Manual Resuscitator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

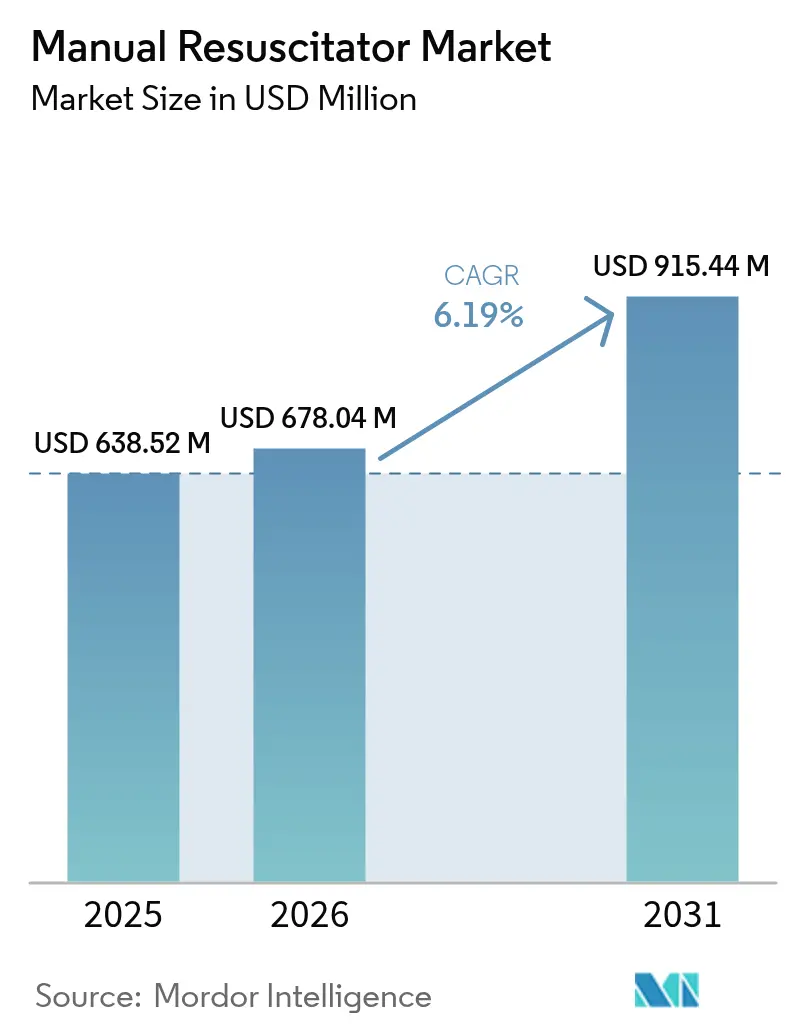

| Market Size (2026) | USD 678.04 Million |

| Market Size (2031) | USD 915.44 Million |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

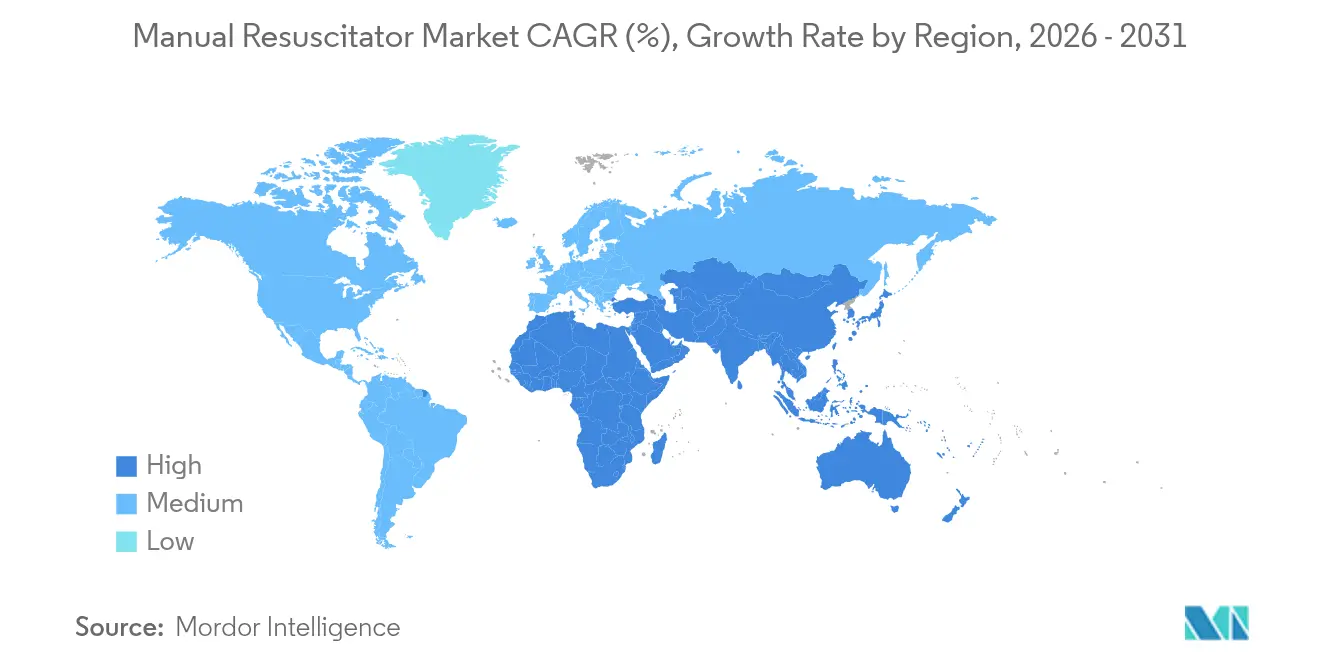

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Manual Resuscitator Market Analysis by Mordor Intelligence

The Manual Resuscitator Market size in 2026 is estimated at USD 678.04 million, growing from 2025 value of USD 638.52 million with 2031 projections showing USD 915.44 million, growing at 6.19% CAGR over 2026-2031.

Rising prevalence of chronic respiratory diseases, persistent levels of out-of-hospital cardiac arrest, and broader adoption of disposable devices continue to underpin momentum. Demand benefits from technology that blends integrated pressure monitoring with positive end-expiratory pressure (PEEP) control, a combination that helps limit ventilation-induced lung injury in vulnerable patients. Post-pandemic infection-control protocols are accelerating the shift to single-use systems, while military and wilderness medicine programs elevate procurement in non-hospital settings. Competitive rivalry remains moderate: incumbents rely on material innovation, small-form connectivity features and targeted acquisitions to widen their respiratory-care portfolios and protect margins in the expanding manual resuscitator market.

Key Report Takeaways

- By product type, self-inflating bags accounted for 46.28% of the manual resuscitator market share in 2025, whereas T-piece resuscitators are projected to log an 8.28% CAGR through 2031.

- By usage, disposable units held 55.78% of the manual resuscitator market size in 2025 and are forecast to grow at a 9.22% CAGR, outpacing reusable counterparts.

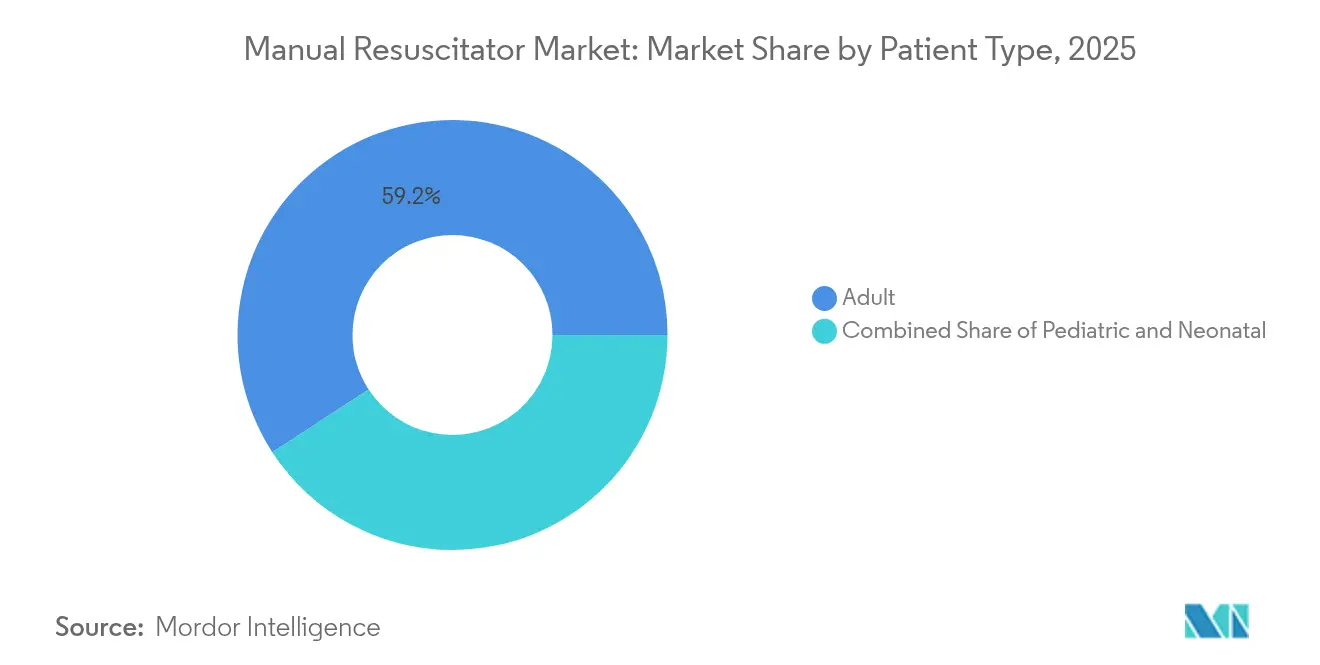

- By patient type, adult applications represented 59.18% revenue share in 2025, while neonatal demand is expected to climb at a 9.68% CAGR to 2031.

- By material, silicone components captured 45.12% share in 2025 and are expanding at a 10.73% CAGR on the back of superior durability and biocompatibility.

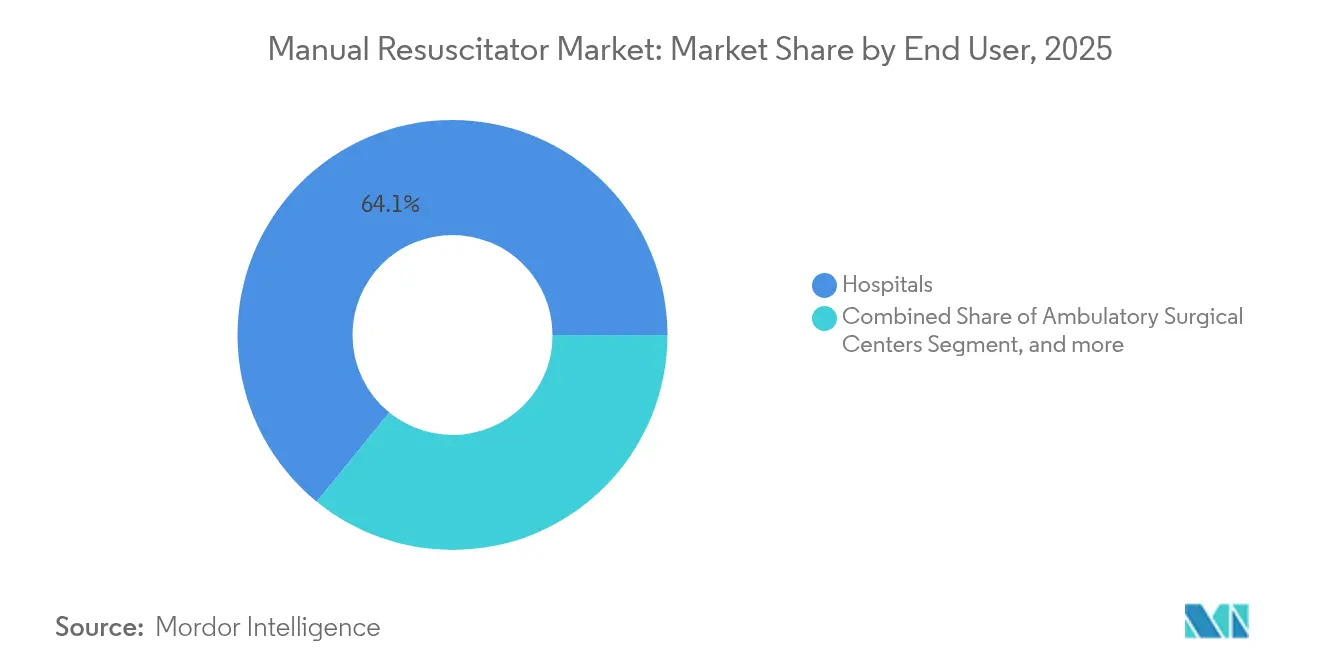

- By end user, hospitals maintained 64.12% share in 2025; specialty clinics are poised for the fastest 6.24% CAGR as outpatient surgical volumes rise under updated CMS preparedness rules.

- By geography, North America represented 37.95% revenue share in 2025, while Asia Pacific is expected to climb at a 8.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Manual Resuscitator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of COPD & Other Chronic Respiratory Diseases | +1.8% | Global, highest in APAC and Americas | Long term (≥ 4 years) |

| Rising Incidence of Sudden Cardiac Arrest Requiring BVM Support | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Increasing Geriatric Population & Home-Care Respiratory Demand | +1.0% | North America, Europe, Japan | Long term (≥ 4 years) |

| Steady Advancements in Integrated Pressure-Monitoring & PEEP Valves | +0.8% | Global, led by US and EU innovation hubs | Medium term (2-4 years) |

| Post-COVID Infection-Control Shift Toward Single-Use Resuscitators | +0.6% | Global, accelerated in healthcare-conscious regions | Short term (≤ 2 years) |

| Growing Adoption in Wilderness, Military & Veterinary Emergency Training | +0.4% | North America, Europe, military deployment zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of COPD and Other Chronic Respiratory Diseases

Low- and middle-income nations carry the heaviest mortality load, hindered by limited screening and late intervention. Tobacco use explains 34.8% of COPD-related disability-adjusted life years, while ambient particulate matter accounts for 22.2%. Escalating respiratory emergencies across Asia-Pacific have moved manual resuscitators into essential bridge-therapy kits, especially for intra-facility transport. Acute exacerbations often outstrip mechanical ventilator availability, cementing the manual resuscitator market as a frontline solution.

Rising Incidence of Sudden Cardiac Arrest Requiring BVM Support

Roughly 356,000 Americans experience out-of-hospital cardiac arrest each year, with survival rates near 10%.[1]Sudden Cardiac Arrest Foundation, “Out-of-Hospital Cardiac Arrest Statistics,” sca-foundation.org The American Heart Association’s 2030 target to lift bystander CPR rates above 50% implicitly raises demand for bag-valve-mask (BVM) devices that sustain oxygenation during the critical first minutes.[2]American Heart Association, “2023 Heart Disease and Stroke Statistics,” heart.org United Kingdom ambulance services manage approximately 30,000 resuscitation attempts annually, achieving return-of-spontaneous-circulation in 30% of cases. Guidelines for athletic venues, where prompt ventilation assists neurological outcomes in young athletes, further broaden the manual resuscitator market. Pandemic-era infection-control measures boosted adoption of single-use resuscitators fitted with high-efficiency particulate air filters to protect rescuers.

Increasing Geriatric Population and Home-Care Respiratory Demand

Adults aged 65 years and older already represent 19% of the United States population, and similar trends are visible across Europe and Japan. Age-linked comorbidities heighten susceptibility to acute respiratory events, prompting greater allocation of emergency equipment in long-term-care facilities. Home-based non-invasive ventilation programs often pair portable oxygen concentrators with manual resuscitators for contingency planning. Insurance reimbursement schemes in Germany and Japan that fund home care devices reinforce steady flow into the manual resuscitator market. Suppliers are responding with compact, ergonomic bags featuring antimicrobial silicone and intuitive pressure gauges that support caregiver use outside hospital settings.

Steady Advancements in Integrated Pressure-Monitoring and PEEP Valves

Smart sensors now embed inside manual resuscitators, offering real-time tidal-volume and rate feedback that raises ventilation accuracy. Ambu data show PEEP valves can hold set pressure despite 80% mask leak vital for newborn lungs.[3]Anna-Karin Larsson et al., “Performance of PEEP Valves in Neonatal Resuscitation,” karger.com T-piece systems deliver more consistent peak inspiratory pressure than self-inflating bags, explaining their higher growth rate. Connectivity features that upload performance metrics to quality-assurance dashboards close the training gap for first responders. Hospitals that standardize on pressure-monitored bags report fewer barotrauma incidents, reinforcing product differentiation across the expanding manual resuscitator market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Alternative Ventilation Solutions | -0.9% | Global, more pronounced in high-tech markets | Medium term (2-4 years) |

| Price Sensitivity in Low- & Middle-Income Markets | -0.7% | APAC emerging markets, Africa, Latin America | Long term (≥ 4 years) |

| Environmental Pushback Against Disposable Plastics & Upcoming EU MDR Documentation | -0.5% | Europe, expanding to other developed regions | Long term (≥ 4 years) |

| Skill-Gap & Inadequate Hands-On Training for Optimal BVM Use | -0.3% | Global, acute in resource-limited settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Ventilation Solutions

High-flow nasal cannula systems and portable non-invasive ventilators provide oxygenation with lower aerosol risk, decreasing reliance on manual bags in some intensive-care algorithms. Mechanical chest-compression devices relieve rescuer fatigue but also shorten the window in which bag ventilation is prioritized. Wider placement of automated external defibrillators reorders the rescue sequence, potentially curbing first-line BVM use. Video laryngoscopes and supraglottic airways offer faster airway control, though manual resuscitators remain indispensable for pre-oxygenation and post-intubation support. Device makers therefore emphasize add-on features rather than raw volume growth to defend the manual resuscitator market.

Price Sensitivity in Low- and Middle-Income Markets

Procurement budgets in parts of Africa, Latin America and emerging Asia often favor basic reusable bags over premium systems with pressure monitors. Import tariffs and fragmented distribution inflate landed costs, making local assembly attractive yet technically challenging. Training shortfalls add indirect expense when devices are under-utilized. Development agencies occasionally donate equipment, but inconsistent after-sales support can hinder sustained use. These economics explain why price tension trims expected CAGR for the manual resuscitator market in budget-constrained regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: T-piece Innovation Strengthens Neonatal Care

Self-inflating bags controlled the largest slice of the manual resuscitator market in 2025 at 46.28%, owing to versatility and independence from gas outlets. T-piece devices, however, are positioned for the most rapid 8.28% CAGR through 2031, supported by evidence that they deliver steadier PEEP across variable lung compliance. Military medics and ambulance crews keep favoring self-inflating bags because of ruggedness and minimal setup. Yet tertiary hospitals increasingly specify T-piece systems for deliveries and pediatric intensive-care units, reflecting policy that demands lung-protective ventilation from the first breath.

Enhanced pressure control and sensor feedback spur premium pricing, which contributes to revenue expansion even as unit volumes stay balanced. Training curricula now incorporate simulations for both technologies, ensuring skill retention among clinicians and paramedics. These contrasting adoption patterns demonstrate why product diversity remains central to competitiveness within the manual resuscitator market.

By Usage: Disposable Uptake Outruns Reusable Platforms

Disposable units represented 55.78% of 2025 revenue and show the fastest 9.22% CAGR thanks to tightened infection-control rules after COVID-19. Hospitals cite reduced turnaround time and elimination of reprocessing error as prime benefits. Sterile packaging also permits field deployment without auxiliary clean-room supplies, appealing to military and humanitarian missions.

Reusable bags keep relevance in teaching labs and resource-constrained clinics where cost per use is decisive. Ambu’s Mark IV, validated for 30 autoclave cycles, exemplifies value over multiyear horizons. The European Union now permits reprocessing of single-use devices under strict validation, creating a niche that straddles disposable and reusable categories. Even so, legal liability and traceability hurdles limit uptake, ensuring disposables retain growth leadership in the manual resuscitator market.

By Patient Type: Neonatal Segment Sets the Growth Pace

Adult applications occupied 59.18% of sales in 2025 because cardiovascular emergencies predominantly involve older populations. Neonatal devices, however, will register a leading 9.68% CAGR as birth asphyxia prevention gains traction in low-income regions. Programs such as Helping Babies Breathe equip rural clinics with self-inflating bags fitted with pressure-relief valves that reduce barotrauma risk.

Pediatric demand maintains a mid-single-digit trajectory, sustained by school-based emergency drills and sports league requirements. The differential growth pattern underscores how targeted fund-raising and multilateral health initiatives can tilt sub-segment dynamics yet still keep the broader manual resuscitator market on a balanced path.

By Material: Silicone Leads on Performance and Sustainability

Silicone achieved 45.12% share in 2025 and is expanding at a 10.73% CAGR. Its thermal stability, transparency and elasticity allow repeated sterilization without cracking or loss of tactile feedback. Biocompatibility reassures clinicians worried about hypersensitivity associated with latex or certain phthalate-plasticized PVC formulations.

PVC remains attractive for cost-sensitive buyers, though regulatory scrutiny of disposable plastics pushes suppliers toward bio-based compounds. Ambu has committed to cutting Scope 1 and 2 emissions by 75% before 2030 and is piloting bioplastic housings that retain mechanical strength. Rubber and niche polymers fill specialized roles where anti-static or oil-resistant properties are critical. Material science therefore continues to differentiate offerings in the manual resuscitator market.

By End User: Specialty Clinics Gain Ground

Hospitals controlled 64.12% of revenue in 2025 given their round-the-clock emergency care obligations. Specialty clinics, however, are forecast to rise at a 6.24% CAGR as outpatient surgery volumes climb under value-based care models. Updated CMS rules now oblige ambulatory centers to stock resuscitation equipment and train staff in BVM use, directly enhancing demand.

Veterinary hospitals represent an emerging niche after 2024 CPR guidelines emphasized tight-fitting masks to mitigate zoonotic transmission. Home-health agencies also procure compact bags for ventilator-dependent patients as part of disaster planning kits. These diverse channels together fortify distribution reach across the manual resuscitator market.

Geography Analysis

North America led with 37.95% revenue share in 2025 on the strength of advanced emergency medical services, extensive CPR training networks and sizeable defense procurement. Tactical Combat Casualty Care protocols credit manual ventilation with helping curb preventable battlefield deaths, which sustains steady military orders. Consistent funding permits hospitals to invest in sensor-enabled bags that streamline quality audits.

Asia-Pacific is poised for the most vigorous 8.71% CAGR to 2031 as China, India and Southeast Asian states fund trauma centers and pre-hospital care expansion. Public insurance schemes in China now reimburse neonatal resuscitation consumables, and India’s Ayushman Bharat program allocates capital budgets for ambulance upgrades. In affluent markets such as Japan and South Korea, healthy aging policies spur procurement for home-care and long-term-care facilities, broadening exposure for the manual resuscitator market.

Europe maintains a mature but resilient trajectory. Pending 2026 rules that require recyclable packaging stir process innovation, while EU Medical Device Regulation 2017/745 opens a pathway for controlled reprocessing. Germany, United Kingdom and France drive volume, while Spain and Italy favor premium silicone models for neonatal wards. Latin America, the Middle East and Africa post mid-single-digit growth: Brazil’s SAMU ambulance network and South Africa’s urban EMS upgrades illustrate incremental gains, yet economic volatility and supply-chain constraints restrain faster penetration.

Regulatory Landscape

Manual resuscitators are regulated as medical devices, with jurisdiction-specific premarket and quality-system requirements. In the United States, they are generally Class II devices (21 CFR 868.5915), typically marketed via FDA 510(k) clearance and aligned to FDA-recognized consensus standards. Recent examples include 510(k) clearances for Compact Medicals butterflyBVM (April 2025) and Laerdals The BAG manual resuscitator and accessories (November 2025). From February 2026, FDAs Quality Management System Regulation (QMSR) became effective, tightening expectations around lifecycle documentation, design controls, and supplier quality practices for manufacturers serving US channels.

Internationally, technical compliance is anchored by standards such as ISO 10651-4:2023 (user-powered resuscitators across age groups), which updates the prior 2002 edition and drives test-plan and technical-file revisions for global portfolios. In Europe, manual resuscitators fall under Regulation (EU) 2017/745 (MDR) (often Class IIa), requiring conformity assessment and ongoing post-market surveillance. Companies have been publishing MDR-aligned conformity documentation for product lines such as Ambus SPUR II. Alongside infection-control and single-use adoption, the documentation burden and notified-body throughput under MDR influence time-to-market, labeling, and traceability choices across reusable and disposable offerings.

Competitive Landscape

Competition is moderate, with the top five vendors estimated to hold significant global revenue. Ambu A/S defends its leadership through iterative design, such as the SPUR II single-use bag that pairs textured grips with transparent housing for secretion checks. Q1 2025 organic sales rose 19.5%, funding R&D into bioplastics and pressure-sensor integration.

Medtronic’s USD 110 million purchase of Aircraft Medical in 2024 added video laryngoscope capability, complementing existing resuscitation offerings. Teleflex expanded its emergency portfolio with the July 2025 acquisition of BIOTRONIK’s vascular unit, giving the company fresh cross-selling channels. Smiths Medical advances connectivity via its Pneupac Ventil™ BVM, which records ventilation metrics for later debrief.

Smaller firms navigate niches: Vyaire Medical targets anesthesia departments with hyper-low-dead-space bags, while BLS Systems cater to military buyers with chemically resistant silicone. Environmental stewardship now shapes tenders; suppliers showcasing life-cycle analysis and reduced greenhouse-gas footprints gain points under European value-based procurement rules. The aggregate picture underscores a manual resuscitator market where innovation, sustainability and portfolio breadth outweigh price alone.

Manual Resuscitator Industry Leaders

Vyaire Medical Inc.

Ambu A/S

Teleflex Inc.

HUM GmbH

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procurement pull-through is strongest where large provider networks standardize emergency respiratory consumables, leaving room for suppliers that can secure broad contracting access and provide complete accessory sets (masks, filters, PEEP valves, manometers). A specific indicator is Mercury Medicals award of a Vizient contract for its Disposable Manual Resuscitators and Accessories portfolio, effective February 1, 2026, which supports formulary adoption across participating US hospitals and can accelerate conversion to single-use kits aligned with infection-control workflows.

Product differentiation is most visible in measurable ventilation performance, training support, and compatibility with adjacent airway and transport ecosystems. Compliance to updated performance requirements (ISO 10651-4:2023) and connector standards (ISO 5356-1:2015), along with materials-safety expectations (e.g., ISO 10993 biocompatibility and ISO 18562 gas-path evaluation), raises demand for documented, standardized designs that simplify hospital validation and cross-site deployment. Within this framework, manufacturers can compete by packaging pressure monitoring and PEEP control into disposable-friendly formats, offering neonatal-focused configurations, and aligning portfolios to pre-hospital and intra-facility transport use cases where clinical teams want consistent, auditable bagging performance across settings.

Recent Industry Developments

- April 2026: Ambu received CE Mark for its full SureSight video laryngoscope portfolio in Europe. The broadened airway visualization platform supports resuscitation workflows where intubation and manual ventilation are paired, and it strengthens Ambus ability to bundle airway and ventilation solutions for hospital and EMS tenders.

- September 2025: The US FDA posted a Class I recall for certain Ambu SPUR II manual resuscitators tied to a blocked manometer port. The action increased scrutiny on pressure-monitoring reliability in bag-valve-mask devices and can shift provider preferences toward designs with clearer verification and quality documentation.

- February 2025: Ambu and Archeon Medical announced a collaboration for distribution of EOlife and EOlifeX manual ventilation systems. The partnership expanded route-to-market coverage for manual ventilation platforms and supported portfolio breadth in segments emphasizing controlled ventilation and training-oriented use.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the manual resuscitator market covers hand-operated ventilation devices (commonly used as bag valve mask systems) that deliver assisted breathing in emergency and clinical care, and the value is measured as manufacturer and distributor revenue in USD.

Scope exclusions: We exclude mechanical ventilators, CPAP or BiPAP devices, and automated CPR systems because they are not manual ventilation tools.

Segmentation Overview

- By Product Type

- Self-Inflating Bags

- Flow-Inflating Bags

- T-Piece Resuscitators

- By Usage

- Disposable

- Reusable

- By Patient Type

- Adult

- Pediatric

- Neonatal

- By Material

- Silicone

- PVC

- Rubber & Others

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Speciality Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on demand triggers, care settings, and procurement behavior for resuscitation equipment. We typically refer to public sources such as the World Health Organization, US FDA databases and safety communications, CDC publications, and the World Bank for macro health indicators. We also use sources like UN Comtrade for trade direction checks and peer reviewed journals for usage patterns across adult and neonatal care.

To translate those signals into a market model, we also review annual reports, investor presentations, product catalogs, and tender portals from public buyers where available, and then map these to the main care sites (hospitals, emergency medical services, and ambulatory settings). We additionally reference a paid subscription focused on company financials and another one used for patent searches to validate company exposure and product activity, especially when public disclosures are limited. These desk sources are not exhaustive, and many other public documents were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions are used to pressure test unit demand, pricing movement, and the split between disposable and reusable products in different care pathways. We speak with a mix of manufacturers, distributors, clinicians, and procurement roles, and then we validate region-level assumptions across APAC, EMEA, and the Americas so one geography does not over-influence the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 21% | APAC: 45% |

| Mid tier: 50% | Functional/Unit leaders: 35% | EMEA: 29% |

| Smaller Players: 21% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach that reconstructs the demand pool from emergency care activity and respiratory event burden, and then it is translated into annual device needs using usage rates by care setting. To keep the output realistic, we corroborate the totals with selective bottom-up approximations, such as sampled ASP times estimated unit volumes from channels, and supplier and distributor cross-checks, and then adjustments are made where the two views do not align.

Inputs used in the model include ambulance and emergency department case volumes, hospital procedure intensity where ventilation support is common, the disposable versus reusable mix, average selling price ranges by material and configuration, and replacement and stocking cycles in EMS and hospitals. When country data is missing, gaps are handled through proxy indicators (for example, similar health system capacity and emergency response coverage) and the assumptions are re-tested in primary calls.

For forecasting, scenario analysis is used to reflect uncertainty around healthcare spending, emergency preparedness cycles, and infection control preferences that can shift the disposable mix. The scenario paths are anchored to expert consensus on near-term volume growth and a practical view of price progression rather than sharp step changes.

Data Validation & Update Cycle

Outputs are checked against independent signals such as regional procurement patterns, trade directionality, and reported category growth from public sources, and then major variances are investigated before final sign-off. We also run anomaly checks on implied unit volumes, ASP bands, and growth rates so the market does not expand in a way that contradicts the real demand drivers.

Reviews happen in multiple steps, with a second analyst re-checking assumptions and calculations, followed by a final consistency pass across regions and use cases. The report is refreshed annually, and interim updates are triggered when there are material events like major regulatory actions, supply disruptions, or sudden changes in emergency care utilization. Before delivery, a fresh review is completed so clients receive the latest updated view.

Mordor Intelligence's Manual Resuscitator Market Size Compared Against Other Published Estimates

Published estimates for manual resuscitators often do not match because the scope can be defined differently, the base year can shift, and pricing and volume assumptions can be refreshed at different times. Even small choices, like whether accessories and adjacent resuscitation tools are counted, can change the total once applied across regions.

A common gap driver is that some sources mix the broader resuscitation device space into their calculations or apply broad pricing uplifts without anchoring them to procurement behavior by care setting. For Mordor Intelligence, only manual resuscitators are counted and the model is tied to demand indicators like emergency care activity and the disposable versus reusable split, which are then re-validated through interviews before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 678.04 M (2026) | |

| Global Research Publisher A | USD 569.10 M (2024) | Uses an earlier base year and can land lower if price updates and post-2024 EMS and hospital replenishment cycles are not fully reflected in the sizing assumptions. |

| Industry Publisher B | USD 600.08 M (2025) | Often presented as a near-term estimate with limited visibility into mix shifts between disposable and reusable products, which can understate value when higher-priced configurations gain share. |

Across the three figures, the spread is largely explained by base-year selection and how pricing and product mix are refreshed, rather than a disagreement that the category is growing. By keeping the scope tight to manual devices and then checking volumes and ASP ranges against real purchasing patterns, the sizing steps stay traceable and repeatable for users reviewing the assumptions.

Key Questions Answered in the Report

What is the value of the manual resuscitator market in 2026?

It is valued at USD 678.04 million and is forecast to hit USD 915.44 million by 2031.

Which product type is growing fastest within manual resuscitators?

T-piece resuscitators are projected to post the highest 8.28% CAGR through 2031.

Why are disposable manual resuscitators gaining traction?

Post-COVID infection-control standards favor single-use devices that eliminate reprocessing risks and save turnaround time.

Which region offers the highest growth opportunity?

Asia-Pacific shows the fastest 8.71% CAGR thanks to large populations, rising healthcare spending and EMS infrastructure upgrades.

What material dominates premium manual resuscitator models?

Silicone leads with 45.12% share and a 10.73% CAGR due to durability and biocompatibility.

Page last updated on: