MRNA Synthesis Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

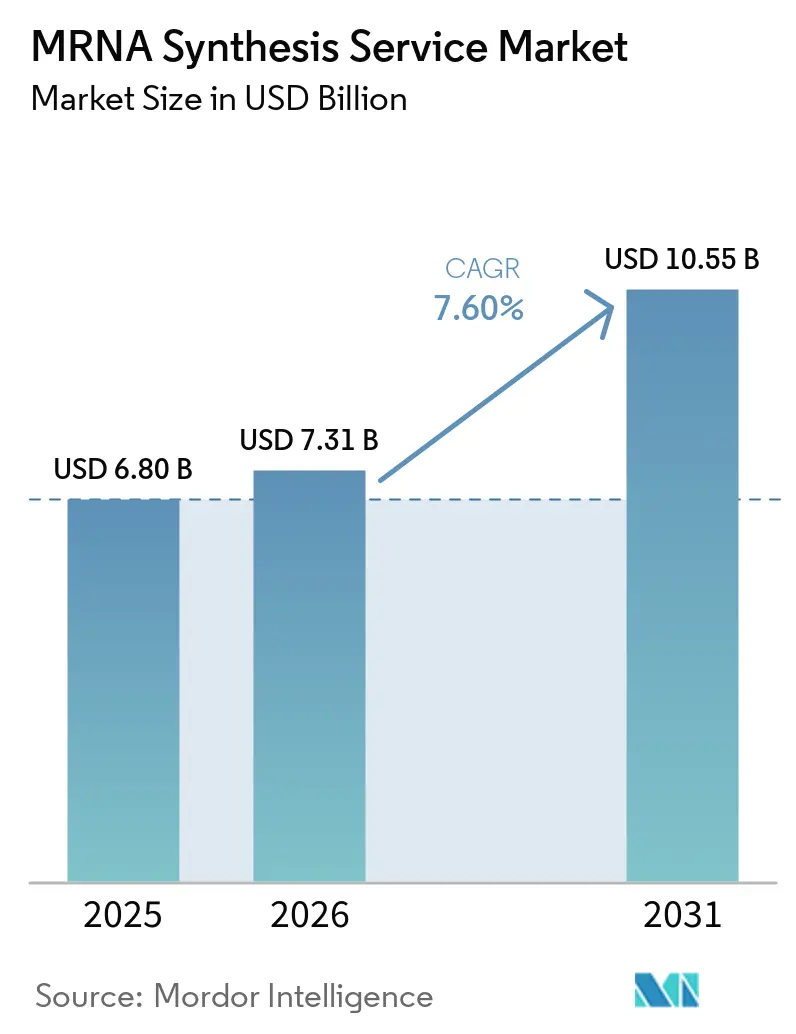

| Market Size (2026) | USD 7.31 Billion |

| Market Size (2031) | USD 10.55 Billion |

| Growth Rate (2026 - 2031) | 7.60% CAGR |

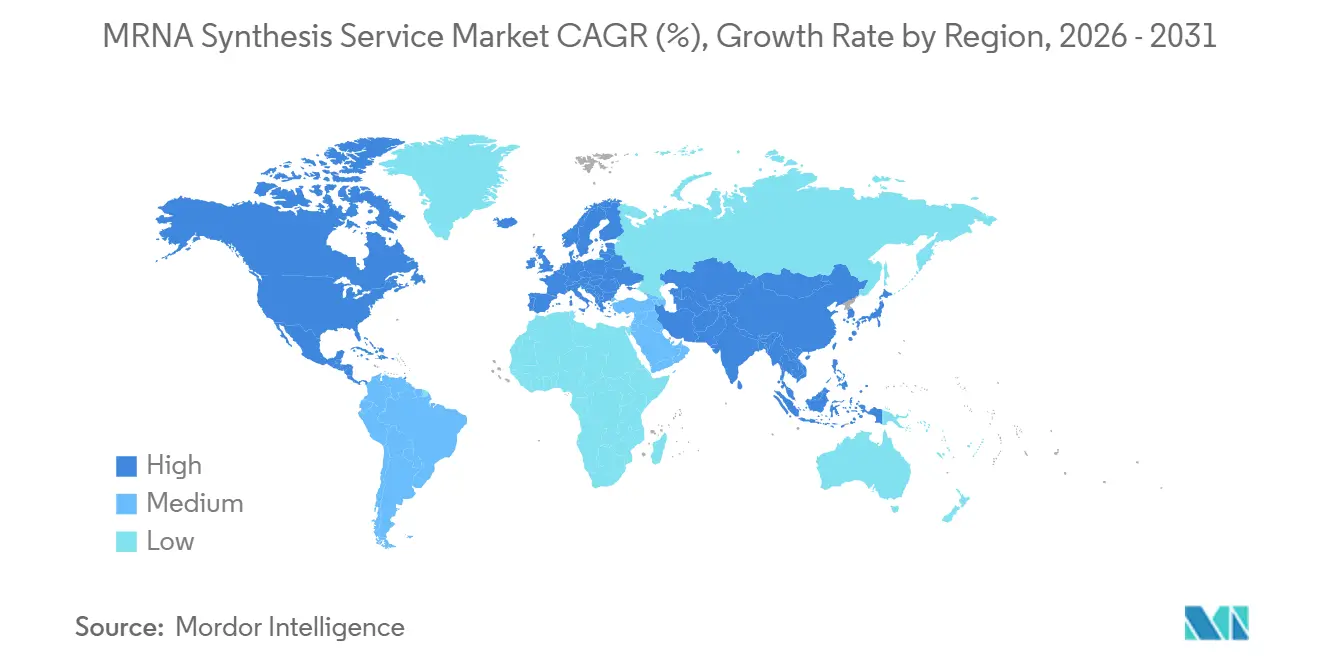

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MRNA Synthesis Service Market Analysis by Mordor Intelligence

The MRNA Synthesis Service Market size is expected to increase from USD 6.80 billion in 2025 to USD 7.31 billion in 2026 and reach USD 10.55 billion by 2031, growing at a CAGR of 7.60% over 2026-2031.

Growing post-pandemic vaccine pipelines, rapid diversification into oncology and gene-editing therapies, and sustained venture and sovereign funding keep demand for outsourced mRNA synthesis strong. Large pharmaceutical companies are refocusing capital on R&D while relying on specialized CDMOs for process development and cGMP production, a shift reinforced by escalating validation requirements and the high cost of in-house facilities. Technological advancements—especially high-efficiency in vitro transcription (IVT), co-transcriptional capping, and AI-guided sequence design—enhance yields, reduce development cycles, and lower per-dose costs. New modular “printer” systems support distributed production, improving supply chain resilience and allowing for rapid regional responses to surges in demand. Competition intensifies as established biologics manufacturers acquire or retrofit plants for mRNA. At the same time, specialist CDMOs differentiate through intellectual-property-backed platforms such as CleanCap, advanced analytics, and integrated lipid-nanoparticle (LNP) formulation offerings.

Key Report Takeaways

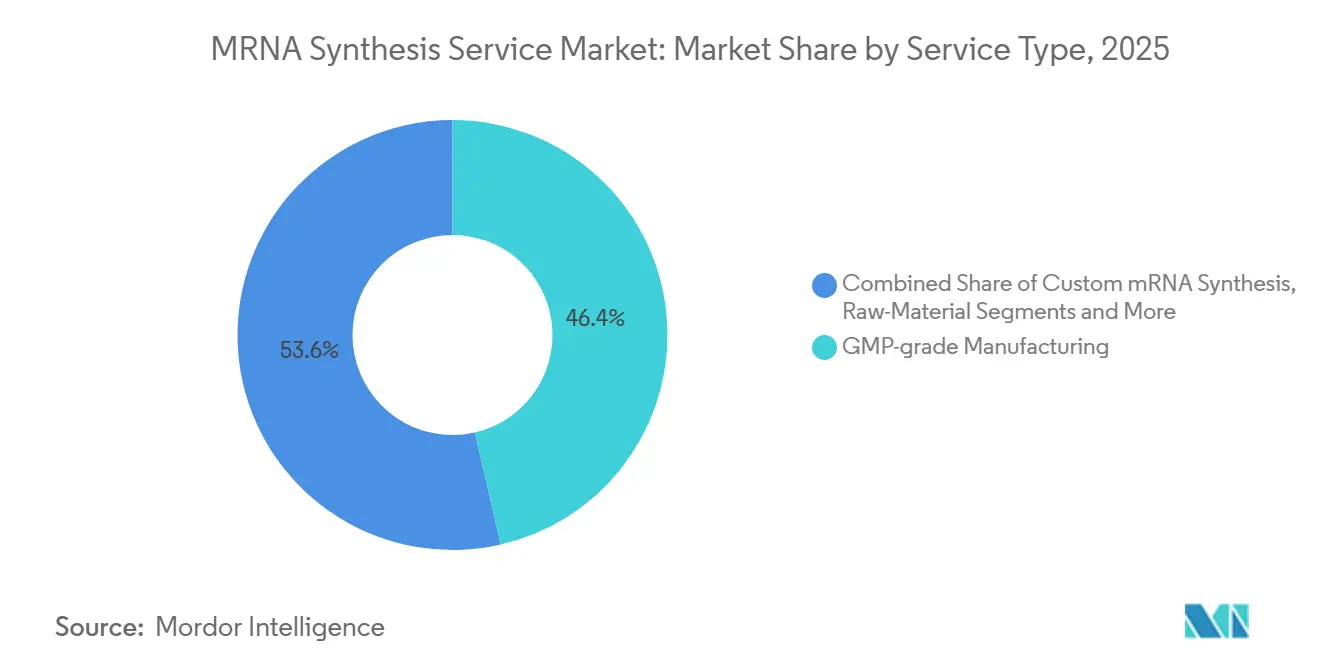

- By service type, GMP-grade manufacturing led with a 46.4% revenue share in 2025, whereas custom synthesis is expected to expand at a 9.1% CAGR through 2031.

- By scale, clinical GMP accounted for 38.9% of the mRNA synthesis services market share in 2025; on-site modular production is projected to grow at the fastest rate, with an 8.4% CAGR, to 2031.

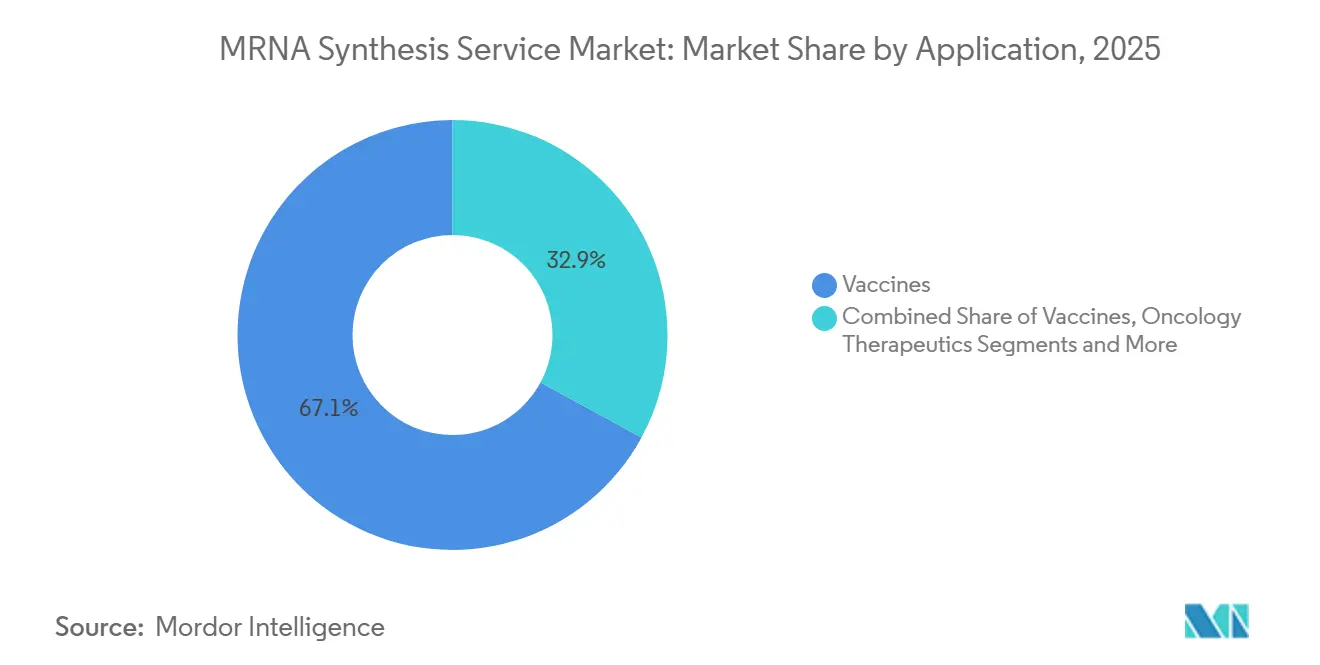

- By application, vaccines held 67.1% of the mRNA synthesis services market share in 2025; gene-editing/CRISPR is projected to grow at a 10.7% CAGR through 2031.

- By end-user, pharmaceutical companies commanded 41.7% share of the mRNA synthesis services market in 2025, while biotechnology firms are advancing at a 7.3% CAGR.

- By geography, North America captured 42.4% revenue in 2025, and the Asia-Pacific is growing at a 6.4% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global MRNA Synthesis Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID vaccine pipeline expansion | +2.10% | Global; early gains in North America & Europe | Medium term (2-4 years) |

| Outsourcing boom to mRNA-focused CDMOs | +1.80% | Global | Short term (≤ 2 years) |

| High-efficiency IVT & capping innovations | +1.40% | North America & EU; spill-over to APAC | Medium term (2-4 years) |

| Venture & government funding influx | +1.20% | U.S., China, EU | Short term (≤ 2 years) |

| Modular “mRNA-printer” micro-factories | +0.90% | APAC core; expanding to MEA | Long term (≥ 4 years) |

| AI-guided sequence optimization & cost drops | +0.20% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Vaccine Pipeline Expansion Drives Therapeutic Diversification

The proven success of nucleoside-modified COVID-19 vaccines turns the spotlight on oncology, RSV, and rare-disease programs now advancing toward approval. Moderna is running as many as 10 late-stage candidates, including personalized cancer vaccines, RSV prophylactics, and a combined influenza/COVID-19 shot. Positive data on mRNA-4157 with pembrolizumab showed a 44% reduction in melanoma recurrence, validating the platform for immuno-oncology.[1]Chen-Yi Chang, “Spiral Microfluidic Chips Enable High-Throughput Lipid Nanoparticle Manufacturing for mRNA Delivery,” Micromachines, mdpi.com CDMOs answer by installing dedicated suites for high-potency and personalized batches; TriLink BioTechnologies recently opened a large-scale cGMP line for late-phase drug-substance production.

Outsourcing Boom Transforms CDMO Competitive Dynamics

Big pharma is scaling back internal capacity as biological complexity and capital intensity soar. Pfizer’s multi-year program targets USD 1.5 billion in manufacturing savings, reallocating funds to clinical assets while partnering with external experts. Recent deals—Agilent acquiring BIOVECTRA for USD 925 million and Maravai LifeSciences purchasing Officinae Bio’s nucleic-acid unit—illustrate consolidation around end-to-end mRNA capabilities.

High-Efficiency IVT and Capping Innovations Reduce Manufacturing Bottlenecks

CleanCap reagents achieve >95% capping efficiency and can cut the cost per gram of mRNA by 20-40%. The new M6 variant raises protein expression by a further 30%. Process refinements, including optimized T7 promoters, push yields to 14 g/L and lower dsRNA contamination by 30%.[2]Xiaoyu Huang, “Artificial Intelligence-Driven Rational Design of Ionizable Lipids for mRNA Delivery,” Nature Communications, nature.com CDMO licensing of these technologies offers faster turnaround and higher potencies to clients, strengthening long-term service contracts.

Venture and Government Funding Influx Accelerates Capacity Expansion

Government pandemic preparedness budgets converge with venture funds targeting mRNA platforms. The U.S. government committed USD 75 million to expand Croda’s lipid facility, bolstering local supply of critical excipients. Meanwhile, GenScript raised USD 224 million to scale CDMO lines in China. Australia allocated USD 200 million to launch Aurora Biosynthetics, adding regional GMP options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GMP compliance & validation bottlenecks | –1.3% | EU & US | Medium term (2-4 years) |

| Supply-chain crunch for high-purity reagents | –0.8% | Global | Short term (≤ 2 years) |

| Vaccine-safety perception headwinds | –0.6% | Global; variable by region | Medium term (2-4 years) |

| Environmental burden of enzymatic reagents | –0.4% | EU & North America; emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GMP Compliance and Validation Bottlenecks Constrain Scale-Up

Revised EMA guidelines for ATMPs and new USP chapters on mRNA vaccines tighten release criteria, mandating advanced analytics such as next-generation sequencing and orthogonal purity assays. The FDA’s Advanced Manufacturing Technologies Framework now requires extensive documentation for novel processes.[3]U.S. Food and Drug Administration, “Advanced Manufacturing Technologies Designation Program; Guidance for Industry,” federalregister.gov CDMOs invest in automated quality systems and digital batch records; Moderna cut R&D spend by USD 1.1 billion through process-validation efficiencies.

Supply-Chain Crunch for High-Purity Reagents Creates Cost Pressures

Global shortages of T7 polymerase, capping enzymes, and nucleotides have extended lead times and inflated costs. Manufacturers respond by dual-sourcing, stockpiling critical inputs, and piloting enzymatic RNA synthesis that replaces chemical steps with water-based reactions, reducing environmental footprint and dependence on scarce reagents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Custom Synthesis Drives Platform Innovation

GMP-grade manufacturing retained the largest share at 46.4% in 2025, reflecting its entrenched infrastructure and regulators’ preference for validated platforms. At the same time, custom synthesis is advancing at a 9.1% CAGR, fueled by demand for individualized cancer vaccines and rare-disease therapies. CDMOs embed AI tools to rapidly iterate sequence constructs, enabling clients to progress from design to IND in under six months. Design-optimization and analytical suites are now standard, as illustrated by the AmplifyBio-RNAV8 collaboration that bundles sequence design, IVT, LNP formulation, and release testing under one roof. The mRNA synthesis services market size for bespoke projects is expected to grow as pay-for-performance models become more prevalent. Intellectual property advantages—such as TriLink’s CleanCap and Aldevron’s high-fidelity plasmids—create durable moats and enable premium pricing.

The widening of service menus mirrors the overall maturation of the mRNA synthesis services market. Raw-material supply agreements safeguard enzyme and nucleotide availability, while hybrid fee structures (capacity reservation plus per-batch charges) help CDMOs offset macroeconomic volatility. As clients aim for accelerated approval pathways, providers integrate regulatory-affairs consulting and companion-diagnostics development, further embedding themselves in sponsor workflows.

By Scale: Modular Production Revolutionizes Manufacturing Paradigms

Clinical GMP batches account for 38.9% of revenue, covering pivotal trials and early launches. The mRNA synthesis services market share for modular facilities, however, is expanding quickest at an 8.4% CAGR. Containerized cleanrooms can be fitted onto a single truck, require minimal civil works, and can transition between 50 mg preclinical runs and multi-kilogram commercial lots within days. BioNTech estimates that a two-unit BioNTainer can deliver 50 million doses annually, with 70% lower capital expenditure (capex) than a traditional plant. For more minor indications, continuous-flow micro-reactors produce on-demand lots, reducing inventory costs.

Legacy commercial-scale suites are consolidating around the use of multiple products. Lonza’s acquisition of Roche’s Vacaville plant added 330,000 L mammalian capacity, now partially retrofitted for mRNA LNP finishing, exemplifying asset repurposing to balance pipeline uncertainty. Hybrid models—central bulk RNA followed by regional fill-finish—enhance resilience to supply-chain shocks.

By Application: Gene Editing Emerges as High-Growth Therapeutic Frontier

Vaccines still dominate at 67.1% share, yet gene-editing and CRISPR therapies post the steepest growth, benefiting from the FDA’s landmark approval of the first ex vivo CRISPR sickle-cell therapy in 2025 and expanding orphan-disease pipelines. Aldevron and Integrated DNA Technologies produced the first patient-specific mRNA CRISPR drug for urea cycle disorder within six months, demonstrating the feasibility of addressing ultra-rare conditions. Oncology programs are leveraging neoantigen vaccines combined with checkpoint inhibitors, while protein-replacement applications are gaining traction for metabolic disorders. The mRNA synthesis services market size for gene-editing payloads is projected to double by 2031 as regulatory pathways clarify and delivery chemistries improve.

By End-User: Biotechnology Companies Drive Innovation Acceleration

Pharmaceutical companies held 41.7% of outsourcing spend in 2025 primarily for high-volume vaccines and late-stage oncology assets. Biotechnology firms, however, are climbing at a 7.3% CAGR, propelled by venture capital and plug-and-play CDMO offerings that obviate the need for bricks-and-mortar plants. Radar Therapeutics, Innovac Therapeutics, and other start-ups leverage milestone-based contracts to conserve cash while accessing premier technology stacks. Academic spin-outs and government labs add incremental demand for preclinical supplies, underscoring the democratization of mRNA R&D.

Geography Analysis

North America controlled 42.4% of revenue in 2025, anchored by a deep talent pool, robust IP protection, and aggressive public-private funding. Three Moderna plants set to go live in 2025—Canada, the U.K., and Australia—will each turn out up to 100 million doses annually, reinforcing cross-regional supply chains while retaining critical steps in the U.S.. The U.S. Biomedical Advanced Research and Development Authority (BARDA) continues to issue multi-year “warm-base” contracts guaranteeing surge capacity.

Europe benefits from cohesive regulatory frameworks and strategic manufacturing hubs. Wacker’s USD 102 million competence center in Germany adds four RNA lines, half reserved for federal pandemic stockpiles. The European Pharmacopoeia’s new general chapter on mRNA quality sets reference standards that streamline batch release across member states.

Asia-Pacific is the fastest-growing region at a 6.4% CAGR. China’s WuXi Biologics and GenScript expansions, South Korea’s Moderna partnership, and Singapore’s role as BioNTech’s ASEAN headquarters illustrate concerted sovereign strategies. Australia’s Aurora Biosynthetics targets end-to-end GMP from plasmid to fill-finish, leveraging USD 200 million in federal backing. Taiwan Bio-Manufacturing Corp aims to replicate the semiconductor foundry model for biopharma, signaling long-term regional ambition.

Middle East & Africa tap into modular systems to bridge infrastructure gaps. HT-Bio’s deployment of KeyPlants PODs in Saudi Arabia marks early adoption. South America expands through tech-transfer agreements in Brazil and Argentina, improving regional vaccine autonomy.

Competitive Landscape

The mRNA synthesis services market features moderate concentration. The top five players—Lonza, TriLink BioTechnologies, Aldevron, Wacker Biotech, and WuXi Biologics—collectively hold roughly 45-50% revenue. Lonza’s USD 1.2 billion Vacaville deal adds mammalian and mRNA flexibility, while a new divisional structure bundles mRNA with cell-and-gene offerings.

TriLink’s non-exclusive CleanCap licenses create a network effect; over 250 INDs rely on the technology, cementing its position as a “gatekeeper” for high-quality 5′ capping. Aldevron expands plasmid capacity and LNP services, securing multi-year supply deals for CRISPR applications.

Wacker is scaling rapid-response lines with EU pandemic contracts, guaranteeing minimum utilization. Smaller specialists differentiate through AI platforms, modular biofoundries, or regional focus.

MRNA Synthesis Service Industry Leaders

Thermo Fisher Scientific

Lonza

TriLink BioTechnologies

Danaher Corporation

Catalent Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Maravai LifeSciences acquired Officinae Bio's DNA and RNA business, bolstering its AI-driven mRNA synthesis capabilities for swift mRNA candidate prototyping.

- November 2024: Maravai LifeSciences initiated mRNA synthesis for a client's Phase II clinical trial at their Flanders 2 GMP facility and unveiled CleanScribe RNA Polymerase to enhance mRNA synthesis quality.

- May 2024: Aldevron teamed up with Acuitas Therapeutics, augmenting mRNA services with lipid nanoparticle encapsulation, ensuring a holistic synthesis-to-formulation approach.

- April 2024: AmplifyBio and RNAV8 Bio forged a partnership, merging sequence design with GMP synthesis, delivering comprehensive mRNA services from design to production.

Global MRNA Synthesis Service Market Report Scope

| Custom mRNA Synthesis |

| GMP-grade Manufacturing |

| Raw-Material & Enzyme Supply |

| Design & Optimisation Services |

| Analytical & QC Services |

| Research Grade (RUO) |

| Pre-clinical Grade |

| Clinical GMP (Phase I-III) |

| Commercial GMP |

| On-Site Modular Production |

| Vaccines |

| Oncology Therapeutics |

| Rare-Disease / Protein-Replacement |

| Gene-Editing / CRISPR |

| Other Therapeutics |

| Biotechnology Companies |

| Pharmaceutical Companies |

| CDMOs & CROs |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Custom mRNA Synthesis | |

| GMP-grade Manufacturing | ||

| Raw-Material & Enzyme Supply | ||

| Design & Optimisation Services | ||

| Analytical & QC Services | ||

| By Scale | Research Grade (RUO) | |

| Pre-clinical Grade | ||

| Clinical GMP (Phase I-III) | ||

| Commercial GMP | ||

| On-Site Modular Production | ||

| By Application | Vaccines | |

| Oncology Therapeutics | ||

| Rare-Disease / Protein-Replacement | ||

| Gene-Editing / CRISPR | ||

| Other Therapeutics | ||

| By End-User | Biotechnology Companies | |

| Pharmaceutical Companies | ||

| CDMOs & CROs | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the mRNA synthesis services market in 2025?

The market stood at USD 6.80 billion in 2025 and is projected to reach USD 10.55 billion by 2031.

Which service segment is growing fastest in mRNA outsourcing?

Custom mRNA synthesis is expanding at a 9.1% CAGR, driven by personalized medicine and AI-enabled design.

Why are modular “printer” plants gaining traction?

Containerized GMP units enable decentralized production, cut construction time, and add resilience to supply disruptions.

Which region shows the fastest growth?

Asia-Pacific is advancing at a 6.4% CAGR thanks to sovereign funding and cost advantages.

What technology most improves mRNA yields?

High-efficiency IVT combined with CleanCap capping pushes yields to 14 g/L and boosts protein expression.

How concentrated is the competitive field?

The top five players control roughly half of revenue, indicating moderate concentration.

Page last updated on: