RNA Therapeutics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

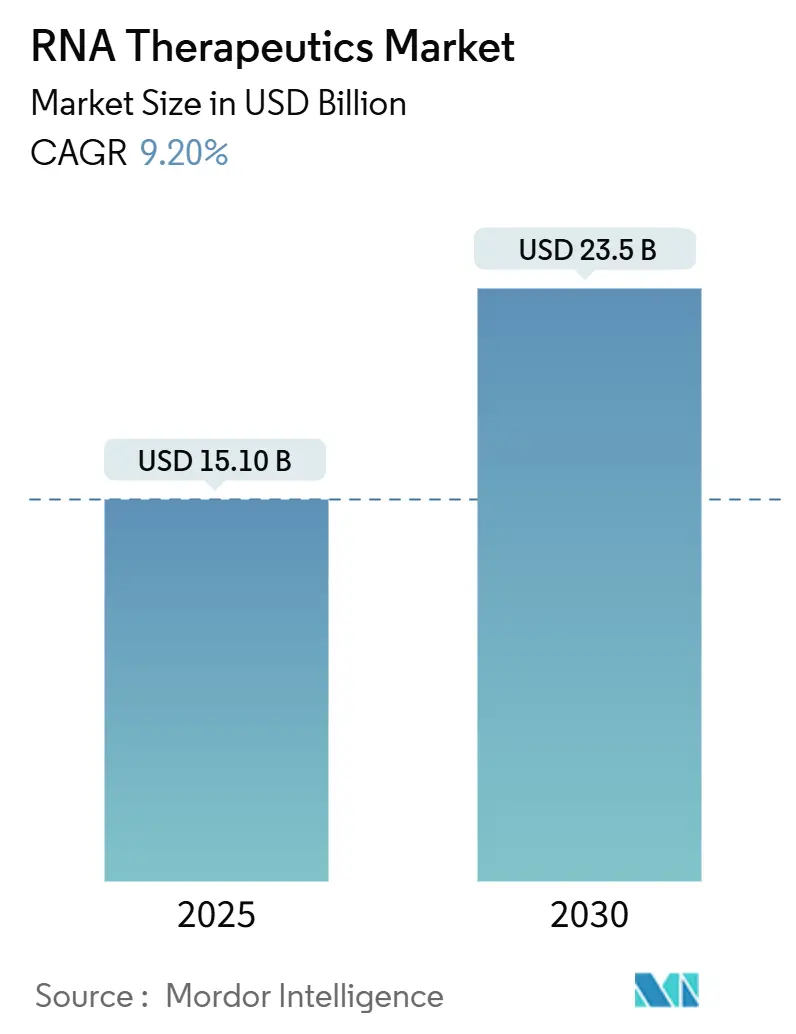

| Market Size (2025) | USD 15.10 Billion |

| Market Size (2030) | USD 23.5 Billion |

| Growth Rate (2025 - 2030) | 9.20% CAGR |

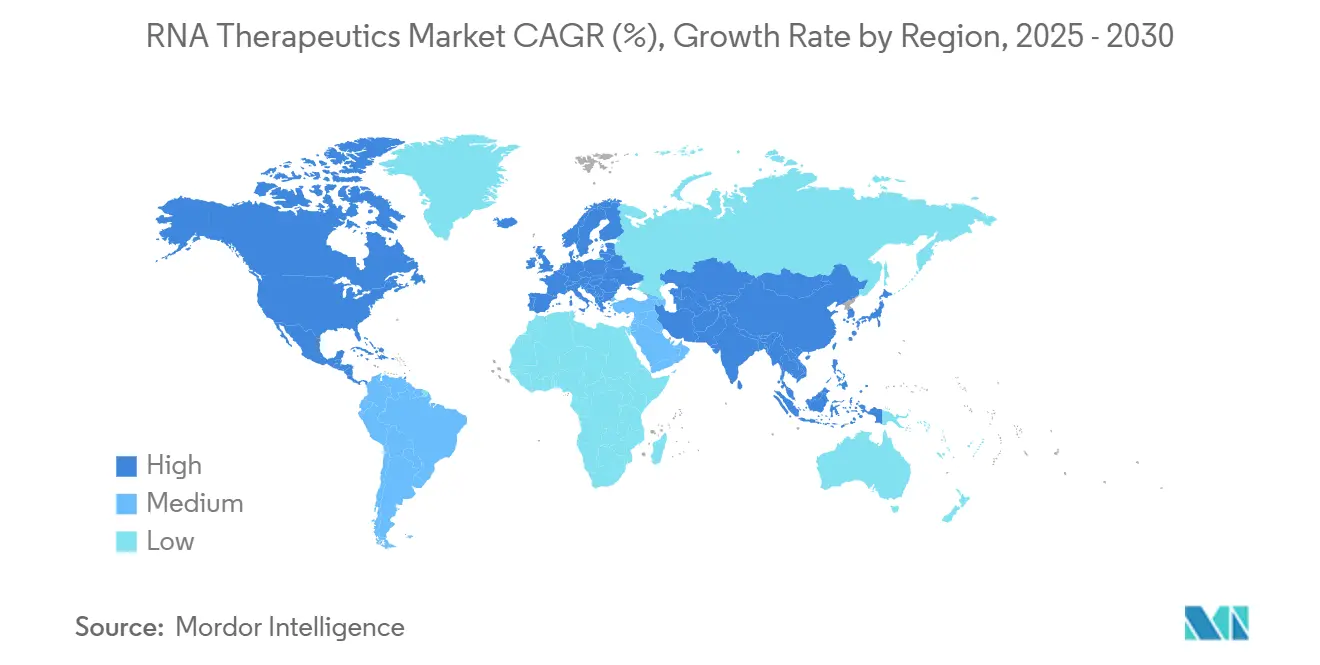

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RNA Therapeutics Market Analysis by Mordor Intelligence

The RNA therapeutics market size stood at USD 15.1 billion in 2025 and is forecast to reach USD 23.5 billion in 2030, translating into a 9.2% CAGR during the assessment period. Venture funding that accelerated after the pandemic has remained buoyant; Moderna alone secured USD 110 million in early-2025, while Stemirna raised almost USD 200 million, underscoring continued capital inflows that sustain pipeline expansion across oncology, rare diseases, and infectious indications. mRNA’s clinical validation has also shortened investor risk perception, pushing more pharmaceutical groups toward platform acquisitions and collaborations. Regulatory agencies have reinforced this momentum by issuing clearer oligonucleotide safety guidance and multiple fast-track designations, reducing development uncertainty. Manufacturing investments in the Asia Pacific are strengthening regional cost competitiveness, while AI-driven design tools cut discovery cycles and enhance delivery optimization, broadening the addressable patient base. Collectively, these factors position the RNA therapeutics market for sustained double-digit expansion as new modalities transition from proof-of-concept to commercial readiness.

Key Report Takeaways

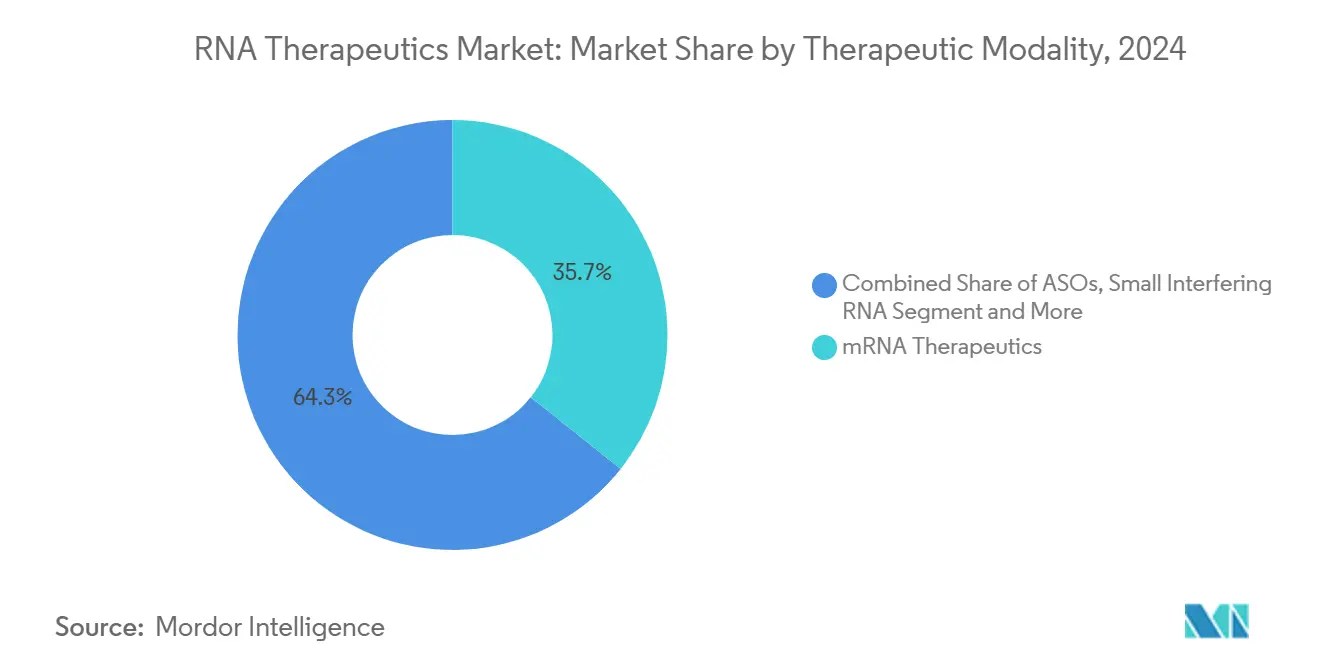

- By therapeutic modality, mRNA commanded 35.7% of the RNA therapeutics market share in 2024; self-amplifying RNA is on track to grow at a 22.5% CAGR through 2030.

- By application, oncology led with 34.2% revenue share of the RNA therapeutics market size in 2024 and is projected to advance at a 15.2% CAGR between 2025 and 2030.

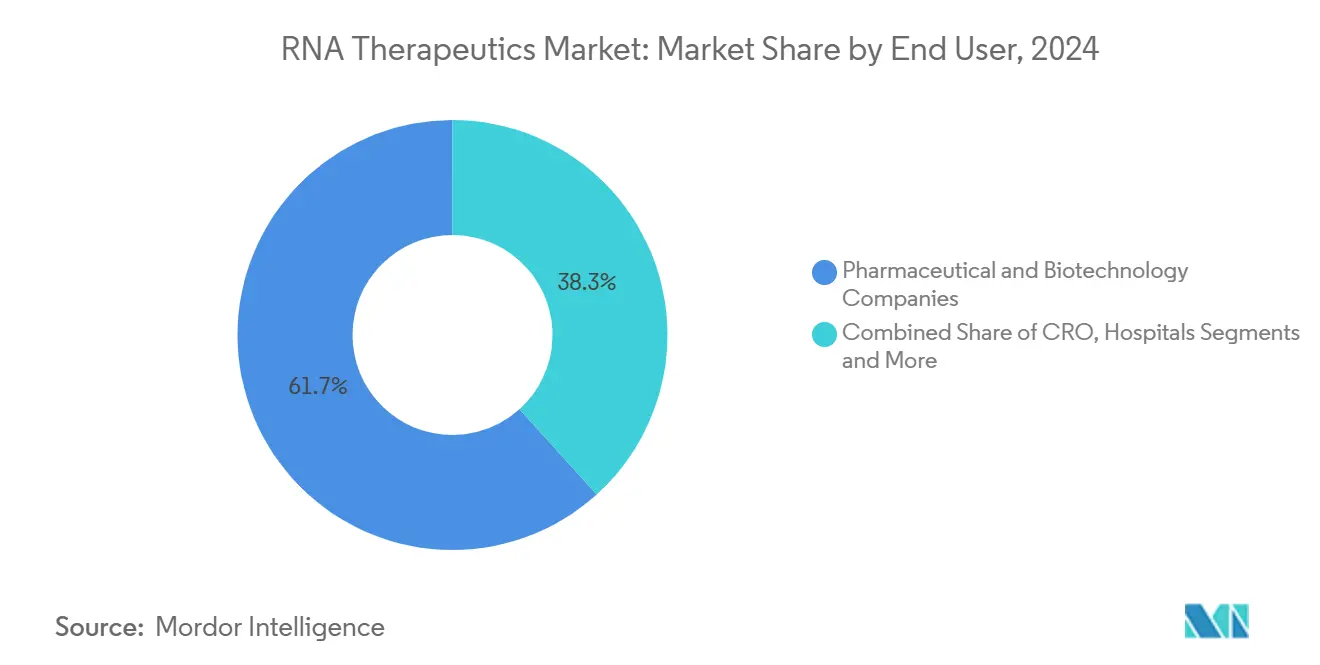

- By end user, pharmaceutical and biotechnology companies held 61.7% demand in 2024, whereas contract research organizations exhibit the highest growth at 9.8% CAGR to 2030.

- By geography, North America represented 36.2% revenue share in 2024, while the Asia Pacific is forecast to expand the fastest at 18.9% CAGR through 2030.

Global RNA Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream COVID-validated vaccine success drives mRNA platform funding | +2.10% | North America, Europe, global spillover | Medium term (2–4 years) |

| Patent-expiry cliff pushes pharma toward novel RNA modalities | +1.80% | North America, European Union, APAC spillover | Long term (≥ 4 years) |

| Accelerated FDA fast-track pathways for rare-disease RNA drugs | +1.40% | Global, led by U.S. precedents | Short term (≤ 2 years) |

| AI-assisted target discovery shortens RNA drug design cycle | +1.20% | Tech hubs in North America, EU, APAC | Medium term (2–4 years) |

| Low-cost self-amplifying RNA cuts dose and COGS by >70% | +1.90% | Global, strongest in cost-sensitive markets | Long term (≥ 4 years) |

| Expanding GMP lipid-nanoparticle CDMO capacity in APAC | +0.80% | APAC manufacturing hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Mainstream COVID-validated Vaccine Success Drives mRNA Platform Funding

The commercial proof delivered by mRNA COVID-19 vaccines repositioned RNA from an experimental tool to a mainstream therapeutic platform, catalyzing the largest financing rounds ever recorded in the field, such as ReNAgade’s USD 300 million Series A and Avidity Biosciences’ USD 345 million follow-on offering. More than 970 RNA programs were active globally by 2024, with accelerated trial enrollment reflecting heightened physician and patient confidence. Regulatory familiarity gained during the pandemic translated into faster review cycles for non-vaccine assets, reducing time-to-market pressure. Pharmaceutical strategists now treat RNA as an essential modality for pipeline diversification, especially in oncology and rare diseases, where the ability to express or silence any protein remains unmatched. Manufacturing investments piggyback on vaccine infrastructure, giving North America and Europe a near-term scale advantage while still benefiting emerging markets through technology transfer programs.

Patent-Expiry Cliff Pushes Pharma Toward Novel RNA Modalities

Blockbuster erosion is intensifying as patents on top-selling small molecules expire; RNA therapeutics shorten development timelines to roughly five years, making them ideal pipeline fillers for companies facing revenue gaps. High-value alliances such as Roche’s USD 1.8 billion RNA exon-editing deal exemplify corporate urgency to secure differentiated assets. Beyond speed, RNA modalities tackle undruggable targets, expanding therapeutic white space without requiring extensive medicinal chemistry campaigns. Regulatory clarity from recent FDA safety guidance further de-risks investment decisions, encouraging earlier-stage deals. This structural driver is expected to reinforce consolidation and licensing activity over the forecast horizon as traditional portfolios mature.

Accelerated FDA Fast-Track Pathways for Rare-Disease RNA Drugs

Dedicated U.S. programs like START and multiple fast-track designations have converged to compress regulatory timelines for orphan RNA assets; recent beneficiaries include RZ-001 for hepatocellular carcinoma and ACDN-01 for Stargardt disease.[1]Office of the Commissioner, “Support for Clinical Trials Advancing Rare Disease Therapeutics (START) Pilot Program,” FDA, fda.gov The agency’s supportive stance signals global regulators to harmonize review criteria, creating a predictable environment for developers targeting small patient populations. Reduced time and cost allow companies to pursue indications historically considered commercially marginal, expanding therapeutic reach. Patient-advocacy groups have also intensified pressure for rapid access, reinforcing the agency’s posture. Collectively, these factors enhance the RNA therapeutics market’s appeal to venture capital and strategic investors seeking earlier inflection points.

AI-Assisted Target Discovery Shortens RNA Drug Design Cycle

Deep-learning models such as MIT’s COMET and KAIST’s BInD automate lipid nanoparticle selection and in-silico design of candidates targeting 2,900 receptors without prior structural data, reducing discovery cycles from years to months.[2]Massachusetts Institute of Technology, “AI Model Predicts Better Nanoparticles for Efficient RNA Vaccine Delivery,” phys.org Computational workflows are particularly synergistic with RNA’s programmable nature, allowing rapid sequence iteration that traditional small molecules cannot match. Early adopters report lower attrition and better manufacturability profiles, translating to higher portfolio productivity. Strategic collaborations, including Daiichi Sankyo’s tie-up with Nosis Biosciences, illustrate the competitive advantage of integrating AI into RNA design pipelines. This driver should yield a steady stream of optimized candidates entering clinical testing over the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Endosomal escape inefficiency caps payload bioavailability | -1.60% | Global, acute in non-liver tissues | Long term (≥ 4 years) |

| Complex cold-chain logistics outside high-income markets | -1.10% | Africa, Latin America, rural Asia | Medium term (2–4 years) |

| Oligonucleotide synthesis capacity bottlenecks | -0.90% | Global, concentrated in specialized plants | Short term (≤ 2 years) |

| Geopolitical export-control risk on dual-use RNA tech | -0.70% | U.S.–China corridors, global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Endosomal Escape Inefficiency Caps Payload Bioavailability

Less than 10% of lipid-nanoparticle cargo typically reaches the cytosol, forcing higher doses that inflate manufacturing costs and amplify safety risks. While extracellular-vesicle–inspired designs and ionizable lipids have raised escape rates above 20% in preclinical models, robust clinical translation remains pending. The challenge is most severe in extrahepatic tissues, where existing tropism advantages are minimal. Companies funnel considerable R&D budgets into novel chemistries and biological vectors, yet the complexity of endosomal pathways suggests multi-year timelines before reliable breakthroughs emerge. Until then, delivery inefficiency will temper the overall RNA therapeutics market growth trajectory.

Complex Cold-Chain Logistics Outside High-Income Markets

Many RNA formulations still require storage at -80 °C, a specification that strains distribution networks in developing economies and rural regions. Supply gaps impede equitable access and slow revenue realization in high-population markets. Research collaborations, such as the GSK–Imperial College initiative to create room-temperature-stable formulations, demonstrate technical progress but remain in early clinical stages.[3]Navta Hussain, “GSK and Imperial to Eliminate Costly Cold-Chain Storage of RNA Vaccines,” Imperial College London, imperial.ac.uk Until thermostable products scale, manufacturers must invest in ultra-cold infrastructure or accept restricted market reach, keeping near-term penetration skewed toward high-income geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Modality: mRNA Dominance Faces saRNA Disruption

Messenger RNA retained a 35.7% share of the RNA therapeutics market in 2024, benefitting from first-mover status and established vaccine supply chains. The RNA therapeutics market size for mRNA assets is projected to expand steadily on the back of cancer vaccines and enzyme-replacement applications that leverage existing manufacturing blueprints. Antisense oligonucleotides maintain durable revenues as illustrated by Spinraza, confirming patient and payer acceptance of RNA interventions in rare neurological diseases.

Self-amplifying RNA, although holding a smaller baseline, is forecast to post a 22.5% CAGR through 2030, reflecting superior dose-economics that can lower per-patient treatment cost by more than 70%. Small-interfering RNA continues to broaden its clinical footprint beyond hepatic targets, demonstrated by Amvuttra’s cardiomyopathy approval, and analysts expect label extensions to diversify revenue streams. Aptamers and microRNA agents remain niche, constrained by delivery and off-target concerns, yet ongoing platform engineering may unlock higher-value indications. Competitive dynamics increasingly favor companies building multi-modality portfolios that hedge technical risk while maximizing disease coverage.

By Application: Oncology Leadership Across Growth Metrics

Oncology captured 34.2% of 2024 revenues, underscoring RNA’s capacity to encode patient-specific neoantigens and silence oncogenic drivers simultaneously. The segment is advancing at a 15.2% CAGR thanks to immuno-oncology synergies, including mRNA-enhanced CAR-T processes that raise cell-therapy persistence. The RNA therapeutics market is poised to benefit further from basket trials that enroll across tumor types using shared molecular signatures, accelerating statistical readouts and regulatory submissions.

Genetic disorder programs remain the second-largest bucket, leveraging splice-modulating chemistries that demonstrate clinically meaningful, often curative, effects with limited dosing frequency. Infectious-disease pipelines remain active beyond COVID-19, targeting universal flu and rapid pandemic response templates that can enter clinical testing within 100 days of pathogen sequencing. Cardiovascular and metabolic disorders show promise through liver-targeted siRNA knockdown of circulating proteins, while neurological applications strive to overcome blood–brain-barrier hurdles using receptor-mediated transport vectors.

By End User: Pharma Concentration Amid CRO Acceleration

Pharmaceutical and biotech enterprises accounted for 61.7% of global demand in 2024, reflecting the integrated capabilities required to shepherd complex RNA assets from discovery to commercialization. These firms view RNA platforms as strategic levers to offset small-molecule patent cliffs and diversify therapeutic risk. The RNA therapeutics market size attributable to contract research organizations is smaller but growing at 9.8% CAGR as sponsors outsource analytics, toxicology, and specialized formulation tasks to accelerate timelines.

Academic centers continue to supply early-stage innovation and license technology outward once translational milestones are met, while hospital networks primarily function as administration sites rather than procurement hubs. The rising complexity of delivery science is prompting hybrid engagement models where CROs embed directly within sponsor teams, providing end-to-end support from oligonucleotide synthesis to regulatory dossier compilation.

Geography Analysis

North America retained a 36.2% share in 2024 owing to FDA pathway familiarity, venture capital depth, and clustering of GMP manufacturing, which jointly lowers onboarding friction for new entrants. The region also houses most AI-drug-design pioneers, accelerating candidate throughput and reinforcing its leadership. Asia Pacific is projected to register an 18.9% CAGR as governments underwrite facility build-outs; ST Pharm’s USD 126 million oligonucleotide expansion and Australia’s Aurora Biosynthetics launch exemplify commitments to localize supply.

European Union markets benefit from harmonized regulatory frameworks and seasoned CDMO networks, yet Brexit-related realignments have shifted some trial and manufacturing activity toward continental hubs.

Middle East & Africa and South America remain opportunity pockets constrained by cold-chain limitations; targeted technology-transfer initiatives and modular fill-finish installations aim to alleviate access gaps. Geopolitical export controls introduced in January 2025 add compliance layers for U.S.–China corridors, nudging multinational sponsors toward dual-sourcing to protect supply continuity.

Competitive Landscape

The RNA therapeutics market sits at a moderate concentration level where early vaccine titans coexist with a long tail of modality specialists. Moderna and BioNTech continue to dominate revenue through pandemic legacy assets and oncology pipeline breadth, while Alnylam and Ionis leverage rare-disease franchises that deliver predictable cash flows. Emerging challengers differentiate via delivery innovations, such as circular RNA constructs that improve expression duration and reduce innate-immune activation; RiboX’s RXRG001 became the first circular asset to secure clinical clearance in late 2024.

Strategic alliances accelerate capability building: Merck partnered with Orna Therapeutics for circular RNA in March 2025, Roche licensed Ascidian’s exon-editing platform, and Evonik allied with ST Pharm to integrate LNP production with oligonucleotide synthesis. AI-centric start-ups, backed by large language models and genomics data lakes, court big-pharma equity to scale wet-lab validation. Patent filings reveal a race toward extrahepatic delivery and endosomal-escape optimization, suggesting that near-term differentiation will hinge on tissue access rather than payload chemistry.

Long-term consolidation is expected as capital intensity grows and regulatory expectations heighten, prompting smaller players either to specialize in platform niches or enter acquisition pathways. However, innovation velocity and diverse modality options ensure sustained competitive dynamism, preventing any single entity from locking out newcomers.

RNA Therapeutics Industry Leaders

Moderna

BioNTech

Alnylam Pharmaceuticals

Ionis Pharmaceuticals

Sarepta Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Merck entered a strategic collaboration with Orna Therapeutics to accelerate circular RNA platforms.

- February 2025: Alnylam secured FDA approval for Amvuttra label expansion into transthyretin amyloid cardiomyopathy.

- November 2024: RiboX’s RXRG001 became the first circular RNA therapy cleared for clinical evaluation in radiation-induced xerostomia.

- November 2024: City Therapeutics launched with USD 135 million Series A funding to advance targeted RNAi pipelines.

Global RNA Therapeutics Market Report Scope

| Antisense Oligonucleotides |

| Small Interfering RNA (siRNA) |

| MicroRNA (miRNA) Therapeutics |

| Messenger RNA (mRNA) Therapeutics |

| RNA Aptamers |

| Oncology |

| Genetic Disorders |

| Infectious Diseases |

| Cardiovascular & Metabolic Diseases |

| Neurological Disorders |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutions |

| Contract Research Organizations |

| Hospitals & Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Modality | Antisense Oligonucleotides | |

| Small Interfering RNA (siRNA) | ||

| MicroRNA (miRNA) Therapeutics | ||

| Messenger RNA (mRNA) Therapeutics | ||

| RNA Aptamers | ||

| By Application | Oncology | |

| Genetic Disorders | ||

| Infectious Diseases | ||

| Cardiovascular & Metabolic Diseases | ||

| Neurological Disorders | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutions | ||

| Contract Research Organizations | ||

| Hospitals & Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the RNA therapeutics market?

The RNA therapeutics market size reached USD 15.0 billion in 2025.

How fast is the field expected to grow toward 2030?

Revenue is projected to expand at a 9.2% CAGR, reaching USD 23.5 billion by 2030.

Which therapeutic modality leads revenue today?

Messenger RNA holds the largest share at 35.7%, supported by robust manufacturing infrastructure.

Which region is growing the fastest?

Asia Pacific is forecast to register an 18.9% CAGR through 2030, driven by new GMP manufacturing capacity.

What major technical hurdle limits broader adoption?

Endosomal escape inefficiency restricts cytosolic delivery, capping payload bioavailability to under 10%.

How are regulators supporting rare-disease programs?

The FDA grants fast-track and orphan designations under initiatives such as the START Pilot Program, shortening development timelines.

Page last updated on: