NAND Flash Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 58.69 Billion |

| Market Size (2031) | USD 76.03 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

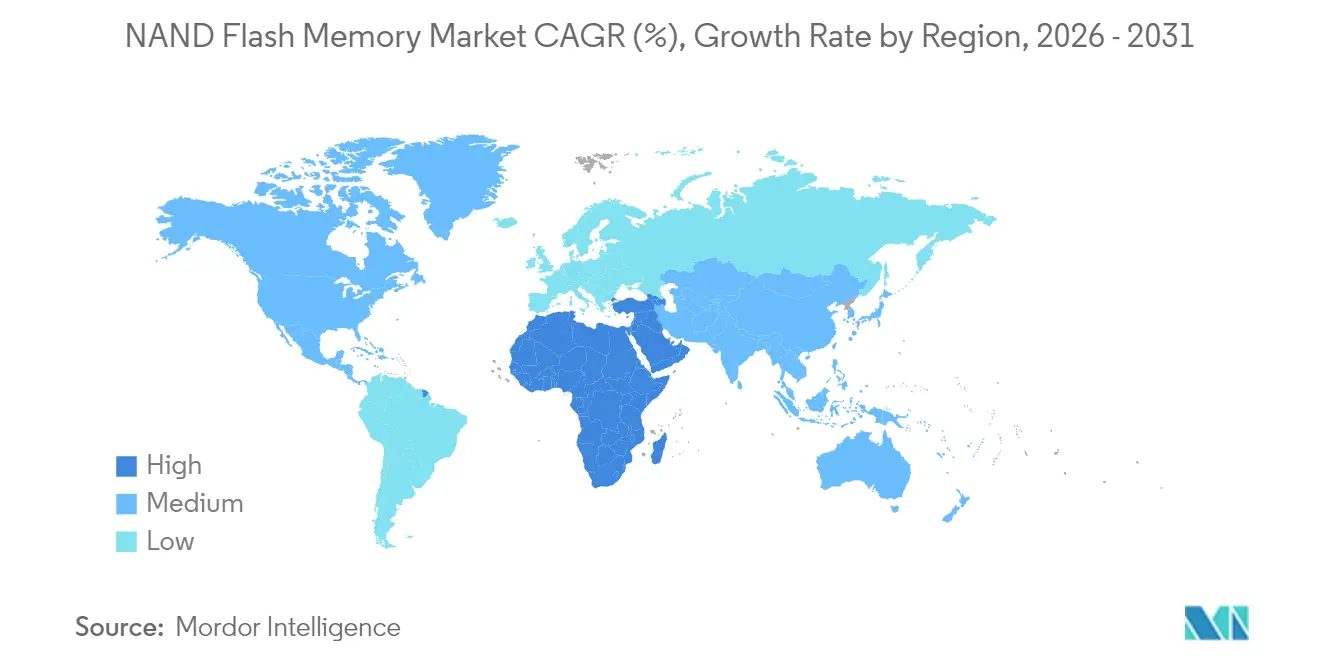

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NAND Flash Memory Market Analysis by Mordor Intelligence

NAND flash memory market size in 2026 is estimated at USD 58.69 billion, growing from 2025 value of USD 55.73 billion with 2031 projections showing USD 76.03 billion, growing at 5.32% CAGR over 2026-2031. This steady expansion is powered by hyperscale data-center capital spending on artificial-intelligence training clusters, the transition of client PCs and game consoles to solid-state storage, and vertically-scaled 3D architectures that keep cost-per-bit on a declining path. At the same time, national incentives to localize semiconductor fabrication, especially in the United States and Saudi Arabia, are strengthening regional supply resilience. Layer-count breakthroughs above 300 layers and PCIe 5.0 adoption are shortening replacement cycles for both enterprise and consumer SSDs. The confluence of 5G rollouts and massive IoT endpoints further widens addressable demand, positioning the NAND flash memory market for durable mid-single-digit growth horizons.

Key Report Takeaways

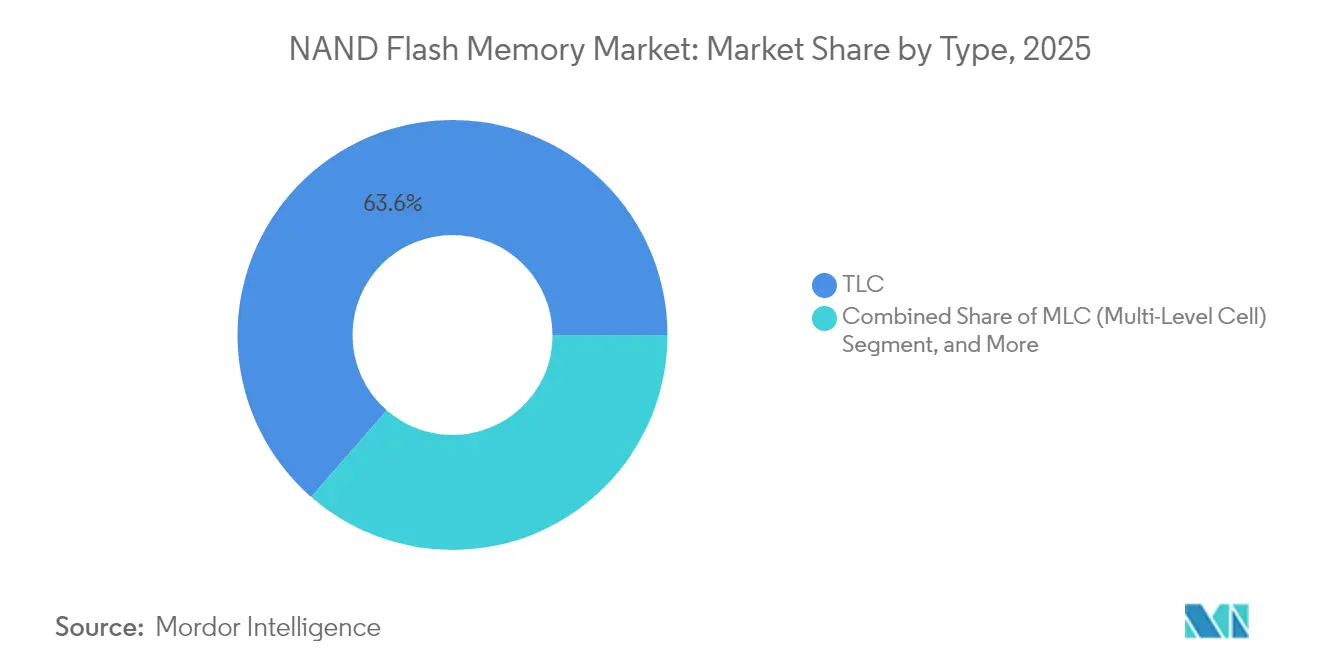

- By type, triple-level cell (TLC) captured 63.58% revenue share of the NAND flash memory market in 2025, whereas quad-level cell (QLC) is projected to expand at 6.35% CAGR through 2031.

- By structure, 3D NAND accounted for 86.85% of the NAND flash memory market size in 2025 and is forecast to grow at a 6.54% CAGR to 2031.

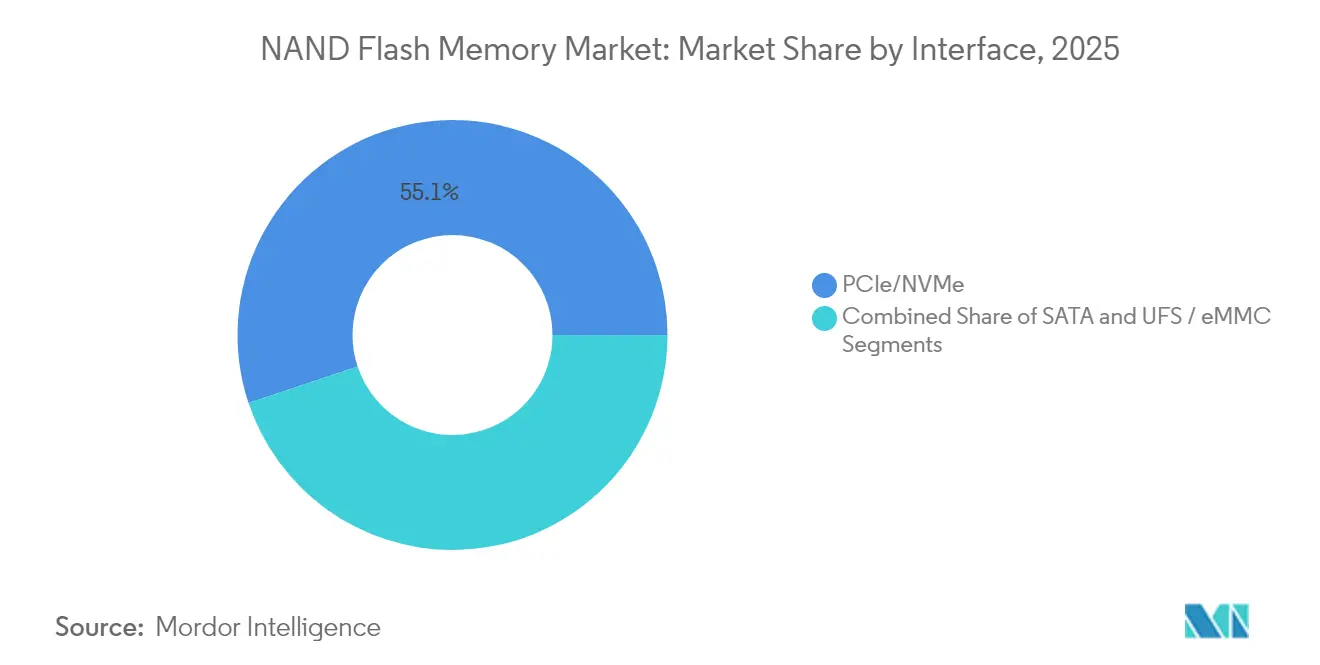

- By interface, PCIe/NVMe commanded 55.12% share of the NAND flash memory market size in 2025, while NVMe-over-PCIe 5.0 is advancing at 7.88% CAGR through 2031.

- By application, smartphones led with 41.05% of the NAND flash memory market share in 2025; enterprise SSDs register the fastest CAGR at 7.42% to 2031.

- By geography, Asia-Pacific held 55.40% of revenue in 2025, whereas the Middle East & Africa region recorded the highest 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global NAND Flash Memory Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-center AI/ML storage surge | +1.80% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| 5G and massive-IoT device proliferation | +1.20% | Global, with early adoption in Asia-Pacific and Europe | Long term (≥ 4 years) |

| PC/Console transition from HDD to SSD | +0.90% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Enterprise pivot to cost-efficient QLC SSDs | +0.70% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| National on-shore NAND fab programs | +0.60% | United States, Europe, and select Asia-Pacific countries | Long term (≥ 4 years) |

| CXL-enabled computational storage adoption | +0.40% | North America and Europe data centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-center AI/ML storage surge

Hyperscale operators are redesigning storage hierarchies so that NVMe SSD pools sit closer to GPU clusters, sustaining multi-gigabyte-per-second throughput for retrieval-augmented generation workloads. Western Digital estimates cumulative demand of 19,000 petabytes of NAND by 2029 for 5G-enabled endpoints alone, underscoring flash’s role in bridging memory and cold-storage performance gaps.[1]Western Digital, “Driving AI Innovation: Western Digital Reveals New Solutions and Delivers Keynote at FMS 2024,” Western Digital Blog, Aug 5 2024, westerndigital.com Procurement roadmaps increasingly favor 30 TB to 100 TB enterprise drives, a shift visible in Samsung’s 128 TB BM1743 SSD showcased in 2024. The resulting pull-through effect accelerates layer-count innovation and controller-level compression techniques that sustain the NAND flash memory market momentum.

5G and massive-IoT device proliferation

Standalone 5G deployments unlock edge analytics use cases, smart factories, connected cars, and smart grids that mandate local non-volatile storage for real-time decision engines. Western Digital’s white paper anticipates a NOR-to-NAND crossover within industrial modules as capacities climb above 8 GB.[2]Western Digital, “Driving AI Innovation: Western Digital Reveals New Solutions and Delivers Keynote at FMS 2024,” Western Digital Blog, Aug 5 2024, westerndigital.com Semiconductor roadmaps now prioritize extended-temperature QLC die and automotive-qualified NVMe designs, broadening the NAND flash memory market footprint across transportation and infrastructure domains.

PC/Console transition from HDD to SSD

The consumer PC refresh cycle is synchronized with Microsoft-led minimum spec shifts that disallow HDD-only configurations for Windows 11 installs. In parallel, gaming consoles pivot to NVMe to support real-time texture streaming, as evidenced by Micron’s 3.6 GB/s G9 TLC platform adopted in next-gen devices.[3]Micron Technology, “Micron Announces Volume Production of Ninth-Generation NAND Flash Technology,” Micron Investor Relations, Jul 30 2024, micron.com Cost parity with 2.5-inch HDDs, expected by 2026, removes the last pricing barrier for mass solid-state adoption, giving the NAND flash memory market a predictable volume baseline.

Enterprise pivot to cost-efficient QLC SSDs

Data-lake, log-storage, and content-delivery workloads are 90% read-dominant, an ideal fit for QLC flash. Solidigm benchmarks reveal up to 61% TCO reductions versus TLC-based arrays, driving cloud platforms to roll out ≥ 64 TB QLC eSSDs for AI data-lakes.[4]Solidigm, “QLC NVMe SSDs Are Optimal for Modern Workloads,” Solidigm Technical Brief, Jul 31 2023, solidigm.com Controller advances such as adaptive write-caching reduce write-amplification, mitigating endurance anxiety and widening QLC’s serviceable-available-market inside the NAND flash memory market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Endurance limits of high-density cells | -0.80% | Global, particularly affecting enterprise segments | Medium term (2-4 years) |

| Pricing cyclicality and cap-ex burden | -1.20% | Global, with pronounced effects in Asia-Pacific | Short term (≤ 2 years) |

| Export-control induced equipment bottlenecks | -0.60% | China and allied countries, global supply chain impacts | Long term (≥ 4 years) |

| Sustainability scrutiny on high-layer fabs | -0.40% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Endurance limits of high-density cells

QLC’s 1,000–3,000 program/erase thresholds remain insufficient for log-heavy databases, forcing over-provisioning that erodes cost benefits. Hackaday notes the physics ceiling approaching as electron-trap wear accelerates in 300-layer stacks.[5]Hackaday, “The Flash Memory Lifespan Question: Why QLC May Be NAND Flash’s Swan Song,” Hackaday, Jul 8 2024, hackaday.com Although advanced error-correction and wear-leveling algorithms offset degradation, alternate memories such as PLC or cross-point remain on the horizon, tempering portions of the NAND flash memory market until longevity is proven.

Pricing cyclicality and cap-ex burden

Four suppliers control ≈ 95% of global output, giving production cuts outsized influence on spot-pricing. TrendForce recorded a deliberate 50% wafer reduction by Samsung in 2023 to arrest price free-fall; a rebound of more than 50% ensued within months.[6]TrendForce, “Market Anticipates a 50% Price Surge for NAND Flash in Short-Term,” TrendForce News, Dec 29 2023, trendforce.com Yet each greenfield fab now costs beyond USD 10 billion, elongating payback periods and creating capital-intensity headwinds that can slow node-transition investment across the NAND flash memory market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: QLC challenges TLC dominance

The NAND flash memory market size for TLC devices held a 63.58% market share with the strength of balanced endurance and cost. QLC, however, is accelerating at 6.35% CAGR as hyperscalers validate its 8-16× density advantage for AI data-lakes, which lifts the overall NAND flash memory market share allocated to QLC by 2031. Samsung’s 280-layer QLC prototype signals a roadmap to 16 TB single-sided M.2 drives, shrinking rack footprints while meeting throughput rules for inference clusters. Controller-level SLC-cache techniques and on-die ECC are narrowing the latency gap with TLC, encouraging broader workloads such as VOD libraries and backup repositories to migrate. TLC will retain primacy in write-intensive ERP and OLTP environments where its 10,000-plus cycle rating secures predictable quality-of-service.

In consumer notebooks, TLC’s favorable power profile sustains its install base, but falling QLC cost-per-bit is already pressuring mid-range SKUs. Micron’s sixth-gen QLC exhibits 34% lower read latency than first-gen samples, eroding the perceived performance divide. As firmware-defined endurance mitigation matures, OEMs will likely introduce tiered offerings where high-capacity SKUs employ QLC, while premium lines continue on advanced TLC nodes. This interplay keeps both technologies central to the NAND flash memory market over the forecast horizon.

By Structure: 3D NAND consolidation

The shift from planar to vertical stacking is virtually complete: 3D NAND commanded 86.85% of the NAND flash memory market share in 2025. Layer-count breakthroughs, SK Hynix’s commercial 321-layer TLC and Samsung’s 400-plus-layer V-NAND, signal confident scaling beyond the 500-layer watermark before decade-end. The economic logic is clear; vertical scaling adds capacity without shrinking cell size, sidestepping lithography constraints. 2D NAND survives in niche aerospace and defense modules where ultra-low-latency writes outweigh capacity.

Layer additions do stress interconnect resistance and cell-to-cell interference. To overcome this, Kioxia’s CMOS-bonded-array strategy decouples peripheral circuits, boosting I/O efficiency and improving yield in ultra-tall stacks. Samsung’s exploration of hafnia ferroelectrics for creamy-interface gates pursues a similar aim: maintain threshold-voltage margins even as stack height extends.

By Interface: PCIe/NVMe acceleration

PCIe/NVMe constituted 55.12% of revenue in 2025, upending SATA’s long-held dominance. The upgrade to PCIe 5.0 doubles bi-directional bandwidth, a necessity for AI inference servers where GPU clusters ingest tens of gigabytes per second. Samsung’s 5.6 GT/s I/O die exemplifies how controller-level link speeds keep pace with compute fabric demands. SATA remains cost-effective for Chromebook-class devices, yet most notebook OEMs are phasing in PCIe 4.0 and 5.0 sockets by 2026. Unified flash storage (UFS) and eMMC maintain resonance in smartphones and IoT modules owing to power and board-space constraints. Emerging auto-grade NVMe designs with functional-safety extensions are set to lift automotive penetration, bringing new verticals into the NAND flash memory market.

By Application: Enterprise SSD momentum

Smartphones delivered 41.05% of shipments in 2025, but their annual growth tops out in low single digits as average capacity stabilizes near 256 GB. Conversely, enterprise SSD units are climbing at a 7.42% CAGR through 2031, swelling the NAND flash memory market size contribution from data-center channels. Western Digital’s 64 TB QLC eSSD and Samsung’s 128 TB BM1743 demonstrate the density race shaping hyperscaler racks. Gaming notebooks and consoles bring high-margin growth in the client segment; Microsoft’s DirectStorage API places explicit pressure on sequential write speeds, galvanizing the NVMe upgrade pathway.

Industrial and automotive electronics trail in volume but yield higher ASPs per gigabyte. Phison’s assessment that Level-2+ ADAS stacks need up to 2 TB of on-board flash underscores upside potential. Here, stringent temperature, vibration, and functional-safety qualifications command premium pricing, carving out defensible niches inside the broader NAND flash memory market.

Geography Analysis

Asia-Pacific contributed 55.40% of sales in 2025, anchored by South Korea’s vertically-integrated champions and China’s colossal device assembly base. Samsung’s mass production of 9th-generation V-NAND (286 layers) and SK Hynix’s 321-layer TLC line affirm the region’s technology lead. Beijing’s domestic champion YMTC pushes 232-layer QLC nodes despite export-control constraints, illustrating indigenous capacity expansion that preserves Asia-Pacific’s outsized influence on the NAND flash memory market.

North America sits second on revenue league tables, propelled by cloud capital-expenditure intensity. The CHIPS and Science Act bankrolls Micron’s USD 125 billion state-side megafab roadmap, lifting U.S. advanced-memory self-sufficiency by 2035. Canada contributes controller-IP design talent, while Mexico scales module-level assembly lines under USMCA provisions, together reinforcing regional supply diversification.

Europe registers mid-single-digit share, constrained by limited memory wafer fabrication. Nonetheless, automotive and industrial OEMs in Germany and France generate robust demand for auto-grade NVMe modules. Sustainability directives such as the European Green Deal pivot buyers toward power-efficient PCIe 5.0 SSDs that lower rack energy density, a niche European fabs aim to capture through next-generation 3D NAND nodes with under-3 pJ/bit read energy footprints.

The Middle East and Africa present the highest growth rate at 8.21% CAGR. Saudi Arabia’s Vision 2030 underwrites wafer-to-back-end complexes around Riyadh, while Abu Dhabi’s sovereign investors explore joint-ventures with controller specialists to bootstrap a regional supply chain. Ample renewable-energy pipelines and attractive tax regimes draw packaging partners, setting the stage for localized production that boosts the NAND flash memory market penetration across GCC data hubs.

Regulatory Landscape

Trade, export-control, and industrial-policy actions shape NAND flash supply chains, since process equipment, advanced SSDs, and adjacent advanced-computing components move through tightly controlled cross-border channels. In the United States, the Bureau of Industry and Security (BIS) updated export controls via an Interim Final Rule published in December 2024, tightening controls on semiconductor manufacturing equipment and certain advanced memory parameters. This reinforced compliance requirements under the Export Administration Regulations (EAR) for manufacturers and tool vendors supporting leading-edge nodes.

In January 2026, U.S. policy signaled further tightening around advanced-computing commodities through a revised BIS license review policy for exports to China and Macau, increasing the compliance burden for global suppliers with data-center SSD and related high-performance computing portfolios. In parallel, the European Commission advanced semiconductor resilience through its Chips Act 2.0 proposal (COM(2026) 504) in June 2026, emphasizing ecosystem transparency and support mechanisms that can affect investment decisions for memory manufacturing and back-end capacity located in, or serving, the EU market.

Value Chain Analysis

The NAND flash memory value chain starts with specialty materials and wafer-processing equipment, moves into high-capital front-end fabrication (3D NAND stacking, etch, deposition), then covers test, assembly, and packaging, before reaching SSD and module integration and OEM or cloud qualification. Upstream manufacturing is highly concentrated among vertically integrated producers and alliances, including Samsung, SK hynix (including Solidigm), Micron, and the Kioxia-SanDisk partnership. Kioxia and SanDisk run joint-venture manufacturing in Japan, including facilities in Yokkaichi and Kitakami, supporting a large share of advanced 3D NAND output and process technology co-development.

Midstream and downstream steps increasingly depend on advanced packaging availability and controller and module integration capacity, with assembly commonly outsourced to overseas contract manufacturers and supported through OSAT ecosystems. Materials constraints have also become a practical limiter: BT substrates (and related low-CTE materials) have faced tightness amid overlapping demand from AI-chip packaging, which can in turn affect SSD controller and module throughput. Supplier actions in July 2026, including Kioxia sampling BiCS10 1Tb TLC from the Kitakami Plant Fab2 and the Kioxia-SanDisk start of BiCS10 production at the same site, underline how leading-edge node transitions now require coordinated readiness across wafers, packaging inputs, and qualification pipelines for enterprise and hyperscale customers.

Competitive Landscape

Market concentration is extreme: the top four vendors commanded major market share of global revenue, enabling scale advantages in lithography investments and controller co-design. Samsung’s high market share stems from early adoption of hybrid-bonded V-NAND that unlocks ≥ 400-layer roadmaps. SK Hynix is increasing its market share by leveraging Three-Plugs etch technology to optimize aspect ratios beyond 300 layers. Western Digital and Kioxia share a flash-foundry alliance that pools wafer output and R&D, although their on-again merger talks face opposition from SK Hynix on antitrust grounds.

Strategic moves now center on interface speed, leadership, and computational storage add-ons. Kioxia and SanDisk’s 4.8 Gb/s Toggle DDR 6.0 interface targets disaggregated GPU memory expansion. Samsung’s work on hafnia ferroelectric channel gates eyes sub-1 V program voltages, trimming both power and write-latency to meet AI inference timetables. Emerging entrants such as YMTC capture niche QLC cloud tenders, but export hurdles limit reach. Controller IP vendors, Silicon Motion, Phison, differentiate via AI-based error-prediction firmware that lifts endurance metrics, enabling ODMs to fine-tune SKUs for distinctive workloads.

NAND Flash Memory Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

KIOXIA Holdings Corporation

Western Digital Corporation

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is in the enterprise SSD segment, where hyperscale and AI infrastructure buyers are pulling higher capacities and faster interfaces into mainstream procurement. Company actions in July 2026 support this direction, with Samsung starting mass production of a PCIe 6.0 enterprise SSD (PM1763) for AI and HPC servers, and Kioxia and SanDisk starting production of 10th-generation BiCS10 3D flash at the Kitakami Plant Fab2. Together, these steps expand access to higher-density, performance-per-watt oriented NAND and SSD platforms for data-lake, model-training, and inference storage tiers that increasingly standardize on NVMe.

A second whitespace is supply-chain resilience and localized capability building across front-end capacity, advanced packaging, and qualification ecosystems. SK hynix announced a large investment plan for Cheongju that pairs new NAND fabrication capacity (M17) with an advanced packaging facility (P&T7), reflecting a dual-track scaling approach across wafer output and packaging throughput for data-center-grade products. At the same time, tighter export controls and evolving tariff and industrial-policy measures in the United States and Europe increase the value of compliant, regionally diversified manufacturing and back-end footprints. This creates room for equipment, materials, packaging, and controller firmware ecosystems that can meet performance targets (PCIe 5.0/6.0, high-capacity QLC/TLC SSDs) while staying within regulatory constraints.

Recent Industry Developments

- July 2026: Samsung Electronics began mass production of the PM1763 PCIe 6.0 enterprise SSD using 9th-generation V-NAND and a 4 nm controller for AI and HPC server environments. The rollout raises the performance benchmark for next-generation data-center storage platforms and accelerates qualification cycles among OEMs and hyperscalers adopting PCIe 6.0 roadmaps.

- June 2025: Kioxia rolled out CD9P Series PCIe 5.0 NVMe SSDs built on 8th-generation BiCS FLASH, improving performance-per-watt and doubling capacity to 61.44 TB. The release strengthened Kioxia's position in GPU-dense server deployments where storage efficiency and rack-level power limits factor into procurement decisions.

- July 2024: Micron announced volume production of its ninth-generation NAND flash technology. The node transition supported higher throughput and density scaling for client and embedded storage products, reinforcing the shift of PCs and consoles toward SSD-first configurations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from NAND flash memory products sold into end uses such as consumer electronics, PCs, enterprise storage, and other digital storage and compute hardware, valued in USD at the supplier level.

Scope exclusions: We exclude DRAM and other non-NAND memory, and we also exclude downstream hardware value that sits beyond the memory component itself.

Segmentation Overview

- By Type

- SLC (Single-Level Cell)

- MLC (Multi-Level Cell)

- TLC (Triple-Level Cell)

- QLC (Quad-Level Cell)

- By Structure

- 2D (Planar) NAND

- 3D NAND

- By Interface

- SATA

- PCIe / NVMe

- UFS / eMMC

- By Application

- Smartphones

- Solid-State Drives (PC and Console)

- Enterprise / Data-center SSD

- Memory Cards and USB Drives

- Industrial and Automotive Electronics

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base around NAND supply, demand, and pricing, since NAND is a cycle-driven market where revenue shifts quickly with bit output and average selling prices. We reviewed public materials such as USITC and UN Comtrade trade statistics, World Semiconductor Trade Statistics (WSTS) releases, OECD macro indicators, and standards and interface references from bodies such as JEDEC (for density and interface context).

After that, we cross-checked the story using company annual reports, earnings call transcripts, investor presentations, and credible press coverage about capacity adds, node transitions, and inventory actions. Select paid subscriptions for company financials and intelligence, news and financials, and patent databases were also used to reduce gaps when public disclosures were limited. The specific list of sources named here is illustrative, and many other public references were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions on pricing direction, wafer starts and utilization behavior, and demand pull from devices such as SSDs and smartphones. We spoke with a mix of memory ecosystem participants, including component suppliers, channel and distribution-linked roles, device and storage procurement stakeholders, and domain experts across APAC, EMEA, and the Americas, so regional cycle timing could be reconciled.

Survey feedback and follow-up calls were then used to confirm whether changes were temporary, driven by inventory correction, or structural, driven by 3D NAND migration and higher bits per device, and this helped us finalize the model ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 38% |

| Mid tier: 55% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 14% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where global NAND revenue is reconstructed from a demand pool view across major applications, and then aligned to industry supply signals, which keeps the totals consistent with cycle behavior. In practice, we tie the model to repeatable inputs such as NAND bit demand growth by application, device shipment trends (smartphones, PCs, and servers), SSD attach rates and average capacity per device, and observed price movement indicators for NAND.

Once the top level is stable, we corroborate it with selective bottom-up checks such as sampled ASP times estimated shipment volume for key form factors, plus channel checks on mix shifts between client and enterprise SSD demand. Where direct splits are not visible, shares are bridged using consistent proxy indicators such as interface migration (for example, PCIe-NVMe versus SATA) and the pace of 3D NAND adoption, and then reconciled back to the total.

Forecasting uses scenario analysis supported by expert consensus on two main levers, bit growth versus price trend, since the market can expand on volume even when pricing is soft. Assumptions are refreshed across the forecast window for capacity discipline, node transitions, and end-market recovery timing, and then the final curve is reviewed to ensure it matches plausible utilization and inventory paths.

Data Validation & Update Cycle

Validation is done in layers so the numbers do not rely on one data stream. Outputs are compared against independent signals such as WSTS category movement, public capacity and capex commentary, trade flow direction, and device shipment trajectories, and then any large variances are investigated before sign-off.

We also run simple anomaly checks on implied ASP and implied bits per device so the results remain realistic across up and down cycles. If a variance is material, the team re-contacts sources to confirm whether the change is timing-driven, mix-driven, or caused by a one-off shock. Reports are refreshed annually, with interim updates when major events occur, and a final pre-delivery review is completed so clients receive an updated view.

Mordor Intelligence's Nand Flash Memory Market Size Compared Against Other Published Estimates

Published market values for NAND flash memory often look different because firms do not always count the same revenue boundary, and they also handle the pricing cycle in different ways. Timing also matters, since a single quarter of ASP change can move the full-year value by several billion dollars.

The gap usually comes from what is included as NAND revenue and what is treated as adjacent semiconductor value, plus differences in how 3D NAND mix and interface shifts are translated into blended ASP. Some publishers lean on a single-year snapshot, while others apply aggressive recovery assumptions that lift the early years of the forecast.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 58.69 B (2026) | |

| Global Consultancy A | USD 64.40 B (2024) | The estimate is anchored to a vendor-share revenue snapshot for 2024, which can be hard to align with an application-led demand pool view, and it may not normalize inventory correction timing across client and enterprise SSD demand. |

| Industry Publisher B | USD 62.44 B (2024) | The published value uses a different year and a higher growth lens, and it can also reflect broader inclusion around device-led storage value when translating capacity additions into revenue without a clear cycle-adjusted ASP path. |

The table shows a spread that is largely explained by year selection and cycle timing, and then by what each model treats as in-scope NAND revenue. In Mordor Intelligence's model, the 2026 value is built by reconciling application demand indicators with supply and price signals, which helps avoid overstating revenue in a short-lived pricing upswing. With the scope stated clearly and the inputs traceable to repeatable metrics, the final figure is easier to audit and reuse for planning.

Key Questions Answered in the Report

How large is global demand for flash in AI data-centers by 2031?

Western Digital estimates cumulative consumption of about 19,000 petabytes, with enterprise SSD capacities moving toward the 100 TB class.

When will PCIe 5.0 SSDs become mainstream in notebooks?

OEM shipment roadmaps indicate most premium and mid-range laptops will standardize on PCIe 5.0 by 2026 as controller costs fall.

What share of shipments will QLC devices capture by 2031?

Forecasts in this report show QLC approaching one-fifth of total bits shipped, driven by hyperscale data-lake and archival workloads.

Which region is growing the fastest for memory-fab investment?

The Middle East and Africa, especially Saudi Arabia's Vision 2030 program, leads with an 8.21% CAGR to 2031.

How many layers can current 3D NAND process nodes reliably reach?

Commercial products are at 321-layers, and R&D samples have crossed the 400-layer threshold, setting a trajectory toward 1,000-layers before 2031.

Page last updated on: