Nano-Magnetic Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

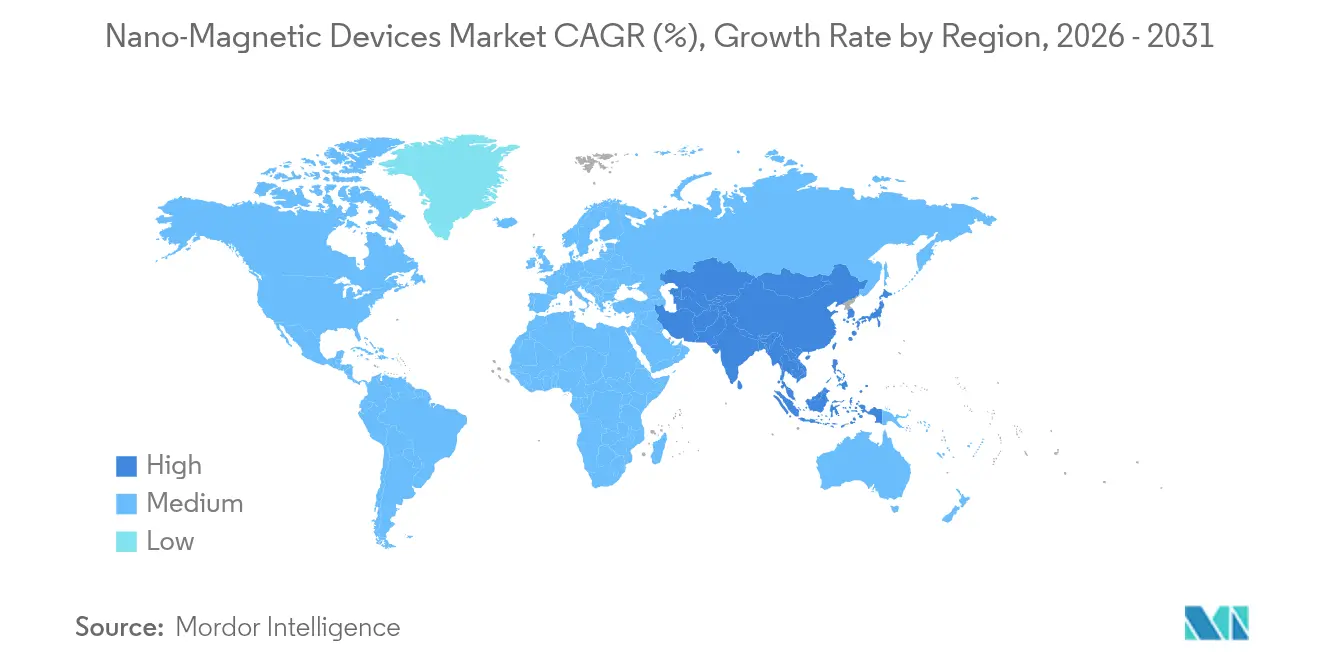

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

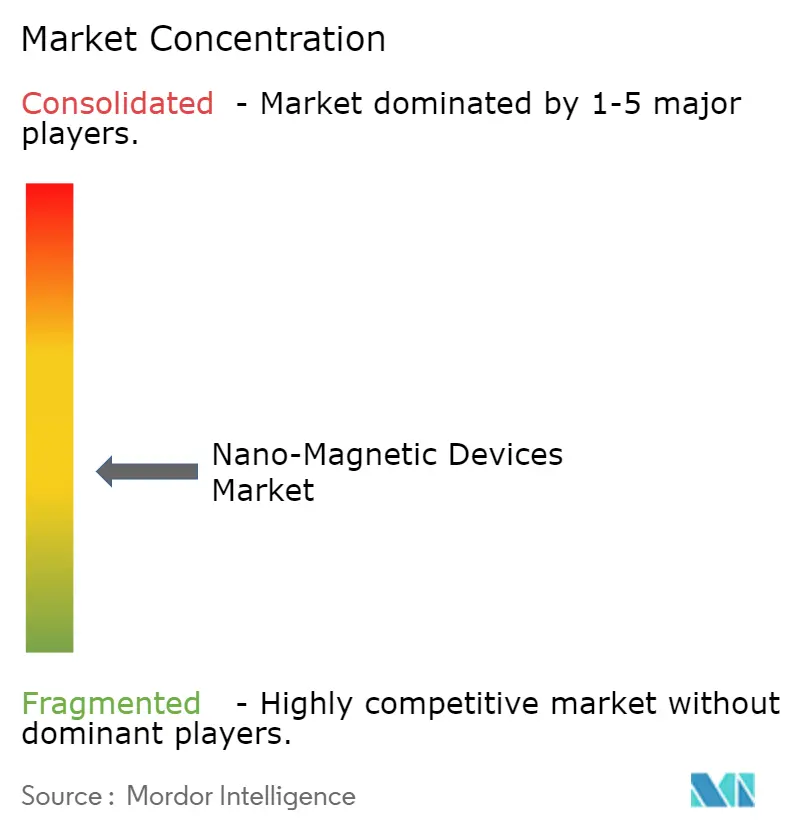

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nano-Magnetic Devices Market Analysis by Mordor Intelligence

The nano-magnetic devices market size is expected to grow from USD 1.12 billion in 2025 to USD 1.17 billion in 2026 and is forecast to reach USD 1.43 billion by 2031 at 4.20% CAGR over 2026-2031. Demand escalates as spin-based architectures displace charge-based electronics, offering lower power consumption and faster switching.[1]U.S. Department of Energy, “Draft_EES2_Roadmap_AMMTO,” energy.gov Government incentives from the CHIPS and Science Act and the EU Chips Act accelerate research, while 300 mm fab upgrades lift manufacturing yields for GMR and TMR sensors. Automotive qualification of MRAM for over-the-air updates, deep-space demand for radiation-hardened memory, and Asia-Pacific fab expansion reinforce long-term growth. Nevertheless, export controls on cobalt and gallium, sub-10 nm patterning losses, and areal density limits for next-gen HDDs temper near-term momentum.

Key Report Takeaways

- By type, sensors led with 41.05% revenue share in 2025; data storage devices are projected to expand at a 6.01% CAGR to 2031.

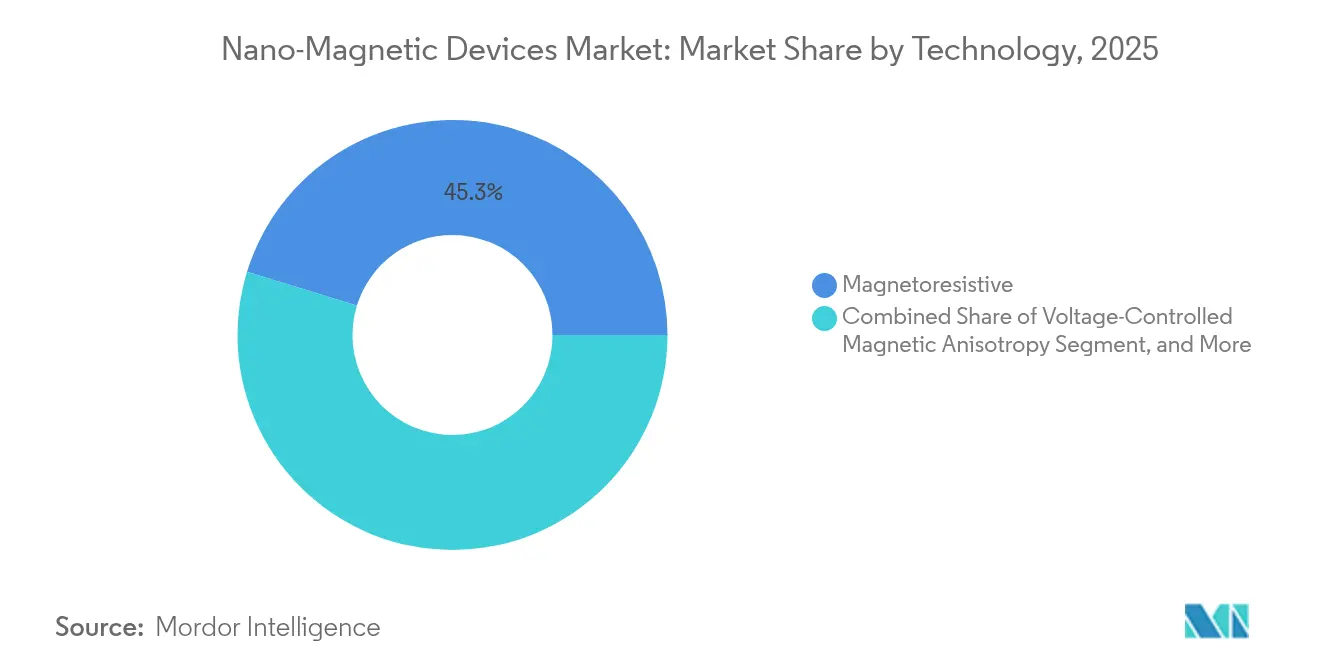

- By technology, magnetoresistive devices held 45.25% of the nano-magnetic devices market share in 2025, while spin-transfer torque technology is advancing at a 5.23% CAGR through 2031.

- By end-use vertical, consumer electronics accounted for 37.44% of the nano-magnetic devices market size in 2025 and automotive & transportation is set to rise at a 5.32% CAGR through 2031.

- By geography, North America commanded 31.25% of the nano-magnetic devices market in 2025, whereas Asia-Pacific is the fastest-growing region with a 4.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nano-Magnetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive qualification of MRAM for OTA updates | +0.8% | North America & EU | Medium term (2-4 years) |

| 300 mm fab upgrades for GMR/TMR sensors | +0.6% | Asia-Pacific, global supply | Short term (≤2 years) |

| Radiation-hard spintronic memory for deep-space missions | +0.4% | North America & EU | Long term (≥4 years) |

| Shift to NdFeB nano-composite magnets in Chinese wind turbines | +0.5% | Asia-Pacific, global | Medium term (2-4 years) |

| CHIPS & EU Chips Act funding for spintronics | +0.7% | Global | Long term (≥4 years) |

| 3-D LiDAR-magnetic fusion sensors for AMRs | +0.3% | Asia-Pacific, global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Automotive Qualification of MRAM for OTA Firmware Updates

Automotive OEMs now certify MRAM that endures unlimited write cycles, eliminating the wear-out concerns of flash memory in software-defined vehicles. TSMC’s embedded MRAM enables microcontrollers that manage frequent over-the-air patches without data corruption.[2]Taiwan Semiconductor Manufacturing Company, “Embedded Non-Volatile Memory for Automotive Applications,” tsmc.com TDK reinforced momentum by unveiling the TAS8240 redundant TMR angle sensor that complies with ASIL D safety norms while operating up to 150 °C. Electric-vehicle production is projected to rise 27%, intensifying demand for magnetic sensing in battery and drivetrain modules.[3]TDK Corporation, “Magnetic sensors: TDK presents new redundant analog TMR angle sensor,” tdk.com Together, robust memory endurance and high-precision sensing cement the nano-magnetic devices market as a core enabler for future automotive electronics.

300 mm Fab Upgrades for GMR/TMR Sensor IC Production

East-Asian foundries have validated 99.6% yield for spin-orbit-torque MTJs on 300 mm wafers, with switching currents of 680 µA at 2 ns and TMR ratios above 119%. These yields drive down unit costs and let manufacturers integrate multi-axis sensors on a single die. Tohoku University guidelines on single-nanometer MTJs secure data retention beyond 10 years at 150 °C while retaining sub-10 ns speed. EUV lithography now reaches 5 nm resolution, guiding further miniaturization. Cost-competitive high-density sensors broaden adoption in consumer electronics and industrial automation, accelerating the nano-magnetic devices market.

Radiation-Hard Spintronic Memory Demand for Deep-Space Missions

Everspin secured USD 9.25 million to supply MRAM macros for radiation-hardened aerospace systems, spotlighting magnetic memory’s resilience under heavy ion exposure.[4]Everspin Technologies, “Contract to Provide MRAM Technology for Radiation Hardened eMRAM,” investor.everspin.com NASA data show MRAM maintains functionality after high-dose gamma and neutron irradiation, a feat unachievable with flash or DRAM. Honeywell’s space-qualified MRAM products target 15-20 year lifespans without wear-out, critical for missions beyond Mars. These capabilities expand the nano-magnetic devices market into deep-space platforms where conventional silicon memories falter.

Shift to NdFeB Nano-Composite Magnets in Chinese Wind Turbines

Chinese turbine makers reduce rare-earth dependency by introducing NdFeB nano-composite magnets that cut particle diameter from 730 nm to 76 nm, raising magnetic energy. Wet ball-milling aided by ethanol enhances uniformity, enabling lighter generators with higher output. Upgraded magnets support rapidly expanding offshore wind installations and create technology spill-overs for global OEMs. The resulting volume demand underpins regional supremacy in the nano-magnetic devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical mineral export controls on cobalt & gallium | -1.2% | Global, acute in North America & EU | Short term (≤2 years) |

| Sub-10 nm patterning yield losses | -0.8% | Global advanced manufacturing hubs | Medium term (2-4 years) |

| Areal density ceiling <3 Tb/in² for HDDs | -0.4% | Global data storage players | Long term (≥4 years) |

| Lack of IEC/JEDEC TMR-sensor standards | -0.6% | Global regulators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Critical Mineral Export Controls on Cobalt and Gallium

China supplies 98% of global gallium, so potential export bans could shave USD 3.4 billion from U.S. GDP and lift gallium prices more than 150%. Gallium arsenide and gallium nitride devices often co-package with magnetic sensors in RF modules, so shortages reverberate through the nano-magnetic devices market. The Pentagon’s radar modernization that relies on GaN further heightens strategic exposure. Recycling initiatives and AI-guided magnet design aim to mitigate risk, but near-term volatility persists.

Sub-10 nm Patterning Yield Losses in Nano-Magnet Fabrication

Creating high-anisotropy islands below 10 nm incurs stochastic EUV resist failures and line edge roughness that slash wafer yields. IMEC’s High-NA EUV lab will pilot 0.55 NA tools by 2026, yet mass production viability is unproven. Until process windows widen, manufacturers cap investments, restraining the nano-magnetic devices market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Data Storage Drives Innovation Despite Sensor Dominance

Sensors dominated 41.05% of the nano-magnetic devices market in 2025, anchored in automotive, industrial, and mobile products. Data storage devices, however, clock a 6.01% CAGR, propelling the nano-magnetic devices market size for storage from USD 0.24 billion in 2026 to USD 0.33 billion by 2031. MRAM’s non-volatility and radiation tolerance underpin adoption in space probes and electric vehicles. Imaging devices gain traction thanks to ultra-sensitive xMR components that capture biomagnetic signals, creating new revenue pools.

MRAM’s unlimited endurance outperforms flash, removing OTA bottlenecks in passenger vehicles. Breakthrough 3-D magnetic recording promises 10 Tbit/in² capacities, sustaining HDD relevance. Emerging spin-logic integrates memory and compute, foreshadowing in-memory processing paradigms.

By Sensors: TMR Technology Challenges Hall-Effect Dominance

Hall-effect sensors held 41.08% of sensor revenue in 2025 due to low cost and mature supply chains. TMR sensors expand at 5.61% CAGR, narrowing the price gap as 300 mm fabs ramp volume. The TAS8240 redundant angle sensor meets ISO 26262 ASIL D, signaling automotive readiness.

GMR occupies mid-tier niches, balancing sensitivity with affordability. Magnetostrictive sensors excel in aerospace hydraulic controls where EMI immunity is vital. TMR-based digital compasses slash azimuth errors from 4.18° to 0.46° after calibration, improving drone navigation. A new 3-axis silicon Hall sensor with offset cancellation lifts sensitivity to 198 V A⁻¹ T⁻¹, showing the Hall family can still innovate.

By Technology: Spin-Transfer Torque Emerges as Next-Generation Platform

Magnetoresistive approaches commanded 45.25% of the nano-magnetic devices market share in 2025, yet spin-transfer torque devices advance at a 5.23% CAGR through 2031. STT-MRAM achieves 680 µA switching currents at 2 ns while retaining data for 10 years at 150 °C.

Voltage-controlled anisotropy research seeks even lower power writes, and spin-orbit torque promises sub-nanosecond flips with high endurance. Cryogenic growth of ultrathin CoFe on MgO paves the way for single-nanometer MTJs. IEEE’s Beyond-CMOS roadmap lists STT- and SOT-MRAM as key options for memory hierarchy redesign

By End-Use Vertical: Automotive Applications Accelerate Beyond Consumer Electronics

Consumer electronics kept 37.44% revenue share in 2025, powered by smartphones and wearables embedding miniaturized magnetometers. Automotive and transportation grow 5.32% annually, lifting the nano-magnetic devices market size for mobility from USD 0.2 billion in 2026 to USD 0.26 billion by 2031 as OTA architectures mature.

Electric-vehicle growth of 27% stimulates TMR demand in battery management and motor control. Medical devices adopt trademarked Nivio xMR sensors that perform magnetocardiography outside shielded rooms, broadening preventive cardiology reach. Aerospace and defense platforms rely on radiation-hard MRAM for mission-critical data logging. Wind energy integrates nano-composite magnets for lighter generators.

Geography Analysis

North America captured 31.25% of the nano-magnetic devices market in 2025, propelled by defense and space programs requiring radiation-tolerant MRAM. Robust university-industry collaborations harness CHIPS Act funding to prototype neuromorphic spintronic chips. The region’s aerospace supply chain values memory endurance over cost, supporting premium pricing.

Asia-Pacific is projected to post a 4.83% CAGR, benefitting from 300 mm fab ramps in Japan, Korea, and China. China’s shift to NdFeB nano-composite magnets strengthens domestic turbine makers and sparks global trickle-down effects. Deployment of 3-D LiDAR-magnetic fusion sensors in Japanese and Korean AMRs underpins smart-factory expansion.

Europe allocates EUR 15.8 billion for Chips Joint Undertaking projects, carving a niche in skyrmionic neuromorphic computing. Germany’s automotive ecosystem demands ASIL D-compliant TMR sensors, while French and Belgian institutes spearhead High-NA EUV lithography. Emerging regions in South America and the Middle East embrace nano-magnetic devices for grid stability and industrial automation, leveraging technology transfer from multinational OEMs.

Competitive Landscape

The nano-magnetic devices market shows moderate concentration, with integrated device manufacturers and specialized spintronics firms sharing value pools. TDK offers a full magnetic sensor line-up and commands design-win leverage across automotive, industrial, and medical sectors. Everspin cooperates with Frontgrade to meet U.S. defense radiation standards, blending fab capacity with secure packaging investor.

Infineon reorganized in January 2025, forming the SURF unit to co-optimize sensor and RF research for a USD 20 billion opportunity by 2027. IBM advances racetrack memory, forecasting 100-fold capacity gains with ten-million-fold speed improvements, supported by public-private grants. Materials Nexus used AI to design rare-earth-free magnets in three months, indicating computational materials discovery could shorten the innovation cycle.

Automotive Tier-1 suppliers demand ASIL D compliance, pressuring vendors to validate long-term reliability. Consumer electronics favor cost and size, sparking intense price competition among Hall-effect providers. Aerospace clients pay premiums for rad-hard certification, isolating that niche from commodity pressures. Such segmentation shapes strategic alliances, technology roadmaps, and capital allocation across the nano-magnetic devices market.

Nano-Magnetic Devices Industry Leaders

-

IBM Corporation

-

Fujitsu Limited

-

Nanomagnetics Instruments

-

Hitachi Metals America Limited

-

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TDK unveiled the Spin Photo Detector using MTJ technology for ultra-fast optical sensing

- February 2025: TDK released the trademarked Nivio xMR sensor capable of biomagnetic field detection for cardiac imaging.

- February 2025: The Chips Joint Undertaking launched EUR 1.67 billion pilot-line calls aimed at sub-2 nm and heterogeneous integration.

- January 2025: Infineon Technologies established the SURF business unit to strengthen sensor and RF portfolios, aiming at a USD 20 billion market by 2027

Global Nano-Magnetic Devices Market Report Scope

The nano-magnetic devices offer a reduced size of electronics, increase its efficiency, and also help to increase product longevity. The nano-magnetic devices market tracks down the adoption of different types of devices like data storage devices, imaging devices, etc. The market study also focuses on the penetration of these devices in various end-use verticals like IT & telecom, energy & utilities, healthcare, etc.

| Sensors | Magnetic Field Sensors |

| Hall-Effect Sensors | |

| GMR Sensors | |

| TMR Sensors | |

| Magnetostrictive Sensors | |

| Data Storage Devices | MRAM |

| Spintronic HDD Read Heads | |

| Tape Storage Heads | |

| Imaging Devices | Magnetic Particle Imaging Systems |

| Nano-MRI Coils | |

| Actuators and Logic Devices | Spintronic Logic/Transistors |

| Micromotors and Actuators | |

| Other Nano-Magnetic Components | Antenna and RF Devices |

| Magnetoresistive |

| Spin-Transfer Torque (STT) |

| Voltage-Controlled Magnetic Anisotropy (VCMA) |

| Superparamagnetic Nanoparticles |

| Consumer Electronics |

| IT and Telecom (Data Centers) |

| Automotive and Transportation |

| Aerospace and Defense |

| Healthcare and Medical Devices |

| Energy and Utilities (Wind, Power Converters) |

| Industrial Automation and Robotics |

| Others (Research and Education) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Sensors | Magnetic Field Sensors | |

| Hall-Effect Sensors | |||

| GMR Sensors | |||

| TMR Sensors | |||

| Magnetostrictive Sensors | |||

| Data Storage Devices | MRAM | ||

| Spintronic HDD Read Heads | |||

| Tape Storage Heads | |||

| Imaging Devices | Magnetic Particle Imaging Systems | ||

| Nano-MRI Coils | |||

| Actuators and Logic Devices | Spintronic Logic/Transistors | ||

| Micromotors and Actuators | |||

| Other Nano-Magnetic Components | Antenna and RF Devices | ||

| By Technology | Magnetoresistive | ||

| Spin-Transfer Torque (STT) | |||

| Voltage-Controlled Magnetic Anisotropy (VCMA) | |||

| Superparamagnetic Nanoparticles | |||

| By End-use Vertical | Consumer Electronics | ||

| IT and Telecom (Data Centers) | |||

| Automotive and Transportation | |||

| Aerospace and Defense | |||

| Healthcare and Medical Devices | |||

| Energy and Utilities (Wind, Power Converters) | |||

| Industrial Automation and Robotics | |||

| Others (Research and Education) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the nano-magnetic devices market?

The nano-magnetic devices market stood at USD 1.17 billion in 2026 and is projected to reach USD 1.43 billion by 2031.

Which segment is growing fastest within the nano-magnetic devices market?

Data storage devices, driven by MRAM adoption, are expected to expand at a 6.01% CAGR through 2031.

Why are TMR sensors gaining traction over Hall-effect sensors?

TMR sensors deliver higher magnetoresistance and better signal-to-noise ratios, enabling compliance with stringent automotive safety standards.

How do export controls on gallium impact the nano-magnetic devices industry?

Potential gallium restrictions could inflate prices by more than 150%, affecting RF modules that integrate magnetic sensors and thus dampening short-term market growth.

Which region will grow the fastest in nano-magnetic devices adoption?

Asia-Pacific is forecast to post a 4.83% CAGR through 2031 owing to large-scale 300 mm fab expansions and wind-energy magnet upgrades.

How does MRAM benefit deep-space missions compared with flash memory?

MRAM offers radiation tolerance and unlimited endurance, ensuring reliable data retention over decades-long deep-space missions

Page last updated on: