Genome Editing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

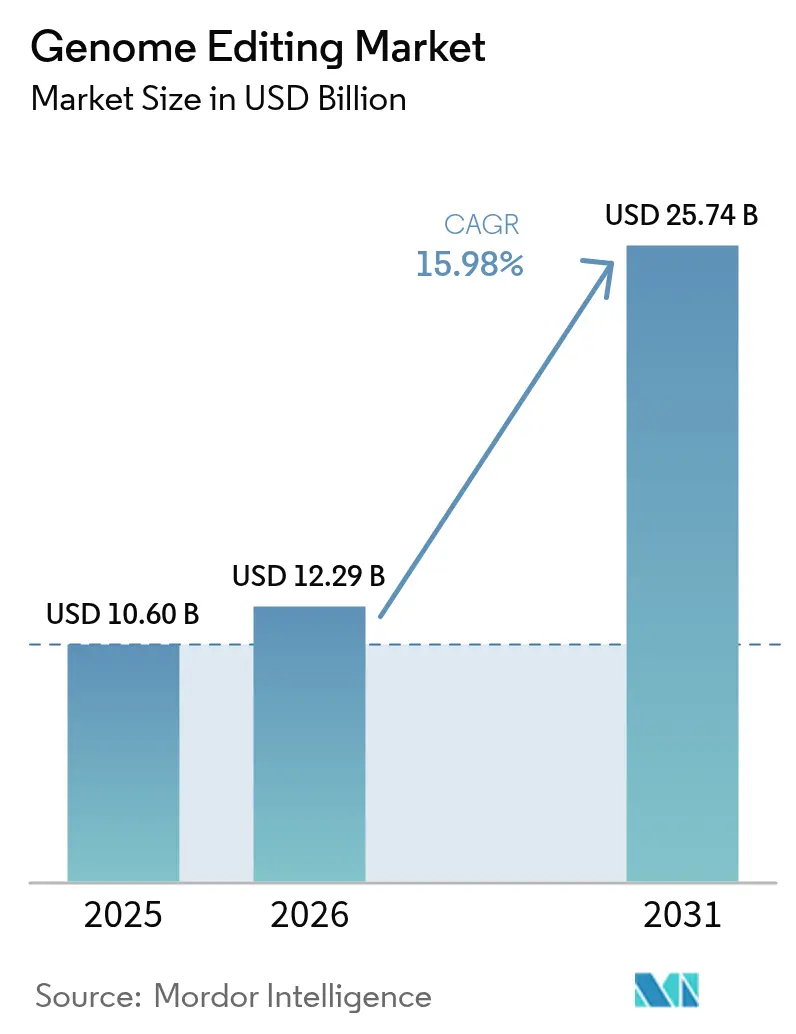

| Market Size (2026) | USD 12.29 Billion |

| Market Size (2031) | USD 25.74 Billion |

| Growth Rate (2026 - 2031) | 15.98% CAGR |

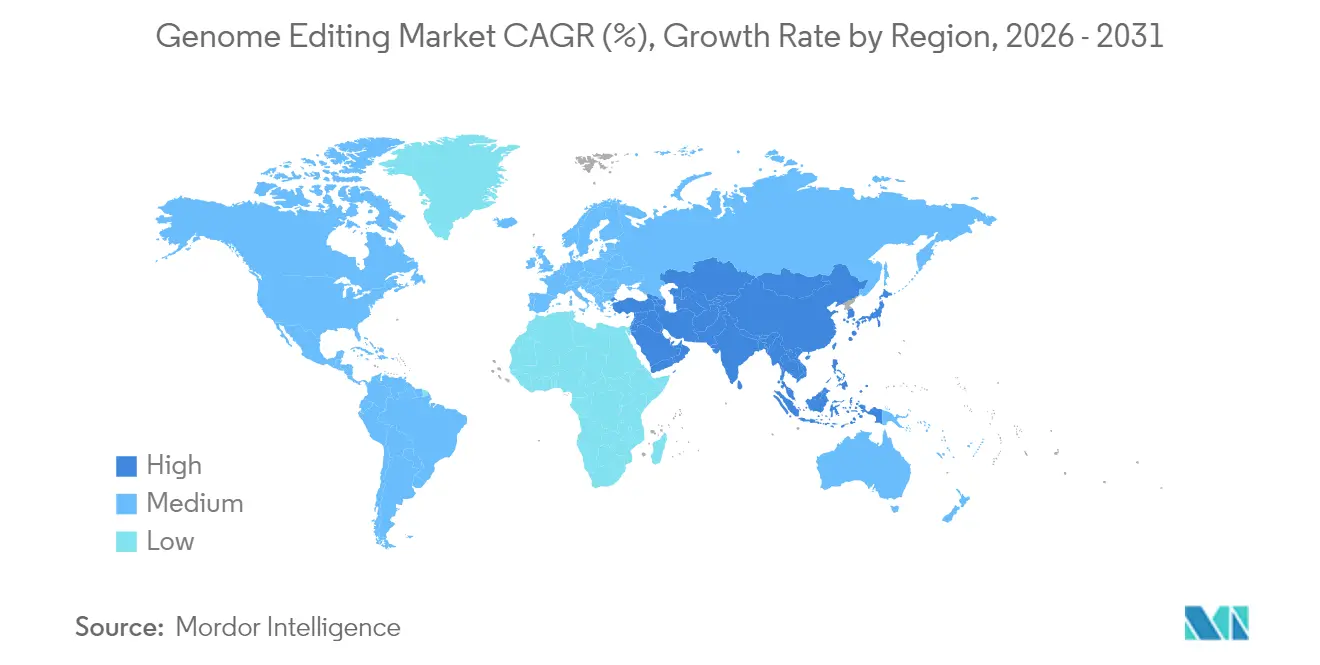

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Genome Editing Market Analysis by Mordor Intelligence

The Genome Editing Market size was valued at USD 10.60 billion in 2025 and estimated to grow from USD 12.29 billion in 2026 to reach USD 25.74 billion by 2031, at a CAGR of 15.98% during the forecast period (2026-2031).

Clinical validation of CRISPR-Cas9, rising demand for climate-resilient crops, and abundant venture capital all converge to accelerate commercial adoption. Growing regulatory confidence is evident in the wave of review designations granted to CRISPR therapeutics, while agricultural regulators in several countries now treat many gene-edited plants as conventionally bred. Competitive strategies focus on expanding GMP-compliant capacity, integrating AI into nuclease design, and signing platform licensing deals that lock in intellectual-property advantages. Intensifying collaboration between large pharmaceutical companies and agile start-ups broadens the therapeutic pipeline and speeds time-to-market, even as manufacturing scale-up, trade policy misalignment, and skilled-labor shortages temper the outlook.

Key Report Takeaways

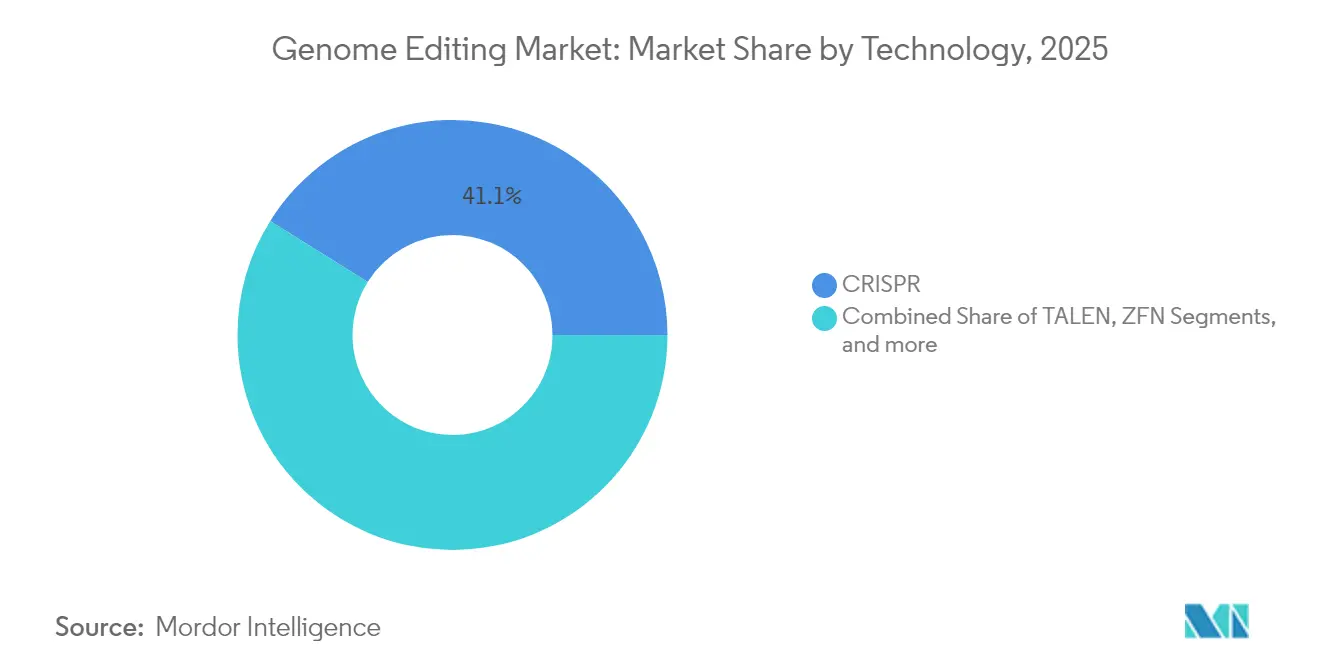

- By technology, CRISPR platforms led with 41.10% of genome editing market share in 2025; TALEN is projected to advance at a 19.49% CAGR to 2031.

- By delivery method, viral vectors accounted for 46.10% of revenue in 2025, while non-viral physical delivery is forecast to expand at 16.21% CAGR through 2031.

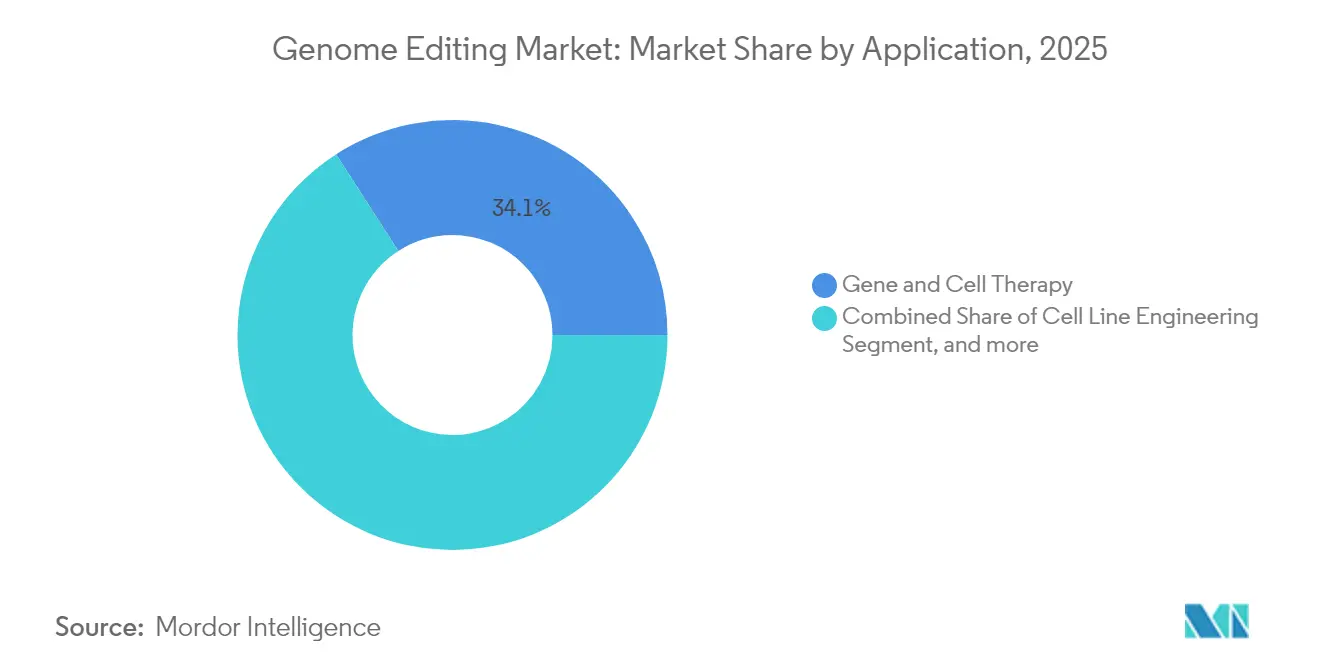

- By application, gene and cell therapy held 34.10% of the genome editing market size in 2025, whereas diagnostics and synthetic biology post the fastest 16.78% CAGR from 2026-2031.

- By end user, pharmaceutical and biotechnology companies captured a 51.85% share of the genome editing market in 2025 and are growing at a 16.65% CAGR to 2031.

- By region, North America retained 40.80% revenue share in 2025; Asia-Pacific is set to grow at a 19.75% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Genome Editing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of CRISPR-Cas Systems in Clinical Trials | +3.2% | Global, with North America & EU leading | Medium term (2-4 years) |

| Expanding Agricultural Biotechnology Demand for Climate-Resilient Crops | +2.8% | Global, with APAC & Latin America core | Long term (≥ 4 years) |

| Surging VC & IPO Funding for Gene-Editing Start-Ups | +2.1% | North America & EU primary, APAC emerging | Short term (≤ 2 years) |

| Mainstreaming In-Vivo Gene-Editing Therapeutics for Rare Diseases | +2.5% | Global, with regulatory advantages in US | Medium term (2-4 years) |

| Automation & AI-Assisted High-Throughput Screening Platforms | +1.8% | Global, concentrated in biotech hubs | Medium term (2-4 years) |

| Government Bio-Economy Roadmaps in Emerging Countries | +1.4% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of CRISPR-Cas Systems in Clinical Trials

FDA approval of the first CRISPR therapy unlocked broader clinical exploration, enabling multi-arm umbrella trials that cut development cycles by up to two years.[1]US Food and Drug Administration, “FDA Approves First CRISPR-Based Therapy,” fda.gov Positive read-outs from hematology, ophthalmology, and solid-tumor studies underscore platform versatility and attract sustained capital inflows.[2]Alexis Rappaport, “CRISPR Applications Expand Beyond Monogenic Disorders,” nature.com Universities and biotech firms are scaling CRISPR-TIL protocols that achieved complete responses in gastrointestinal cancers, moving beyond monogenic indications.

Expanding Agricultural Biotechnology Demand for Climate-Resilient Crops

Genome-edited rice, drought-tolerant corn, and heat-resistant livestock exemplify solutions that mitigate climate shocks while maintaining yield.[3]US Department of Agriculture, “Biotechnology Risk Assessment Research Grants,” usda.gov Regulatory exemptions in 16 jurisdictions where no foreign DNA persists accelerate commercialization, allowing small breeders to enter the genome editing market without onerous GMO hurdles. Public–private programs channel CRISPR tools toward nutritional fortification in staple crops, broadening market opportunities in developing regions.

Surging VC & IPO Funding for Gene-Editing Start-Ups

Despite a cyclical dip in 2024, high-quality platforms still close nine-figure rounds and craft alliances that blend big-pharma capital with nimble R&D. Strategic investments funnel resources into ultracompact CRISPR enzymes, AI-guided design suites, and programmable integrases, reinforcing technology pipelines.

Mainstreaming In-Vivo Gene-Editing Therapeutics for Rare Diseases

Single-dose in vivo programs deliver durable protein knockdown, with lipid nanoparticle systems achieving organ-specific editing beyond the liver. FDA guidance prioritizes expedited review for rare-disease candidates, prompting sponsors to stack filing queues with in-vivo products slated for launch later in the decade.

Restraints Impact Analysis of Genome Editing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain Long-Term Off-Target Safety Profile in Humans | -2.3% | Global, with stricter EU oversight | Long term (≥ 4 years) |

| High CAPEX For GMP-Compliant Gene-Editing Manufacturing Suites | -1.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Cross-Border Regulatory Fragmentation for Edited Seeds | -1.6% | Global trade, EU-US divergence critical | Medium term (2-4 years) |

| Talent Shortage in Advanced Molecular Biology Skillsets | -1.2% | Global, concentrated in biotech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uncertain Long-Term Off-Target Safety Profile in Humans

Ultra-deep sequencing continues to reveal hundreds of potential off-target sites, prompting regulators to demand expanded biodistribution and durability studies before late-stage trials can proceed. High-fidelity Cas variants and prime-editing approaches lessen risk, but limited long-term human data keep post-marketing surveillance requirements stringent, especially in the EU.

High CAPEX For GMP-Compliant Gene-Editing Manufacturing Suites

Green-field plants require USD 200-500 million and specialist clean-room designs. Although podular construction reduces overrun risk, capital intensity limits entry by smaller firms and fuels consolidation around CDMOs with existing footprints. Automation lowers per-batch cost yet demands skilled operators in short supply, extending time-to-capacity ramp-up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Genome Editing Market Segment Analysis

By Technology:

CRISPR Leads While TALEN AcceleratesCRISPR delivered 41.10% genome editing market share in 2025, but TALEN exhibits a 19.49% CAGR that is reshaping the competitive mix. Evolving AI tools dramatically cut guide-RNA optimization cycles and expand the nuclease design space, spawning derivatives such as Open-CRISPR with novel sequence homology. Base- and prime-editing modalities gain traction as safety-oriented alternatives and may carve dedicated submarkets, especially in indication areas sensitive to double-strand break risks.

At the same time, zinc finger nucleases preserve niches in ultra-specific applications where intellectual-property freedom outweighs throughput. Meganucleases and oligonucleotide-directed mutagenesis round out the toolkit for industrial synthetic-biology workflows. Consequently, platform providers increasingly bundle editing modalities with predictive AI software and screening libraries, anchoring broader solution sales across therapeutic, agricultural, and industrial customers.

By Delivery Method:

Viral Vectors Dominate, Non-Viral Innovation SurgesViral vectors generated 46.10% of 2025 revenue through predictable transduction efficiency and a well-understood regulatory path, ensuring continued demand in high-value ex-vivo therapies. Yet non-viral physical approaches will expand at 16.21% CAGR as electroporation, microfluidic squeezing, and tissue-selective lipid nanoparticles solve the immunogenicity and payload-size limits inherent to viral systems.

Robotic microinjection platforms quadruple embryo-editing throughput, spurring agricultural breeders to adopt non-viral protocols at scale. Ribonucleoprotein complexes deliver transient editing that fades before adaptive immunity triggers, appealing to chronic-disease programs requiring repeat dosing. Chemical carriers remain relevant for screening and research but cede ground in clinical settings to more efficient physical tools.

By Application:

Therapeutics Still Command Yet Diagnostics AccelerateGene and cell therapy maintained 34.10% of 2025 revenue and anchor most near-term commercial launches. Diagnostics, however, will post a 16.78% CAGR as CRISPR-Cas13-based RNA detection platforms enter infectious-disease and oncology screening markets. Agricultural crop engineering continues to expand as climate policy encourages resilient varieties, though regulatory fragmentation slows cross-border trade. High-throughput drug discovery and functional-genomics screens draw steady capital investment, leveraging automated CRISPR libraries to elucidate disease mechanisms.

Technological convergence with single-cell multi-omics refines disease-pathway mapping, allowing therapeutics developers to stratify patients more accurately and boost clinical-trial success rates. Synthetic-biology initiatives use genome editing to elevate lipid, enzyme, or nutraceutical yields, underpinning next-generation bio-manufacturing ecosystems.

By End User:

Pharma Leadership Coupled with Academic PioneeringPharmaceutical and biotechnology enterprises held 51.85% of the 2025 demand and are forecast to expand at a 16.65% CAGR as precision-medicine pipelines multiply. The genome editing industry benefits from academic institutes that seed fundamental discoveries and spin out fresh ventures. CROs capture workflow outsourcing from firms that lack internal editing expertise, while plant-breeding companies scale up to meet climate-resilience targets.

Commercial rollout of treatment centers for approved CRISPR therapies illustrates the logistical lift required to translate innovation into patient access. Big-pharma partnerships inject capital and global reach into emerging platforms, exemplified by nine-figure deals targeting cardiovascular and metabolic disorders. Workforce development programs attempt to close the molecular-biology talent gap, yet tight labor markets persist in biotech hubs.

Geography Analysis

North America Genome Editing Market

North America captured 40.80% of 2025 revenue, anchored by deep venture funding, leading clinical-trial infrastructure, and supportive FDA policies. Federal bio-economy initiatives allocate multi-billion-dollar budgets to genomics R&D and advanced manufacturing, reinforcing domestic supply chains. Nonetheless, construction-cost inflation and scarcity of GMP personnel place upward pressure on operating expenses for new facilities.

Europe Genome Editing Market

Europe combines world-class academic research with fragmented regulations that slow agricultural commercialization. The EU’s GMO designation for most gene-edited crops conflicts with more permissive stances in the United Kingdom and Switzerland, prompting calls for policy harmonization. Meanwhile, biotech investment funds and Horizon Europe grants channel resources into therapeutic programs, sustaining R&D despite trade-policy uncertainty.

APAC Genome Editing Market

Asia-Pacific is the fastest-growing region at 19.75% CAGR, propelled by Chinese industrial-policy incentives, Japanese regulatory streamlining for genome-edited foods, and Australia’s RNA Blueprint aiming for an USD 8 billion contribution to GDP. India’s risk-tiered guidelines create an expedited path for low-risk edits, catalyzing start-up formation. Technology-transfer limits and patent-pool negotiations will shape the trajectory of foreign market entrants.

Regulatory Landscape

Genome editing regulation continues to tighten around safety characterization for human applications while differentiating rules for agricultural products across major jurisdictions. In the United States, the FDA has maintained its January 2024 final guidance on human gene therapy products incorporating human genome editing as a core reference for CMC, nonclinical, and clinical expectations, and in April 2026 it issued a draft guidance focused on safety assessment of genome editing in human gene therapy products using next-generation sequencing (NGS), signaling a greater emphasis on standardized, high-resolution off-target and genomic integrity evaluation.

In Europe, Regulation (EU) 2026/1388 (adopted June 17, 2026) establishes a dedicated framework for plants obtained by certain new genomic techniques (NGTs) and their products, creating a clearer pathway for some gene-edited crops while retaining health and environmental safeguards. In China, a statutory framework for biomedical technologies, including stem cells and gene editing, took effect on May 1, 2026, while agricultural policy direction has also elevated gene editing as a core technology under the State Council's modernization plan, reinforcing the need for distinct compliance strategies between therapeutic and agricultural genome editing programs.

Competitive Landscape

The competitive field is moderately fragmented. Thermo Fisher Scientific leverages its Life Sciences Solutions unit, which accounts for a significant share of corporate revenue, to supply reagents and instruments across research, diagnostics, and bioprocessing segments. Merck KGaA’s Sigma-Aldrich complements similar tool portfolios and maintains strong customer lock-in through consumable subscriptions.

Platform innovators are reshaping market boundaries. CRISPR Therapeutics transitioned to revenue generation following CASGEVY’s launch and now advances cardiovascular and oncology assets while holding USD 1.86 billion in cash. Intellia Therapeutics prioritizes in vivo editing and expects its cash runway to extend beyond 2027 after a 27% workforce realignment. Partnering activity intensifies, typified by Regeneron’s alliance with Mammoth Biosciences, which combines ultracompact nucleases with antibody-targeting. Patent portfolios remain decisive; access to foundational CRISPR IP offers incumbents defensive moats that smaller entrants must navigate via cross-licensing or novel enzyme discovery.

Midsized CDMOs diversify into cell-and-gene therapy suites, but high CAPEX and variable utilization have already sparked consolidation. Select service providers experiment with continuous-manufacturing lines that could halve per-dose costs once regulatory acceptance solidifies

Genome Editing Industry Leaders

GenScript USA Inc.

Integrated DNA Technologies Inc.

New England Biolabs Inc.

Sangamo Biosciences Inc.

Thermo Fisher Scientific Inc.

GenScript Biotech Corporation

- *Disclaimer: Major Players sorted in no particular order

Genome Editing Market Companies Covered in this Report

- Thermo Fisher Scientific

- Merck

- CRISPR Therapeutics AG

- Editas Medicine

- Horizon Discovery

- Intellia Therapeutics Inc.

- Beam Therapeutics Inc.

- Sangamo Therapeutics

- Genscript

- Synthego Corporation

- Takara Bio

- Integrated DNA Technologies

- Lonza Group

- New England Biolabs

- OriGene Technologies

- Caribou Biosciences Inc.

- Bluebird Bio

- Bio-Rad Laboratories

- Agilent Technologies

- QIAGEN

Market Opportunities and Future Outlook

Regulatory clarification is creating near-term whitespace in therapeutic development workflows and agricultural commercialization, with direct implications for tools, services, and delivery-vector demand. The FDA's April 2026 draft guidance on NGS-based safety assessment for genome-edited human gene therapy products, together with its June 2026 draft guidance on leveraging prior knowledge for genome-editing gene therapies, supports more structured, repeatable evidence packages across programs. That, in turn, favors providers of off-target analytics, standardized assay kits, reference materials, and compliant bioinformatics pipelines that reduce friction from discovery through IND-enabling studies.

In agriculture, adoption of Regulation (EU) 2026/1388 (June 2026) establishes a defined framework for NGT plants and products, expanding the addressable market for genome-editing inputs in European crop engineering and associated trait-validation services, particularly for edits that avoid foreign DNA. On the clinical side, the market is also seeing momentum toward more complex cell engineering and solid-tumor applications, illustrated by Chinese regulatory approval in July 2026 for CARsgen Therapeutics' satri-cel for gastric cancer. This progress lifts requirements for high-quality editing reagents, safety testing including NGS-based assessment, and scalable manufacturing partnerships for customized or small-batch therapeutic products.

Recent Industry Developments in Genome Editing Market

- July 2026: CARsgen Therapeutics received Chinese regulatory approval for satri-cel (satricabtagene autoleucel) for gastric cancer, cited as the first CAR T approval for a solid tumor in that market. The milestone expands the commercial proof points for edited or engineered cell therapies beyond hematologic cancers and increases demand for clinical-grade genome-editing inputs and analytical release testing aligned to evolving safety expectations.

- July 2025: Integrated DNA Technologies announced an expansion of its CRISPR translational research portfolio, including additions such as Alt-R HDR Enhancer Protein and Cas9 mRNA. Broadening reagent and workflow options strengthens vendor lock-in for preclinical-to-translational users and supports faster iteration cycles for teams optimizing editing efficiency and delivery formats.

- December 2024: GenScript Biotech partnered with Base Therapeutics to support the NK510 base-edited NK cell therapy program, supplying cGMP sgRNA and its CytoSinct cell isolation technology after the program received FDA IND clearance. This underscores increasing reliance on specialized suppliers that can combine GMP-grade nucleic acids with enabling cell-processing technologies for IND-stage genome editing therapeutics.

Genome Editing Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues generated from genome editing tools and workflows that enable targeted DNA or RNA changes. It includes key reagents, instruments, delivery systems, and related services used in research and applied settings.

Scope exclusions: We exclude traditional sequencing consumables and stand-alone gene-synthesis orders when they are not directly tied to an editing workflow.

Segments Covered in This Report

- By Technology

- Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR)

- Transcription Activator-Like Effector Nuclease (TALEN)

- Zinc Finger Nuclease (ZFN)

- Meganucleases

- Oligonucleotide-directed Mutagenesis (ODM)

- Other Technologies

- By Delivery Method

- Viral Vectors

- Non-viral Physical Methods

- Non-viral Chemical Methods

- By Application

- Cell Line Engineering

- Gene & Cell Therapy

- Drug Discovery & Functional Genomics

- Agricultural Crop Engineering

- Diagnostics & Synthetic Biology

- By End User

- Pharmaceutical & Biotechnology Companies

- Academic & Government Research Institutes

- Contract Research Organizations

- Agriculture & Food Companies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts from measurable signals that are difficult to dispute, then converts those signals into revenue using realistic usage and pricing logic. We typically pull reference statistics from public sources such as National Institutes of Health funding databases, US Food and Drug Administration releases, European Medicines Agency updates, and clinical trial registries such as ClinicalTrials.gov.

To keep the work grounded, we also review patents and peer-reviewed journals to see which lab protocols are turning into repeatable products. We then use company filings, investor decks, and association websites to map commercial activity. Where needed, paid subscriptions are used only for company financials and intelligence, patent lookups, and shipment-level trade views for select inputs. This desk list is not exhaustive, and we also used other public and paid sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test desk assumptions on what is counted as genome editing revenue, how pricing is moving, and where adoption is accelerating versus staying in early research. We spoke with tool suppliers, service providers, and end users such as biopharma teams and academic labs across major regions, so gaps in public data could be closed and key variables could be triangulated with stated buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 52% |

| Mid tier: 55% | Functional/Unit leaders: 36% | EMEA: 29% |

| Smaller Players: 16% | Managers: 50% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is first constructed using a top-down logic where research intensity and clinical translation signals are converted into an addressable demand pool, then tied to spend per workflow. To keep the structure honest, we corroborate it with selective bottom-up approximations, such as sampled product pricing multiplied by estimated unit volumes for core consumables, plus channel checks on service run rates. Totals are adjusted only when several checks point in the same direction.

Inputs used in the model include the number and pace of gene editing related clinical trials, regulatory milestones for genome editing therapies, public research funding direction, patent filing momentum, and practical adoption indicators such as installed-base growth of relevant lab instruments and typical reagent consumption per experiment. Forecasting is done mainly through scenario analysis supported by trend smoothing, where near-term demand is anchored to observable pipelines and funding. For longer-term curves, we moderate outcomes based on expert views on safety, off-target concerns, and manufacturing readiness. When bottom-up visibility is patchy for smaller suppliers, we handle gaps with conservative penetration and price bands, then recheck through primary calls.

Data Validation & Update Cycle

Validation is done by comparing modeled revenue with independent signals such as trial activity, funding direction, and observable commercial launches, then drilling into any large variances until the cause is clear. If an assumption change moves a total too far, the team re-contacts experts and revisits the source trail. Final numbers are reviewed in more than one analyst pass before sign-off.

The report is refreshed annually, and interim updates are made when a material event changes demand or pricing in a visible way. Right before delivery, we perform a fresh check so the final tables reflect the latest public disclosures and confirmed market signals.

Mordor Intelligence's Genome Editing Market Size Compared Against Other Published Estimates

Published numbers for genome editing do not always match because firms choose different year bases, include different workflow items, and apply different pricing and adoption assumptions. Differences also show up when one publisher relies heavily on early pipeline optimism, while another restricts the addressable pool to what is already used in routine lab and therapeutic programs.

The biggest gap drivers in this market are scope (whether delivery vectors and enabling services are included, and whether non-editing adjacent genomics spend is mixed in), how clinical and research demand is weighted, and how ASPs shift over time as scale improves. Another common reason is refresh cadence, since a single new approval, safety update, or funding shift can change near-term expectations, and those changes do not hit every model at the same time. The table below highlights that the spread is mainly explained by excluding stand-alone gene synthesis and non-editing sequencing consumables from the revenue pool, a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.29 B (2026) | |

| Global Consultancy A | USD 13.24 B (2026) | This estimate appears to use a broader revenue net for genome editing. It can pull in adjacent workflow revenue without explicitly stripping out non-editing sequencing or loosely linked synthesis activity, which lifts the 2026 total. |

| Industry Association B | USD 9.30 B (2024) | This figure is anchored to a 2024 base year. It reflects a more conservative translation curve from research to commercial demand, which keeps adoption and ASP uplift tighter in the near term, making it lower than 2026-based views. |

Looking across the three figures, the difference is not just math, it is what each model chooses to count and how fast it lets demand scale. By keeping the revenue pool tied to editing-specific workflows and then cross-checking it against trials, funding, and adoption signals, the resulting number stays traceable to clear inputs and can be repeated when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the genome editing market?

The genome editing market is valued at USD 12.29 billion in 2026.

How fast will the genome editing market grow through 2031?

Revenue is projected to rise at a 15.98% CAGR, reaching USD 25.74 billion by 2031.

Which technology holds the largest genome editing market share?

CRISPR platforms led with 41.10% share in 2025, ahead of other nuclease systems.

Why is Asia-Pacific the fastest-growing regional market?

Supportive policies in China, Japan, Australia, and India foster rapid adoption, producing a forecast 19.75% CAGR to 2031.

What is the greatest risk facing commercial expansion?

Cross-border regulatory fragmentation, particularly for gene-edited crops, remains the primary drag on global market access.

Which companies are setting the pace for innovation?

CRISPR Therapeutics, Intellia Therapeutics, Mammoth Biosciences, Thermo Fisher Scientific, and Merck KGaA are among the leaders, each advancing distinctive platforms or integrated solutions.

Page last updated on: