White Biotech Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 454.60 Billion |

| Market Size (2031) | USD 580.82 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

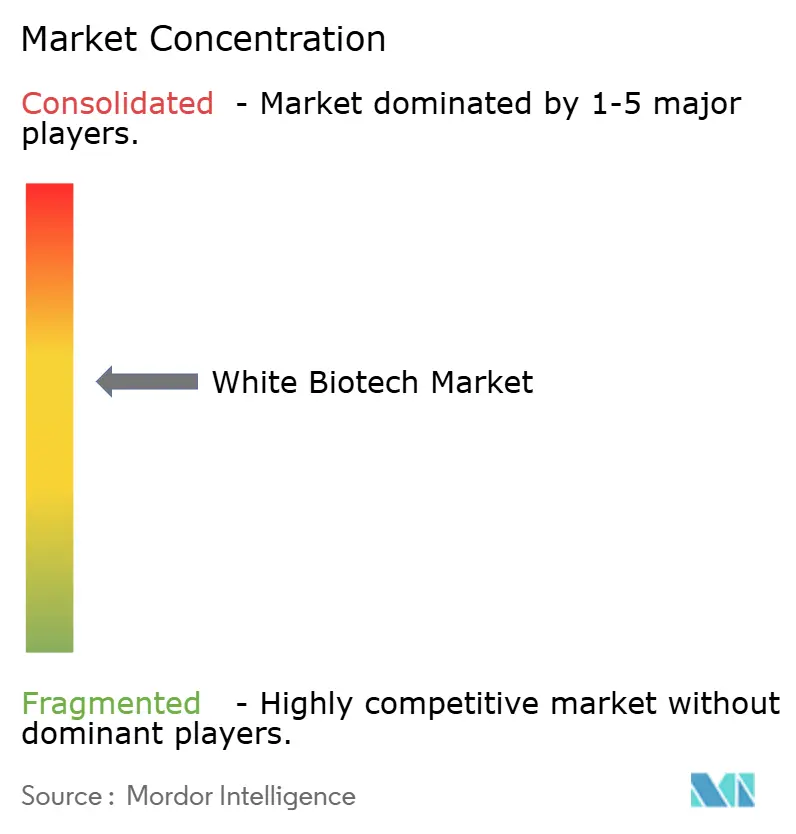

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

White Biotech Market Analysis by Mordor Intelligence

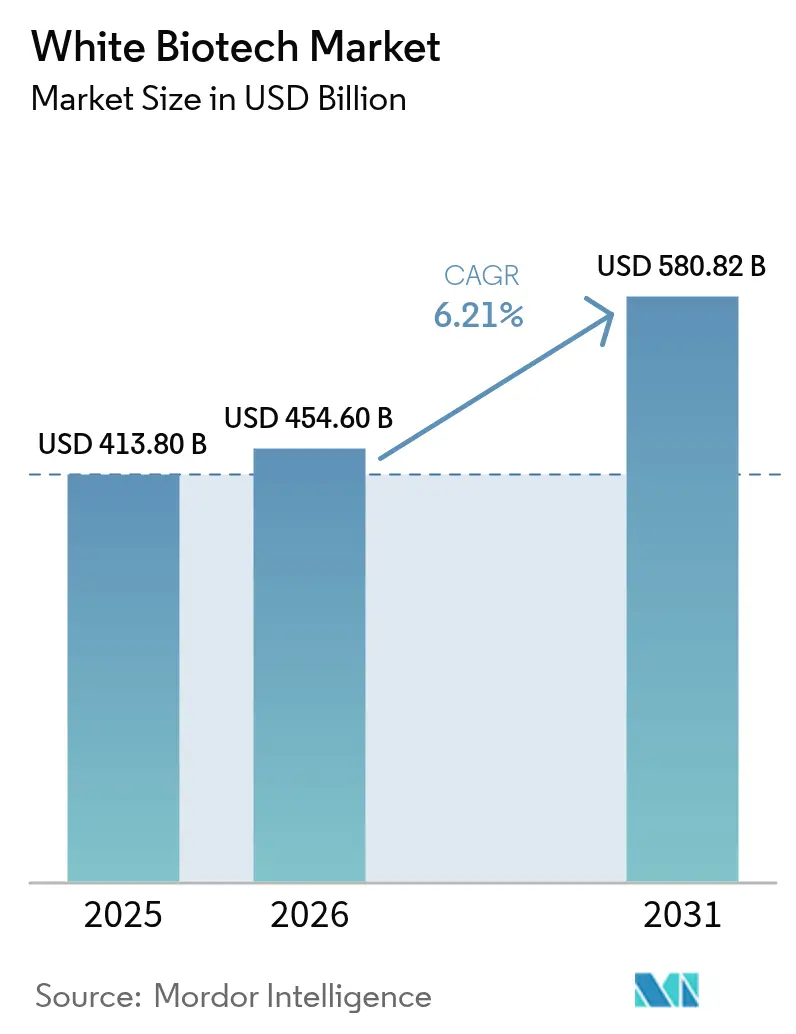

The white biotech market size was valued at USD 413.8 billion in 2025 and is estimated to grow from USD 454.6 billion in 2026 to reach USD 580.82 billion by 2031, at a CAGR of 6.21% during the forecast period (2026-2031). Policy-driven demand for sustainable aviation fuel, ethanol, and bio-derived polymers is redirecting capital away from petrochemical assets toward fermentation platforms, with carbon-pricing regimes and blending mandates translating regulatory intent into predictable revenue streams. Synthetic-biology breakthroughs are compressing R&D timelines, cutting enzyme dosage requirements, and lifting yields for high-value biochemicals, which further improves the total cost of ownership for buyers in food, feed, and industrial end-markets. Integrated producers are scaling new capacity in North America, Europe, and Asia-Pacific, yet cost-effective feedstock procurement and long construction cycles remain structural hurdles. Overall, the white biotech market is progressing from niche opportunity to mainstream supply chain component, helped by a growing pool of offtake agreements from consumer-brands and airlines that require verifiable reductions in Scope 3 emissions.

Key Report Takeaways

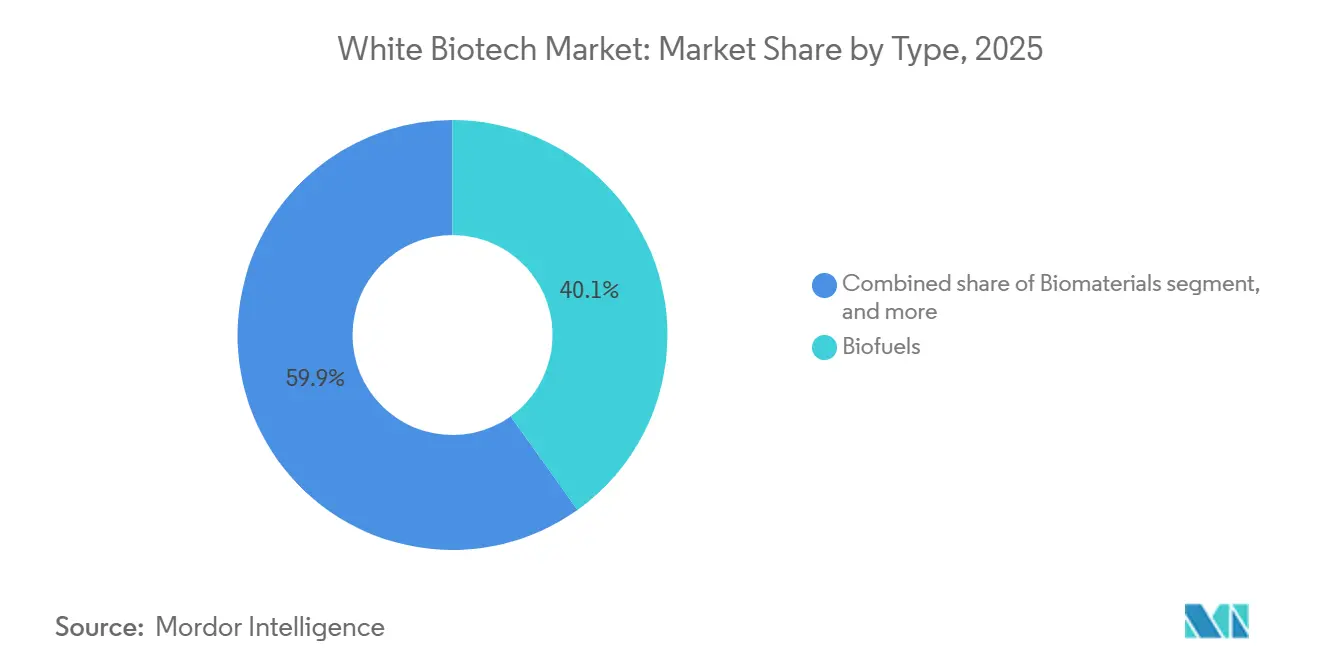

- By type, biofuels led with 40.12% of the white biotech market share in 2025, while biomaterials are expanding at a 7.29% CAGR through 2031

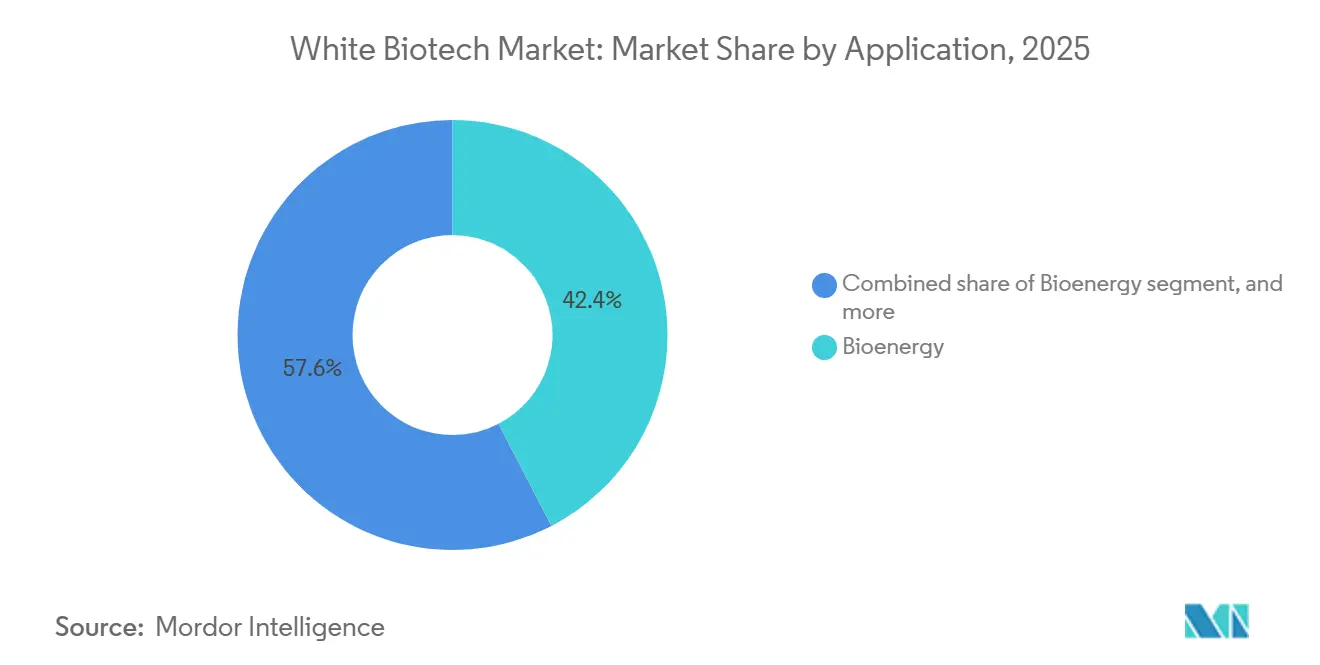

- By application, bioenergy accounted for 42.39% of revenue in 2025, and food and beverages are advancing at an 8.21% CAGR to 2031.

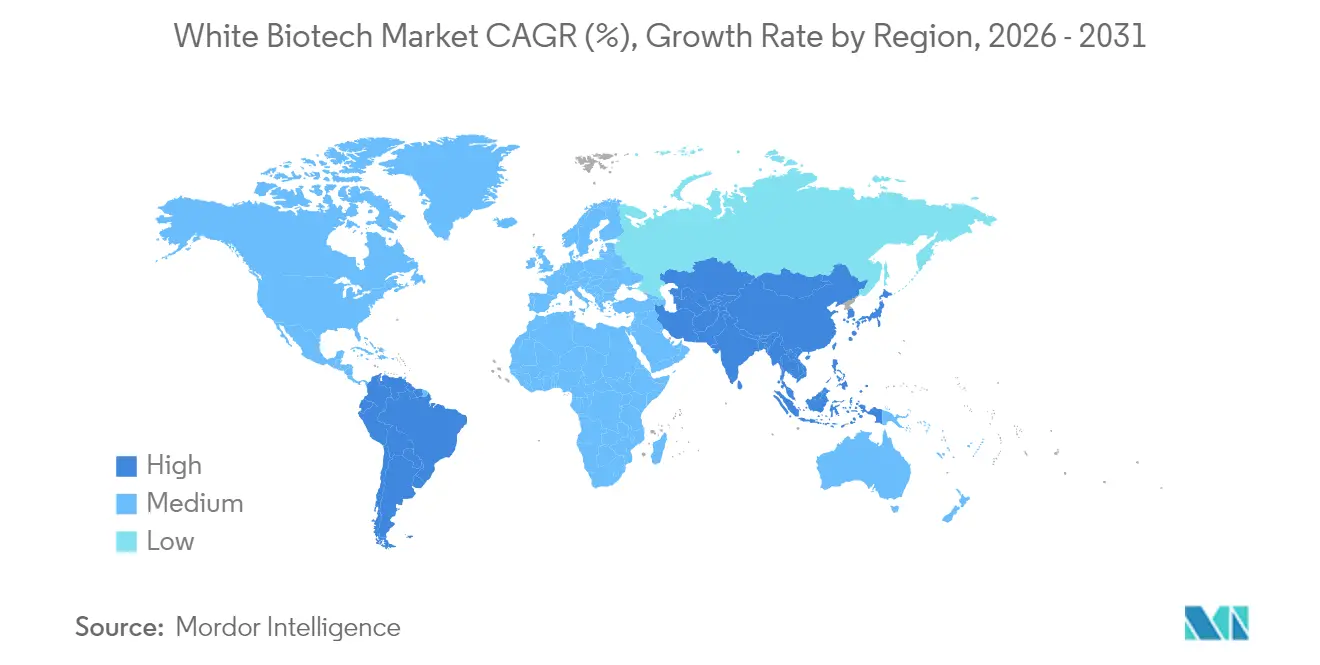

- By geography, North America captured 31.59% of the 2025 value, but Asia-Pacific is projected to record a 9.22% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global White Biotech Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Sustainable Industrial Processes | +1.2% | Global, with concentration in EU and North America | Medium term (2-4 years) |

| Supportive Regulatory Frameworks and Green Incentives | +1.5% | North America, EU, Asia-Pacific (China, India) | Short term (≤ 2 years) |

| Advancements in Synthetic Biology and Metabolic Engineering | +0.9% | Global, led by North America and EU R&D hubs | Long term (≥ 4 years) |

| Growing Adoption of Biofuels and Bioplastics | +1.3% | Global, with Asia-Pacific and South America leading volume | Short term (≤ 2 years) |

| Expanding Applications of Industrial Enzymes in Food and Beverage | +0.7% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Rising Consumer Preference for Bio-Based and Natural Products | +0.6% | North America, EU, urban centers in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Sustainable Industrial Processes

Decarbonization commitments are reshaping procurement criteria across chemicals, materials, and energy sectors, with corporate buyers increasingly specifying bio-based content thresholds to meet Scope 3 emissions targets. The European Union's updated Bioeconomy Strategy, released in 2024, prioritizes circular value chains that convert agricultural residues and municipal organic waste into bio-based intermediates, reducing reliance on fossil feedstocks[1]Source: European Commission, “EU Bioeconomy Strategy Update 2024,” ec.europa.eu. This policy shift is mirrored in private-sector commitments: Unilever announced in 2025 that 50% of its surfactant volumes would derive from renewable carbon by 2030, creating pull-through demand for bio-based fatty alcohols and glycerin. Carbon-pricing mechanisms in jurisdictions such as the EU Emissions Trading System and California's Low Carbon Fuel Standard assign tangible cost penalties to fossil-derived inputs, tilting total-cost-of-ownership calculations in favor of fermentation-derived alternatives even when upfront production costs remain higher. Industrial buyers are also scrutinizing supply-chain transparency, favoring suppliers that can document feedstock traceability and lifecycle carbon intensity, which advantages white biotech producers with certified sustainability frameworks such as ISCC PLUS or RSB.

Supportive Regulatory Frameworks and Green Incentives

Blending mandates and tax credits are accelerating capital deployment into biofuel and biochemical capacity. The United States Inflation Reduction Act, enacted in 2022 and operationalized through 2024-2025, offers production tax credits of up to USD 1.75 per gallon for sustainable aviation fuel that achieves a 50% lifecycle emissions reduction relative to petroleum jet fuel, with an additional USD 0.01 per percentage point of further reduction. This incentive structure has catalyzed announcements of over 20 new SAF projects in North America, including expansions by Chevron's Renewable Energy Group and partnerships between airlines and renewable-diesel producers. India's National Policy on Biofuels, amended in 2024, raised the ethanol-blending target to 20% by 2025-2026 and introduced a viability-gap funding mechanism for second-generation ethanol plants, de-risking investments in lignocellulosic conversion, according to the Ministry of Petroleum and Natural Gas, India[2]Source: Ministry of Petroleum and Natural Gas, “India Achieves 20% Ethanol Blending Target,” pib.gov.in. Brazil's RenovaBio program, which issues decarbonization credits (CBIOs) tradable on the stock exchange, generated over 40 million credits in 2024, providing a revenue stream that improves project economics for sugarcane-based biorefineries. Compliance frameworks such as the EU's Renewable Energy Directive III and ReFuelEU Aviation are creating long-term offtake certainty, which lenders require to finance capital-intensive fermentation and upgrading infrastructure.

Advancements in Synthetic Biology and Metabolic Engineering

CRISPR-based genome editing and machine-learning-guided strain optimization are compressing development timelines and improving yields for fermentation-derived products. Researchers at the Massachusetts Institute of Technology demonstrated in 2025 that AI-driven metabolic flux analysis could increase succinate production in engineered Escherichia coli by 34% relative to traditional random mutagenesis, reducing feedstock consumption per kilogram of output. This capability is particularly valuable for high-value biochemicals, where even modest yield gains translate into significant margin expansion. Synthetic-biology platforms are also enabling the production of molecules previously accessible only through petrochemical synthesis or extraction from scarce natural sources. Amyris, a California-based biotech firm, scaled commercial production of bio-based squalane, a cosmetic ingredient traditionally derived from shark liver or petrochemical olefins, using engineered yeast strains, capturing premium pricing in personal-care markets. Enzyme engineering is advancing in parallel: directed evolution and computational protein design have yielded cellulases and ligninases with higher thermostability and substrate specificity, lowering enzyme dosing requirements in cellulosic ethanol production and reducing operating costs by an estimated 15-20%. These tools are democratizing access to bio-manufacturing, enabling smaller firms to compete on innovation rather than scale alone.

Growing Adoption of Biofuels and Bioplastics

Aviation and packaging sectors are driving step-change demand for drop-in biofuels and compostable polymers. Global sustainable aviation fuel consumption reached approximately 600 million liters in 2025, a fivefold increase from 2023, propelled by airline commitments and regulatory mandates in Europe and California. Airlines are entering long-term offtake agreements at fixed premiums over conventional jet fuel, providing revenue visibility that justifies the construction of hydroprocessed esters and fatty acids (HEFA) and alcohol-to-jet facilities. In bioplastics, polylactic acid capacity expansions are concentrated in Asia-Pacific: Emirates Biotech announced a 160,000-tonne-per-annum PLA plant in the United Arab Emirates, scheduled for 2028, targeting Middle Eastern and European packaging markets. Polyhydroxyalkanoate production capacity is projected to grow tenfold by 2027 as brands such as Danone and PepsiCo trial PHA-based bottles to meet plastic-reduction pledges. Regulatory tailwinds include the EU's Single-Use Plastics Directive and Extended Producer Responsibility schemes that penalize non-recyclable packaging, creating cost arbitrage favoring compostable alternatives in food-service applications.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Cost-Effective Feedstocks | -0.8% | EU, North America, emerging markets with competing land use | Short term (≤ 2 years) |

| Lack of Infrastructure for Large-Scale Fermentation in Emerging Markets | -0.6% | Asia-Pacific (ex-China), MEA, parts of South America | Medium term (2-4 years) |

| High Capital Investment and Infrastructure Requirements | -0.7% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Complexity in Scaling Up Bioprocesses | -0.5% | Global, affecting first-time commercial deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Cost-Effective Feedstocks

As competing demands, ranging from pellet exports for European power generation to applications in animal feed and food, drive up prices for agricultural residues and energy crops, the biomass feedstock markets are tightening. In late 2024, European wood-pellet prices jumped to EUR 180-220 per ton (USD 195-238 per ton). This surge was fueled by coal-to-biomass conversions in Germany and the Netherlands. As a result, cellulosic ethanol producers found themselves grappling with negative crush margins unless they could secure their own feedstock sources. Meanwhile, in the United States, corn prices rose to an average of USD 4.80 per bushel in 2025, up from USD 4.20 in 2023. This increase squeezed ethanol-refining margins, leading some facilities to temporarily halt operations during off-peak demand. For dispersed agricultural residues like wheat straw, corn stover, and sugarcane bagasse, logistics costs, covering collection, densification, and transport, often surpass USD 30-40 per tonne. This high cost diminishes the advantage these residues have over concentrated fossil feedstocks, which can be delivered more economically via pipeline or rail. While second-generation feedstocks, including municipal solid waste and industrial CO₂ streams, present diversification opportunities, they come with challenges. These feedstocks necessitate preprocessing infrastructure and navigate regulatory uncertainties, especially concerning waste-classification standards. Regions lacking established biomass supply chains face heightened feedstock risks. Here, producers are compelled to invest in agronomic extensions, storage facilities, and quality-assurance protocols before they can scale their production.

High Capital Investment and Infrastructure Requirements

Greenfield biorefinery construction demands USD 100-500 million in upfront capital, with project timelines stretching 3-5 years from final investment decision to commercial operation. A 200-million-liter-per-year cellulosic ethanol facility typically requires USD 250-300 million for pretreatment reactors, enzymatic hydrolysis tanks, fermentation vessels, distillation columns, and wastewater treatment, alongside working capital for feedstock inventory and enzyme procurement. Debt financing hinges on long-term offtake agreements and government loan guarantees, which are scarce in markets without established biofuel mandates. Equity investors demand internal rates of return exceeding 12-15%, difficult to achieve when competing against depreciated petrochemical assets with sunk capital costs. Modular biorefinery designs and co-location with existing industrial sites, such as pulp mills or sugar refineries, can reduce capital intensity by 20-30% through shared utilities and waste-heat integration, but require complex partnership structures and technology-licensing agreements. Emerging markets face additional hurdles: limited access to project finance, currency risk, and gaps in engineering, procurement, and construction expertise for bioprocessing equipment. These barriers explain why over 60% of announced bioplastics capacity additions during 2020-2025 were concentrated in North America, Europe, and China, despite lower feedstock costs in regions such as Southeast Asia and sub-Saharan Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Biofuels Lead, Biomaterials Accelerate

In 2025, biofuels represented 40.12% of total revenue, emphasizing the competitive edge ethanol and renewable diesel gain from blending mandates that ensure consistent demand. While this dominance establishes biofuels as the largest contributor to the white biotech market, their operating margins remain constrained due to price sensitivity. In Europe, sustainable aviation fuel commands a premium of USD 1.50-2.00 per liter over jet A-1, enhancing the profitability of new HEFA and alcohol-to-jet facilities. To address palm oil price volatility, biodiesel producers are increasingly adopting waste-oil feedstocks. Meanwhile, biomaterials, led by PLA and PHA, are expected to grow at a strong 7.29% CAGR, the fastest rate within the white biotech sector, particularly as spot PLA prices approach those of polypropylene.

Marking a shift from niche to mainstream, NatureWorks has launched a 75,000-tonne PLA facility in Thailand, while Balrampur Chini Mills has established an 80,000-tonne unit in India. Beverage companies are targeting 30% renewable content in their bottles, driving the adoption of bio-based PET, which is derived from sugarcane ethanol. Although industrial enzymes operate on a smaller scale, their unique functionalities enable them to achieve high margins, leading to increased use in brewing, baking, and animal feed. Biochemicals such as bio-succinic acid, aimed at high-value applications in polyurethane and solvents, are supported by the development of a 50,000-tonne plant in Iowa by DSM-Firmenich and Cargill. These advancements not only expand the scope of the white biotech market but also reduce its reliance on fuel-driven economics.

By Application: Bioenergy Dominates, Food and Beverages Surge

In 2025, bioenergy contributed 42.39% of the total turnover, driven by the widespread adoption of ethanol blending and renewable diesel, particularly supported by LCFS credits in California. This segment holds the largest share of the white biotech market; however, its growth potential is tempered by margin pressures stemming from fluctuating commodity prices. The food and beverage sector, projected to grow at a robust 8.21% CAGR, has emerged as the fastest-growing application. This growth is fueled by the increasing use of enzyme solutions, which enable clean-label reformulations and deliver energy savings in processes such as brewing and baking.

Pharmaceuticals continue to depend heavily on fermentation technologies for the production of antibiotics and vitamins. In this context, China is expanding its bio-vitamin E production capacity to meet the rising demand in the health supplement market. The animal feed segment is also witnessing growth, driven by the adoption of phytase and protease enzymes, which help comply with stringent nutrient runoff regulations in the EU and North America. Other industrial applications, including textiles, cleaning products, and coatings, remain smaller in scale but are steadily expanding. This growth is attributed to the increasing preference for bio-based alternatives over harsh chemicals, as brands aim to meet eco-label standards. The diversification and expansion of these applications highlight the resilience and adaptability of the white biotech market.

Geography Analysis

North America, expected to account for 31.59% of the 2025 value, remains a key player in the white biotech market. This dominance is driven by the Inflation Reduction Act, which facilitated over USD 10 billion in biorefinery investments through substantial SAF and renewable diesel credits. Ethanol production reached 15.8 billion gallons, while renewable diesel capacity grew to 5.2 billion gallons, supported by advancements in soybean oil and used cooking oil. Canada utilizes canola and forest residues for biodiesel and biomethane production, whereas Mexico, despite limited mandates, is targeting an E10 goal by 2027. With corn supplies tightening, the region's future growth will depend on cellulosic or waste-based feedstocks, shaping the next phase of North America's white biotech market. Europe is progressing steadily, supported by the Fit for 55 package, ReFuelEU Aviation's 6% SAF mandate, and a target to produce 35 billion cubic meters of biomethane by 2030, according to the European Commission[3]Source: European Commission, “ReFuelEU Aviation: Sustainable Aviation Fuel Mandate,” ec.europa.eu. Germany, France, and the Netherlands are deploying anaerobic digesters, while Sweden and Finland are incorporating lignin extraction into forest biorefineries. However, high feedstock costs and complex sustainability certifications are compressing margins in Southern Europe, where biomass often moves north for processing. Despite these challenges, the cascading-use principles outlined in the EU Bioeconomy Strategy ensure continued investment, strengthening Europe's position in the white biotech market.

The Asia-Pacific region is projected to achieve the fastest CAGR of 9.22% in the white biotech market, driven by China's dual-carbon objectives, India's ethanol blending progress, and palm-oil refinery projects in Southeast Asia. China approved six cellulosic ethanol plants with a combined capacity of 1.5 billion liters in 2024. India, leveraging supportive policies and abundant sugar and maize feedstock, achieved a 20% blending target in 2025, ahead of schedule by two quarters. Indonesia and Malaysia exported 8 million tonnes of biodiesel in 2025, though buyers are increasingly demanding RSPO certification. Japan and South Korea are focusing on bio-based chemicals for the cosmetic and pharmaceutical industries. Meanwhile, Australia is exploring straw-based ethanol but requires stronger policy support to scale production. This rapid growth solidifies Asia-Pacific's role as a critical demand center in the global white biotech market.

In South America, Brazil leads as the world's second-largest ethanol producer, generating 32 billion liters in 2025, supported by the RenovaBio decarbonization credit market. Brazil's competitive advantage, driven by low-cost sugarcane yields, is offset by political instability and currency fluctuations, which deter foreign investment. Argentina's soybean-based biodiesel faces declining demand from the EU, while Colombia is considering palm-oil refinery projects. These factors collectively define a mid-sized, feedstock-rich segment of the white biotech market. The Middle East and Africa, though still emerging, hold strategic potential. The UAE is constructing a 160,000-tonne PLA plant to meet European and Gulf packaging demand. Saudi Arabia, under its Vision 2030 initiative, has identified bio-based chemicals as a diversification priority. Sub-Saharan Africa, despite its abundant resources, lacks the necessary conversion infrastructure, leading to value losses from unprocessed biomass. The region's future share in the white biotech market will depend on incremental policy support and technology transfers.

Competitive Landscape

Established companies in the white biotech market capitalize on their scale advantages; however, they are increasingly challenged by technology-driven startups and strategic partnerships that disrupt traditional operations. The market remains highly competitive, with major players consistently channeling significant investments into research and development to sustain their market dominance. The ongoing trend of consolidation highlights the industry's focus on achieving greater operational efficiency and integrating advanced technological capabilities to address the evolving demands of the market effectively.

With rapid technological advancements and a growing demand for innovative solutions, the market is shifting toward platform-based competition. Companies such as Ginkgo Bioworks are actively expanding their partnerships across the research and development value chain. By leveraging synthetic biology, they aim to shorten product development timelines and reduce commercialization risks. These collaborations not only promote the exchange of knowledge and optimization of resources but also accelerate innovation in biotechnology applications across a wide range of industries, driving the market forward.

Precision fermentation, particularly for food applications, represents a significant growth area, offering opportunities to develop sustainable protein alternatives and functional ingredients. Companies like Biomatter are at the forefront of innovation, introducing AI-powered enzyme optimization platforms that challenge traditional research and development methodologies. These advancements enable faster product development and enhance process efficiency. New entrants in the market are adopting extremophilic bacteria and innovative fermentation techniques to address critical issues such as water scarcity and energy consumption. Meanwhile, established companies are responding to these disruptions by pursuing acquisitions and entering into technology licensing agreements, ensuring they maintain their competitive edge in this rapidly evolving and dynamic market landscape.

White Biotech Industry Leaders

Lonza Group Ltd

International Flavors & Fragrances Inc.

Corbion NV

DSM-Firmenich AG

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Manus Bio and Inscripta merged to establish an industrial biomanufacturing platform that integrates genome engineering with cell factory technologies. The combined entity aims to reduce development times and enhance the economics of bio-based alternatives in the food, beauty, and agriculture markets.

- February 2025: Novonesis completed the acquisition of DSM-Firmenich's share in their Feed Enzymes Alliance for EUR1.5 billion (USD1.56 billion). The transaction positions Novonesis to offer combined enzymes and probiotics to customers amid rising global protein demand.

- November 2024: IFF developed TEXSTAR™, an enzymatic texturizing solution that enhances the texture of dairy and plant-based fermented products. TEXSTAR™ converts sucrose into poly- and oligosaccharides during fermentation through enzymatic processes, improving texture, smoothness, and shine without requiring additional stabilizers, unlike traditional starch-based stabilizers.

Global White Biotech Market Report Scope

White biotechnology, also known as industrial biotechnology, refers to the use of enzymes and microorganisms to produce bio-based products for use in sectors, such as chemicals, food and feed, healthcare, consumer goods, and automotive.

The white biotech market is segmented on the basis of type, application, and geography. Based on type, the white biotech market report is segmented into biofuels, biomaterials, biochemicals, and industrial enzymes. Based on application, the market report is segmented into bioenergy, pharmaceuticals, food and beverage, feed, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

The market sizing has been done in value terms in USD for all the above-mentioned segments.

| Biofuels |

| Bioaterials |

| Biochemicals |

| Industrial Enzymes |

| Bioenergy |

| Pharmaceuticals |

| Food and Beverages |

| Animal Feed |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Biofuels | |

| Bioaterials | ||

| Biochemicals | ||

| Industrial Enzymes | ||

| By Application | Bioenergy | |

| Pharmaceuticals | ||

| Food and Beverages | ||

| Animal Feed | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the white biotech market expected to grow between 2026 and 2031?

The white biotech market is projected to expand at a 6.21% CAGR from 2026 to 2031, taking value to USD 580.82 billion.

Which segment currently provides the largest revenue in white biotech?

Bioenergy, powered by ethanol blending and renewable diesel, delivered 42.39% of 2025 revenue.

What is the fastest-growing application area for white biotech solutions?

Food and beverages lead with an expected 8.21% CAGR as enzymes enable clean-label reformulation and energy savings.

Which region will add the most incremental demand by 2031?

Asia-Pacific is forecast to grow at 9.22% through 2031, the steepest regional CAGR, driven by China and India.

Page last updated on: