Mid and High-Level Precision GPS Receiver Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

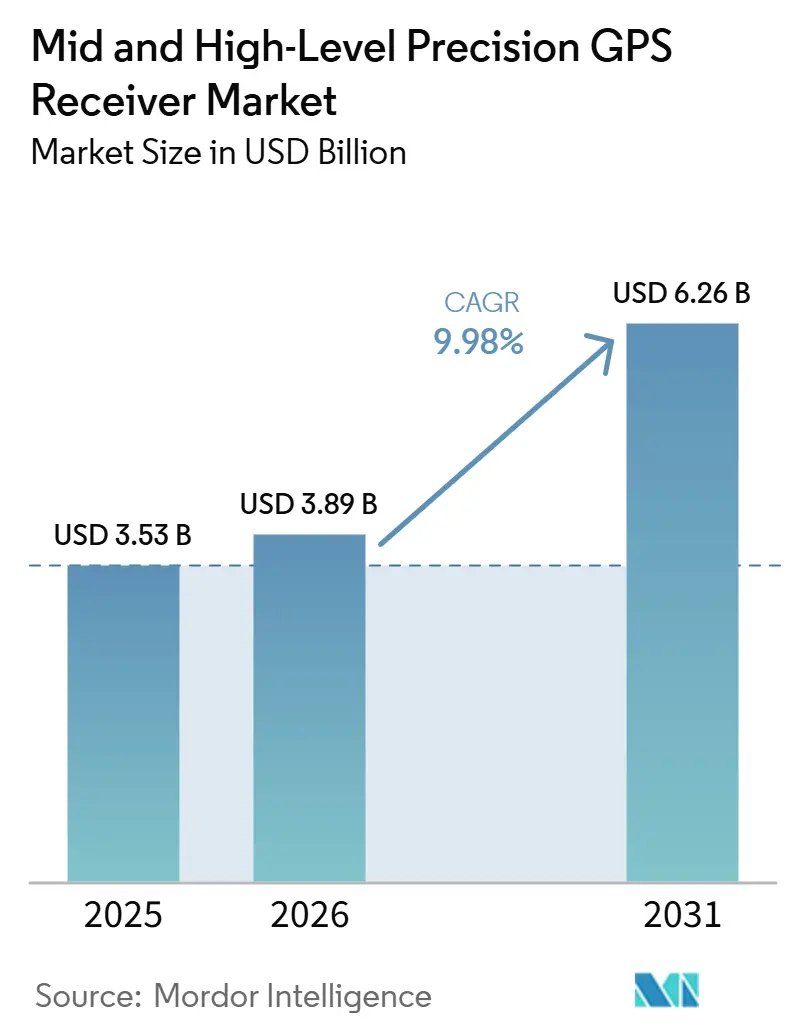

| Market Size (2026) | USD 3.89 Billion |

| Market Size (2030) | USD 6.26 Billion |

| Growth Rate (2026 - 2031) | 9.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mid and High-Level Precision GPS Receiver Market Analysis by Mordor Intelligence

The Mid and High-Level Precision GPS Receiver market size is projected to expand from USD 3.53 billion in 2025 and USD 3.89 billion in 2026 to USD 6.26 billion by 2031, registering a CAGR of 9.98% between 2026 and 2031. An accelerating shift toward hybrid PPP-RTK correction services, the integration of multi-frequency chipsets into heavy machinery, and the growing need for centimeter-level asset data in digital twin programs are reinforcing demand. Correction signals delivered by low Earth orbit satellites shorten convergence times below 60 seconds, enabling continuous operation in offshore or remote zones. Multi-band receivers that track emerging Galileo E6 and BeiDou B2b codes now safeguard safety-critical applications such as autonomous vehicle testing and precision mining. Meanwhile, construction and agriculture customers favor integrated smart antennas that blend GNSS, inertial, and cellular functions, cutting engineering overhead and speeding deployment.

Key Report Takeaways

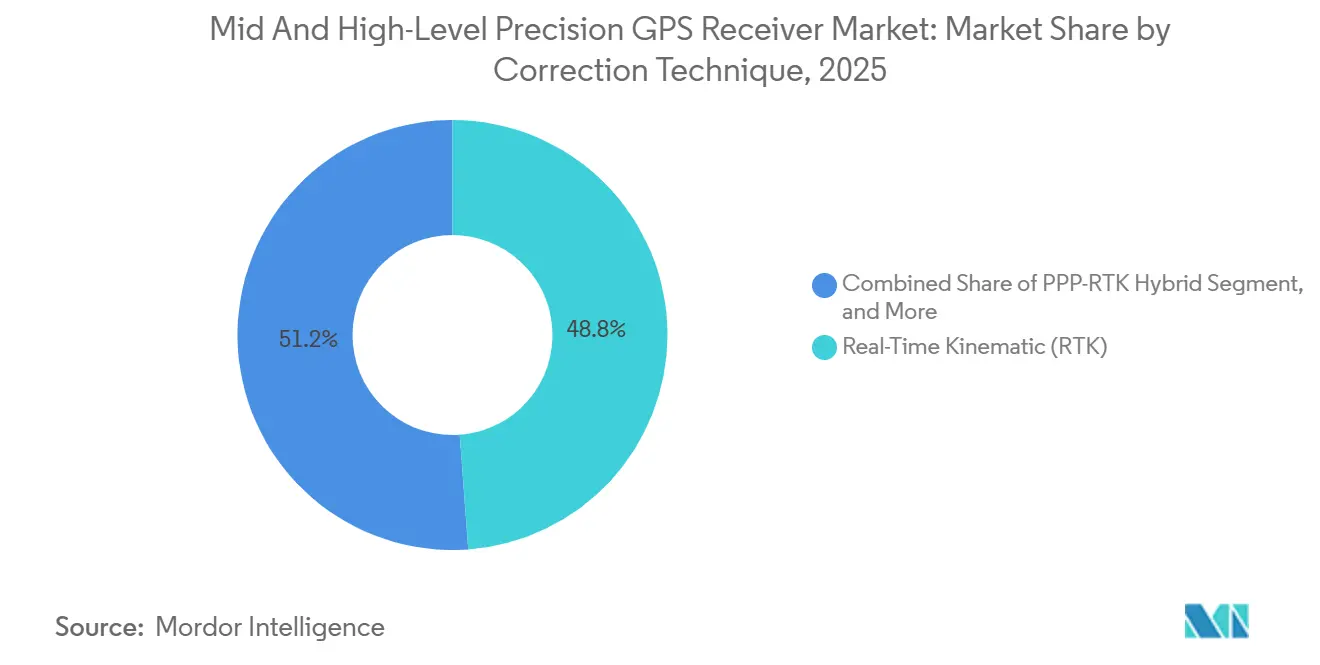

- By correction technique, Real-time kinematic solutions led with 48.84% of the Mid and High-Level Precision GPS Receiver market share in 2025, while PPP-RTK hybrids post the fastest projected expansion at a 10.67% CAGR through 2031.

- By frequency capability, Dual-frequency L1/L2 products held 46.39% share of the Mid and High-Level Precision GPS Receiver market size in 2025, yet multi-frequency boards are forecast to advance 11.06% annually to 2031.

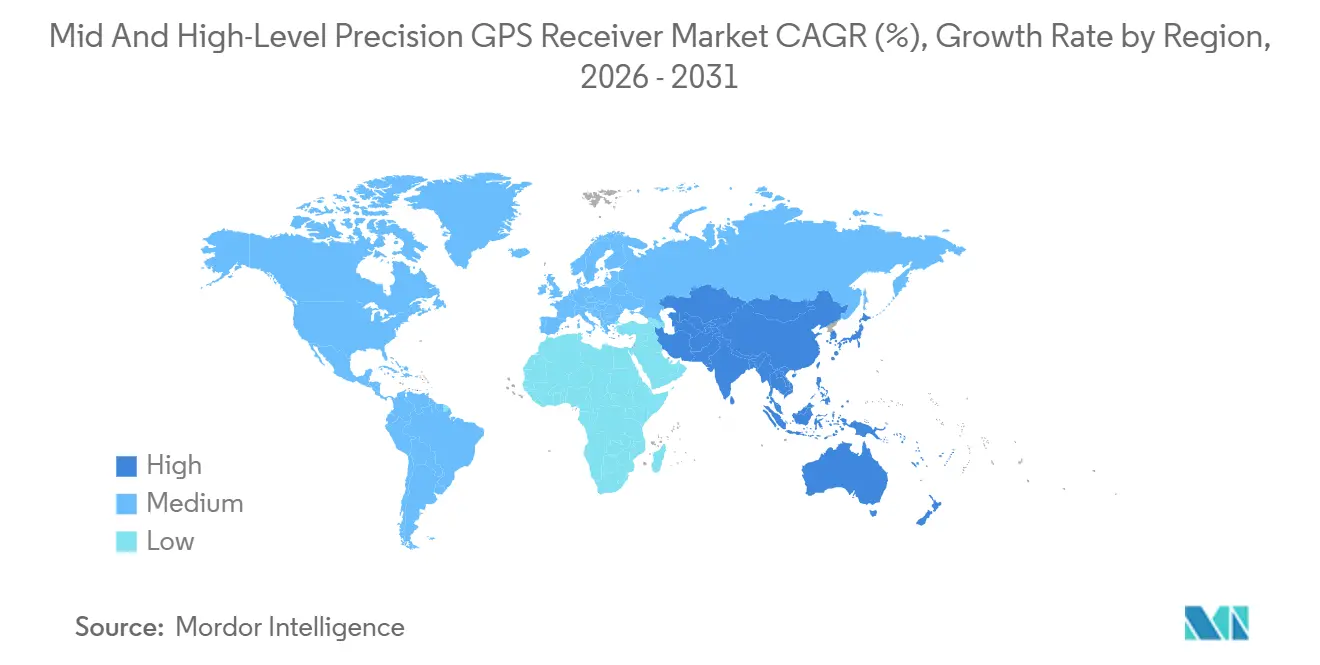

- By geography, Asia-Pacific contributed 42.42% of the Mid and High-Level Precision GPS Receiver market in 2025 and is expected to grow at 10.83% through 2031, outpacing every other region.

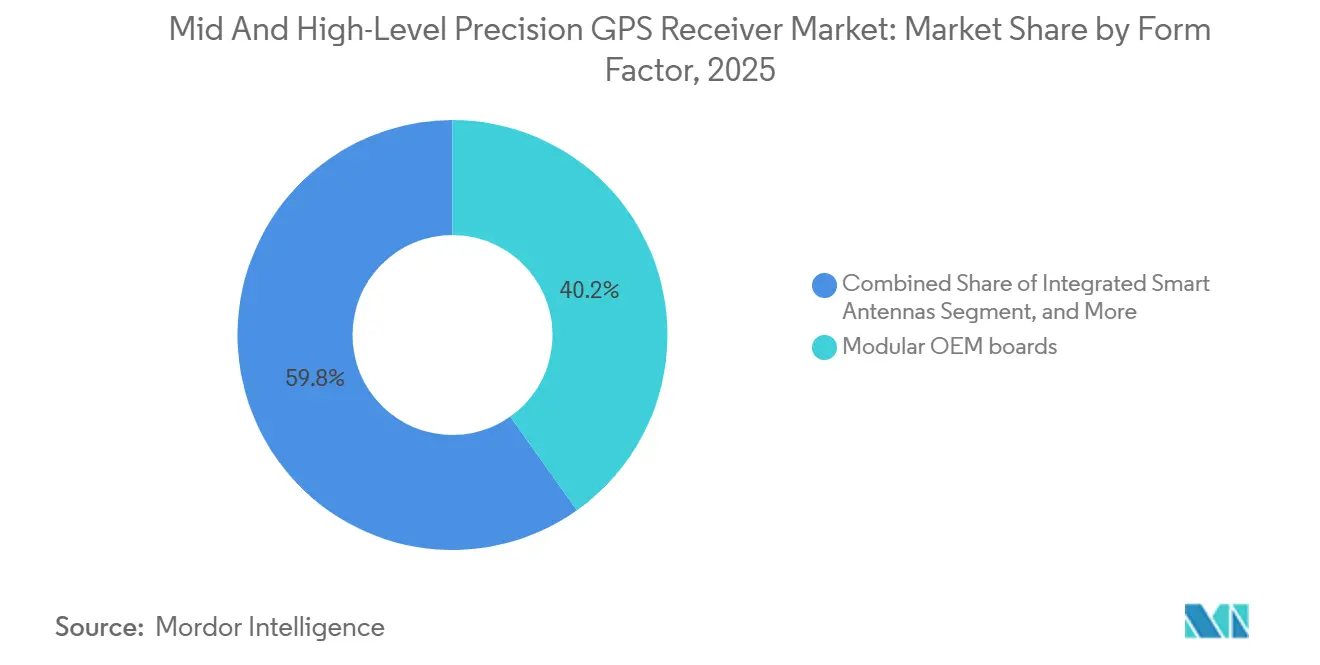

- By form factor, Modular OEM boards captured 40.18% of the Mid and High-Level Precision GPS Receiver market in 2025, whereas smart antennas are rising at a 10.98% CAGR on the back of plug-and-play demand.

- By end-use industry, Surveying and mapping accounted for 32.29% of the Mid and High-Level Precision GPS Receiver market in 2025, but autonomous ground and aerial vehicles represent the fastest-growing customer group with a 10.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mid and High-Level Precision GPS Receiver Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Precision Agriculture Automation | +2.80% | North America, Brazil, Argentina, Europe, Australia | Medium term (2–4 years) |

| Uptake of Construction and Mining Machine Control Systems | +2.40% | North America, Europe, Asia-Pacific, Middle East | Medium term (2–4 years) |

| Rising Demand for Autonomous Vehicle Validation and Testing | +1.90% | North America, Europe, China, Japan, South Korea | Long term (≥ 4 years) |

| Roll-out of Low Earth Orbit PPP-RTK Correction Services | +1.50% | Global | Short term (≤ 2 years) |

| Proliferation of Digital Twin Infrastructure Programs | +1.00% | Europe, Singapore, North America | Long term (≥ 4 years) |

| Integration of GNSS with 5G NTN for Centimeter-Level Indoor Positioning | +0.70% | Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Precision Agriculture Automation

Large growers are embedding real-time kinematic receivers into variable-rate planters and boom-mounted cameras that identify individual weeds, reducing herbicide use by up to 80%.[1]Deere and Company, “See and Spray Ultimate Reduces Herbicide Use,” deere.com Brazilian soybean operations now maintain 15-centimeter row spacing that enables mechanical cultivation and lowers chemical outlays. Argentinian grain producers synchronize autonomous carts with combines to extend harvest windows by two to three hours. Convergence below 100 milliseconds supports tractors traveling faster than 12 kilometers per hour. Collectively, these improvements increase yield consistency and shorten payback cycles, keeping the Mid and High-Level Precision GPS Receiver market on a steep adoption curve.

Uptake of Construction and Mining Machine Control Systems

Autonomous haul trucks in Australian and Chilean mines maintain 10-centimeter accuracy at 60 kilometers per hour through multi-frequency receivers paired with inertial units. Dozers equipped with intelligent machine control cut material waste by 30% and reduce fuel consumption. Highway contractors in the United States automate paving depths within 2 centimeters, trimming project schedules 10% to 15%. Building information modeling mandates across Europe and Singapore compel contractors to verify as-built data against digital files, driving receiver upgrades. Falling antenna prices and wider RTK coverage extend these systems to mid-tier contractors, widening the Mid and High-Level Precision GPS Receiver market footprint.

Rising Demand for Autonomous Vehicle Validation and Testing

Lane-level ground truth is indispensable for sensor fusion benchmarking. Waymo fleets in Phoenix and San Francisco log centimeter-accurate reference trajectories that validate lidar and camera outputs.[2]Waymo LLC, “Waymo Driver Evaluation Data,” waymo.com Aurora Innovation pairs multi-band GNSS with inertial navigation to maintain continuity in tunnels, fulfilling SAE Level 4 requirements. Trimble partnered with Qualcomm to preload RTX corrections into Snapdragon Auto modems, paving the way for production vehicles after 2028.[3]Trimble Inc., “Trimble and Qualcomm Collaborate on High-Precision Positioning,” trimble.com Ten-hertz position updates with latency under 50 milliseconds exceed consumer module capabilities, accelerating a shift toward high-precision boards. These programs fuel future demand across the Mid and High-Level Precision GPS Receiver market.

Roll-out of Low Earth Orbit PPP-RTK Correction Services

Xona Space Systems is launching PULSAR satellites that achieve precise point positioning convergence in under 60 seconds.[4]Xona Space Systems, “PULSAR Satellites Deliver Sub-Minute Convergence,” xonaspace.com Trimble invested USD 10 million to integrate PULSAR signals into its RTX service, extending coverage to offshore and polar regions. Topcon and Swift Navigation also plan to deliver LEO corrections, promising sub-5-centimeter accuracy with minimal infrastructure. Faster convergence unlocks marine dredging and remote mining operations where base stations are impractical. As early users validate performance, global subscriptions should climb, broadening the Mid and High-Level Precision GPS Receiver market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for Centimeter-Grade Receivers | -1.80% | Emerging markets worldwide | Short term (≤ 2 years) |

| Limited Coverage and Subscription Cost of Correction Services | -1.40% | Remote and offshore zones | Medium term (2–4 years) |

| Export Control and ITAR Restrictions on Multi-Constellation Boards | -0.90% | US manufacturers and embargoed regions | Medium term (2–4 years) |

| Adjacent-Band RF Interference from 5G and Ligado Deployments | -0.60% | North America and mid-band 5G corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Centimeter-Grade Receivers

Survey-grade devices cost USD 5,000 to USD 25,000, a hurdle for small farms and emerging-market surveyors. Multi-band chipsets, precision oscillators, and adaptive antennas push bill-of-material costs high enough to slow replacement cycles. u-blox unveiled the ZED-X20P module, claiming 90% lower total ownership, yet pricing still targets industrial buyers. Open-source options from Emlid and ArduSimple lower entry prices, but lack enterprise warranty and support. Absent volume price erosion, the Mid and High-Level Precision GPS Receiver market loses momentum among cost-sensitive users.

Limited Coverage and Subscription Cost of Correction Services

Annual RTK or PPP-RTK fees range from USD 1,200 to USD 3,600 per receiver, sizable recurring charges for contractors and growers. Sparse reference networks in Africa, parts of South America, and mid-ocean regions leave gaps in accuracy. Swift Navigation’s Series E funding targets a larger Skylark footprint, yet global 5-centimeter performance still needs dozens of LEO satellites. Where coverage remains patchy, users delay upgrades, moderating near-term growth in the Mid and High-Level Precision GPS Receiver market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Correction Technique Hybrid Architectures Gain Traction

Real-time kinematic solutions dominated 2025 with 48.84% of the Mid and High-Level Precision GPS Receiver market share, reflecting their use in surveying, construction, and row-crop farming. PPP-RTK hybrids now grow at 10.67% annually because they remove base-station dependencies and reduce convergence to under 1 minute. Differential GNSS and SBAS methods linger in aviation and maritime sectors that accept 20-centimeter accuracy. Precise point positioning, once limited by long convergence, gains relevance as Galileo offers free corrections via E6 signals. Trimble’s PULSAR integration exemplifies the pivot toward global, low-latency corrections.

Hybrid services rewrite procurement economics by blending PPP coverage with RTK speed. Operators in offshore wind projects and remote mining choose these links to avoid building costly terrestrial networks. Correction providers bundle cloud analytics, enabling predictive maintenance and fleet-wide performance dashboards. As a result, service revenue overtakes hardware margin inside the Mid and High-Level Precision GPS Receiver market. Regulatory bodies welcome authenticated signals that embed integrity flags, reinforcing trust in safety-critical workflows.

By Frequency Capability Multi-Band Receivers Capture Premium Segments

Dual-frequency units accounted for 46.39% of the Mid and High-Level Precision GPS Receiver market in 2025, thanks to a balanced cost-to-performance ratio. Multi-band boards expand at 11.06% per year as they resolve ambiguities faster, resist jamming, and exploit new Galileo E6 and BeiDou B2b signals. Single-band devices remain a low-cost option, but volumes slide as chip prices for dual-frequency modules drop below USD 50.

Septentrio’s mosaic-G5 shrank its footprint by 60% and reduced power by 40%, removing past barriers to dense sensor fusion in robotics. Automotive designers favor L1-L5 configurations because L5’s pilot component improves urban canyon resilience. Authentication data embedded in E6 enables position integrity checks essential for automated driving. These advantages funnel premium spending into multi-band lines, extending the runway for the Mid and High-Level Precision GPS Receiver market.

By Form Factor Smart Antennas Simplify Integration

Modular OEM boards accounted for 40.18% share in 2025, underpinning factory-installed solutions in graders, tractors, and survey rovers. Smart antennas are rising 10.98% annually because they combine GNSS, inertial, cellular, and correction processing in a single sealed housing. Reduced cabling lowers electromagnetic noise and simplifies regulatory testing.

u-blox’s ZED-F20P triple-band module updates at 25 hertz, suiting robotics that demand quick feedback loops. Backpack survey rovers integrate tactical-grade IMUs to ensure vertical accuracy through satellite outages. Tablet computers with embedded antennas expand the options for forestry or utility crews needing sub-meter resolution. Each improvement expands the addressable use cases and, in turn, the Mid and High-Level Precision GPS Receiver market.

By End-Use Industry Autonomous Vehicles Accelerate Demand

Surveying and mapping accounted for 32.29% of the 2025 value, yet autonomous platforms posted the steepest 10.78% CAGR to 2031. Highway authorities now require centimeter ground truth for safety driver disengagement logs, nudging fleet operators toward high-precision subscriptions. Construction and mining deploy machine control to shave 20% off cost overruns and address worker shortages.

Precision agriculture integrates RTK guidance into seeders, fertilizer rigs, and sprayers, slashing input costs per hectare. Marine dredging pairs multi-band receivers with multibeam sonar to maintain channels within strict depth tolerances. Government certifications secured by SingularXYZ unlock public procurement budgets. The cumulative effect sustains multi-year demand streaks inside the Mid and High-Level Precision GPS Receiver market.

Geography Analysis

Asia-Pacific led with 42.42% revenue in 2025 and is projected to retain a 10.83% CAGR through 2031. China mandates BeiDou integration across smartphones and connected cars, effectively guaranteeing baseline shipment volumes. India is rolling out 1,500 reference stations that cut project setup costs by 30% and encourage small survey firms to upgrade equipment. Japan’s QZSS augmentation service underpins rice transplanters that raise yields 8%, confirming return on investment for growers.

North America and Europe together contributed nearly 45% of the 2025 turnover. The U.S. aviation sector is upgrading WAAS for dual-frequency use to allow precision approaches at secondary airports. Germany’s contractors fit multi-band receivers onto excavators to comply with digital twin validation at a 2-centimeter tolerance. The United Kingdom’s expanded OS Net improves mapping accuracy for flood management, boosting receiver sales among civil engineers.

The Middle East, Africa, and South America together held 13% share in 2025, yet show strong upside. Saudi Arabia’s NEOM project establishes new geodetic networks to guide mega-infrastructure layouts. Brazil’s soybean growers automate grain handling with dual-band boards that coordinate harvest logistics. South Africa’s deep mines add multi-band receivers to track ore removal in GPS-denied shafts, while Egypt’s Suez Canal Authority maintains dredged depths using hydrographic kits. Collective demand from these initiatives keeps the Mid and High-Level Precision GPS Receiver market expanding worldwide.

Competitive Landscape

Trimble, Hexagon, and Topcon dominate the market through comprehensive portfolios that integrate hardware, software, and correction services. Hexagon has strengthened its position by acquiring companies with advanced anti-jamming technologies, enhancing its capabilities in the defense sector. Trimble has entered into strategic partnerships to incorporate advanced corrections technology and has made significant investments to accelerate the adoption of its solutions.

Venture-backed companies are intensifying competition by separating hardware from services. Swift Navigation is expanding its coverage and collaborating with major semiconductor companies to integrate advanced positioning software into standard chipsets. Point One Navigation is offering bundled solutions that combine cloud localization with cost-effective hardware, challenging the pricing strategies of established players.

The technological competition is focused on multi-frequency support, authenticated signals, and software-defined architectures that allow for firmware upgrades. Companies like u-blox are shifting their focus toward positioning intelligence, while open-source challengers such as Emlid are providing more affordable options for price-sensitive users. However, these challengers may face challenges in offering long-term support. The market's future is being shaped by strategies centered on partnerships, technological advancements, and subscription-based models, which are expected to influence profitability and growth in the precision GPS receiver market.

Mid and High-Level Precision GPS Receiver Industry Leaders

Trimble Inc.

Hexagon AB (Leica Geosystems Division)

Topcon Positioning Systems Inc.

Hemisphere GNSS Inc.

Septentrio NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Septentrio enlarged its AsteRx EB line with rugged units that integrate IMUs and cellular modems for continuous positioning in mapping and machine control applications.

- February 2026: CHC Navigation hosted CHCNAV Connect 2026, announcing vertical integration plans and new distribution partners in Southeast Asia, Africa, and South America.

- January 2026: Trimble integrated RTX ProPoint corrections into the Lucid Gravity electric vehicle to deliver centimeter positioning for next-generation driver assistance.

- September 2025: u-blox introduced the ANN-MB3 triple-band RTK antenna targeting robotics, automotive, and farming equipment.

Global Mid and High-Level Precision GPS Receiver Market Report Scope

The Mid and High-Level Precision GPS Receiver Market Report is Segmented by Correction Technique (RTK, PPP, PPP-RTK Hybrid, Differential GNSS/SBAS), Frequency Capability (Single-Frequency L1, Dual-Frequency L1/L2, Dual-Frequency L1/L5, Multi-Frequency ≥3 Bands), Form Factor (Modular OEM Boards, Integrated Smart Antennas, Rugged Handhelds and Controllers, Backpack/Pole-Mounted Rovers), End-Use Industry (Surveying and Mapping, Precision Agriculture, Construction and Mining, Marine and Dredging, Autonomous Vehicles), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Real-Time Kinematic (RTK) |

| Precise Point Positioning (PPP) |

| PPP-RTK Hybrid |

| Differential GNSS / SBAS |

| Single-Frequency (L1) |

| Dual-Frequency (L1/L2) |

| Dual-Frequency (L1/L5) |

| Multi-Frequency (?3 Bands) |

| Modular OEM Boards |

| Integrated Smart Antennas |

| Rugged Handhelds and Controllers |

| Backpack / Pole-Mounted Rovers |

| Surveying and Mapping |

| Precision Agriculture |

| Construction and Mining |

| Marine and Dredging |

| Autonomous Ground and Aerial Vehicles |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Correction Technique | Real-Time Kinematic (RTK) | |

| Precise Point Positioning (PPP) | ||

| PPP-RTK Hybrid | ||

| Differential GNSS / SBAS | ||

| By Frequency Capability | Single-Frequency (L1) | |

| Dual-Frequency (L1/L2) | ||

| Dual-Frequency (L1/L5) | ||

| Multi-Frequency (?3 Bands) | ||

| By Form Factor | Modular OEM Boards | |

| Integrated Smart Antennas | ||

| Rugged Handhelds and Controllers | ||

| Backpack / Pole-Mounted Rovers | ||

| By End-Use Industry | Surveying and Mapping | |

| Precision Agriculture | ||

| Construction and Mining | ||

| Marine and Dredging | ||

| Autonomous Ground and Aerial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Mid and High-Level Precision GPS Receiver market?

The Mid and High-Level Precision GPS Receiver market size reached USD 3.89 billion in 2026 and is projected at USD 6.26 billion by 2031, according to Mordor Intelligence.

How fast is the market expected to grow over the forecast period?

The Mid and High-Level Precision GPS Receiver market is forecast to record a 9.98% CAGR between 2026 and 2031, based on Mordor Intelligence estimates.

Which correction technique is gaining the most momentum?

PPP-RTK hybrid architectures are expanding 10.67% annually because they combine rapid convergence with global coverage.

Why is Asia-Pacific the largest regional contributor?

Mandatory BeiDou integration in China, Indias expanding reference network, and Japans centimeter augmentation service together underpin 42.42% of global 2025 revenue.

Which form factor is growing fastest?

Integrated smart antennas are registering a 10.98% CAGR as equipment makers prefer sealed, plug-and-play solutions.

How concentrated is the supplier landscape?

The top three vendors hold roughly half of global revenue, indicating moderate concentration, with a score of 6 on a 1-10 scale.

Page last updated on: