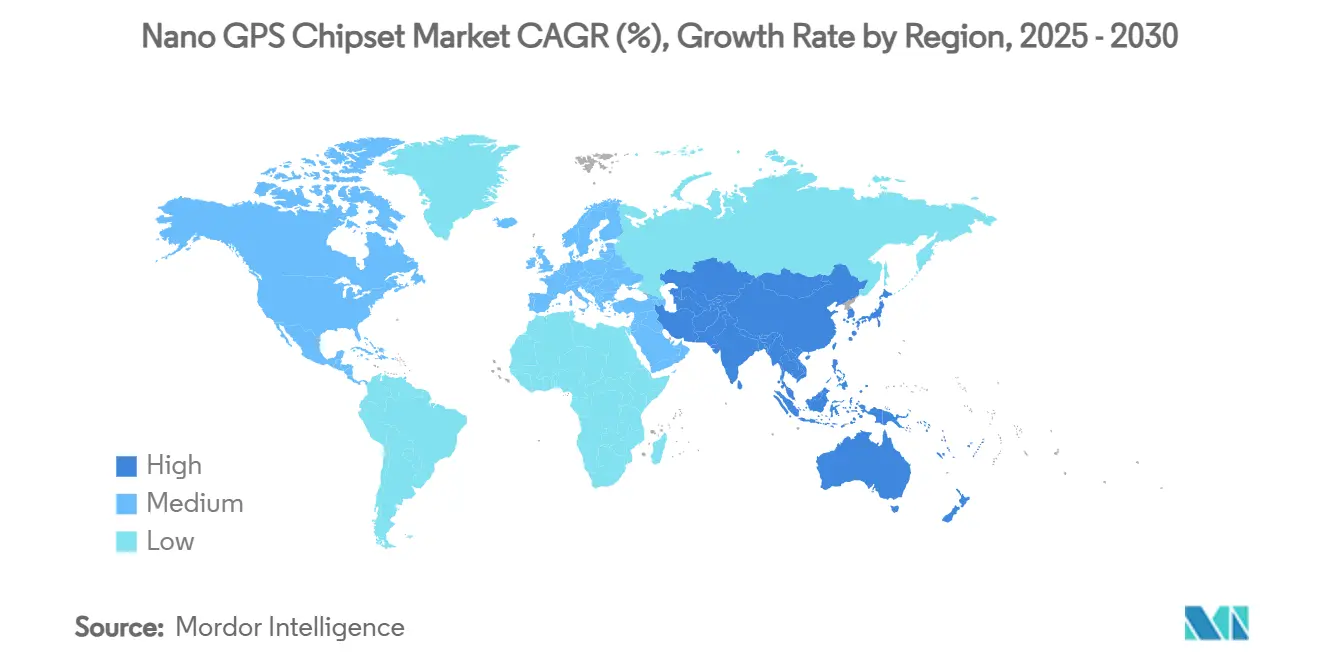

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

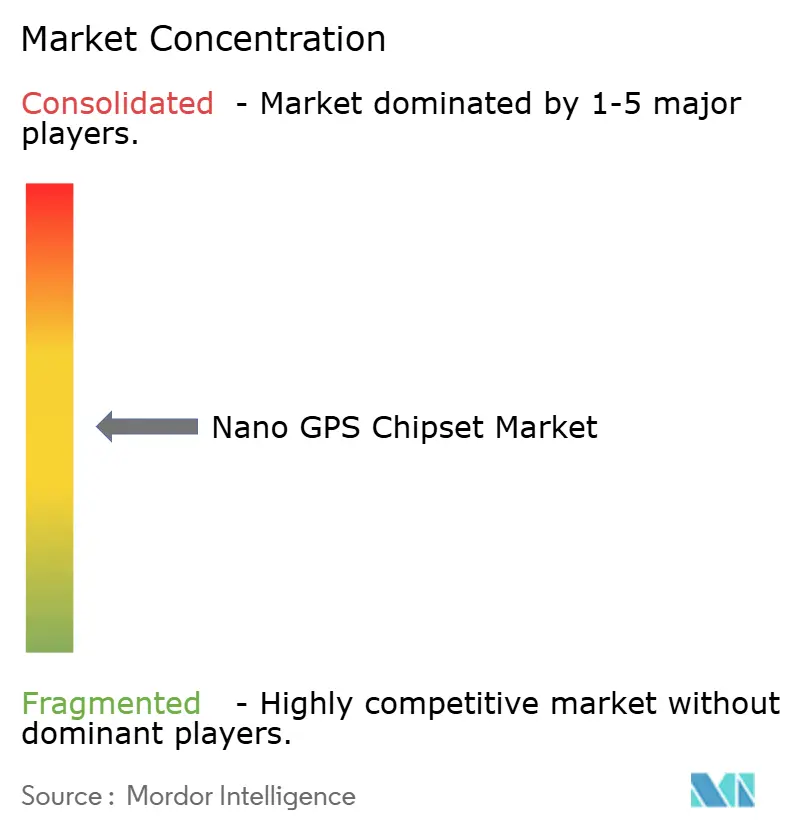

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nano GPS Chipset Market Analysis by Mordor Intelligence

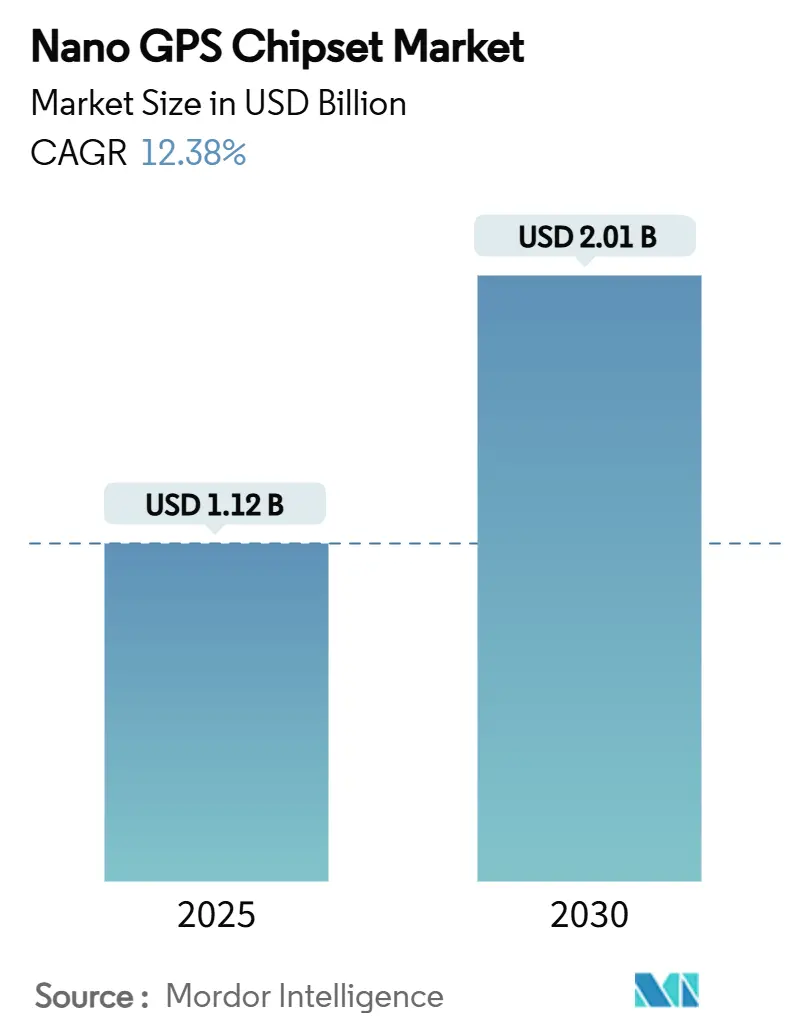

The Nano GPS chipset market size stood at USD 1.12 billion in 2025 and is forecast to reach USD 2.01 billion by 2030, advancing at a 12.38% CAGR. This growth reflects sustained demand for sub-10 mm² dies that can deliver reliable global navigation while consuming single-digit milliwatts, a combination that keeps the Nano GPS chipset market firmly embedded in next-generation IoT, wearables, and defense platforms. Momentum stems from three reinforcing trends: tighter process integration that lowers power budgets, dual-band (L1/L5) implementations that push accuracy toward centimeter levels, and defense-funded “assured PNT” programs that drive volumes in radiation-hardened variants. Leading vendors are co-optimizing RF front ends with digital signal processors to maximize yield below 22 nm even as yield losses remain a key cost driver. Meanwhile, regional policy—especially export controls on advanced mixed-signal nodes—reshapes global supply alliances and encourages on-shore manufacturing investments that favor early adopters of advanced packaging.

Key Report Takeaways

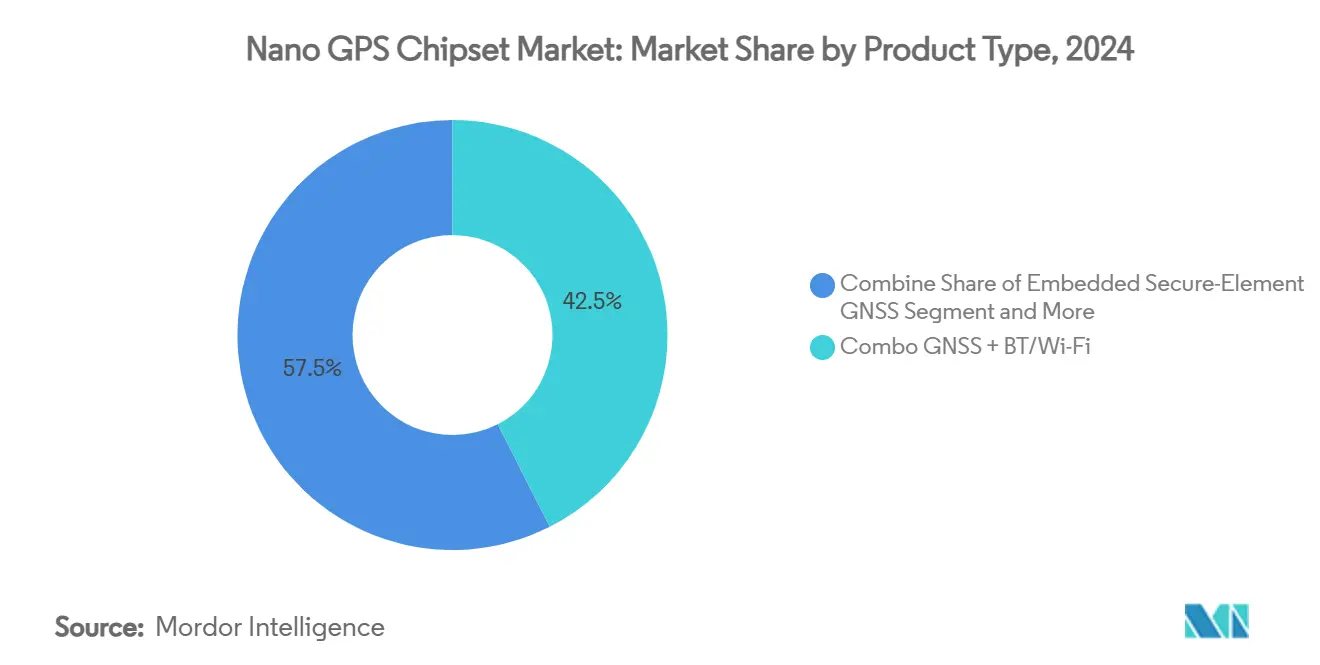

- By product type, combo GNSS + BT/Wi-Fi solutions led with 42.54% revenue share in 2024; embedded secure-element GNSS is projected to expand at a 15.02% CAGR through 2030.

- By integration level, the SoC/MCU-integrated segment held 51.34% of the Nano GPS chipset market share in 2024, while antenna-in-package solutions are growing fastest at 14.34% CAGR to 2030.

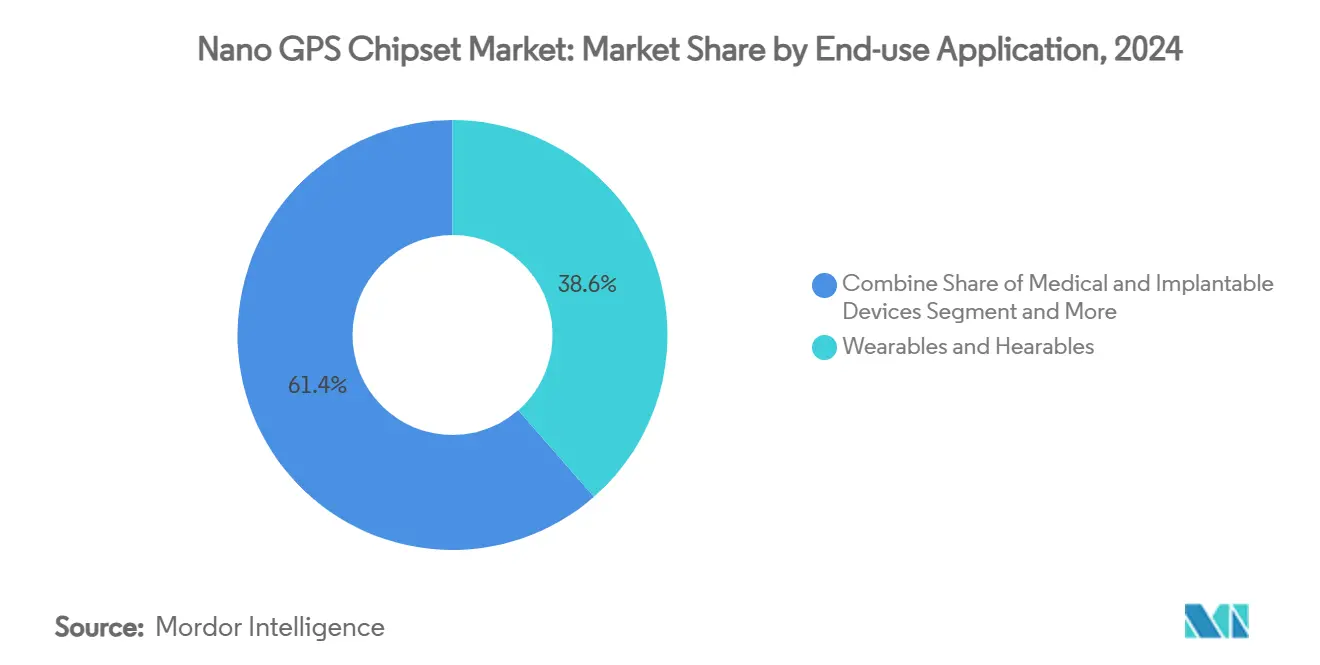

- By end-use application, wearables and hearables accounted for 38.56% of the Nano GPS chipset market size in 2024; medical and implantable devices are advancing at a 16.12% CAGR.

- By process node, 40-65 nm designs captured 47.22% share of the Nano GPS chipset market size in 2024, whereas ≤22 nm FinFET designs register the highest 14.87% CAGR.

- By geography, North America commanded 38.95% of the Nano GPS chipset market size in 2024; Asia-Pacific is forecast to post the quickest 15.98% CAGR to 2030.

Global Nano GPS Chipset Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Satellite-miniaturisation road-maps adopted by tier-1 foundries | +2.8% | Global, led by Taiwan and South Korea | Medium term (2-4 years) |

| Ultra-low-power IoT design wins in NB-IoT and LTE-M wearables | +2.1% | North America & EU expanding to APAC | Short term (≤ 2 years) |

| Multi-frequency L1/L5 adoption in sub-10 mm² dies | +1.9% | Global, strongest in automotive & agri | Medium term (2-4 years) |

| Defence-funded “PNT-on-chip” programs | +1.5% | North America & EU with ally transfer | Long term (≥ 4 years) |

| Open-source GNSS RF-front-end IP libraries | +0.9% | Global, early uptake in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Satellite-Miniaturisation Road-Maps Adopted by Tier-1 Foundries

Tier-1 foundries are rolling out advanced logic platforms that embed Super Power Rail topologies and NanoFLEX transistor architectures, delivering 8-10% performance uplift and up to 20% power savings—margins that directly benefit always-on GNSS dies suitable for medical implants and asset tags. The shift from planar MOSFET to FinFET and soon to gate-all-around FET structures helps maintain signal integrity despite shrinking geometries, yet mixed-signal yield losses beyond 22 nm still hover above 8%. Foundry road maps, therefore, dictate which vendors can reliably ship large volumes and, by extension, define short-term leadership in the Nano GPS chipset market. Advanced packaging, including 2.5-D interposers and system-in-package stacks, further squeezes RF, power-management, and secure-element blocks onto footprints under 25 mm². As a result, product designers find fresh headroom to embed precision GNSS in applications—such as subcutaneous cardiac monitors or centimetric agricultural seeding rigs—that previously lacked the space envelope.

Ultra-Low-Power IoT Design Wins in NB-IoT and LTE-M Wearables

Commercial modules that unite cellular NB-IoT, LTE-M, and GNSS now post power draws below 6 mW during dual-band fixes, a milestone illustrated by Broadcom’s BCM4778 receiver and u-blox’s CloudTrack-enabled SARA modules. Multi-protocol chipsets ensure a single RF path can handle both positioning and data backhaul, trimming the bill of materials while prolonging battery life in smart watches to days instead of hours. That efficiency flips the cost–benefit calculus for industrial trackers, allowing supply-chain operators to deploy millions of disposable tags that remain geolocated through entire shipping cycles. In turn, the Nano GPS chipset market expands into low-ARPU niches—parcel tracking and perishables logistics among them—where high-power GNSS had been uncompetitive. Growing carrier support for Release 17 NTN features opens satellite fallback paths, pushing even rural agriculture and wildlife monitoring solutions to adopt nano-scale GNSS as standard silicon.

Multi-Frequency L1/L5 Adoption in Sub-10 mm² Dies

Dual-band architectures now fit within dies smaller than 10 mm², eliminating the historical trade-off between accuracy and form factor. L5 brings an extra 10 dB signal-in-noise advantage over legacy L1, improving lane-level navigation in dense urban settings and reducing convergence times for precise point positioning services.[1]Taoglas, “Dual-Band GNSS ‘Patch-in-a-Patch’ Antenna,” taoglas.com Chip-scale antennas stay a bottleneck: sub-1 cm² asset tags suffer limited gain, prompting vendors to invest in metamaterial and antenna-in-package solutions that reclaim radiating area. Despite physics constraints, advanced beam-forming algorithms and tighter front-end-back-end code coupling help maintain sensitivity without enlarging the footprint. These advances allow precision agriculture tools to meet the 2 cm row-spacing requirements that maximize corn yield, while consumer smartphones deliver turn-by-turn guidance accurate enough for shared-bicycle docking.

Defence-Funded “PNT-on-Chip” Programs (US DoD, EU GALILEO)

Public-sector R&D budgets create an upstream technology pipeline that commercial vendors quickly adapt for mass‐market SKUs. Quantum-inertial sensors funded under the US Defense Innovation Unit’s Transition of Quantum Sensing program give rise to radiation-hardened timing blocks that later migrate into automotive GNSS designs. [2] Defense Innovation Unit, “Transition of Quantum Sensing Field Testing,” diu.milThe Air Force Research Laboratory’s NTS-3 satellite will validate spoof-resistant authentication signals, a feature expected to surface in consumer drones by 2027. European Union co-funding of assured PNT IP cores further accelerates dual-band adoption in OEM telematics. These military demands indirectly inflate the total addressable Nano GPS chipset market because core IP investments are amortized across defense and civilian volumes, allowing vendors to price new parts aggressively.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield loss >8% below 22 nm for mixed-signal GNSS RF | -1.8% | Global, focused on advanced foundry hubs | Short term (≤ 2 years) |

| ITAR-like export restrictions on dual-use nanonavigation ICs | -1.2% | US–China corridors with allied spillovers | Medium term (2-4 years) |

| Limited antenna gain in sub-1 cm² asset tags | -0.8% | Global, affecting IoT and wearables | Short term (≤ 2 years) |

| Lithium price volatility impacting coin-cell BOM | -0.6% | Global battery supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Yield Loss > 8% Below 22 nm for Mixed-Signal GNSS RF

Advanced nodes amplify parasitic capacitance and corner variability, challenging the tight phase-noise budgets that GNSS RF chains demand. Excess reticle leakage forces reruns that push wafer costs upward, squeezing margins in high-volume trackers priced under USD 2 per chipset. [3]MDPI, “CMOS Scaling for the 5 nm Node and Beyond,” mdpi.com Vendors balance this by bin-sorting parts into premium automotive or cost-sensitive asset-tracking bins, but any excursion can derail shipment forecasts. Consequently, some OEMs lock designs at 28 nm—even at the cost of 25 % higher power draw—to avoid unpredictable lead-times, slowing full-node migration across the Nano GPS chipset market.

ITAR-Like Export Restrictions on Dual-Use Nano-Navigation ICs

Revisions to the U.S. Commerce Control List now cover gate-all-around FET structures and advanced PNT ASICs, requiring special licenses for shipment into Group D:5 destinations. [4]Federal Register, “Commerce Control List Additions and Revisions,” federalregister.gov Vendors servicing Asian OEMs must spin separate versions that omit high-precision timing or anti-spoof features, diverting engineering resources and inflating R&D overhead. Regional trust barriers also prompt automotive Tier-1s to favor in-region silicon, fracturing what was once a global design-win environment and dampening the universal scale advantages that drive down average selling prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combo Solutions Drive Integration Convergence

Combo GNSS + BT/Wi-Fi solutions captured 42.54% of the Nano GPS chipset market size in 2024, highlighting the appeal of single-package connectivity that curbs board space and certification costs. The configuration allows smart-watch OEMs to drop discrete radios, accelerating time-to-market while lifting yield because foundries can validate full RF paths in a controlled environment.

Embedded secure-element GNSS parts, though smaller in today’s revenue mix, register a brisk 15.02% CAGR as automotive cybersecurity regulations and defense export rules tighten. The segment embeds tamper-proof key storage that supports EU eCall, US 5GAA standards, and anti-spoof message authentication. With new UNECE rules mandating over-the-air update security, Tier-1 suppliers weave secure GNSS into infotainment and ADAS domain controllers, pushing combo solutions toward the mainstream of the Nano GPS chipset market.

Second-generation combo devices adopt dual-band GNSS and tri-radio support (Wi-Fi 6, BLE 5.4, and 802.15.4) within footprints under 150 mm². This densification slashes system power by integrating a single power-management IC and shared clock tree, benefitting ultra-compact industrial sensors. As more edge AI workloads run locally, vendors prioritize baseline RTOS support to streamline algorithm updates without sacrificing battery life, placing combo silicon firmly at the heart of rapid IoT prototyping.

By Integration Level: SoC Architectures Dominate Miniaturization

SoC/MCU-integrated designs absorbed 51.34% of 2024 revenue, marking them as the center of gravity for the Nano GPS chipset market. Marrying dual Arm Cortex-M7 cores to phase-change memory removes the need for external flash, shaving both footprint and BOM while offering deterministic execution for safety-critical tasks.

Antenna-in-package (AiP) innovations propel the fastest 14.34% CAGR, feeding demand in medical implants and animal trackers where a discrete patch antenna is infeasible. AiP integrates the radiating element atop the RF front end, minimizing feed-line losses and simplifying enclosure design.

While discrete chips endure in survey-grade receivers requiring octa-band and centimeter accuracy, the forward trajectory clearly favors single-die integration. Over the forecast window, vendors intend to migrate AiP concepts to millimeter-wave altimeter bands, positioning SoC road maps as the main gatekeeper for function consolidation across the Nano GPS chipset market.

By End-Use Application: Medical Devices Emerge as Growth Driver

Wearables and hearables retained a 38.56% share of the Nano GPS chipset market size in 2024, as fitness trackers remain a default accessory for urban consumers. Compact dual-band GNSS ensures sub-meter step-count accuracy while maintaining five-day battery autonomy, a non-negotiable buying criterion for mass-market smart watches.

Medical and implantable devices head the growth leaderboard at a 16.12% CAGR. Next-gen pacemakers leverage sub-5 mW GNSS to establish location-triggered diagnostic uploads, letting clinicians audit arrhythmia events against environmental stressors. Biocompatible Parylene-coated antennas and titanium can-mounted feedthroughs solve tissue attenuation hurdles, marking a breakthrough that ushers the Nano GPS chipset market into regulated healthcare domains.

Pet trackers, livestock collars, and precision-agri sensors extend the TAM by piggybacking on shared module platforms. Asset and logistics trackers benefit from new Release 17 satellite-NTN features, ensuring coverage in maritime shipping lanes where cellular footprints vanish. Collectively, these verticals stretch the application palette that sustains 12-plus-percent CAGR even as consumer wearables approach saturation in developed economies.

By Process Node: Advanced Nodes Drive Performance Evolution

Mid-range 40-65 nm nodes dominated with 47.22% of Nano GPS chipset market share in 2024, offering an optimal price–power compromise for volume trackers. Yet ≤22 nm FinFET designs post the highest 14.87% CAGR, enabled by yield-improving backside-power delivery and AI-assisted design rule checkers.

FinFET’s superior electrostatic control yields 25% dynamic power cuts, letting dual-band fixes occur at or below 6 mW. Automotive OEMs eye those savings to support redundancy in level-3 autonomous stacks, which must run GNSS alongside lidar and HD-map updates. Meanwhile, 28 nm remains a safe harbor for cost-sensitive labels, underscoring that node migration in the Nano GPS chipset market will remain bifurcated until gate-all-around nodes hit scale around 2028.

Geography Analysis

North America entered 2025 with the largest Nano GPS chipset market size among all regions, benefiting from a robust ecosystem of defense primes, precision-agri integrators, and early 5G coverage that seamlessly augments GNSS. Government grants for complementary PNT technologies, totaling USD 7.2 million, further strengthen resilience features that trickle down into commercial designs.

Asia-Pacific exhibits the steepest growth curve, moving from manufacturing hub to design nexus as China’s BeiDou Phase IV satellites enhance regional accuracy to 1.5 meters and India’s NavIC upgrade adds L1 civilian signals. Governments pair constellation expansion with local semiconductor subsidies, propelling the Nano GPS chipset market into a self-sustaining virtuous cycle of supply and demand.

Europe leverages the fully-operational Galileo constellation and a strong automotive base to secure high-value design wins in ADAS and insurance telematics. Tightening cybersecurity directives elevate secure-element GNSS adoption. Yet higher energy prices compel some fabs to outsource sub-16 nm production to Asia, nudging strategic autonomy debates. The Middle East and Africa tap precision-agri to offset water scarcity, while Latin America pilots land-reform mapping projects—both lean on low-cost APAC silicon, extending the market’s global spread.

Competitive Landscape

The Nano GPS chipset market remains moderately fragmented, with the top five vendors controlling an estimated 52% of 2024 revenue. Market leaders such as u-blox, Broadcom, MediaTek, and Qualcomm compete on power efficiency, multi-band capability, and integrated security. u-blox couples hardware with cloud intelligence, offering one-stop positioning services that lower total cost of ownership for fleet managers. Broadcom tailors 4 mW dual-band designs for premium wearables, while MediaTek exploits its 3 nm mobile platform to integrate GNSS into automotive cockpits, promising seamless handovers between sub-6 GHz 5G and satellite signals.

Emerging Asian fabless entrants target cost-driven SMB customers with open-source RF front-ends and RISC-V cores, accelerating commoditization in entry-level asset trackers. Strategic collaborations proliferate: Qualcomm pairs Trimble’s centimeter-level ProPoint Go engine with its Snapdragon Auto modem to court Level-2+ autonomy programs, and STMicroelectronics aligns with Qualcomm to plug AI-enhanced wireless connectivity into its MCU ecosystem.

Supply-chain resilience is an escalating differentiator. Parrot’s CHUCK 3.0 autopilot, built on non-Chinese components, illustrates how OEMs mitigate geopolitical risks by sourcing GNSS silicon from ITAR-compliant suppliers. Meanwhile, quantum sensing start-ups backed by defense funds, such as Vector Atomic, threaten to upend the status quo with chip-scale atomic instruments that could displace traditional GNSS in critical infrastructure. Incumbents hedge by acquiring beam-forming IP houses and entering multi-source agreements with foundries across continents to ensure uninterrupted wafer access.

Nano GPS Chipset Industry Leaders

u-blox Holding AG

Broadcom Inc.

MediaTek Inc.

Qualcomm Technologies Inc.

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Parrot rolled out CHUCK 3.0, an AI autopilot featuring optical navigation and multi-band spoof-proof radios for UAVs.

- May 2025: MediaTek unveiled the Dimensity Auto C-X1 cockpit platform built on 3 nm, plus the MT2739 modem supporting 5G-Advanced for vehicles.

- March 2025: The Defense Innovation Unit started field testing quantum-sensor prototypes across inertial and magnetic domains to strengthen GPS-denied navigation.

- February 2025: STMicroelectronics released the Teseo VI GNSS family with dual Arm Cortex-M7 cores and quad-band support for automotive ADAS.

Global Nano GPS Chipset Market Report Scope

| Stand-alone Nano-GNSS IC |

| Combo GNSS + BT/Wi-Fi |

| System-in-Package (SiP) |

| Embedded Secure-Element GNSS |

| Discrete Chip |

| SoC / MCU-Integrated |

| Antenna-in-Package |

| Wearables and Hearables |

| Asset / Logistics Trackers |

| Pet and Livestock Monitoring |

| Medical and Implantable Devices |

| Mini-UAV / Drone Avionics |

| Precision-Agri Sensors |

| 90 nm + |

| 40 - 65 nm |

| 28 - 32 nm |

| ?22 nm FinFET |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Stand-alone Nano-GNSS IC | ||

| Combo GNSS + BT/Wi-Fi | |||

| System-in-Package (SiP) | |||

| Embedded Secure-Element GNSS | |||

| By Integration Level | Discrete Chip | ||

| SoC / MCU-Integrated | |||

| Antenna-in-Package | |||

| By End-use Application | Wearables and Hearables | ||

| Asset / Logistics Trackers | |||

| Pet and Livestock Monitoring | |||

| Medical and Implantable Devices | |||

| Mini-UAV / Drone Avionics | |||

| Precision-Agri Sensors | |||

| By Process Node | 90 nm + | ||

| 40 - 65 nm | |||

| 28 - 32 nm | |||

| ?22 nm FinFET | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large was the Nano GPS chipset space in 2025?

It reached USD 1.12 billion, reflecting strong uptake in IoT, wearables and defense devices.

What compound annual growth rate is expected through 2030?

The market is projected to grow at a 12.38% CAGR, taking revenues to USD 2.01 billion.

Which region is forecast to post the fastest expansion by 2030?

Asia-Pacific, driven by BeiDou and NavIC rollouts plus manufacturing incentives, is set to grow at 15.98% CAGR.

Why are combo GNSS + BT/Wi-Fi chipsets gaining share?

They pack multiple radios into one package, cutting board space, lowering power budgets and simplifying certification, which boosted their 2024 share to 42.54%.

Which process node currently leads Nano GPS production?

The 40-65 nm node holds the largest 47.22% share, balancing performance and cost, while ≤22 nm FinFET nodes record the highest growth.

How do ITAR-like export rules affect suppliers?

New controls on advanced PNT ASICs require licenses for certain destinations, prompting vendors to create feature-reduced variants and increasing R&D overhead.

Page last updated on: