India Musical Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

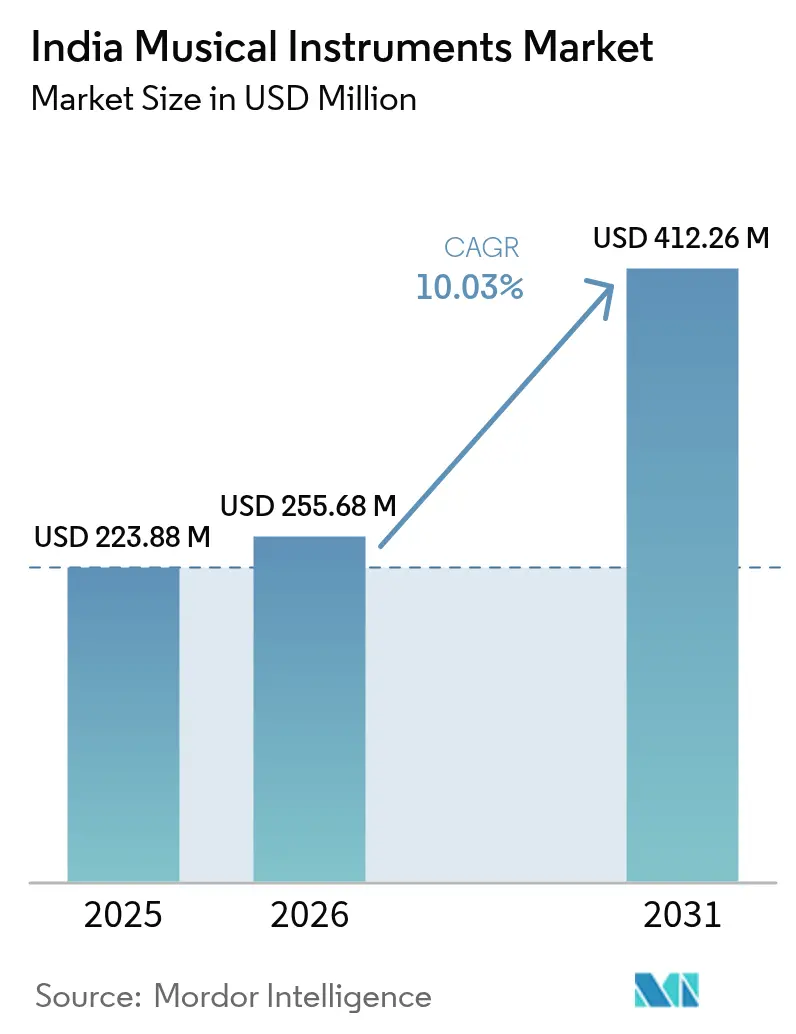

| Base Year Market Size (2025) | USD 223.88 Million |

| Market Size (2026) | USD 255.68 Million |

| Market Size (2031) | USD 412.26 Million |

| Growth Rate (2026 - 2031) | 10.03% CAGR |

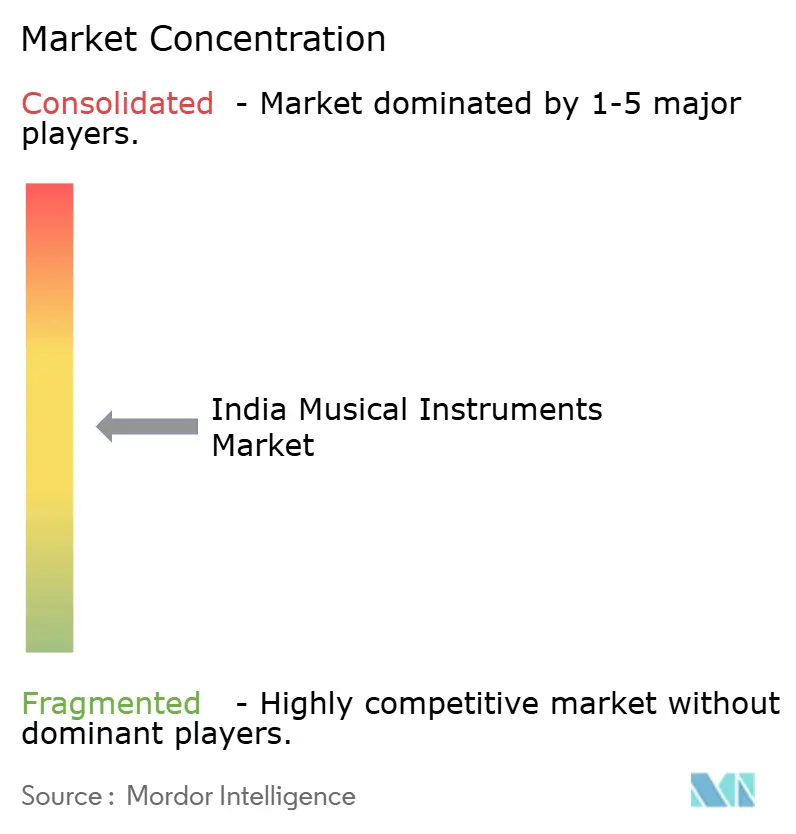

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Musical Instruments Market Analysis by Mordor Intelligence

The India Musical Instruments Market size is expected to increase from USD 223.88 million in 2025 to USD 255.68 million in 2026 and reach USD 412.26 million by 2031, growing at a CAGR of 10.03% over 2026-2031. Growth rests on rising disposable incomes across tier-2 and tier-3 cities, policy support such as the Kala Sanskriti Vikas Yojana, and the rapid take-up of digital music-learning platforms that funnel novice players toward first-time purchases. Compact electronic models appeal to apartment dwellers in major metros where space limits acoustic alternatives, while tax exemption for 134 traditional instruments protects demand for tablas, sitars, and veenas despite a 28% GST on most modern devices. Music ed-tech firms integrate sales links within lesson plans, turning classrooms into scaled retail funnels and widening access for price-sensitive learners. National Education Policy 2020 embeds arts training in core curricula, encouraging schools to place bulk orders that stabilise demand even when discretionary spending softens. Government artisan schemes, including the INR 13,000 crore PM Vishwakarma Yojana, add a livelihood safety net for craft clusters, ensuring stable supply of hand-made instruments.

Key Report Takeaways

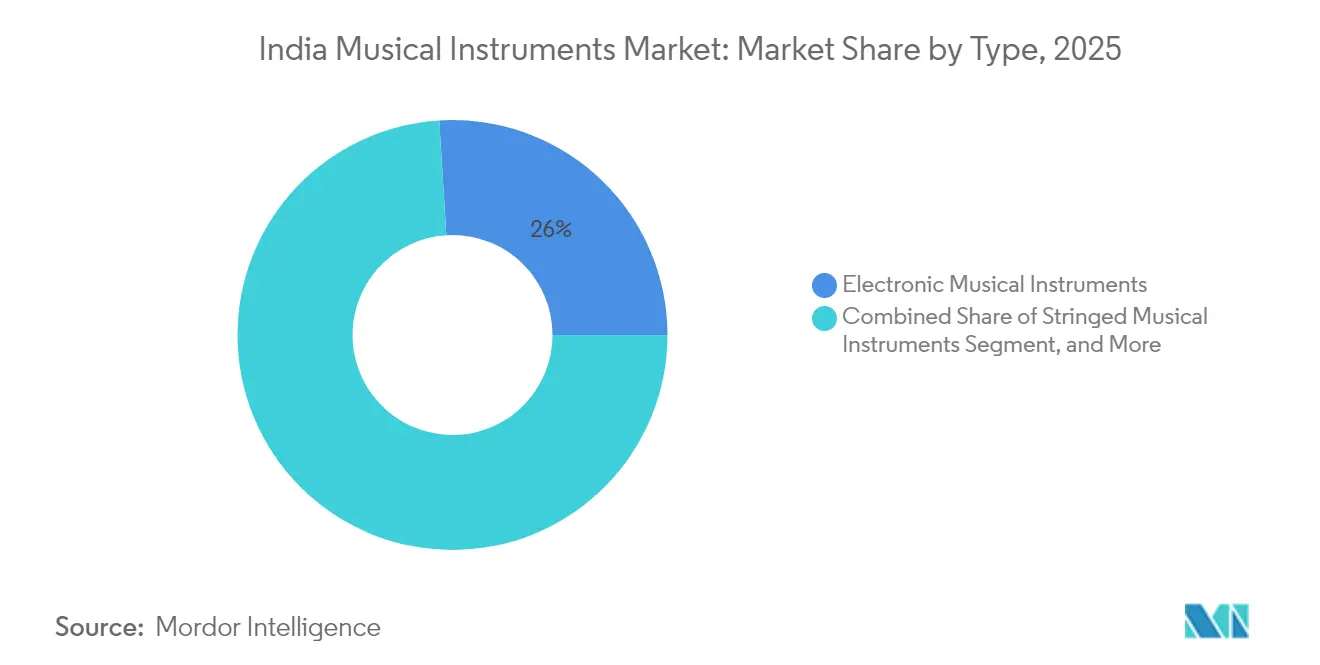

- By product type, electronic instruments led with 25.98% revenue share in 2025 while the Others segment is projected to grow at 12.27% CAGR through 2031.

- By distribution channel, offline retail captured 78.35% of the India musical instruments market share in 2025, whereas online retail is advancing at an 11.17% CAGR to 2031.

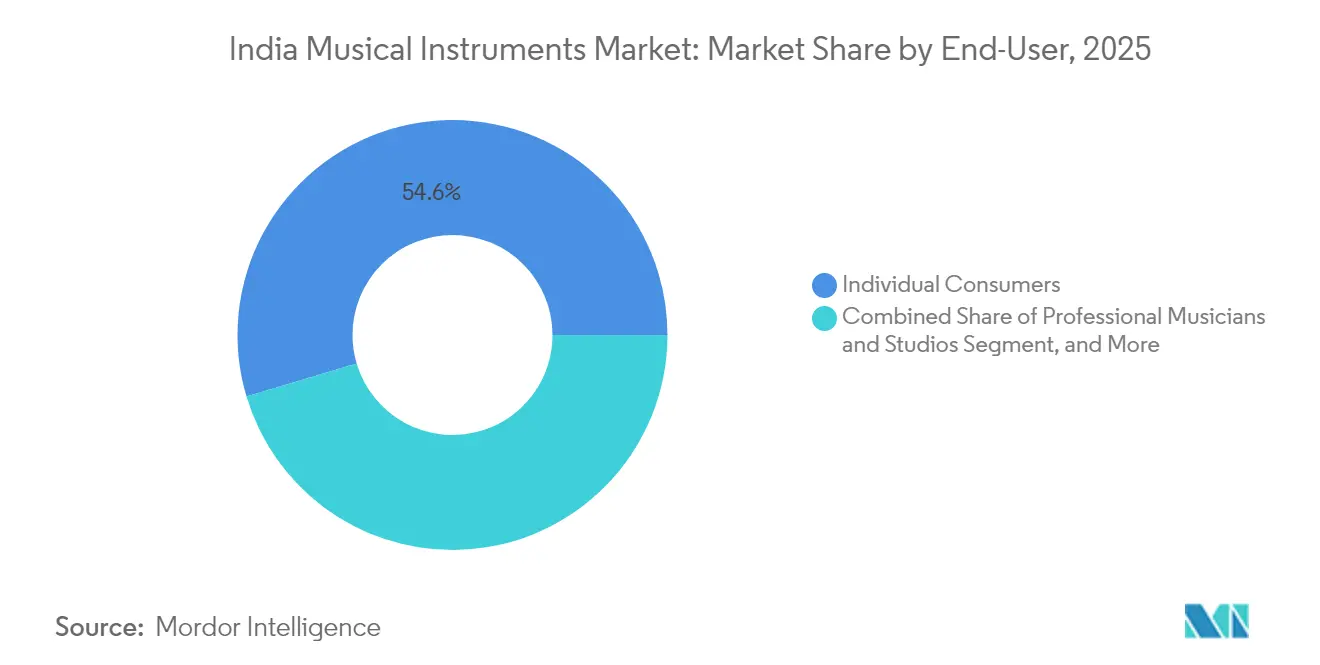

- By end-user, individual consumers accounted for 54.62% share of the India musical instruments market size in 2025, but educational institutions are forecast to expand at 13.38% CAGR during 2026–2031.

- By price range, entry-level units priced below ₹10,000 commanded 45.92% share of the India musical instruments market size in 2025, while the premium tier above INR 50,000 is set to rise at 10.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on musical instrument market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Musical Instruments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes in tier-2 and tier-3 cities | +2.80% | Maharashtra, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| Proliferation of indie-music and OTT-led demand for recording gear | +2.10% | Mumbai, Delhi, Bangalore | Short term (≤ 2 years) |

| Government Kala Sanskriti Vikas Yojana subsidies for classical instruments | +1.50% | Pan-India | Long term (≥ 4 years) |

| Growth of music ed-tech platforms boosting entry-level sales | +2.30% | Metros expanding to tier-2 | Short term (≤ 2 years) |

| Emergence of compact digital instruments for small urban homes | +1.90% | Major metros | Medium term (2-4 years) |

| Enhanced music education infrastructure through NEP 2020 | +1.70% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes in Tier-2 and Tier-3 Cities

Income gains beyond the top metros lift household spending on cultural pursuits, pushing annual discretionary outlays in Coimbatore, Nashik and Indore markedly higher. Parents view music lessons as a pathway to holistic development and social status. As new music schools open across these cities, retailers report brisk sales of entry-level keyboards and acoustic guitars aimed at first-time learners. Regional preference remains distinct; southern markets tilt toward classical stringed varieties, while northern clusters opt for modern guitars and drum kits. Manufacturers respond with blended product lines that combine traditional tonal presets with digital portability, ensuring relevance across cultural segments.

Proliferation of Indie-Music and OTT-Led Demand for Recording Gear

Streaming platforms fund large volumes of original content, so home studios have become mainstream for creators composing underscores and jingles. Indie artists monetize work through JioSaavn and Gaana, fuelling purchases of audio interfaces, MIDI controllers and compact keyboards that integrate Indian patch libraries. Electronic brands enjoy cross-selling opportunities for headphones, microphones and practice amps, deepening average order values. The trend particularly favours the India musical instruments market as professional-grade gear now ships in smaller form factors that fit domestic environments without compromising on fidelity.

Government Kala Sanskriti Vikas Yojana Subsidies for Classical Instruments

Central funding offsets costs for tablas, sitars and veenas supplied to schools and cultural centres, creating guaranteed volume streams for artisan workshops. [1]Press Information Bureau, “YEAR END REVIEW – 2024,” pib.gov.in Procurement contracts stipulate certified quality, helping formalise cottage production and stabilise livelihoods. Skill-development sessions within the programme sustain generational knowledge transfer, curbing erosion of specialist craftsmanship in hubs such as Miraj. Over time, reliable institutional orders are expected to anchor as much as one-fifth of traditional segment revenues inside the India musical instruments market.

Growth of Music Ed-Tech Platforms Boosting Entry-Level Instrument Sales

Platforms such as FSM Buddy and Artium Academy embed shopping carts into lesson dashboards, nudging students to purchase recommended models priced under ₹10,000. AI-based feedback shortens learning curves, encouraging continual upgrades to higher-spec units. Schools adopting cloud-based learning management systems arrange bulk procurement through these platforms, compressing the buyer journey and reducing inventory risk for manufacturers. The India musical instruments market thus benefits from a virtuous loop where learning access pulls hardware demand and hardware ownership feeds sustained course enrolments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High 28% GST slab on finished musical instruments | -2.40% | National | Short term (≤ 2 years) |

| Dominance of low-cost unorganised makers compressing margins | -1.80% | Delhi, Mumbai, Kolkata | Medium term (2-4 years) |

| Limited after-sales service network in rural markets | -1.20% | Rural and semi-urban India | Long term (≥ 4 years) |

| Economic sensitivity to discretionary spending fluctuations | -1.50% | Tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High 28% GST Slab on Finished Musical Instruments

Guitars, pianos and electronic keyboards attract one of the highest GST rates, inflating end-user prices and dampening middle-class uptake. Retailers note double-digit dips in western-instrument categories since the slab took effect. Classroom enrolments that rely on these instruments fall when parents defer purchases, pushing teachers to recommend lower-cost substitutes or shift to tax-exempt Indian instruments. The resulting distortion encourages grey-market imports and under-invoicing practices that erode the organised trade’s share inside the India musical instruments market.

Dominance of Low-Cost Unorganised Makers Compressing Margins

Family-run workshops produce tablas and dholaks at prices up to 40% below branded equivalents, compelling formal players to either reduce margins or exit certain subsegments. While affordability aids penetration, inconsistent build quality can shorten instrument life, discouraging repeat purchases through formal channels. Organised firms struggle to justify R&D outlays when price competition remains severe, slowing innovation in tone-wood substitutes or ergonomic enhancements. Over time, the quality gap threatens to dilute export prospects for Indian-made traditional gear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electronic Instruments Lead Digital Transformation

Electronic instruments accounted for 25.98% of the India musical instruments market in 2025. Urban buyers prize keyboards such as Yamaha’s PSR-I500, which houses 40 Indian voices and 50 auto-accompaniments, letting students practise both raga scales and pop backings on a single device. Acoustic stringed instruments, including sitars and guitars, retain cultural appeal, but their growth trails hybrid models that embed digital sound engines inside wooden bodies. Percussion sales ride a dual wave from classical tabla exams and Western drum set demand among college bands. Parts and accessories build an annuity stream that often carries higher gross margins than primary units. The Others category expands at 12.27% CAGR, spotlighting modular devices that blend electronic loops with classical tones, a sign that the India musical instruments market continues to fuse heritage with tech-savvy expression.

Electronic adoption also benefits from easy volume control, vital in apartment living where noise bylaws constrain acoustic practice. Manufacturers integrate Bluetooth and app-based tutorials, letting learners log progress and share compositions online. As 5G coverage widens, real-time collaboration tools will likely extend instrument functionality further, positioning electronics as the platform for future experiential add-ons such as AR fingering guides and AI-driven tone correction. The segment thus serves as the gateway through which many first-time users enter the India musical instruments market.

By Distribution Channel: Offline Retail Dominance Faces Digital Disruption

Offline retail held 78.35% of the India musical instruments market share in 2025. Purchasers of violins, sitars and grand pianos insist on trial sessions to evaluate resonance and ergonomics. Heritage chains such as Furtados combine showrooms with in-house tutors, creating experience centres that convert curious walk-ins into committed learners. Brick-and-mortar specialists maintain service workshops for tuning and repairs, a trust factor hard to replicate online. Regionally, smaller towns rely on local stores versed in cultural repertoire who can assemble custom instrument sets for temple orchestras or folk festivals.

E-commerce grows at 11.17% CAGR as logistics networks mature. Platforms upload 360-degree demos, user reviews and financing options, shrinking discovery friction. The pandemic normalised remote buying for student-grade guitars and keyboards, even though premium sales still skew store-based. Retailers now run hybrid models: QR codes in-store link to extended online catalogues, while online platforms stage pop-up experience zones during cultural festivals. Over the forecast period, share shifts slowly but meaningfully toward digital, cementing omnichannel distribution within the India musical instruments market.

By End-User: Individual Consumers Drive Market Growth

Individuals represented 54.62% of demand in 2025, validating the democratisation of home music making. YouTube how-to videos and freemium learning apps lower the knowledge barrier; entry-level guitars shipping for under ₹5,000 encourage experimentation. Weekend hobbyists in Bengaluru and Pune form community jam circles that feed word-of-mouth sales. Household favour varies by region: Carnatic lovers in Chennai purchase veenas, while Delhi students gravitate toward ukuleles and digital pianos. Manufacturers tailor marketing messages to these lifestyle cohorts, reinforcing the inclusive ethos now anchoring the India musical instruments market.

Educational institutions post the fastest outlook at 13.38% CAGR, driven by NEP 2020 mandates. The Subramaniam Academy of Performing Arts offers turnkey curricula, prompting schools to standardise instrument kits and bulk-buy from select suppliers. Volume contracts smooth revenue for branded players, and after-sales maintenance agreements further embed supplier relationships. Professional musicians, broadcast studios and cultural organisations round out demand, collectively favouring high-spec products that elevate perceived brand prestige and inspire aspirational purchases among students.

By Price Range: Entry-Level Dominance Reflects Affordability Focus

Entry-level models below INR 10,000 (USD 116.84) captured 45.92% of the India musical instruments market size in 2025. Cost-conscious parents select budget keyboards bundled with foldable stands and online lesson codes, keeping total spend within discretionary limits. Manufacturers optimise bill-of-materials through global sourcing, achieving acceptable tonal quality for first-year learners. Extended warranties and buy-back programmes ease upgrade anxiety, smoothing progression into mid-range SKUs once skill advances.

Premium units above INR 50,000 (USD 584.19) grow at 10.95% CAGR as income levels and discerning tastes rise in urban centres. Concert pianists and recording artists demand European spruce soundboards, hand-wound pickups or carbon-fiber bows for consistent performance. Brands import flagship lines on indent-order basis, offering concierge delivery and annual servicing to justify pricing. The mid-range between INR 10,000 (USD 116.84) and INR 50,000 (USD 584.19) serves aspirants who require reliability for graded exams without paying top-tier premiums. This stratification allows the India musical instruments market to cater to diverse wallets while nurturing lifetime value through step-up journeys.

Segment Analysis: By Distribution Channel

The western region, anchored by Maharashtra and Gujarat, leads consumption, buoyed by Mumbai’s film industry which requires a steady pipeline of session musicians and recording gear rentals. Miraj in Sangli district remains a vital craft hub for harmoniums and sitars, though artisans adopt CNC routers and kiln-dried woods to improve consistency without forsaking hand finishing. Rising prosperity in Pune and Surat fosters vibrant amateur music scenes that fill evening classes and weekend jam cafés.

Southern states like Karnataka and Tamil Nadu exhibit balanced demand for Carnatic staples such as mridangams alongside modern keyboards used in independent film scoring. Bengaluru’s technology workforce embraces online lessons, driving subscriptions to ed-tech platforms that ship starter kits to student doorsteps. State cultural departments allocate grants for classical music festivals, indirectly sustaining instrument rentals and sales. Chennai conservatories order bulk violins and veenas each academic cycle, reinforcing institutional channels inside the India musical instruments market.

Northern markets centred on Delhi-NCR favour contemporary guitars, drum kits and studio monitors, reflecting a vibrant indie-band culture and dense cluster of advertising agencies producing jingles. Proximity to air-cargo infrastructure supports direct imports of American and Japanese marques, while local luthiers offer bespoke sitars with fibre-reinforced bridges to touring maestros. Eastern India, especially West Bengal, maintains strong heritage demand for classical instruments despite lower overall purchasing power. Growing urbanisation in Kolkata increases appetite for electronic keyboards that can toggle between Western chords and Rabindra Sangeet presets. Collectively, regional mosaics ensure the India musical instruments market evolves through diverse cultural lenses rather than a single homogeneous trend.

Competitive Landscape

The India musical instruments market is moderately fragmented. Global names Yamaha, Casio and Roland dominate electronic and keyboard categories by virtue of global R&D pipelines and reliable supply chains. Yamaha localises content libraries, adding tabla rhythms and Hindustani scale presets to its PSR series, while assembling select models locally to mitigate duty costs. Roland opened flagship stores in Mumbai and Delhi in 2025 to demo its latest digital drum and piano lines, aiming for deeper engagement with professional users.

Domestic players run wide price corridors. Kadence sources ukuleles from its Bengaluru facility and has signalled plans to manufacture classical string instruments to tap school orders. Radel Electronics maintains a niche in electronic tanpuras and sruti boxes prized by classical vocalists. Givson and Bhargava maintain value propositions in entry-level guitars and harmoniums. Informal cottage workshops in Kolkata and Miraj supply affordable tablas and sitars, keeping organised share below half in those subsegments. Competition increasingly hinges on ecosystem play: Furtados’ FSM Buddy platform links instrument sales, financing and curriculum; Casio partners with online marketplaces for bundle promotions including headphones and lesson vouchers.

Mergers and acquisitions hint at rising consolidation. Marshall’s purchase by HongShan Capital Group, though global in scope, is expected to support digital retail roll-outs in India after 2025. [3]AudioXpress Editors, “Morel establishes manufacturing facility in India,” audioxpress.com Morel’s joint venture with Supreme Group signals vertical integration into local driver manufacturing for hifi and automobile audio. As organised players expand service centres and finance options, their combined share is projected to inch upward, yet significant room remains for artisan clusters that differentiate on tonal authenticity, ensuring vibrant competition across price points.

India Musical Instruments Industry Leaders

-

Yamaha Corporation

-

Kawai Musical Instruments Mfg Co. Ltd

-

Roland Corporation

-

Cor-Tek Corporation

-

Fender Musical Instruments Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Roland Corporation expanded its India footprint by opening flagship stores in Mumbai and Delhi.

- February 2025: Ram Ratna Wires approved new facilities in Rajasthan and Silvassa that will supply copper windings used in speaker and pickup manufacture.

- January 2025: Marshall Group completed its EUR 1.1 billion (USD 1.29 billion) acquisition by HongShan Capital Group, enhancing digital distribution capacity.

- December 2024: Yamaha Corporation launched its School Project in India to broaden instrument literacy among public-school students.

India Musical Instruments Market Report Scope

The market is defined by the revenue generated from the sale of various types of musical instruments offered by different market players across India. The market trends are evaluated by analyzing the investments made in product innovation, diversification, and expansion. Further, technological advancements encouraged the production and development of a wide range of improved musical instrument versions, which is crucial in determining the growth of the market studied.

The Indian musical instruments market is segmented by type (electronic musical instruments, string musical instruments, wind instruments, acoustic pianos and stringed keyboard instruments, percussion instruments, and other musical instruments (parts and accessories)) and distribution channel (online and offline). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Electronic Musical Instruments |

| Stringed Musical Instruments |

| Wind Instruments |

| Percussion Instruments |

| Keyboard and Piano Instruments |

| Parts and Accessories |

| Others |

| Online Retail |

| Offline Retail |

| Individual Consumers (Hobbyists) |

| Professional Musicians and Studios |

| Educational Institutions |

| Religious and Cultural Organisations |

| Entry-level ( < 10 k) |

| Mid-range (10 k - 50 k) |

| Premium (> 50 k) |

| By Type | Electronic Musical Instruments |

| Stringed Musical Instruments | |

| Wind Instruments | |

| Percussion Instruments | |

| Keyboard and Piano Instruments | |

| Parts and Accessories | |

| Others | |

| By Distribution Channel | Online Retail |

| Offline Retail | |

| By End-User | Individual Consumers (Hobbyists) |

| Professional Musicians and Studios | |

| Educational Institutions | |

| Religious and Cultural Organisations | |

| By Price Range | Entry-level ( < 10 k) |

| Mid-range (10 k - 50 k) | |

| Premium (> 50 k) |

Key Questions Answered in the Report

What is the current size of the India musical instruments market?

The market was valued at USD 255.68 million in 2026 and is projected to reach USD 412.26 million by 2031 based on a 10.03% CAGR.

Which product segment holds the largest share?

Electronic instruments account for 25.98% of sales, driven by space-saving designs that fit urban lifestyles.

How does GST affect instrument prices?

A 28% GST on most modern instruments raises retail prices, while 134 traditional models remain exempt, creating sizeable price differentials that influence purchase decisions.

Why are educational institutions a high-growth end-user?

National Education Policy 2020 mandates arts integration, and structured programmes like those from the Subramaniam Academy prompt schools to procure instruments in bulk, leading to a 13.38% CAGR for this segment.

What role do digital platforms play in market expansion?

Music ed-tech apps integrate shopping links and personalised lessons, stimulating entry-level purchases and expanding reach into tier-2 cities where physical training centres are scarce.

Which regions are emerging as new growth hotspots?

Tier-2 and tier-3 cities such as Coimbatore, Nashik and Indore show accelerating demand due to rising incomes and growing cultural aspirations.

Page last updated on: