Mutation Detection Kits In Genome Editing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

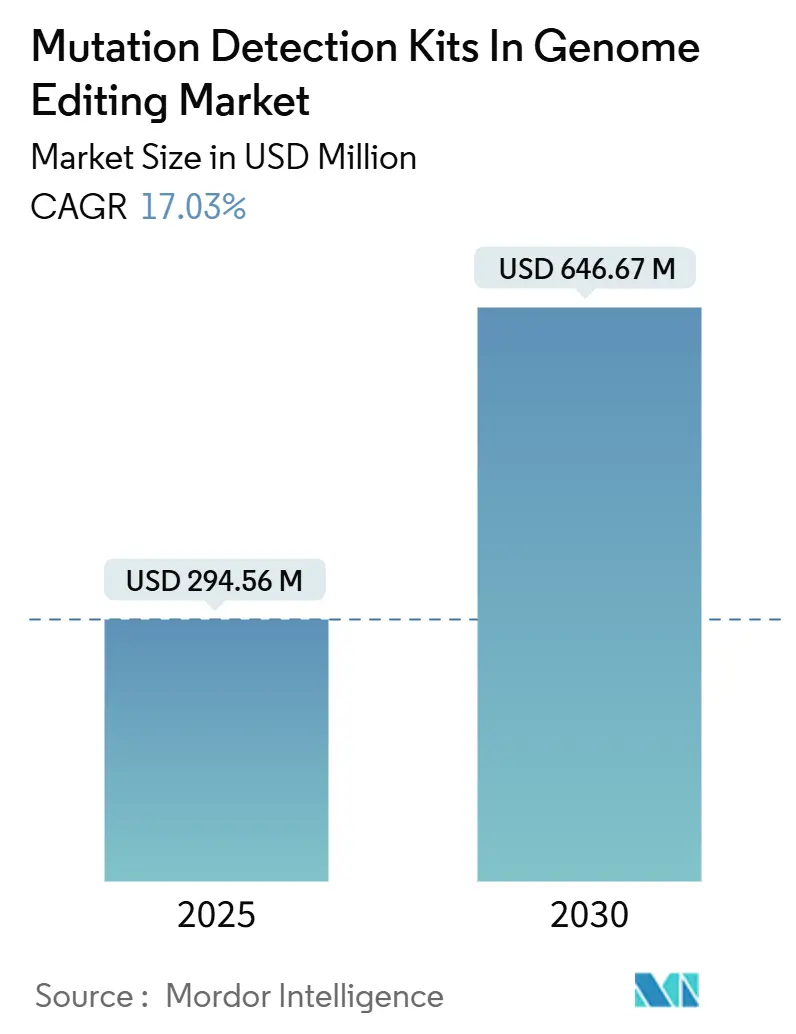

| Market Size (2025) | USD 294.56 Million |

| Market Size (2030) | USD 646.67 Million |

| Growth Rate (2025 - 2030) | 17.03% CAGR |

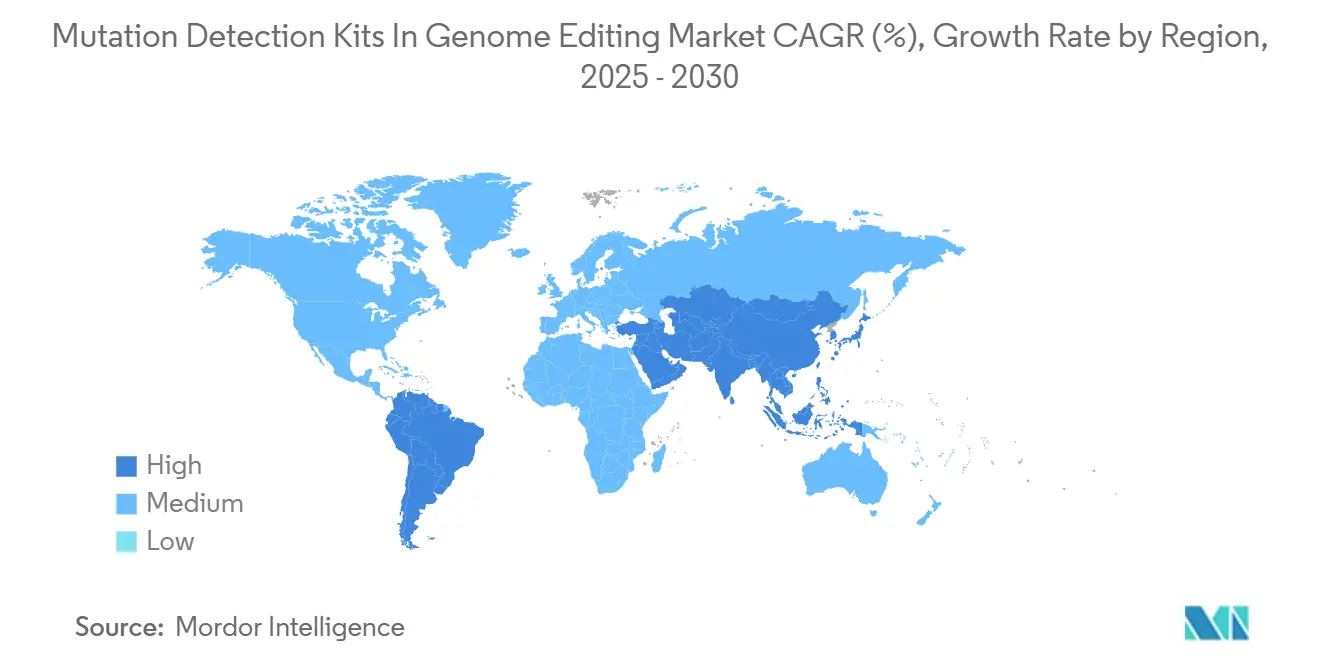

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mutation Detection Kits In Genome Editing Market Analysis by Mordor Intelligence

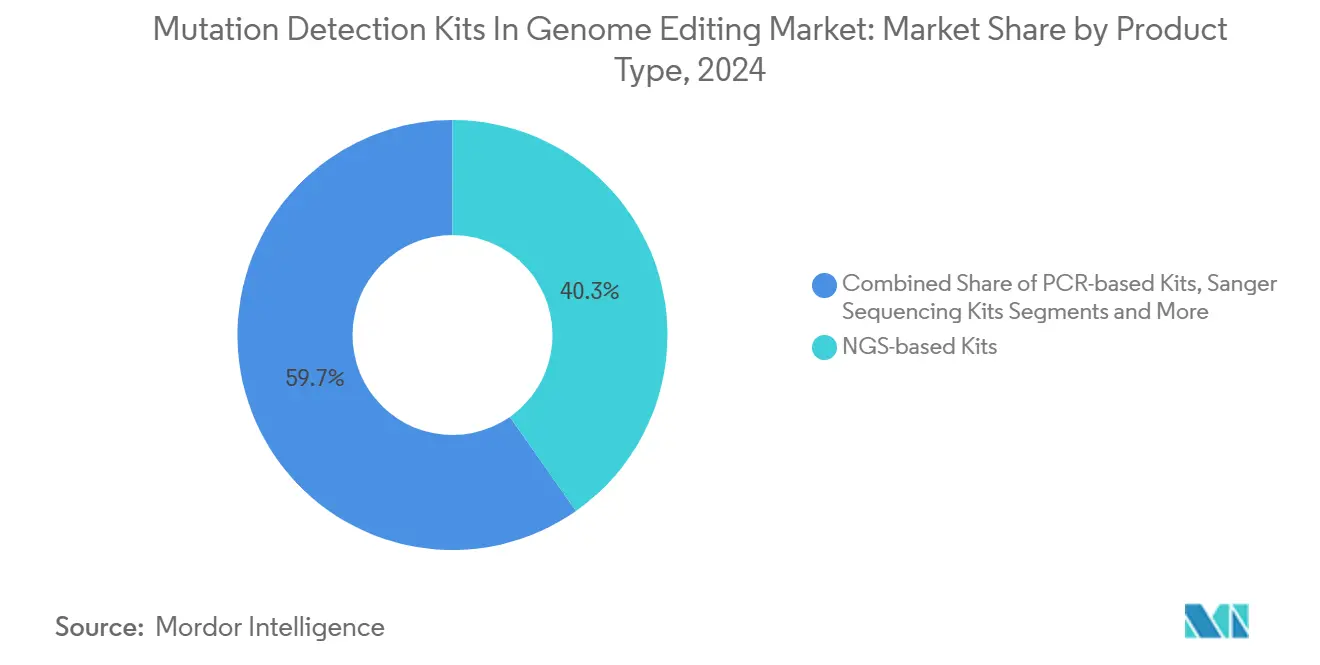

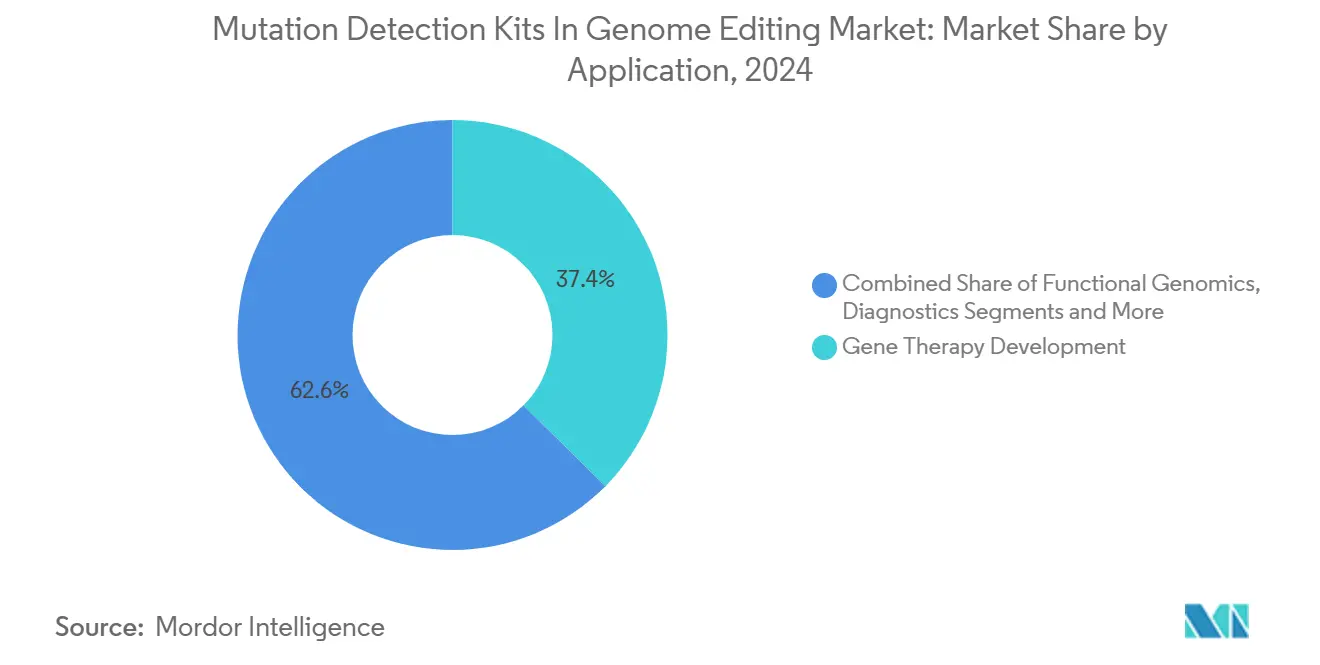

The mutation detection kits in genome editing market size stands at USD 294.56 million in 2025 and is forecast to reach USD 646.67 million by 2030, advancing at a 17.03% CAGR. This steep growth curve mirrors three concurrent shifts: lower next-generation sequencing (NGS) prices, clear regulatory pathways for analytical validation in gene therapy, and a widening clinical pipeline that relies on CRISPR technologies. NGS-based kits presently hold 40.27% share because they read complex edits at single-base resolution, while CRISPR/Cas-specific offerings grow fastest as therapeutic developers pivot to base- and prime-editing programs. Digital PCR (dPCR) platforms, though smaller today, post the highest adoption trajectory thanks to unrivaled sensitivity that picks up edits at 0.005% variant allele frequency. Gene-therapy work, rather than pure discovery, drives 37.41% of demand, and biopharma end users account for 43.74%, underscoring a commercial rather than academic pull. Regionally, North America commands 45.52% share on the strength of the FDA’s 2024 rules that standardize NGS tumor-profiling reviews and phase out enforcement discretion for laboratory-developed tests.[1]U.S. Food and Drug Administration, “FDA Takes Action Aimed at Helping to Ensure the Safety and Effectiveness of Laboratory Developed Tests,” FDA.gov

Key Report Takeaways

- By product type, NGS-based kits led with 40.27% of mutation detection kits in genome editing market share in 2024.

- By detection technology, NGS held a 45.71% share in the studied market and digital PCR is set to expand at a 21.44% CAGR through 2030.

- By application, gene therapy development held 37.41% of the mutation detection kits in genome editing market size in 2024 and carries a 20.68% CAGR outlook.

- By end user, biopharma and biotech companies controlled 43.74% share of the mutation detection kits in genome editing market in 2024.

- North America maintained 45.52% share of the mutation detection kits in genome editing market in 2024, while Asia-Pacific records a 19.31% CAGR to 2030.

Global Mutation Detection Kits In Genome Editing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Clinical Pipeline Of Gene-Edited Therapies | +3.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Increasing CRISPR/Cas9 Publication Volume | +2.8% | Global | Long term (≥ 4 years) |

| Declining Costs Of Next-Generation Sequencing (NGS) | +4.1% | Global | Short term (≤ 2 years) |

| Regulatory Push For Validated QC Assays In Gene Therapy | +2.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| CRISPR Base-Editing Assays Need Ultra-Sensitive Detection | +2.4% | Global, early adoption in North America | Short term (≤ 2 years) |

| Multiplexed Ddpcr Adoption In Ag-Biotech Field Trials | +1.7% | APAC core, spill-over to Americas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Clinical Pipeline of Gene-Edited Therapies

More than 40 CRISPR therapeutics are now in human trials, up sharply from 2024, and the first approvals—such as Casgevy for sickle cell disease—validate genome editing for mainstream care. Each investigational program needs orthogonal assays to confirm on-target precision and rule out off-target risks, turning high-sensitivity detection into a regulatory gatekeeper. Developers no longer settle for single-assay kits and instead adopt platform bundles that combine NGS breadth with dPCR depth. The volume of trials supports recurring kit purchases across dose-escalation, pivotal, and long-term follow-up stages. That predictable demand profile spurs kit makers to invest in tailored CRISPR validation chemistries that integrate seamlessly with biopharma quality-management systems.

Declining Costs of Next-Generation Sequencing

Whole-genome runs averaged USD 600 in 2024, down from USD 1,000 one year earlier, stripping economic barriers for routine validation in both human and agricultural studies.[2]Ahmed Samy, “Next-Generation Sequencing Technologies and Challenges,” Life, mdpi.com Lower per-sample cost means labs can sequence more clones per batch, widening statistical power while staying within budgets. Emerging-market players that once relied on targeted PCR now leapfrog directly to NGS, broadening the mutation detection kits in genome editing market footprint. Cost relief also fuels multiplex strategies, where one lane tracks multiple edit sites, cutting reagent use and analyst time. Suppliers respond with kit formats calibrated for rapid library prep and barcoding, further compressing per-assay spend.

Regulatory Push for Validated QC Assays in Gene Therapy

The FDA’s 2024 analytical-procedure guidance elevates validation stringency, and its final rule on laboratory-developed tests sets a four-year timetable for compliance. Small-mid biotech firms that once built bespoke assays now source commercial kits with full validation dossiers to satisfy auditors. Europe mirrors this stance by requiring methods that discriminate genome-edited crops from conventional cultivars, nudging ag-biotech toward ultra-sensitive detection workflows.[3]Alexandra Ribarits, “Detection Methods Fit-for-Purpose in Enforcement Control of Genetically Modified Plants Produced with Novel Genomic Techniques,” Agronomy, mdpi.com Kit makers that pre-package validation controls and software see uptake accelerate, as labs prefer turnkey solutions that pass regulatory muster.

CRISPR Base-Editing Assays Need Ultra-Sensitive Detection

Base and prime editors induce single-nucleotide swaps without double-strand breaks, so trace edits can hide in large wild-type backgrounds. Digital PCR reaches 0.005% variant allele detection, an order of magnitude beneath standard qPCR, becoming the default for clinical-grade base-editing validation. Labs also quantify edit:non-edit ratios for potency metrics, making absolute quantification indispensable. Because one therapeutic often edits multiple loci, demand rises for multiplex dPCR chips that sustain sensitivity across all targets in one reaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Premium NGS-Based Detection Kits | -2.1% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Lack Of Standardized Lab Protocols | -1.8% | Global, with regional variations | Medium term (2-4 years) |

| IP Fragmentation Around Mismatch-Cleavage Enzymes | -1.4% | Global, concentrated in North America & EU | Long term (≥ 4 years) |

| Supply-Chain Volatility For Recombinant Cas Nucleases | -1.9% | Global, with Asia-Pacific manufacturing concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium NGS-Based Detection Kits

Turnkey NGS validation kits often list above USD 10,000, a price that freezes out many academic labs and cash-constrained start-ups. High price tags reflect not only reagents but also bundled reference standards and software licenses needed for regulatory filings. The cost hurdle is especially acute in ag-biotech, where field trials span thousands of plants and budgets are tied to crop-cycle revenues. Until volume pricing or alternative chemistries emerge, uptake in lower-income regions stays modest, trimming global growth.

Lack of Standardized Lab Protocols

Protocol heterogeneity slows kit interchangeability across labs. One research center may employ unique extraction buffers or thermal-cycling profiles, making data incomparable with another center’s results. This variability drives repeat validation work, inflating timelines and deterring rapid kit adoption. Professional societies are drafting best-practice documents, yet regional buy-in varies, delaying convergence on a single workflow that would enable mass-market scaling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: NGS Platforms Drive Comprehensive Validation

NGS-based kits captured 40.27% of the mutation detection kits in the genome editing market share in 2024, reflecting regulators' preference for one-and-done assays that flag both intended edits and off-target events. The mutation detection kits in genome editing market size tied to this product cohort is projected to expand at a 17.03% CAGR, mirroring overall industry momentum. CRISPR/Cas-specific kits outpace all others with 21.35% CAGR because base- and prime-editing pipelines require purpose-built chemistries that standard PCR cannot address. PCR-based kits persist where budgets are tight and depth of analysis is secondary. Bio-Rad’s 2024 ddPLEX ESR1 launch illustrates how vendors bundle multiplexed dPCR inside user-friendly consumables, making high sensitivity attainable without NGS.

Product evolution tilts toward hybrid offerings that mix barcoded PCR amplification with NGS readouts or couple immuno-capture steps with fluorescence detection to streamline workflow. Sanger kits retain niche value when users need chain-termination confirmation of single targets. Miscellaneous assay kits, including high-resolution melt and mismatch cleavage, serve quick screen needs. As vendors align portfolios, overlap grows, yet a premium tier of fully validated, software-integrated NGS kits stays distinct for clinical developers.

By Detection Technology: Digital PCR Gains Ultra-Sensitive Applications

Next-generation sequencing owns 45.71% share of detection-technology revenue thanks to genome-wide reach, but digital PCR posts the fastest 21.44% CAGR underpinned by sub-0.1% allele sensitivity. The mutation detection kits in the genome editing market size derived from digital PCR will climb steadily as clinical protocols embrace absolute quantification for potency assays. High-resolution melt and mismatch cleavage remain attractive for early screening because they offer quick yes-or-no answers, though their sensitivity tops out earlier.

Technology choice increasingly maps to application nuance: NGS for exhaustive safety, dPCR for rare-event quantification, CRISPR-guided diagnostics for point-of-care speed. Rather than converge, the landscape fragments into specialized lanes. Vendors invest accordingly, pairing dPCR chips with cloud software that crunches droplet counts or bundling nanopore sequencers with rapid library preps. Users assemble workflows that splice multiple modalities, an approach expected to heighten overall spend per program.

By Application: Gene Therapy Development Dominates Validation Demand

Gene therapy development owned 37.41% of the mutation detection kits in genome editing market in 2024 and is projected at a 20.68% CAGR through 2030. That dominance hinges on strict regulator guidance that mandates orthogonal confirmation of edit fidelity before dosing patients. Functional genomics, though smaller, offers steady turnover as basic researchers characterize gene function; its orders are diffuse but frequent. Crop-trait development gains momentum where genome editing sidesteps GMO regulations, yet still needs off-target surveillance that basic PCR lacks.

Diagnostics applications, mainly liquid biopsy for oncology, inch upward as CRISPR detection reaches sub-femtomolar sensitivity. Drug discovery screens benefit from multiplex detection to track multiple edits in pooled CRISPR libraries. A long tail of niche uses—synthetic biology chassis validation and microbial cell factory monitoring—adds incremental but reliable revenue, rounding out application diversity.

By End-user: Biopharma Companies Lead Adoption Across All Segments

Biopharma and biotech enterprises controlled 43.74% of revenue in 2024 because they advance therapies that hinge on audit-ready validation packages. Their recurring batch-release testing supports multi-year kit subscriptions, cementing predictable cash flow for suppliers. Academic centers follow as the innovation engine feeding commercial pipelines, while contract research organizations act as volume multipliers by running assays for sponsor clients.

Agro-biotech firms take larger shares in Asia-Pacific owing to rice, maize, and soybean genome-editing programs that demand season-long monitoring. Clinical laboratories are an emergent buyer class as CRISPR-powered diagnostics progress toward FDA clearance. Remaining demand comes from government institutes and specialty service providers that fill analytical gaps. Each user archetype pursues kits that match its compliance burden and budget bandwidth, pushing vendors to tier product lines from research-grade to regulatory-grade.

Geography Analysis

North America held 45.52% of the mutation detection kits in genome editing market in 2024. The FDA’s fast-track review for NGS tumor profiling and its phased oversight of laboratory-developed tests create predictable compliance milestones that encourage up-front investment in validated kits. Concentrated clusters in Boston, the Bay Area, and San Diego shorten supply lines and magnify ecosystem spillovers, while Canada’s Genome Innovation Network supplies collaborative grant funding that lowers purchase barriers for academic labs.

Europe ranks second with a strong pharmaceutical base and collaborative research networks. Germany and the United Kingdom spearhead adoption, leveraging EU-wide Horizon funding that demands standardized validation metrics. Regulatory nuance adds complexity: the bloc requires assays that can differentiate edited plants from conventionally bred crops, nudging demand toward ultra-sensitive kits that satisfy both medical and ag-biosafety reviewers.

Asia-Pacific is the fastest-growing region at 19.31% CAGR. China funds national precision-medicine initiatives and fast-tracks agricultural biotech permits, leading volume growth. Japan layers advanced instrumentation know-how atop an aging-population imperative for gene therapies, while India’s National Biopharma Mission channels grants toward CRISPR crop trials. Australia and South Korea round out the region with regulatory clarity and translational-research hubs that feed regional demand for premium kits.

Competitive Landscape

The market shows moderate fragmentation. Legacy life-science giants—Thermo Fisher Scientific, New England Biolabs, Integrated DNA Technologies—bundle detection kits within expansive reagent portfolios, leveraging global distribution and ISO-compliant quality management. Specialized players such as CRISPR Therapeutics or Mammoth Biosciences introduce proprietary chemistries tailored to novel editors, and their partnerships with big pharma speed validation across clinical pipelines.

Competitive strategy gravitates toward vertical integration. Large firms acquire niche assay developers to ensure soup-to-nuts offerings, while midsize suppliers license IP aggressively to avoid royalty stacking. Demand for fully validated solutions shifts the battleground from raw assay performance to delivered regulatory readiness, and vendors with embedded bioinformatics suites gain an edge.

Supply-chain resilience is a rising differentiator. Firms that dual-source recombinant nucleases or localize enzyme production in multiple continents win purchase orders during shortage cycles. IP stability also sways buying decisions because customers seek freedom-to-operate confidence before locking into multi-year kit contracts. Looking ahead, white-space opportunities cluster around field-deployable multiplex dPCR for crop trials and sub-0.01% allele detection kits for prime editing.

Mutation Detection Kits In Genome Editing Industry Leaders

Thermo Fisher Scientific

Integrated DNA Technologies (IDT)

Qiagen

New England Biolabs

Agilent Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Lantheus Holdings closed acquisitions of Evergreen Theragnostics and Life Molecular Imaging, broadening neuroendocrine and Alzheimer’s diagnostic offerings that depend on high-precision mutation analysis.

- November 2024: Roche agreed to acquire Poseida Therapeutics for USD 1.5 billion, expanding gene therapy assets and elevating demand for specialized detection platforms suited to complex edits.

- April 2024: Regeneron and Mammoth Biosciences formed a CRISPR collaboration combining Regeneron’s clinical reach with Mammoth’s novel enzyme systems, setting the stage for bespoke validation kit development.

Global Mutation Detection Kits In Genome Editing Market Report Scope

| PCR-based Kits |

| NGS-based Kits |

| CRISPR/Cas-specific Kits |

| Sanger Sequencing Kits |

| Other Assay Kits |

| Mismatch Cleavage Assay |

| High-Resolution Melting (HRM) |

| Digital PCR |

| Next-Generation Sequencing |

| Other Technologies |

| Gene Therapy Development |

| Functional Genomics |

| Crop Trait Development |

| Drug Discovery & Screening |

| Diagnostics |

| Other Applications |

| Biopharma & Biotech Companies |

| Academic & Research Institutes |

| Contract Research Organizations |

| Agro-biotech Companies |

| Clinical Laboratories |

| Other End-users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | PCR-based Kits | |

| NGS-based Kits | ||

| CRISPR/Cas-specific Kits | ||

| Sanger Sequencing Kits | ||

| Other Assay Kits | ||

| By Detection Technology | Mismatch Cleavage Assay | |

| High-Resolution Melting (HRM) | ||

| Digital PCR | ||

| Next-Generation Sequencing | ||

| Other Technologies | ||

| By Application | Gene Therapy Development | |

| Functional Genomics | ||

| Crop Trait Development | ||

| Drug Discovery & Screening | ||

| Diagnostics | ||

| Other Applications | ||

| By End-user | Biopharma & Biotech Companies | |

| Academic & Research Institutes | ||

| Contract Research Organizations | ||

| Agro-biotech Companies | ||

| Clinical Laboratories | ||

| Other End-users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the mutation detection kits in genome editing market in 2025?

The mutation detection kits in genome editing market size is USD 294.56 million in 2025.

What CAGR is expected for mutation detection kits through 2030?

Revenue is set to advance at a 17.03% CAGR between 2025 and 2030.

Which product category currently leads sales?

NGS-based kits lead with 40.27% share of 2024 revenue.

Which detection technology is growing fastest?

Digital PCR platforms record the highest 21.44% CAGR due to ultra-sensitivity requirements.

Which region is expanding quickest?

Asia-Pacific posts a 19.31% CAGR, driven by government-backed precision-medicine and ag-biotech programs.

Who are the primary end users?

Biopharma and biotech firms account for 43.74% of 2024 demand, followed by academic institutes and CROs.

Page last updated on: