Morocco Poultry Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.08 Billion |

| Market Size (2026) | USD 4.27 Billion |

| Market Size (2031) | USD 5.39 Billion |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Morocco Poultry Market Analysis by Mordor Intelligence

The Morocco poultry market size is expected to grow from USD 4.08 billion in 2025 to USD 4.27 billion in 2026 and is forecast to reach USD 5.39 billion by 2031 at 4.75% CAGR over 2026-2031. Robust domestic demand, supportive government programs, and Morocco’s gateway location between Europe and West Africa underpin expansion. Rising disposable incomes, expanding urban populations, and a steady shift toward protein-rich diets are encouraging higher per-capita chicken and egg consumption. Consumer preferences are increasingly shifting toward convenient processed poultry products, such as nuggets, sausages, and marinated items, creating opportunities for enhanced product diversification and innovation. Rapid investment in cold-chain logistics and processing plants is enabling producers to deliver differentiated, value-added products that capture higher margins. Integrated operators are responding to volatility in global feed prices by investing in grain storage and forward-contracting strategies. Meanwhile, regulatory tightening by the National Office for Food Safety (ONSSA) is improving export readiness and stimulating adoption of international quality standards.

Key Report Takeaways

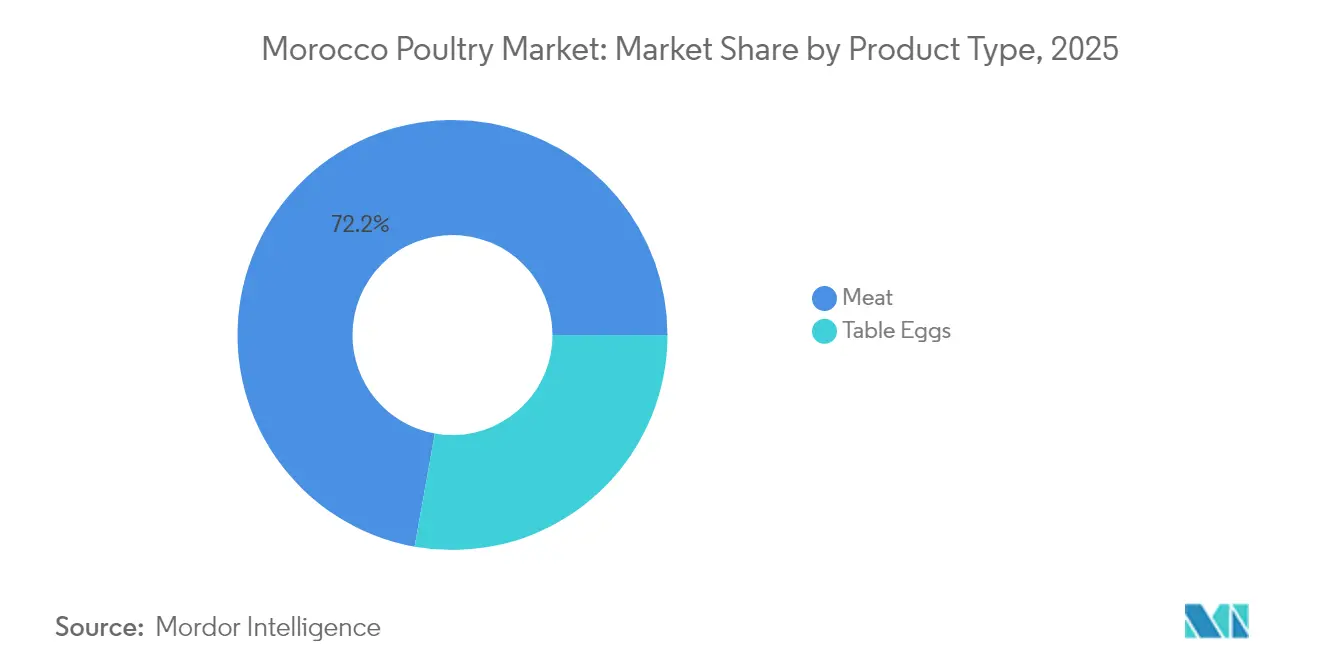

- By product type, meat accounted for 72.18% of the Morocco poultry market share in 2025; table eggs are projected to expand at a 7.15% CAGR through 2031.

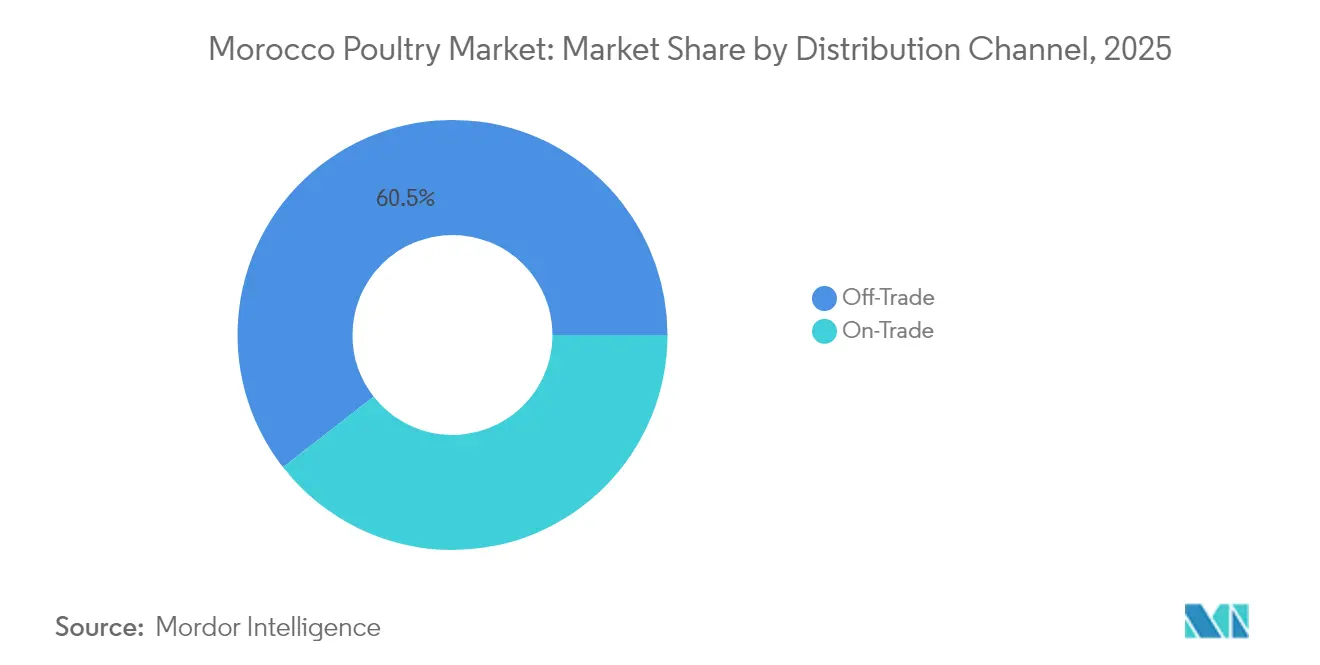

- By distribution channel, off-trade captured 60.55% of the Morocco poultry market share in 2025; off-trade revenue is forecast to rise at a 4.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Poultry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of QSR chains | +1.2% | National, concentrated in Casablanca, Rabat, Marrakech | Medium term (2-4 years) |

| Technological advancements in production | +0.8% | National, with early adoption in integrated facilities | Long term (≥ 4 years) |

| Demand for product quality and variety | +0.7% | National, stronger in urban centers | Medium term (2-4 years) |

| Supply chain modernization and efficiency | +0.6% | National, priority in northern regions | Long term (≥ 4 years) |

| Government-led modernization initiatives | +0.9% | National, with regional development focus | Long term (≥ 4 years) |

| Rising consumer awareness of food safety | +0.5% | National, accelerated in metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of QSR chains

The expansion of quick-service restaurant (QSR) chains in Morocco's urban areas is transforming poultry demand. Institutional buyers are increasingly opting for standardized, processed chicken products instead of traditional whole-bird purchases. Tourism significantly supports Morocco's QSR sector by driving higher demand and foot traffic in key tourist destinations. In 2024, Morocco recorded an impressive 17.4 million visitors, according to the Ministry of Tourism[1]Source: Ministry of Tourism, "Morocco Sets New Tourism Benchmarks in 2024", www.mtaess.gov.ma. Additionally, the government allocated nearly MAD 69 billion to infrastructure projects in the Tanger-Tétouan-Al Hoceima region in 2024. These projects are expected to create approximately 60,000 jobs, boosting disposable income and foodservice consumption. With 66% of Morocco's population living in urban areas in 2024, as reported by the World Bank[2]Source, World Bank, "Urban population (% of total population) - Morocco", www.data.worldbank.org, the demand shift is evident. This urbanization trend pushes poultry producers to enhance their processing capabilities and cold-chain infrastructure to meet institutional customer needs. Consequently, the market is experiencing consolidation, as smaller producers struggle to fulfill the volume and consistency requirements of QSR chains. International franchise operators are increasingly relying on integrated suppliers to ensure consistent product specifications across multiple locations.

Technological advancements in production

Moroccan poultry operations are undergoing a transformation, driven by digital initiatives. AI-powered monitoring systems and automated processing technologies are boosting productivity and minimizing reliance on labor. These advanced monitoring systems, equipped with sensors and cameras, can foresee disease outbreaks even before clinical symptoms manifest. This capability not only curtails mortality rates but also lessens the need for antibiotics. On a global scale, automated deboning solutions are becoming increasingly popular. These systems can handle up to 7,000 breasts per hour and simultaneously cut labor needs by 60%. Furthermore, the adoption of precision livestock farming technologies allows for real-time enhancements in feed conversion ratios and environmental controls. To stay competitive in export markets, Moroccan producers are encouraged to embrace innovations like Ceva's Genesys technology, which automates gender separation at hatch.

Government-led modernization initiatives

Morocco's Generation Green strategy is driving a comprehensive transformation of the agricultural sector, providing significant benefits to poultry producers through subsidized modernization initiatives and improved market access infrastructure. The World Bank has introduced a USD 250 million climate-smart investment program, set to be implemented by 2025, which aims to support 120,000 farmers, including poultry producers[3]Source: FAO Investment Centre, "Strengthening Morocco’s food safety and quality with climate-smart investment", www.fao.org. This program focuses on enhancing food safety standards and implementing measures to improve climate resilience within the agricultural sector. Demonstrating its commitment to value-chain development, the OCP Innovation Fund for Agriculture has established a poultry slaughtering abattoir in Beni Mellal, showcasing the importance of public-private partnerships in advancing the industry. These efforts include offering preferential financing terms to facilitate facility upgrades and the adoption of advanced technologies. Furthermore, the government's strong emphasis on halal certification and compliance with international quality standards positions Moroccan poultry producers to capitalize on expanded export opportunities in global markets.

Supply chain modernization and efficiency

As producers focus on export markets and aim to extend product shelf life for domestic distribution, cold-chain infrastructure development and logistics optimization play a crucial role in driving market growth. Improved cold storage and transportation facilities enhance the preservation of poultry products, reducing spoilage and increasing shelf life. This improvement boosts product availability and quality in both urban and rural markets, strengthening consumer confidence and driving demand. Modern supply chains now adhere to stricter hygiene and safety standards, including certified slaughterhouses and processing plants, which are gradually replacing informal markets with inconsistent quality. Consumers increasingly prefer these safer, certified products, contributing to the overall market value. Additionally, AI and machine learning applications in cold-chain capacity planning are revolutionizing the management of temperature-sensitive products. Integrated producers, such as Zalar Holding, have significantly invested in grain storage and processing facilities with support from the European Investment Bank, enhancing their supply chain resilience. Moreover, modern logistics networks are reducing product loss rates and enabling producers to efficiently serve geographically dispersed markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent hygiene and regulatory compliance | -0.8% | National, stricter enforcement in export facilities | Short term (≤ 2 years) |

| Fragmented cold-chain logistics | -0.6% | National, acute in rural and southern regions | Medium term (2-4 years) |

| Limited investment capital for modernization | -0.7% | National, affecting small and medium producers | Long term (≥ 4 years) |

| Dependency on feed quality and availability | -1.1% | National, severe impact during drought years | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent hygiene and regulatory compliance

Stricter food safety standards and regulatory enforcement are driving up compliance costs, disproportionately affecting smaller producers and potentially restricting market access for non-compliant facilities. In Morocco, most poultry sales take place in “ryachats”, live bird markets, and informal slaughterhouses that largely operate outside regulated hygiene frameworks. Government efforts to enforce hygiene regulations face challenges due to strong cultural preferences and consumer trust in traditional buying and slaughtering practices, which hinder the formal sector's growth. A turkey meat analysis in Kenitra revealed a 35% non-compliance rate for Total Aerobic Mesophilic Flora, along with high levels of total coliforms and fecal coliforms at 68% and 75%, respectively. Meeting regulatory requirements necessitates significant investments in HACCP systems, laboratory testing, and facility upgrades, creating financial burdens for smaller operators. Additionally, international export standards demand further certifications and traceability systems, adding to operational complexity. Regulatory controls on imports, feed additives, veterinary drugs, and food safety can also result in delays and logistical inefficiencies, disrupting supply stability and cost management.

Dependency on feed quality and availability

Morocco's poultry production is under significant pressure due to climatic variations and the volatility of feed costs. The country is currently enduring its most severe drought in three decades, which has led to a sharp decline in wheat production. In response to these adverse conditions, farmers are transitioning from wheat cultivation to barley, a crop better suited to withstand drought. This shift is fundamentally altering the availability and composition of feed ingredients for the poultry sector. According to the U.S. Department of Agriculture, Morocco is projected to import 7.3 million metric tons of wheat and 0.9 million metric tons of barley during the 2025/26 period[4]Source: United States Department of Agriculture, "Morocco: Grain and Feed Annual", www.usda.gov. These substantial import requirements leave producers highly exposed to fluctuations in international prices and potential disruptions in supply chains. Feed costs, which typically account for 60-70% of total production expenses, are particularly sensitive to such price changes, significantly affecting profitability margins. Moreover, the sector's heavy reliance on imported feed ingredients heightens its susceptibility to risks associated with currency exchange rate fluctuations and geopolitical disruptions in supply chains, further compounding the challenges faced by poultry producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat Dominance Drives Market Evolution

In 2025, chicken's affordability, versatility, and cultural acceptance have established it as Morocco's primary protein source, securing the meat segment a dominant 72.18% market share. Fresh chilled meat products remain the top choice among consumers, while urban residents and foodservice operators are increasingly opting for processed options such as nuggets, sausages, and marinated tenders. Frozen and canned meats address niche markets, catering to institutional buyers and export clients who require extended shelf life.

Table eggs, growing at a strong 7.15% CAGR through 2031, are gaining traction due to rising health awareness and dietary diversification among Moroccan consumers. With lower capital requirements compared to meat production, smaller producers are entering the market and leveraging local distribution networks. Awareness campaigns emphasizing eggs' nutritional benefits and affordability are driving consumption beyond traditional breakfast use. This growth aligns with Morocco's demographic changes and urbanization trends, as younger consumers increasingly incorporate eggs into various meals throughout the day.

By Distribution Channel: Off-Trade Supremacy Reflects Retail Evolution

The off-trade channel's dominant 60.55% market share in 2025 and sustained 4.72% CAGR growth through 2031. This highlights the crucial role of retail infrastructure in driving market growth. Supermarkets and hypermarkets, supported by cold-chain investments, dominate this segment. Consumers are increasingly drawn to branded, packaged products that feature clear expiration dates and quality certifications. Leading retailers such as LabelVie Group's Carrefour Morocco and Marjane Holding are adopting vertical integration strategies to manage quality and margins while offering competitive pricing. Convenience stores in urban areas are expanding quickly, driven by shifting lifestyles and growing demand for ready-to-cook products among working professionals.

Although online retail channels in Morocco are still emerging, they show strong growth potential, particularly after COVID-19 accelerated e-commerce adoption across the country. However, the segment faces hurdles, including last-mile cold-chain delivery issues and the need to build consumer trust in purchasing fresh food online. Traditional wet markets and independent retailers continue to serve rural areas and price-sensitive consumers, but their market share is gradually decreasing as modern retail formats expand into secondary cities. BIM Stores' private-label frozen chicken strategy illustrates how discount retailers are gaining market share through value-driven positioning and strategic sourcing partnerships.

Geography Analysis

Morocco's strategic geographic location strengthens its domestic market as the primary center of consumption while also creating significant export opportunities in North Africa and Sub-Saharan regions. The northern regions, particularly the Tanger-Tétouan-Al Hoceima area, leverage their proximity to European markets, supported by advanced port infrastructure that facilitates efficient trade. In Casablanca and Rabat, demand for premium poultry products is increasing, driven by consumers willing to pay more for organic, free-range, and branded options. These trends highlight a shift in consumer preferences toward higher-quality and ethically sourced products. Additionally, the Atlantic coastal regions benefit from a robust cold-chain infrastructure and processing facilities, effectively serving both domestic and export markets while ensuring product quality and supply chain efficiency.

In the southern regions, water scarcity poses a significant challenge to production expansion. However, the completion of the Dakhla desalination project is expected to address this issue by providing an additional 37 million cubic meters of water annually, supporting agricultural and industrial activities. Rural areas continue to exhibit traditional consumption patterns, favoring whole birds and locally-sourced products. However, urbanization is gradually shifting these preferences, leading to increased demand for processed and convenience poultry products in urban centers. The eastern border regions, despite occasional disruptions in cross-border commerce due to political tensions, benefit from trade relationships with Algeria, contributing to the region's economic activity.

Export markets offer substantial growth potential for Morocco, with the country's halal certification and strategic location near European and African markets providing a competitive edge. Morocco's recent decision to lift restrictions on Brazilian poultry imports, following the resolution of the H5N1 outbreak, reflects its proactive and adaptive regulatory approach to international trade opportunities. Furthermore, regional integration initiatives under the African Continental Free Trade Area are expected to enhance market access for Moroccan producers, enabling them to expand their reach and capitalize on emerging opportunities across the broader African market.

Competitive Landscape

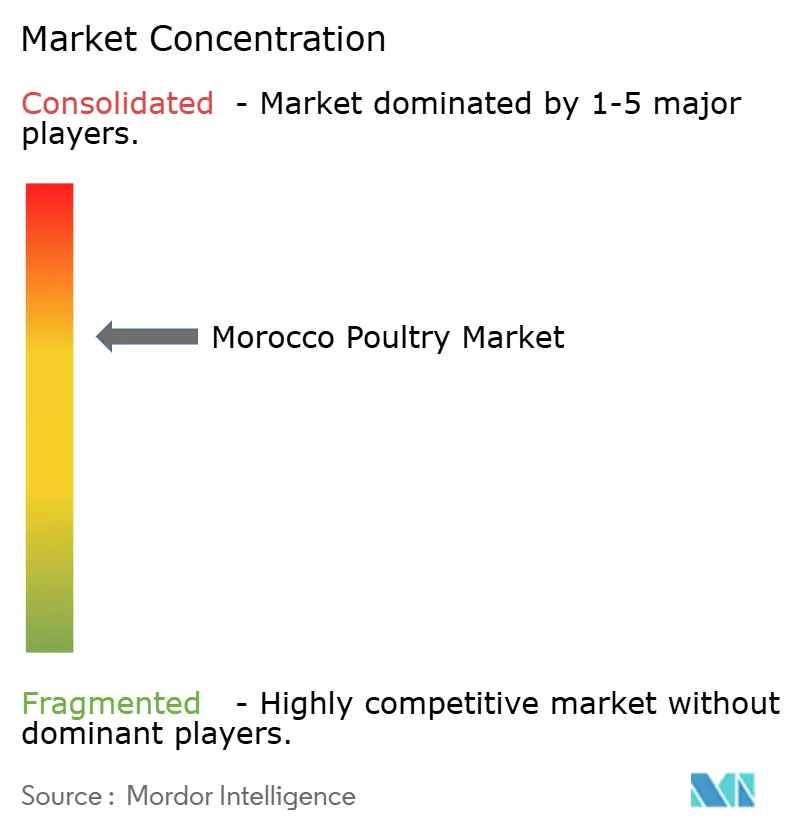

The Morocco Poultry Market is moderately consolidated, with several integrated players competing across production, processing, and distribution segments. However, market concentration is increasing as larger operators capitalize on economies of scale and vertical integration strategies to maximize value across the supply chain. Zalar Holding has established itself as the leading integrated producer, engaging in grain trading, animal feed, hatchery operations, broiler farming, and meat processing.

Key players in the market include Zalar Holding, Koutoubia Holding, ALF Sahel, Dar El Fellous, and Matinales, among others. These companies are implementing strategies such as product innovations, partnerships, strengthening their online and offline marketing efforts, and mergers and acquisitions. These initiatives aim to enhance their market presence and expand their product portfolios, thereby driving market growth. Product innovation remains a primary focus for many players, as they develop new poultry products to meet changing consumer preferences.

Strategic partnerships with international companies are becoming more prevalent. For example, Zalar has partnered with Mitsui to produce Japanese-style fried chicken products for export markets. Technology adoption is emerging as a critical competitive advantage, as seen with GST AVICOLE's batch monitoring systems, which enable smaller producers to achieve professional production standards. Retail integration strategies are also evident, with LabelVie Group's Carrefour Morocco operations and Marjane Holding introducing private-label poultry products to better control margins and maintain quality standards. The competitive landscape is shaped by ONSSA regulatory requirements, which tend to favor larger, well-funded operators capable of investing in compliance infrastructure and quality management systems.

Morocco Poultry Industry Leaders

-

Zalar Holding

-

Koutoubia Holding

-

ALF Sahel

-

Dar El Fellous

-

Matinales

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Zalar Holding acquired a 33% stake in Graderco from the Hamdouch family. Zalar Group has achieved its position as the sole operator with vertical integration across the entire poultry meat value chain through a combination of organic growth and strategic mergers and acquisitions.

- May 2023: The Moroccan government and the Interprofessional Federation of the Poultry Sector (FISA) have signed a new program contract for the poultry industry, which will remain in effect until 2030. This program involves an investment of USD 198 million to achieve key objectives, including increasing poultry meat production to 92,000 tonnes and egg production to 7.6 billion units.

Morocco Poultry Market Report Scope

Poultry refers to domesticated birds kept for meat, eggs, and feathers.

The Moroccan poultry market is segmented by product type and distribution channel. By product type, the market is segmented into table eggs, broiler meat, and processed meat. The processed meat segment is further sub-segmented into nuggets and popcorn, sausages, burgers, marinated poultry products, and other processed meat products. By distribution channel, the market is segmented into hotels, restaurants, catering, modern trade, and other distribution channels. For each segment, the market sizing and forecasts are offered based on value (USD).

| Table Eggs | |||

| Meat | Product Form | Canned | |

| Fresh Chilled | |||

| Frozen | |||

| Processed | Deli Meats | ||

| Marinated/ Tenders | |||

| Meatbolls | |||

| Nuggets | |||

| Sausages | |||

| Other Processed Meat | |||

| Off-Trade | Supermarket/ Hypermarket |

| Convenience Store | |

| Online Store | |

| Other Off-Trade Channels | |

| On-Trade | Hotel |

| Restaurants | |

| Cafes |

| Product Type | Table Eggs | |||

| Meat | Product Form | Canned | ||

| Fresh Chilled | ||||

| Frozen | ||||

| Processed | Deli Meats | |||

| Marinated/ Tenders | ||||

| Meatbolls | ||||

| Nuggets | ||||

| Sausages | ||||

| Other Processed Meat | ||||

| Distribution Channel | Off-Trade | Supermarket/ Hypermarket | ||

| Convenience Store | ||||

| Online Store | ||||

| Other Off-Trade Channels | ||||

| On-Trade | Hotel | |||

| Restaurants | ||||

| Cafes | ||||

Key Questions Answered in the Report

What is the current value of the Morocco poultry market?

It is valued at USD 4.27 billion in 2026 and is projected to reach USD 5.39 billion by 2031.

How fast is table-egg demand growing in Morocco?

Table eggs are forecast to grow at 7.15% CAGR through 2031, outpacing other product categories.

Which sales channel leads poultry distribution in Morocco?

Off-trade retail—including supermarkets and hypermarkets—commands 60.55% of national poultry sales.

Why are feed costs a major concern for Moroccan poultry producers?

Drought-driven domestic grain shortfalls oblige imports of 7.3 million t of wheat and 0.9 million t of barley for 2025/26, exposing producers to global price swings.

Page last updated on: