Muscle Stimulator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

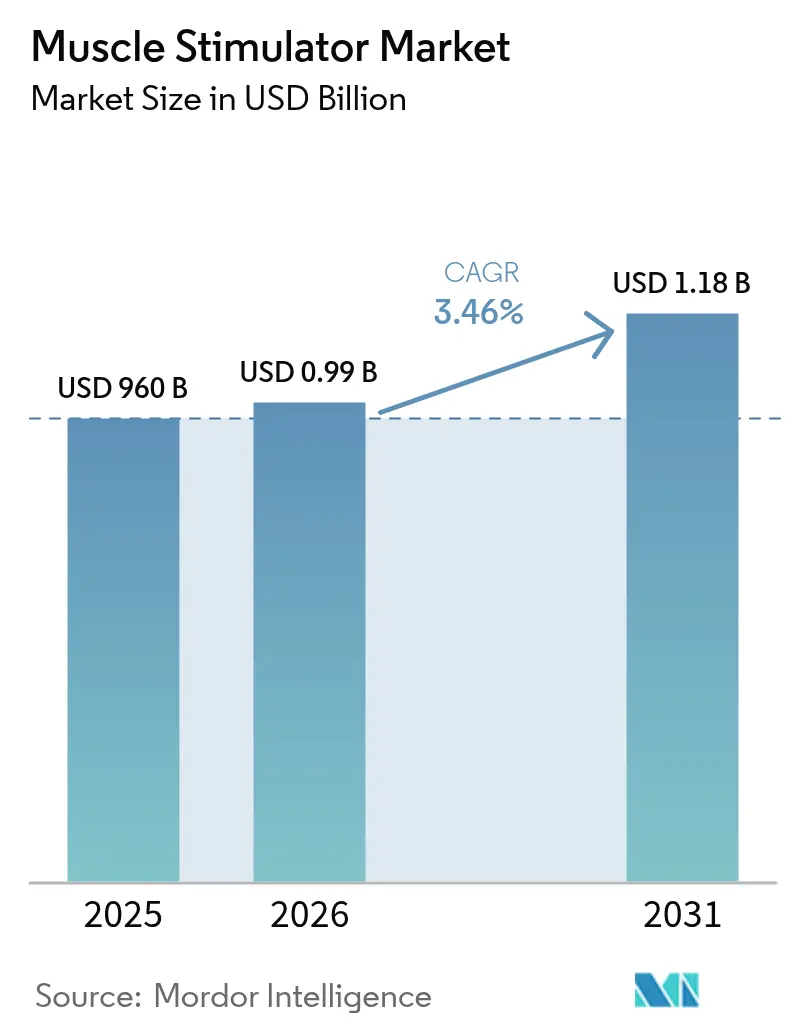

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Muscle Stimulator Market Analysis by Mordor Intelligence

The muscle stimulator market size is expected to grow from USD 960 million in 2025 to USD 993.2 million in 2026 and is forecast to reach USD 1.18 billion by 2031 at 3.46% CAGR over 2026-2031. This measured expansion reflects a transition from clinic-centric equipment toward connected, consumer-oriented devices enabled by miniaturized electronics, longer-life micro-batteries and app-based interfaces. Demand is reinforced by the global rise in chronic pain, increasing preference for non-pharmacological care, and growing integration of smart electrodes with cloud platforms that let clinicians adjust settings remotely. Growth remains moderate because reimbursement rules differ widely by country, while multi-step regulatory pathways lengthen time-to-market for novel closed-loop and bioabsorbable systems. Competitive momentum is intensifying as consumer electronics brands enter the space, compelling incumbent device firms to differentiate through digital services and advanced materials.

Key Report Takeaways

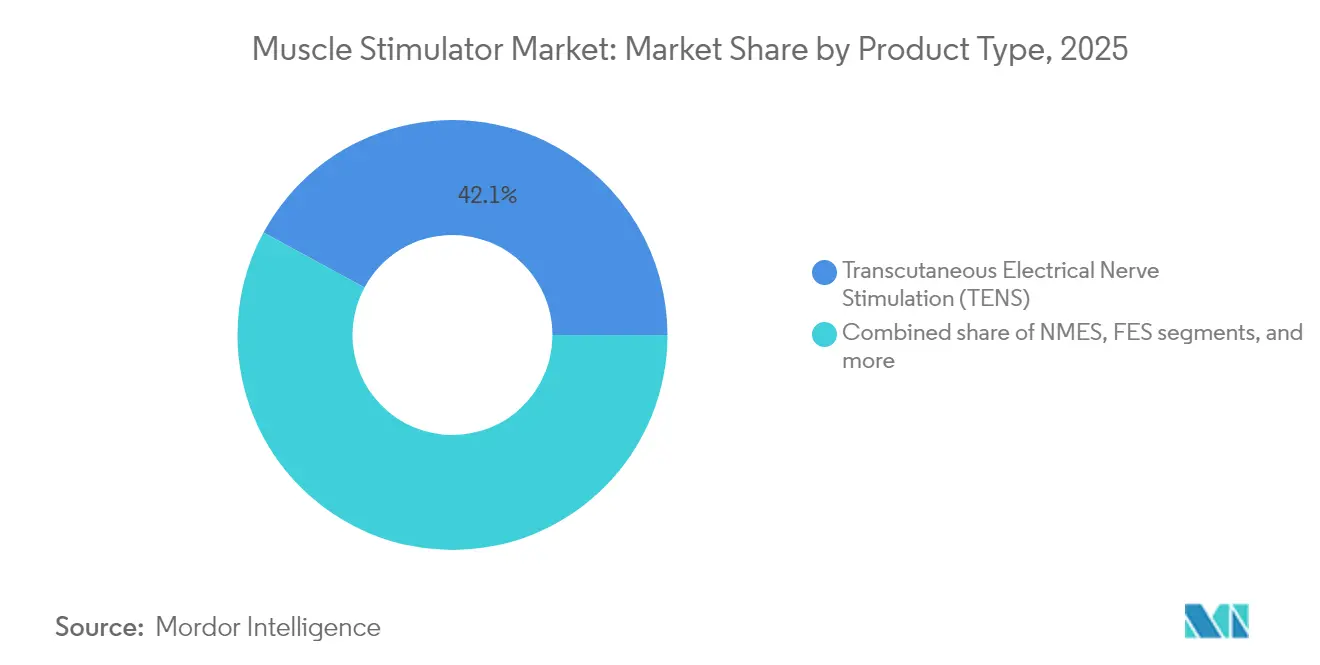

- By product type, Transcutaneous Electrical Nerve Stimulation (TENS) led with 42.10% revenue share of the muscle stimulator market in 2025; Functional Electrical Stimulation (FES) is projected to grow at a 4.93% CAGR through 2031.

- By modality, portable/bench-top systems held a commanding 63.70% of the muscle stimulator market share in 2025, whereas hand-held units are set to expand at 4.12% CAGR from 2026-2031.

- By application, pain management captured 58.05% of the muscle stimulator market size in 2025; neurological rehabilitation is poised for the fastest 4.61% CAGR to 2031.

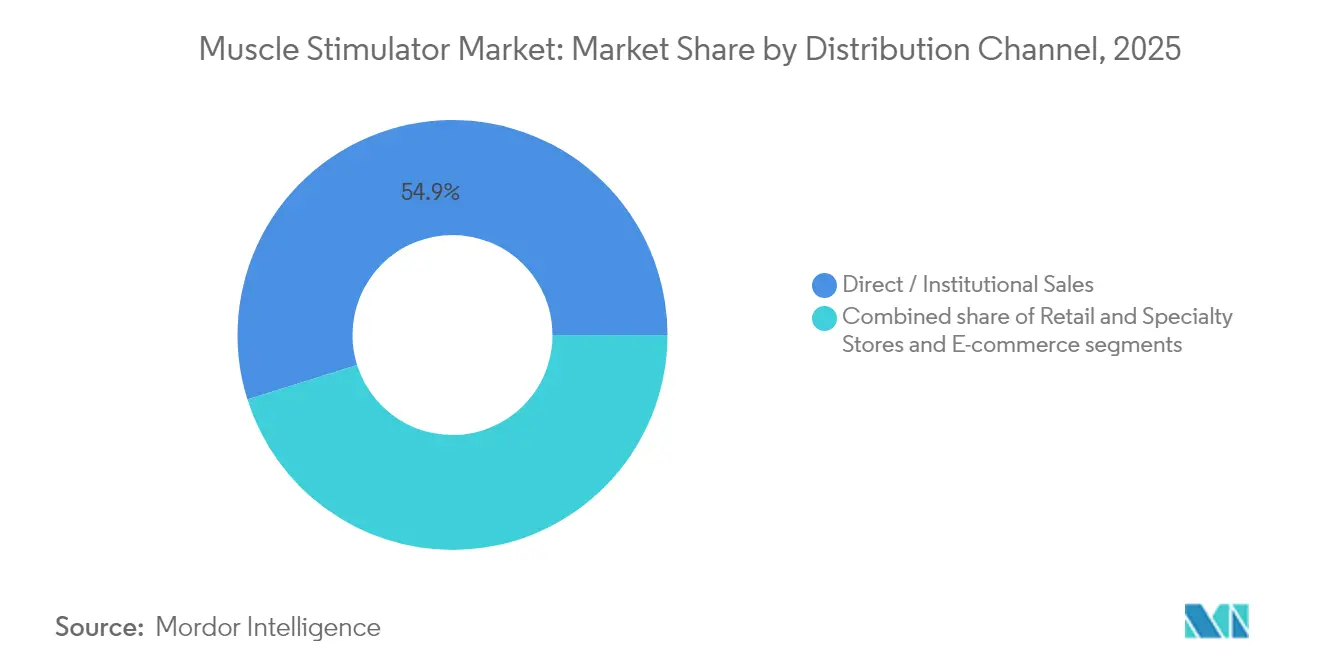

- By distribution channel, direct or institutional sales accounted for 54.85% of 2025 revenue, while e-commerce is forecast to post a 5.21% CAGR.

- By end-user, hospitals contributed 47.30% of 2025 demand; home-care settings will advance at a 5.09% CAGR between 2026 and 2031.

- By geography, North America dominated with 41.25% of 2025 revenue; Asia-Pacific will record the highest 4.68% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Muscle Stimulator Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitally Enabled Home-Use Adoption | 1.1% | Global, with stronger penetration in North America and Europe | Medium term (2-4 years) |

| Age-Linked Chronic Pain Prevalence | 0.9% | Global, with higher impact in regions with aging populations (Japan, Europe, North America) | Long term (≥ 4 years) |

| Sports Medicine Integration | 0.7% | North America, Europe, and high-income Asia Pacific countries | Medium term (2-4 years) |

| AI-Driven Personalized Therapy Protocols | 0.7% | North America, Europe, and high-income Asia Pacific countries | Medium term (2-4 years) |

| Connected Wearable Compatibility | 0.6% | North America, Europe, and urban centers in Asia Pacific | Short term (≤ 2 years) |

| Miniaturized Battery Innovation | 0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitally Enabled Home-Use Adoption

Smartphone-paired stimulators, cloud dashboards, and tele-supervised protocols are shifting treatment toward the home. One trial reported 84.17% adherence[1]Rudri Purohit et al., “Feasibility of Smartphone-Based Exercise Training Integrated with Functional Electrical Stimulation for Stroke Rehabilitation,” MDPI Sensors, mdpi.com among stroke survivors using an app-guided FES program, well above clinic-only regimens. User-friendly interfaces lower technical barriers, while reimbursement pilots for remote physical therapy encourage insurers to cover connected devices. As data streams accumulate, algorithm-driven dose adjustments further personalize therapy and cut clinic visits, reinforcing demand across the muscle stimulator market.

Age-Linked Chronic Pain Prevalence

Populations aged ≥ 65 now account for over 60% of chronic pain cases, and non-drug solutions are increasingly preferred to minimize opioid exposure. High-frequency spinal cord stimulation has yielded 26.1% incremental pain relief for long-COVID patients[2]A. Zulbaran-Rojas et al., “Transcutaneous Electrical Nerve Stimulation for Fibromyalgia-Like Syndrome in Patients with Long-COVID,” Scientific Reports, nature.com, validating electrical modalities in complex syndromes. The economic burden of pain—measured in healthcare outlays and lost productivity—propels public and private payers to support cost-effective neuromodulation, sustaining steady expansion of the muscle stimulator market.

Sports Medicine Integration

Elite teams and rehabilitation centers embed neuromuscular electrical stimulation into injury-prevention, post-surgery strength recovery, and performance programs. NIH-funded research[3]National Institutes of Health, “Implementation of Neuromuscular Electrical Stimulation after Total Knee Arthroplasty,” reporter.nih.govshowed substantial quadriceps strength gains after total knee arthroplasty when NMES was supplemented with standard rehab. Sport-specific protocols are migrating to amateur athletes and fitness enthusiasts, broadening the muscle stimulator market’s customer base and spurring device makers to refine form factors for use during training.

Connected Wearable Compatibility

Integration with biometric wearables enables stimulators to self-adjust using heart-rate variability, muscle oxygen saturation, or skin impedance. Closed-loop designs[4]Scott G. Pritzlaff et al., “Patient Experience with Open-Loop Spinal Cord Stimulation Devices,” Pain Physician, painphysicianjournal.com reduce overstimulation incidents that affect 58% of open-loop spinal cord stimulation (SCS) device users, extending session comfort. Mainstream consumer wearables embedding stimulation modules extend reach beyond clinical channels and generate large datasets that feed future algorithm refinement.

Restraints Impact Analysis of Muscle Stimulator Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Long-Term Efficacy Evidence | -0.6% | Global | Medium term (2-4 years) |

| Skin-Burn & Irritation Risk | -0.4% | Global | Short term (≤ 2 years) |

| High Capital Cost of Advanced FES | -0.3% | Emerging markets in Asia Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Regulatory Approval Delays | -0.3% | Global, with higher impact in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Long-Term Efficacy Evidence

Randomized trials with multiyear follow-up remain scarce, especially for newer pulse-width-modulated or bioabsorbable platforms. A 16-study review on FES cycling for spinal cord injury reported inconsistent spasticity outcomes, underscoring methodological gaps. Without durable evidence, payers often label emerging indications investigational, dampening near-term demand despite FDA clearances.

Skin-Burn and Irritation Risk

Transcutaneous electrodes can cause irritation in up to 25% of users. Carbon-based dry textiles and aloe-infused hydrogels lessen reactions, and smart current-distribution algorithms map skin impedance to avoid hotspots, yet long-term home users remain wary. Device selection for sensitive populations therefore demands careful clinician oversight, tempering widespread self-administration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Muscle Stimulator Market Segment Analysis

By Product Type:

TENS Sustains Leadership as FES AcceleratesThe TENS segment generated 42.10% of 2025 revenue and benefits from decades of clinical familiarity in pain relief. Ultrahigh-frequency protocols now extend post-session analgesia for neuropathic pain, raising patient satisfaction. FES, expanding at a 4.93% CAGR, leverages neuroplasticity research to restore function in stroke and spinal cord injury, pushing commercialization in upper- and lower-limb systems. NMES remains pivotal in strength conditioning, whereas interferential units maintain a niche for deep-tissue treatment. Microcurrent stimulators, while smaller in volume, draw interest for wound-healing and cell-regeneration applications. AI-optimized pulse width that modulates activation depth, up to 21-fold variance, illustrates product differentiation beyond price, supporting long-tail growth within the muscle stimulator market.

Adoption dynamics illustrate that hospital rehabilitation wings continue to purchase multi-protocol consoles, yet consumers gravitate toward single-purpose pads integrated with mobile coaching apps. Suppliers are therefore segmenting portfolios: one line targets high-acuity neurorehabilitation with closed-loop sensing, and another focuses on over-the-counter wellness. As bioabsorbable mechanoelectric sutures progress through pre-clinical studies, manufacturers anticipate disruptive post-surgical indications that could re-shape the muscle stimulator industry’s competitive order.

By Modality:

Portable Systems Anchor Access, Hand-Held Units ProliferatePortable bench-top consoles held 63.70% revenue share in 2025, valued for multi-channel outputs suitable for outpatient departments and satellite clinics. Cloud connectivity uploads usage logs to electronic health records, helping providers validate therapy adherence. Form-factor reductions of 30-40% achieved through compact power electronics and efficient heat sinks make these carts easier to reposition across wards, cutting idle time and improving return on capital.

Hand-held stimulators, predicted to advance at 4.12% CAGR, extend therapy to gyms, homes and athletic fields. Longer-life solid-state batteries and energy-harvesting patches address past re-charging frustrations, while Bluetooth programming reduces setup complexity. Research on self-powered piezoelectric systems that convert biomechanical motion to therapeutic currents hints at future wire-free devices. As these innovations mature, they enlarge the addressable muscle stimulator market size for point-of-care and consumer channels.

By Application:

Pain Management Dominates, Neuro-Rehab SurgesPain management captured 58.05% of 2025 demand, as clinicians seek opioid-sparing modalities. TENS efficacy in post-operative, neuropathic, and long-COVID pain is increasingly documented, prompting guideline updates in physiotherapy societies. Musculoskeletal rehabilitation remains a major revenue sub-node, with sports clinics integrating NMES to expedite return-to-play timelines. Virtual-reality-paired stimulation improves engagement in shoulder and hand therapy, an emerging differentiator among device lines.

Neurological rehabilitation is forecast to deliver the highest 4.61% CAGR through 2031. Adaptive FES gait systems that adjust pulse timing based on real-time plantar pressure data enhance symmetry in stroke survivors, opening broader reimbursement for ambulation assistance. Combining VR with FES also elevates motivation and neuroplastic gains in upper-limb protocols. Growth in these evidence-based indications reinforces the depth and resilience of the muscle stimulator market.

By Distribution Channel:

Institutional Sales Prevail, E-Commerce AcceleratesDirect institutional procurement represented 54.85% of 2025 revenue. Hospitals and rehab centers prefer bundled training, service contracts, and volume-based pricing. Recent CMS guidance that reimburses taVNS for chronic lower-back pain has buoyed capital budgets for neuromodulation lines in integrated delivery networks. Moreover, milestone insurer payments, such as USD 15,420 for a neuromodulation device, signal strengthening reimbursement confidence, preserving institutional dominance.

E-commerce sales, however, are set for 5.21% CAGR. Tele-health consults now authorize prescription-only stimulators via secure online portals, shortening delivery lead-times and expanding reach into rural areas. Reviews and user-generated content boost consumer trust, while subscription electrodes and mobile apps create recurring revenue models. Retail pharmacies and specialty sports stores continue to serve first-time buyers who value hands-on trials, balancing channel mix within the muscle stimulator market.

By End-User:

Hospitals Lead, Home-Care Expands RapidlyHospitals generated 47.30% of 2025 revenue, leveraging multi-specialty utilization, from anesthesiology to orthopedics, to justify high-spec consoles. Pay-for-performance models encourage early mobilization, and electrical stimulation is embedded in fast-track surgical pathways to reduce length of stay. Data captured in hospital settings also underpins registry studies that feed payer dossiers, reinforcing in-patient volume.

Home-care, the fastest-growing end-user at 5.09% CAGR, benefits from policy shifts promoting outpatient recovery and patient self-management. Surveys reveal that people with spinal cord injuries prioritize spasticity relief and bladder control, outcomes well addressed by tailored home FES units. Physiotherapy centers remain vital for skill-intensive regimens, while sports clinics expand premium packages that integrate pre-event warm-up and post-event recovery stimulation. Smaller segments such as long-term care facilities adopt devices that combine stimulation with falls-prevention analytics, enlarging the overall muscle stimulator market.

Geography Analysis

North America Muscle Stimulator Market

North America commanded 41.25% of 2025 revenue on the back of extensive insurance coverage, high chronic pain prevalence, and rapid uptake of closed-loop spinal cord stimulators. In the United States, first-time insurer payments for portable neuromodulation devices set reimbursement benchmarks that ripple across private payers. The region’s 3.08% CAGR reflects an established yet innovation-hungry landscape where digital-first entrants court tech-savvy consumers. Canada’s universal system supports clinic adoption, while Mexico leverages cross-border medical tourism for pain procedures, collectively bolstering the muscle stimulator market.

APAC Muscle Stimulator Market

Asia Pacific is expected to post the fastest 4.68% CAGR through 2031, driven by infrastructure investments and demographic aging. China and India prioritize non-pharmacological pain care in national guidelines, spurring purchases by public hospitals and private wellness chains. Japan leads in neuro-rehabilitation device adoption, with insurers covering advanced FES for post-stroke mobility. South Korea’s contract manufacturers supply global brands, while domestic firms launch low-profile wearables for geriatric home use, expanding the muscle stimulator market size across the region.

EMEA and South America Muscle Stimulator Market

Europe maintains robust share through stringent evidence-based procurement in Germany, the United Kingdom and the Nordics. Pan-EU medical device regulation demands rigorous post-market surveillance, pushing suppliers to run pan-European registries that validate outcomes. Central and Eastern European countries tap EU structural funds to upgrade rehab centers, widening installation bases. Meanwhile, Middle East & Africa and South America grow from low starting points, projecting 3.98% and 3.75% CAGRs respectively. Brazil’s orthopedic clinics adopt NMES for post-arthroplasty rehab, while Gulf Cooperation Council hospitals deploy premium neuro-stimulation suites in medical tourism initiatives. Emerging urban centers across these regions continue to add incremental volume to the global muscle stimulator market.

Competitive Landscape

The muscle stimulator market is moderately fragmented, with globally diversified med-tech vendors, niche neuro-stimulation specialists, and agile consumer electronics firms jostling for share. Top players concentrate on full-featured platforms spanning pain, neuro-rehab and incontinence, often pairing hardware with subscription-based analytics dashboards. Mid-tier innovators pursue AI-enhanced waveform customization, while start-ups exploit flexible printed electrodes and biodegradable materials to differentiate.

Strategic partnerships flourish: device companies link with tele-health providers to bundle virtual coaching; battery developers co-design ultra-thin cells for smart garments; sports franchises pilot in-app performance data feeds to refine training algorithms. Closed-loop SCS launches mark a pivotal shift toward autonomous patient-responsive systems, addressing survey findings that 58% of open-loop users face overstimulation. Bioabsorbable mechanoelectric fibers capable of converting motion into wound-site electrical therapy exemplify convergence between materials science and neuromodulation, opening white-space indications in surgical recovery.

Market entry barriers are easing in consumer segments, but clinical-grade pathways remain demanding due to safety and data requirements. Consequently, dual-brand portfolios emerge: a class-II cleared medical unit for chronic pain, and an over-the-counter muscle-recovery pad for fitness. Established firms leverage scale to secure component supply and regulatory expertise, whereas newcomers rely on crowdfunding and influencer marketing for direct-to-consumer traction. As evidence accumulates and payers reward outcomes-based care, competitive advantage will increasingly hinge on integrated ecosystems that combine adaptive hardware, real-time analytics, and user-centric design across the muscle stimulator market.

Muscle Stimulator Industry Leaders

Beurer

EMS Physio Ltd

Enovis (DJO, LLC)

NeuroMetrix, Inc

Zynex Medical

- *Disclaimer: Major Players sorted in no particular order

Muscle Stimulator Market Companies Covered in this Report

- Abbott Laboratories

- AxioBionics

- Beurer

- BioMedical Life Systems

- BTL

- Chattanooga (DJO)

- Compex

- EMS Physio

- Enovis Corporation

- GAMA Healthcare

- Globus Corporation

- Ito Physiotherapy & Rehabilitation

- Liberate Medical

- Mettler Electronics

- NeuroMetrix

- OG Wellness Technologies

- OMRON

- Restorative Therapies

- RS Medical

- Tone-A-Matic

- Zimmer MedizinSysteme

- Zynex Medical

Recent Industry Developments in Muscle Stimulator Market

- April 2025: Abbott introduced a next-generation delivery system for its Proclaim DRG neurostimulator, improving lead-placement precision for complex regional pain syndrome treatment.

- February 2025: Blue Cross Blue Shield of Rhode Island updated coverage to deem TENS medically necessary for chronic pain, acute postoperative pain, and low back pain while continuing to exclude TAPS for certain uses.

- September 2024: Zynex obtained FDA clearance for its portable TensWave unit, broadening prescription-eligible non-pharmacological pain options.

- April 2024: Medtronic secured FDA approval for Inceptiv, its first closed-loop rechargeable spinal cord stimulator that senses ECAPs and auto-adjusts therapy in real time.

Muscle Stimulator Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the muscle stimulator market as all external, electrically powered devices that deliver controlled current to skeletal muscle or peripheral nerves for pain relief, rehabilitation, or performance support across clinical, sports, and home settings. The universe therefore spans TENS, NMES, FES, interferential, and micro-current units supplied as handheld, portable, or bench-top systems. According to Mordor Intelligence, the global revenue generated by these devices reached USD 0.96 billion in 2025.

Scope exclusion: Implantable neuro-stimulators, radio-frequency ablation systems, and purely cosmetic EMS wearables fall outside this analysis.

Segments Covered in This Report

- By Product Type

- Neuromuscular Electrical Stimulation (NMES)

- Functional Electrical Stimulation (FES)

- Transcutaneous Electrical Nerve Stimulation (TENS)

- Interferential (IF)

- Micro Current Electrical Neuromuscular Stimulator

- Other Products

- By Modality

- Hand-held Devices

- Portable/Bench-top Systems

- By Application

- Pain Management

- Musculoskeletal Disorders

- Neurological Rehabilitation

- Other Applications

- By Distribution Channel

- Direct/Institutional Sales

- Retail & Specialty Stores

- E-commerce

- By End-User

- Hospitals

- Physiotherapy & Rehabilitation Centers

- Sports Clinics

- Home-Care Settings

- Other End-Users

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed physiotherapists, biomedical engineers, procurement heads at multi-specialty hospitals, and e-commerce category managers across North America, Europe, and Asia-Pacific. These conversations clarified average selling prices, typical replacement cycles, and emerging demand pockets, and they helped us challenge preliminary desk-based assumptions before locking the model.

Desk Research

Our analysts began with public datasets such as the US FDA 510(k) and European MDR listings for cleared stimulation devices, UN Comtrade HS 9021 export flows, and population-level pain prevalence from WHO Global Health Observatory. Industry position papers from MedTech Europe, the American Physical Therapy Association, and the International Federation of Sports Physical Therapy supplied utilization context. Company 10-Ks, distributor catalogs, and news archived on Dow Jones Factiva added price and channel details. We also tapped D&B Hoovers for private-company revenue signals. The sources cited above are illustrative; many additional publications informed data collection and cross-checks.

Market-Sizing & Forecasting

Top-down reconstruction started with 2024 production and trade data, which were then adjusted for in-country inventory build-ups and warranty returns to estimate net shipments. Select bottom-up validations, sampled supplier revenues and clinic-level unit adoption, checked reasonableness. Key variables feeding the model include: 1) chronic pain prevalence by age cohort, 2) rehabilitation session volumes reimbursed per insurance schedule, 3) average selling price erosion linked to low-cost Asian imports, 4) penetration of direct-to-consumer online channels, and 5) physiotherapist-to-population ratios. A multivariate regression forecast, anchored to those drivers, projects demand through 2030, after which scenario analysis adjusts for technology shifts. Data gaps in supplier roll-ups were bridged with weighted regional proxies confirmed during interviews.

Data Validation & Update Cycle

Model outputs undergo variance checks against import values, hospital procurement logs, and payer claim trends. Any anomaly above a preset threshold triggers a senior review and follow-up calls with experts. Reports refresh annually, and material events, such as new reimbursement codes, prompt interim updates. Before release, an analyst performs a fresh sense-check so clients receive the latest view.

How Mordor Intelligence's Muscle Stimulator Market Size Compares to Other Published Estimates

Published figures often diverge because firms pick different device sets, price assumptions, and refresh cadences. By aligning scope tightly with cleared external stimulators and updating unit economics each year, Mordor delivers a stable point of reference for planners.

Key gap drivers include: some studies exclude direct-to-home sales, others bundle implantable systems, and a few freeze exchange rates for the entire horizon, which inflates or deflates values versus our dynamic currency treatment.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.96 bn (2025) | Mordor Intelligence | - |

| USD 0.82 bn (2024) | Global Consultancy A | Omits e-commerce and physiotherapy clinic replacements |

| USD 0.74 bn (2024) | Industry Tracker B | Excludes bench-top systems, uses static 2023 ASPs |

In sum, the disciplined variable selection, annual refresh, and dual-path validation ensure Mordor's baseline remains the most transparent and reproducible yardstick for decision makers seeking dependable sizing of the muscle stimulator opportunity.

Key Questions Answered in the Report

How is miniaturization shaping next-generation muscle stimulators?

Advances in compact batteries and low-power electronics are enabling lighter, wearable designs that patients can use during daily activities or athletic training without clinical supervision.

Advances in compact batteries and low-power electronics are enabling lighter, wearable designs that patients can use during daily activities or athletic training without clinical supervision.

Closed-loop stimulators adjust pulse parameters in real time using physiologic feedback, reducing overstimulation events and narrowing the gap between prescribed and delivered therapy.

Why are sports medicine programs increasingly integrating neuromuscular electrical stimulation?

Athletic trainers deploy stimulation protocols to accelerate post-injury strength recovery and to maintain muscle condition during immobilization, shortening return-to-play timelines.

How are reimbursement policies evolving for home-use electrical stimulation devices?

Insurers are beginning to issue indication-specific coverage, such as for chronic low-back pain, once manufacturers provide evidence of clinical benefit and remote-monitoring safeguards.

What technological hurdle still limits widespread consumer adoption of transcutaneous stimulators?

Skin irritation and burn risk from conventional hydrogel electrodes continues to deter long-term use, prompting R&D into textile-embedded dry electrodes and adaptive current-distribution algorithms.

How does data generated by connected stimulators benefit clinicians?

Cloud-synced usage logs and symptom scores give therapists objective insight into adherence and response, allowing timely adjustment of waveforms and session frequency for each patient.

Page last updated on: