Nanopore Sequencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

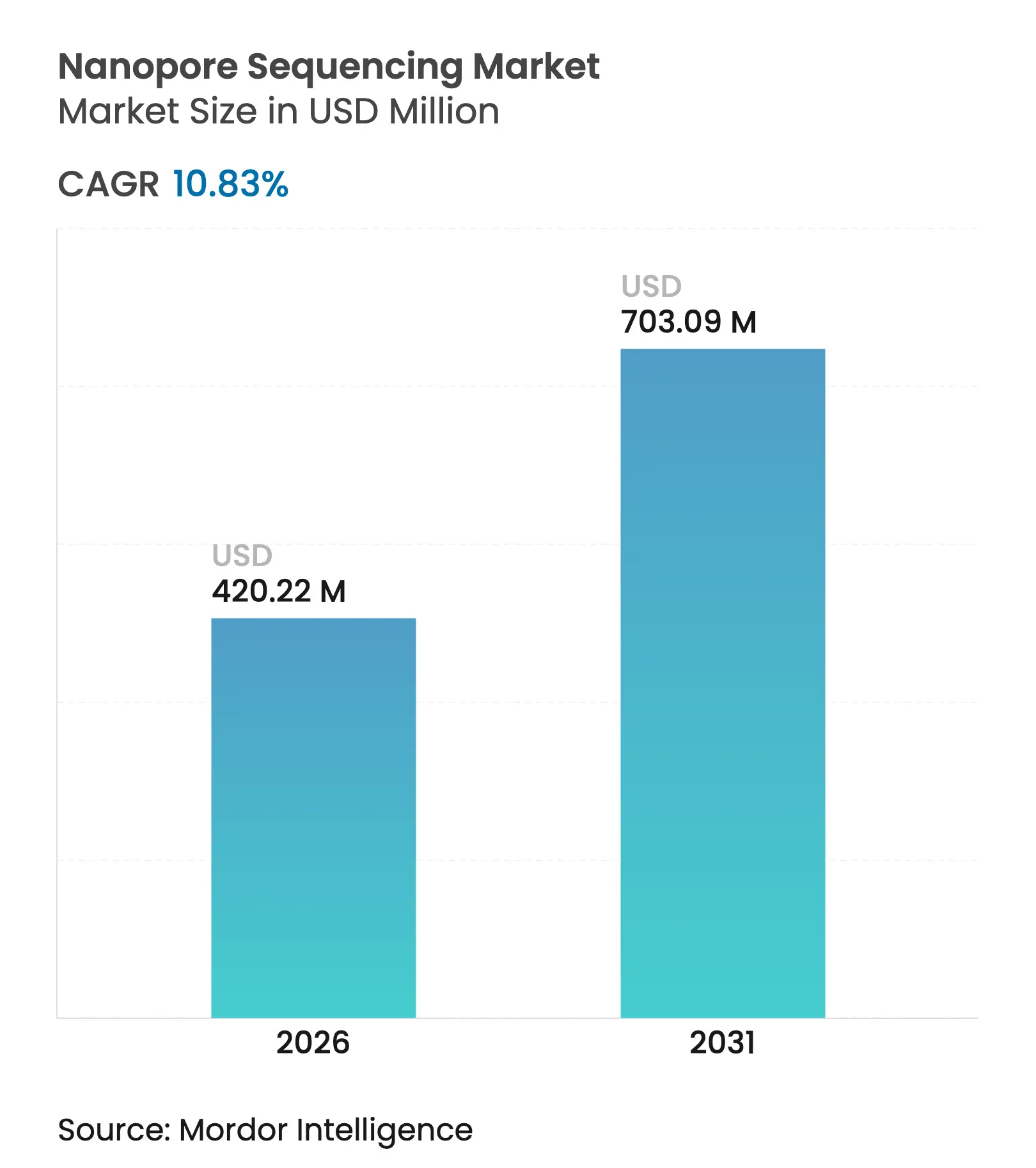

| Market Size (2026) | USD 420.22 Million |

| Market Size (2031) | USD 703.09 Million |

| Growth Rate (2026 - 2031) | 10.83 % CAGR |

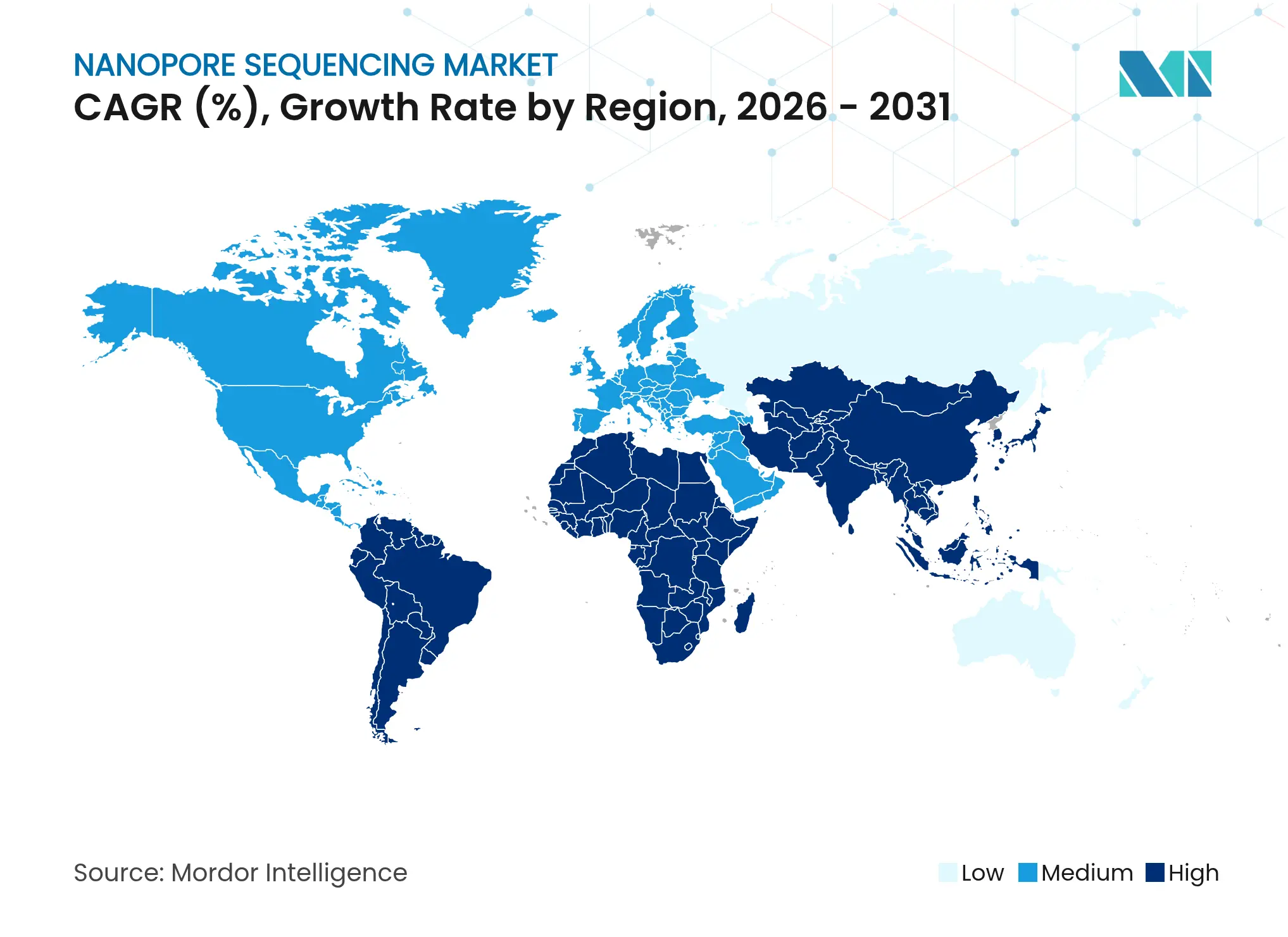

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

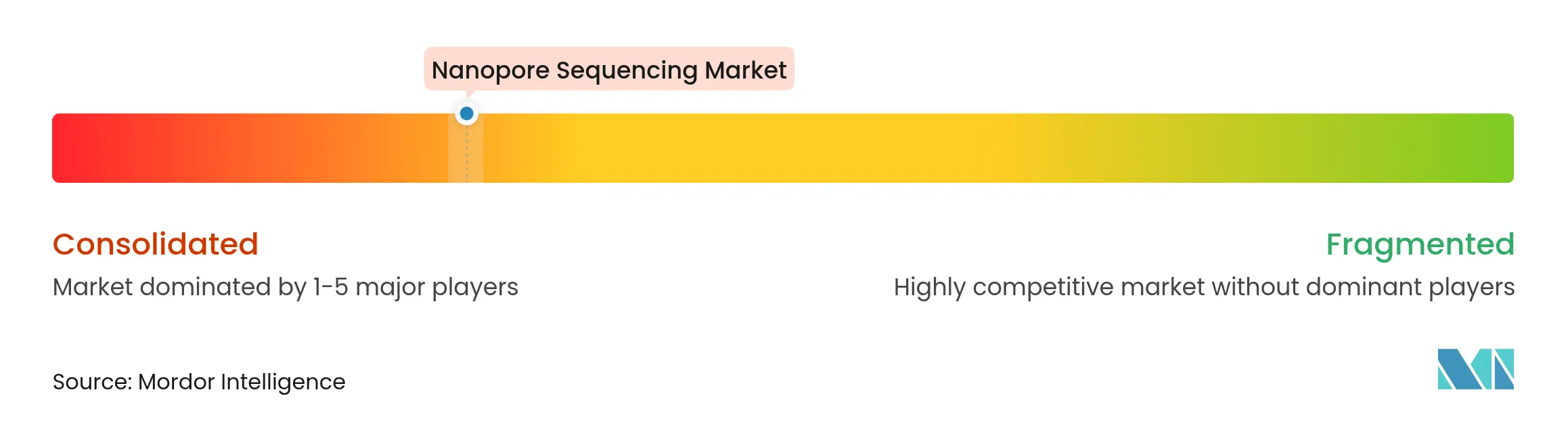

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Nanopore Sequencing Market Analysis by Mordor Intelligence

The nanopore sequencing market size was valued at USD 379.17 million in 2025 and estimated to grow from USD 420.22 million in 2026 to reach USD 703.09 million by 2031, at a CAGR of 10.83% during the forecast period (2026-2031). A steep learning curve in pore chemistry, rising AI-enabled analytics, and the spread of pocket-sized devices now let laboratories, clinics, and field teams interrogate genomes wherever samples occur. Hardware prices are gradually falling, propelling demand for data-centric software that curates, interprets, and triages raw reads in real time. North America continues to dominate revenue because its hospitals adopted precision-medicine programs early, yet Asia-Pacific posts the highest growth as governments channel funds into genomics infrastructure and sovereign data platforms. Competitive focus therefore shifts from throughput bragging rights to clinical-grade accuracy, seamless sample-to-answer workflows, and the breadth of third-party assay ecosystems that ride on a common operating system.

Key Report Takeaways

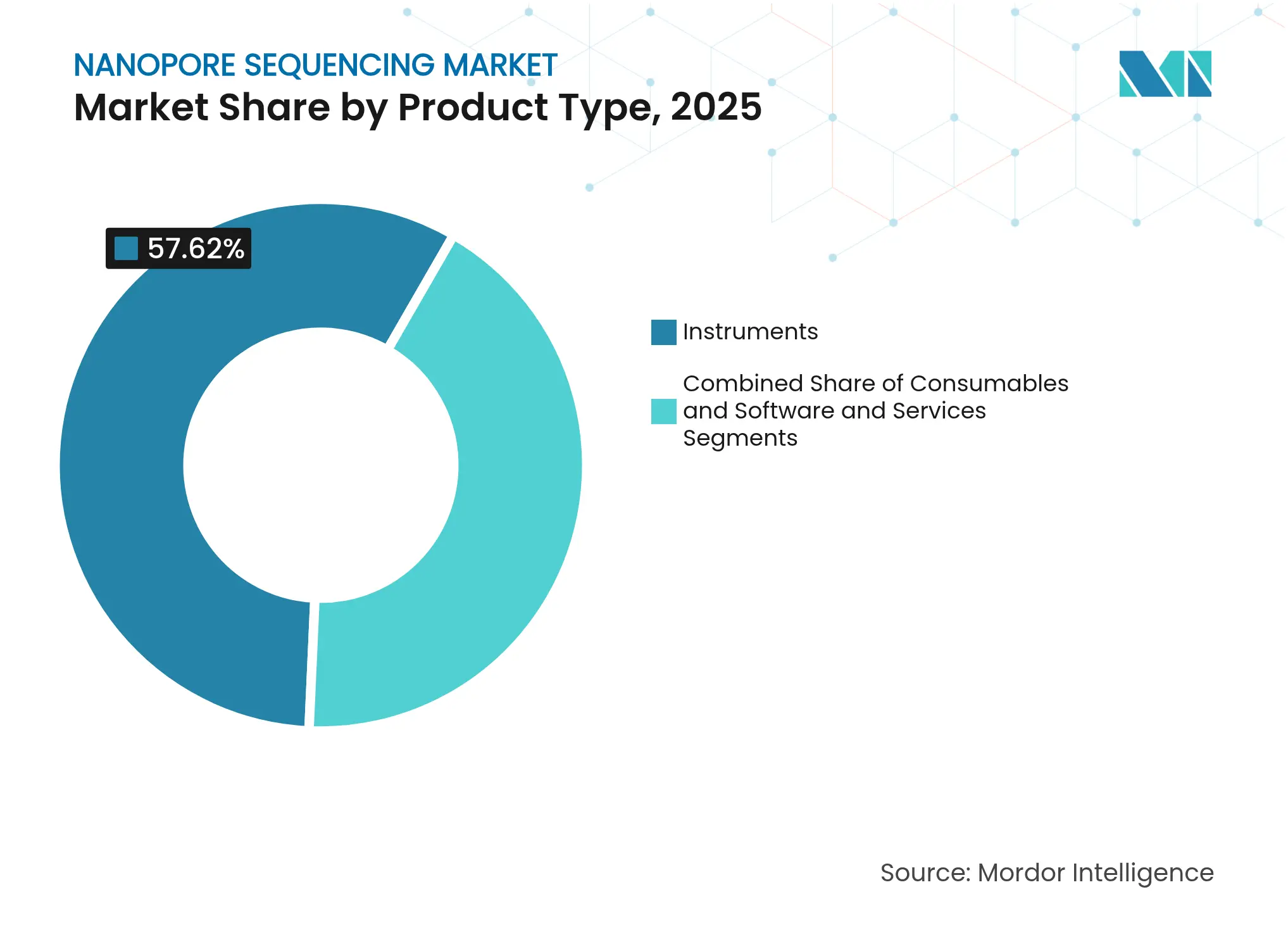

- By product type, instruments held 57.62% of nanopore sequencing market share in 2025; software & services is expanding at a 13.09% CAGR through 2031.

- By technology, biological nanopores accounted for 70.72% revenue in 2025, while solid-state nanopores are projected to rise at a 14.62% CAGR.

- By application, clinical diagnostics delivered 36.05% of sector revenue in 2025; infectious-disease surveillance is growing fastest with a 12.98% CAGR.

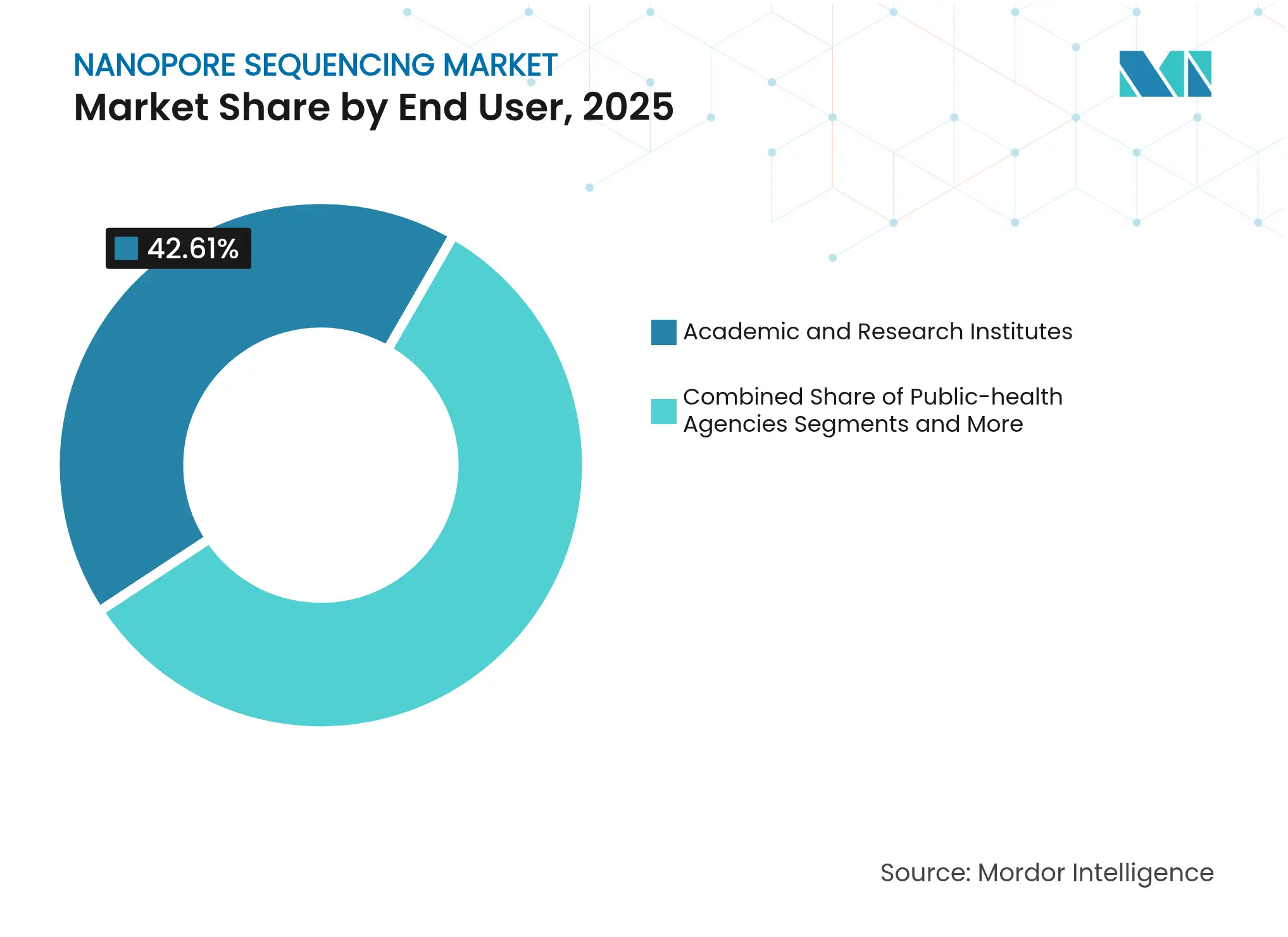

- By end user, academic & research institutes captured 42.61% share in 2025; public-health agencies are on track for a 13.92% CAGR.

- By sequencing throughput, portable devices represented 51.12% of 2025 revenue and also record the highest 13.85% CAGR.

- By geography, North America commanded 40.74% revenue in 2025; Asia-Pacific leads in growth with a 13.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nanopore Sequencing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing prevalence of genetic

disorders

Increasing prevalence of genetic

disorders

| +1.8% | Global, highest in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.8%

|

Geographic Relevance

:

Global, highest in North America

& EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Technological advances in pore

chemistry & base-calling

Technological advances in pore

chemistry & base-calling

| +2.1% | Global, led by UK & US innovation hubs | Short term (≤ 2 years) | |||

Declining sequencing costs &

device portability

Declining sequencing costs &

device portability

| +1.5% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) | |||

Precision-medicine demand in

oncology

Precision-medicine demand in

oncology

| +1.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) | |||

On-site food safety &

environmental monitoring uptake

On-site food safety &

environmental monitoring uptake

| +1.2% | Global, early adoption in developed markets | Medium term (2-4 years) | |||

Edge sequencing enabled by AI

analytics

Edge sequencing enabled by AI

analytics

| +1.7% | Global, concentrated in tech-forward regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Prevalence of Genetic Disorders

Genetic disease registries show a continuous rise in cases that demand deeper interrogation of structural variants and repeat expansions. Nanopore read lengths now span telomere-to-telomere, laying bare once-opaque regions that harbor clinically actionable mutations. Real-time runs shorten the interval between consent and diagnosis, a critical factor in neonatal intensive-care settings. Public-health agencies are expanding newborn-screening panels to reflect these capabilities.[1]Centers for Disease Control and Prevention, “Public Health Genomics at CDC,” cdc.gov Health systems therefore integrate long-read workflows into routine practice and train staff on interpretation, creating predictable demand for consumables and subscription analytics.

Technological Advances in Pore Chemistry & Base-Calling

Q20+ chemistry drove raw read accuracy above 99%, while on-device neural networks now detect single-base edits at similar rates. These milestones refute concerns over error profiles that formerly limited clinical adoption. Engineers exploiting wafer-scale lithography move solid-state devices closer to cost parity, aligning genomic hardware with Moore’s Law trajectories.[2]Lihuan Zhao, “Wafer-Scale Fabrication of Solid-State Nanopore Array With a Novel SpacerX Process,” Microsystems & Nanoengineering, nature.com Start-ups bundle adaptive sampling that selectively enriches target loci, trimming run-times and reagent use. Such innovations shorten the feedback loop between concept and commercial kit, reinforcing a virtuous cycle of accuracy and affordability.

Declining Sequencing Costs & Device Portability

Laptops and pocket PCs now power handheld sequencers that weigh less than 100 g, enabling field teams to read microbial genomes in remote clinics or at crop-disease hotspots. A study in Indonesia showed real-time tracking of drug-resistant microbes in slaughterhouse wastewater using a battery-powered MinION.[3]Richard Harth, “Portable DNA Sequencing Successfully Tracks Drug-Resistant Microbes in Slaughterhouse Wastewater,” Phys.org, phys.org Library prep kits now ship as single-step lyophilized pellets, cutting consumable outlay and reducing cold-chain exposure. Per-sample economics therefore approach or undercut short-read workflows, especially when factoring in logistics savings and time-to-insight advantages.

Precision-Medicine Demand in Oncology

Oncologists increasingly rely on long-read assays that capture fusion genes, methylation signatures, and copy-number events in a single test. FDA approvals of comprehensive genomic profiling panels underline regulatory confidence in NGS for patient management. Liquid biopsy protocols using nanopore technology enable longitudinal tumor monitoring without repeated tissue biopsies. Providers gain faster turnaround that guides therapy selection within clinically meaningful windows, boosting adoption in oncology centers of excellence across high-income economies and, progressively, in large tertiary hospitals worldwide.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Data-analysis complexity & lack

of standards

Data-analysis complexity & lack

of standards

| -1.4% | Global, especially smaller laboratories | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.4%

|

Geographic Relevance

:

Global, especially smaller

laboratories

|

Impact Timeline

:

Medium term (2-4 years)

|

High error rates limiting clinical adoption

High error rates limiting clinical adoption

| -1.1% | Global, highest in regulated markets | Short term (≤ 2 years) | |||

Supply-chain constraints for

nanopore components

Supply-chain constraints for

nanopore components

| -0.9% | Global, concentrated in semiconductor regions | Medium term (2-4 years) | |||

Data-privacy regulation for field

sequencers

Data-privacy regulation for field

sequencers

| -0.8% | EU & North America, expanding globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Data-Analysis Complexity & Lack of Standards

Long-read datasets dwarf short-read files in volume and heterogeneity, taxing storage budgets and bioinformatics pipelines. Many regional labs lack staff who can tune neural-network base-callers, forcing outsourcing that erodes the speed advantage. CDC’s Next Generation Sequencing Quality Initiative releases SOPs and reference datasets, yet harmonization across platforms remains patchy.[4]Centers for Disease Control and Prevention, “The Next Generation Sequencing Quality Initiative,” cdc.gov Regulatory filings therefore demand extra validation, inflating development costs. Without shared benchmarks, cross-study meta-analyses struggle for statistical power, delaying guideline inclusion.

High Error Rates Limiting Clinical Adoption

Despite accuracy gains, homopolymer stretches and GC-rich motifs still inflate indel counts in nanopore reads. Diagnostic labs must layer confirmatory PCR or orthogonal sequencing, doubling workloads. Payers hesitate to reimburse composite workflows until real-world concordance builds. Academic papers often highlight performance improvements, yet marketing claims require rigorous head-to-head studies that extend approval timelines. The result is a trust gap that vendors must close via controlled trials and transparent quality metrics.

Segment Analysis

By Product Type: Hardware Dominance Meets Software Momentum

Instruments generated the largest contribution to the nanopore sequencing market in 2025, capturing 57.62% revenue as research centers upgraded to high-output rigs. This hardware footprint underpins recurring demand for consumables and onboard compute upgrades. Conversely, software & services, though smaller in cash terms, is scaling fastest at a 13.09% CAGR because users seek turnkey analytics, variant annotation, and report automatization. That pivot tilts profit pools toward subscription models, positioning platform owners to cross-sell AI modules that improve call accuracy or compress file sizes. The emphasis on interpretation democratizes genomics, because a clinician can trigger cloud pipelines without mastering command-line scripts. Vendors now release graphical dashboards that flag quality issues in real time, a feature that proves vital in clinical sequencing where reruns carry ethical and financial costs.

Consumables continue to post steady single-digit growth thanks to built-in obsolescence of flow cells and reagent kits. Manufacturers experiment with reagent sachets that permit room-temperature shipping, shaving logistics charges for customers in tropical regions. In parallel, community-driven protocols lower library-prep barriers through fast transposase tagging. Together, these trends anchor stable repeat purchase cycles, even as headline instrument prices tick downward. With capital budgets under scrutiny, many labs adopt leasing or pay-per-use models, spreading costs over multiyear service contracts that bundle training and tech support.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Biological Stability Versus Solid-State Scale

Biological pores still underpin most commercial runs because protein engineering has optimized their selectivity, noise profile, and compatibility with diverse chemistries, locking in 70.72% of 2025 revenue. Users appreciate predictable lot-to-lot performance, a prerequisite for clinical regulators. Yet solid-state nanopores post a striking 14.62% CAGR, appealing to semiconductor firms that view sequencing chips as a natural adjacency. Once manufacturing yields pass critical thresholds, economies of scale could compress device pricing and widen the funnel of users in lower-middle-income economies. Over the forecast horizon, hybrid devices may splice protein gates onto silicon scaffolds, marrying accuracy with ruggedness and opening applications in extreme environments such as deep-sea biosurveys or planetary missions.

The competitive dialogue now goes beyond accuracy alone. Researchers ask whether platforms support multiomics reads, for example simultaneous mapping of DNA methylation or direct RNA transcription. Biological systems answer through modified pores and reagents, whereas solid-state proponents tout electrical field tuning that can, in theory, sense base modifications without chemistry tweaks. Investors funnel capital into both camps, betting that the winner will offer the broadest capture of analytes at the lowest total cost of ownership.

By Application: Diagnostics Anchor Revenue, Surveillance Fuels Growth

Clinical diagnostics remained the biggest revenue pillar, delivering 36.05% of the nanopore sequencing market in 2025 because tertiary hospitals validated long-read workflows for structural-variant detection. Reimbursement milestones in the US and EU gave CFOs confidence to green-light capital purchases. However, infectious-disease surveillance now supplies the fastest incremental revenue, expanding at a 12.98% CAGR. Governments invest in airport-based monitoring hubs that sequence viral genomes in incoming passengers within six hours, an ability proven during COVID-19 flare-ups. That operational readiness prompts airlines, cruise lines, and border agencies to integrate sequencing into routine biosafety protocols.

Secondary growth vectors include pharmacogenomics, where long reads resolve haplotype phase information that guides drug dosing, and ag-genomics, where breeders scan crop germplasm for resilience traits. Environmental monitoring use cases tiptoe toward real-time metagenomics dashboards that plot pathogen hotspots on geospatial maps. These application niches collectively hedge revenue against cyclical slowdowns in any single sector, thereby stabilizing vendor order books.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: Academia Leads, Public Health Accelerates

Academic and research institutes still represent the largest customer bloc with 42.61% of 2025 spending, reflecting their early-adopter culture and grant-funded mandates to explore frontier technologies. Yet public-health agencies furnish the steepest growth trajectory at 13.92% CAGR as ministries recognize the value of genomic surveillance in containing antimicrobial resistance and zoonotic spillover. Many agencies negotiate framework agreements that lock in discount tiers for consumables, smoothing procurement cycles and ensuring surge capacity during outbreaks.

Pharma companies enlarge their install bases to streamline target discovery and companion-diagnostic development, with oncology programs driving both short- and long-term demand. Hospitals form multidisciplinary genomics boards that interpret results for rare-disease clinics, moving sequencing closer to frontline care. Veterinary laboratories also join the user mix, sequencing animal pathogens that might jump species barriers, thereby reinforcing One-Health paradigms that link human, animal, and environmental health strategies.

Note: Segment shares of all individual segments available upon report purchase

By Sequencing Throughput: Portables Democratize Genomics

Portable sequencers, defined as devices yielding ≤ 20 Gb per run, owned 51.12% of 2025 sales and continue to clock the fastest 13.85% CAGR. Their self-contained design lets wildlife biologists sequence endangered species on site or forest rangers confirm invasive pests before clearing timber. Cloud dashboards sync results once connectivity returns, allowing expert teams in metropolitan centers to validate findings. Benchtop models serve mid-volume labs that require higher outputs but still value small footprints, while large hospitals adopt high-throughput rigs to batch hundreds of oncology samples per day.

The portable segment benefits from vibrant developer communities that publish field-optimized protocols such as lyophilized reagents, solar-powered battery packs, and ruggedized casings. Vendors ship starter bundles with step-by-step smartphone guides, lowering the intimidation barrier for first-time users. As throughput rises, on-device FPGA boards accelerate base-calling, keeping analysis times within clinical windows. This end-to-end convenience solidifies the portable device’s role as the gateway that on-boards new entrants into the wider nanopore sequencing market.

Geography Analysis

North America generated 40.74% of 2025 revenue because its reimbursed precision-medicine programs created dependable volume for cancer and rare-disease assays. Academic-medical centers rolled out hospital-integrated sequencing cores, anchoring commercial collaborations that funnel developmental chemistries toward clinical validation. Public-private partnerships such as the Advanced Molecular Detection program expand workforce training budgets, which translates into sustained consumable pull-through.

Europe occupies the second-largest slice but grows at a mid-single-digit pace as the forthcoming European Health Data Space regulation clarifies cross-border data-sharing rules, lowering friction for multi-site studies. National health services invest in newborn-screening expansion and antimicrobial-resistance tracking, channeling funds into point-of-care sequencers at district hospitals. EU conformity requirements foster a competitive aftermarket for CE-IVD-labeled kits, supporting regional SME innovators.

Asia-Pacific, with a 13.25% CAGR, outpaces every other bloc on sheer momentum. China’s ban on selected foreign sequencers opened niches for domestic champions who bundle nanopore platforms with cloud bioinformatics aligned to Mandarin-language interfaces. India earmarks grants for centers of excellence that train pathologists in long-read analytics. Australia’s biosecurity authorities deploy portable rigs along coastlines to profile invasive species, coupling environmental DNA assays with AI-driven dashboards for rapid action.

Latin America and the Middle East & Africa remain early in adoption but benefit from falling device prices and multilateral donor programs tackling tuberculosis, malaria, and food-borne outbreaks. Mobile labs mounted in vans now traverse rural districts, returning same-day variant reports that earlier required shipping to central labs abroad. Local universities partner with global NGOs to build bioinformatics curricula, seeding future growth as skilled labor pools expand.

Competitive Landscape

Market Concentration

Oxford Nanopore Technologies leads the nanopore sequencing market through relentless chemistry iterations, modular device tiers, and an open-source analysis ecosystem that fosters third-party protocol innovation. Its 2025 collaboration with Cepheid plugs rapid sample processing into long-read sequencing, turning around actionable infectious-disease reports in under three hours. Meanwhile, Illumina and Pacific Biosciences extend long-read portfolios to hedge against erosion in short-read dominance, signaling an arms race that tightens performance benchmarks.

Solid-state start-ups backed by semiconductor giants target wafer-level fabrication to slash flow-cell costs and integrate nanopores directly onto CMOS sensors. Their roadmap promises single-chip devices that slide into existing diagnostic-instrument form factors, potentially disrupting incumbents reliant on protein pore manufacturing. Software developers differentiate by compressing raw signal files without accuracy loss and by embedding regulatory-compliant audit trails, features that resonate with hospitals facing escalating data-storage fees.

Strategic acquisitions accelerate talent consolidation; larger firms snap up AI analytics shops or sample-prep specialists to assemble turnkey platforms. Cross-licensing agreements emerge as players recognize mutual benefits in standardizing adapter chemistries that unlock multi-vendor kit compatibility. Overall competition is vigorous yet collaborative, as stakeholders co-author white papers that establish minimum performance metrics for clinical submissions, thereby growing the total addressable market rather than fighting zero-sum battles.

Nanopore Sequencing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Volta Labs announced the Library Prep App for Oxford Nanopore LSK114 on the Callisto System, enabling higher-throughput long-read library prep.

- May 2025: Oxford Nanopore Technologies detailed a streamlined product lineup and new RNA analysis tools at London Calling 2025, targeting a 60–70% output boost by 2026.

- April 2025: Oxford Nanopore Technologies and Cepheid signed a strategic pact to combine GeneXpert sample prep with nanopore sequencing for rapid infectious-disease workflows.

- April 2025: Oxford Nanopore inked letters of intent with BRIC-CDFD and BRIC-NIBMG to establish two Indian genomics centers of excellence.

Table of Contents for Nanopore Sequencing Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Prevalence Of Genetic Disorders

- 4.2.2Technological Advances In Pore Chemistry & Base-Calling

- 4.2.3Declining Sequencing Costs & Device Portability

- 4.2.4Precision-Medicine Demand In Oncology

- 4.2.5On-Site Food Safety & Environmental Monitoring Uptake

- 4.2.6Edge Sequencing Enabled By AI Analytics

- 4.3Market Restraints

- 4.3.1Data-Analysis Complexity & Lack Of Standards

- 4.3.2High Error Rates Limiting Clinical Adoption

- 4.3.3Supply-Chain Constraints For Nanopore Components

- 4.3.4Data-Privacy Regulation For Field Sequencers

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Product Type

- 5.1.1Instruments

- 5.1.1.1Portable Sequencers

- 5.1.1.2Benchtop Sequencers

- 5.1.1.3High-throughput Sequencers

- 5.1.2Consumables

- 5.1.2.1Flow Cells

- 5.1.2.2Library Preparation Kits

- 5.1.2.3Reagents & Accessories

- 5.1.3Software & Services

- 5.1.3.1Base-calling & Data-analysis Software

- 5.1.3.2Cloud Sequencing Services

- 5.2By Technology

- 5.2.1Biological Nanopores

- 5.2.2Solid-state Nanopores

- 5.2.3Hybrid Nanopores

- 5.3By Application

- 5.3.1Clinical Diagnostics

- 5.3.2Human Genomics

- 5.3.3Oncology & Precision Medicine

- 5.3.4Plant & Animal Genomics

- 5.3.5Infectious-disease Surveillance

- 5.3.6Drug Development & Pharmacogenomics

- 5.3.7Food Safety & Environmental Monitoring

- 5.4By End User

- 5.4.1Hospitals & Diagnostic Centers

- 5.4.2Academic & Research Institutes

- 5.4.3Pharmaceutical & Biotechnology Companies

- 5.4.4Public-health Agencies

- 5.4.5Agrigenomics & Veterinary Labs

- 5.5By Sequencing Throughput

- 5.5.1Portable (≤ 20 Gb/run)

- 5.5.2Benchtop (20–200 Gb/run)

- 5.5.3High-throughput (≥ 200 Gb/run)

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Oxford Nanopore Technologies

- 6.3.2Illumina Inc.

- 6.3.3Pacific Biosciences

- 6.3.4Qitan Tech

- 6.3.5BGI Genomics

- 6.3.6F. Hoffmann-La Roche Ltd

- 6.3.7Thermo Fisher Scientific

- 6.3.8Quantapore Inc.

- 6.3.9Cyclomics

- 6.3.10Electronic Biosciences Inc.

- 6.3.11Nabsys Inc.

- 6.3.12iNanoBio Inc.

- 6.3.13Roswell Biotech

- 6.3.14Quantum-Si

- 6.3.15Imec

- 6.3.16GenapSys Inc.

- 6.3.17Singlera Genomics

- 6.3.18biomodal

- 6.3.19ONT-EPI2ME Labs

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Nanopore Sequencing Market Report Scope

As per the scope of the report, nanopore sequencing devices use flow cells which contain an array of nanopores embedded in an electro-resistant membrane. Each nanopore corresponds to its own electrode connected to a channel and sensor chip, which measures the electric current that flows through the nanopore. When a molecule passes through a nanopore, the current is disrupted to produce a characteristic ‘squiggle’. The squiggle is then decoded using base calling algorithms to determine the DNA or RNA sequence in real time.

The nanopore sequencing market is segmented into product type, application, technology, end-user and geography. By product type, the market is segmented into instruments and consumables. By application, the market is segmented into clinical diagnostics, human genomics, plant and animal research and drug development and pharmacogenomics. By technology, the market is segmented into DNA sequencing, RNA sequencing, and epigenetic sequencing. By end user, the market is segmented into hospitals and diagnostic centers, academic and research institutes, pharmaceutical and biotechnology companies and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market size is provided in terms of USD value.